Financial Accounting: Transactions, Statements, and Principles

VerifiedAdded on 2022/11/28

|26

|4432

|386

Homework Assignment

AI Summary

This financial accounting assignment provides a comprehensive overview of key concepts. It begins with an introduction to financial accounting and its importance, followed by an in-depth analysis of business transactions, single and double-entry systems, and the role of trial balances. The assignment includes detailed journal entries and ledger accounts, culminating in the preparation of a trial balance. It also explores the differences between financial statements and financial reporting, the various users of financial information, and the fundamental accounting principles, including accrual, conservatism, cost, going concern, full disclosure, materiality, and revenue recognition. The assignment then delves into the formulation of financial statements like the profit and loss account, balance sheet, and cash flow statements, with additional focus on bank reconciliation, control, and suspense accounts. The content is presented through detailed scenarios and practical examples to enhance understanding of accounting concepts.

FINANCIAL ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION.......................................................................................................................................3

SCENARIO 1..............................................................................................................................................3

Question 1...............................................................................................................................................3

Question 2...............................................................................................................................................4

Question 3.............................................................................................................................................11

Question 4.............................................................................................................................................13

Question 5.............................................................................................................................................14

Question 6.............................................................................................................................................15

Question 7.............................................................................................................................................17

SCENARIO- 2...........................................................................................................................................18

Question 1.............................................................................................................................................18

Question 2.............................................................................................................................................19

Question 3.............................................................................................................................................20

Question 4.............................................................................................................................................20

Question 5.............................................................................................................................................22

CONCLUSION.........................................................................................................................................24

REFERENCES..........................................................................................................................................26

INTRODUCTION.......................................................................................................................................3

SCENARIO 1..............................................................................................................................................3

Question 1...............................................................................................................................................3

Question 2...............................................................................................................................................4

Question 3.............................................................................................................................................11

Question 4.............................................................................................................................................13

Question 5.............................................................................................................................................14

Question 6.............................................................................................................................................15

Question 7.............................................................................................................................................17

SCENARIO- 2...........................................................................................................................................18

Question 1.............................................................................................................................................18

Question 2.............................................................................................................................................19

Question 3.............................................................................................................................................20

Question 4.............................................................................................................................................20

Question 5.............................................................................................................................................22

CONCLUSION.........................................................................................................................................24

REFERENCES..........................................................................................................................................26

INTRODUCTION

Financial accounting is significant procedure concerned with activities like summarizing,

recording and interpreting data in proper way. In present scenario, it has becomes crucial for

organization to develop financial accounting plans for accomplishing its business objective. The

present report will give emphasis explaining business transaction, single & double entry, trial

balance. Journal entries, ledgers to prepare trail balance will be included to give detail

information. Difference between financial statement & reporting along with users will be given.

Fundamentals accounting principles will be highlighted in current case study. It will focus on

formulation of profit & loss account, balance sheet, cash flow statements. Bank reconciliation,

control and suspense accounts along with necessity will be addressed in present report. The

current case study will help to get deep emphasis regarding accounting concepts with practical

examples

SCENARIO 1

Question 1

Business transaction is an activity in which two or more parties are involved for

accomplishing their company objectives such as selling goods, services, etc. There are

different types of transactions held in company which occurs in form of cash or credit for

the purpose like purchase of material, assets, selling goods, etc. It becomes essential for

organization to record each and every transaction in order to get accurate monetary

position (Waqas and Md-Rus, 2018). Other transactions are paying wages, interest,

deriving dividend, raising finance, debt, etc. The broad classification of transactions are

exerted as internal and external so that proper segregation for measuring in terms of

money can become possible. In order to get sustainability and stability in industry it

becomes important to derive significant recording, summarizing and interpreting business

transactions.

Single entry provides one way picture of organization through recording one aspect of

company’s activities. On the other side double entry book keeping system gives emphasis

Financial accounting is significant procedure concerned with activities like summarizing,

recording and interpreting data in proper way. In present scenario, it has becomes crucial for

organization to develop financial accounting plans for accomplishing its business objective. The

present report will give emphasis explaining business transaction, single & double entry, trial

balance. Journal entries, ledgers to prepare trail balance will be included to give detail

information. Difference between financial statement & reporting along with users will be given.

Fundamentals accounting principles will be highlighted in current case study. It will focus on

formulation of profit & loss account, balance sheet, cash flow statements. Bank reconciliation,

control and suspense accounts along with necessity will be addressed in present report. The

current case study will help to get deep emphasis regarding accounting concepts with practical

examples

SCENARIO 1

Question 1

Business transaction is an activity in which two or more parties are involved for

accomplishing their company objectives such as selling goods, services, etc. There are

different types of transactions held in company which occurs in form of cash or credit for

the purpose like purchase of material, assets, selling goods, etc. It becomes essential for

organization to record each and every transaction in order to get accurate monetary

position (Waqas and Md-Rus, 2018). Other transactions are paying wages, interest,

deriving dividend, raising finance, debt, etc. The broad classification of transactions are

exerted as internal and external so that proper segregation for measuring in terms of

money can become possible. In order to get sustainability and stability in industry it

becomes important to derive significant recording, summarizing and interpreting business

transactions.

