Financial Accounting Assignment Solution with Analysis

VerifiedAdded on 2023/01/10

|16

|3183

|74

Homework Assignment

AI Summary

This assignment solution addresses a financial accounting problem, beginning with the preparation of a trading account, profit and loss account, and balance sheet for a fabric shop proprietor. It then critically evaluates the features of financial information, emphasizing its importance to users and stakeholders. The solution includes a detailed ratio analysis, calculating and interpreting various ratios such as gross profit margin, return on capital employed, current ratio, trade payable days, and debtor collection period. Furthermore, the assignment demonstrates the creation of journal entries, ledger accounts, and a trial balance to record financial transactions. Finally, the solution explains the significance of different accounting concepts, such as the straight-line method for depreciation, providing a comprehensive overview of the financial accounting principles involved.

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................3

Question 1a).....................................................................................................................................3

Question 1b).....................................................................................................................................4

Critically evaluating the features of financial information that is beneficial and important for

users.............................................................................................................................................4

Question 2a).....................................................................................................................................5

Question 2b).....................................................................................................................................7

2...................................................................................................................................................9

Question 2c)...................................................................................................................................10

3. Explaining the importance and meaning of different accounting concepts .........................12

CONCLUSION .............................................................................................................................13

REFERENCES .............................................................................................................................14

INTRODUCTION ..........................................................................................................................3

Question 1a).....................................................................................................................................3

Question 1b).....................................................................................................................................4

Critically evaluating the features of financial information that is beneficial and important for

users.............................................................................................................................................4

Question 2a).....................................................................................................................................5

Question 2b).....................................................................................................................................7

2...................................................................................................................................................9

Question 2c)...................................................................................................................................10

3. Explaining the importance and meaning of different accounting concepts .........................12

CONCLUSION .............................................................................................................................13

REFERENCES .............................................................................................................................14

INTRODUCTION

Accounting is the procedure in recording the business transactions with respect to an

organization. It involves assessing, summarizing & reporting such transactions for over-sighting

agencies, tax collection firms and the regulators. The present report includes preparation of the

final accounts for computing the profitability and financial state of the company. Furthermore,

the report presents ratio analysis for measuring performance of firm over 2 years. Moreover, it

includes framing of journal, ledger balances and trial balance of company's financial

transactions.

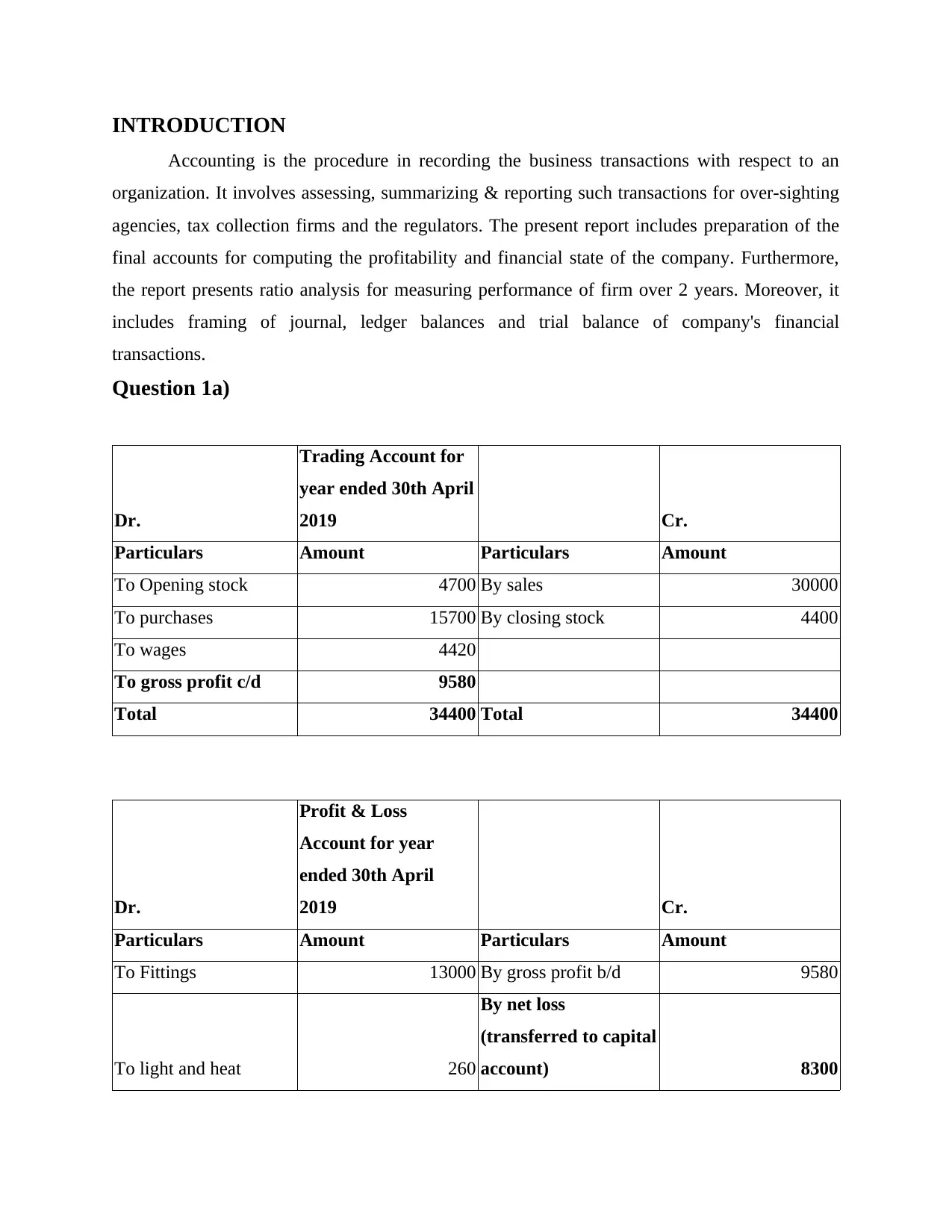

Question 1a)

Dr.

Trading Account for

year ended 30th April

2019 Cr.

Particulars Amount Particulars Amount

To Opening stock 4700 By sales 30000

To purchases 15700 By closing stock 4400

To wages 4420

To gross profit c/d 9580

Total 34400 Total 34400

Dr.

Profit & Loss

Account for year

ended 30th April

2019 Cr.

Particulars Amount Particulars Amount

To Fittings 13000 By gross profit b/d 9580

To light and heat 260

By net loss

(transferred to capital

account) 8300

Accounting is the procedure in recording the business transactions with respect to an

organization. It involves assessing, summarizing & reporting such transactions for over-sighting

agencies, tax collection firms and the regulators. The present report includes preparation of the

final accounts for computing the profitability and financial state of the company. Furthermore,

the report presents ratio analysis for measuring performance of firm over 2 years. Moreover, it

includes framing of journal, ledger balances and trial balance of company's financial

transactions.

