Financial Accounting Report: Muhammad's Business, Akram & Milky

VerifiedAdded on 2020/10/22

|16

|4595

|222

Report

AI Summary

This financial accounting report comprehensively addresses key concepts in financial accounting, including the preparation of journals, ledgers, and trial balances for Muhammad's business. It also details the creation of final accounts, specifically a profit and loss account, and balance sheet for Carol Andrew. The report further extends to bank reconciliation statements for Akram and the process of creating rectified entries for Milky, utilizing appropriate journal entries and addressing the suspense account. The content covers a range of accounting tasks, from recording transactions to summarizing financial data, demonstrating a solid understanding of accounting principles and practices, and providing a practical application of these concepts through specific business scenarios and the preparation of key financial statements. The report also provides a detailed explanation of terms and concepts involved in Bank Reconciliation Statement.

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

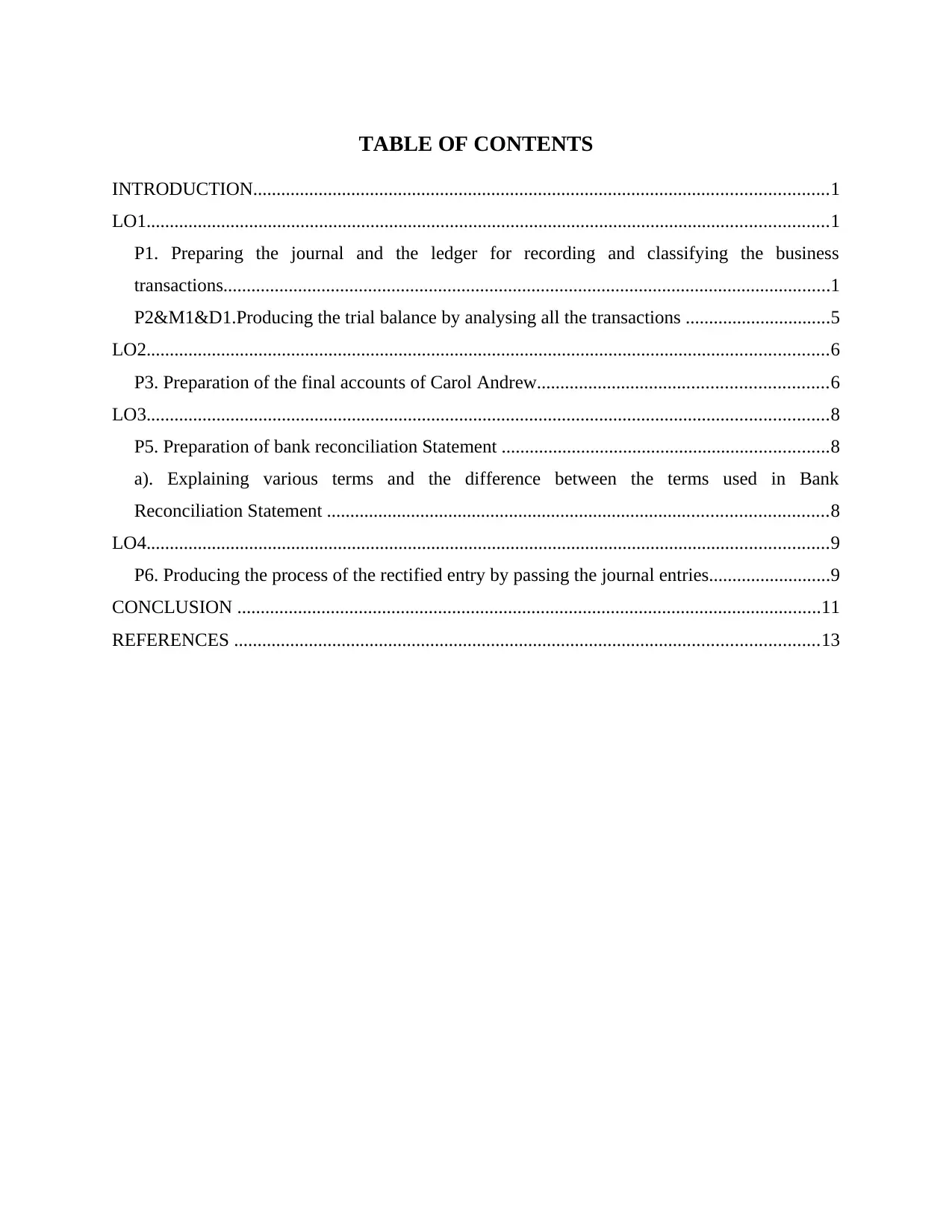

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

LO1..................................................................................................................................................1

P1. Preparing the journal and the ledger for recording and classifying the business

transactions..................................................................................................................................1

P2&M1&D1.Producing the trial balance by analysing all the transactions ...............................5

LO2..................................................................................................................................................6

P3. Preparation of the final accounts of Carol Andrew..............................................................6

LO3..................................................................................................................................................8

P5. Preparation of bank reconciliation Statement ......................................................................8

a). Explaining various terms and the difference between the terms used in Bank

Reconciliation Statement ...........................................................................................................8

LO4..................................................................................................................................................9

P6. Producing the process of the rectified entry by passing the journal entries..........................9

CONCLUSION .............................................................................................................................11

REFERENCES .............................................................................................................................13

INTRODUCTION...........................................................................................................................1

LO1..................................................................................................................................................1

P1. Preparing the journal and the ledger for recording and classifying the business

transactions..................................................................................................................................1

P2&M1&D1.Producing the trial balance by analysing all the transactions ...............................5

LO2..................................................................................................................................................6

P3. Preparation of the final accounts of Carol Andrew..............................................................6

LO3..................................................................................................................................................8

P5. Preparation of bank reconciliation Statement ......................................................................8

a). Explaining various terms and the difference between the terms used in Bank

Reconciliation Statement ...........................................................................................................8

LO4..................................................................................................................................................9

P6. Producing the process of the rectified entry by passing the journal entries..........................9

CONCLUSION .............................................................................................................................11

REFERENCES .............................................................................................................................13

INTRODUCTION

Financial accounting is the area of the accounting in that emphasizes on facilitating the

useful information to the internal and the external users such as the management, owners,

employees, creditors, government, investors and the tax authorities. It is the way in which the

business could record its financial transactions so that it could be communicated or reported to

the ultimate users. It provides for the financial information which helps the users in making the

critical decisions regarding their investment by tracking the performance and the position of the

organization through the accounting. It is known as practice of identifying, recording, classifying

, summarizing, interpreting and communicating the results. It provides for the preparation of the

financial statements like profit and loss account, balance sheet and the cash flow statement that

reflects the true and fair view of the performance and the position of the companies in the overall

market as it is formulated by following all the guidelines provisioned by the GAAP and the

international accounting standards. It facilitates the information regarding the income, assets ,

liabilities and the common equity. The present study is based on the preparation of the journal,

ledger, trial balance, profit and loss account and the balance sheet for different companies or the

firm. Furthermore, the report includes the formulation of the journal, ledger and the trial balance

for Muhammad's business and final accounts for Carol Andrew. In the scenario 2, the bank

reconciliation for the month of the February is prepared of Akram and Rectified entries for the

Milky by passing the appropriate journal entries and suspense account.

