Financial Accounting Assignment: Scenario Analysis and Statements

VerifiedAdded on 2023/01/10

|20

|4181

|83

Homework Assignment

AI Summary

This financial accounting assignment provides a comprehensive overview of key accounting principles and practices. It begins with an introduction to financial accounting and its role in recording, summarizing, and reporting business transactions. The assignment then delves into two scenarios, each posing several questions that require the application of accounting concepts. These include differentiating between various types of business transactions (cash, credit, internal, and external), understanding the double-entry system, preparing journal entries, creating ledger accounts, and constructing a trial balance. The assignment also explores the differences between financial statements and financial reports, the fundamental principles of accounting, and the preparation of a profit and loss statement and balance sheet. The solution includes detailed explanations, examples, and calculations to facilitate a thorough understanding of the concepts covered.

FINANCIAL

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

SCENARIO 1...................................................................................................................................1

Question 1 ...................................................................................................................................1

Question 2....................................................................................................................................3

Question 3....................................................................................................................................7

Question 4....................................................................................................................................8

Question 5....................................................................................................................................9

SCENARIO 2.................................................................................................................................11

Question 1..................................................................................................................................11

Question 2..................................................................................................................................12

Question 3..................................................................................................................................12

Question 4..................................................................................................................................13

Question 5..................................................................................................................................15

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

INTRODUCTION...........................................................................................................................1

SCENARIO 1...................................................................................................................................1

Question 1 ...................................................................................................................................1

Question 2....................................................................................................................................3

Question 3....................................................................................................................................7

Question 4....................................................................................................................................8

Question 5....................................................................................................................................9

SCENARIO 2.................................................................................................................................11

Question 1..................................................................................................................................11

Question 2..................................................................................................................................12

Question 3..................................................................................................................................12

Question 4..................................................................................................................................13

Question 5..................................................................................................................................15

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

INTRODUCTION

Financial accounting refers to the specialised accounting branch which involves the

process to record, summarise and report myriad of the transactions that result from the business

operations in a specific time period. The transactions of the business are summarised for

preparing the financial statements which records the operating performance of the company over

specific period. Financial accounting uses various established principles of accounting. Selection

of the accounting principles for use in course of the financial accounting is dependent on the

nature of business. The accounting principles are framed for providing consistent information to

the creditors, investors, tax authorities and regulators. Managerial accounting is in contrast with

the financial accounting as management accounting is used for internal processes and does not

follow any standards and set procedure. Managerial reports are prepared for the internal

processes. Present report is based over the concepts of financial accounting and managerial

accounting. Report will be providing an understanding of double entry system of book keeping.

It will include journals, ledger accounts, trial balance, income statement, balance sheet and bank

reconciliation statement.

SCENARIO 1

Question 1

Different Types of Business transactions

Business transaction refers to the event which is measurable in monetary terms and is

having an impact over financial position of business. There are two types of business

transactions

1. Credit and Cash Transactions

2. External and Internal transactions

Cash & Credit Transactions

Cash transaction is the one where cash is received or paid immediately at time when the

transactions occur. They are not restricted to currency coins and notes to make or receive

payments but extends to all the transactions made using credit or debit cards.

Credit Transaction do not change hands immediately when the transaction is occurring.

Cash in such transactions is paid or received at the future date (Sangster, 2016). Credit

transactions are generally related to the purchase and sales of goods and materials.

Internal & External transactions

1

Financial accounting refers to the specialised accounting branch which involves the

process to record, summarise and report myriad of the transactions that result from the business

operations in a specific time period. The transactions of the business are summarised for

preparing the financial statements which records the operating performance of the company over

specific period. Financial accounting uses various established principles of accounting. Selection

of the accounting principles for use in course of the financial accounting is dependent on the

nature of business. The accounting principles are framed for providing consistent information to

the creditors, investors, tax authorities and regulators. Managerial accounting is in contrast with

the financial accounting as management accounting is used for internal processes and does not

follow any standards and set procedure. Managerial reports are prepared for the internal

processes. Present report is based over the concepts of financial accounting and managerial

accounting. Report will be providing an understanding of double entry system of book keeping.

It will include journals, ledger accounts, trial balance, income statement, balance sheet and bank

reconciliation statement.

SCENARIO 1

Question 1

Different Types of Business transactions

Business transaction refers to the event which is measurable in monetary terms and is

having an impact over financial position of business. There are two types of business

transactions

1. Credit and Cash Transactions

2. External and Internal transactions

Cash & Credit Transactions

Cash transaction is the one where cash is received or paid immediately at time when the

transactions occur. They are not restricted to currency coins and notes to make or receive

payments but extends to all the transactions made using credit or debit cards.

Credit Transaction do not change hands immediately when the transaction is occurring.

Cash in such transactions is paid or received at the future date (Sangster, 2016). Credit

transactions are generally related to the purchase and sales of goods and materials.

Internal & External transactions

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Internal transactions are the transactions where external parties are not involved.

Transaction does not involve exchange of value between the parties but transaction for the event

is measurable in terms of money and has impact over the financial positions such as depreciation.

External transaction refers to transaction where value is exchanged with the external

parties. All transactions which are not internal are the external transactions. The external

transactions are performed by the business on regular basis. Majority of the transactions are

external in the business.

Single entry and double entry book keeping

Single entry book-keeping refers to the simple & straightforward method of the book

keeping where every transaction is recorded in as single entry in the journal. The book keeping

method is cash based which records in the inflow and outflow of the cash in journal.

Double entry system refers to the method in which every transaction of the business is

recorded and entry is affecting at least two accounts one as debit and other as credit. In double

entry book keeping amount recorded in debit must equal to amount recorded as credit.

Trial balance and its importance.

Transaction recoded in double entry book keeping has credit for each debit. When the

accounts are debited they should be credited with the equal amount. It is therefore evident that

total of the debit balance will equal to total of credit balance. Trial balance is the statement

prepared with one debit side and one credit side. It is the list of balances standing over ledger

accounts & cash book of the concern.

Trial balance is prepared for ensuring that the total of debit side is equal to the total of

credit side. Discrepancy in total signals that there is presence of the mathematical error in

accounting transactions or their posting to the ledger accounts. It is used for compiling the

financial statements that reveals the financial performance and position of the company. The two

statements prepared from the trial balance are income statement and balance sheet (Maynard,

2017). This is used by the management for making sound business decisions. Seeing the trial

balance they could get the idea over the income and expenses of the enterprise for the period.

Auditors use the trial balance for examining the physical assets for determining the material

discrepancies.

2

Transaction does not involve exchange of value between the parties but transaction for the event

is measurable in terms of money and has impact over the financial positions such as depreciation.

External transaction refers to transaction where value is exchanged with the external

parties. All transactions which are not internal are the external transactions. The external

transactions are performed by the business on regular basis. Majority of the transactions are

external in the business.