Question 1a)

Dr.

Trading Account for

year ended 30th April

2019 Cr.

Particulars Amount Particulars Amount

To Opening stock 4700 By sales 30000

To purchases 15700 By closing stock 4400

To wages 4420

To gross profit c/d 9580

Total 34400 Total 34400

Dr.

Profit & Loss

Account for year

ended 30th April

2019 Cr.

Particulars Amount Particulars Amount

To Fittings 13000 By gross profit b/d 9580

To light and heat 260

By net loss

(transferred to capital

account) 8300

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

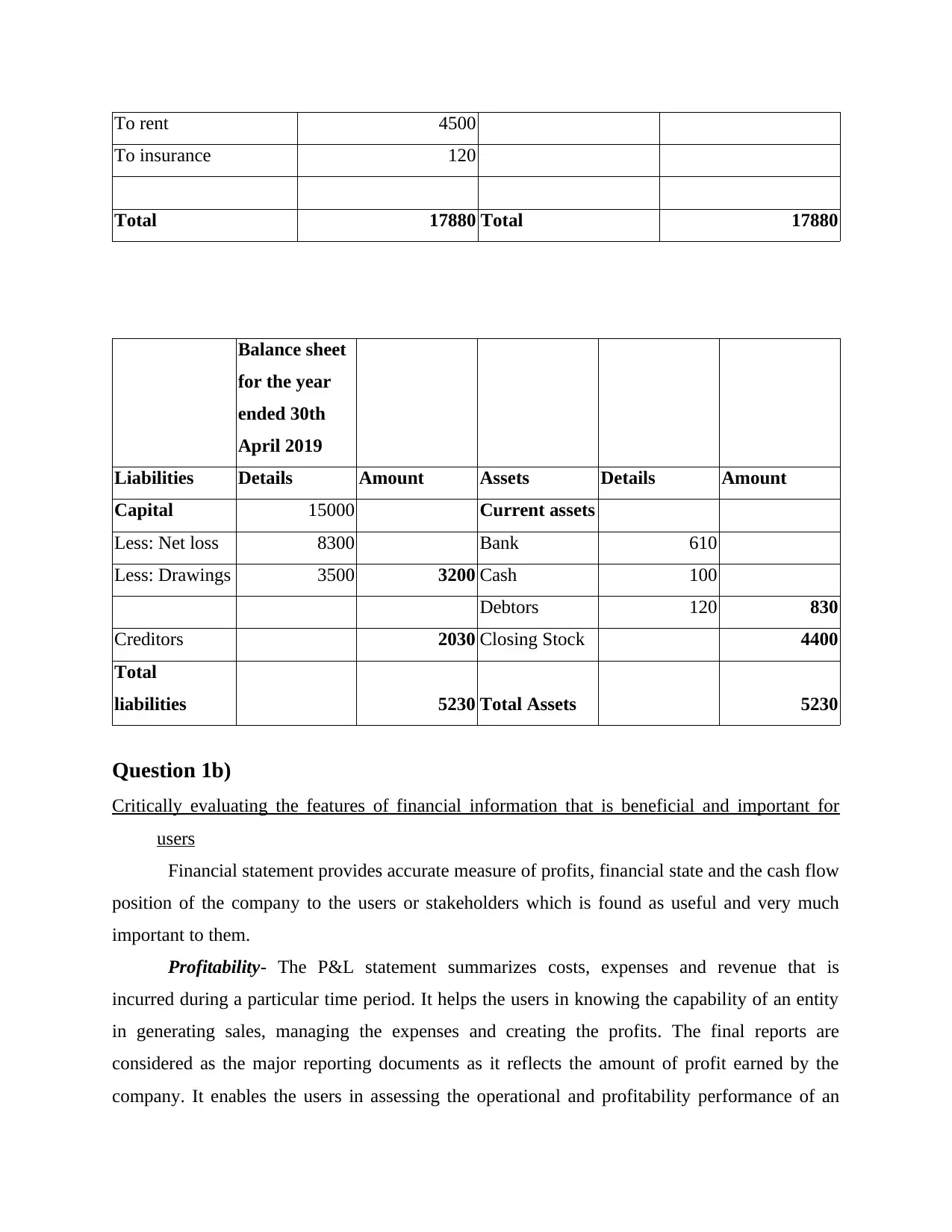

To rent 4500

To insurance 120

Total 17880 Total 17880

Balance sheet

for the year

ended 30th

April 2019

Liabilities Details Amount Assets Details Amount

Capital 15000 Current assets

Less: Net loss 8300 Bank 610

Less: Drawings 3500 3200 Cash 100

Debtors 120 830

Creditors 2030 Closing Stock 4400

Total

liabilities 5230 Total Assets 5230

Question 1b)

Critically evaluating the features of financial information that is beneficial and important for

users

Financial statement provides accurate measure of profits, financial state and the cash flow

position of the company to the users or stakeholders which is found as useful and very much

important to them.

Profitability- The P&L statement summarizes costs, expenses and revenue that is

incurred during a particular time period. It helps the users in knowing the capability of an entity

in generating sales, managing the expenses and creating the profits. The final reports are

considered as the major reporting documents as it reflects the amount of profit earned by the

company. It enables the users in assessing the operational and profitability performance of an

To insurance 120

Total 17880 Total 17880

Balance sheet

for the year

ended 30th

April 2019

Liabilities Details Amount Assets Details Amount

Capital 15000 Current assets

Less: Net loss 8300 Bank 610

Less: Drawings 3500 3200 Cash 100

Debtors 120 830

Creditors 2030 Closing Stock 4400

Total

liabilities 5230 Total Assets 5230

Question 1b)

Critically evaluating the features of financial information that is beneficial and important for

users

Financial statement provides accurate measure of profits, financial state and the cash flow

position of the company to the users or stakeholders which is found as useful and very much

important to them.

Profitability- The P&L statement summarizes costs, expenses and revenue that is

incurred during a particular time period. It helps the users in knowing the capability of an entity

in generating sales, managing the expenses and creating the profits. The final reports are

considered as the major reporting documents as it reflects the amount of profit earned by the

company. It enables the users in assessing the operational and profitability performance of an

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

entity so that they could make suitable decisions relating to withdrawal or making further

investment (Mihai, 2016). This information also helps the stakeholders in tracking and making

comparative analysis of the company's performance within overall market and industry so that

they could measure their rate of return effectively and efficiently. It also helps the internal users

in analysing the expenses or disbursement made in producing the product and revenue generated

by selling the goods. This kind of information acts as the basis in predicting the future

performance of the company in terms of its profits and costs. Government reviews the income

statement for investigating that the firm is operating its business in compliance with all

accounting concepts and meeting their tax obligations. It helps the management team for

understanding net income of the business that might be helpful in the process of decision-making

(Vitolla and Raimo, 2018). Moreover, it gives a true picture relating to indirect expenses so that

proper action could be taken to control it and increasing revenue.