LO1.

P1. Preparing the journal and the ledger for recording and classifying the business transactions

Journal- It is stated as the record of the financial transactions in a logical order. The

transactions are recorded as per considering the double entry book keeping system which means

that every transaction contains the dual effect of recording that is debit as well as the credit. It is

used for referring the trading transactions which involves the details of the trades that are made

by the investor (Mullinova, 2016). Journal is the called as the primary books of the accounting

as it includes the recording aspect of the transactions. Journal entries act as the basis for the

general ledger accounts. The process in which recording takes place is known as the journalizing

and the record of the every single transaction is called as journal entry. Journal is also said as the

book of the original entry.

1

Financial accounting is the area of the accounting in that emphasizes on facilitating the

useful information to the internal and the external users such as the management, owners,

employees, creditors, government, investors and the tax authorities. It is the way in which the

business could record its financial transactions so that it could be communicated or reported to

the ultimate users. It provides for the financial information which helps the users in making the

critical decisions regarding their investment by tracking the performance and the position of the

organization through the accounting. It is known as practice of identifying, recording, classifying

, summarizing, interpreting and communicating the results. It provides for the preparation of the

financial statements like profit and loss account, balance sheet and the cash flow statement that

reflects the true and fair view of the performance and the position of the companies in the overall

market as it is formulated by following all the guidelines provisioned by the GAAP and the

international accounting standards. It facilitates the information regarding the income, assets ,

liabilities and the common equity. The present study is based on the preparation of the journal,

ledger, trial balance, profit and loss account and the balance sheet for different companies or the

firm. Furthermore, the report includes the formulation of the journal, ledger and the trial balance

for Muhammad's business and final accounts for Carol Andrew. In the scenario 2, the bank

reconciliation for the month of the February is prepared of Akram and Rectified entries for the

Milky by passing the appropriate journal entries and suspense account.

LO1.

P1. Preparing the journal and the ledger for recording and classifying the business transactions

Journal- It is stated as the record of the financial transactions in a logical order. The

transactions are recorded as per considering the double entry book keeping system which means

that every transaction contains the dual effect of recording that is debit as well as the credit. It is

used for referring the trading transactions which involves the details of the trades that are made

by the investor (Mullinova, 2016). Journal is the called as the primary books of the accounting

as it includes the recording aspect of the transactions. Journal entries act as the basis for the

general ledger accounts. The process in which recording takes place is known as the journalizing

and the record of the every single transaction is called as journal entry. Journal is also said as the

