Financial Accounting Solutions for University Course - Semester 1

VerifiedAdded on 2021/12/16

|16

|2562

|43

Homework Assignment

AI Summary

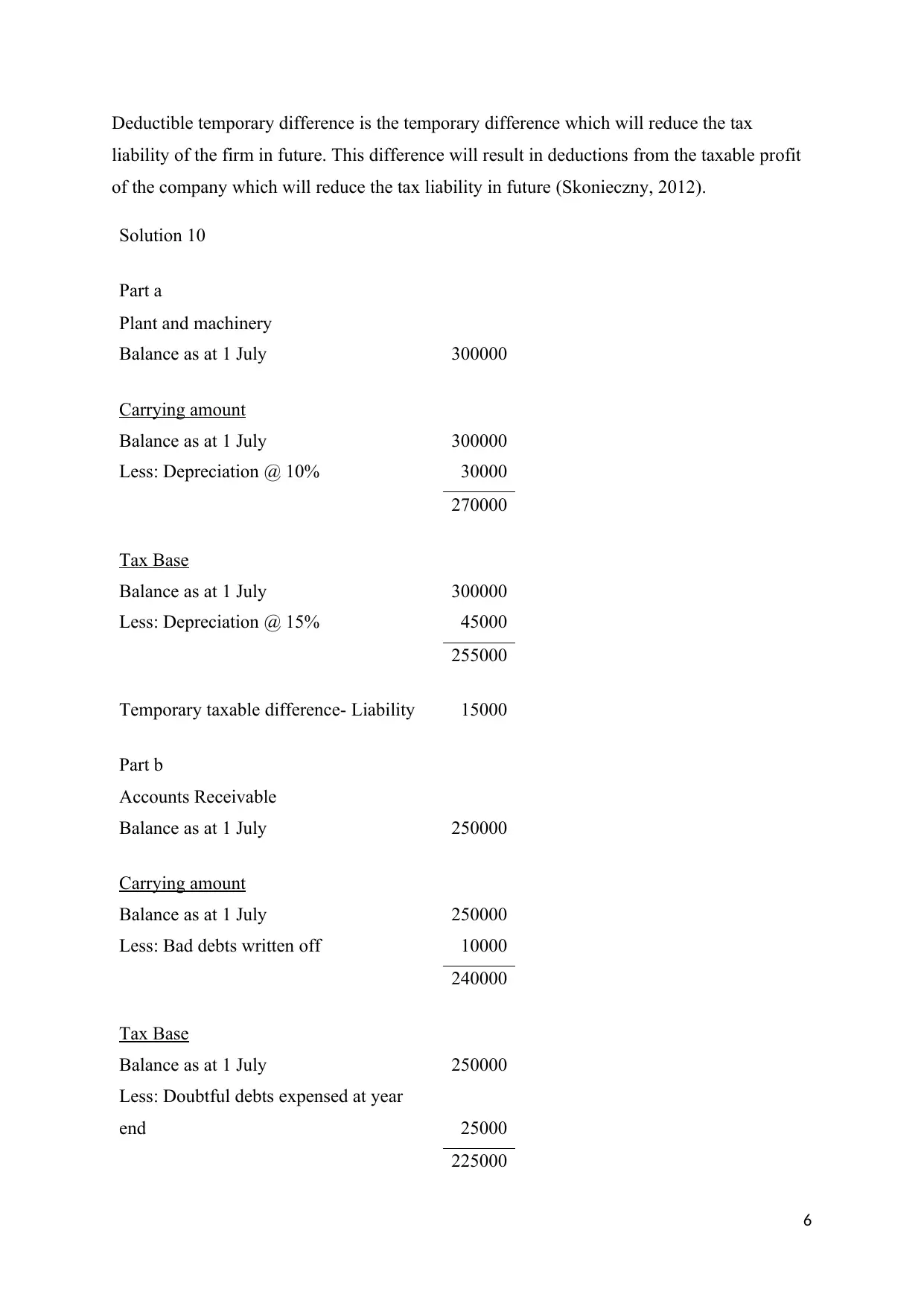

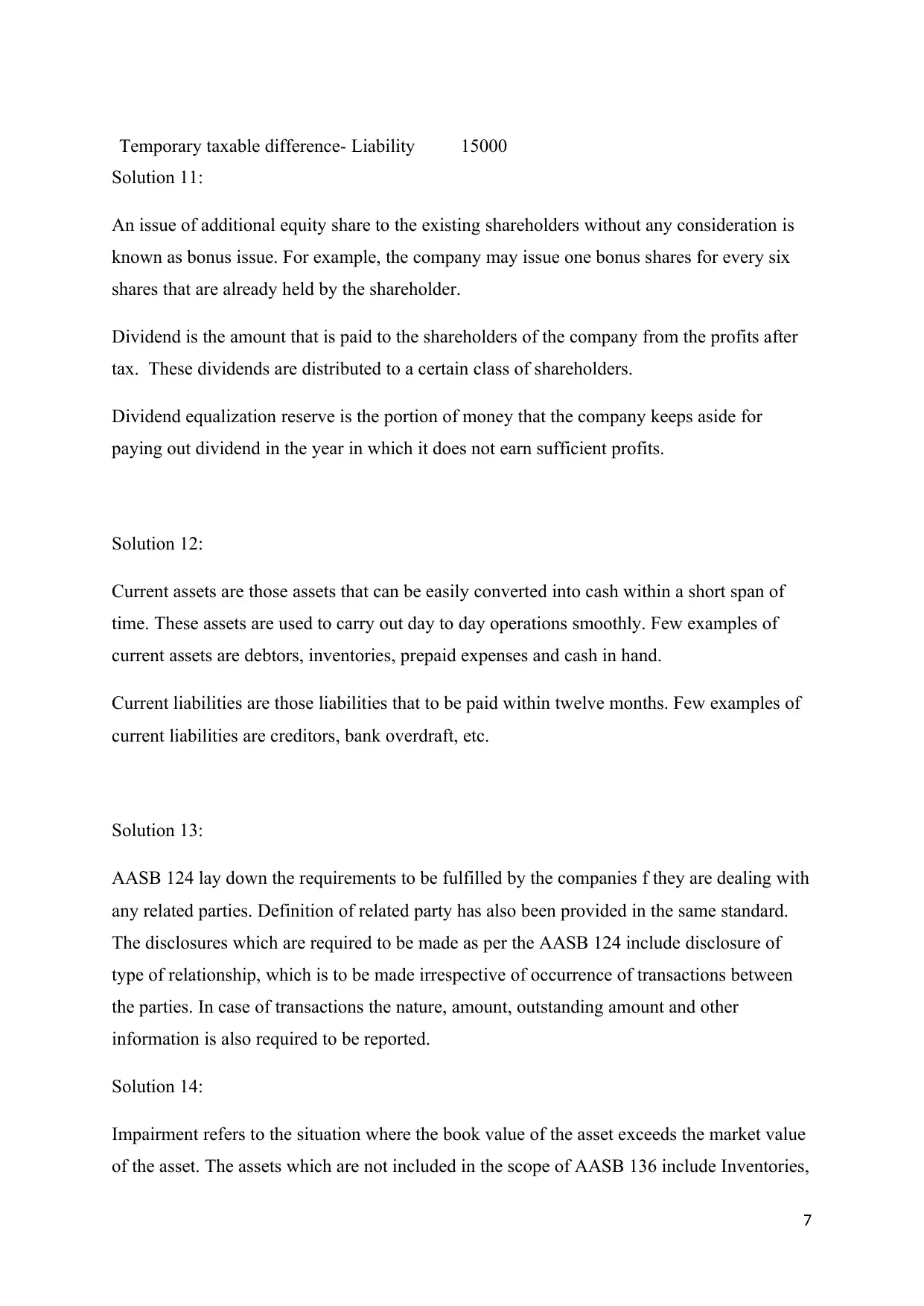

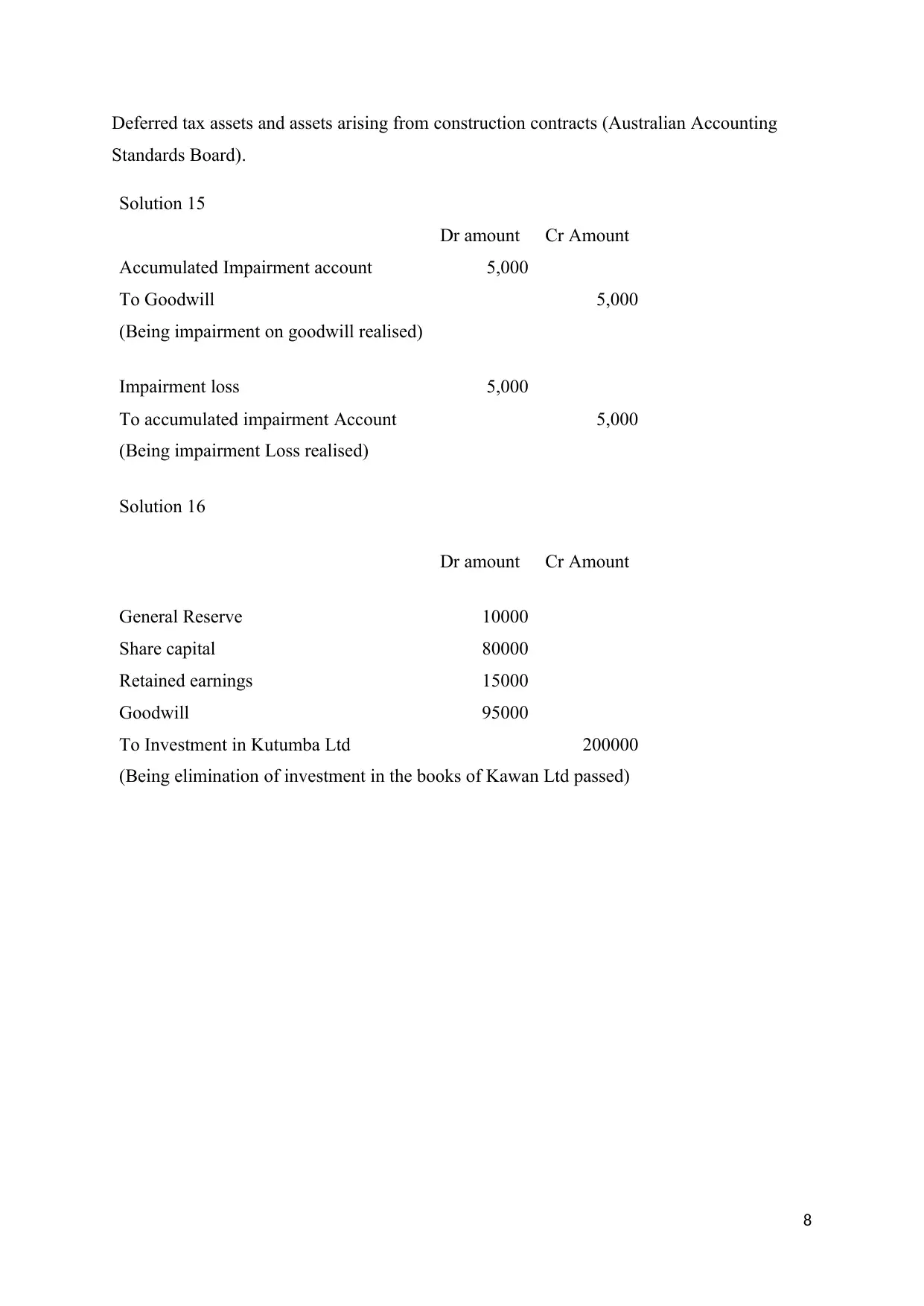