Financial position- The balance sheet is the one of the key statement that provides the

information relating to liabilities, shareholders equity and the assets of the company of a specific

accounting or financial year. The main objective of this statement is to provide an idea to

interested users regarding the financial health along with an information what an entity owes or

owns. It is found as crucial for owners & accountant in understanding the way in which it could

be read and interpreted (Kim and et.al., 2016). This document offers quick view of an entity's

financial standing. It helps in knowing the bank that the firm qualifies in getting additional credit

or the loans. IN addition to this, it also assists the potential investors in understanding where their

respective funding would go & what they could expect for receiving in future periods. Investor

shows their keen interest in making investment in the firm which contains high liquid assets

because it shows that an enterprise would be achieving growing success in coming years. This

report also helps in analysing the leverage, efficiency and liquidity position so by facilitating

information in relation to the debts, owners equity, debtors, creditors, inventory, current

liabilities and assets.

Cash position- The cash flow report provides an aggregate data relating to all the cash

receipts from business operations and an external sources of investment. It also involves cash

outflows which pays for the business investments and activities during the given point of time.

This statement is been used for measuring cash perspective of business that is outflow & inflow

of cash (Goumas, Charamis and Tabouratzi, 2018). It helps the users to assess cash availability

investment (Mihai, 2016). This information also helps the stakeholders in tracking and making

comparative analysis of the company's performance within overall market and industry so that

they could measure their rate of return effectively and efficiently. It also helps the internal users

in analysing the expenses or disbursement made in producing the product and revenue generated

by selling the goods. This kind of information acts as the basis in predicting the future

performance of the company in terms of its profits and costs. Government reviews the income

statement for investigating that the firm is operating its business in compliance with all

accounting concepts and meeting their tax obligations. It helps the management team for

understanding net income of the business that might be helpful in the process of decision-making

(Vitolla and Raimo, 2018). Moreover, it gives a true picture relating to indirect expenses so that

proper action could be taken to control it and increasing revenue.

Financial position- The balance sheet is the one of the key statement that provides the

information relating to liabilities, shareholders equity and the assets of the company of a specific

accounting or financial year. The main objective of this statement is to provide an idea to

interested users regarding the financial health along with an information what an entity owes or

owns. It is found as crucial for owners & accountant in understanding the way in which it could

be read and interpreted (Kim and et.al., 2016). This document offers quick view of an entity's

financial standing. It helps in knowing the bank that the firm qualifies in getting additional credit

or the loans. IN addition to this, it also assists the potential investors in understanding where their

respective funding would go & what they could expect for receiving in future periods. Investor

shows their keen interest in making investment in the firm which contains high liquid assets

because it shows that an enterprise would be achieving growing success in coming years. This

report also helps in analysing the leverage, efficiency and liquidity position so by facilitating

information in relation to the debts, owners equity, debtors, creditors, inventory, current

liabilities and assets.

Cash position- The cash flow report provides an aggregate data relating to all the cash

receipts from business operations and an external sources of investment. It also involves cash

outflows which pays for the business investments and activities during the given point of time.

This statement is been used for measuring cash perspective of business that is outflow & inflow

of cash (Goumas, Charamis and Tabouratzi, 2018). It helps the users to assess cash availability

within their business and the funds required to meet contingent circumstances in coming period.

It helps the financial analyst in planning for short and long term with assessing an optimum cash

level & the requirement of working capital in the firm. Through this firm, an entity could know

whether its funds are idle or there is lack or excess of funds. After knowing an actual position,

managers of firm could take the decisions accordingly.

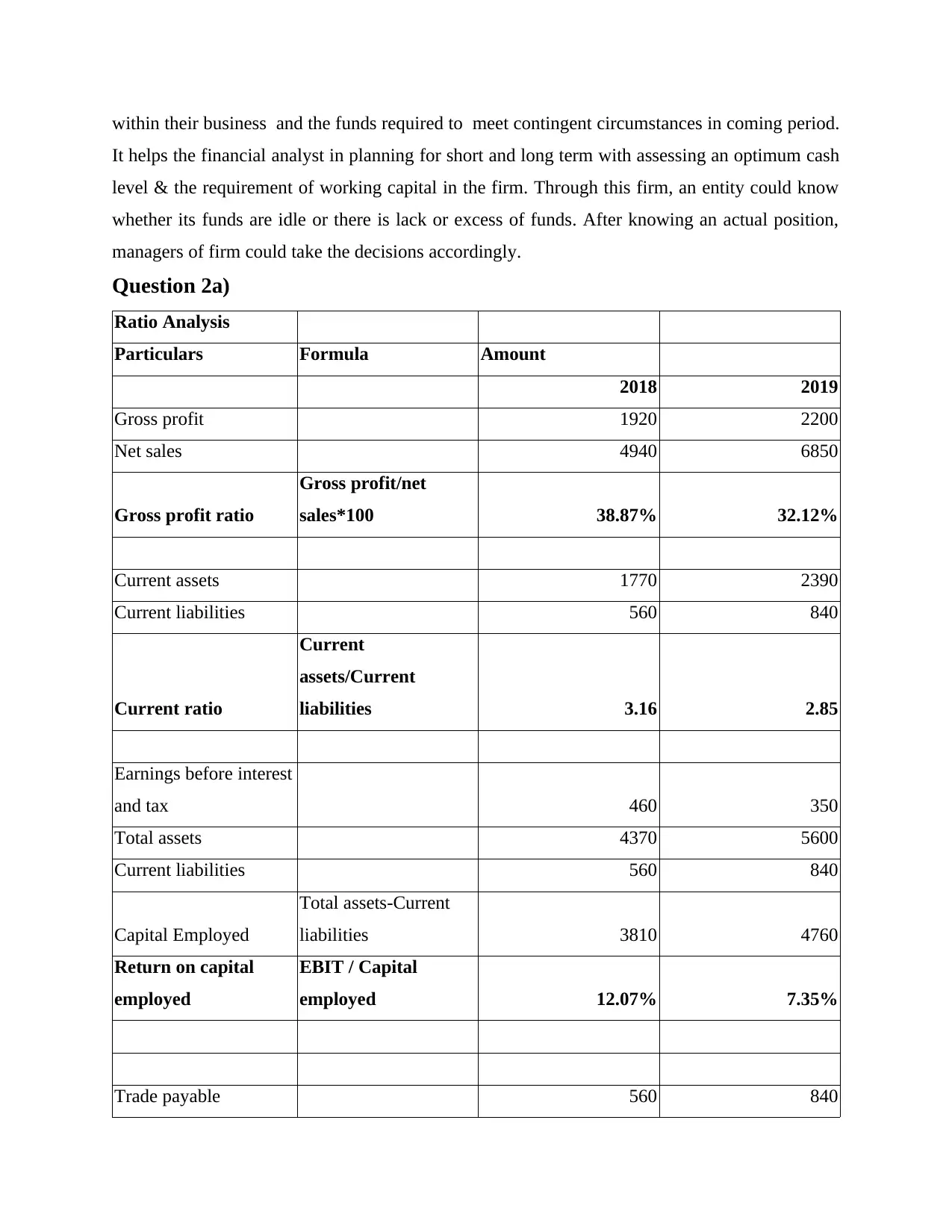

Question 2a)

