Intermediate Financial Accounting: AASB 137 and AASB 138 Analysis

VerifiedAdded on 2021/05/31

|8

|1053

|28

Homework Assignment

AI Summary

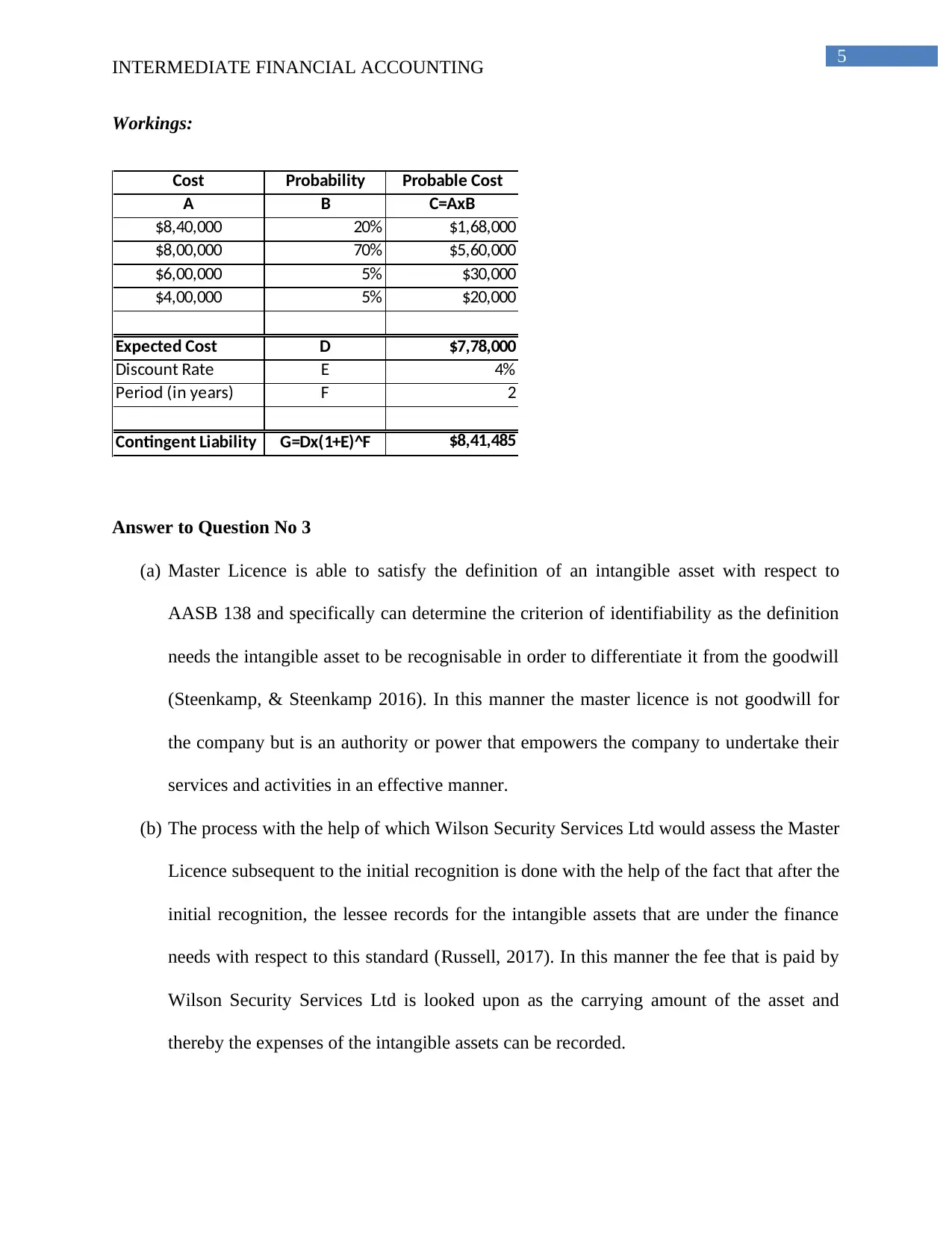

This document presents a comprehensive solution to an intermediate financial accounting assignment. The assignment addresses key concepts including provisions as defined by AASB 137, specifically analyzing a company's obligation to restore a polluted environment and the methods for estimating provision amounts. It then delves into intangible assets, focusing on the definition and recognition of a Master Licence under AASB 138. The solution determines the Master Licence's identifiability, differentiates it from goodwill, and assesses its subsequent measurement. The analysis includes whether the Master Licence has a finite or infinite useful life, considering the license's time frame and renewal possibilities. The document provides detailed workings and a reference list supporting the analysis.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.