Single entry and double entry book keeping

Single entry book-keeping refers to the simple & straightforward method of the book

keeping where every transaction is recorded in as single entry in the journal. The book keeping

method is cash based which records in the inflow and outflow of the cash in journal.

Double entry system refers to the method in which every transaction of the business is

recorded and entry is affecting at least two accounts one as debit and other as credit. In double

entry book keeping amount recorded in debit must equal to amount recorded as credit.

Trial balance and its importance.

Transaction recoded in double entry book keeping has credit for each debit. When the

accounts are debited they should be credited with the equal amount. It is therefore evident that

total of the debit balance will equal to total of credit balance. Trial balance is the statement

prepared with one debit side and one credit side. It is the list of balances standing over ledger

accounts & cash book of the concern.

Trial balance is prepared for ensuring that the total of debit side is equal to the total of

credit side. Discrepancy in total signals that there is presence of the mathematical error in

accounting transactions or their posting to the ledger accounts. It is used for compiling the

financial statements that reveals the financial performance and position of the company. The two

statements prepared from the trial balance are income statement and balance sheet (Maynard,

2017). This is used by the management for making sound business decisions. Seeing the trial

balance they could get the idea over the income and expenses of the enterprise for the period.

Auditors use the trial balance for examining the physical assets for determining the material