Single entry provides one way picture of organization through recording one aspect of

company’s activities. On the other side double entry book keeping system gives emphasis

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

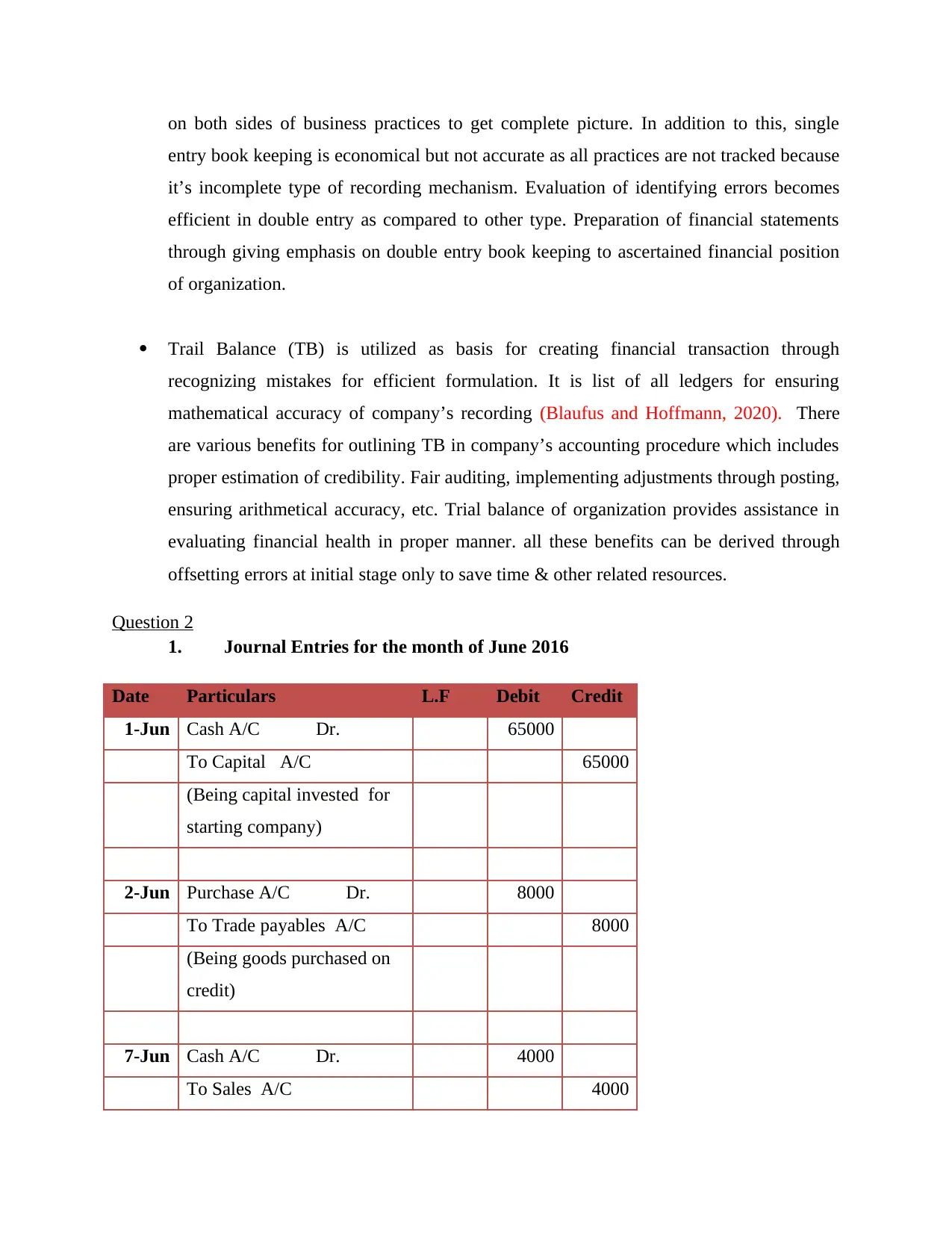

on both sides of business practices to get complete picture. In addition to this, single

entry book keeping is economical but not accurate as all practices are not tracked because

it’s incomplete type of recording mechanism. Evaluation of identifying errors becomes

efficient in double entry as compared to other type. Preparation of financial statements

through giving emphasis on double entry book keeping to ascertained financial position

of organization.

Trail Balance (TB) is utilized as basis for creating financial transaction through

recognizing mistakes for efficient formulation. It is list of all ledgers for ensuring

mathematical accuracy of company’s recording (Blaufus and Hoffmann, 2020). There

are various benefits for outlining TB in company’s accounting procedure which includes

proper estimation of credibility. Fair auditing, implementing adjustments through posting,

ensuring arithmetical accuracy, etc. Trial balance of organization provides assistance in

evaluating financial health in proper manner. all these benefits can be derived through

offsetting errors at initial stage only to save time & other related resources.

Question 2

1. Journal Entries for the month of June 2016

Date Particulars L.F Debit Credit

1-Jun Cash A/C Dr. 65000

To Capital A/C 65000

(Being capital invested for

starting company)

2-Jun Purchase A/C Dr. 8000

To Trade payables A/C 8000

(Being goods purchased on

credit)

7-Jun Cash A/C Dr. 4000

To Sales A/C 4000

entry book keeping is economical but not accurate as all practices are not tracked because

it’s incomplete type of recording mechanism. Evaluation of identifying errors becomes

efficient in double entry as compared to other type. Preparation of financial statements

through giving emphasis on double entry book keeping to ascertained financial position

of organization.

Trail Balance (TB) is utilized as basis for creating financial transaction through

recognizing mistakes for efficient formulation. It is list of all ledgers for ensuring

mathematical accuracy of company’s recording (Blaufus and Hoffmann, 2020). There

are various benefits for outlining TB in company’s accounting procedure which includes

proper estimation of credibility. Fair auditing, implementing adjustments through posting,

ensuring arithmetical accuracy, etc. Trial balance of organization provides assistance in

evaluating financial health in proper manner. all these benefits can be derived through

offsetting errors at initial stage only to save time & other related resources.

