Financial Accounting Assignment: Comprehensive Analysis and Reporting

VerifiedAdded on 2022/11/23

|25

|4223

|92

Homework Assignment

AI Summary

This financial accounting assignment solution delves into fundamental concepts and practical applications. It begins with an overview of business transactions, categorizing them as cash/credit and internal/external, and then contrasts single-entry and double-entry accounting systems. The solution includes detailed journal entries, ledger accounts, and a trial balance for a given month, demonstrating the accounting cycle. It further explains financial statements and reports, their purposes, and the various users of financial information. The assignment also covers core accounting principles, such as matching, materiality, cost, accrual, full disclosure, revenue recognition, and going concern. Finally, it presents an income statement illustrating revenue, cost of goods sold, and gross profit calculations, providing a comprehensive understanding of financial accounting principles and their practical application.

FINANCIAL ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION.......................................................................................................................................3

MAIN BODY..............................................................................................................................................3

SCENARIO 1..............................................................................................................................................3

Question 1...............................................................................................................................................3

Question 2...............................................................................................................................................4

Question 3.............................................................................................................................................11

Question 4.............................................................................................................................................12

Question 5.............................................................................................................................................13

Question 6.............................................................................................................................................15

Question 7.............................................................................................................................................17

SCENARIO 2............................................................................................................................................18

Question 1.............................................................................................................................................18

Question 2.............................................................................................................................................19

Question 3.............................................................................................................................................20

Question 4.............................................................................................................................................20

Question 5.............................................................................................................................................22

CONCLUSION.........................................................................................................................................24

REFERENCES..........................................................................................................................................26

INTRODUCTION.......................................................................................................................................3

MAIN BODY..............................................................................................................................................3

SCENARIO 1..............................................................................................................................................3

Question 1...............................................................................................................................................3

Question 2...............................................................................................................................................4

Question 3.............................................................................................................................................11

Question 4.............................................................................................................................................12

Question 5.............................................................................................................................................13

Question 6.............................................................................................................................................15

Question 7.............................................................................................................................................17

SCENARIO 2............................................................................................................................................18

Question 1.............................................................................................................................................18

Question 2.............................................................................................................................................19

Question 3.............................................................................................................................................20

Question 4.............................................................................................................................................20

Question 5.............................................................................................................................................22

CONCLUSION.........................................................................................................................................24

REFERENCES..........................................................................................................................................26

INTRODUCTION

The Financial Accounting refers to the cycle of recording, summing up and dissecting the

financial exchanges to have productive decision making methodology. In the current situation,

there is essential prerequisite to acquire upper hands through creating efficient accounting

procedures for having useful practices in industry to lead the organization from comparative

association. The current report incorporates the depiction in regards to various business

transactions, different types of accounting framework, trail balance, contrast between financial

statements and the reporting along with other basic financial accounting concepts. In addition to

this, it provides an insight into creation of journal, ledger, cash flow statement or the

reconciliation statement.

MAIN BODY

SCENARIO 1

Question 1

Business transactions mainly refers to the exchange of the goods and services among the

two parties which helps in meeting up the desired organizational goals and objectives. The

business transactions can be classified into the two types: which are Cash and credit transactions

and internal and external transactions. The former one involves both cash and credit business

transactions. The event when the cash is paid or received immediately when the transaction

occurs, it is called cash transaction. On the other hand, credit transaction refers to the event when

the cash is not paid or received immediately but the transaction happens and the payment is done

in the future specified date is called as the credit transaction (Business transaction. 2020). The

internal transaction are those business transactions in which there is no external parties involved.

These exchanges don't include in the trading of values between two groups yet the

eventcomprises the exchange is quantifiable in money related terms and effects the monetary

situation of the business. Instances of such exchanges incorporate chronicle devaluation of fixed

resources and understanding the deficiency of resources brought about by fire and so on. On the

other side, external transactions are those which involves exchange of value with the third

parties. Mainly all the transactions excluding internal transactions are external only and accounts

The Financial Accounting refers to the cycle of recording, summing up and dissecting the

financial exchanges to have productive decision making methodology. In the current situation,

there is essential prerequisite to acquire upper hands through creating efficient accounting

procedures for having useful practices in industry to lead the organization from comparative

association. The current report incorporates the depiction in regards to various business

transactions, different types of accounting framework, trail balance, contrast between financial

statements and the reporting along with other basic financial accounting concepts. In addition to

this, it provides an insight into creation of journal, ledger, cash flow statement or the

reconciliation statement.

MAIN BODY

SCENARIO 1

Question 1

Business transactions mainly refers to the exchange of the goods and services among the

two parties which helps in meeting up the desired organizational goals and objectives. The

business transactions can be classified into the two types: which are Cash and credit transactions

and internal and external transactions. The former one involves both cash and credit business

transactions. The event when the cash is paid or received immediately when the transaction

occurs, it is called cash transaction. On the other hand, credit transaction refers to the event when

the cash is not paid or received immediately but the transaction happens and the payment is done

in the future specified date is called as the credit transaction (Business transaction. 2020). The

internal transaction are those business transactions in which there is no external parties involved.

These exchanges don't include in the trading of values between two groups yet the

eventcomprises the exchange is quantifiable in money related terms and effects the monetary

situation of the business. Instances of such exchanges incorporate chronicle devaluation of fixed

resources and understanding the deficiency of resources brought about by fire and so on. On the

other side, external transactions are those which involves exchange of value with the third

parties. Mainly all the transactions excluding internal transactions are external only and accounts

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

for the usual transactions of the business. For instance, purchase of material from suppliers,

utility bills, payment of rent or salaries to employees and so forth.