discrepancies.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

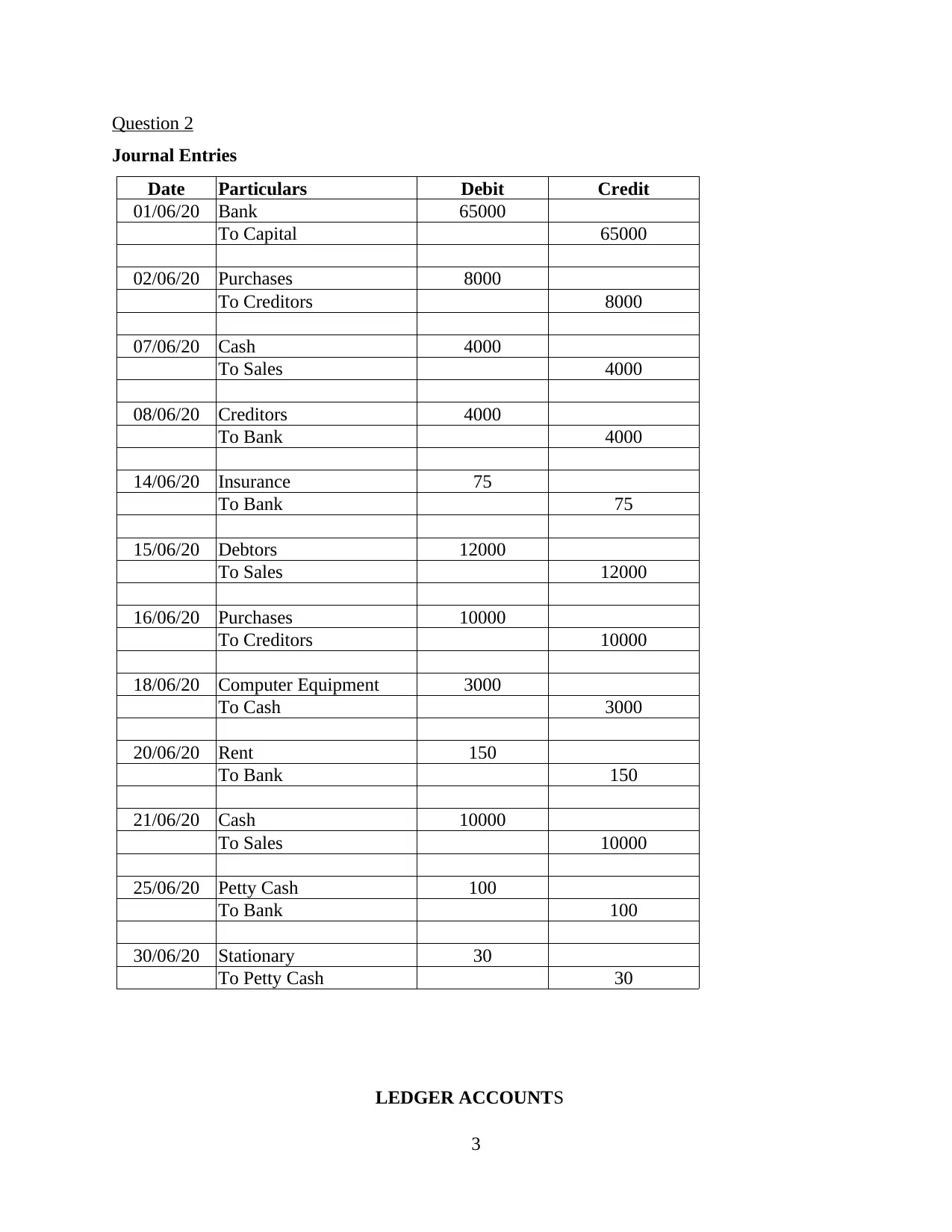

Question 2

Journal Entries

Date Particulars Debit Credit

01/06/20 Bank 65000

To Capital 65000

02/06/20 Purchases 8000

To Creditors 8000

07/06/20 Cash 4000

To Sales 4000

08/06/20 Creditors 4000

To Bank 4000

14/06/20 Insurance 75

To Bank 75

15/06/20 Debtors 12000

To Sales 12000

16/06/20 Purchases 10000

To Creditors 10000

18/06/20 Computer Equipment 3000

To Cash 3000

20/06/20 Rent 150

To Bank 150

21/06/20 Cash 10000

To Sales 10000

25/06/20 Petty Cash 100

To Bank 100

30/06/20 Stationary 30

To Petty Cash 30

LEDGER ACCOUNTS

3

Journal Entries

Date Particulars Debit Credit

01/06/20 Bank 65000

To Capital 65000

02/06/20 Purchases 8000

To Creditors 8000

07/06/20 Cash 4000

To Sales 4000

08/06/20 Creditors 4000

To Bank 4000

14/06/20 Insurance 75

To Bank 75

15/06/20 Debtors 12000

To Sales 12000

16/06/20 Purchases 10000

To Creditors 10000

18/06/20 Computer Equipment 3000

To Cash 3000

20/06/20 Rent 150

To Bank 150

21/06/20 Cash 10000

To Sales 10000

25/06/20 Petty Cash 100

To Bank 100

30/06/20 Stationary 30

To Petty Cash 30

LEDGER ACCOUNTS

3

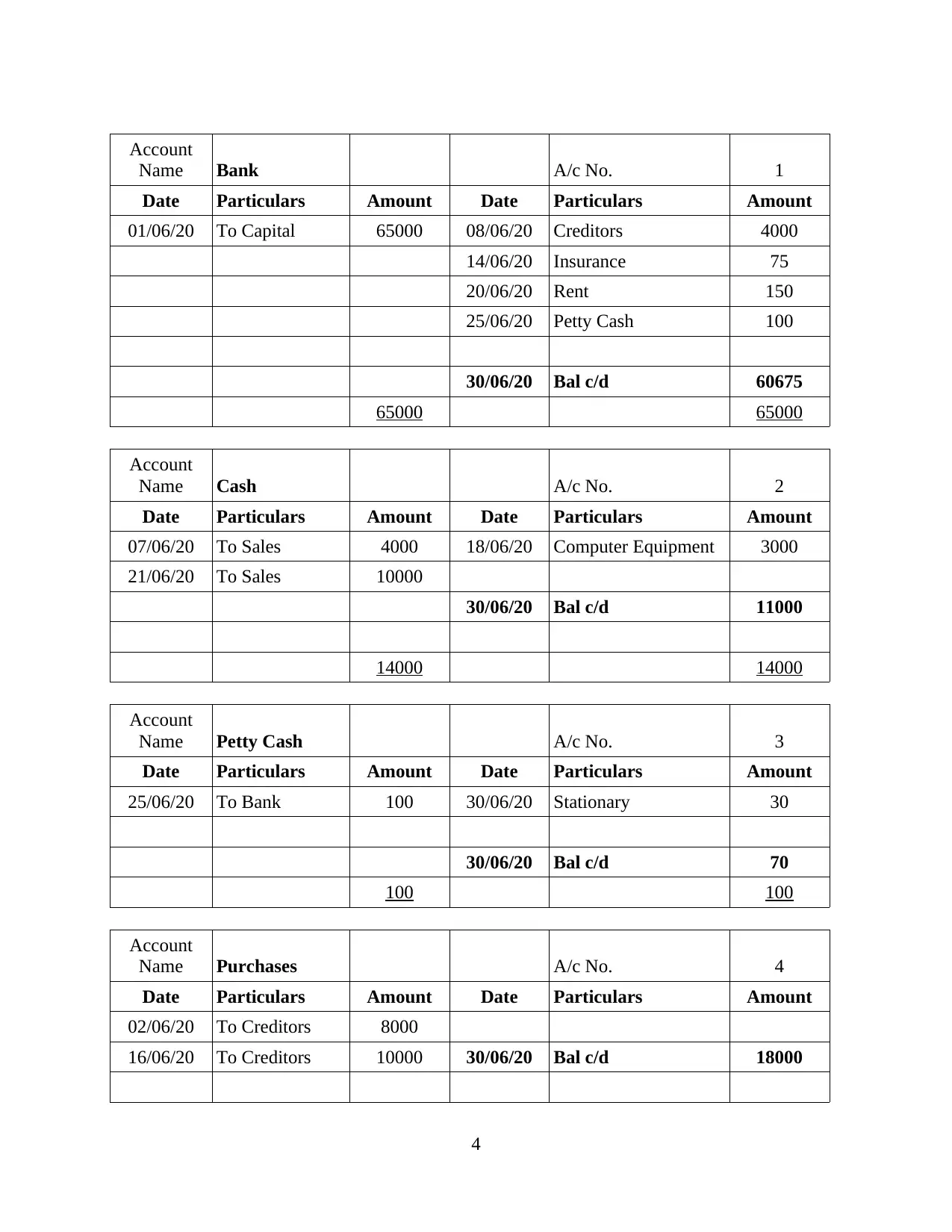

Account

Name Bank A/c No. 1

Date Particulars Amount Date Particulars Amount

01/06/20 To Capital 65000 08/06/20 Creditors 4000

14/06/20 Insurance 75

20/06/20 Rent 150

25/06/20 Petty Cash 100

30/06/20 Bal c/d 60675

65000 65000

Account

Name Cash A/c No. 2

Date Particulars Amount Date Particulars Amount

07/06/20 To Sales 4000 18/06/20 Computer Equipment 3000

21/06/20 To Sales 10000

30/06/20 Bal c/d 11000

14000 14000

Account

Name Petty Cash A/c No. 3

Date Particulars Amount Date Particulars Amount

25/06/20 To Bank 100 30/06/20 Stationary 30

30/06/20 Bal c/d 70

100 100

Account

Name Purchases A/c No. 4

Date Particulars Amount Date Particulars Amount

02/06/20 To Creditors 8000

16/06/20 To Creditors 10000 30/06/20 Bal c/d 18000

4

Name Bank A/c No. 1

Date Particulars Amount Date Particulars Amount