Question 2

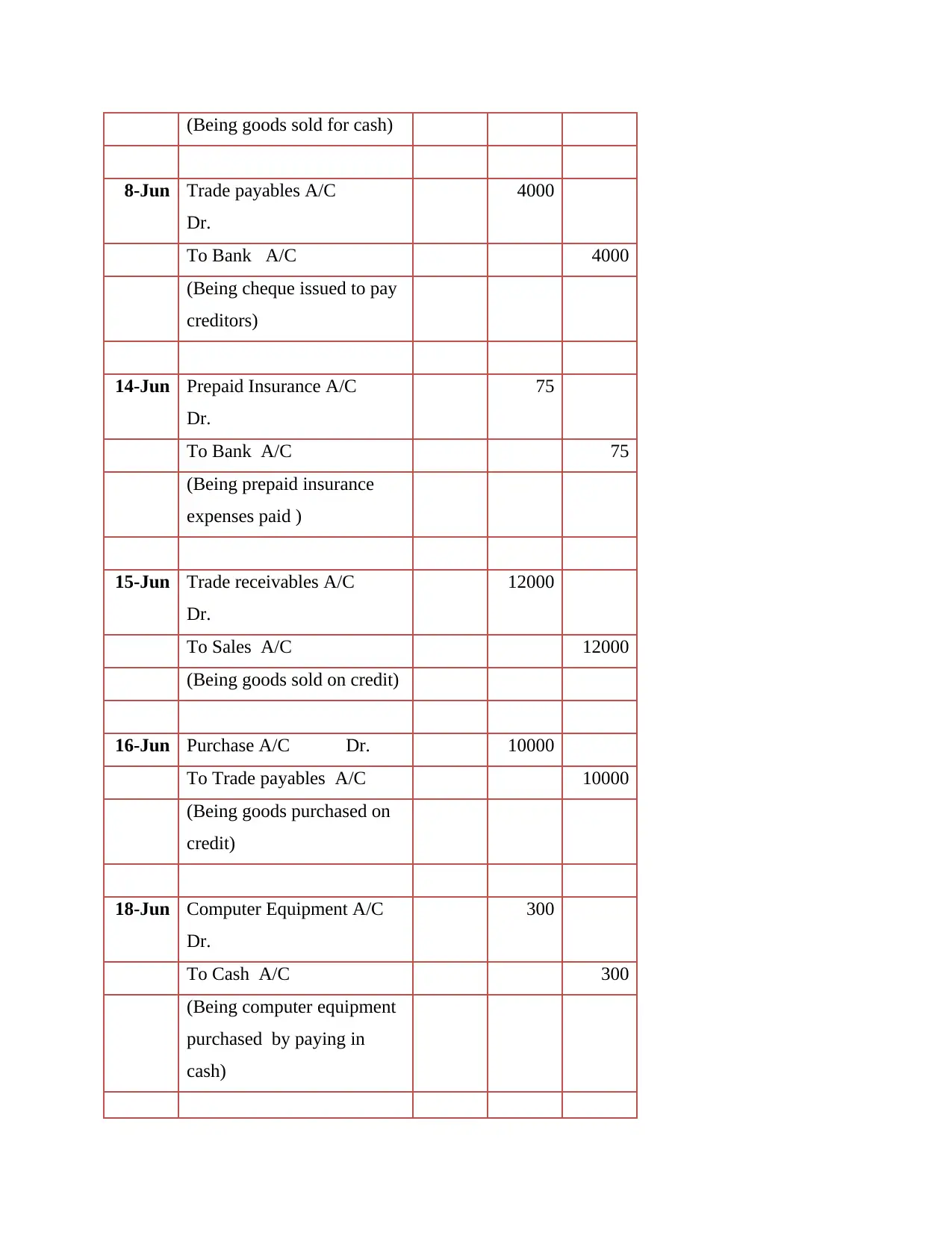

1. Journal Entries for the month of June 2016

Date Particulars L.F Debit Credit

1-Jun Cash A/C Dr. 65000

To Capital A/C 65000

(Being capital invested for

starting company)

2-Jun Purchase A/C Dr. 8000

To Trade payables A/C 8000

(Being goods purchased on

credit)

7-Jun Cash A/C Dr. 4000

To Sales A/C 4000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(Being goods sold for cash)

8-Jun Trade payables A/C

Dr.

4000

To Bank A/C 4000

(Being cheque issued to pay

creditors)

14-Jun Prepaid Insurance A/C

Dr.

75

To Bank A/C 75

(Being prepaid insurance

expenses paid )

15-Jun Trade receivables A/C

Dr.

12000

To Sales A/C 12000

(Being goods sold on credit)

16-Jun Purchase A/C Dr. 10000

To Trade payables A/C 10000

(Being goods purchased on

credit)

18-Jun Computer Equipment A/C

Dr.

300

To Cash A/C 300

(Being computer equipment

purchased by paying in

cash)

8-Jun Trade payables A/C

Dr.

4000

To Bank A/C 4000

(Being cheque issued to pay

creditors)

14-Jun Prepaid Insurance A/C

Dr.

75

To Bank A/C 75

(Being prepaid insurance

expenses paid )

15-Jun Trade receivables A/C

Dr.

12000

To Sales A/C 12000

(Being goods sold on credit)

16-Jun Purchase A/C Dr. 10000

To Trade payables A/C 10000

(Being goods purchased on

credit)

18-Jun Computer Equipment A/C

Dr.

300

To Cash A/C 300

(Being computer equipment

purchased by paying in

cash)