A single-entry accounting framework records each bookkeeping exchange with a single

section to the bookkeeping records, as opposed to the more normal two-fold section framework.

The single accounting framework is focused on the aftereffects of a business that are accounted

for in the pay proclamation (Single- Vs. Double-Entry Bookkeeping. 2019). The center data

followed in a single-entry framework is cash payment and money receipts. The main form of

recording in this system is the cash book.In double entry bookkeeping accounting, the

transactions are recorded on two sides, debit and credit. This results into maintaining the

accuracy of the bookkeeping, reducing errors and omissions.it is used by all the business

organizations.

The trial balance refers to the statement which provides the balancing figures of all the

ledger accounts (Trial Balance. 2020). The main purpose behind creating trial balance is to

ensure mathematical accuracy. This is further used for the purpose of creating the financial

statements which involves the income statement, balance sheet, cash flow statement.

Question 2

1. Journal Entries for the month of June 2016

Date Particulars L.F Debit Credit

1-Jun Cash A/C Dr. 65000

To Capital A/C 65000

(Being capital invested for

starting company)

2-Jun Purchase A/C Dr. 8000

To Trade payables A/C 8000

(Being goods purchased on

credit)

7-Jun Cash A/C Dr. 4000

To Sales A/C 4000

utility bills, payment of rent or salaries to employees and so forth.

A single-entry accounting framework records each bookkeeping exchange with a single

section to the bookkeeping records, as opposed to the more normal two-fold section framework.

The single accounting framework is focused on the aftereffects of a business that are accounted

for in the pay proclamation (Single- Vs. Double-Entry Bookkeeping. 2019). The center data

followed in a single-entry framework is cash payment and money receipts. The main form of

recording in this system is the cash book.In double entry bookkeeping accounting, the

transactions are recorded on two sides, debit and credit. This results into maintaining the

accuracy of the bookkeeping, reducing errors and omissions.it is used by all the business

organizations.

The trial balance refers to the statement which provides the balancing figures of all the

ledger accounts (Trial Balance. 2020). The main purpose behind creating trial balance is to

ensure mathematical accuracy. This is further used for the purpose of creating the financial

statements which involves the income statement, balance sheet, cash flow statement.

Question 2

1. Journal Entries for the month of June 2016

Date Particulars L.F Debit Credit

1-Jun Cash A/C Dr. 65000

To Capital A/C 65000

(Being capital invested for

starting company)

2-Jun Purchase A/C Dr. 8000

To Trade payables A/C 8000

(Being goods purchased on

credit)

