Financial Accounting Homework: Scenario Analysis and Journal Entries

VerifiedAdded on 2023/01/06

|24

|4585

|47

Homework Assignment

AI Summary

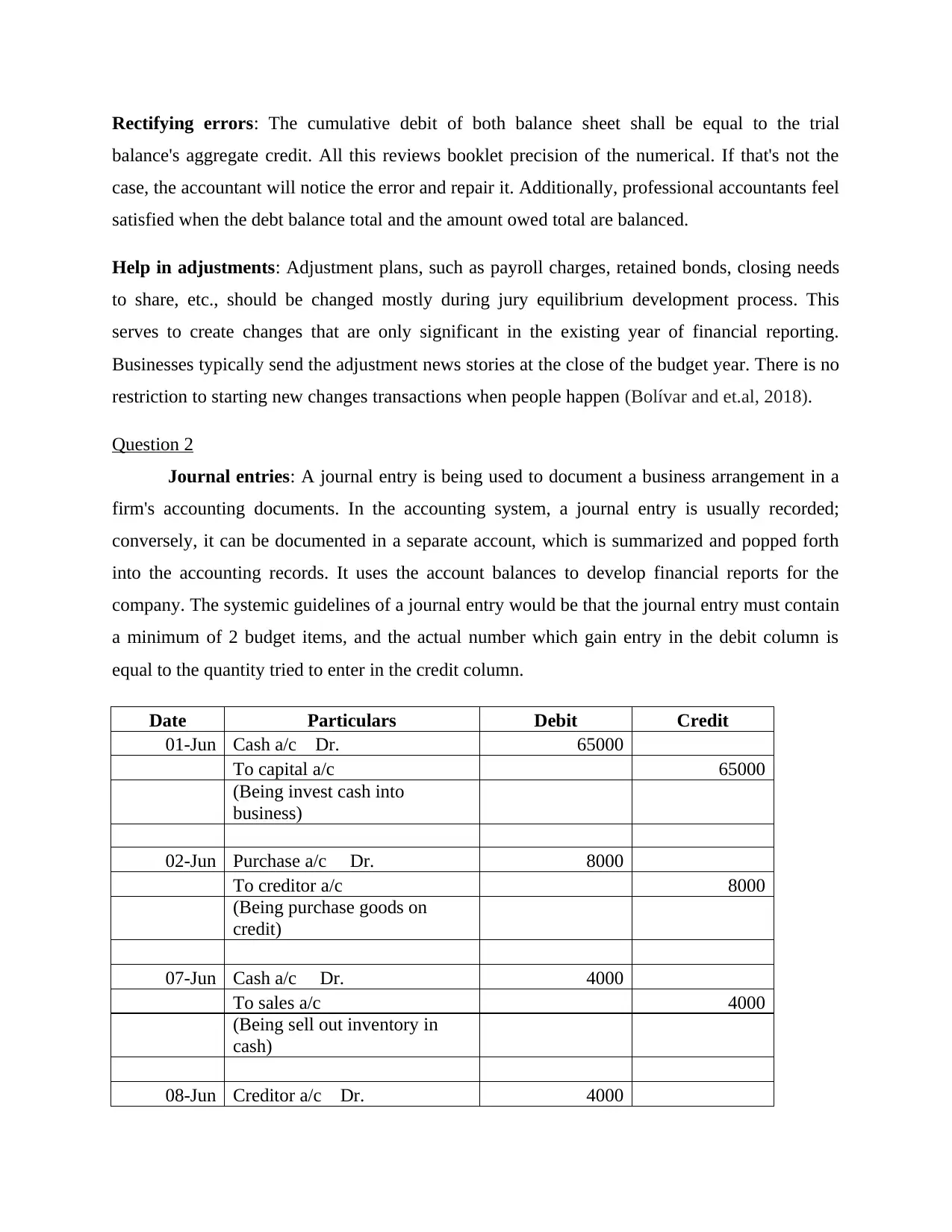

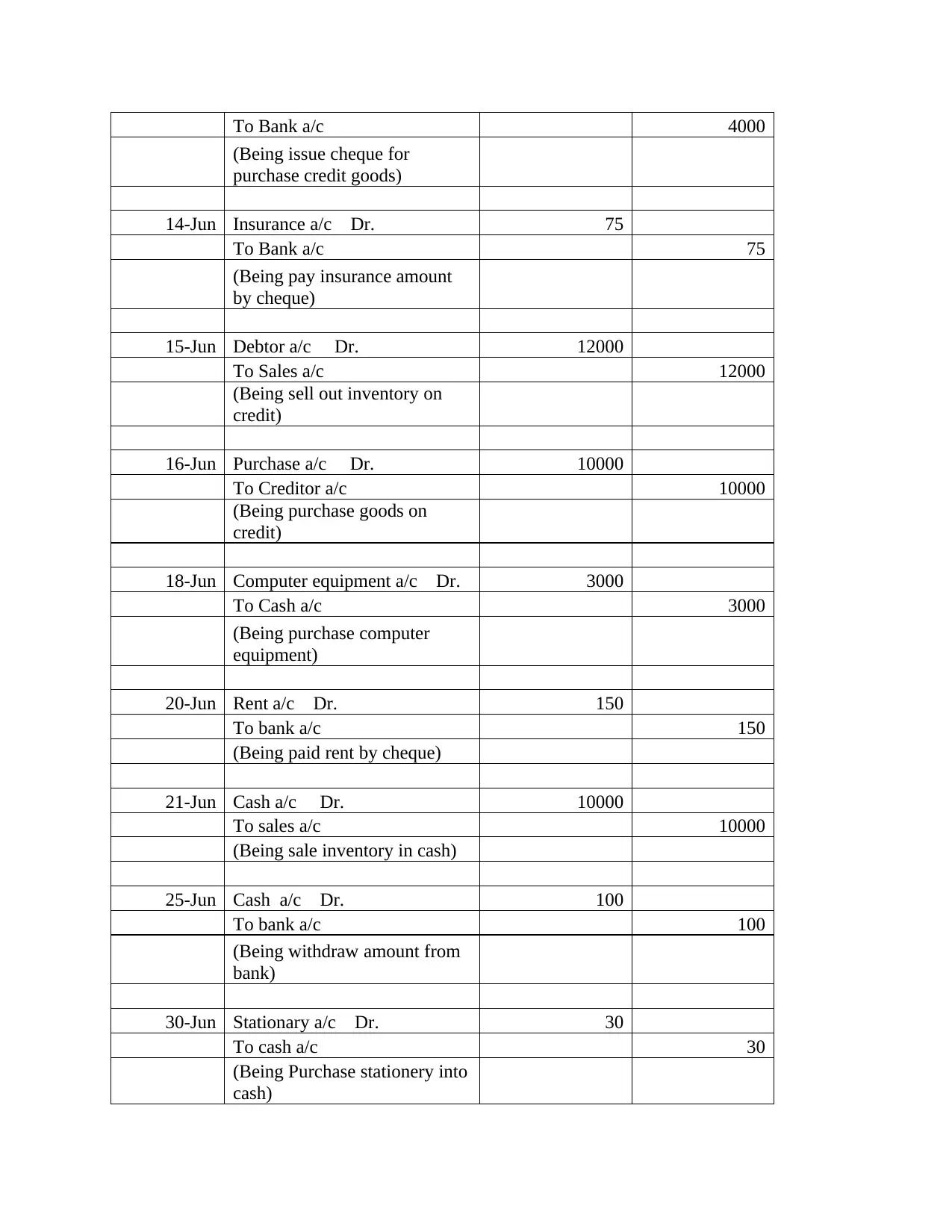