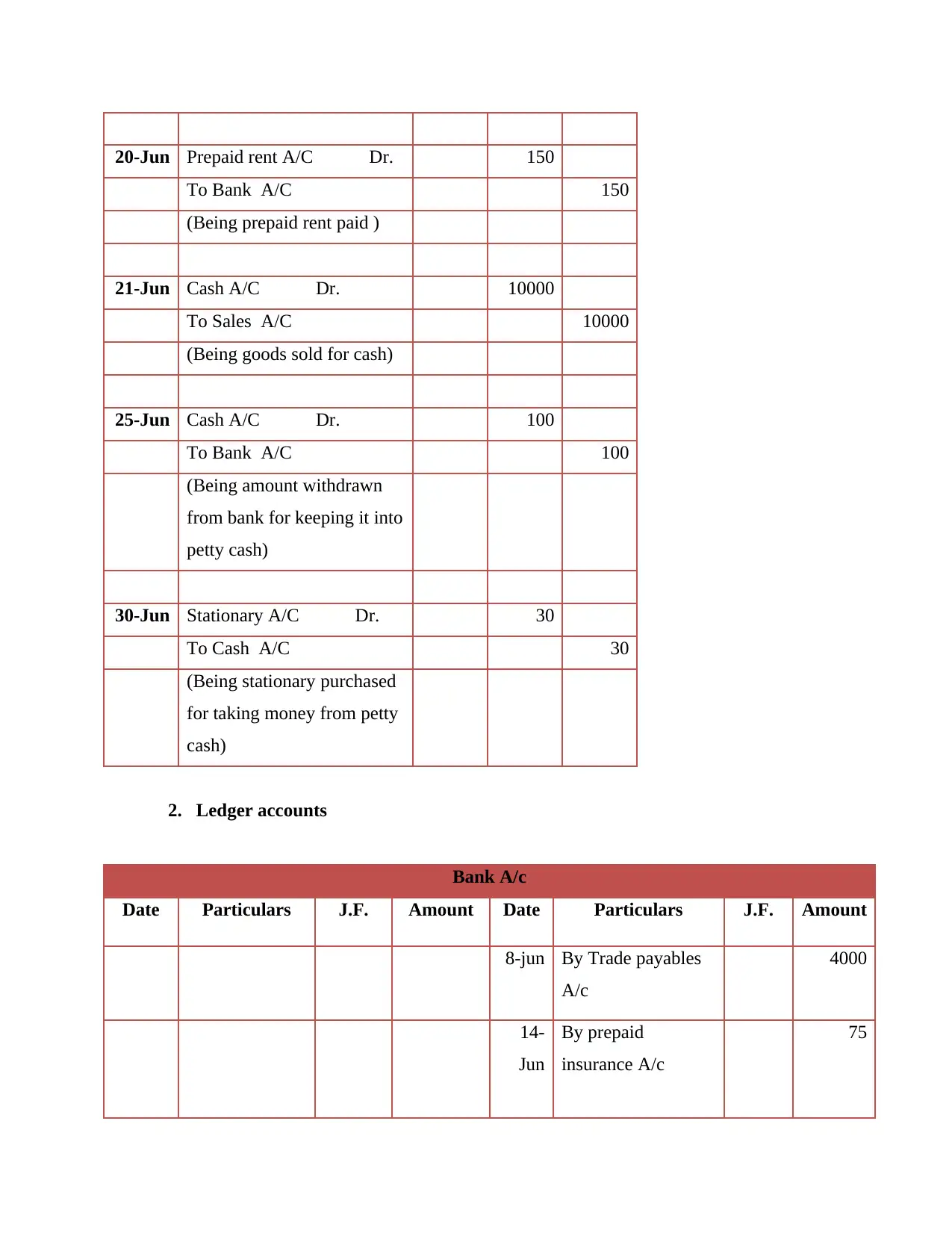

20-Jun Prepaid rent A/C Dr. 150

To Bank A/C 150

(Being prepaid rent paid )

21-Jun Cash A/C Dr. 10000

To Sales A/C 10000

(Being goods sold for cash)

25-Jun Cash A/C Dr. 100

To Bank A/C 100

(Being amount withdrawn

from bank for keeping it into

petty cash)

30-Jun Stationary A/C Dr. 30

To Cash A/C 30

(Being stationary purchased

for taking money from petty

cash)

