Financial Accounting 1 Report: Business Transactions and Accounting

VerifiedAdded on 2023/01/10

|22

|4205

|32

Report

AI Summary

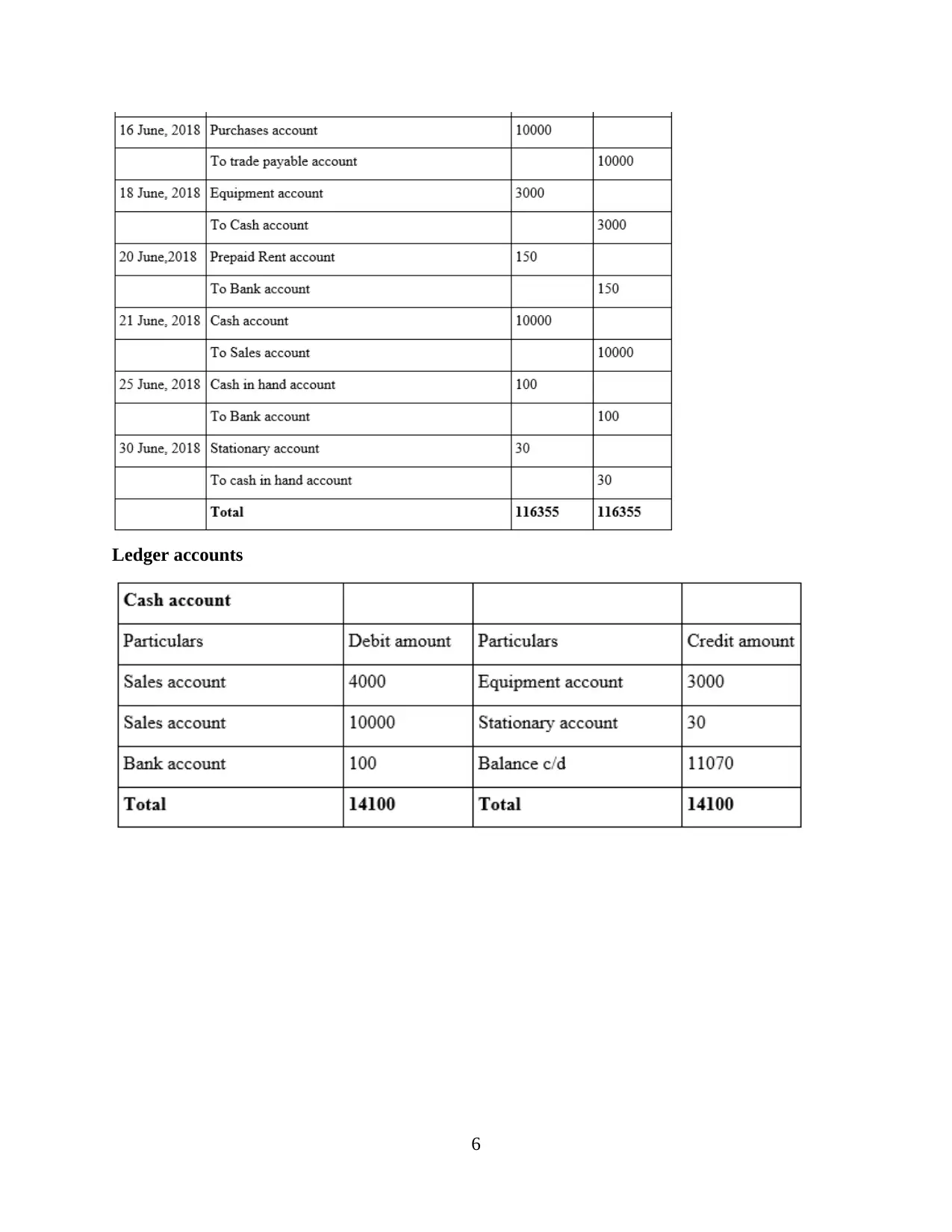

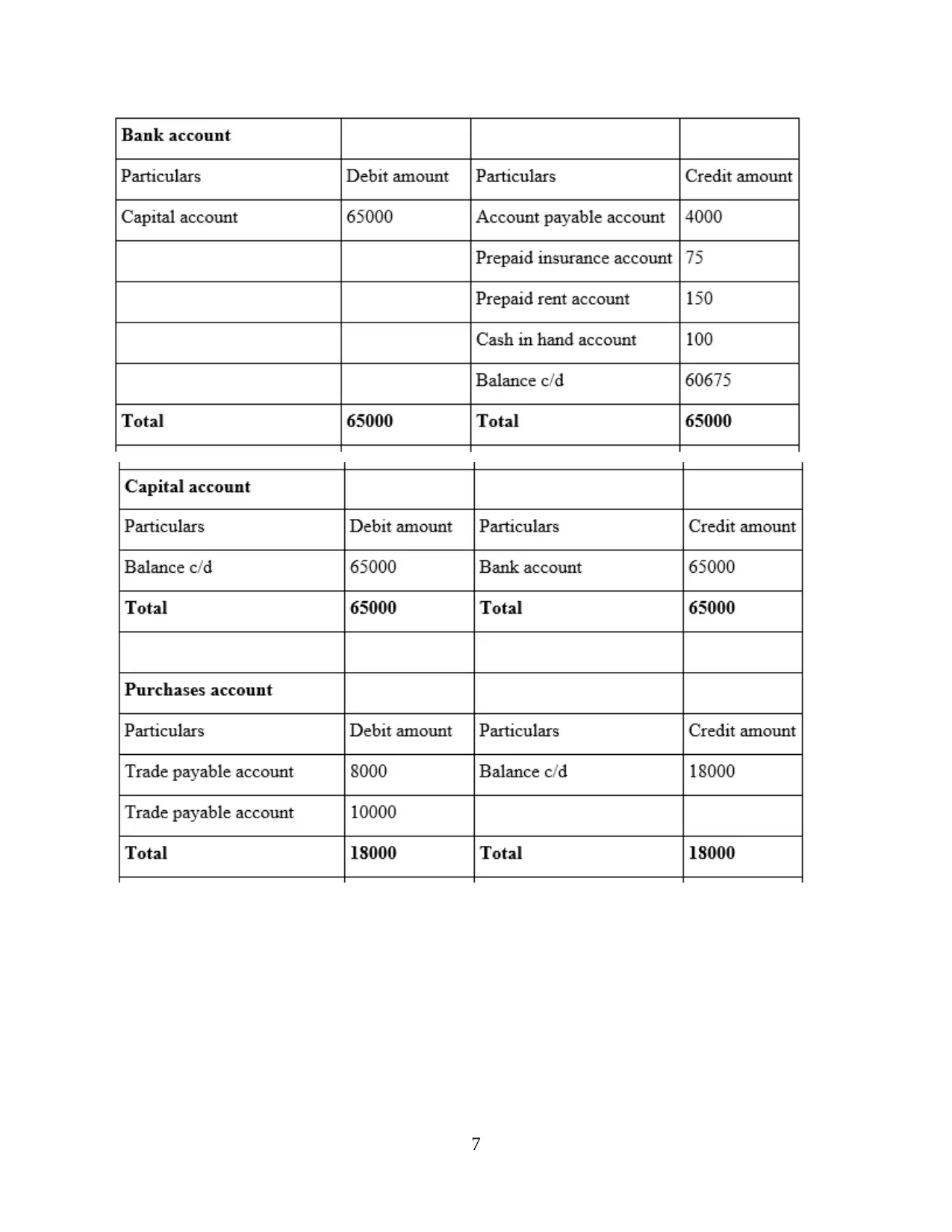

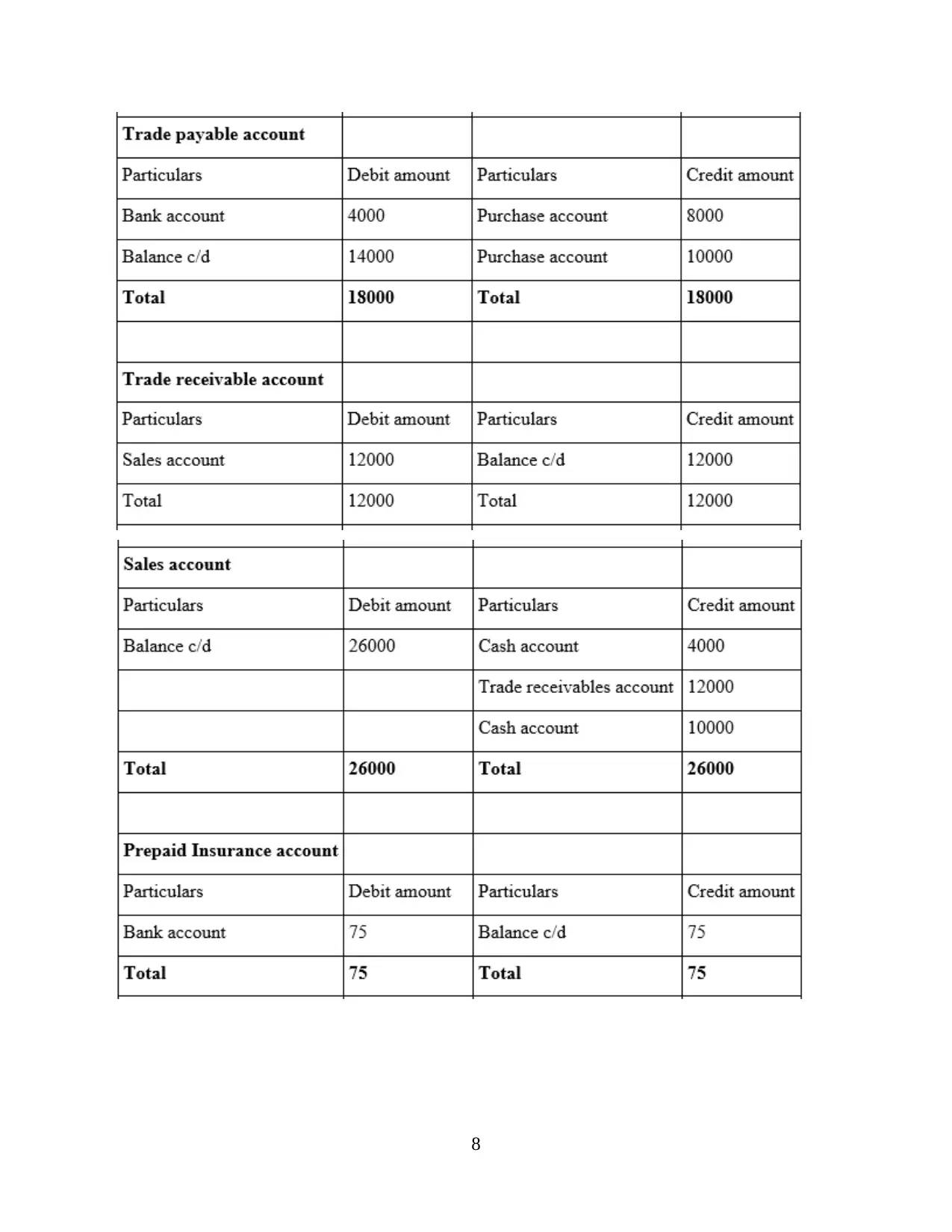