7-Jun Cash A/C Dr. 4000

To Sales A/C 4000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

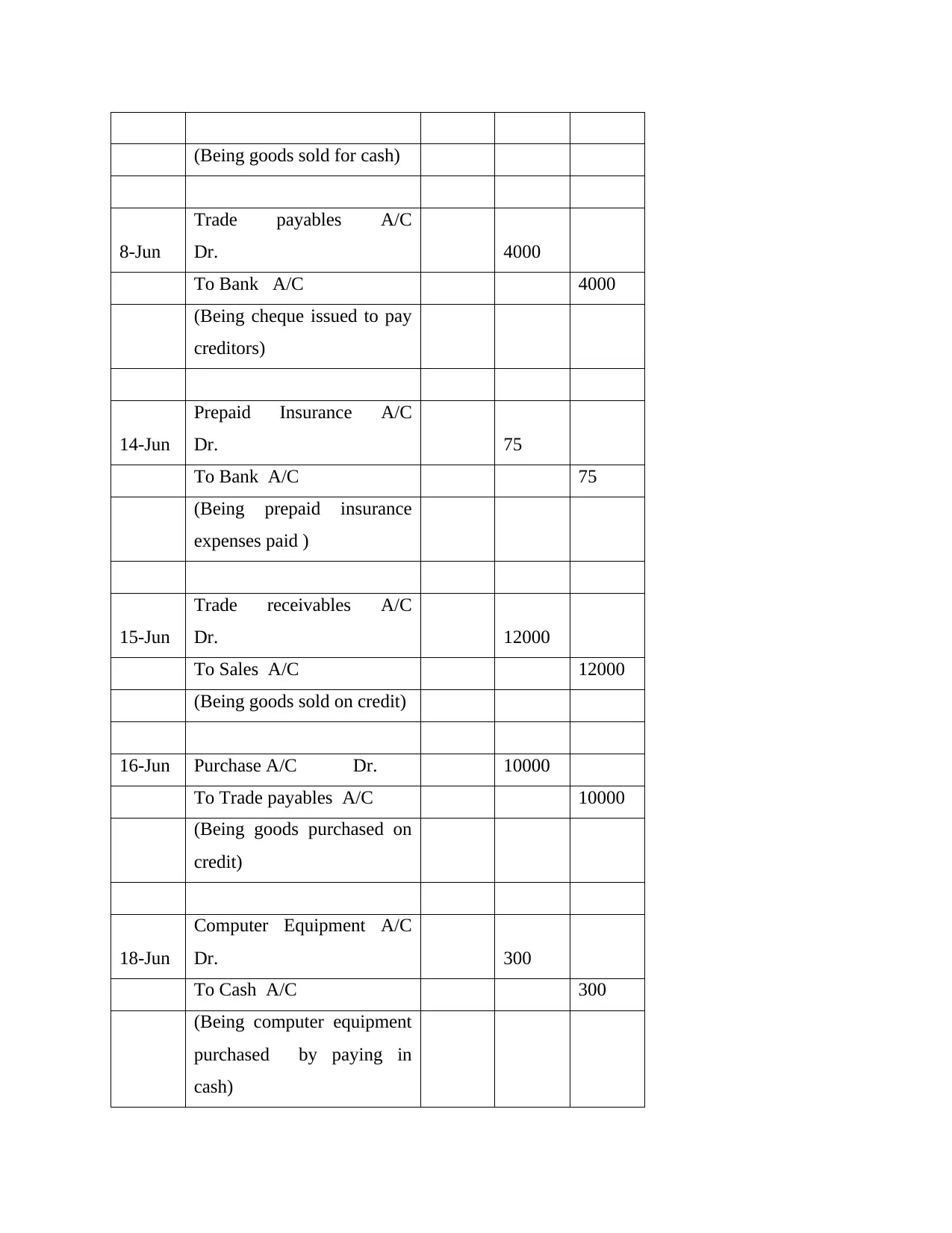

(Being goods sold for cash)

8-Jun

Trade payables A/C

Dr. 4000

To Bank A/C 4000

(Being cheque issued to pay

creditors)

14-Jun

Prepaid Insurance A/C

Dr. 75

To Bank A/C 75

(Being prepaid insurance

expenses paid )

15-Jun

Trade receivables A/C

Dr. 12000

To Sales A/C 12000

(Being goods sold on credit)

16-Jun Purchase A/C Dr. 10000

To Trade payables A/C 10000

(Being goods purchased on

credit)

18-Jun

Computer Equipment A/C

Dr. 300

To Cash A/C 300

(Being computer equipment

purchased by paying in

cash)

8-Jun

Trade payables A/C

Dr. 4000

To Bank A/C 4000

(Being cheque issued to pay

creditors)

14-Jun

Prepaid Insurance A/C

Dr. 75

To Bank A/C 75

(Being prepaid insurance

expenses paid )

15-Jun

Trade receivables A/C

Dr. 12000

To Sales A/C 12000

(Being goods sold on credit)

16-Jun Purchase A/C Dr. 10000

To Trade payables A/C 10000

(Being goods purchased on

credit)

18-Jun

Computer Equipment A/C

Dr. 300

To Cash A/C 300

(Being computer equipment

purchased by paying in

cash)

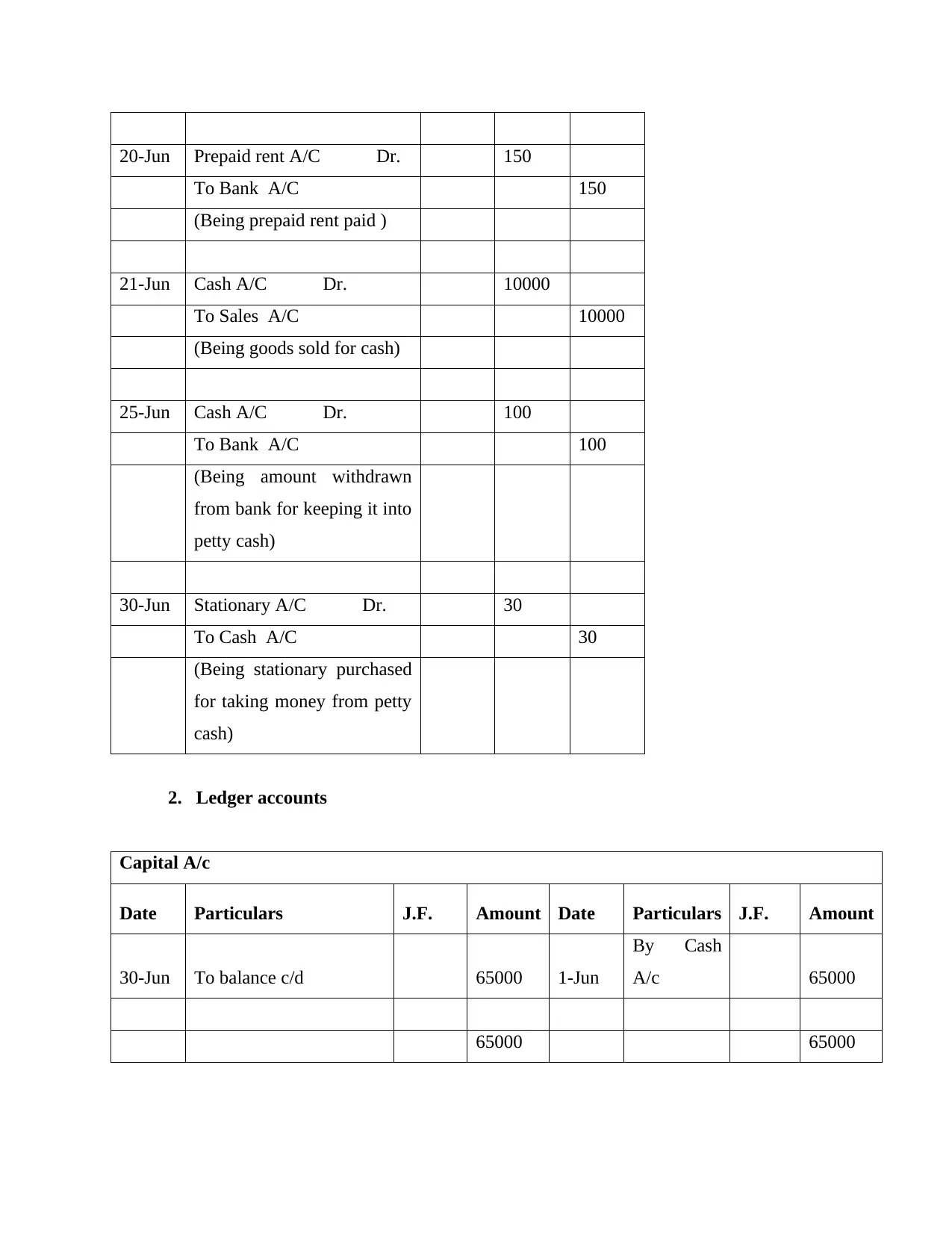

20-Jun Prepaid rent A/C Dr. 150

To Bank A/C 150

(Being prepaid rent paid )