book of the original entry.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

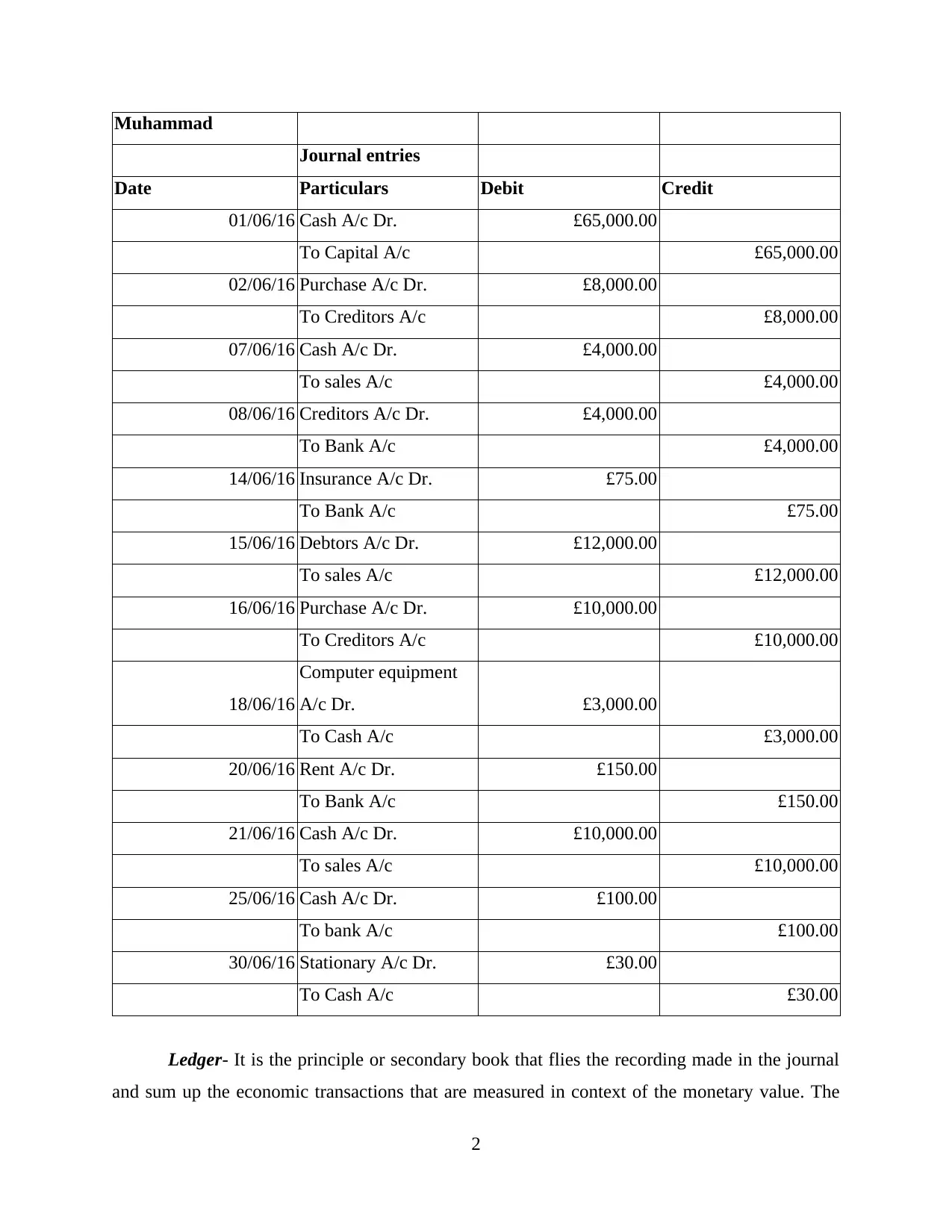

Muhammad

Journal entries

Date Particulars Debit Credit

01/06/16 Cash A/c Dr. £65,000.00

To Capital A/c £65,000.00

02/06/16 Purchase A/c Dr. £8,000.00

To Creditors A/c £8,000.00

07/06/16 Cash A/c Dr. £4,000.00

To sales A/c £4,000.00

08/06/16 Creditors A/c Dr. £4,000.00

To Bank A/c £4,000.00

14/06/16 Insurance A/c Dr. £75.00

To Bank A/c £75.00

15/06/16 Debtors A/c Dr. £12,000.00

To sales A/c £12,000.00

16/06/16 Purchase A/c Dr. £10,000.00

To Creditors A/c £10,000.00

18/06/16

Computer equipment

A/c Dr. £3,000.00

To Cash A/c £3,000.00

20/06/16 Rent A/c Dr. £150.00

To Bank A/c £150.00

21/06/16 Cash A/c Dr. £10,000.00

To sales A/c £10,000.00

25/06/16 Cash A/c Dr. £100.00

To bank A/c £100.00

30/06/16 Stationary A/c Dr. £30.00

To Cash A/c £30.00

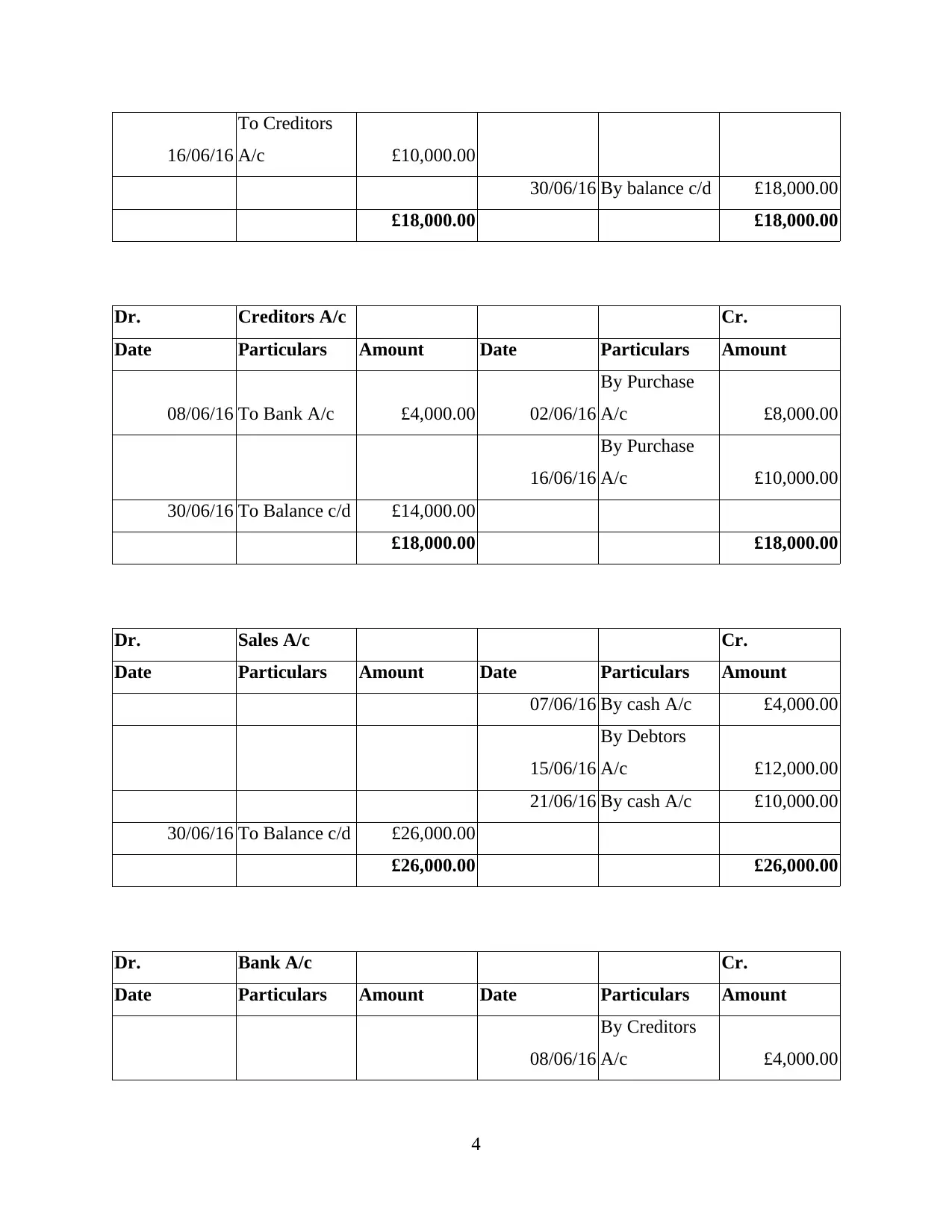

Ledger- It is the principle or secondary book that flies the recording made in the journal

and sum up the economic transactions that are measured in context of the monetary value. The

2

Journal entries

Date Particulars Debit Credit

01/06/16 Cash A/c Dr. £65,000.00

To Capital A/c £65,000.00

02/06/16 Purchase A/c Dr. £8,000.00

To Creditors A/c £8,000.00

07/06/16 Cash A/c Dr. £4,000.00

To sales A/c £4,000.00

08/06/16 Creditors A/c Dr. £4,000.00

To Bank A/c £4,000.00

14/06/16 Insurance A/c Dr. £75.00

To Bank A/c £75.00

15/06/16 Debtors A/c Dr. £12,000.00

To sales A/c £12,000.00

16/06/16 Purchase A/c Dr. £10,000.00

To Creditors A/c £10,000.00

18/06/16

Computer equipment

A/c Dr. £3,000.00

To Cash A/c £3,000.00

20/06/16 Rent A/c Dr. £150.00

To Bank A/c £150.00

21/06/16 Cash A/c Dr. £10,000.00

To sales A/c £10,000.00

25/06/16 Cash A/c Dr. £100.00

To bank A/c £100.00

30/06/16 Stationary A/c Dr. £30.00

To Cash A/c £30.00

Ledger- It is the principle or secondary book that flies the recording made in the journal

and sum up the economic transactions that are measured in context of the monetary value. The

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

transactions recorded are classifies into various accounts with the separate columns of the debits

and the credit (Tong and Saladrigues, 2018). It indicates the summary of the amount of all the

transactions entered in for supporting the journal. Ledger facilitates the preparation of the trial

balance as it shows the carry forward balance of each and every account. The major purpose of

the ledger is to summarize all the journal entries so that it can be used for the future referencing

and also for formulating the financial statements.

Ledger A/c

Dr. Cash A/c Cr.

Date Particulars Amount Date Particulars Amount

01/06/16 To Capital A/c £65,000.00 18/06/16

By Computer

Equipment A/c £3,000.00

07/06/16 To sales A/c £4,000.00 30/06/16

By stationary

A/c £30.00

21/06/16 To sales A/c £10,000.00

25/06/16 To bank A/c £100.00

30/06/16 By balance c/d £76,070.00

£79,100.00 £79,100.00

Dr. Capital A/c Cr.

Date Particulars Amount Date Particulars Amount

01/06/16 By cash A/c £65,000.00

30/06/16 To Balance c/d £65,000.00

£65,000.00 £65,000.00

Dr. Purchase A/c Cr.

Date Particulars Amount Date Particulars Amount

02/06/16

To Creditors

A/c £8,000.00

3

and the credit (Tong and Saladrigues, 2018). It indicates the summary of the amount of all the

transactions entered in for supporting the journal. Ledger facilitates the preparation of the trial

balance as it shows the carry forward balance of each and every account. The major purpose of

the ledger is to summarize all the journal entries so that it can be used for the future referencing

and also for formulating the financial statements.

Ledger A/c

Dr. Cash A/c Cr.