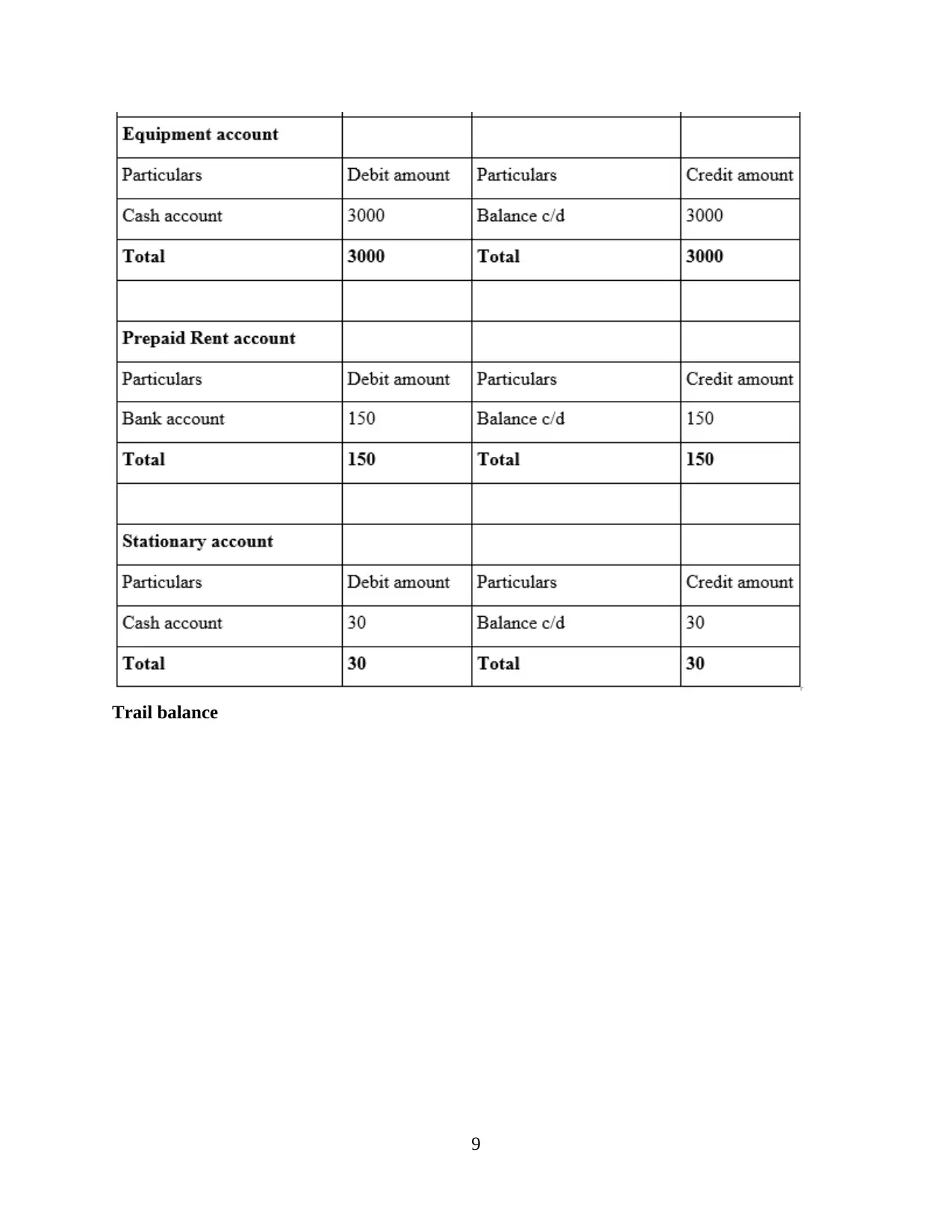

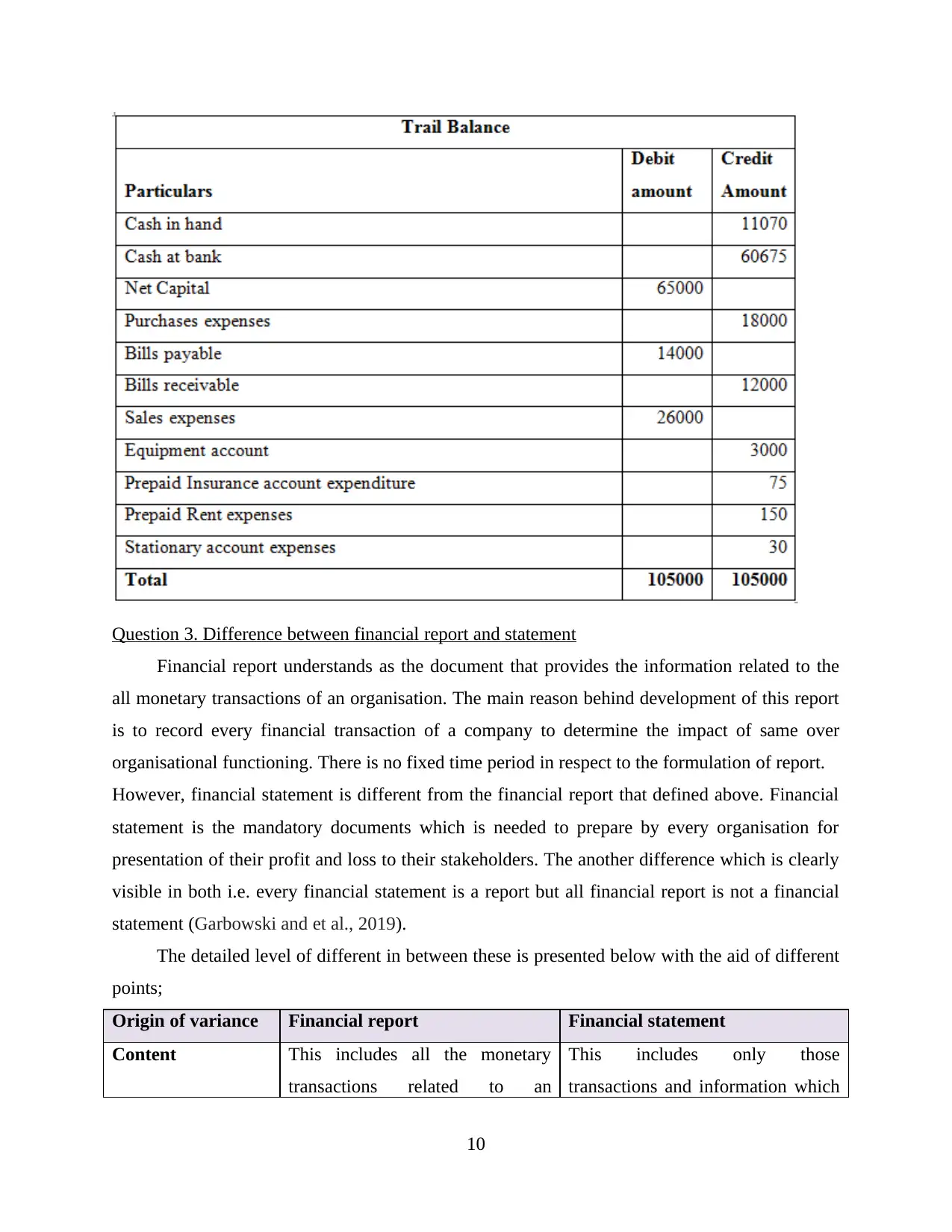

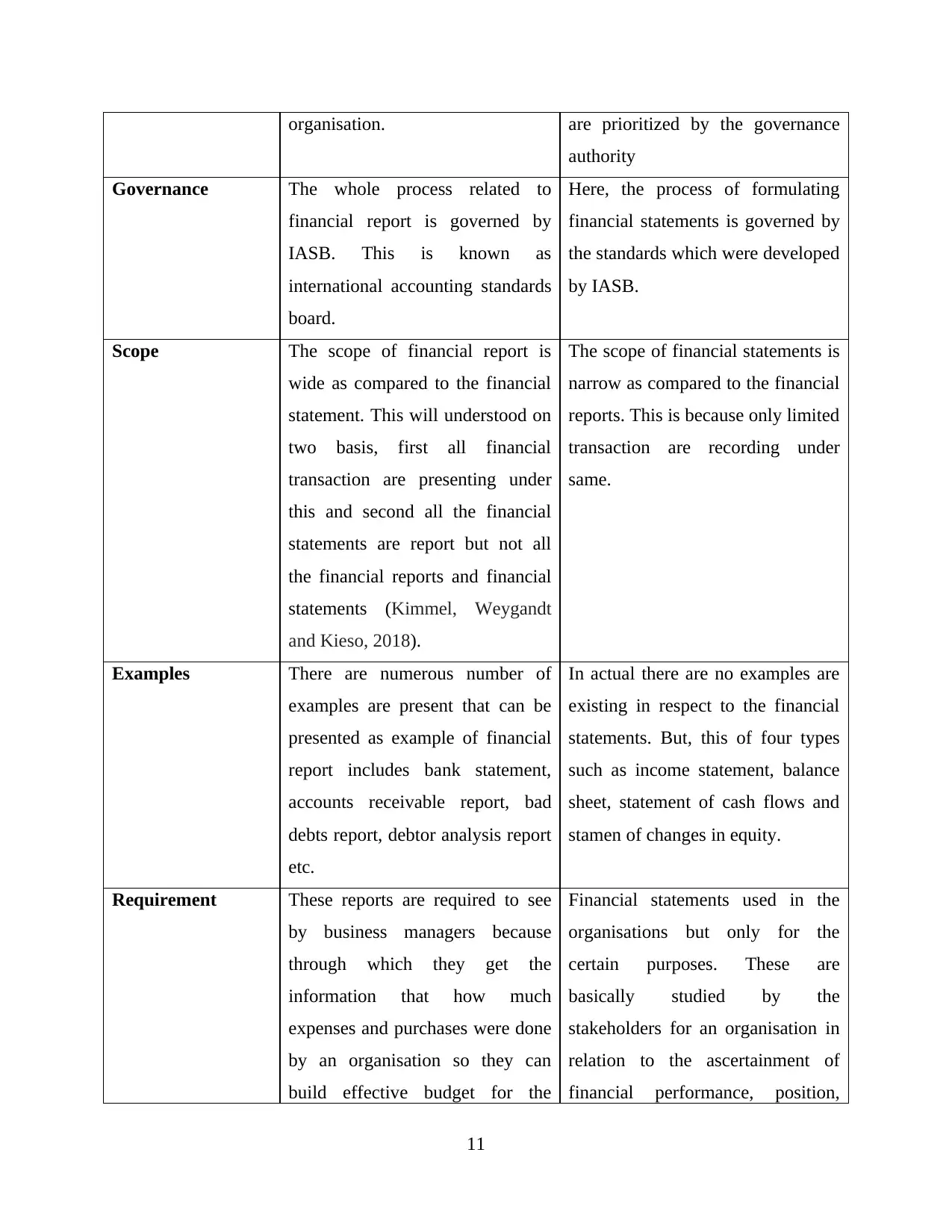

This report provides a comprehensive overview of financial accounting principles and practices. It begins by exploring different types of business transactions, differentiating between internal and external transactions, and explaining single-entry and double-entry bookkeeping methods. The report then delves into the importance of trial balances and their role in ensuring the arithmetical accuracy of accounts. It further examines journal entries, ledger accounts, and the preparation of trial balances. A significant portion of the report contrasts financial reports and financial statements, highlighting their differences in content, scope, and users. The report also outlines the fundamental principles of accounting, including monetary unit assumption, going concern, and matching principles. Finally, the report includes profit and loss accounts and balance sheets to demonstrate the practical application of these concepts. The second part of the report focuses on bank reconciliation, control accounts, and suspense accounts, providing a detailed understanding of these crucial accounting processes.

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.