21-Jun Cash A/C Dr. 10000

To Sales A/C 10000

(Being goods sold for cash)

25-Jun Cash A/C Dr. 100

To Bank A/C 100

(Being amount withdrawn

from bank for keeping it into

petty cash)

30-Jun Stationary A/C Dr. 30

To Cash A/C 30

(Being stationary purchased

for taking money from petty

cash)

2. Ledger accounts

Capital A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

30-Jun To balance c/d 65000 1-Jun

By Cash

A/c 65000

65000 65000

To Bank A/C 150

(Being prepaid rent paid )

21-Jun Cash A/C Dr. 10000

To Sales A/C 10000

(Being goods sold for cash)

25-Jun Cash A/C Dr. 100

To Bank A/C 100

(Being amount withdrawn

from bank for keeping it into

petty cash)

30-Jun Stationary A/C Dr. 30

To Cash A/C 30

(Being stationary purchased

for taking money from petty

cash)

2. Ledger accounts

Capital A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

30-Jun To balance c/d 65000 1-Jun

By Cash

A/c 65000

65000 65000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

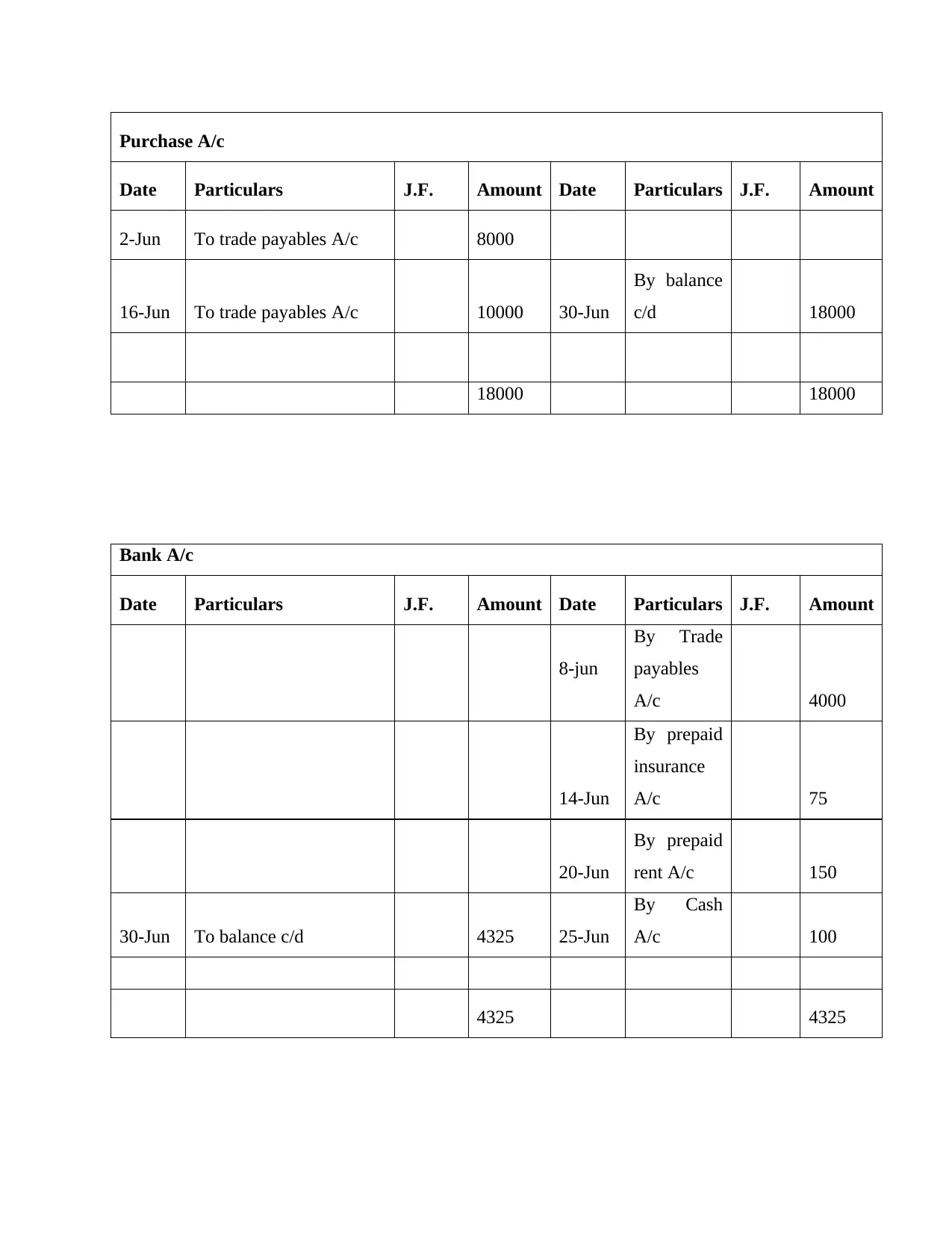

Purchase A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

2-Jun To trade payables A/c 8000

16-Jun To trade payables A/c 10000 30-Jun

By balance

c/d 18000

18000 18000

Bank A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

8-jun

By Trade

payables

A/c 4000

14-Jun

By prepaid

insurance

A/c 75

20-Jun

By prepaid

rent A/c 150

30-Jun To balance c/d 4325 25-Jun

By Cash

A/c 100

4325 4325

Date Particulars J.F. Amount Date Particulars J.F. Amount

2-Jun To trade payables A/c 8000

16-Jun To trade payables A/c 10000 30-Jun