Ratio Analysis

Particulars Formula Amount

2018 2019

Gross profit 1920 2200

Net sales 4940 6850

Gross profit ratio

Gross profit/net

sales*100 38.87% 32.12%

Current assets 1770 2390

Current liabilities 560 840

Current ratio

Current

assets/Current

liabilities 3.16 2.85

Earnings before interest

and tax 460 350

Total assets 4370 5600

Current liabilities 560 840

Capital Employed

Total assets-Current

liabilities 3810 4760

Return on capital

employed

EBIT / Capital

employed 12.07% 7.35%

Trade payable 560 840

It helps the financial analyst in planning for short and long term with assessing an optimum cash

level & the requirement of working capital in the firm. Through this firm, an entity could know

whether its funds are idle or there is lack or excess of funds. After knowing an actual position,

managers of firm could take the decisions accordingly.

Question 2a)

Ratio Analysis

Particulars Formula Amount

2018 2019

Gross profit 1920 2200

Net sales 4940 6850

Gross profit ratio

Gross profit/net

sales*100 38.87% 32.12%

Current assets 1770 2390

Current liabilities 560 840

Current ratio

Current

assets/Current

liabilities 3.16 2.85

Earnings before interest

and tax 460 350

Total assets 4370 5600

Current liabilities 560 840

Capital Employed

Total assets-Current

liabilities 3810 4760

Return on capital

employed

EBIT / Capital

employed 12.07% 7.35%

Trade payable 560 840

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

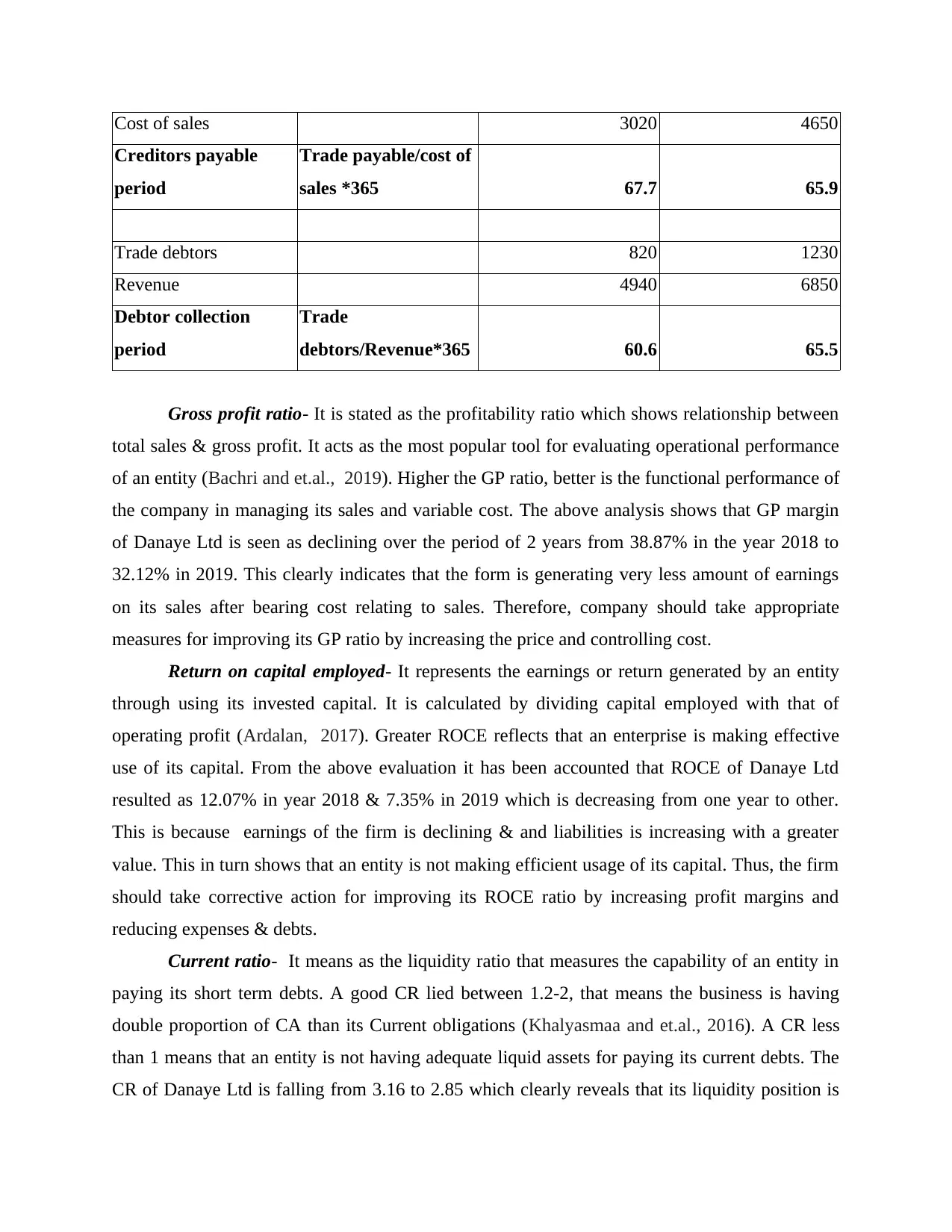

Cost of sales 3020 4650

Creditors payable

period

Trade payable/cost of

sales *365 67.7 65.9

Trade debtors 820 1230

Revenue 4940 6850

Debtor collection

period

Trade

debtors/Revenue*365 60.6 65.5

Gross profit ratio- It is stated as the profitability ratio which shows relationship between

total sales & gross profit. It acts as the most popular tool for evaluating operational performance

of an entity (Bachri and et.al., 2019). Higher the GP ratio, better is the functional performance of

the company in managing its sales and variable cost. The above analysis shows that GP margin

of Danaye Ltd is seen as declining over the period of 2 years from 38.87% in the year 2018 to

32.12% in 2019. This clearly indicates that the form is generating very less amount of earnings

on its sales after bearing cost relating to sales. Therefore, company should take appropriate

measures for improving its GP ratio by increasing the price and controlling cost.

Return on capital employed- It represents the earnings or return generated by an entity

through using its invested capital. It is calculated by dividing capital employed with that of

operating profit (Ardalan, 2017). Greater ROCE reflects that an enterprise is making effective

use of its capital. From the above evaluation it has been accounted that ROCE of Danaye Ltd

resulted as 12.07% in year 2018 & 7.35% in 2019 which is decreasing from one year to other.