Date Particulars Amount Date Particulars Amount

01/06/16 To Capital A/c £65,000.00 18/06/16

By Computer

Equipment A/c £3,000.00

07/06/16 To sales A/c £4,000.00 30/06/16

By stationary

A/c £30.00

21/06/16 To sales A/c £10,000.00

25/06/16 To bank A/c £100.00

30/06/16 By balance c/d £76,070.00

£79,100.00 £79,100.00

Dr. Capital A/c Cr.

Date Particulars Amount Date Particulars Amount

01/06/16 By cash A/c £65,000.00

30/06/16 To Balance c/d £65,000.00

£65,000.00 £65,000.00

Dr. Purchase A/c Cr.

Date Particulars Amount Date Particulars Amount

02/06/16

To Creditors

A/c £8,000.00

3

16/06/16

To Creditors

A/c £10,000.00

30/06/16 By balance c/d £18,000.00

£18,000.00 £18,000.00

Dr. Creditors A/c Cr.

Date Particulars Amount Date Particulars Amount

08/06/16 To Bank A/c £4,000.00 02/06/16

By Purchase

A/c £8,000.00

16/06/16

By Purchase

A/c £10,000.00

30/06/16 To Balance c/d £14,000.00

£18,000.00 £18,000.00

Dr. Sales A/c Cr.

Date Particulars Amount Date Particulars Amount

07/06/16 By cash A/c £4,000.00

15/06/16

By Debtors

A/c £12,000.00

21/06/16 By cash A/c £10,000.00

30/06/16 To Balance c/d £26,000.00

£26,000.00 £26,000.00

Dr. Bank A/c Cr.

Date Particulars Amount Date Particulars Amount

08/06/16

By Creditors

A/c £4,000.00

4

To Creditors

A/c £10,000.00

30/06/16 By balance c/d £18,000.00

£18,000.00 £18,000.00

Dr. Creditors A/c Cr.

Date Particulars Amount Date Particulars Amount

08/06/16 To Bank A/c £4,000.00 02/06/16

By Purchase

A/c £8,000.00

16/06/16

By Purchase

A/c £10,000.00

30/06/16 To Balance c/d £14,000.00

£18,000.00 £18,000.00

Dr. Sales A/c Cr.

Date Particulars Amount Date Particulars Amount

07/06/16 By cash A/c £4,000.00

15/06/16

By Debtors

A/c £12,000.00

21/06/16 By cash A/c £10,000.00

30/06/16 To Balance c/d £26,000.00

£26,000.00 £26,000.00

Dr. Bank A/c Cr.

Date Particulars Amount Date Particulars Amount

08/06/16

By Creditors

A/c £4,000.00

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

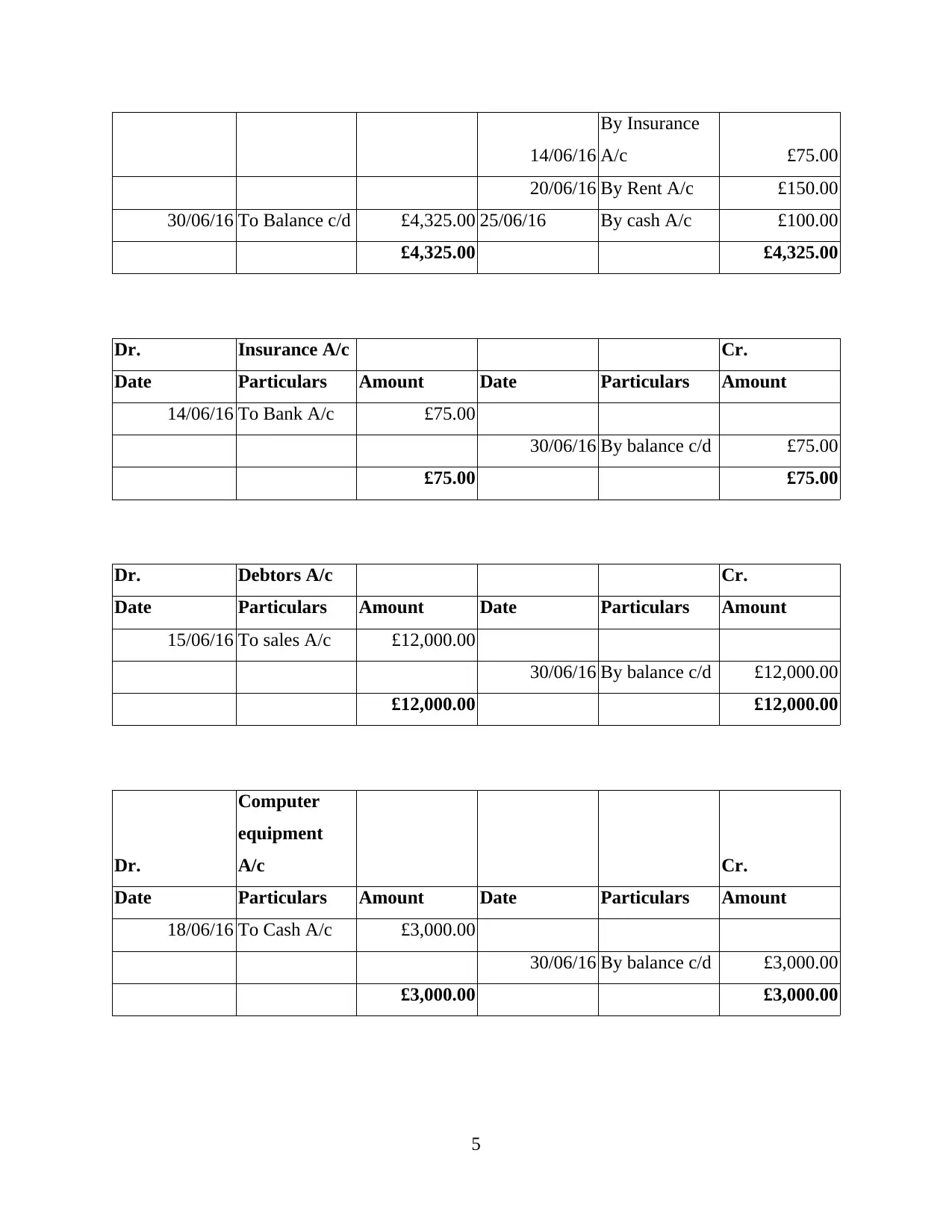

14/06/16

By Insurance

A/c £75.00

20/06/16 By Rent A/c £150.00

30/06/16 To Balance c/d £4,325.00 25/06/16 By cash A/c £100.00

£4,325.00 £4,325.00

Dr. Insurance A/c Cr.

Date Particulars Amount Date Particulars Amount

14/06/16 To Bank A/c £75.00

30/06/16 By balance c/d £75.00

£75.00 £75.00

Dr. Debtors A/c Cr.

Date Particulars Amount Date Particulars Amount

15/06/16 To sales A/c £12,000.00

30/06/16 By balance c/d £12,000.00

£12,000.00 £12,000.00

Dr.

Computer

equipment

A/c Cr.