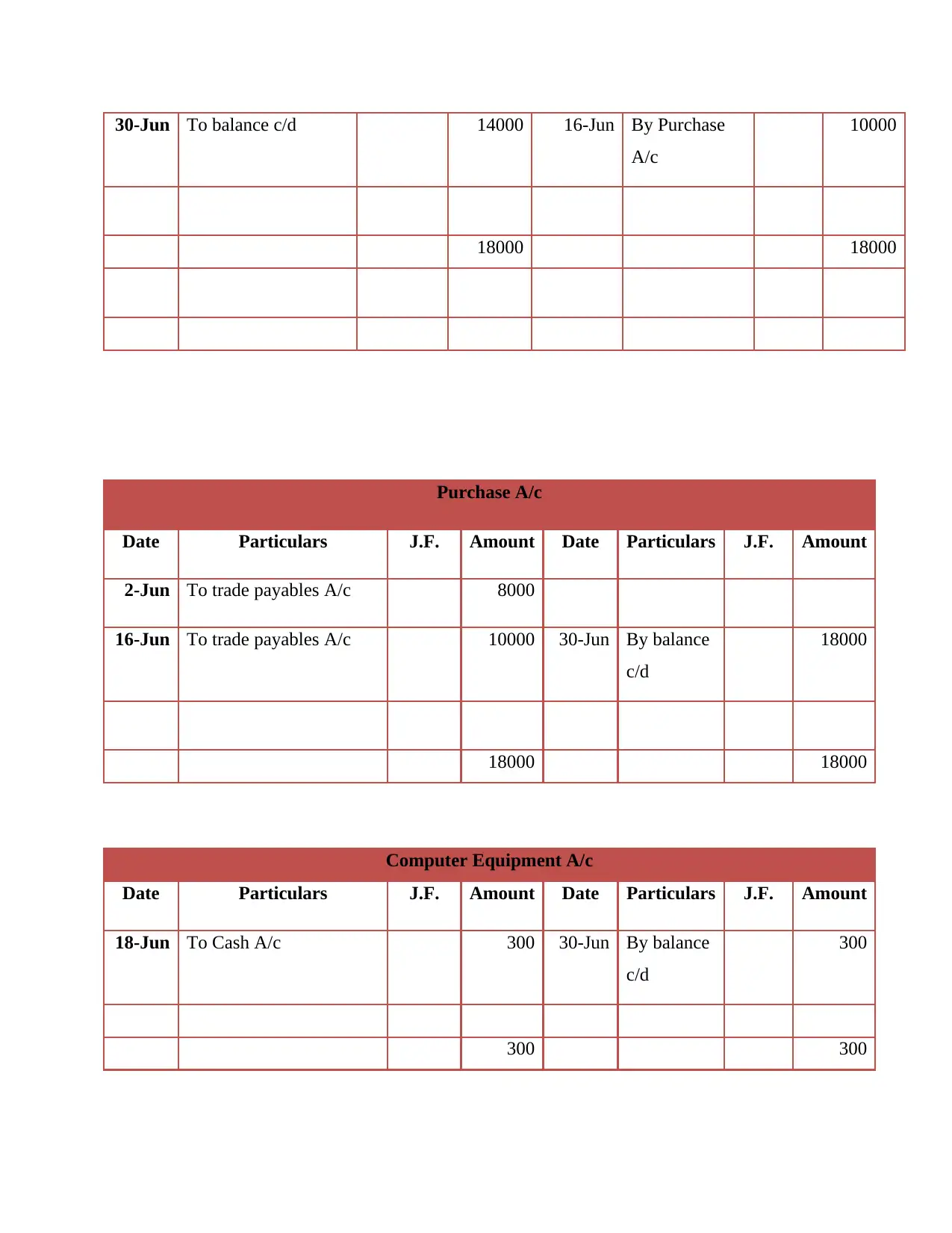

2. Ledger accounts

Bank A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

8-jun By Trade payables

A/c

4000

14-

Jun

By prepaid

insurance A/c

75

To Bank A/C 150

(Being prepaid rent paid )

21-Jun Cash A/C Dr. 10000

To Sales A/C 10000

(Being goods sold for cash)

25-Jun Cash A/C Dr. 100

To Bank A/C 100

(Being amount withdrawn

from bank for keeping it into

petty cash)

30-Jun Stationary A/C Dr. 30

To Cash A/C 30

(Being stationary purchased

for taking money from petty

cash)