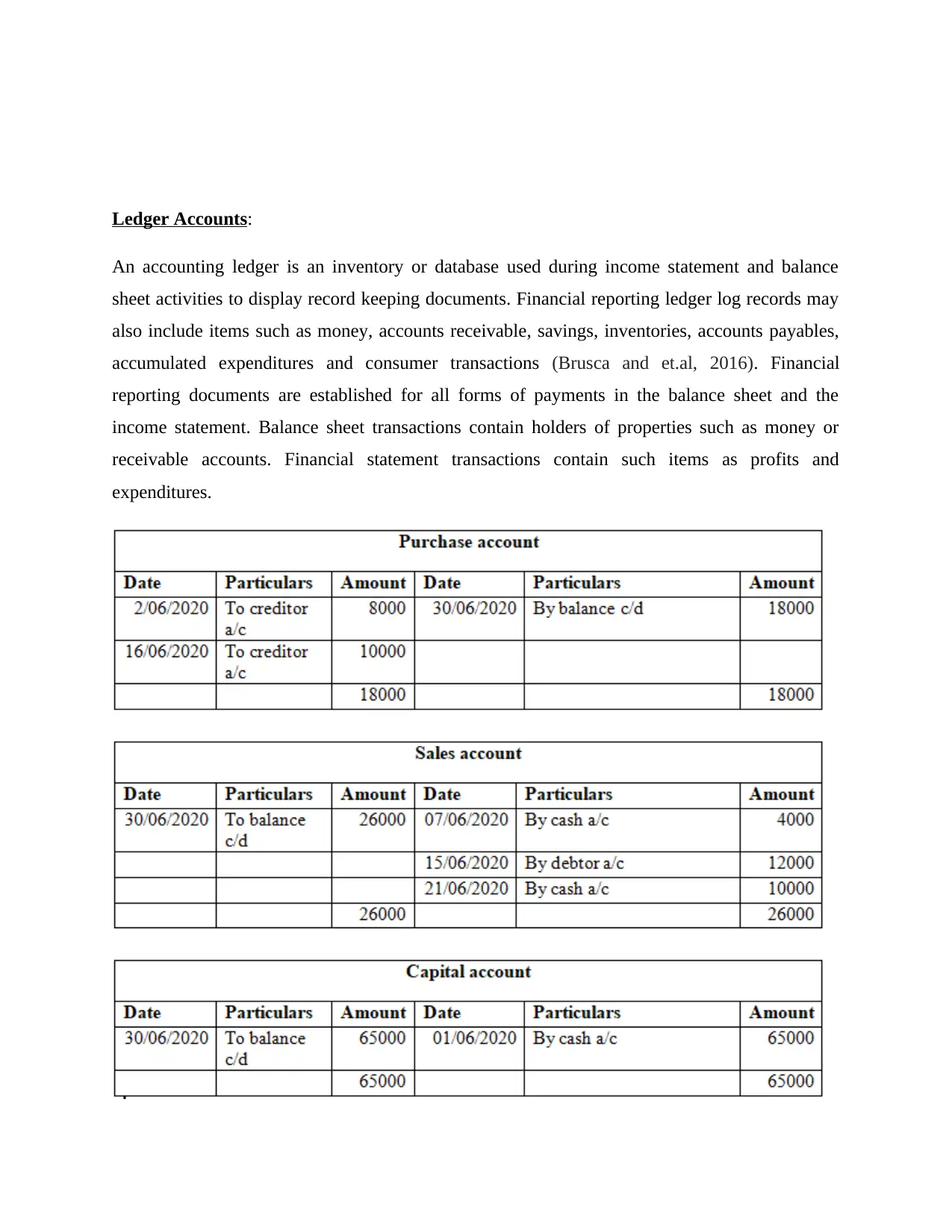

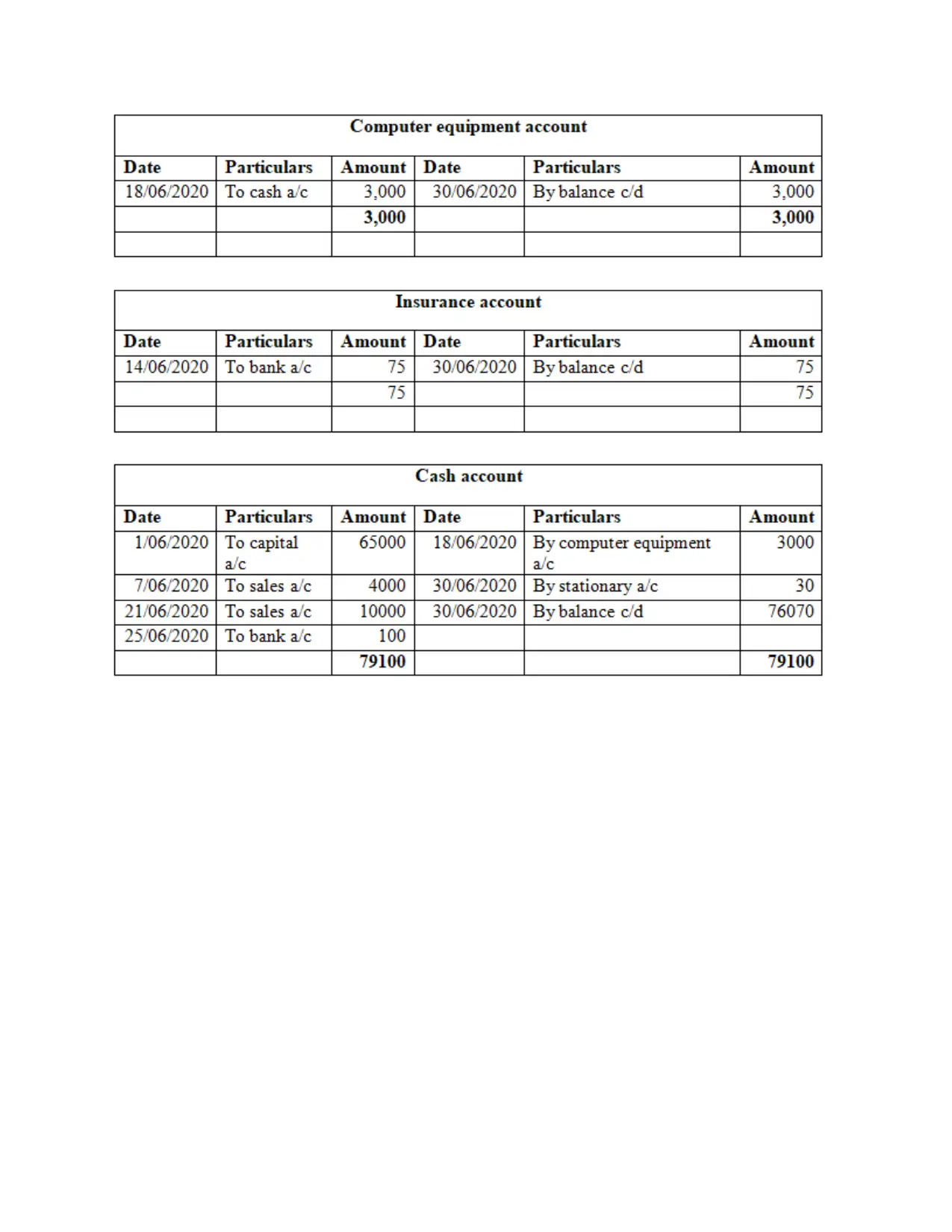

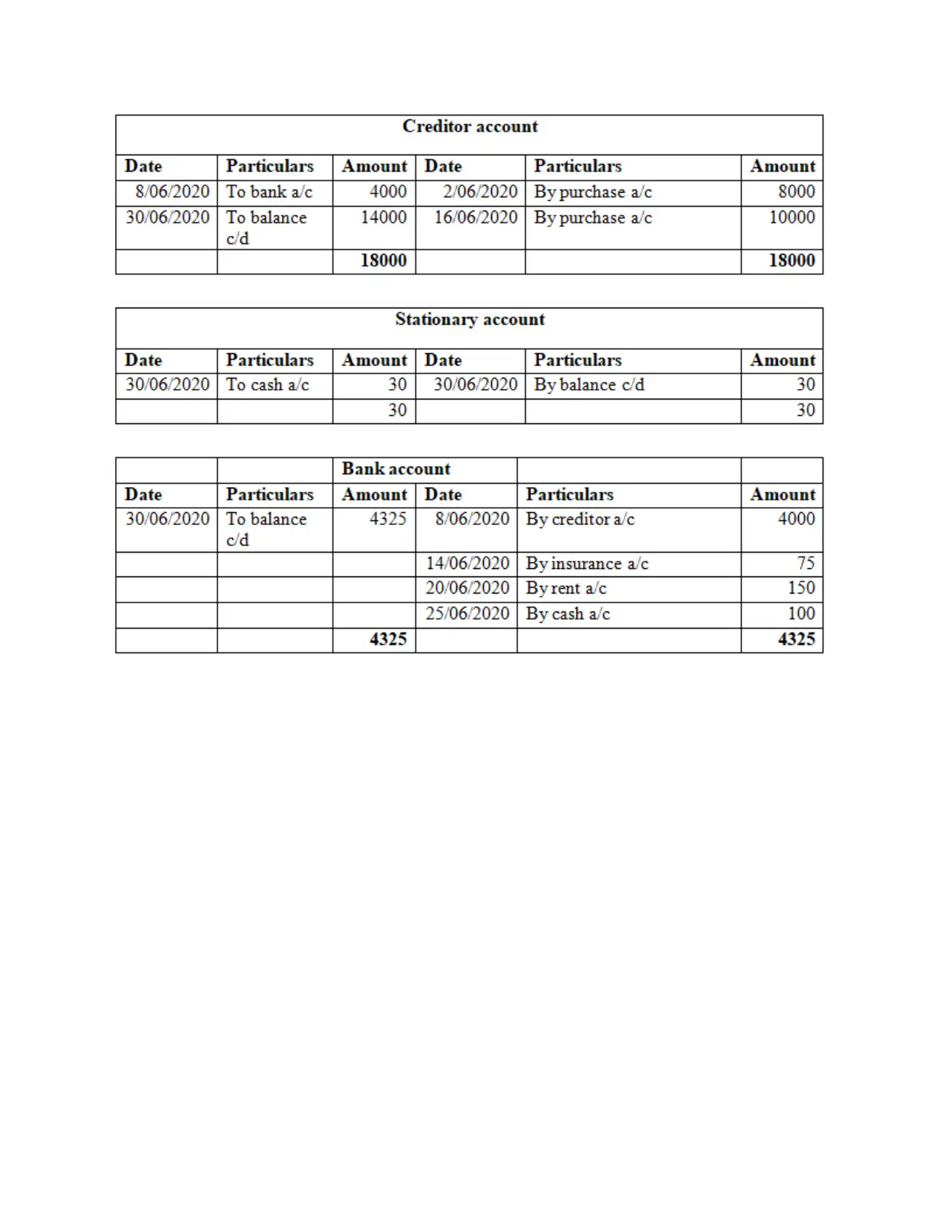

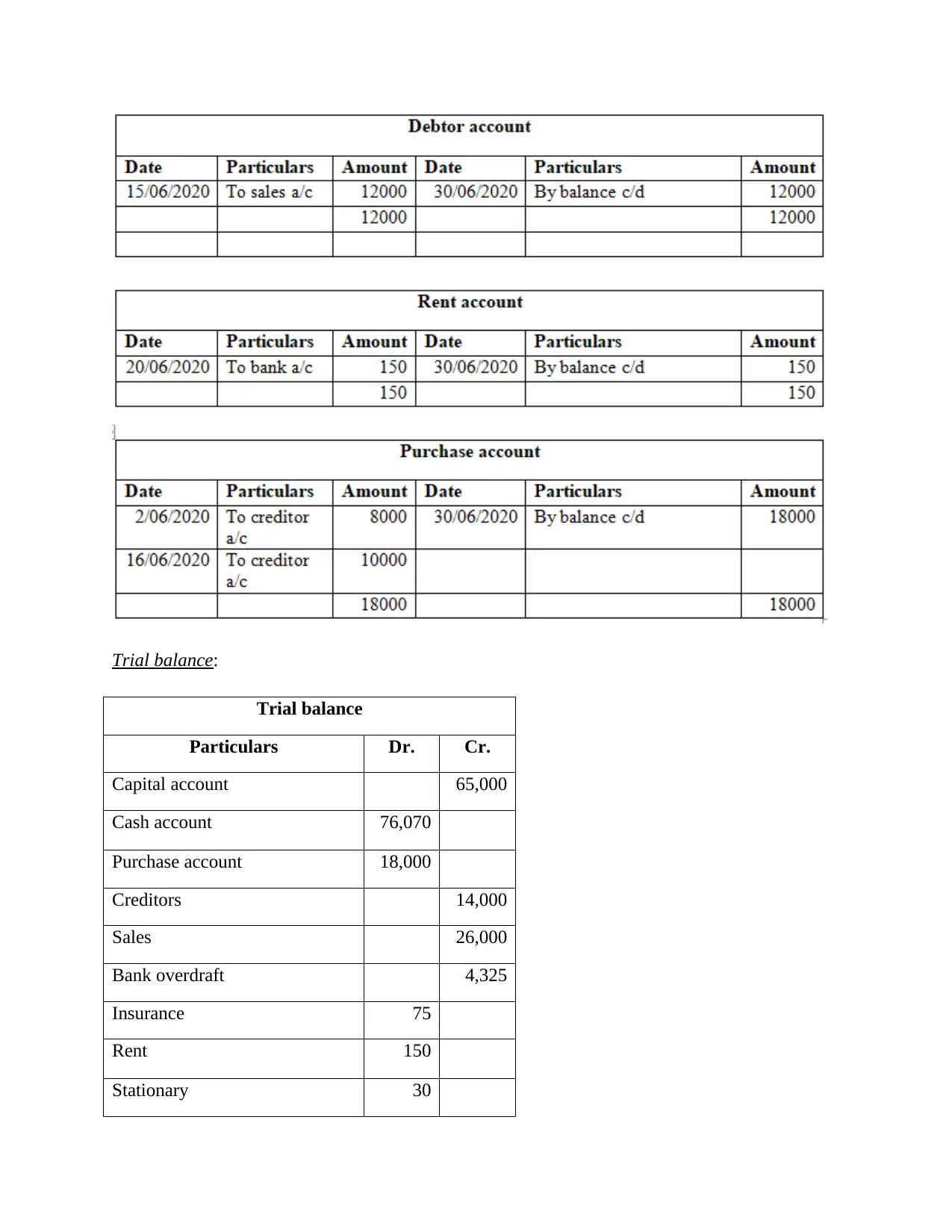

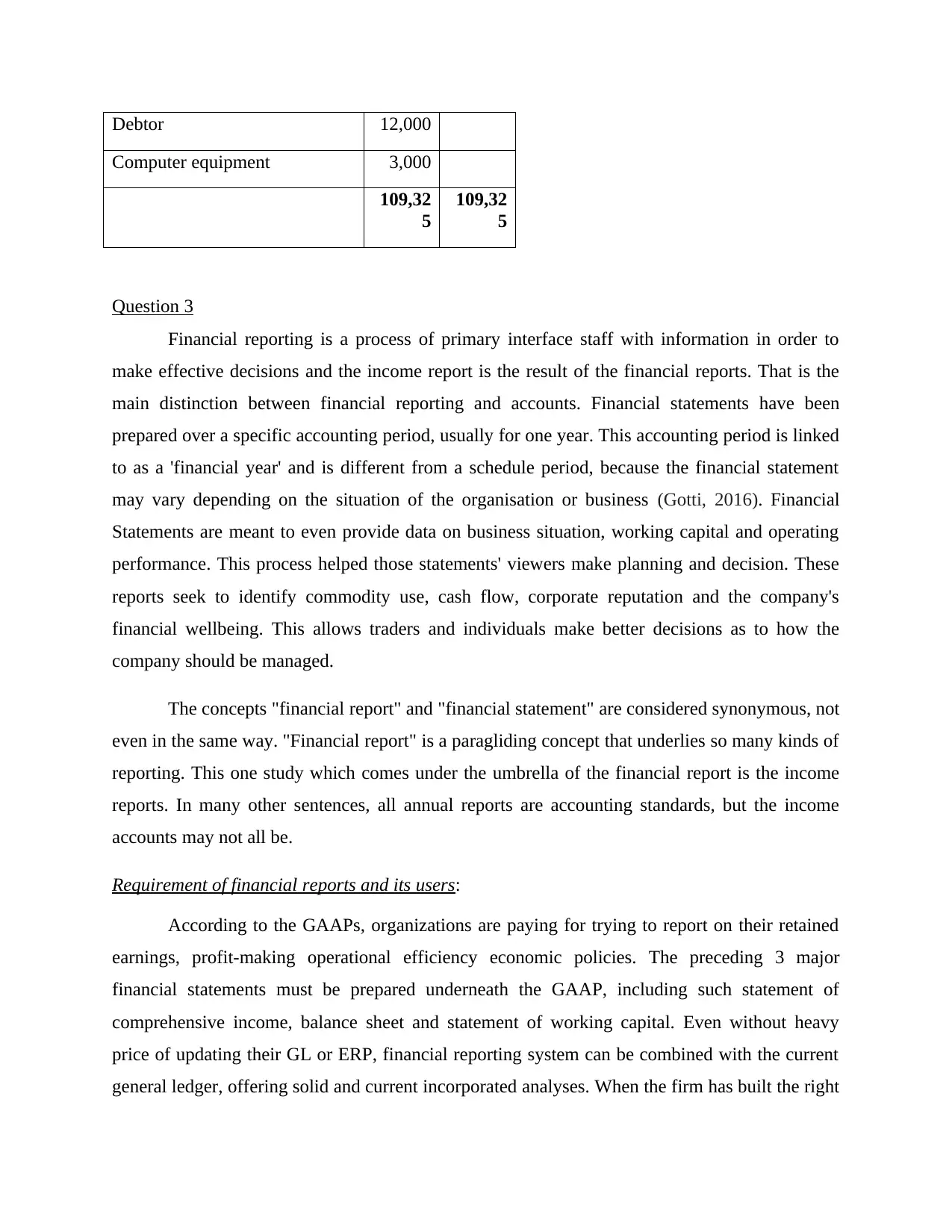

This document presents a comprehensive solution to a financial accounting homework assignment. The solution covers various aspects of financial accounting, including the documentation of business activities, journal entries, ledger accounts, and the preparation of financial statements. The assignment explores different forms of business transactions, such as sales, purchases, and payments, and explains the differences between single-entry and double-entry bookkeeping. It also highlights the importance of trial balances in checking accuracy and preparing financial statements. Furthermore, the solution delves into the concept of financial reporting and its users, discussing the role of financial statements in providing information for effective decision-making. The document also explains key accounting standards like the accrual principle, conservatism principle, and full disclosure principle. The solution includes examples of journal entries, ledger accounts, and a trial balance, demonstrating the practical application of accounting concepts. Overall, this assignment provides a detailed analysis of financial accounting principles and practices.

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.