Date Particulars Amount Date Particulars Amount

18/06/16 To Cash A/c £3,000.00

30/06/16 By balance c/d £3,000.00

£3,000.00 £3,000.00

5

By Insurance

A/c £75.00

20/06/16 By Rent A/c £150.00

30/06/16 To Balance c/d £4,325.00 25/06/16 By cash A/c £100.00

£4,325.00 £4,325.00

Dr. Insurance A/c Cr.

Date Particulars Amount Date Particulars Amount

14/06/16 To Bank A/c £75.00

30/06/16 By balance c/d £75.00

£75.00 £75.00

Dr. Debtors A/c Cr.

Date Particulars Amount Date Particulars Amount

15/06/16 To sales A/c £12,000.00

30/06/16 By balance c/d £12,000.00

£12,000.00 £12,000.00

Dr.

Computer

equipment

A/c Cr.

Date Particulars Amount Date Particulars Amount

18/06/16 To Cash A/c £3,000.00

30/06/16 By balance c/d £3,000.00

£3,000.00 £3,000.00

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

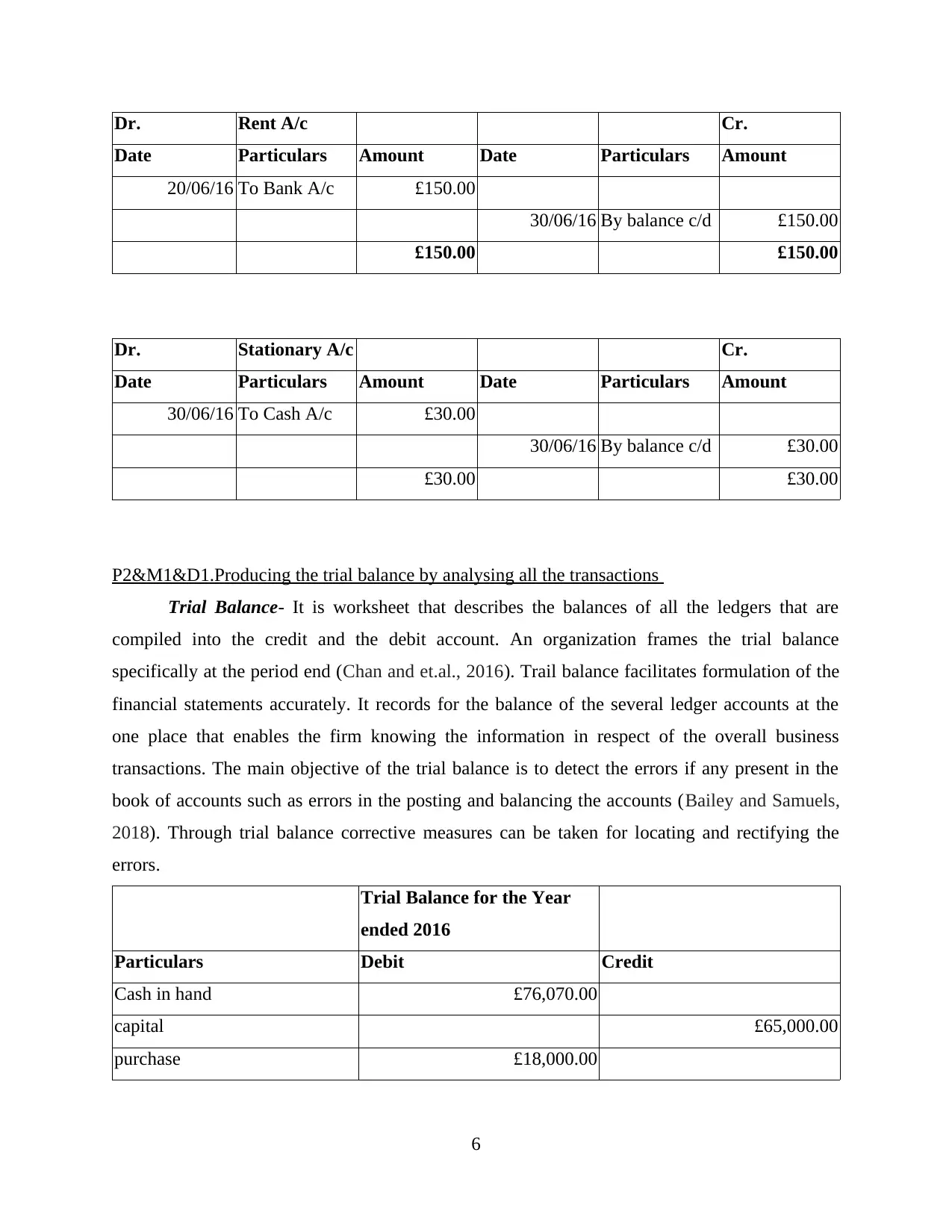

Dr. Rent A/c Cr.

Date Particulars Amount Date Particulars Amount

20/06/16 To Bank A/c £150.00

30/06/16 By balance c/d £150.00

£150.00 £150.00

Dr. Stationary A/c Cr.

Date Particulars Amount Date Particulars Amount

30/06/16 To Cash A/c £30.00

30/06/16 By balance c/d £30.00

£30.00 £30.00

P2&M1&D1.Producing the trial balance by analysing all the transactions

Trial Balance- It is worksheet that describes the balances of all the ledgers that are

compiled into the credit and the debit account. An organization frames the trial balance

specifically at the period end (Chan and et.al., 2016). Trail balance facilitates formulation of the

financial statements accurately. It records for the balance of the several ledger accounts at the

one place that enables the firm knowing the information in respect of the overall business

transactions. The main objective of the trial balance is to detect the errors if any present in the

book of accounts such as errors in the posting and balancing the accounts (Bailey and Samuels,

2018). Through trial balance corrective measures can be taken for locating and rectifying the

errors.

Trial Balance for the Year

ended 2016

Particulars Debit Credit

Cash in hand £76,070.00

capital £65,000.00

purchase £18,000.00

6

Date Particulars Amount Date Particulars Amount

20/06/16 To Bank A/c £150.00

30/06/16 By balance c/d £150.00

£150.00 £150.00

Dr. Stationary A/c Cr.

Date Particulars Amount Date Particulars Amount

30/06/16 To Cash A/c £30.00

30/06/16 By balance c/d £30.00

£30.00 £30.00

P2&M1&D1.Producing the trial balance by analysing all the transactions

Trial Balance- It is worksheet that describes the balances of all the ledgers that are

compiled into the credit and the debit account. An organization frames the trial balance

specifically at the period end (Chan and et.al., 2016). Trail balance facilitates formulation of the

financial statements accurately. It records for the balance of the several ledger accounts at the

one place that enables the firm knowing the information in respect of the overall business

transactions. The main objective of the trial balance is to detect the errors if any present in the

book of accounts such as errors in the posting and balancing the accounts (Bailey and Samuels,

2018). Through trial balance corrective measures can be taken for locating and rectifying the

errors.

Trial Balance for the Year

ended 2016

Particulars Debit Credit

Cash in hand £76,070.00

capital £65,000.00

purchase £18,000.00

6

creditors £14,000.00

sales £26,000.00

Bank £4,325.00

Insurance £75.00

Debtors £12,000.00

Computer equipment £3,000.00

Rent £150.00

Stationary £30.00

£109,325.00 £109,325.00

LO2.