01/06/20 To Capital 65000 08/06/20 Creditors 4000

14/06/20 Insurance 75

20/06/20 Rent 150

25/06/20 Petty Cash 100

30/06/20 Bal c/d 60675

65000 65000

Account

Name Cash A/c No. 2

Date Particulars Amount Date Particulars Amount

07/06/20 To Sales 4000 18/06/20 Computer Equipment 3000

21/06/20 To Sales 10000

30/06/20 Bal c/d 11000

14000 14000

Account

Name Petty Cash A/c No. 3

Date Particulars Amount Date Particulars Amount

25/06/20 To Bank 100 30/06/20 Stationary 30

30/06/20 Bal c/d 70

100 100

Account

Name Purchases A/c No. 4

Date Particulars Amount Date Particulars Amount

02/06/20 To Creditors 8000

16/06/20 To Creditors 10000 30/06/20 Bal c/d 18000

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

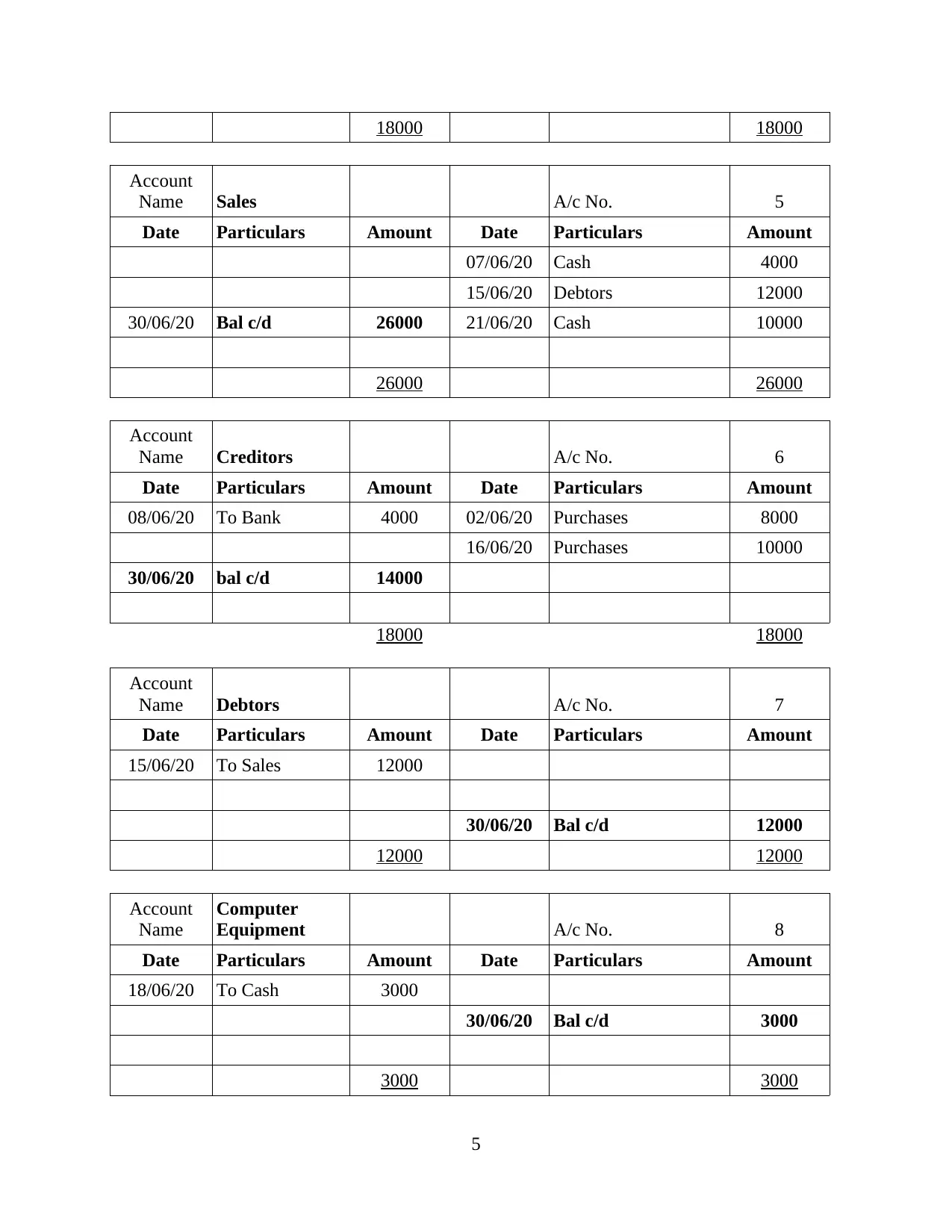

18000 18000

Account

Name Sales A/c No. 5

Date Particulars Amount Date Particulars Amount

07/06/20 Cash 4000

15/06/20 Debtors 12000

30/06/20 Bal c/d 26000 21/06/20 Cash 10000

26000 26000

Account

Name Creditors A/c No. 6

Date Particulars Amount Date Particulars Amount

08/06/20 To Bank 4000 02/06/20 Purchases 8000

16/06/20 Purchases 10000

30/06/20 bal c/d 14000

18000 18000

Account

Name Debtors A/c No. 7

Date Particulars Amount Date Particulars Amount

15/06/20 To Sales 12000

30/06/20 Bal c/d 12000

12000 12000

Account

Name

Computer

Equipment A/c No. 8

Date Particulars Amount Date Particulars Amount

18/06/20 To Cash 3000

30/06/20 Bal c/d 3000

3000 3000

5

Account

Name Sales A/c No. 5

Date Particulars Amount Date Particulars Amount

07/06/20 Cash 4000

15/06/20 Debtors 12000

30/06/20 Bal c/d 26000 21/06/20 Cash 10000

26000 26000

Account

Name Creditors A/c No. 6

Date Particulars Amount Date Particulars Amount

08/06/20 To Bank 4000 02/06/20 Purchases 8000

16/06/20 Purchases 10000

30/06/20 bal c/d 14000

18000 18000

Account

Name Debtors A/c No. 7

Date Particulars Amount Date Particulars Amount

15/06/20 To Sales 12000

30/06/20 Bal c/d 12000

12000 12000

Account

Name

Computer

Equipment A/c No. 8

Date Particulars Amount Date Particulars Amount