By balance

c/d 18000

18000 18000

Bank A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

8-jun

By Trade

payables

A/c 4000

14-Jun

By prepaid

insurance

A/c 75

20-Jun

By prepaid

rent A/c 150

30-Jun To balance c/d 4325 25-Jun

By Cash

A/c 100

4325 4325

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

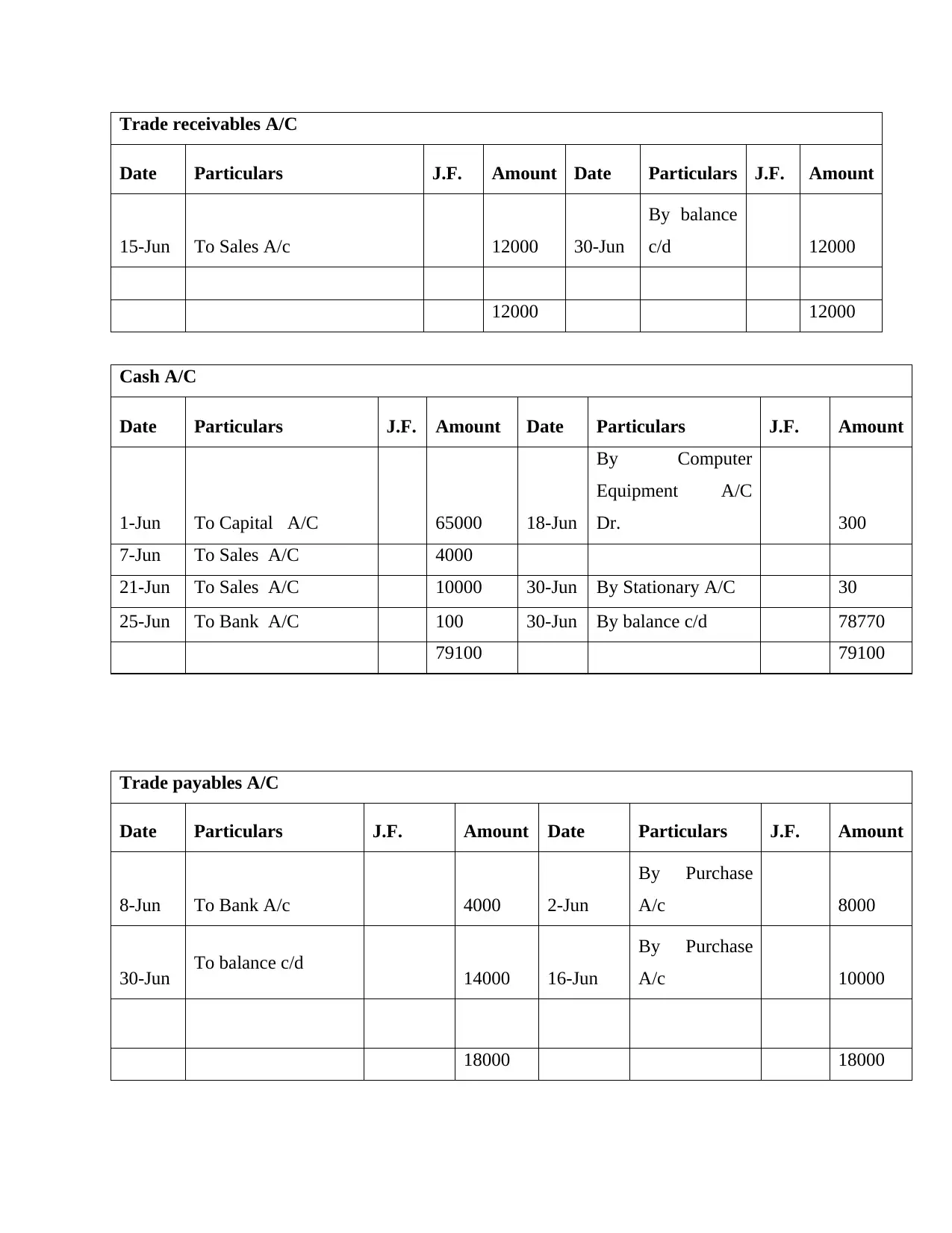

Trade receivables A/C

Date Particulars J.F. Amount Date Particulars J.F. Amount

15-Jun To Sales A/c 12000 30-Jun

By balance

c/d 12000

12000 12000

Cash A/C

Date Particulars J.F. Amount Date Particulars J.F. Amount

1-Jun To Capital A/C 65000 18-Jun

By Computer

Equipment A/C

Dr. 300

7-Jun To Sales A/C 4000

21-Jun To Sales A/C 10000 30-Jun By Stationary A/C 30

25-Jun To Bank A/C 100 30-Jun By balance c/d 78770

79100 79100

Trade payables A/C

Date Particulars J.F. Amount Date Particulars J.F. Amount

8-Jun To Bank A/c 4000 2-Jun

By Purchase

A/c 8000

30-Jun To balance c/d 14000 16-Jun

By Purchase

A/c 10000

18000 18000

Date Particulars J.F. Amount Date Particulars J.F. Amount

15-Jun To Sales A/c 12000 30-Jun

By balance

c/d 12000

12000 12000

Cash A/C

Date Particulars J.F. Amount Date Particulars J.F. Amount

1-Jun To Capital A/C 65000 18-Jun

By Computer

Equipment A/C

Dr. 300

7-Jun To Sales A/C 4000

21-Jun To Sales A/C 10000 30-Jun By Stationary A/C 30

25-Jun To Bank A/C 100 30-Jun By balance c/d 78770

79100 79100

Trade payables A/C

Date Particulars J.F. Amount Date Particulars J.F. Amount

8-Jun To Bank A/c 4000 2-Jun

By Purchase

A/c 8000

30-Jun To balance c/d 14000 16-Jun