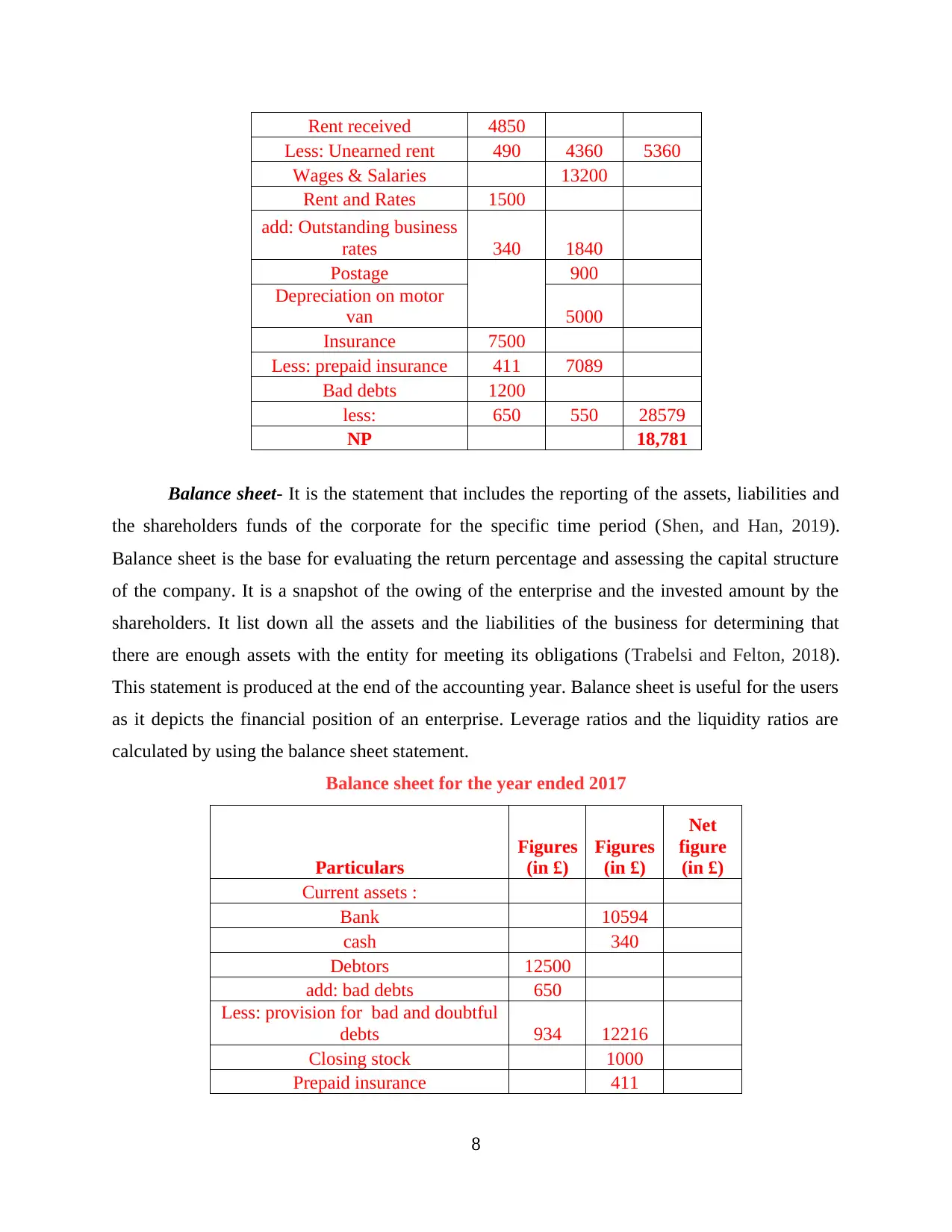

P3. Preparation of the final accounts of Carol Andrew

Profit and loss account- It is the income statement that summarizes the sales revenue,

operating cost and the expenses that are incurred during an accounting period (Chychyla, Leone,

and Minutti-Meza, 2019). This statement shows the profits and the losses of the business during

the specific time period. It allows the firm in knowing its performance and the ability of an entity

in generating the profits with increment in the revenue and by reduction in the cost. Gross

profits, operating profits and the net profit margins are ascertained through profit and loss

account which are useful for evaluating the ratio analysis so that comparison can be assessed for

several years.

Profitability statement of carol andrew for the year ended 2017

Particulars

Figures

(in £)

Figures

(in £)

Net

figure

(in £)

Sales 125,000

Less: sales return 1000 124,000

Closing stock 1000 125,000

Opening stock 9500

Purchases 75000

Less: purchase return 1500 73500 83000

GP 42,000

interest received 1000

7

sales £26,000.00

Bank £4,325.00

Insurance £75.00

Debtors £12,000.00

Computer equipment £3,000.00

Rent £150.00

Stationary £30.00

£109,325.00 £109,325.00

LO2.

P3. Preparation of the final accounts of Carol Andrew

Profit and loss account- It is the income statement that summarizes the sales revenue,

operating cost and the expenses that are incurred during an accounting period (Chychyla, Leone,

and Minutti-Meza, 2019). This statement shows the profits and the losses of the business during

the specific time period. It allows the firm in knowing its performance and the ability of an entity

in generating the profits with increment in the revenue and by reduction in the cost. Gross

profits, operating profits and the net profit margins are ascertained through profit and loss

account which are useful for evaluating the ratio analysis so that comparison can be assessed for

several years.

Profitability statement of carol andrew for the year ended 2017

Particulars

Figures

(in £)

Figures

(in £)

Net

figure

(in £)

Sales 125,000

Less: sales return 1000 124,000

Closing stock 1000 125,000

Opening stock 9500

Purchases 75000

Less: purchase return 1500 73500 83000

GP 42,000

interest received 1000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Rent received 4850

Less: Unearned rent 490 4360 5360

Wages & Salaries 13200

Rent and Rates 1500

add: Outstanding business

rates 340 1840

Postage 900

Depreciation on motor

van 5000

Insurance 7500

Less: prepaid insurance 411 7089

Bad debts 1200

less: 650 550 28579

NP 18,781

Balance sheet- It is the statement that includes the reporting of the assets, liabilities and

the shareholders funds of the corporate for the specific time period (Shen, and Han, 2019).

Balance sheet is the base for evaluating the return percentage and assessing the capital structure

of the company. It is a snapshot of the owing of the enterprise and the invested amount by the

shareholders. It list down all the assets and the liabilities of the business for determining that

there are enough assets with the entity for meeting its obligations (Trabelsi and Felton, 2018).

This statement is produced at the end of the accounting year. Balance sheet is useful for the users

as it depicts the financial position of an enterprise. Leverage ratios and the liquidity ratios are

calculated by using the balance sheet statement.