18/06/20 To Cash 3000

30/06/20 Bal c/d 3000

3000 3000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

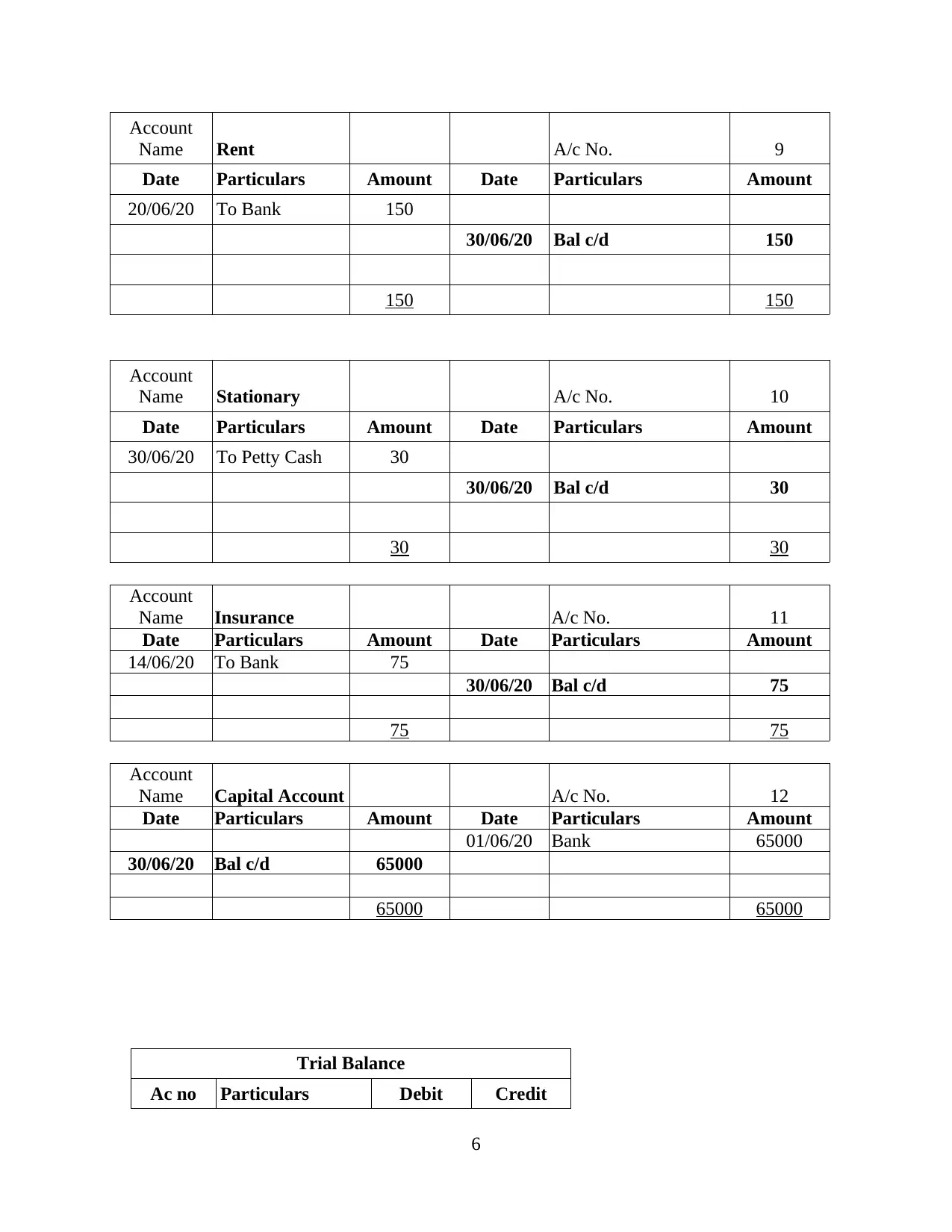

Account

Name Rent A/c No. 9

Date Particulars Amount Date Particulars Amount

20/06/20 To Bank 150

30/06/20 Bal c/d 150

150 150

Account

Name Stationary A/c No. 10

Date Particulars Amount Date Particulars Amount

30/06/20 To Petty Cash 30

30/06/20 Bal c/d 30

30 30

Account

Name Insurance A/c No. 11

Date Particulars Amount Date Particulars Amount

14/06/20 To Bank 75

30/06/20 Bal c/d 75

75 75

Account

Name Capital Account A/c No. 12

Date Particulars Amount Date Particulars Amount

01/06/20 Bank 65000

30/06/20 Bal c/d 65000

65000 65000

Trial Balance

Ac no Particulars Debit Credit

6

Name Rent A/c No. 9

Date Particulars Amount Date Particulars Amount

20/06/20 To Bank 150

30/06/20 Bal c/d 150

150 150

Account

Name Stationary A/c No. 10

Date Particulars Amount Date Particulars Amount

30/06/20 To Petty Cash 30

30/06/20 Bal c/d 30

30 30

Account

Name Insurance A/c No. 11

Date Particulars Amount Date Particulars Amount

14/06/20 To Bank 75

30/06/20 Bal c/d 75

75 75

Account

Name Capital Account A/c No. 12

Date Particulars Amount Date Particulars Amount

01/06/20 Bank 65000

30/06/20 Bal c/d 65000

65000 65000

Trial Balance

Ac no Particulars Debit Credit

6

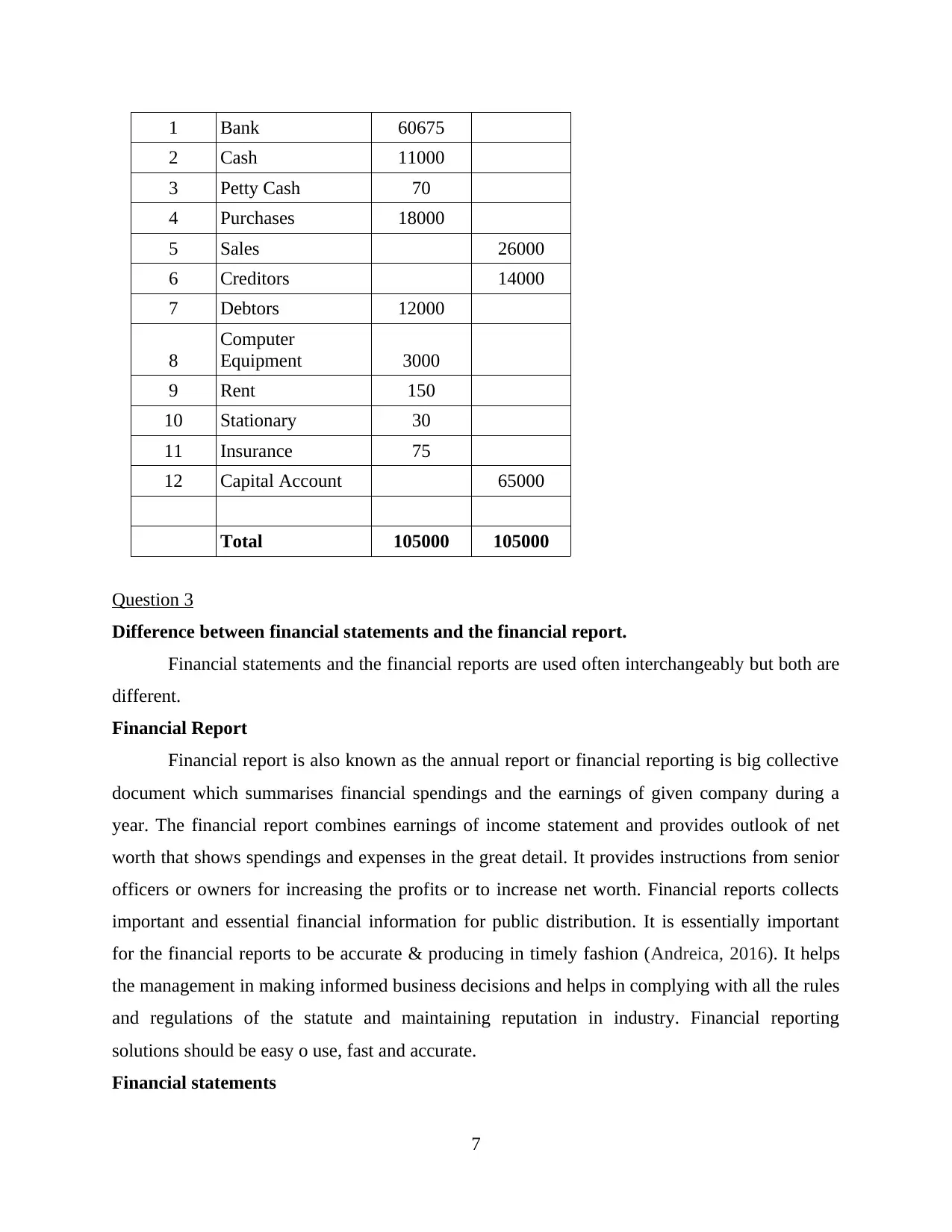

1 Bank 60675

2 Cash 11000

3 Petty Cash 70

4 Purchases 18000

5 Sales 26000

6 Creditors 14000

7 Debtors 12000

8

Computer

Equipment 3000

9 Rent 150

10 Stationary 30

11 Insurance 75

12 Capital Account 65000

Total 105000 105000

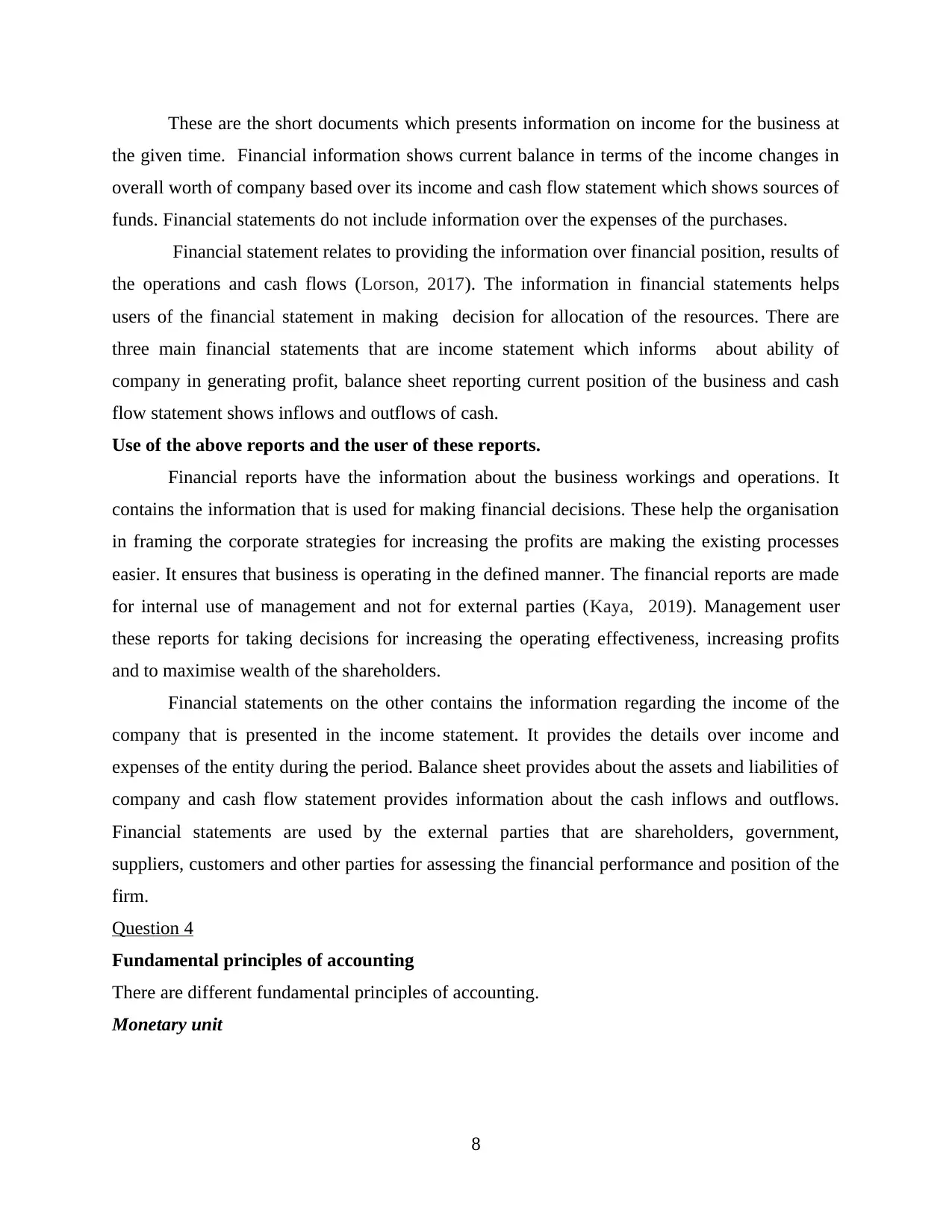

Question 3

Difference between financial statements and the financial report.

Financial statements and the financial reports are used often interchangeably but both are

different.

Financial Report

Financial report is also known as the annual report or financial reporting is big collective

document which summarises financial spendings and the earnings of given company during a

