Financial Accounting Homework: Consolidation, Cash Flow and IFRS

VerifiedAdded on 2022/12/28

|11

|2045

|2

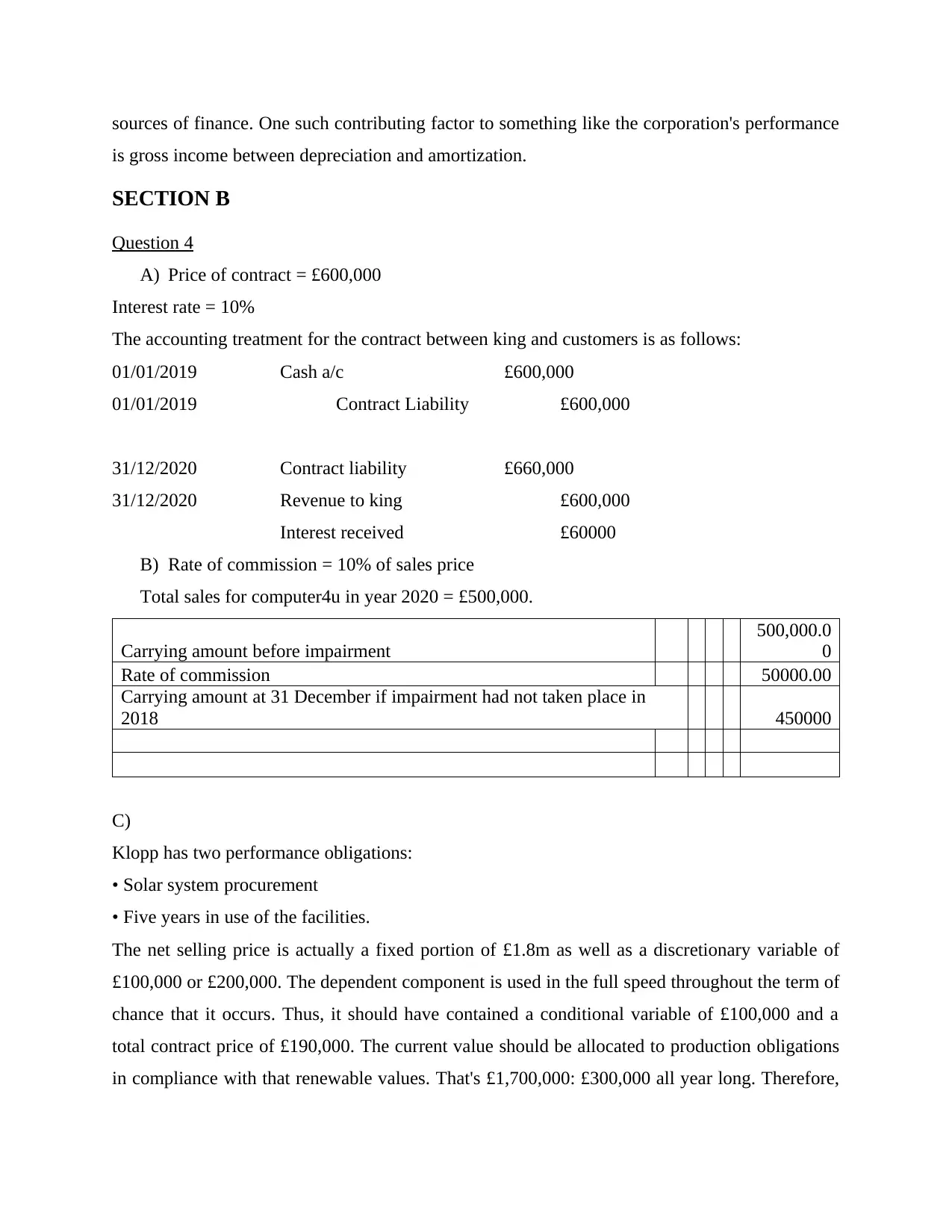

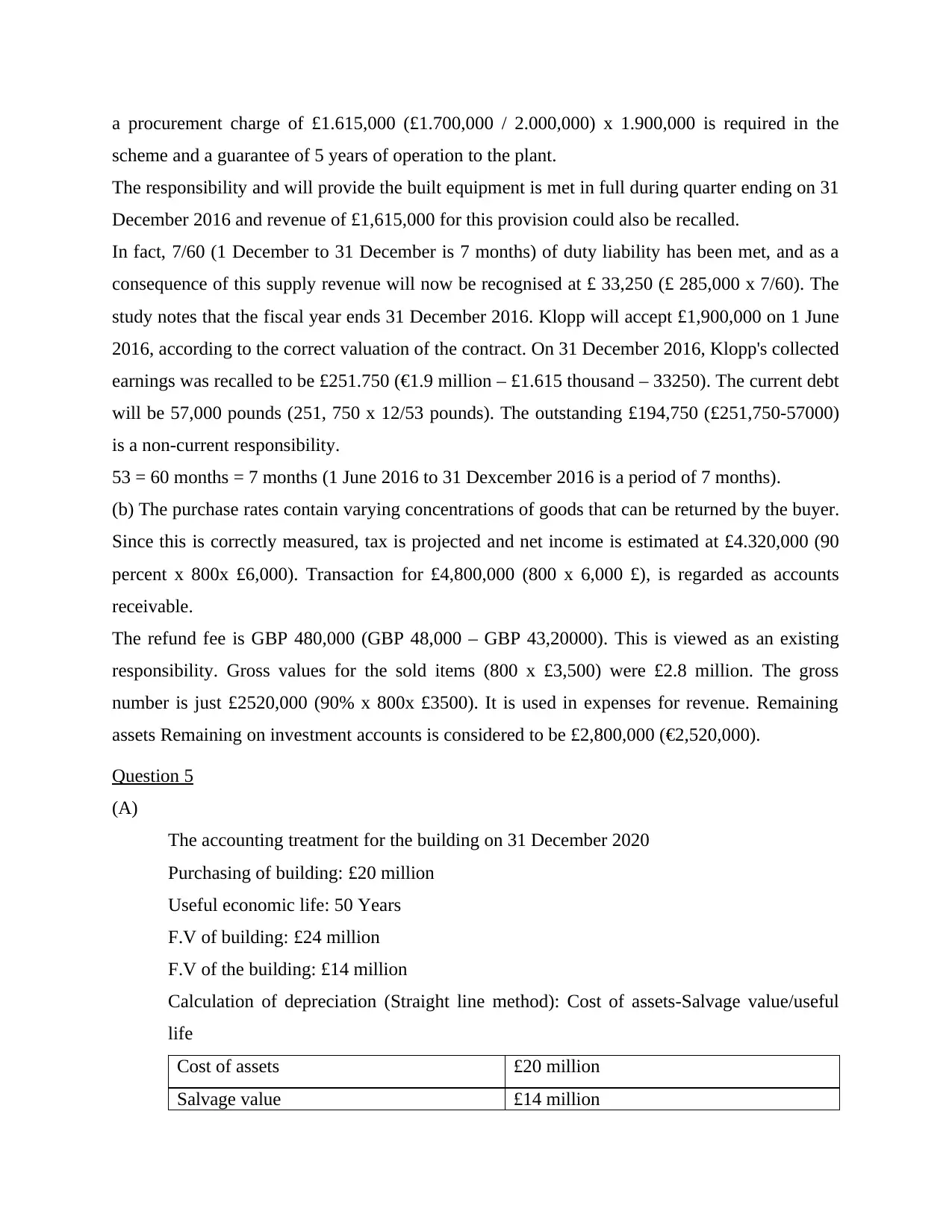