This is because earnings of the firm is declining & and liabilities is increasing with a greater

value. This in turn shows that an entity is not making efficient usage of its capital. Thus, the firm

should take corrective action for improving its ROCE ratio by increasing profit margins and

reducing expenses & debts.

Current ratio- It means as the liquidity ratio that measures the capability of an entity in

paying its short term debts. A good CR lied between 1.2-2, that means the business is having

double proportion of CA than its Current obligations (Khalyasmaa and et.al., 2016). A CR less

than 1 means that an entity is not having adequate liquid assets for paying its current debts. The

CR of Danaye Ltd is falling from 3.16 to 2.85 which clearly reveals that its liquidity position is

Creditors payable

period

Trade payable/cost of

sales *365 67.7 65.9

Trade debtors 820 1230

Revenue 4940 6850

Debtor collection

period

Trade

debtors/Revenue*365 60.6 65.5

Gross profit ratio- It is stated as the profitability ratio which shows relationship between

total sales & gross profit. It acts as the most popular tool for evaluating operational performance

of an entity (Bachri and et.al., 2019). Higher the GP ratio, better is the functional performance of

the company in managing its sales and variable cost. The above analysis shows that GP margin

of Danaye Ltd is seen as declining over the period of 2 years from 38.87% in the year 2018 to

32.12% in 2019. This clearly indicates that the form is generating very less amount of earnings

on its sales after bearing cost relating to sales. Therefore, company should take appropriate

measures for improving its GP ratio by increasing the price and controlling cost.

Return on capital employed- It represents the earnings or return generated by an entity

through using its invested capital. It is calculated by dividing capital employed with that of

operating profit (Ardalan, 2017). Greater ROCE reflects that an enterprise is making effective

use of its capital. From the above evaluation it has been accounted that ROCE of Danaye Ltd

resulted as 12.07% in year 2018 & 7.35% in 2019 which is decreasing from one year to other.

This is because earnings of the firm is declining & and liabilities is increasing with a greater

value. This in turn shows that an entity is not making efficient usage of its capital. Thus, the firm

should take corrective action for improving its ROCE ratio by increasing profit margins and

reducing expenses & debts.

Current ratio- It means as the liquidity ratio that measures the capability of an entity in

paying its short term debts. A good CR lied between 1.2-2, that means the business is having

double proportion of CA than its Current obligations (Khalyasmaa and et.al., 2016). A CR less

than 1 means that an entity is not having adequate liquid assets for paying its current debts. The

CR of Danaye Ltd is falling from 3.16 to 2.85 which clearly reveals that its liquidity position is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

good as its ratio is greater than 1 and reaching to ideal position. This signifies that the firm is

making an effective utilization of its current assets for making payment of its current debts.

Trade payable days- This ratio shows an average time the firm is taking in paying off its

invoices and bills. As the ACP of Danaye Ltd is declining from 68 days to 66 days, which

reflects that an entity is paying its payables within the specified and appropriate time frame (Wen

and Zhu, 2019). This shows that the firm is efficient in paying off its liabilities or payment to its

creditor on time.

Receivable days- It means as the no. of days for which invoice of customers remains as

outstanding before it is been collected. The assessment showed that debtor collection period of

Danaye Ltd is increasing from 60.6 days to 65.5 days which means that over the year its debtor

are taking more time in paying to firm (Bujaki, Lento and Sayed, 2019). However, 65 days is

considered as better ratio so overall it is represented that efficiency condition of the company is

good.

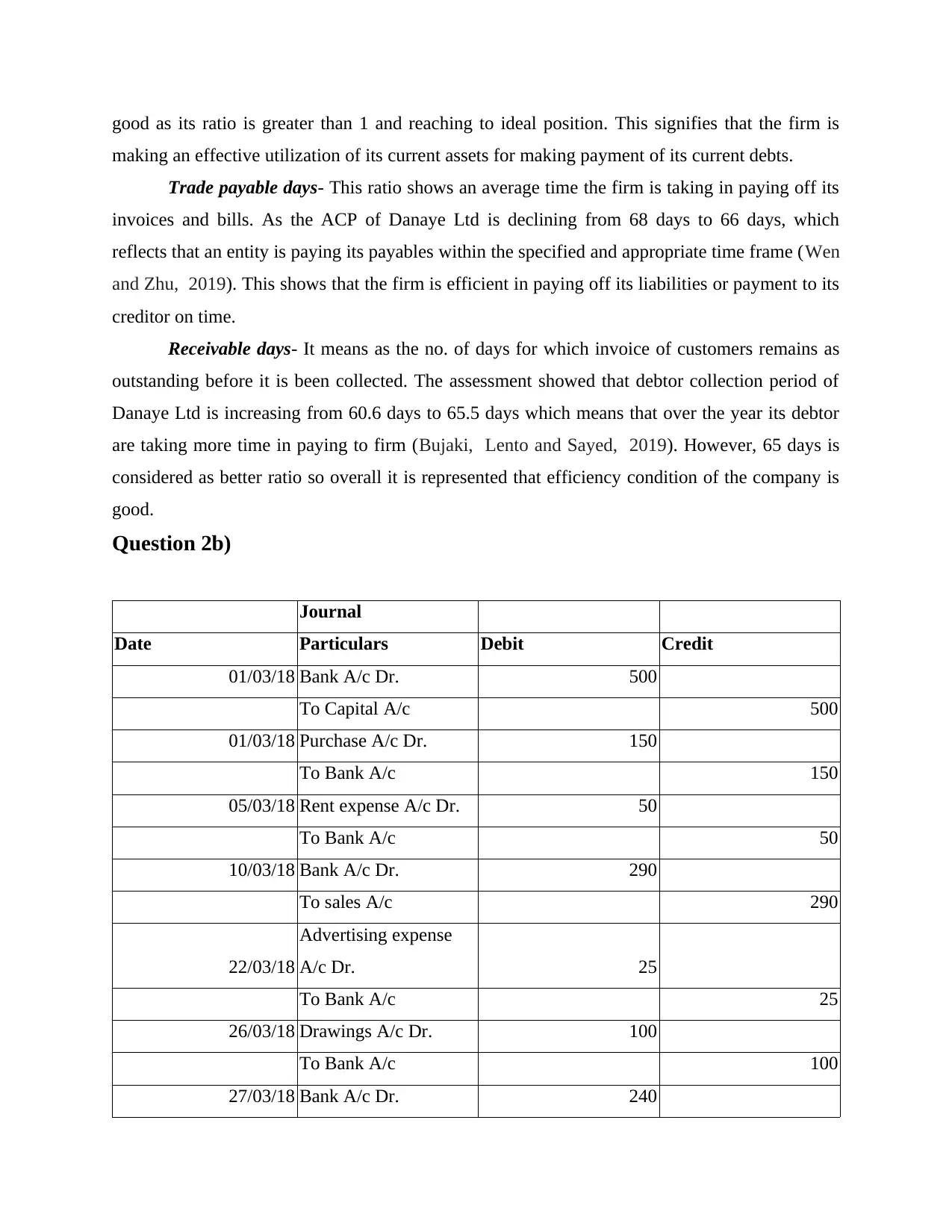

Question 2b)