year. The financial report combines earnings of income statement and provides outlook of net

worth that shows spendings and expenses in the great detail. It provides instructions from senior

officers or owners for increasing the profits or to increase net worth. Financial reports collects

important and essential financial information for public distribution. It is essentially important

for the financial reports to be accurate & producing in timely fashion (Andreica, 2016). It helps

the management in making informed business decisions and helps in complying with all the rules

and regulations of the statute and maintaining reputation in industry. Financial reporting

solutions should be easy o use, fast and accurate.

Financial statements

7

2 Cash 11000

3 Petty Cash 70

4 Purchases 18000

5 Sales 26000

6 Creditors 14000

7 Debtors 12000

8

Computer

Equipment 3000

9 Rent 150

10 Stationary 30

11 Insurance 75

12 Capital Account 65000

Total 105000 105000

Question 3

Difference between financial statements and the financial report.

Financial statements and the financial reports are used often interchangeably but both are

different.

Financial Report

Financial report is also known as the annual report or financial reporting is big collective

document which summarises financial spendings and the earnings of given company during a

year. The financial report combines earnings of income statement and provides outlook of net

worth that shows spendings and expenses in the great detail. It provides instructions from senior

officers or owners for increasing the profits or to increase net worth. Financial reports collects

important and essential financial information for public distribution. It is essentially important

for the financial reports to be accurate & producing in timely fashion (Andreica, 2016). It helps

the management in making informed business decisions and helps in complying with all the rules

and regulations of the statute and maintaining reputation in industry. Financial reporting

solutions should be easy o use, fast and accurate.