Balance sheet for the year ended 2017

Particulars

Figures

(in £)

Figures

(in £)

Net

figure

(in £)

Current assets :

Bank 10594

cash 340

Debtors 12500

add: bad debts 650

Less: provision for bad and doubtful

debts 934 12216

Closing stock 1000

Prepaid insurance 411

8

Less: Unearned rent 490 4360 5360

Wages & Salaries 13200

Rent and Rates 1500

add: Outstanding business

rates 340 1840

Postage 900

Depreciation on motor

van 5000

Insurance 7500

Less: prepaid insurance 411 7089

Bad debts 1200

less: 650 550 28579

NP 18,781

Balance sheet- It is the statement that includes the reporting of the assets, liabilities and

the shareholders funds of the corporate for the specific time period (Shen, and Han, 2019).

Balance sheet is the base for evaluating the return percentage and assessing the capital structure

of the company. It is a snapshot of the owing of the enterprise and the invested amount by the

shareholders. It list down all the assets and the liabilities of the business for determining that

there are enough assets with the entity for meeting its obligations (Trabelsi and Felton, 2018).

This statement is produced at the end of the accounting year. Balance sheet is useful for the users

as it depicts the financial position of an enterprise. Leverage ratios and the liquidity ratios are

calculated by using the balance sheet statement.

Balance sheet for the year ended 2017

Particulars

Figures

(in £)

Figures

(in £)

Net

figure

(in £)

Current assets :

Bank 10594

cash 340

Debtors 12500

add: bad debts 650

Less: provision for bad and doubtful

debts 934 12216

Closing stock 1000

Prepaid insurance 411

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

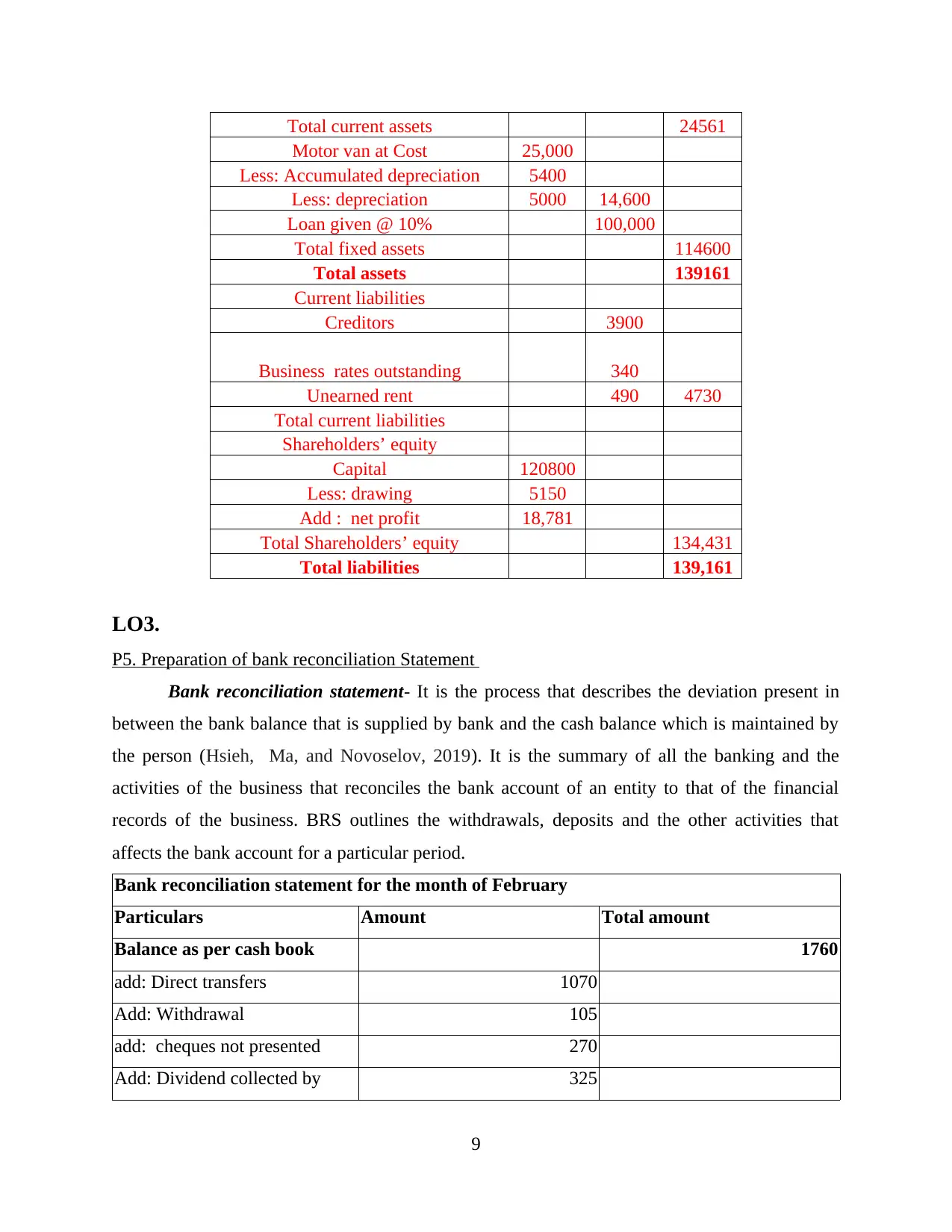

Total current assets 24561

Motor van at Cost 25,000

Less: Accumulated depreciation 5400

Less: depreciation 5000 14,600

Loan given @ 10% 100,000

Total fixed assets 114600

Total assets 139161

Current liabilities

Creditors 3900

Business rates outstanding 340

Unearned rent 490 4730

Total current liabilities

Shareholders’ equity

Capital 120800

Less: drawing 5150

Add : net profit 18,781

Total Shareholders’ equity 134,431

Total liabilities 139,161

LO3.

P5. Preparation of bank reconciliation Statement

Bank reconciliation statement- It is the process that describes the deviation present in

between the bank balance that is supplied by bank and the cash balance which is maintained by

the person (Hsieh, Ma, and Novoselov, 2019). It is the summary of all the banking and the

activities of the business that reconciles the bank account of an entity to that of the financial

records of the business. BRS outlines the withdrawals, deposits and the other activities that

affects the bank account for a particular period.

Bank reconciliation statement for the month of February

Particulars Amount Total amount

Balance as per cash book 1760

add: Direct transfers 1070

Add: Withdrawal 105

add: cheques not presented 270

Add: Dividend collected by 325

9

Motor van at Cost 25,000

Less: Accumulated depreciation 5400

Less: depreciation 5000 14,600

Loan given @ 10% 100,000

Total fixed assets 114600

Total assets 139161

Current liabilities

Creditors 3900

Business rates outstanding 340

Unearned rent 490 4730

Total current liabilities

Shareholders’ equity

Capital 120800

Less: drawing 5150

Add : net profit 18,781

Total Shareholders’ equity 134,431

Total liabilities 139,161

LO3.

P5. Preparation of bank reconciliation Statement

Bank reconciliation statement- It is the process that describes the deviation present in

between the bank balance that is supplied by bank and the cash balance which is maintained by

the person (Hsieh, Ma, and Novoselov, 2019). It is the summary of all the banking and the

activities of the business that reconciles the bank account of an entity to that of the financial

records of the business. BRS outlines the withdrawals, deposits and the other activities that

affects the bank account for a particular period.