Journal

Date Particulars Debit Credit

01/03/18 Bank A/c Dr. 500

To Capital A/c 500

01/03/18 Purchase A/c Dr. 150

To Bank A/c 150

05/03/18 Rent expense A/c Dr. 50

To Bank A/c 50

10/03/18 Bank A/c Dr. 290

To sales A/c 290

22/03/18

Advertising expense

A/c Dr. 25

To Bank A/c 25

26/03/18 Drawings A/c Dr. 100

To Bank A/c 100

27/03/18 Bank A/c Dr. 240

making an effective utilization of its current assets for making payment of its current debts.

Trade payable days- This ratio shows an average time the firm is taking in paying off its

invoices and bills. As the ACP of Danaye Ltd is declining from 68 days to 66 days, which

reflects that an entity is paying its payables within the specified and appropriate time frame (Wen

and Zhu, 2019). This shows that the firm is efficient in paying off its liabilities or payment to its

creditor on time.

Receivable days- It means as the no. of days for which invoice of customers remains as

outstanding before it is been collected. The assessment showed that debtor collection period of

Danaye Ltd is increasing from 60.6 days to 65.5 days which means that over the year its debtor

are taking more time in paying to firm (Bujaki, Lento and Sayed, 2019). However, 65 days is

considered as better ratio so overall it is represented that efficiency condition of the company is

good.

Question 2b)

Journal

Date Particulars Debit Credit

01/03/18 Bank A/c Dr. 500

To Capital A/c 500

01/03/18 Purchase A/c Dr. 150

To Bank A/c 150

05/03/18 Rent expense A/c Dr. 50

To Bank A/c 50

10/03/18 Bank A/c Dr. 290

To sales A/c 290

22/03/18

Advertising expense

A/c Dr. 25

To Bank A/c 25

26/03/18 Drawings A/c Dr. 100

To Bank A/c 100

27/03/18 Bank A/c Dr. 240

To sales A/c 240

02/04/18 Purchase A/c Dr. 100

To Bank A/c 100

05/04/18 Rent expense A/c Dr. 50

To Bank A/c 50

14/04/18 Bank A/c Dr. 450

To L Lock A/c 450

16/04/18 Bank A/c Dr. 330

To sales A/c 330

23/04/18 Drawings A/c Dr. 75

To Bank A/c 75

26/04/18 Bank A/c Dr. 180

To sales A/c 180

29/04/18

Adversting expense

A/c Dr. 30

To Bank A/c 30

Total 2570 2570

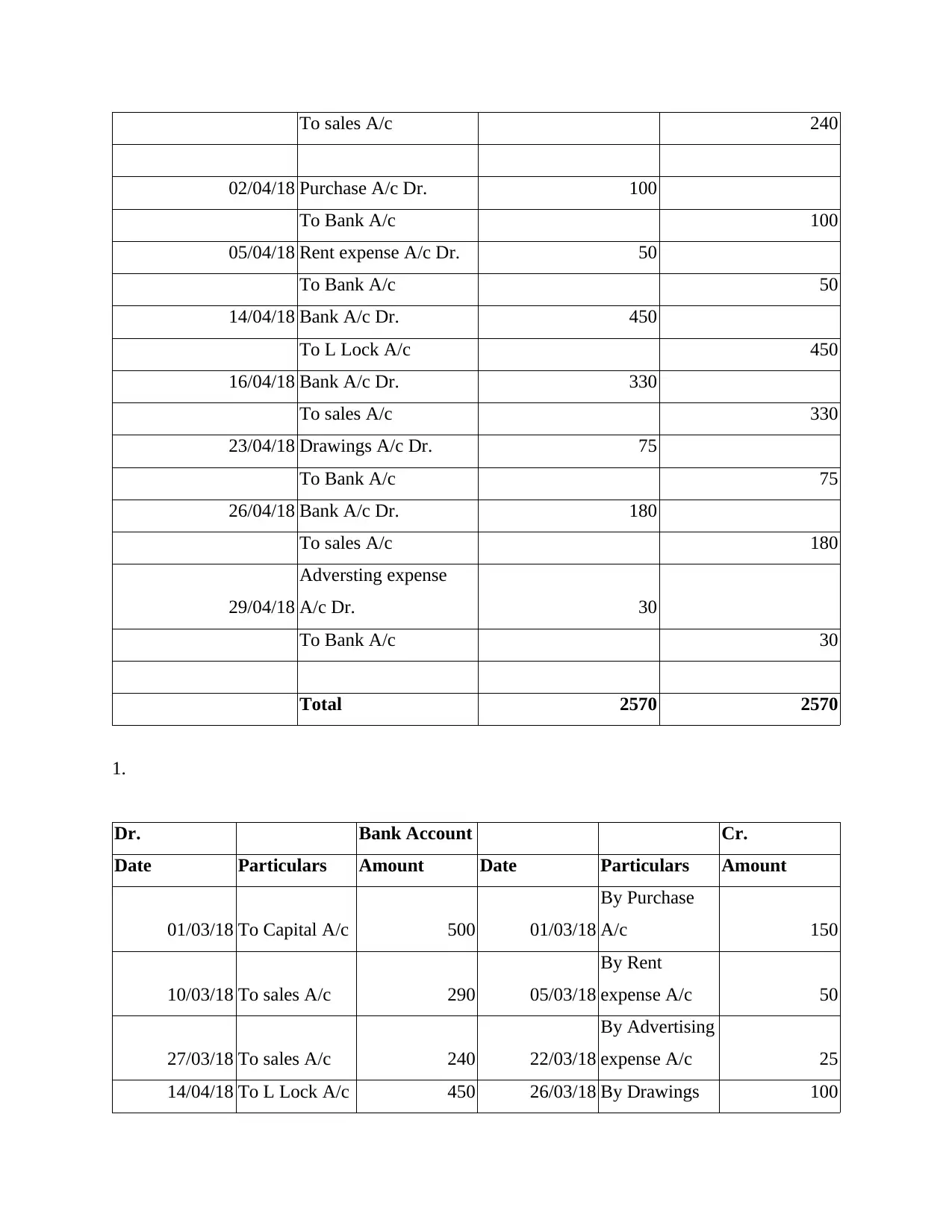

1.

