Recording Business Transactions and Financial Statements Analysis

VerifiedAdded on 2023/01/03

|11

|2092

|92

Homework Assignment

AI Summary

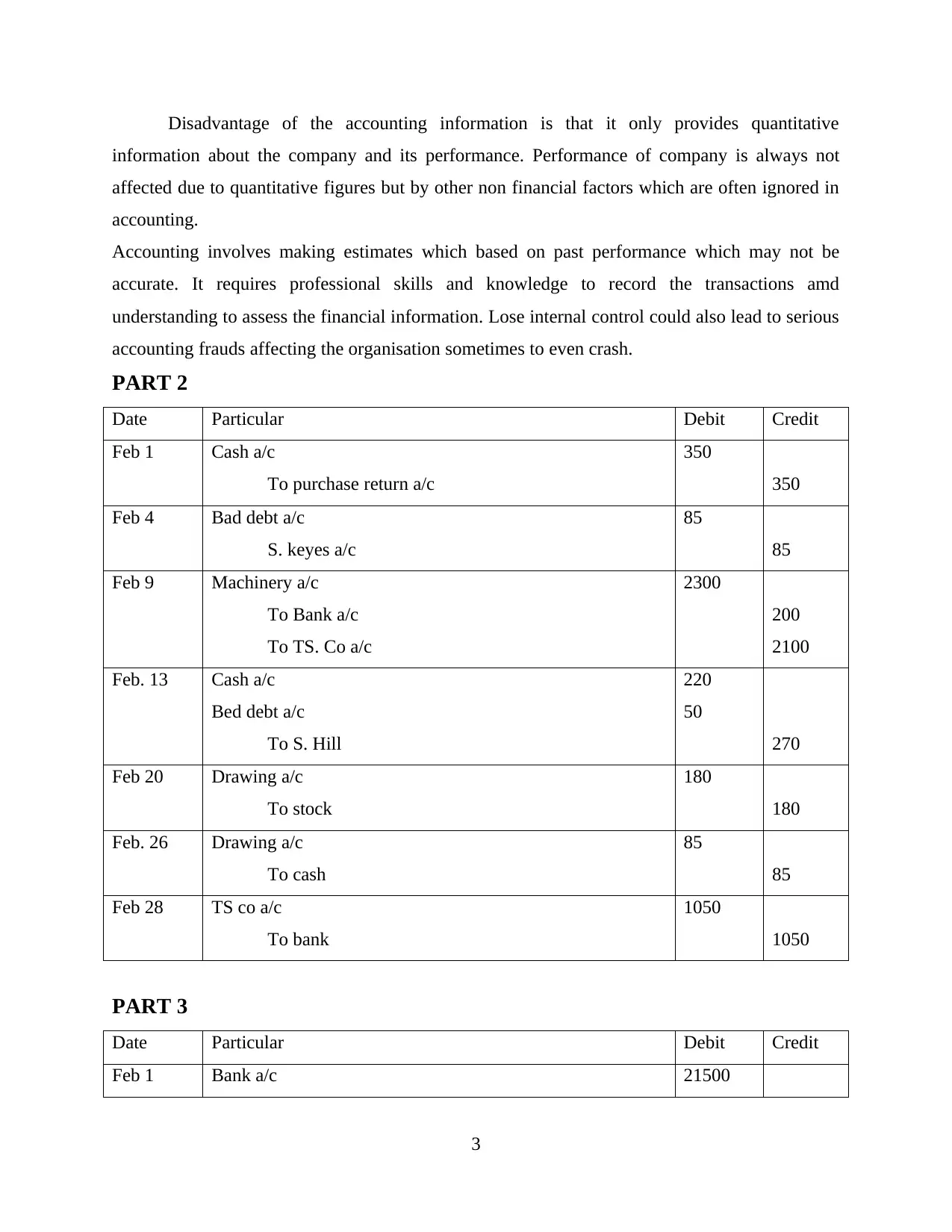

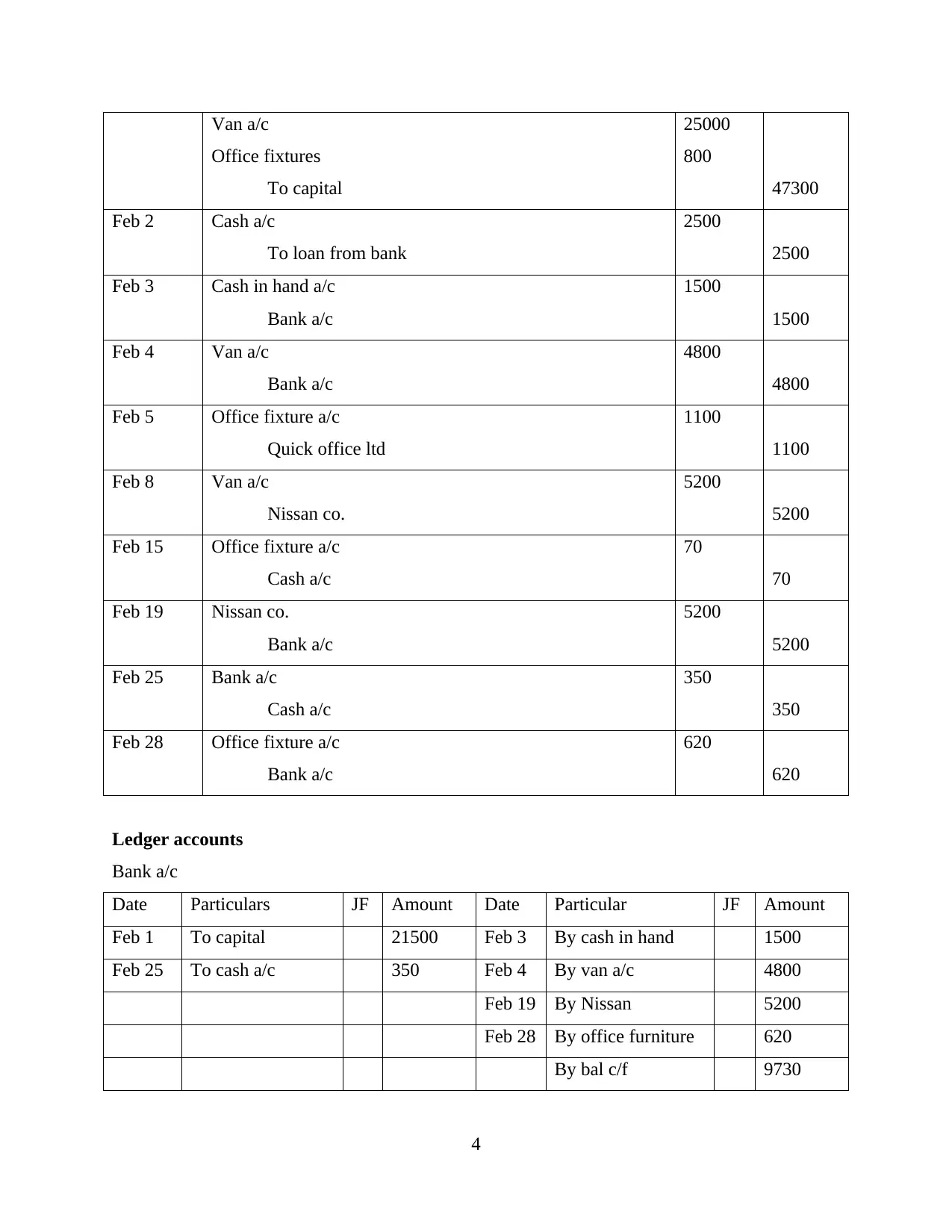

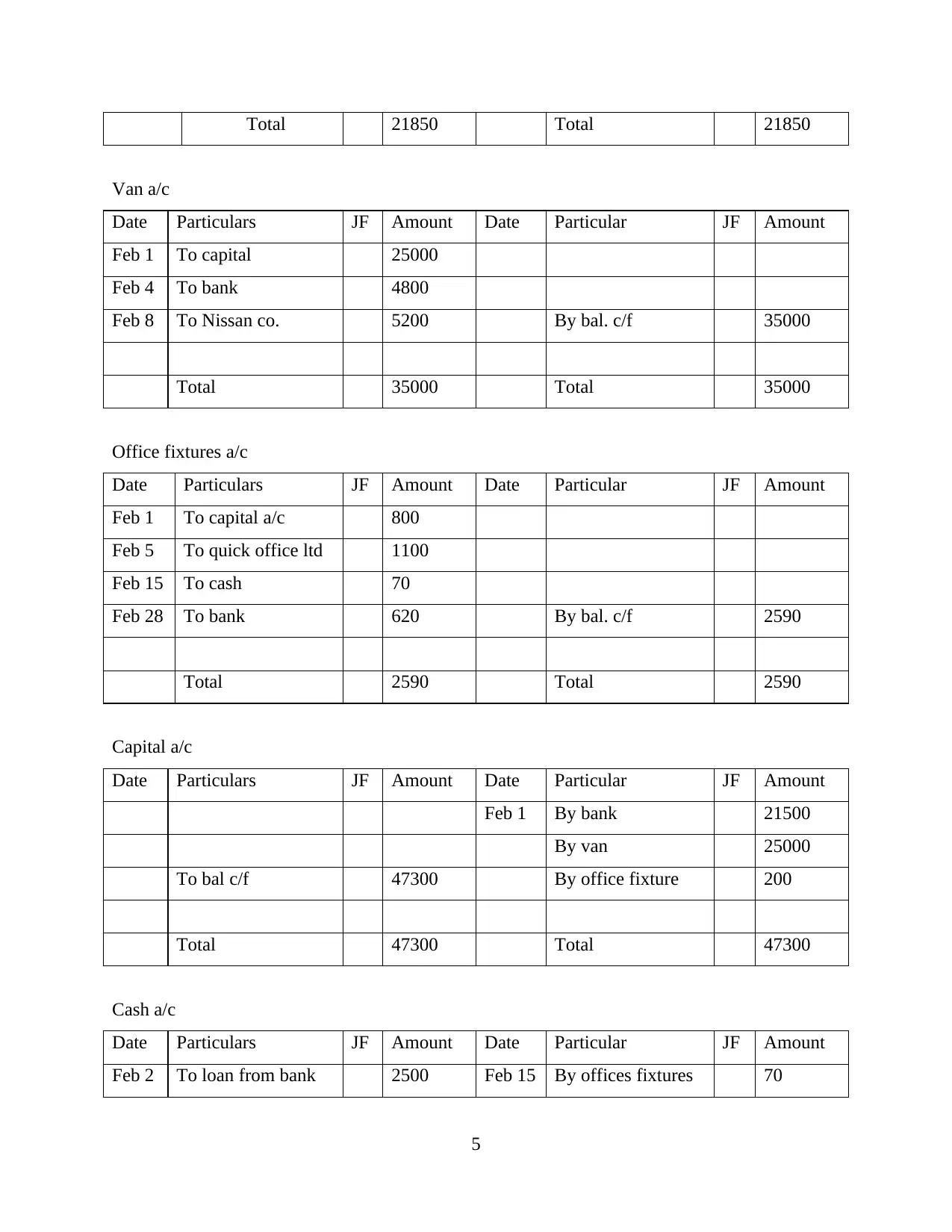