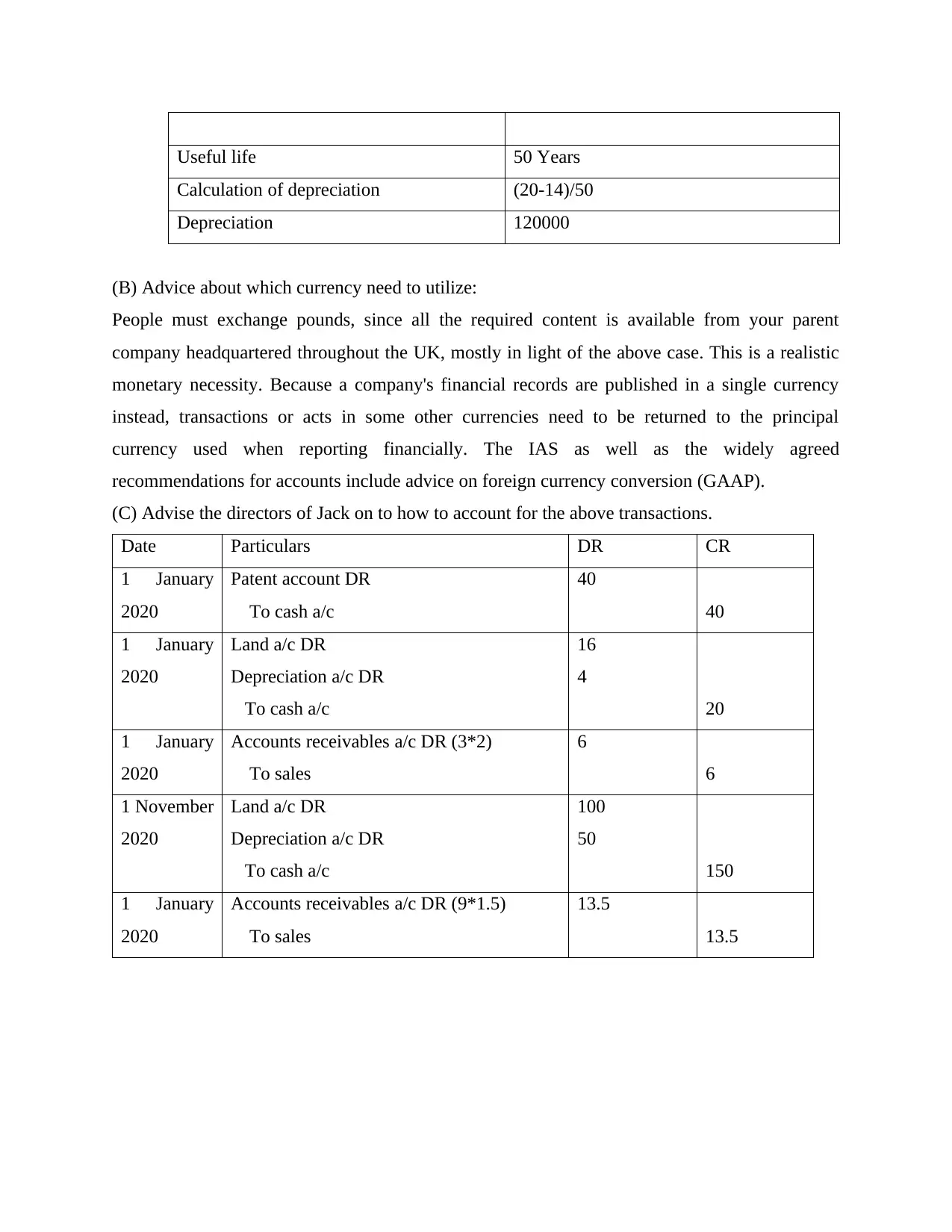

Homework Assignment

AI Summary

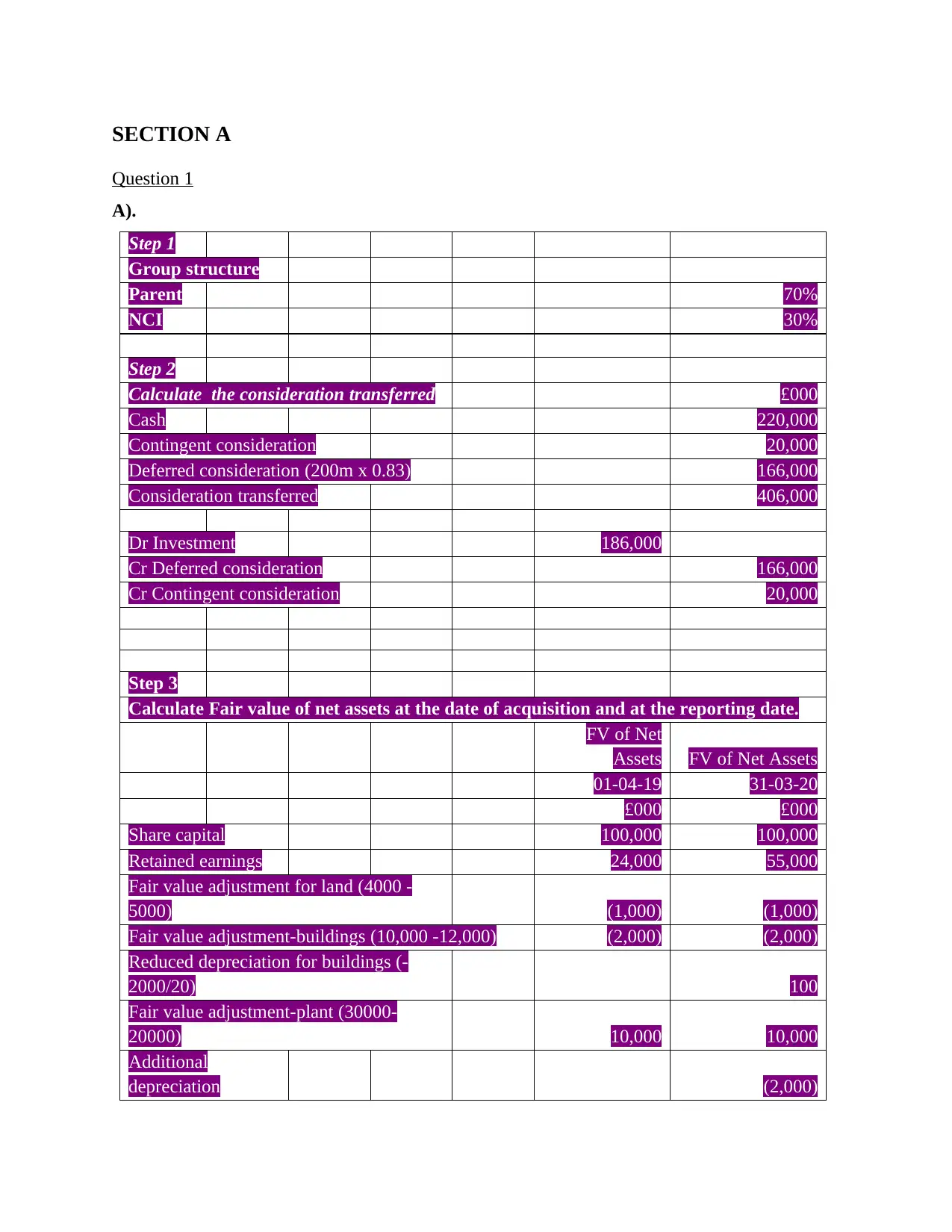

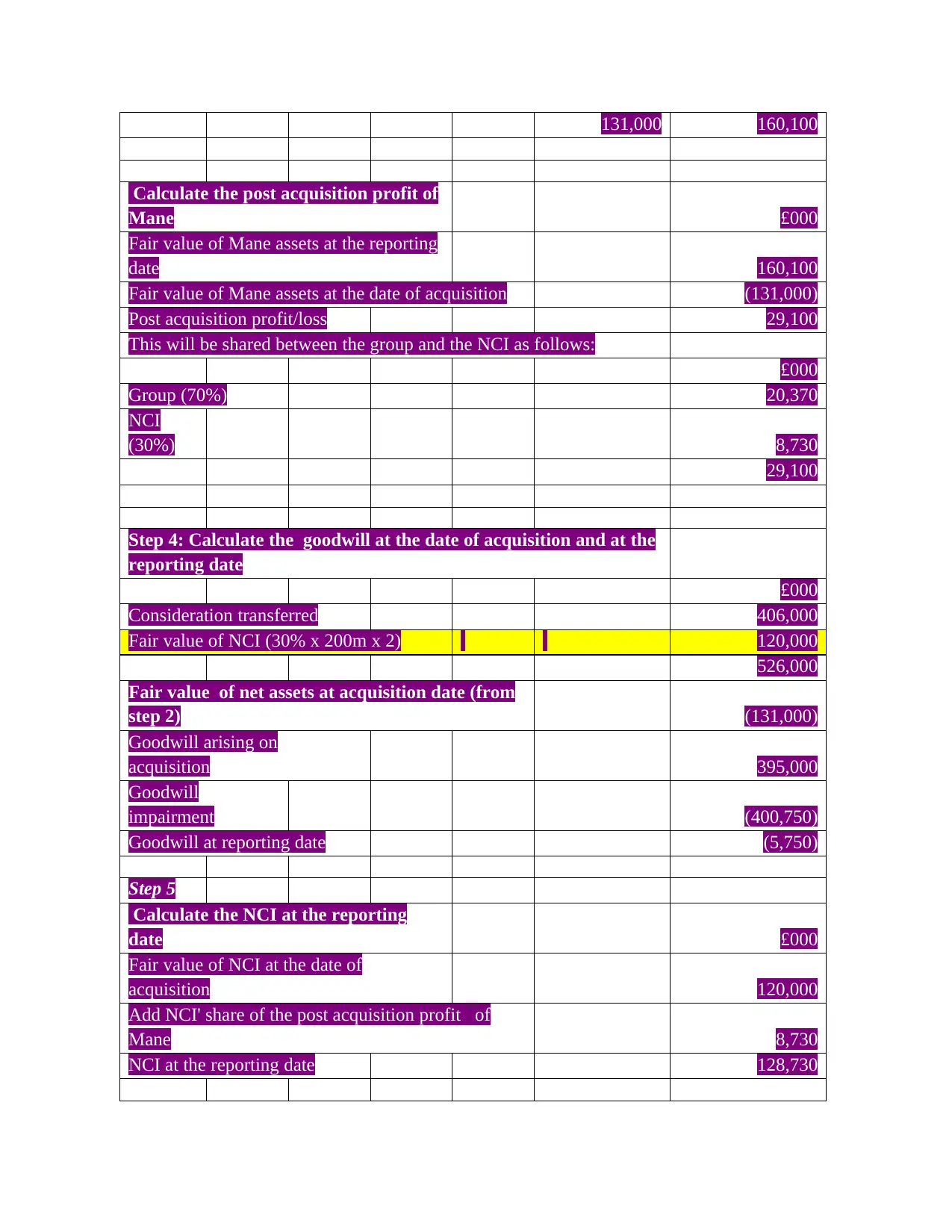

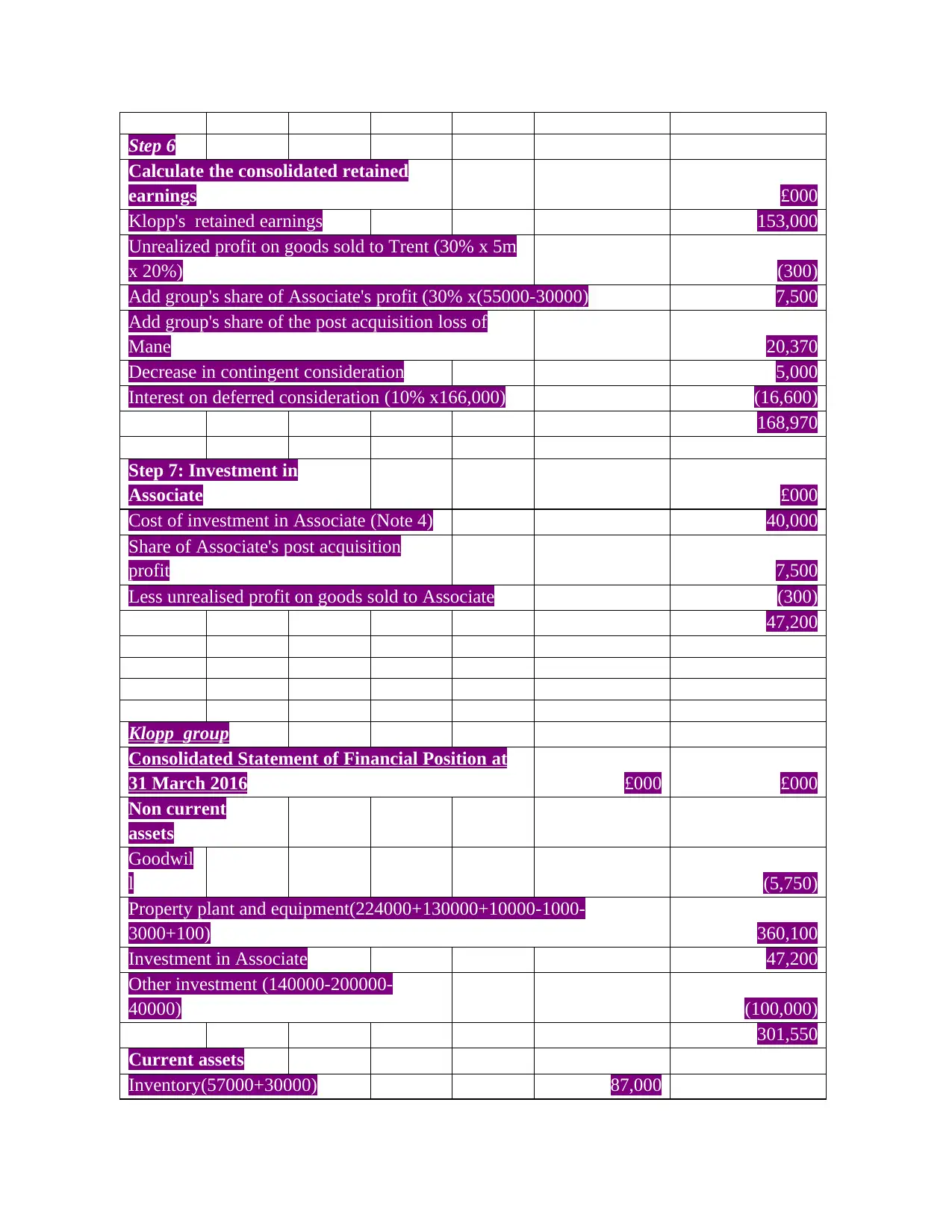

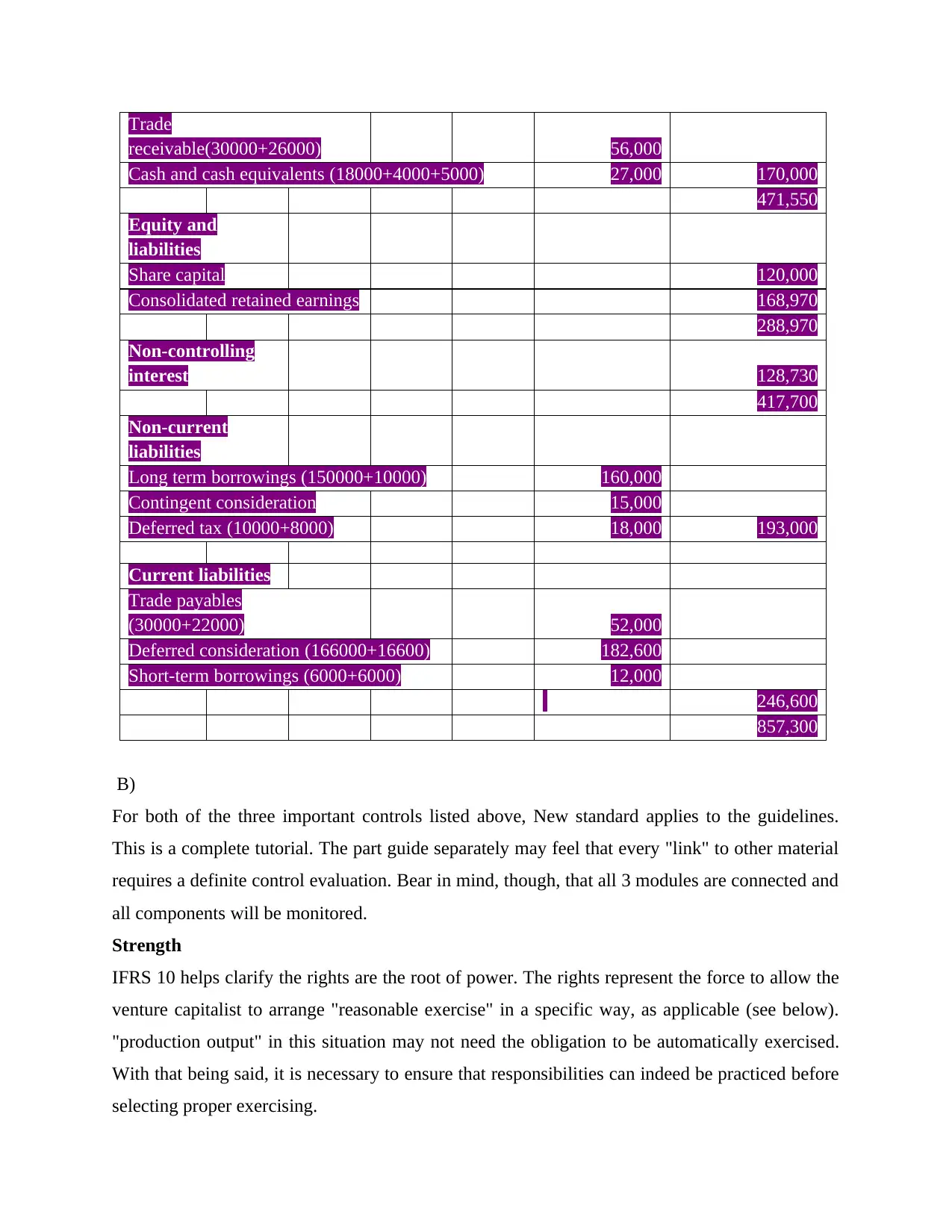