2. Ledger accounts

Bank A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

8-jun By Trade payables

A/c

4000

14-

Jun

By prepaid

insurance A/c

75

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

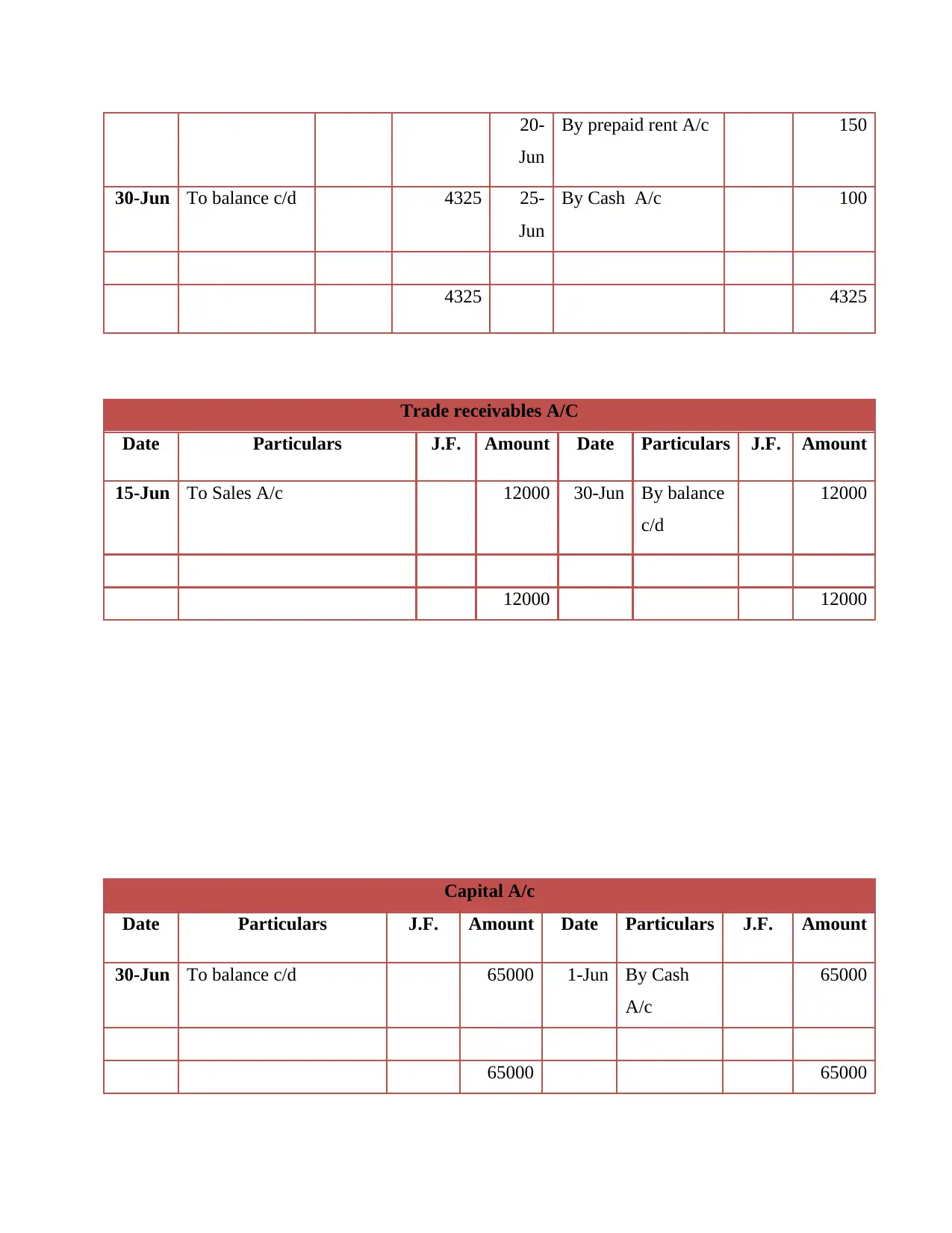

20-

Jun

By prepaid rent A/c 150

30-Jun To balance c/d 4325 25-

Jun

By Cash A/c 100

4325 4325

Trade receivables A/C

Date Particulars J.F. Amount Date Particulars J.F. Amount

15-Jun To Sales A/c 12000 30-Jun By balance

c/d

12000

12000 12000

Capital A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

30-Jun To balance c/d 65000 1-Jun By Cash

A/c

65000

65000 65000

Jun

By prepaid rent A/c 150

30-Jun To balance c/d 4325 25-

Jun

By Cash A/c 100

4325 4325

Trade receivables A/C

Date Particulars J.F. Amount Date Particulars J.F. Amount

15-Jun To Sales A/c 12000 30-Jun By balance

c/d

12000

12000 12000

Capital A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

30-Jun To balance c/d 65000 1-Jun By Cash

A/c

65000

65000 65000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

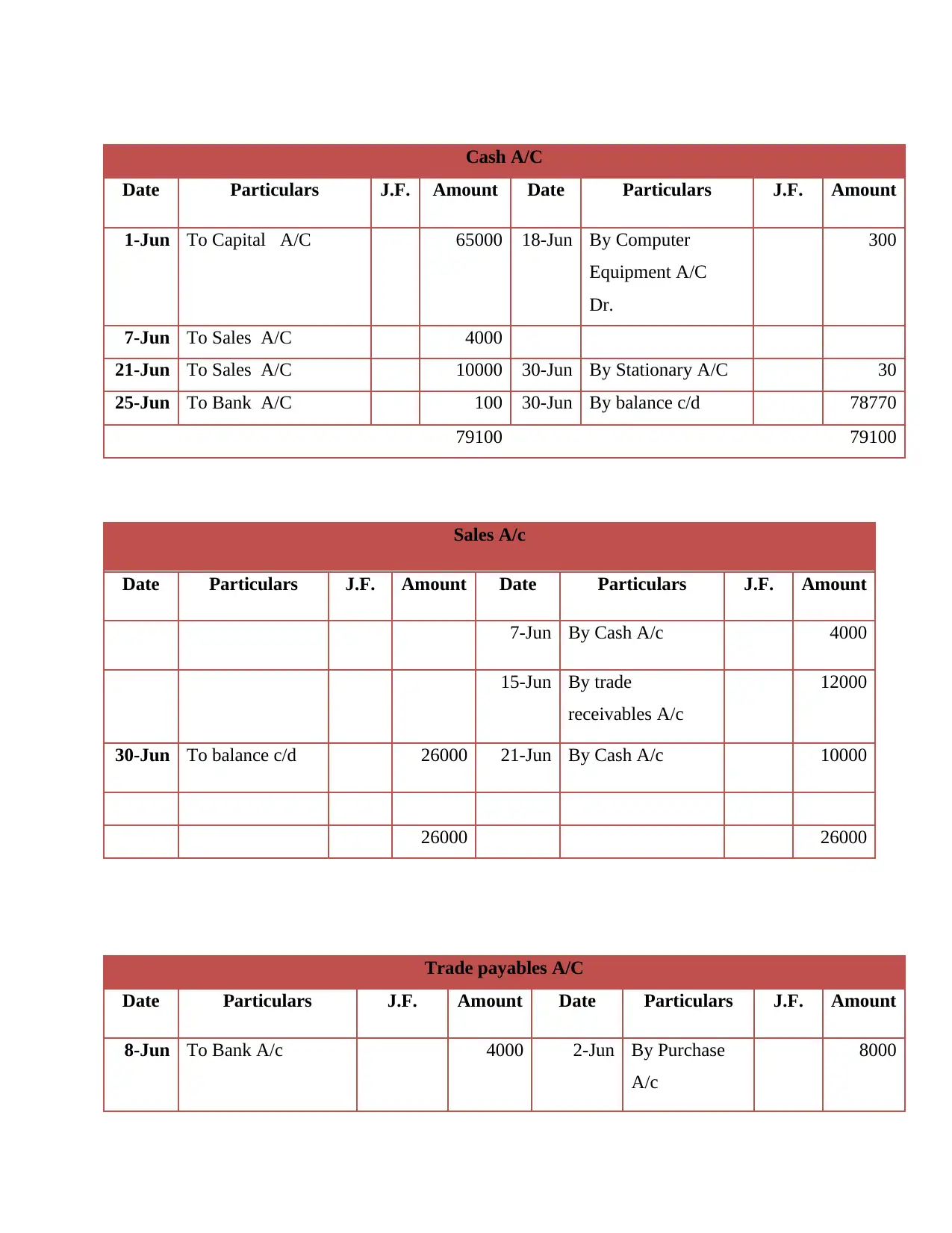

Cash A/C

Date Particulars J.F. Amount Date Particulars J.F. Amount

1-Jun To Capital A/C 65000 18-Jun By Computer

Equipment A/C

Dr.

300

7-Jun To Sales A/C 4000

21-Jun To Sales A/C 10000 30-Jun By Stationary A/C 30

25-Jun To Bank A/C 100 30-Jun By balance c/d 78770

79100 79100

Sales A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

7-Jun By Cash A/c 4000

15-Jun By trade

receivables A/c

12000

30-Jun To balance c/d 26000 21-Jun By Cash A/c 10000

26000 26000

Trade payables A/C

Date Particulars J.F. Amount Date Particulars J.F. Amount

8-Jun To Bank A/c 4000 2-Jun By Purchase

A/c

8000

Date Particulars J.F. Amount Date Particulars J.F. Amount

1-Jun To Capital A/C 65000 18-Jun By Computer

Equipment A/C

Dr.

