Financial Accounting Assignment: Analyzing Transactions and Statements

VerifiedAdded on 2022/12/23

|22

|3227

|26

Homework Assignment

AI Summary

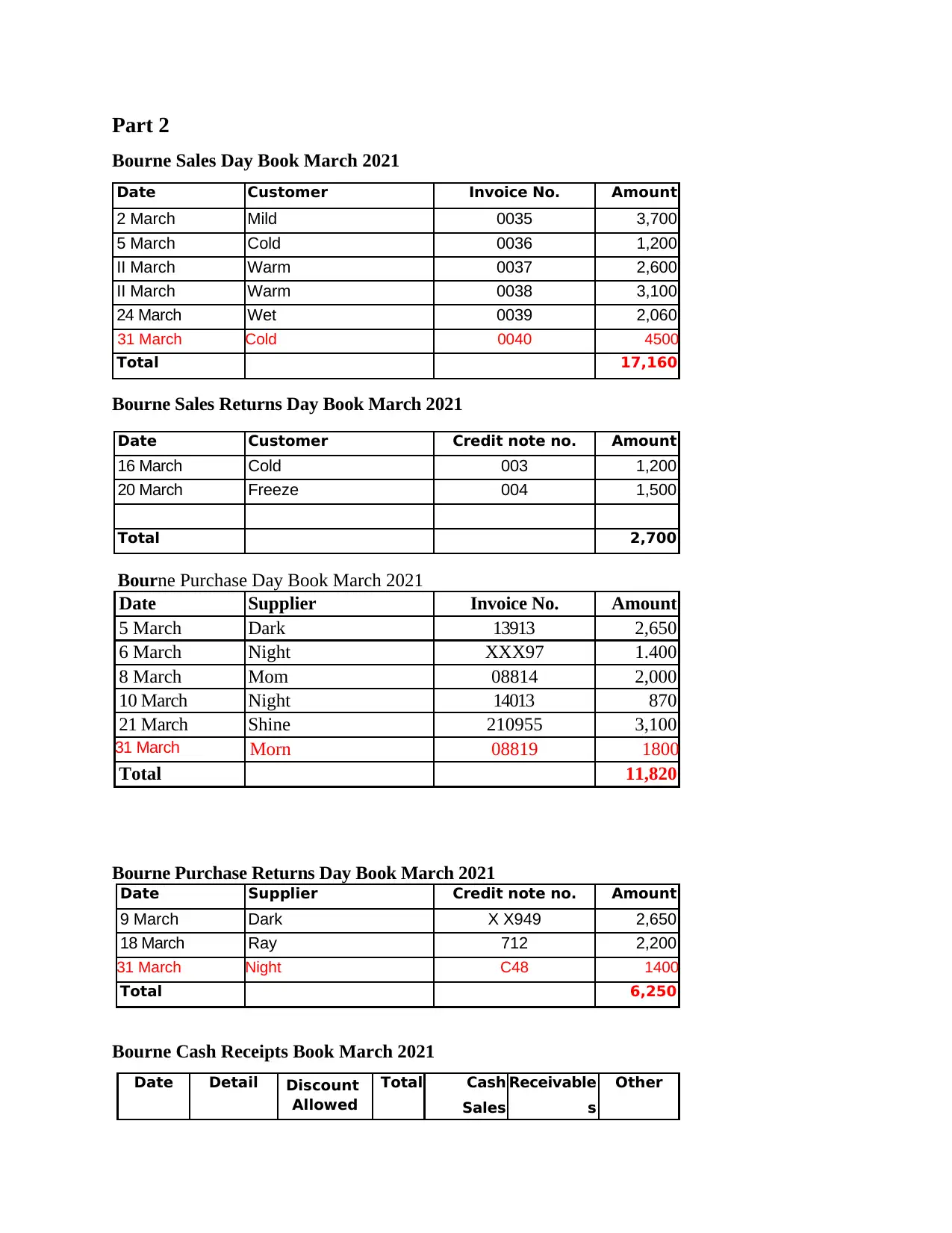

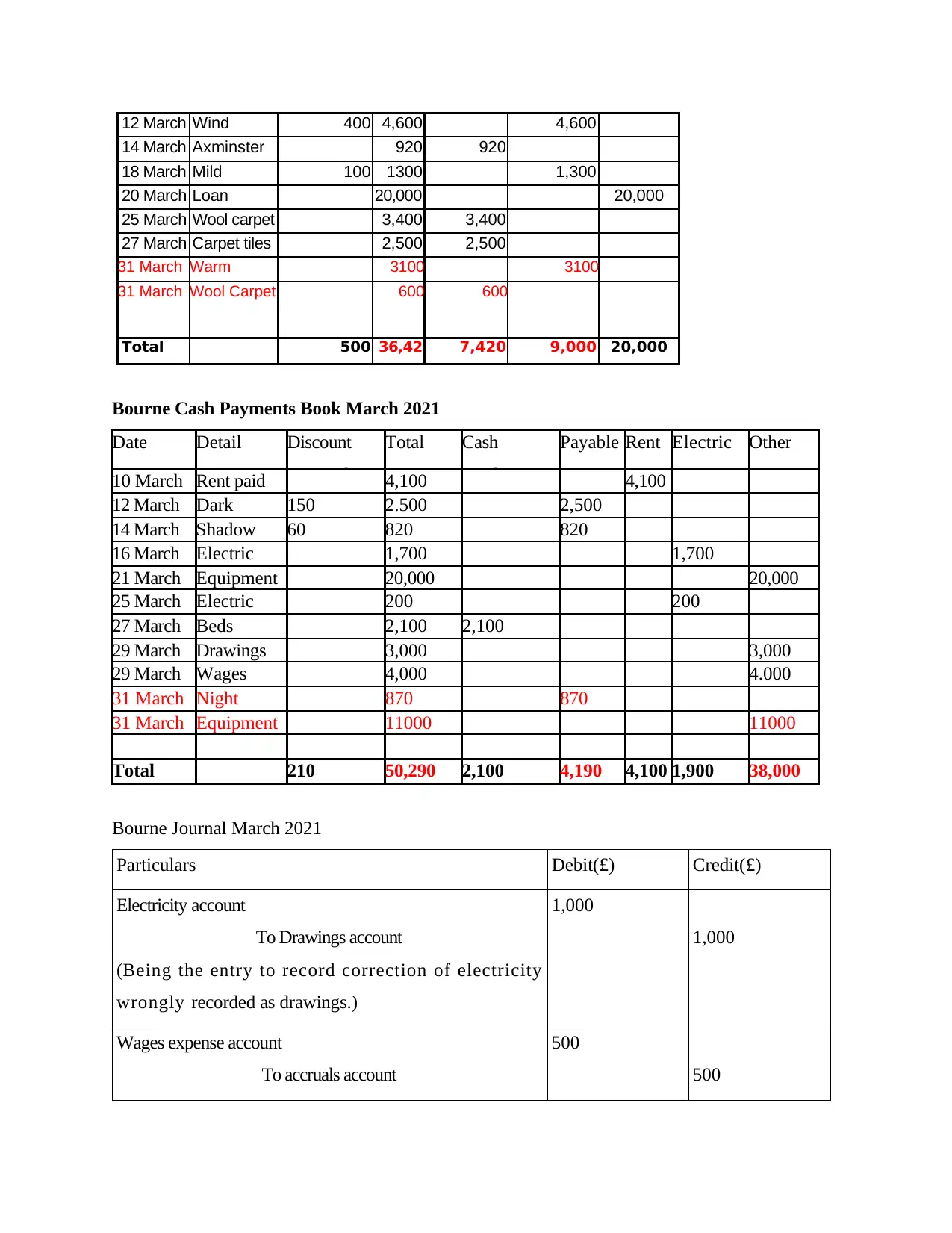