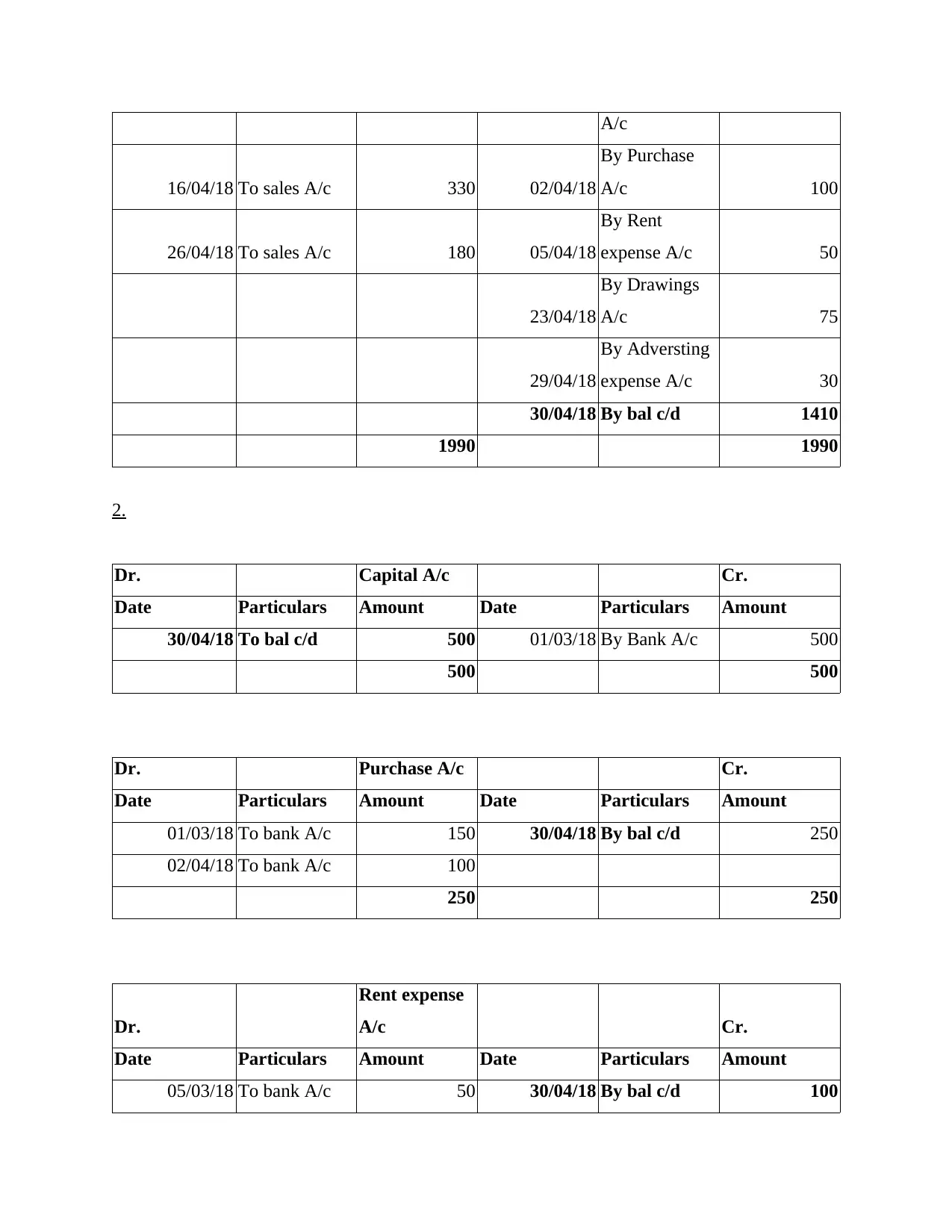

Dr. Bank Account Cr.

Date Particulars Amount Date Particulars Amount

01/03/18 To Capital A/c 500 01/03/18

By Purchase

A/c 150

10/03/18 To sales A/c 290 05/03/18

By Rent

expense A/c 50

27/03/18 To sales A/c 240 22/03/18

By Advertising

expense A/c 25

14/04/18 To L Lock A/c 450 26/03/18 By Drawings 100

02/04/18 Purchase A/c Dr. 100

To Bank A/c 100

05/04/18 Rent expense A/c Dr. 50

To Bank A/c 50

14/04/18 Bank A/c Dr. 450

To L Lock A/c 450

16/04/18 Bank A/c Dr. 330

To sales A/c 330

23/04/18 Drawings A/c Dr. 75

To Bank A/c 75

26/04/18 Bank A/c Dr. 180

To sales A/c 180

29/04/18

Adversting expense

A/c Dr. 30

To Bank A/c 30

Total 2570 2570

1.

Dr. Bank Account Cr.