By Purchase

A/c 10000

18000 18000

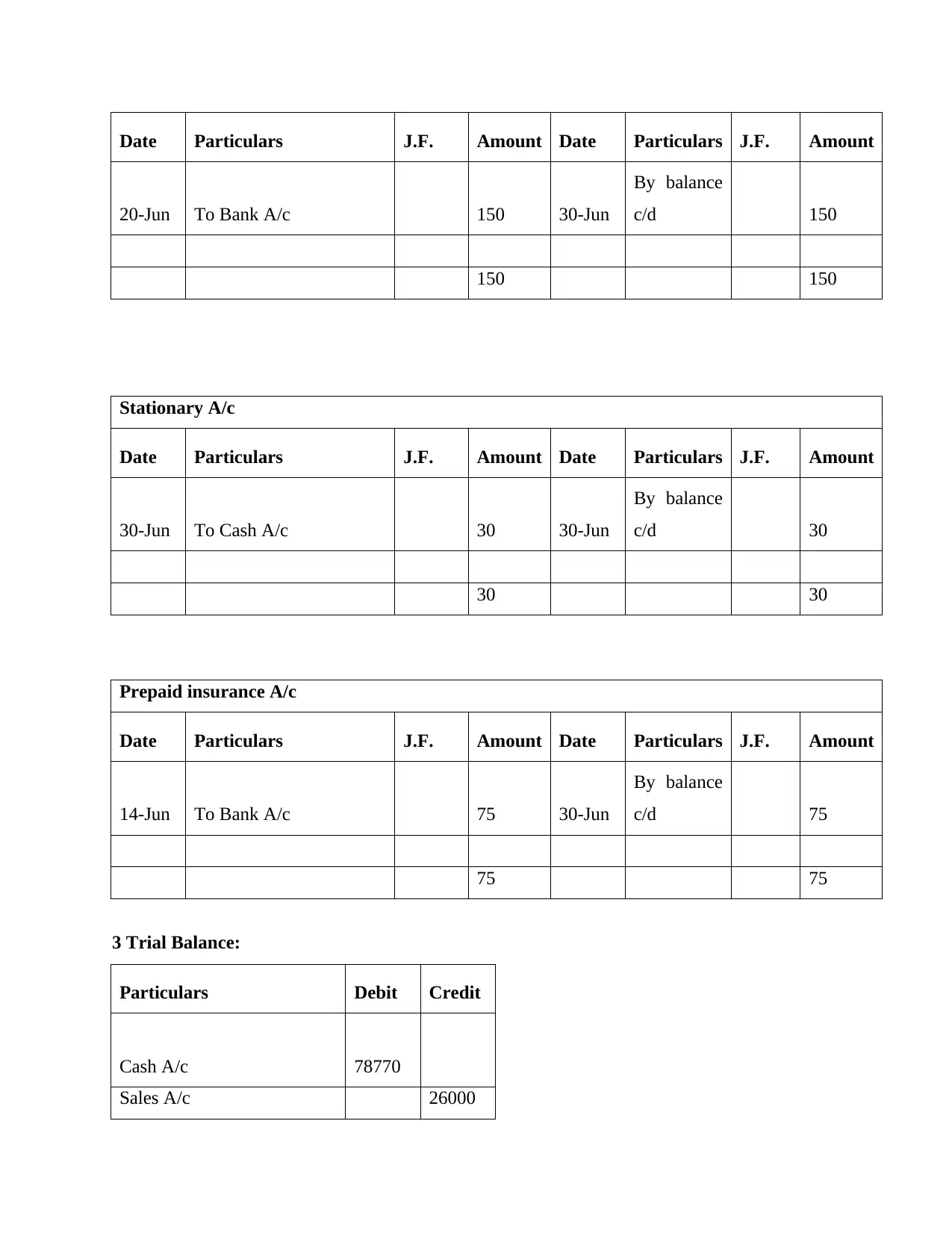

Sales A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

7-Jun

By Cash

A/c 4000

15-Jun

By trade

receivables

A/c 12000

30-Jun To balance c/d 26000 21-Jun

By Cash

A/c 10000

26000 26000

Computer Equipment A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

18-Jun To Cash A/c 300 30-Jun

By balance

c/d 300

300 300

Prepaid Rent A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

7-Jun

By Cash

A/c 4000

15-Jun

By trade

receivables

A/c 12000

30-Jun To balance c/d 26000 21-Jun

By Cash

A/c 10000

26000 26000

Computer Equipment A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

18-Jun To Cash A/c 300 30-Jun

By balance

c/d 300

300 300

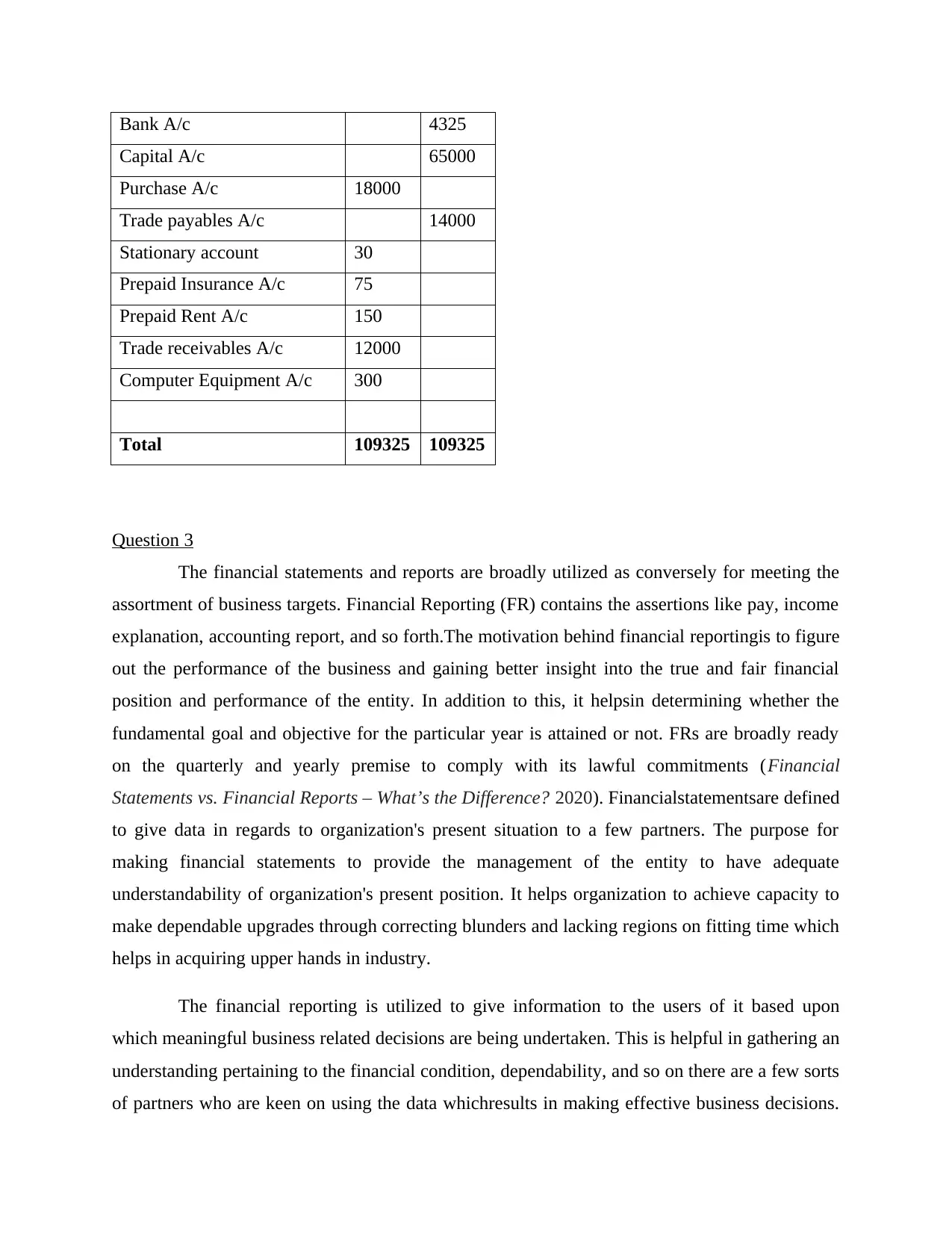

Prepaid Rent A/c

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Date Particulars J.F. Amount Date Particulars J.F. Amount

20-Jun To Bank A/c 150 30-Jun

By balance

c/d 150

150 150

Stationary A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

30-Jun To Cash A/c 30 30-Jun

By balance

c/d 30

30 30

Prepaid insurance A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

14-Jun To Bank A/c 75 30-Jun

By balance

c/d 75

75 75

3 Trial Balance:

Particulars Debit Credit

Cash A/c 78770

Sales A/c 26000

20-Jun To Bank A/c 150 30-Jun

By balance

c/d 150

150 150

Stationary A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

30-Jun To Cash A/c 30 30-Jun

By balance

c/d 30

30 30

Prepaid insurance A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

14-Jun To Bank A/c 75 30-Jun