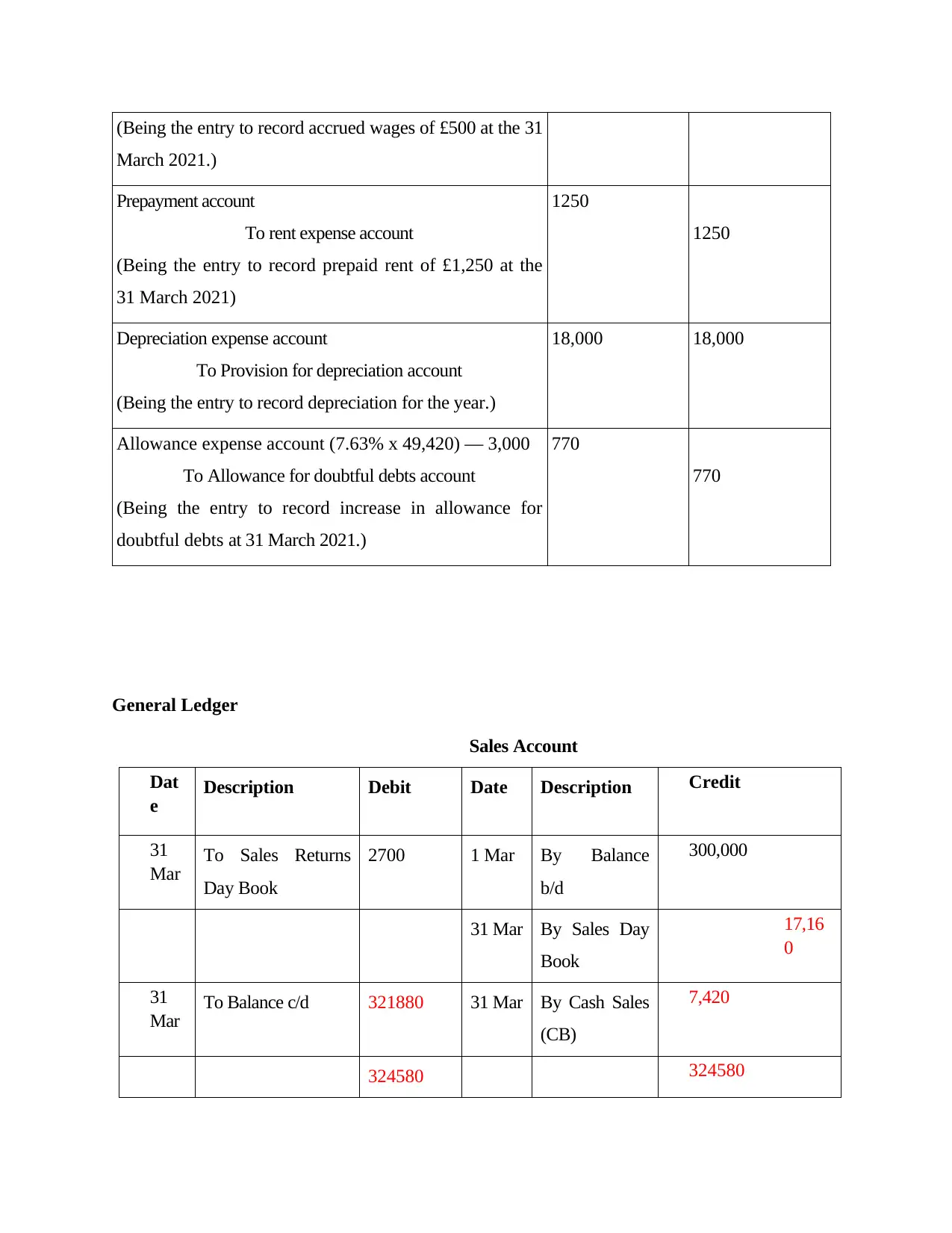

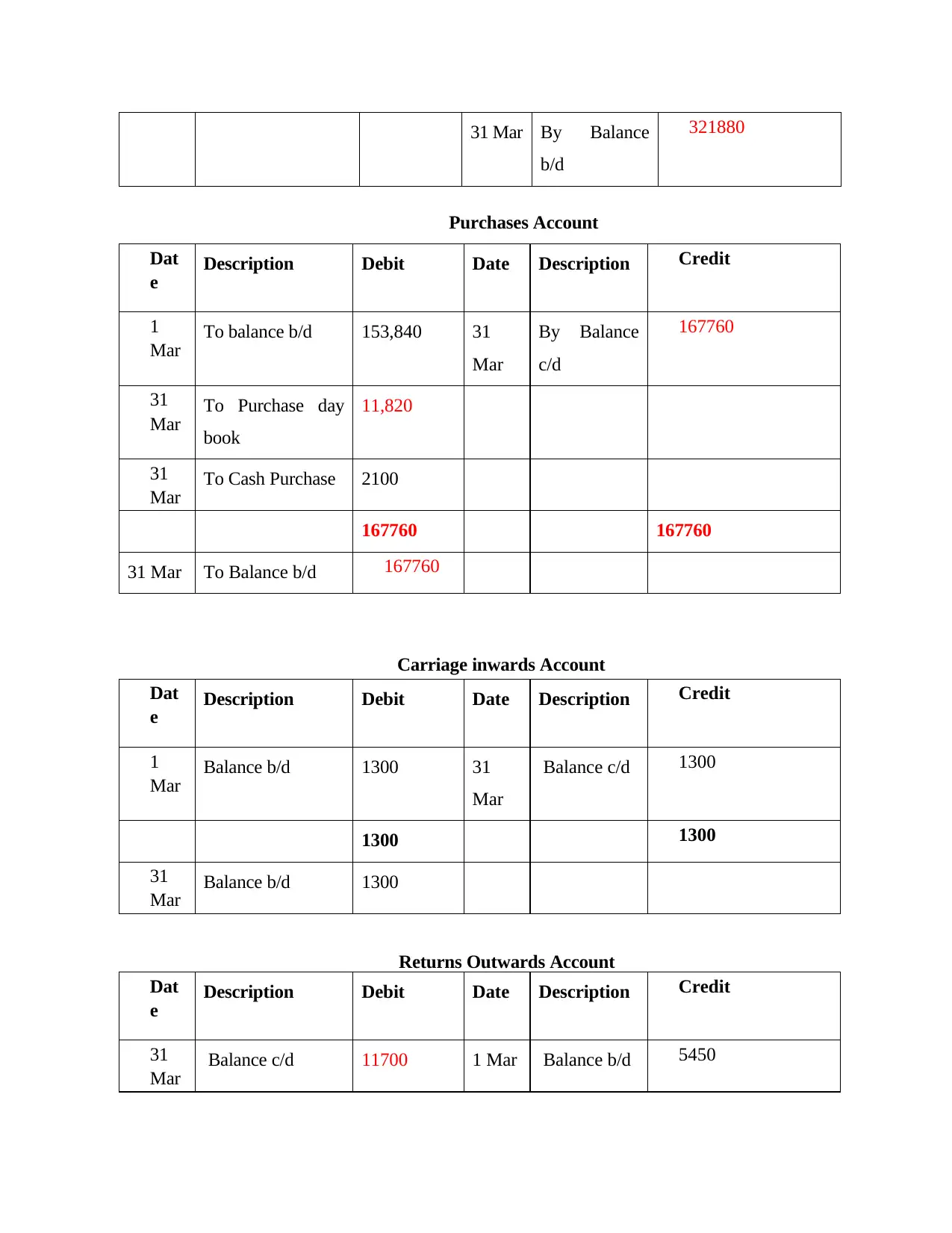

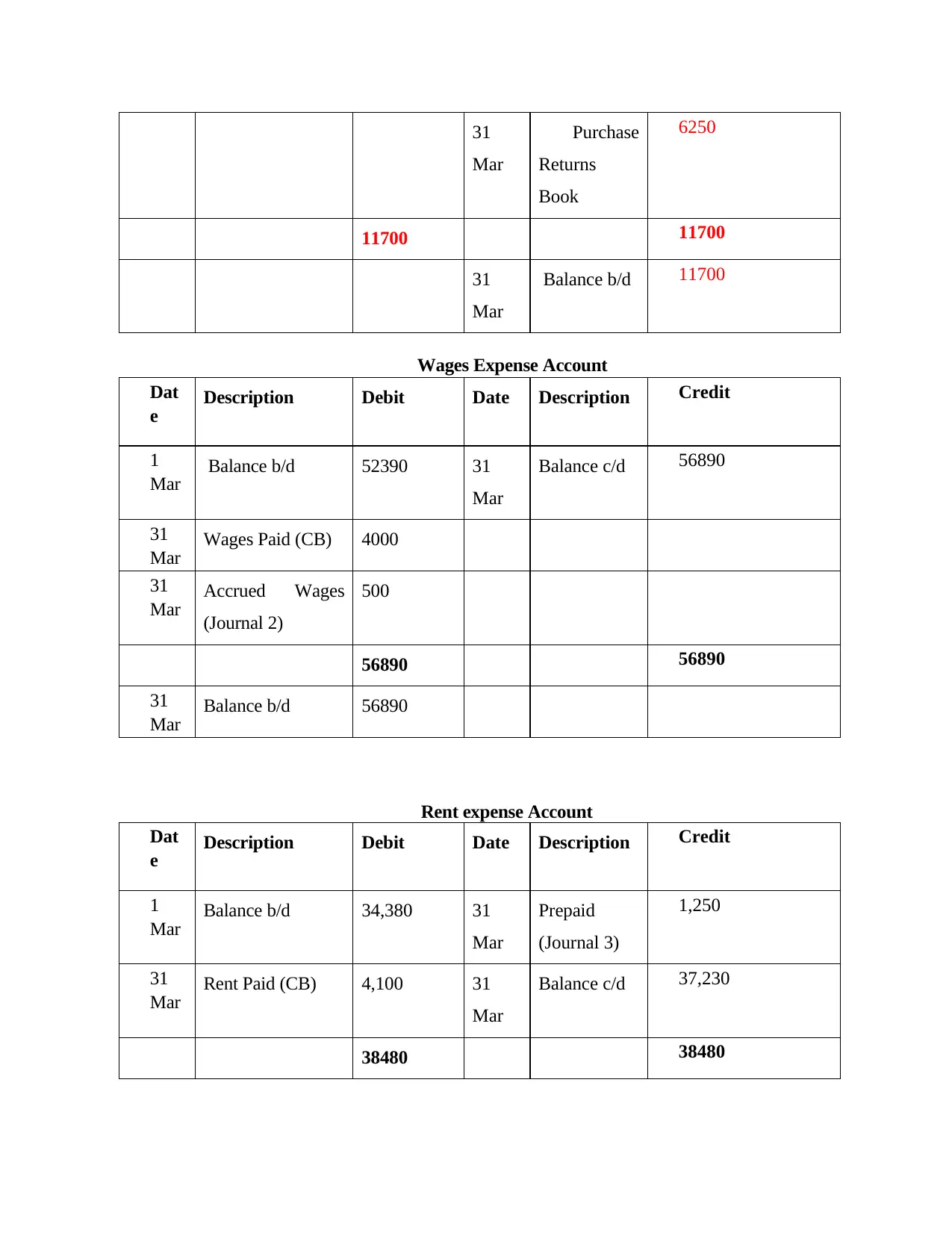

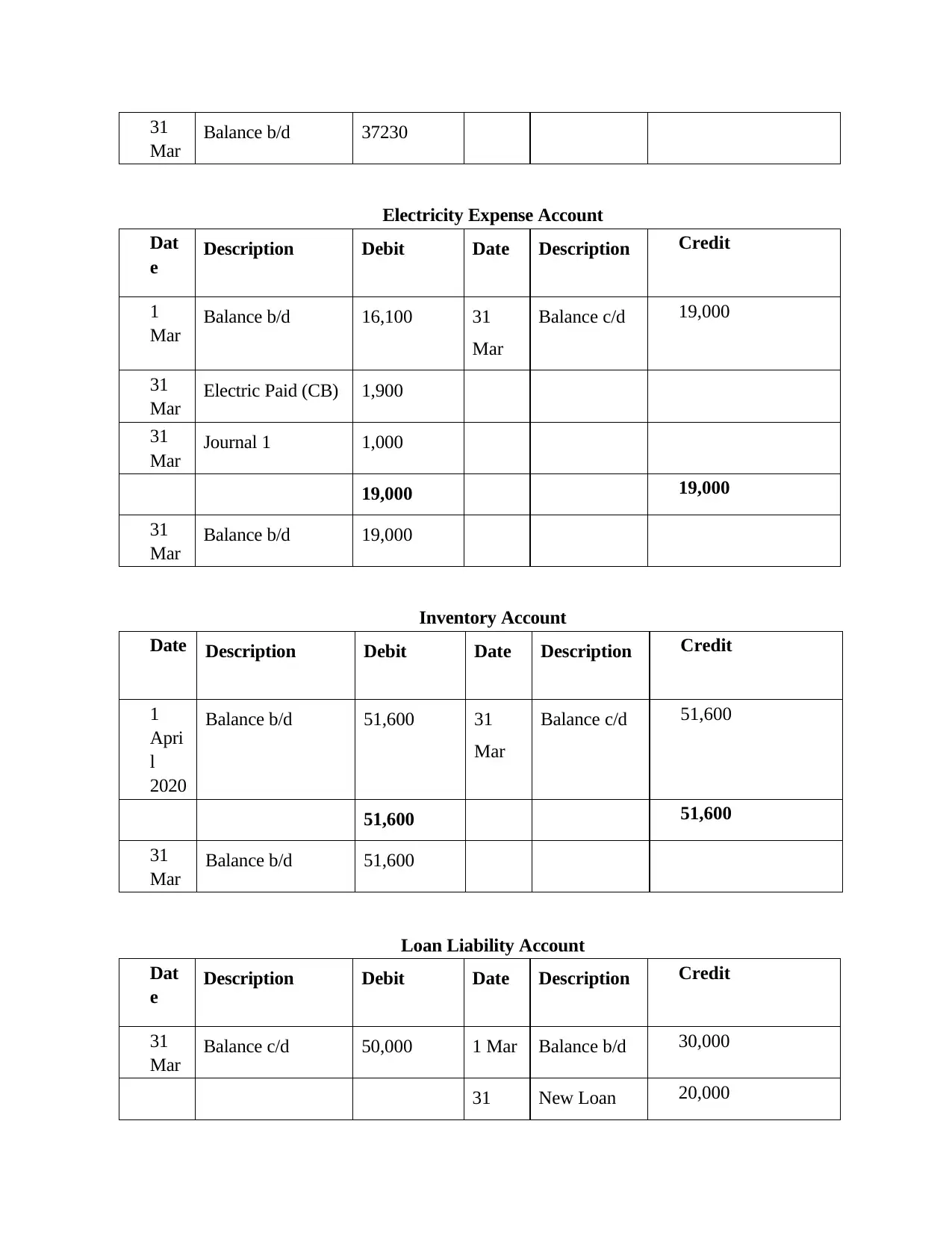

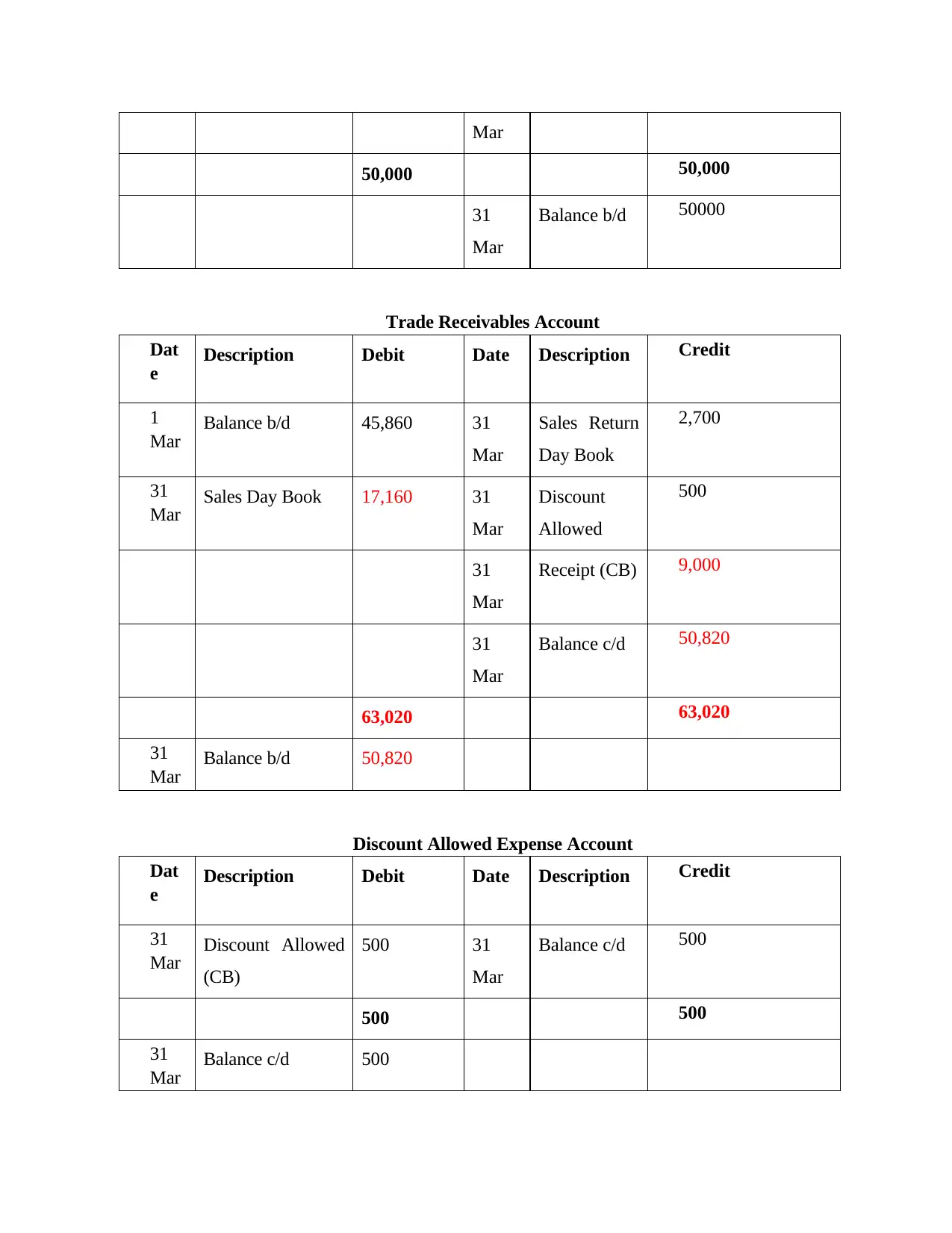