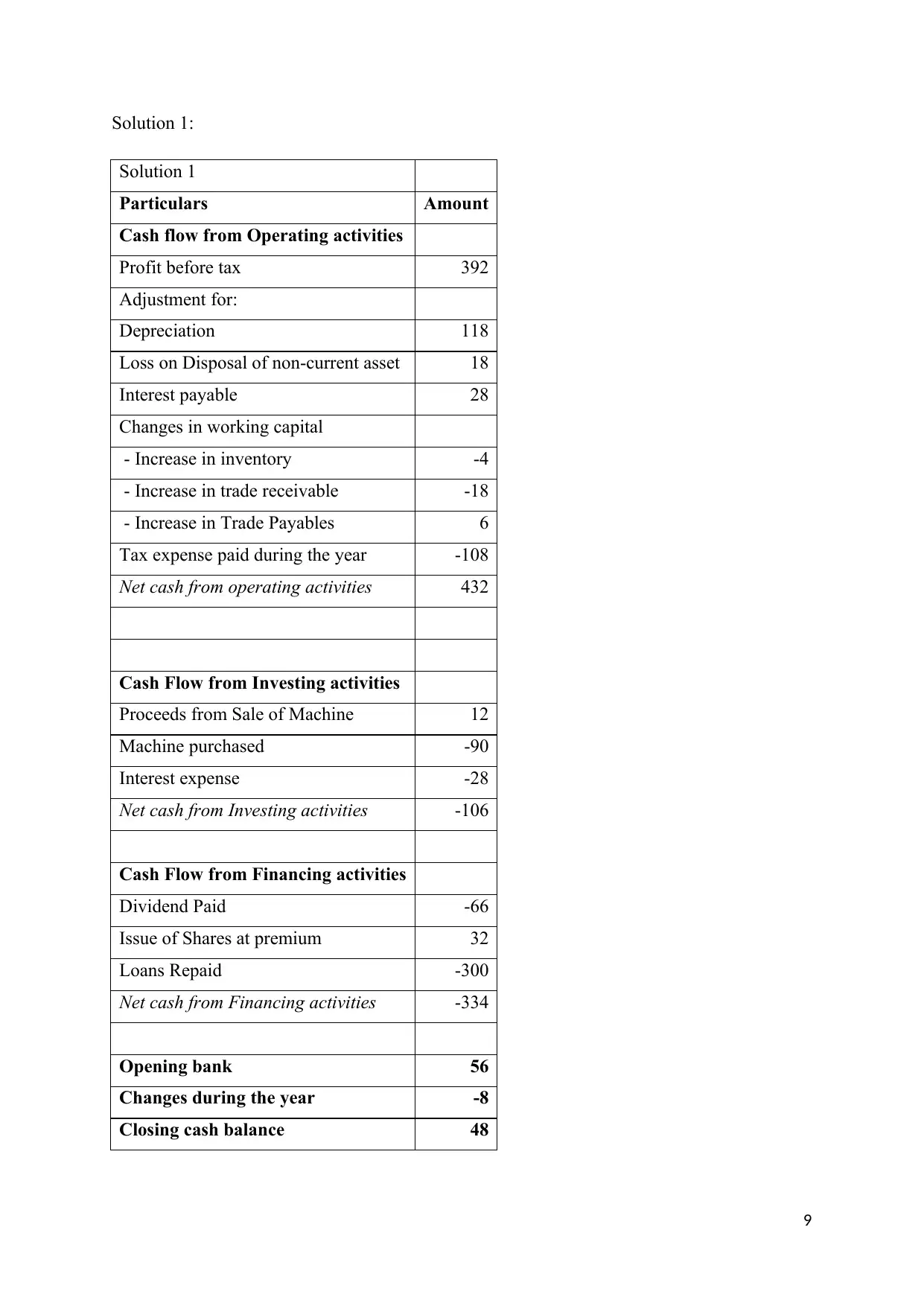

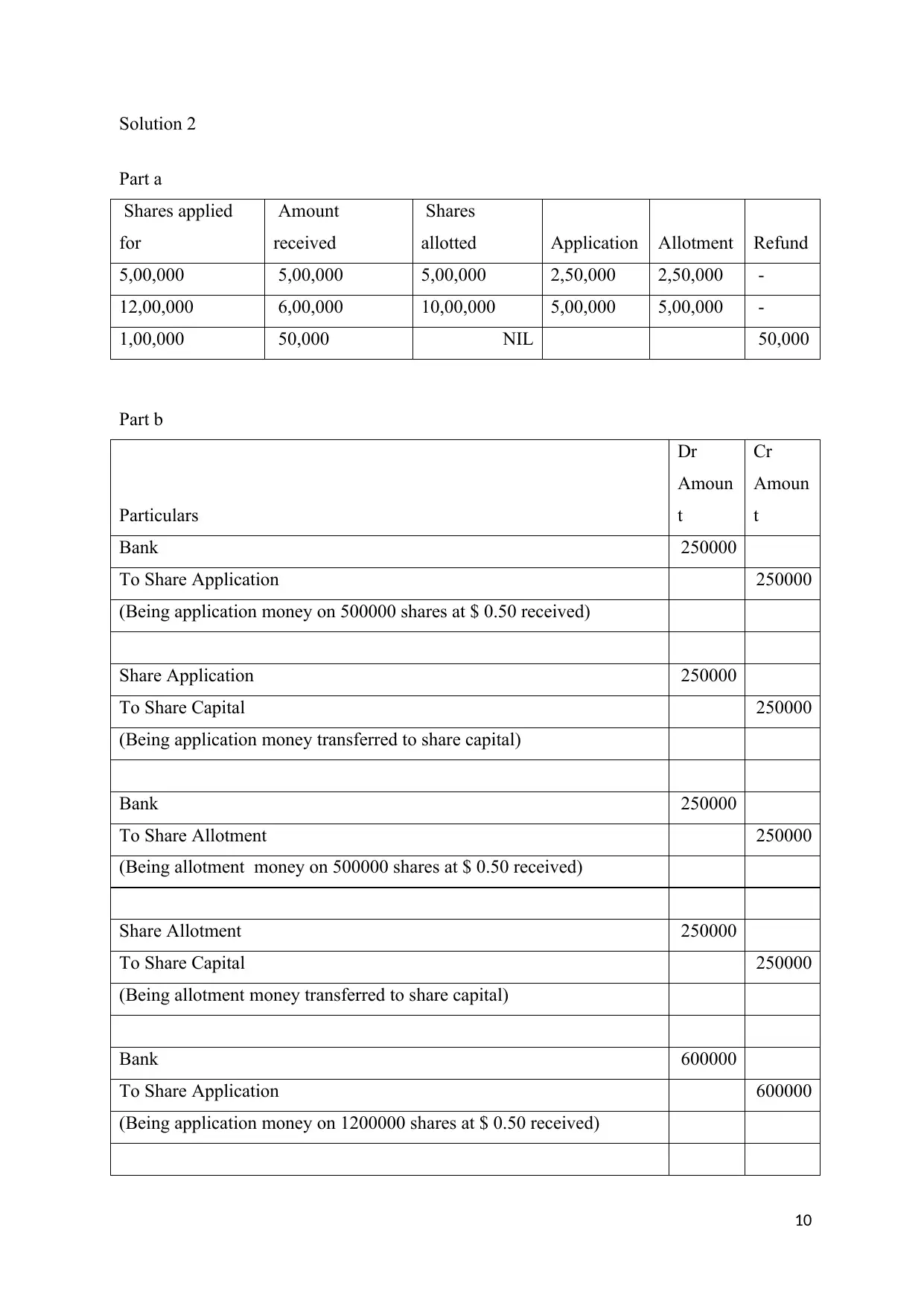

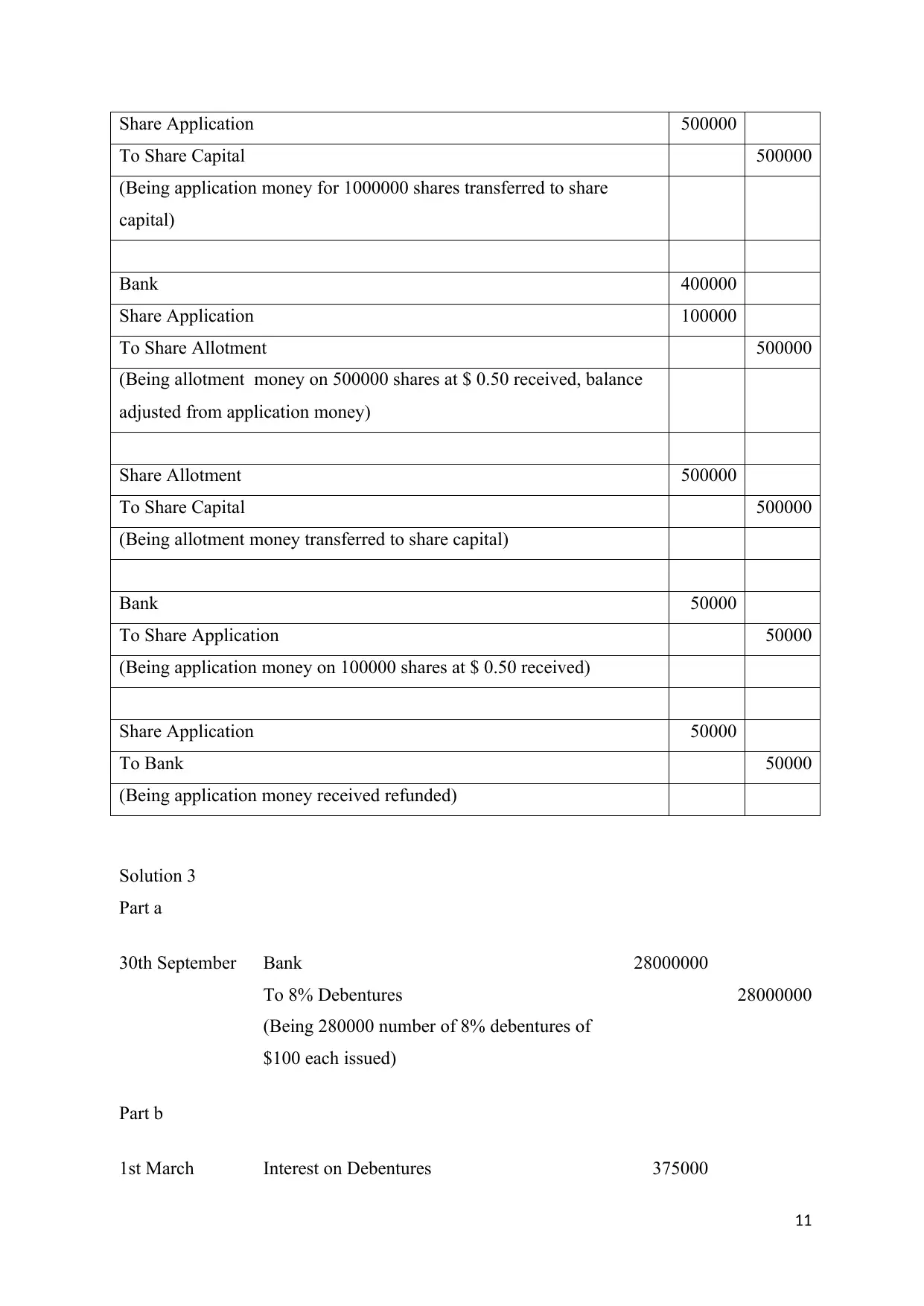

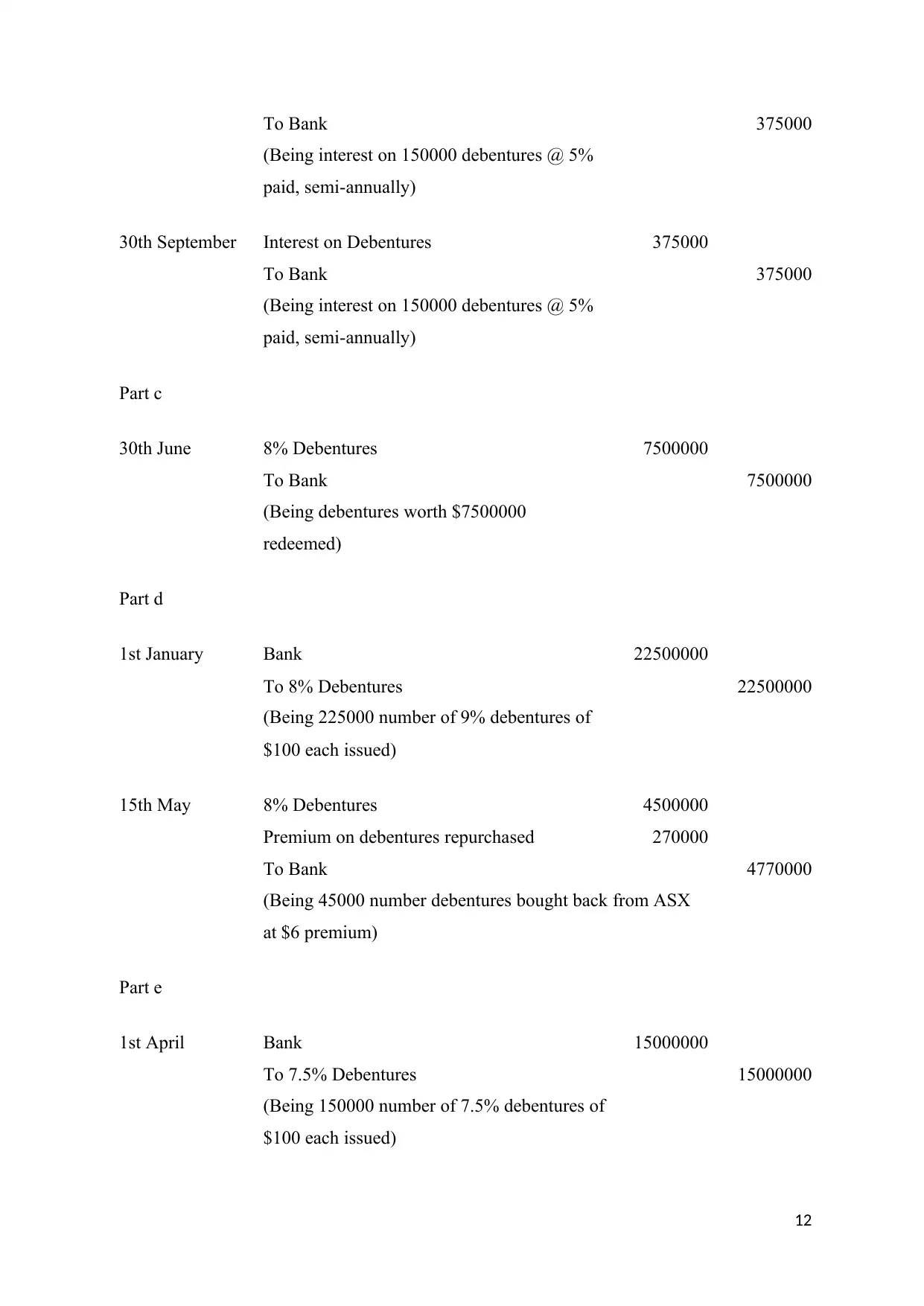

This document presents comprehensive solutions to a financial accounting assignment. It covers a wide range of topics, starting with definitions and explanations of financial statements like the statement of comprehensive income, statement of cash flows, and statement of changes in equity. The solutions delve into different types of business organizations (merchandising, manufacturing, service, governmental, and non-profit) and the application of financial statement elements such as wages expense, cost of goods sold, sales revenue, and various balance sheet items. Furthermore, the assignment addresses the users of financial statements, the concept of goodwill and intangible assets, and accounting for share issues, including unpaid calls. The solutions also include journal entries for debenture issuance, redemption, and interest payments. The document explores temporary differences, bonus issues, dividends, and the classification of current assets and liabilities. It also covers related party disclosures, impairment of assets, and consolidation entries. Finally, it provides detailed solutions to cash flow statements, share application and allotment entries, and debenture-related transactions, including issuance, interest payments, and redemption. The document aims to provide students with detailed understanding of the financial accounting concepts and their practical application.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.