Date Particulars Amount Date Particulars Amount

01/03/18 To Capital A/c 500 01/03/18

By Purchase

A/c 150

10/03/18 To sales A/c 290 05/03/18

By Rent

expense A/c 50

27/03/18 To sales A/c 240 22/03/18

By Advertising

expense A/c 25

14/04/18 To L Lock A/c 450 26/03/18 By Drawings 100

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

A/c

16/04/18 To sales A/c 330 02/04/18

By Purchase

A/c 100

26/04/18 To sales A/c 180 05/04/18

By Rent

expense A/c 50

23/04/18

By Drawings

A/c 75

29/04/18

By Adversting

expense A/c 30

30/04/18 By bal c/d 1410

1990 1990

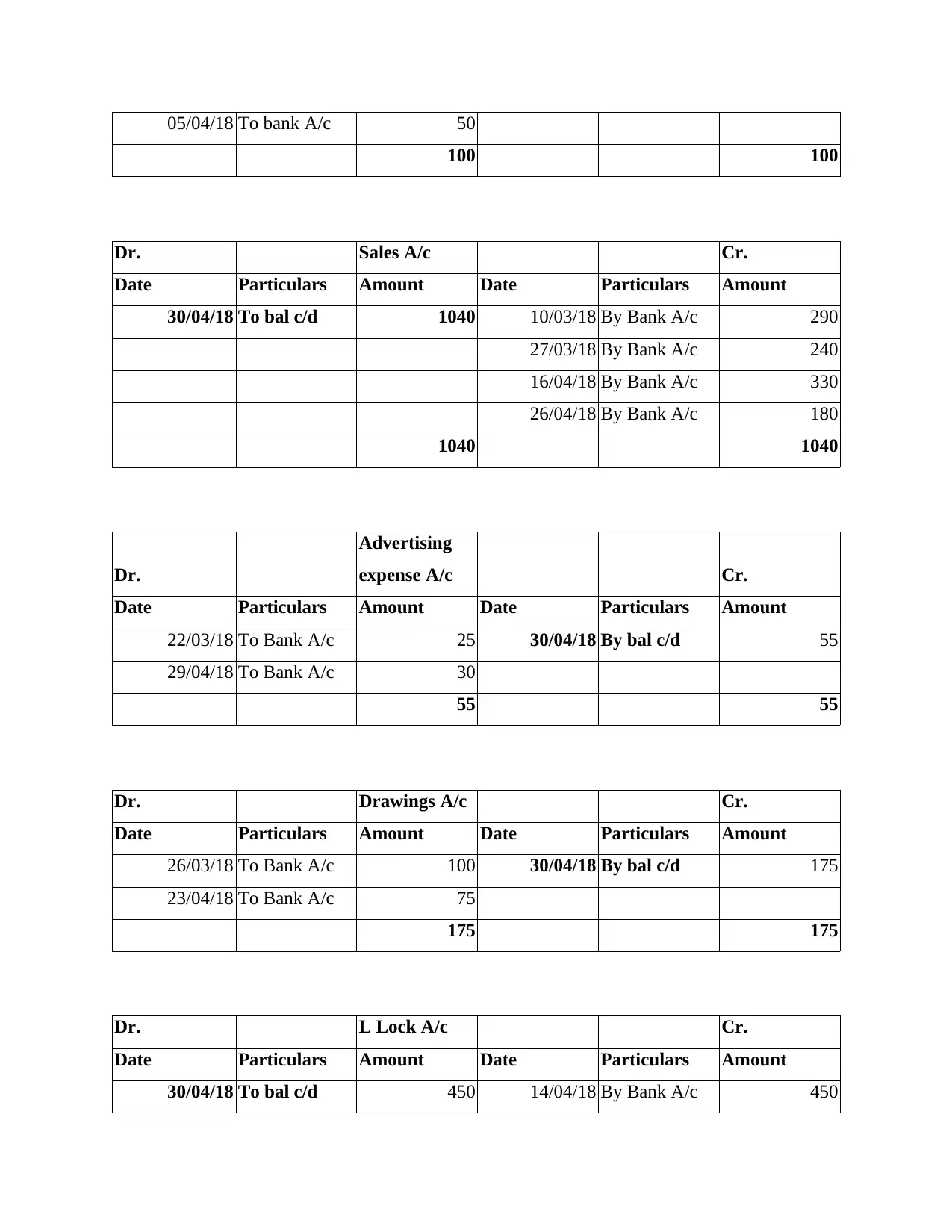

2.

Dr. Capital A/c Cr.

Date Particulars Amount Date Particulars Amount

30/04/18 To bal c/d 500 01/03/18 By Bank A/c 500

500 500

Dr. Purchase A/c Cr.

Date Particulars Amount Date Particulars Amount

01/03/18 To bank A/c 150 30/04/18 By bal c/d 250

02/04/18 To bank A/c 100

250 250

Dr.

Rent expense

A/c Cr.

Date Particulars Amount Date Particulars Amount

05/03/18 To bank A/c 50 30/04/18 By bal c/d 100

16/04/18 To sales A/c 330 02/04/18

By Purchase

A/c 100

26/04/18 To sales A/c 180 05/04/18

By Rent

expense A/c 50

23/04/18

By Drawings

A/c 75

29/04/18

By Adversting

expense A/c 30

30/04/18 By bal c/d 1410

1990 1990

2.

Dr. Capital A/c Cr.

Date Particulars Amount Date Particulars Amount

30/04/18 To bal c/d 500 01/03/18 By Bank A/c 500

500 500

Dr. Purchase A/c Cr.

Date Particulars Amount Date Particulars Amount

01/03/18 To bank A/c 150 30/04/18 By bal c/d 250

02/04/18 To bank A/c 100

250 250

Dr.

Rent expense

A/c Cr.

Date Particulars Amount Date Particulars Amount

05/03/18 To bank A/c 50 30/04/18 By bal c/d 100

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

05/04/18 To bank A/c 50

100 100

Dr. Sales A/c Cr.

Date Particulars Amount Date Particulars Amount

30/04/18 To bal c/d 1040 10/03/18 By Bank A/c 290

27/03/18 By Bank A/c 240

16/04/18 By Bank A/c 330

26/04/18 By Bank A/c 180

1040 1040

Dr.

Advertising

expense A/c Cr.

Date Particulars Amount Date Particulars Amount

22/03/18 To Bank A/c 25 30/04/18 By bal c/d 55

29/04/18 To Bank A/c 30

55 55

Dr. Drawings A/c Cr.

Date Particulars Amount Date Particulars Amount

26/03/18 To Bank A/c 100 30/04/18 By bal c/d 175

23/04/18 To Bank A/c 75

175 175

Dr. L Lock A/c Cr.

Date Particulars Amount Date Particulars Amount

30/04/18 To bal c/d 450 14/04/18 By Bank A/c 450

100 100

Dr. Sales A/c Cr.

Date Particulars Amount Date Particulars Amount

30/04/18 To bal c/d 1040 10/03/18 By Bank A/c 290

27/03/18 By Bank A/c 240

16/04/18 By Bank A/c 330

26/04/18 By Bank A/c 180

1040 1040

Dr.

Advertising

expense A/c Cr.

Date Particulars Amount Date Particulars Amount

22/03/18 To Bank A/c 25 30/04/18 By bal c/d 55

29/04/18 To Bank A/c 30

55 55

Dr. Drawings A/c Cr.

Date Particulars Amount Date Particulars Amount

26/03/18 To Bank A/c 100 30/04/18 By bal c/d 175

23/04/18 To Bank A/c 75

175 175

Dr. L Lock A/c Cr.

Date Particulars Amount Date Particulars Amount

30/04/18 To bal c/d 450 14/04/18 By Bank A/c 450

450 450

Question 2c)

Under Straight line method-

Dr.

Provision For

Depreciation

on Machinery

Account Cr.

Date Particulars Amount Date Particulars Amount

31/12/17 To bal c/d 2000 31/12/17

By

Depreciation

Expense 2000

2000 2000

01/01/18 By bal b/d 2000

31/12/18 To bal c/d 4000 31/12/18

By

Depreciation

Expense 2000

4000 4000

01/01/19 By bal b/d 4000

31/12/19 To bal c/d 6000 31/12/18

By

Depreciation

Expense 2000

6000 6000

Under reducing balance method-

Dr.

Provision For

Depreciation

on Machinery

Account Cr.

Question 2c)

Under Straight line method-

Dr.

Provision For

Depreciation

on Machinery

Account Cr.

Date Particulars Amount Date Particulars Amount

31/12/17 To bal c/d 2000 31/12/17

By

Depreciation

Expense 2000

2000 2000

01/01/18 By bal b/d 2000

31/12/18 To bal c/d 4000 31/12/18

By

Depreciation

Expense 2000

4000 4000

01/01/19 By bal b/d 4000

31/12/19 To bal c/d 6000 31/12/18

By

Depreciation

Expense 2000

6000 6000

Under reducing balance method-

Dr.

Provision For

Depreciation

on Machinery

Account Cr.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.