Financial statements

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

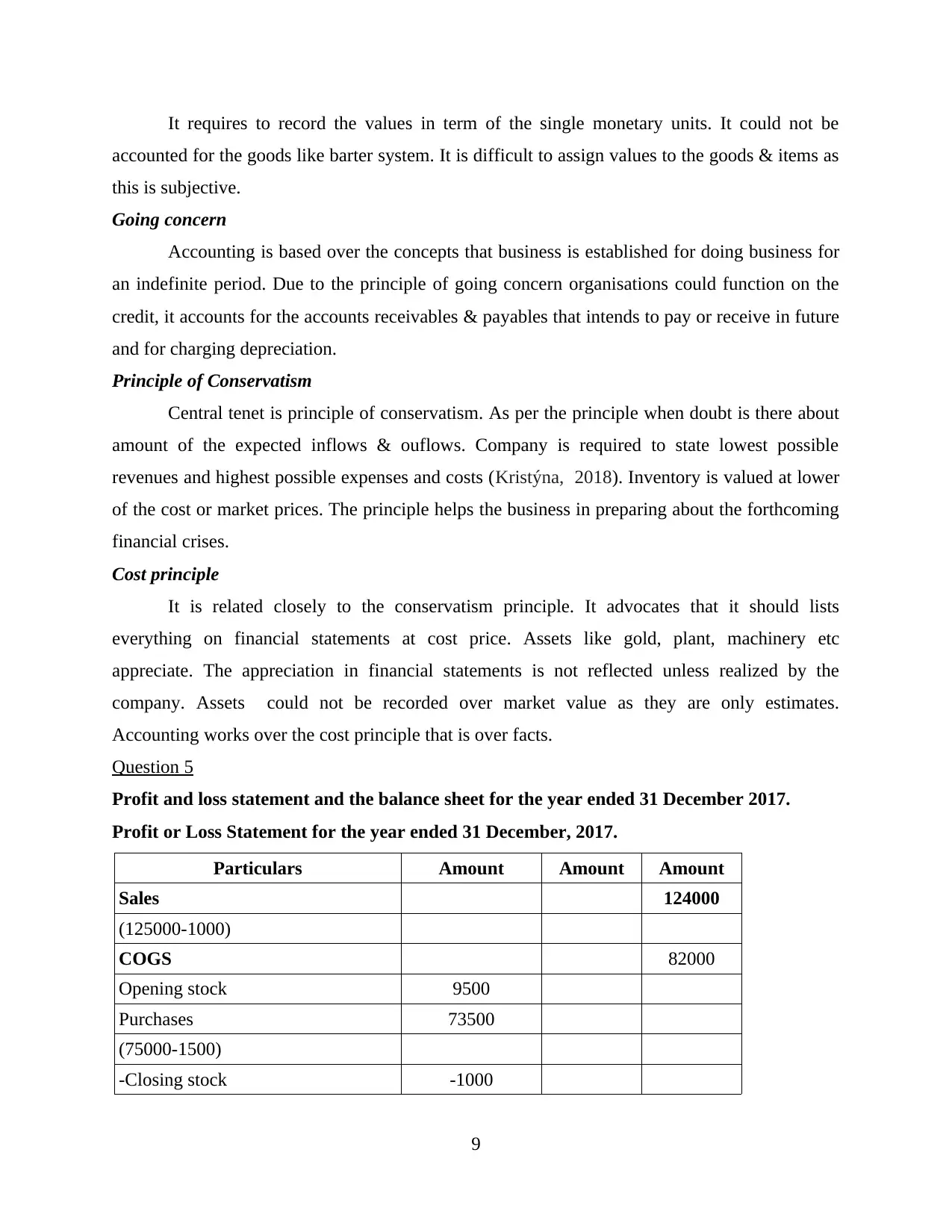

These are the short documents which presents information on income for the business at

the given time. Financial information shows current balance in terms of the income changes in

overall worth of company based over its income and cash flow statement which shows sources of

funds. Financial statements do not include information over the expenses of the purchases.

Financial statement relates to providing the information over financial position, results of

the operations and cash flows (Lorson, 2017). The information in financial statements helps

users of the financial statement in making decision for allocation of the resources. There are

three main financial statements that are income statement which informs about ability of

company in generating profit, balance sheet reporting current position of the business and cash

flow statement shows inflows and outflows of cash.

Use of the above reports and the user of these reports.

Financial reports have the information about the business workings and operations. It

contains the information that is used for making financial decisions. These help the organisation

in framing the corporate strategies for increasing the profits are making the existing processes

easier. It ensures that business is operating in the defined manner. The financial reports are made

for internal use of management and not for external parties (Kaya, 2019). Management user

these reports for taking decisions for increasing the operating effectiveness, increasing profits

and to maximise wealth of the shareholders.

Financial statements on the other contains the information regarding the income of the

company that is presented in the income statement. It provides the details over income and

expenses of the entity during the period. Balance sheet provides about the assets and liabilities of

company and cash flow statement provides information about the cash inflows and outflows.

Financial statements are used by the external parties that are shareholders, government,

suppliers, customers and other parties for assessing the financial performance and position of the

firm.

Question 4

Fundamental principles of accounting

There are different fundamental principles of accounting.

Monetary unit

8

the given time. Financial information shows current balance in terms of the income changes in

overall worth of company based over its income and cash flow statement which shows sources of

funds. Financial statements do not include information over the expenses of the purchases.

Financial statement relates to providing the information over financial position, results of

the operations and cash flows (Lorson, 2017). The information in financial statements helps

users of the financial statement in making decision for allocation of the resources. There are

three main financial statements that are income statement which informs about ability of

company in generating profit, balance sheet reporting current position of the business and cash

flow statement shows inflows and outflows of cash.

Use of the above reports and the user of these reports.

Financial reports have the information about the business workings and operations. It

contains the information that is used for making financial decisions. These help the organisation

in framing the corporate strategies for increasing the profits are making the existing processes

easier. It ensures that business is operating in the defined manner. The financial reports are made

for internal use of management and not for external parties (Kaya, 2019). Management user

these reports for taking decisions for increasing the operating effectiveness, increasing profits

and to maximise wealth of the shareholders.

Financial statements on the other contains the information regarding the income of the

company that is presented in the income statement. It provides the details over income and

expenses of the entity during the period. Balance sheet provides about the assets and liabilities of

company and cash flow statement provides information about the cash inflows and outflows.

Financial statements are used by the external parties that are shareholders, government,

suppliers, customers and other parties for assessing the financial performance and position of the

firm.

Question 4

Fundamental principles of accounting

There are different fundamental principles of accounting.

Monetary unit

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It requires to record the values in term of the single monetary units. It could not be

accounted for the goods like barter system. It is difficult to assign values to the goods & items as

this is subjective.

Going concern

Accounting is based over the concepts that business is established for doing business for

an indefinite period. Due to the principle of going concern organisations could function on the

credit, it accounts for the accounts receivables & payables that intends to pay or receive in future

and for charging depreciation.

Principle of Conservatism

Central tenet is principle of conservatism. As per the principle when doubt is there about

amount of the expected inflows & ouflows. Company is required to state lowest possible

revenues and highest possible expenses and costs (Kristýna, 2018). Inventory is valued at lower

of the cost or market prices. The principle helps the business in preparing about the forthcoming

financial crises.

Cost principle

It is related closely to the conservatism principle. It advocates that it should lists

everything on financial statements at cost price. Assets like gold, plant, machinery etc

appreciate. The appreciation in financial statements is not reflected unless realized by the

company. Assets could not be recorded over market value as they are only estimates.

Accounting works over the cost principle that is over facts.