By balance

c/d 75

75 75

3 Trial Balance:

Particulars Debit Credit

Cash A/c 78770

Sales A/c 26000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Bank A/c 4325

Capital A/c 65000

Purchase A/c 18000

Trade payables A/c 14000

Stationary account 30

Prepaid Insurance A/c 75

Prepaid Rent A/c 150

Trade receivables A/c 12000

Computer Equipment A/c 300

Total 109325 109325

Question 3

The financial statements and reports are broadly utilized as conversely for meeting the

assortment of business targets. Financial Reporting (FR) contains the assertions like pay, income

explanation, accounting report, and so forth.The motivation behind financial reportingis to figure

out the performance of the business and gaining better insight into the true and fair financial

position and performance of the entity. In addition to this, it helpsin determining whether the

fundamental goal and objective for the particular year is attained or not. FRs are broadly ready

on the quarterly and yearly premise to comply with its lawful commitments (Financial

Statements vs. Financial Reports – What’s the Difference? 2020). Financialstatementsare defined

to give data in regards to organization's present situation to a few partners. The purpose for

making financial statements to provide the management of the entity to have adequate

understandability of organization's present position. It helps organization to achieve capacity to

make dependable upgrades through correcting blunders and lacking regions on fitting time which

helps in acquiring upper hands in industry.