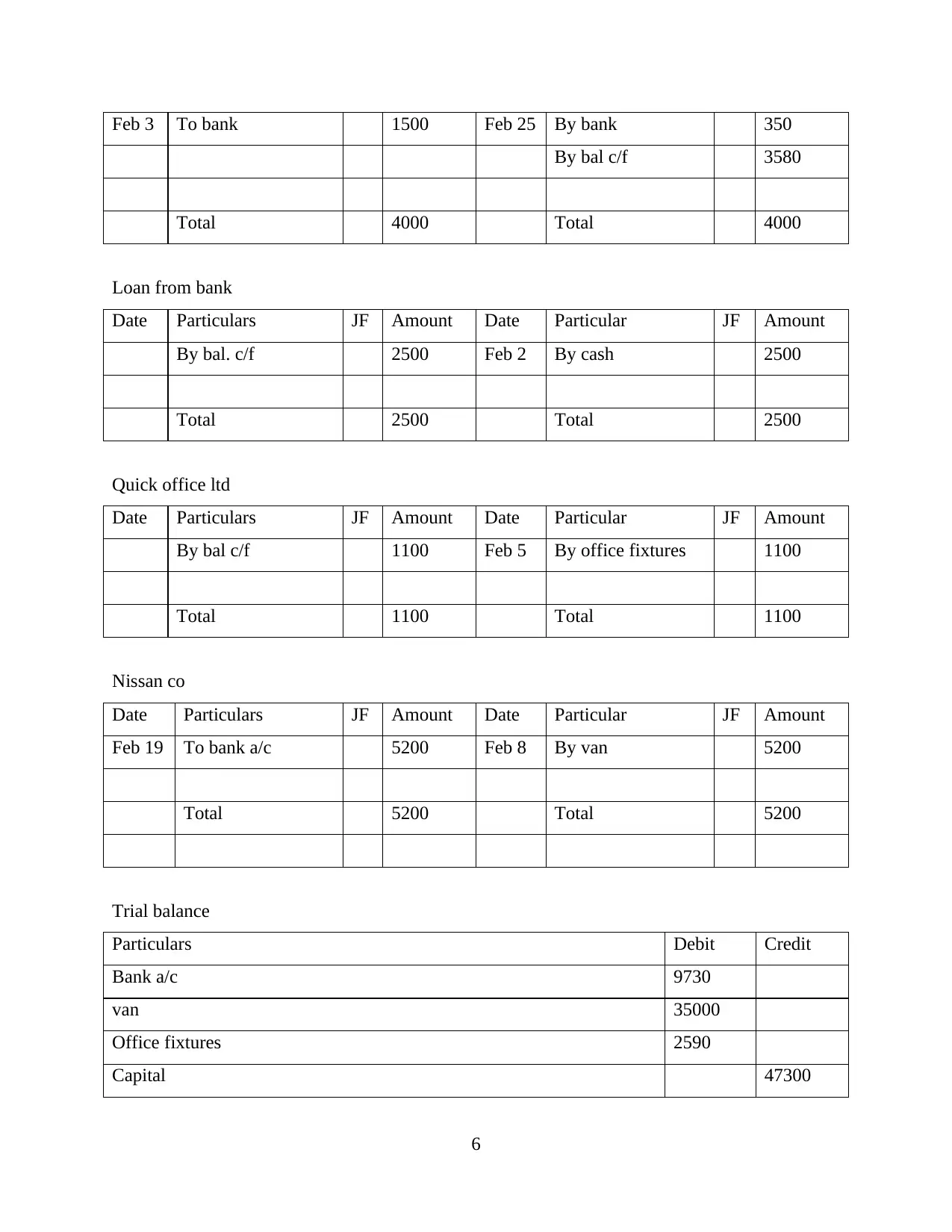

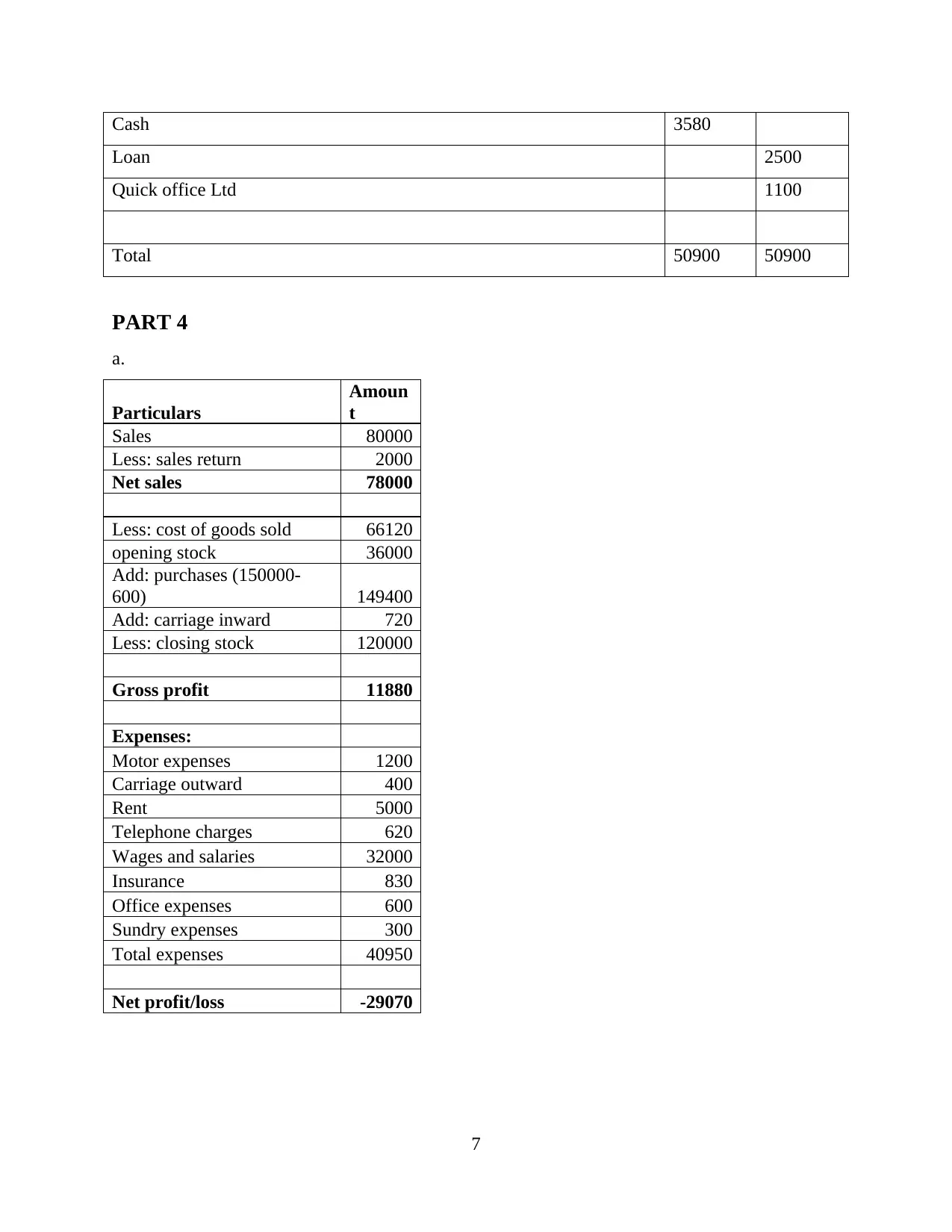

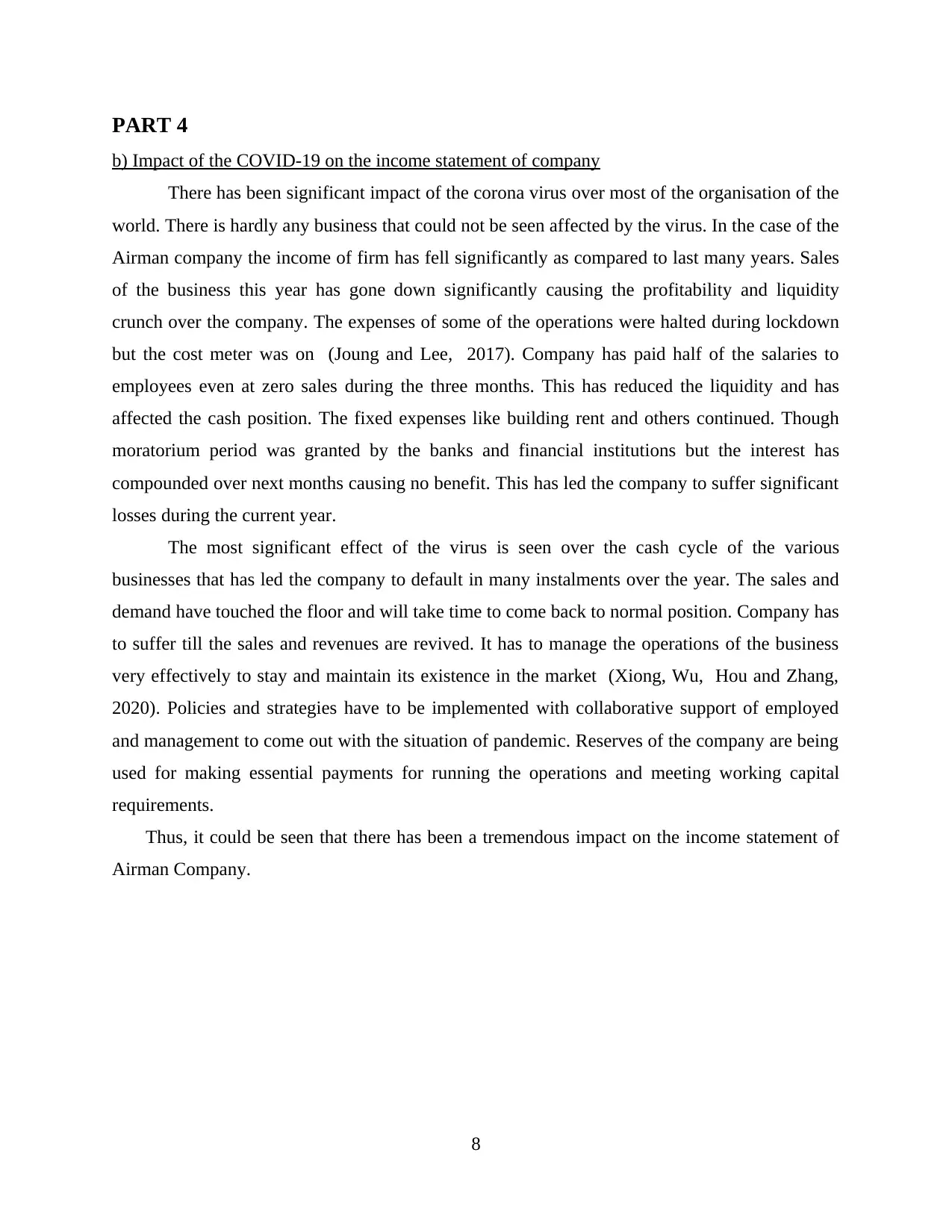

This assignment provides a comprehensive overview of financial accounting, emphasizing the recording, analysis, and reporting of business transactions. It includes an introduction to financial accounting, highlighting the importance of financial statements like the balance sheet, income statement, and cash flow statement. The assignment explores the role of decision-makers and their need for accounting information, identifying various users such as management, shareholders, creditors, and government bodies. It also discusses the advantages and disadvantages of accounting, emphasizing its role in recording transactions, comparing results, and complying with statutory requirements. The assignment includes numerical examples of accounting transactions, ledger accounts, and a trial balance. Furthermore, it presents an income statement and analyzes the impact of COVID-19 on a company's financial performance, specifically addressing the decrease in sales, liquidity issues, and the influence of fixed expenses and government policies. The document concludes with a list of references used for research and analysis.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.