300

7-Jun To Sales A/C 4000

21-Jun To Sales A/C 10000 30-Jun By Stationary A/C 30

25-Jun To Bank A/C 100 30-Jun By balance c/d 78770

79100 79100

Sales A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

7-Jun By Cash A/c 4000

15-Jun By trade

receivables A/c

12000

30-Jun To balance c/d 26000 21-Jun By Cash A/c 10000

26000 26000

Trade payables A/C

Date Particulars J.F. Amount Date Particulars J.F. Amount

8-Jun To Bank A/c 4000 2-Jun By Purchase

A/c

8000

30-Jun To balance c/d 14000 16-Jun By Purchase

A/c

10000

18000 18000

Purchase A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

2-Jun To trade payables A/c 8000

16-Jun To trade payables A/c 10000 30-Jun By balance

c/d

18000

18000 18000

Computer Equipment A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

18-Jun To Cash A/c 300 30-Jun By balance

c/d

300

300 300

A/c

10000

18000 18000

Purchase A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

2-Jun To trade payables A/c 8000

16-Jun To trade payables A/c 10000 30-Jun By balance

c/d

18000

18000 18000

Computer Equipment A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

18-Jun To Cash A/c 300 30-Jun By balance

c/d

300

300 300

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Prepaid Rent A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

20-Jun To Bank A/c 150 30-Jun By balance

c/d

150

150 150

Stationary A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

30-Jun To Cash A/c 30 30-Jun By balance

c/d

30

30 30

Prepaid insurance A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

14-Jun To Bank A/c 75 30-Jun By balance

c/d

75

75 75

3 Trial Balance:

Particulars Debit Credit

Date Particulars J.F. Amount Date Particulars J.F. Amount

20-Jun To Bank A/c 150 30-Jun By balance

c/d

150

150 150

Stationary A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

30-Jun To Cash A/c 30 30-Jun By balance

c/d

30

30 30

Prepaid insurance A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

14-Jun To Bank A/c 75 30-Jun By balance

c/d

75

75 75

3 Trial Balance:

Particulars Debit Credit

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

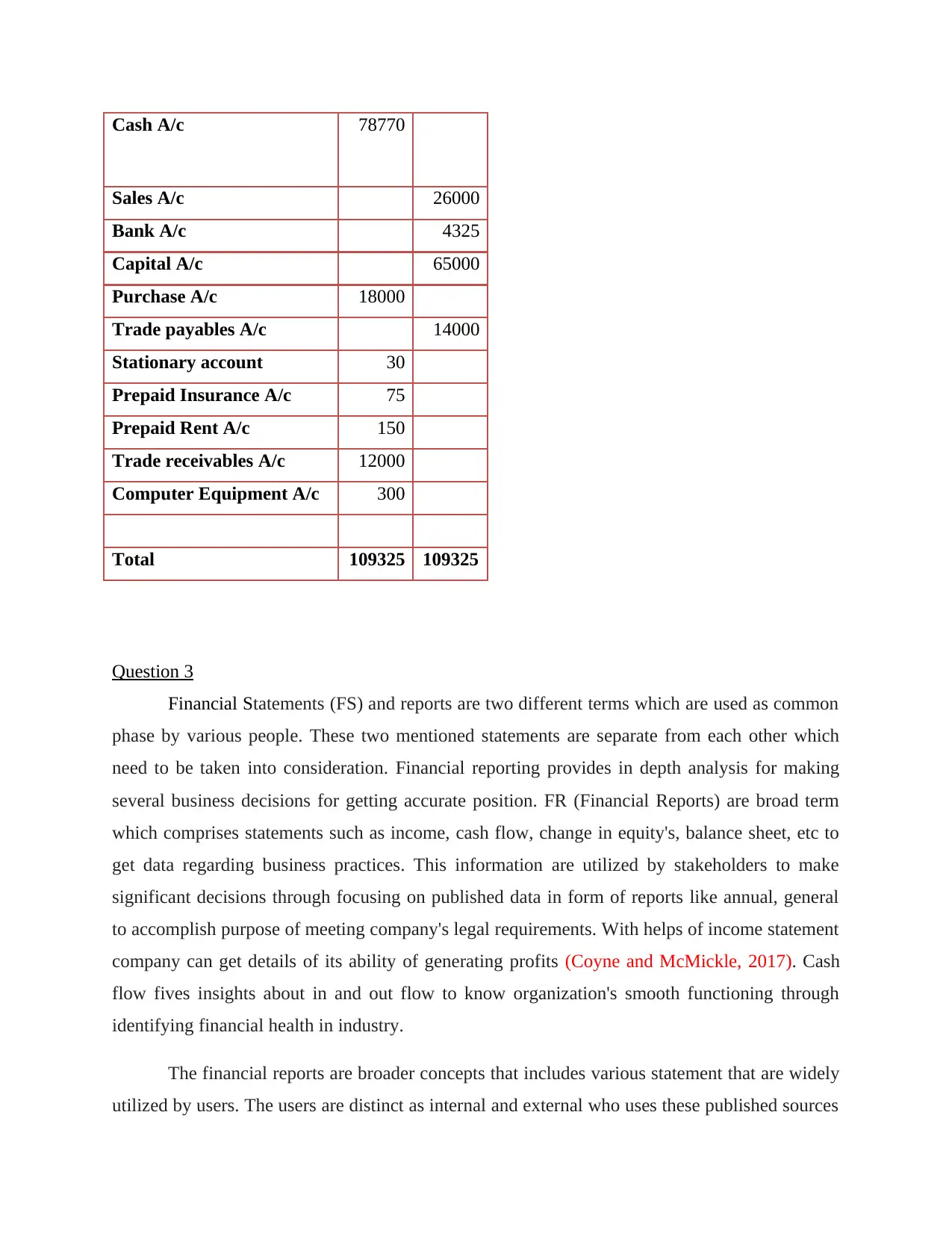

Cash A/c 78770

Sales A/c 26000

Bank A/c 4325

Capital A/c 65000

Purchase A/c 18000

Trade payables A/c 14000

Stationary account 30

Prepaid Insurance A/c 75

Prepaid Rent A/c 150

Trade receivables A/c 12000

Computer Equipment A/c 300

Total 109325 109325

Question 3

Financial Statements (FS) and reports are two different terms which are used as common