The financial reporting is utilized to give information to the users of it based upon

which meaningful business related decisions are being undertaken. This is helpful in gathering an

understanding pertaining to the financial condition, dependability, and so on there are a few sorts

of partners who are keen on using the data whichresults in making effective business decisions.

Capital A/c 65000

Purchase A/c 18000

Trade payables A/c 14000

Stationary account 30

Prepaid Insurance A/c 75

Prepaid Rent A/c 150

Trade receivables A/c 12000

Computer Equipment A/c 300

Total 109325 109325

Question 3

The financial statements and reports are broadly utilized as conversely for meeting the

assortment of business targets. Financial Reporting (FR) contains the assertions like pay, income

explanation, accounting report, and so forth.The motivation behind financial reportingis to figure

out the performance of the business and gaining better insight into the true and fair financial

position and performance of the entity. In addition to this, it helpsin determining whether the

fundamental goal and objective for the particular year is attained or not. FRs are broadly ready

on the quarterly and yearly premise to comply with its lawful commitments (Financial

Statements vs. Financial Reports – What’s the Difference? 2020). Financialstatementsare defined

to give data in regards to organization's present situation to a few partners. The purpose for

making financial statements to provide the management of the entity to have adequate

understandability of organization's present position. It helps organization to achieve capacity to

make dependable upgrades through correcting blunders and lacking regions on fitting time which

helps in acquiring upper hands in industry.

The financial reporting is utilized to give information to the users of it based upon

which meaningful business related decisions are being undertaken. This is helpful in gathering an

understanding pertaining to the financial condition, dependability, and so on there are a few sorts

of partners who are keen on using the data whichresults in making effective business decisions.

There are number of users of the financial reports which are both internal and external to the

business. They are all together called as the stakeholders of the company. The users of the

financial reportcomprise of representatives, proprietors, suppliers, vendors, financial backers,

financial organizations, analyst, banks, customers, government organizations and so on, that are

identified with either interior or outer business environment. The primary motivation behind

financial institution like banks is to used given data is to have capacity to detail compelling

dynamic.

Question 4

Accounting principles are important for the smooth functioning of enterprise so that

effectual decision making can be exerted by company for formulating systematic procedure. The

accounting principles give guidance to company for having desirable financial health. It includes

accrual, matching, conservatism, materiality, etc.

Matching principle is concerned with recording expenses of company at the same time

when the revenue has been generated (Kimmel, Weygandt and Kieso, 2018). It is one of

the most important fundamental principle that gives instructions to organization that there

should be appropriate balance in these both in order accurate position of liquidity can be

ascertained. It gives several benefits like smooth and organized business processing with

significant knowledge of in and out going.

Materiality Principle says that accountings standard can be neglected if does not have

much impact on the processing of company. The purpose behind this is to make

organizational processing effectual and smooth through removing irrelevant obstacles via

reducing inappropriate practices. It is basically related with making business aware of

recording all information that can make the financial statement material. It helps

company to gain trustworthiness and effectiveness in industry.

Cost principle states that assets should be recorde at the sometime when it has acquired to

get significant alertness of actual amount spend on that. There is guidance to avoid

considering market value through executing changes in busies practices transaction. It is

concerned with taking all expenses which are actually incurred in particular period of

time. This gives properly instructions to have information regarding the current

requirements of funds.

business. They are all together called as the stakeholders of the company. The users of the

financial reportcomprise of representatives, proprietors, suppliers, vendors, financial backers,

financial organizations, analyst, banks, customers, government organizations and so on, that are

identified with either interior or outer business environment. The primary motivation behind

financial institution like banks is to used given data is to have capacity to detail compelling

dynamic.

Question 4

Accounting principles are important for the smooth functioning of enterprise so that

effectual decision making can be exerted by company for formulating systematic procedure. The

accounting principles give guidance to company for having desirable financial health. It includes

accrual, matching, conservatism, materiality, etc.

Matching principle is concerned with recording expenses of company at the same time

when the revenue has been generated (Kimmel, Weygandt and Kieso, 2018). It is one of

the most important fundamental principle that gives instructions to organization that there

should be appropriate balance in these both in order accurate position of liquidity can be

ascertained. It gives several benefits like smooth and organized business processing with

significant knowledge of in and out going.

Materiality Principle says that accountings standard can be neglected if does not have

much impact on the processing of company. The purpose behind this is to make

organizational processing effectual and smooth through removing irrelevant obstacles via

reducing inappropriate practices. It is basically related with making business aware of

recording all information that can make the financial statement material. It helps

company to gain trustworthiness and effectiveness in industry.

Cost principle states that assets should be recorde at the sometime when it has acquired to

get significant alertness of actual amount spend on that. There is guidance to avoid

considering market value through executing changes in busies practices transaction. It is

concerned with taking all expenses which are actually incurred in particular period of

time. This gives properly instructions to have information regarding the current

requirements of funds.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.