Bank reconciliation statement for the month of February

Particulars Amount Total amount

Balance as per cash book 1760

add: Direct transfers 1070

Add: Withdrawal 105

add: cheques not presented 270

Add: Dividend collected by 325

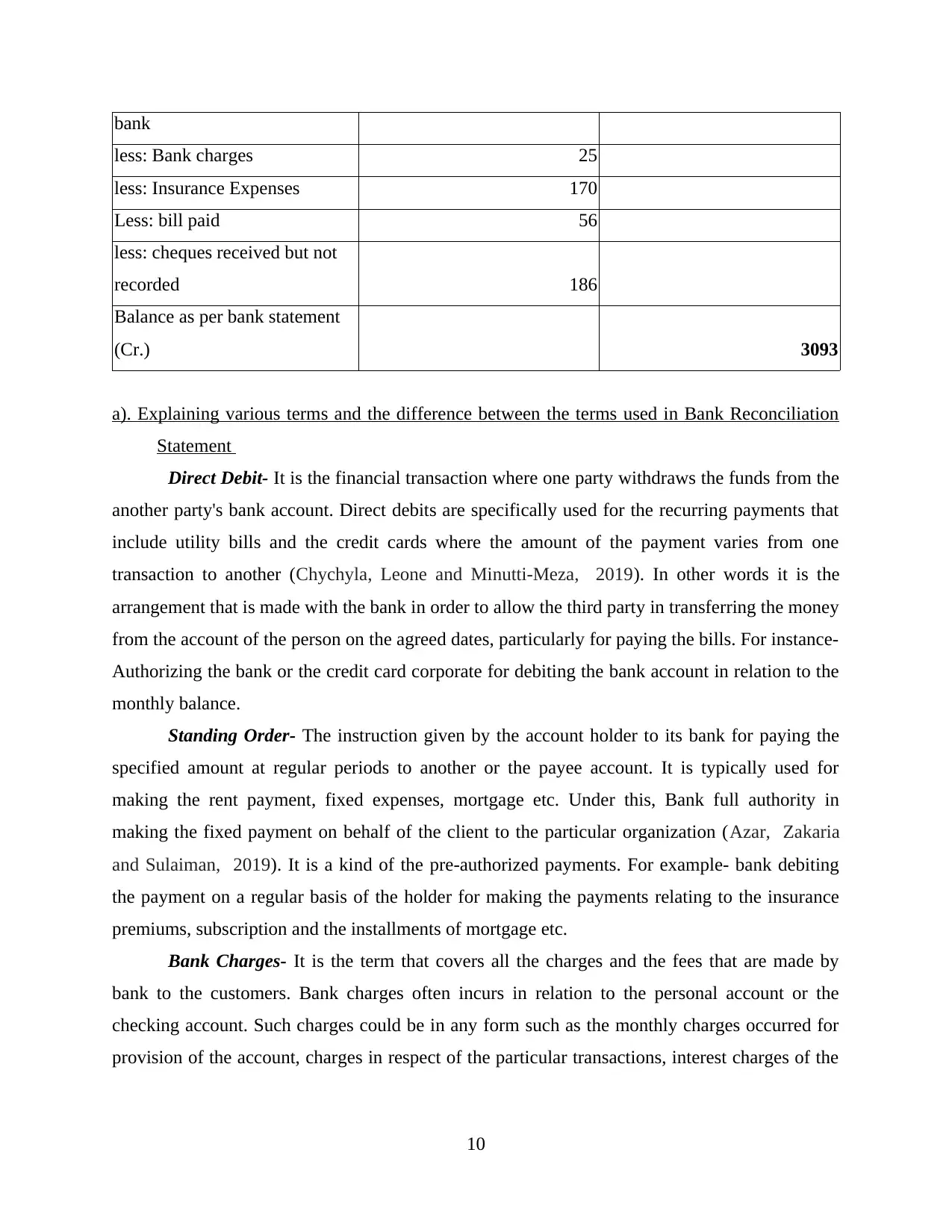

9

bank

less: Bank charges 25

less: Insurance Expenses 170

Less: bill paid 56

less: cheques received but not

recorded 186

Balance as per bank statement

(Cr.) 3093

a). Explaining various terms and the difference between the terms used in Bank Reconciliation

Statement

Direct Debit- It is the financial transaction where one party withdraws the funds from the

another party's bank account. Direct debits are specifically used for the recurring payments that

include utility bills and the credit cards where the amount of the payment varies from one

transaction to another (Chychyla, Leone and Minutti-Meza, 2019). In other words it is the

arrangement that is made with the bank in order to allow the third party in transferring the money

from the account of the person on the agreed dates, particularly for paying the bills. For instance-

Authorizing the bank or the credit card corporate for debiting the bank account in relation to the

monthly balance.

Standing Order- The instruction given by the account holder to its bank for paying the

specified amount at regular periods to another or the payee account. It is typically used for

making the rent payment, fixed expenses, mortgage etc. Under this, Bank full authority in

making the fixed payment on behalf of the client to the particular organization (Azar, Zakaria

and Sulaiman, 2019). It is a kind of the pre-authorized payments. For example- bank debiting

the payment on a regular basis of the holder for making the payments relating to the insurance

premiums, subscription and the installments of mortgage etc.

Bank Charges- It is the term that covers all the charges and the fees that are made by

bank to the customers. Bank charges often incurs in relation to the personal account or the

checking account. Such charges could be in any form such as the monthly charges occurred for

provision of the account, charges in respect of the particular transactions, interest charges of the

10

less: Bank charges 25

less: Insurance Expenses 170

Less: bill paid 56

less: cheques received but not

recorded 186

Balance as per bank statement

(Cr.) 3093

a). Explaining various terms and the difference between the terms used in Bank Reconciliation

Statement

Direct Debit- It is the financial transaction where one party withdraws the funds from the

another party's bank account. Direct debits are specifically used for the recurring payments that

include utility bills and the credit cards where the amount of the payment varies from one

transaction to another (Chychyla, Leone and Minutti-Meza, 2019). In other words it is the

arrangement that is made with the bank in order to allow the third party in transferring the money

from the account of the person on the agreed dates, particularly for paying the bills. For instance-

Authorizing the bank or the credit card corporate for debiting the bank account in relation to the

monthly balance.

Standing Order- The instruction given by the account holder to its bank for paying the

specified amount at regular periods to another or the payee account. It is typically used for

making the rent payment, fixed expenses, mortgage etc. Under this, Bank full authority in

making the fixed payment on behalf of the client to the particular organization (Azar, Zakaria

and Sulaiman, 2019). It is a kind of the pre-authorized payments. For example- bank debiting

the payment on a regular basis of the holder for making the payments relating to the insurance

premiums, subscription and the installments of mortgage etc.

Bank Charges- It is the term that covers all the charges and the fees that are made by

bank to the customers. Bank charges often incurs in relation to the personal account or the

checking account. Such charges could be in any form such as the monthly charges occurred for

provision of the account, charges in respect of the particular transactions, interest charges of the

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.