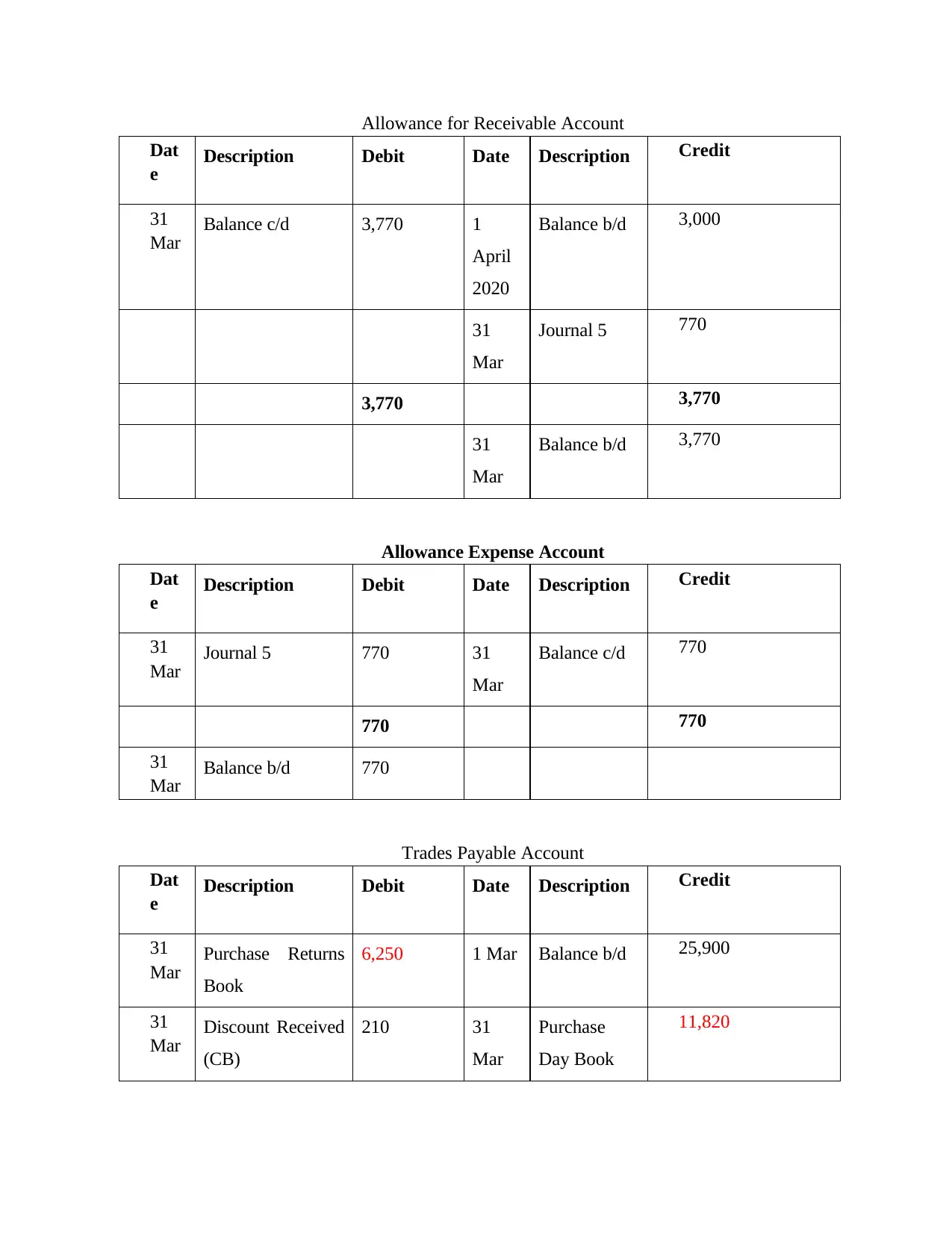

This financial accounting assignment solution meticulously examines the impact of various transactions on a company's financial position and profitability. It begins with an introduction to financial accounting, followed by a detailed analysis of several transactions, including credit and cash sales, purchases, returns, and payments, and their effects on the accounting equation. The assignment further delves into the preparation of sales and purchase day books, cash receipts and payments books, and the journal, illustrating how these records are used to track financial activities. Comprehensive general ledgers for various accounts, such as sales, purchases, wages, and equipment, are presented, along with a trial balance, income statement, and statement of financial position. The solution highlights the importance of accurate record-keeping and the impact of errors, providing a thorough understanding of financial reporting and analysis. The assignment concludes with a statement of financial position, presenting the assets, liabilities, and equity of the company, and an income statement, which summarizes the revenues, expenses, and net profit. The assignment helps students understand the principles of financial accounting.

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.