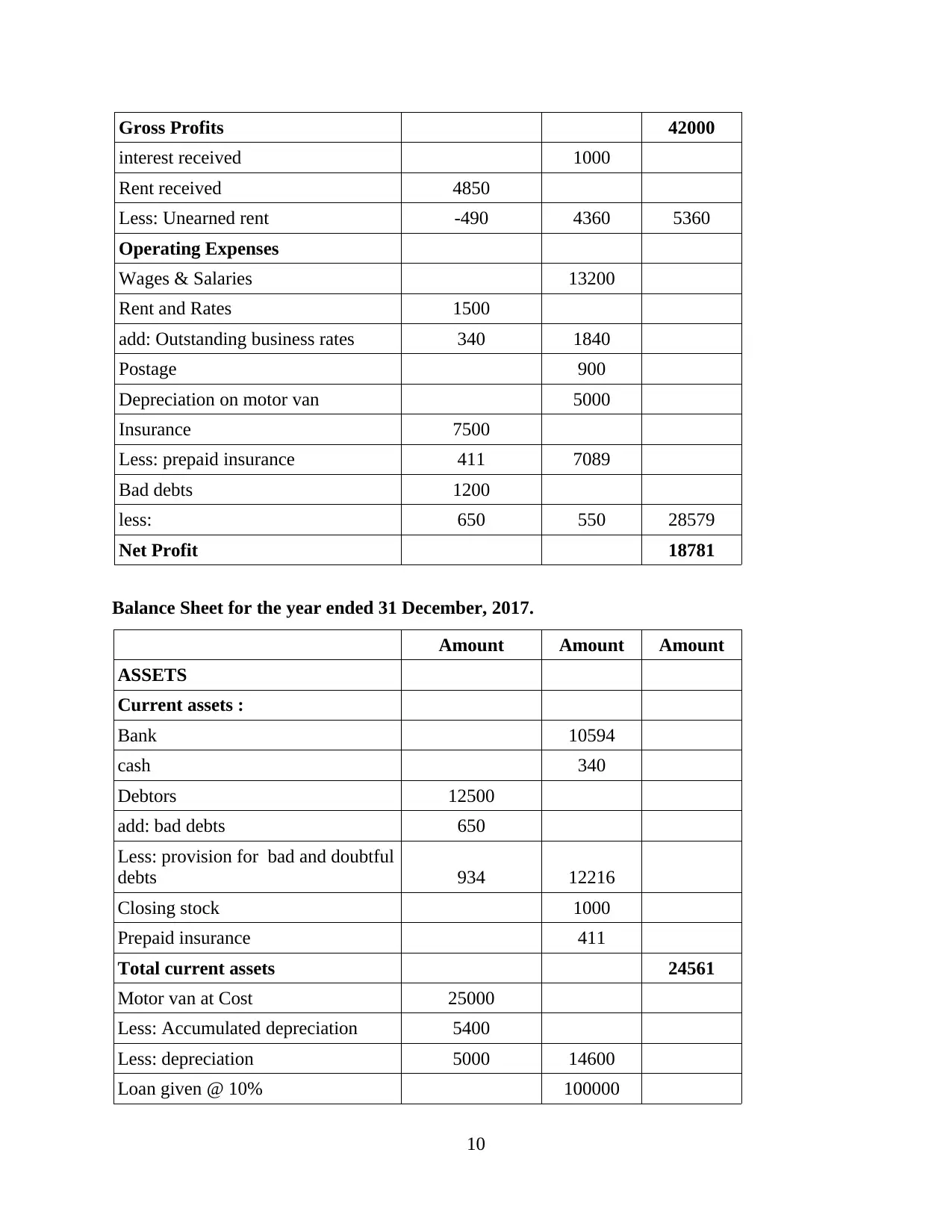

Question 5

Profit and loss statement and the balance sheet for the year ended 31 December 2017.

Profit or Loss Statement for the year ended 31 December, 2017.

Particulars Amount Amount Amount

Sales 124000

(125000-1000)

COGS 82000

Opening stock 9500

Purchases 73500

(75000-1500)

-Closing stock -1000

9

accounted for the goods like barter system. It is difficult to assign values to the goods & items as

this is subjective.

Going concern

Accounting is based over the concepts that business is established for doing business for

an indefinite period. Due to the principle of going concern organisations could function on the

credit, it accounts for the accounts receivables & payables that intends to pay or receive in future

and for charging depreciation.

Principle of Conservatism

Central tenet is principle of conservatism. As per the principle when doubt is there about

amount of the expected inflows & ouflows. Company is required to state lowest possible

revenues and highest possible expenses and costs (Kristýna, 2018). Inventory is valued at lower

of the cost or market prices. The principle helps the business in preparing about the forthcoming

financial crises.

Cost principle

It is related closely to the conservatism principle. It advocates that it should lists

everything on financial statements at cost price. Assets like gold, plant, machinery etc

appreciate. The appreciation in financial statements is not reflected unless realized by the

company. Assets could not be recorded over market value as they are only estimates.

Accounting works over the cost principle that is over facts.

Question 5

Profit and loss statement and the balance sheet for the year ended 31 December 2017.

Profit or Loss Statement for the year ended 31 December, 2017.

Particulars Amount Amount Amount

Sales 124000

(125000-1000)

COGS 82000

Opening stock 9500

Purchases 73500

(75000-1500)

-Closing stock -1000

9

Gross Profits 42000

interest received 1000

Rent received 4850

Less: Unearned rent -490 4360 5360

Operating Expenses

Wages & Salaries 13200

Rent and Rates 1500

add: Outstanding business rates 340 1840

Postage 900

Depreciation on motor van 5000

Insurance 7500

Less: prepaid insurance 411 7089

Bad debts 1200

less: 650 550 28579

Net Profit 18781

Balance Sheet for the year ended 31 December, 2017.

Amount Amount Amount

ASSETS

Current assets :

Bank 10594

cash 340

Debtors 12500

add: bad debts 650

Less: provision for bad and doubtful

debts 934 12216

Closing stock 1000

Prepaid insurance 411

Total current assets 24561

Motor van at Cost 25000

Less: Accumulated depreciation 5400

Less: depreciation 5000 14600

Loan given @ 10% 100000

10

interest received 1000

Rent received 4850

Less: Unearned rent -490 4360 5360

Operating Expenses

Wages & Salaries 13200

Rent and Rates 1500

add: Outstanding business rates 340 1840

Postage 900

Depreciation on motor van 5000

Insurance 7500

Less: prepaid insurance 411 7089

Bad debts 1200

less: 650 550 28579

Net Profit 18781

Balance Sheet for the year ended 31 December, 2017.

Amount Amount Amount

ASSETS

Current assets :

Bank 10594

cash 340

Debtors 12500

add: bad debts 650

Less: provision for bad and doubtful

debts 934 12216

Closing stock 1000

Prepaid insurance 411

Total current assets 24561

Motor van at Cost 25000

Less: Accumulated depreciation 5400

Less: depreciation 5000 14600

Loan given @ 10% 100000

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.