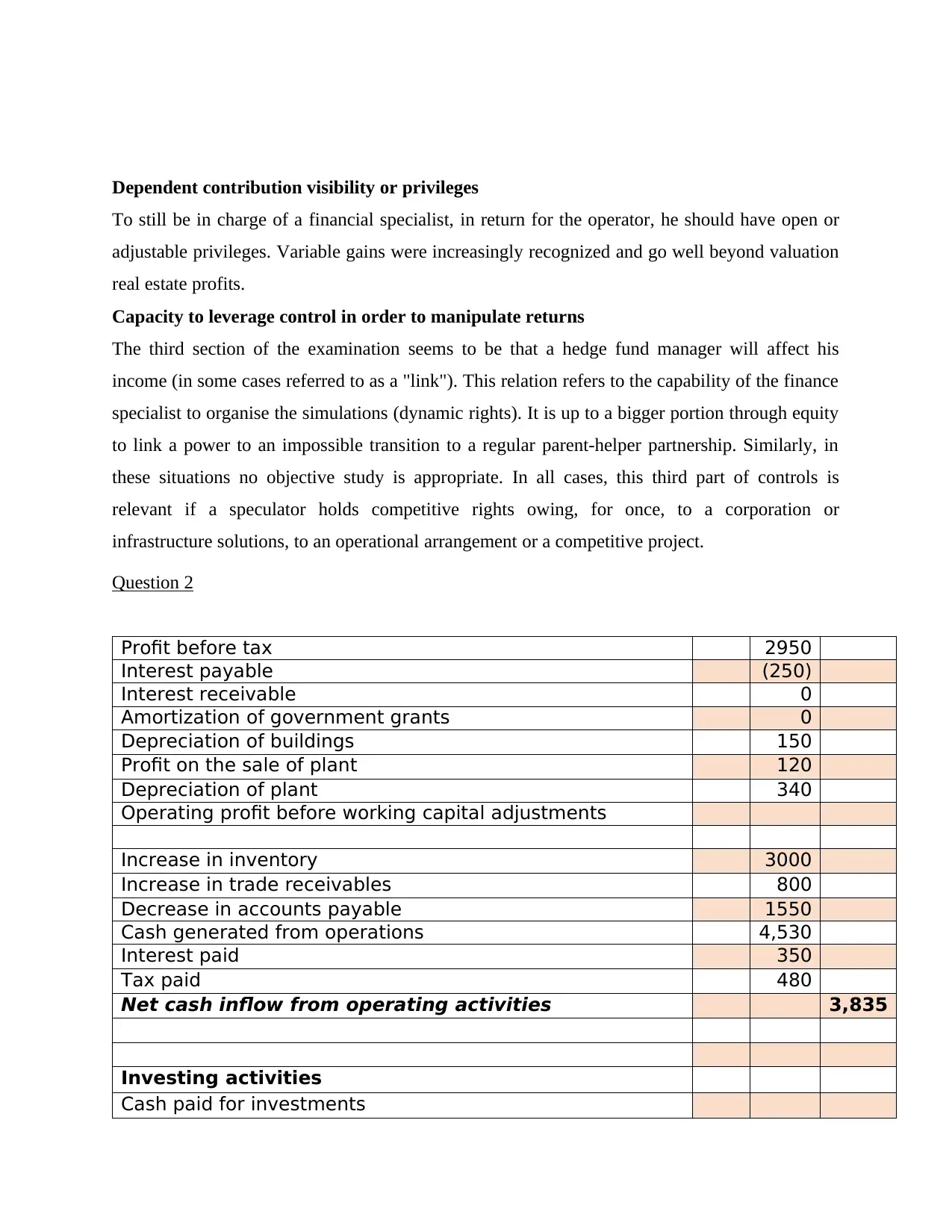

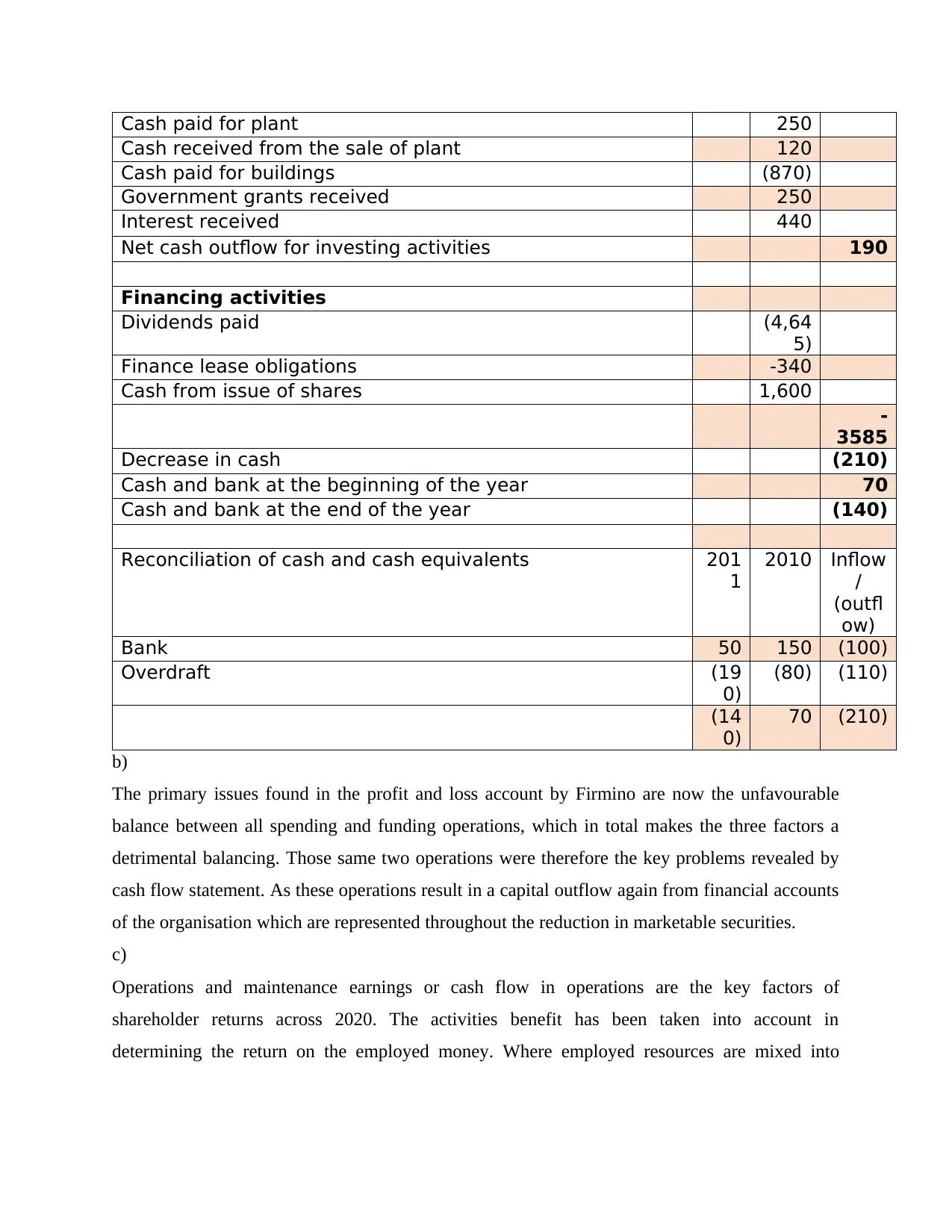

This document presents a comprehensive solution to a financial accounting assignment. Section A focuses on consolidated financial statements, including calculations for goodwill, non-controlling interest (NCI), and the impact of fair value adjustments. It demonstrates the consolidation process, including the calculation of post-acquisition profit and the preparation of a consolidated statement of financial position. Section B explores IFRS 10, emphasizing control assessments and the rights-based approach. It also analyzes a cash flow statement, identifying key issues and the impact of various transactions on cash flow. The assignment further delves into specific accounting treatments for contracts, including revenue recognition, commission calculations, and performance obligations. Finally, it addresses currency conversion and depreciation calculations, offering guidance on accounting for various transactions and providing advice on the appropriate currency to use for financial reporting. This assignment solution is a complete guide for understanding consolidation, cash flow statements, and IFRS principles.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.