phase by various people. These two mentioned statements are separate from each other which

need to be taken into consideration. Financial reporting provides in depth analysis for making

several business decisions for getting accurate position. FR (Financial Reports) are broad term

which comprises statements such as income, cash flow, change in equity's, balance sheet, etc to

get data regarding business practices. This information are utilized by stakeholders to make

significant decisions through focusing on published data in form of reports like annual, general

to accomplish purpose of meeting company's legal requirements. With helps of income statement

company can get details of its ability of generating profits (Coyne and McMickle, 2017). Cash

flow fives insights about in and out flow to know organization's smooth functioning through

identifying financial health in industry.

The financial reports are broader concepts that includes various statement that are widely

utilized by users. The users are distinct as internal and external who uses these published sources

Sales A/c 26000

Bank A/c 4325

Capital A/c 65000

Purchase A/c 18000

Trade payables A/c 14000

Stationary account 30

Prepaid Insurance A/c 75

Prepaid Rent A/c 150

Trade receivables A/c 12000

Computer Equipment A/c 300

Total 109325 109325

Question 3

Financial Statements (FS) and reports are two different terms which are used as common

phase by various people. These two mentioned statements are separate from each other which

need to be taken into consideration. Financial reporting provides in depth analysis for making

several business decisions for getting accurate position. FR (Financial Reports) are broad term

which comprises statements such as income, cash flow, change in equity's, balance sheet, etc to

get data regarding business practices. This information are utilized by stakeholders to make

significant decisions through focusing on published data in form of reports like annual, general

to accomplish purpose of meeting company's legal requirements. With helps of income statement

company can get details of its ability of generating profits (Coyne and McMickle, 2017). Cash

flow fives insights about in and out flow to know organization's smooth functioning through

identifying financial health in industry.

The financial reports are broader concepts that includes various statement that are widely

utilized by users. The users are distinct as internal and external who uses these published sources

for accomplishing their particular purpose (What is Financial accounting? 2021). Company

shared information to complete its obligations towards society, government, etc. Reason behind

giving emphasis on mentioned part is to obtain knowledge regarding company's liquidity,

efficiency, profitability, etc. Investors utilize financial information to met its objective of

identifying firm's revenue generating capacity so that higher return on it can be obtained.

Investment analyst show interest in analyzing presented statement to give guidance to clients

regarding corrective path for moving towards desirable position. In addition to this, financial

institutions, bank, creditors, etc make evaluation of these shared data to recognize firm's

credibility and trustworthiness in order to know its paying capacity. These assist in having

information relating to organization solvency position through analyzing current and fixed assets

in turn efficiency to meet legal as well other obligations can be known.

There are various other stakeholders who show interest in company's practices to reach

particular conclusion. Internal users such as owner, management and employees go through

specified financial statements to know lacking areas. Company's progress through performance

evaluation on the basis of operational efficiency via determining operating, net and gross profits.

In addition to this, the purpose behind formulation s to make comparison between previous and

current performance so that position in sector can be assessed. With helps of data entity can

evaluate its accuracy of price strategies, business structure, policies, marketing and promotional

actions contribution in success (Köchling and Posch, 2018). Competitors as well look into other

organization's practices to assess success determinate so that appropriate course of action can be

taken. Government ensures relevancy, reliable, timelines, comparison, etc such qualitative

characteristics are followed by business to give stakeholders assistance in fulfilling objective. It

is also given emphasis by government on firm's activities regarding taxation for checking its

fairness.

Question 4

Accounting principles are regulations and rules that are served as guidelines for

formulating financial statements. It is utilized as accounting standards for recording, analysis and

controlling financial information. These principles are universally applicable which gives

assistance in meeting various obligation in systematic patter.

Accrual principle

shared information to complete its obligations towards society, government, etc. Reason behind

giving emphasis on mentioned part is to obtain knowledge regarding company's liquidity,

efficiency, profitability, etc. Investors utilize financial information to met its objective of

identifying firm's revenue generating capacity so that higher return on it can be obtained.

Investment analyst show interest in analyzing presented statement to give guidance to clients

regarding corrective path for moving towards desirable position. In addition to this, financial

institutions, bank, creditors, etc make evaluation of these shared data to recognize firm's

credibility and trustworthiness in order to know its paying capacity. These assist in having

information relating to organization solvency position through analyzing current and fixed assets

in turn efficiency to meet legal as well other obligations can be known.

There are various other stakeholders who show interest in company's practices to reach

particular conclusion. Internal users such as owner, management and employees go through

specified financial statements to know lacking areas. Company's progress through performance

evaluation on the basis of operational efficiency via determining operating, net and gross profits.

In addition to this, the purpose behind formulation s to make comparison between previous and

current performance so that position in sector can be assessed. With helps of data entity can

evaluate its accuracy of price strategies, business structure, policies, marketing and promotional

actions contribution in success (Köchling and Posch, 2018). Competitors as well look into other

organization's practices to assess success determinate so that appropriate course of action can be

taken. Government ensures relevancy, reliable, timelines, comparison, etc such qualitative

characteristics are followed by business to give stakeholders assistance in fulfilling objective. It

is also given emphasis by government on firm's activities regarding taxation for checking its

fairness.

Question 4

Accounting principles are regulations and rules that are served as guidelines for

formulating financial statements. It is utilized as accounting standards for recording, analysis and

controlling financial information. These principles are universally applicable which gives

assistance in meeting various obligation in systematic patter.

Accrual principle

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.