Financial Accounting Homework: Detailed Solutions for All Questions

VerifiedAdded on 2023/06/06

|22

|1871

|358

Homework Assignment

AI Summary

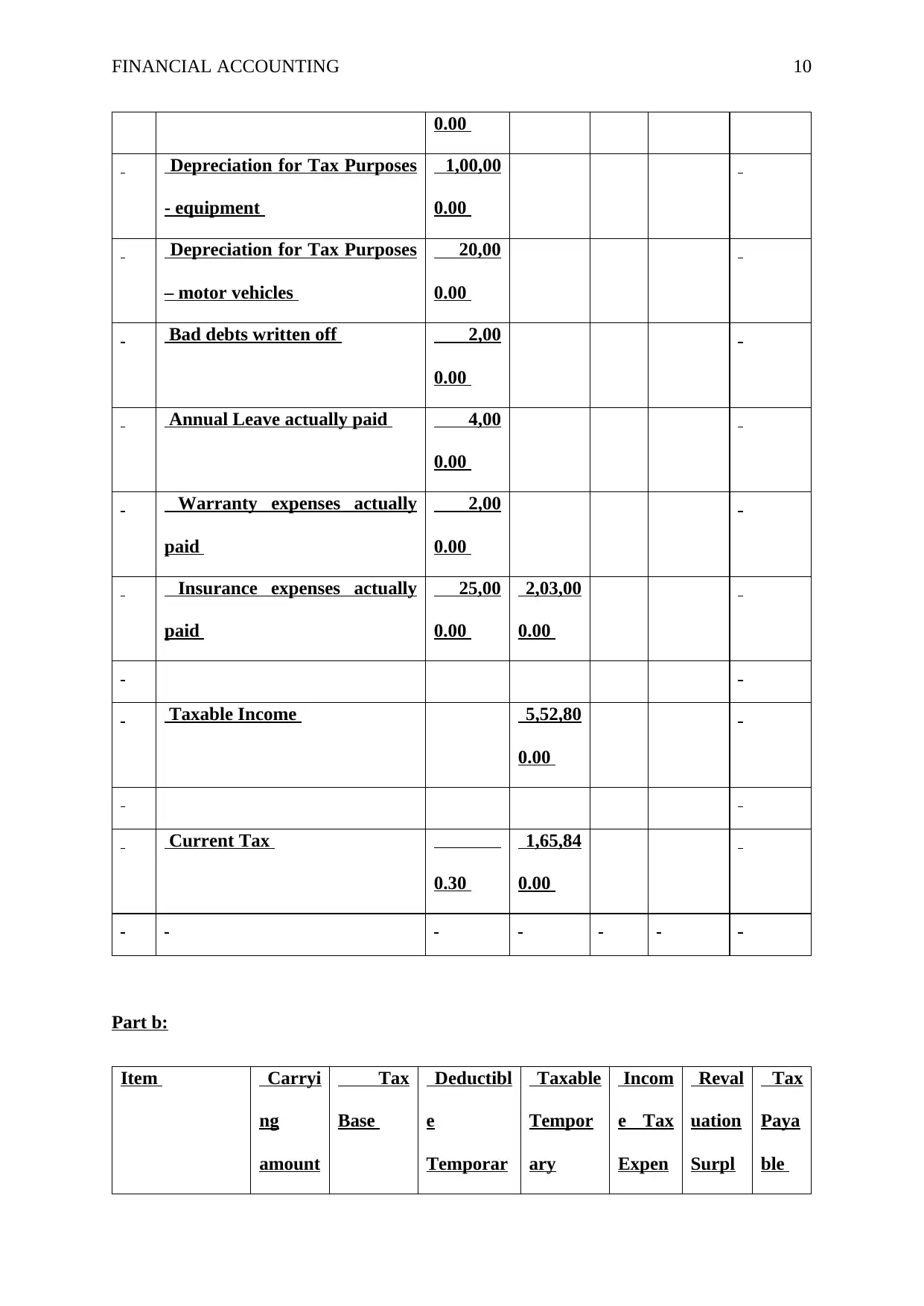

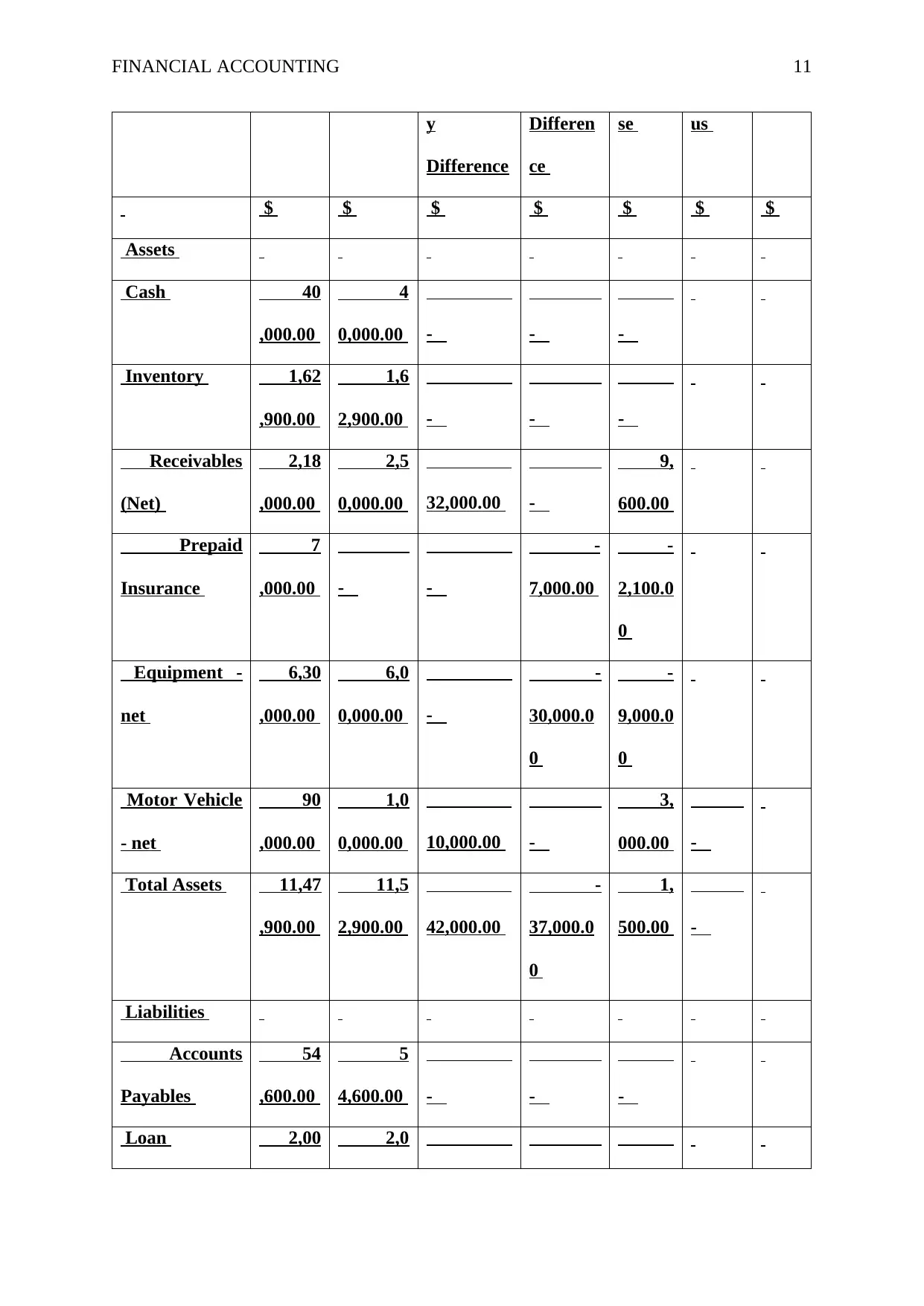

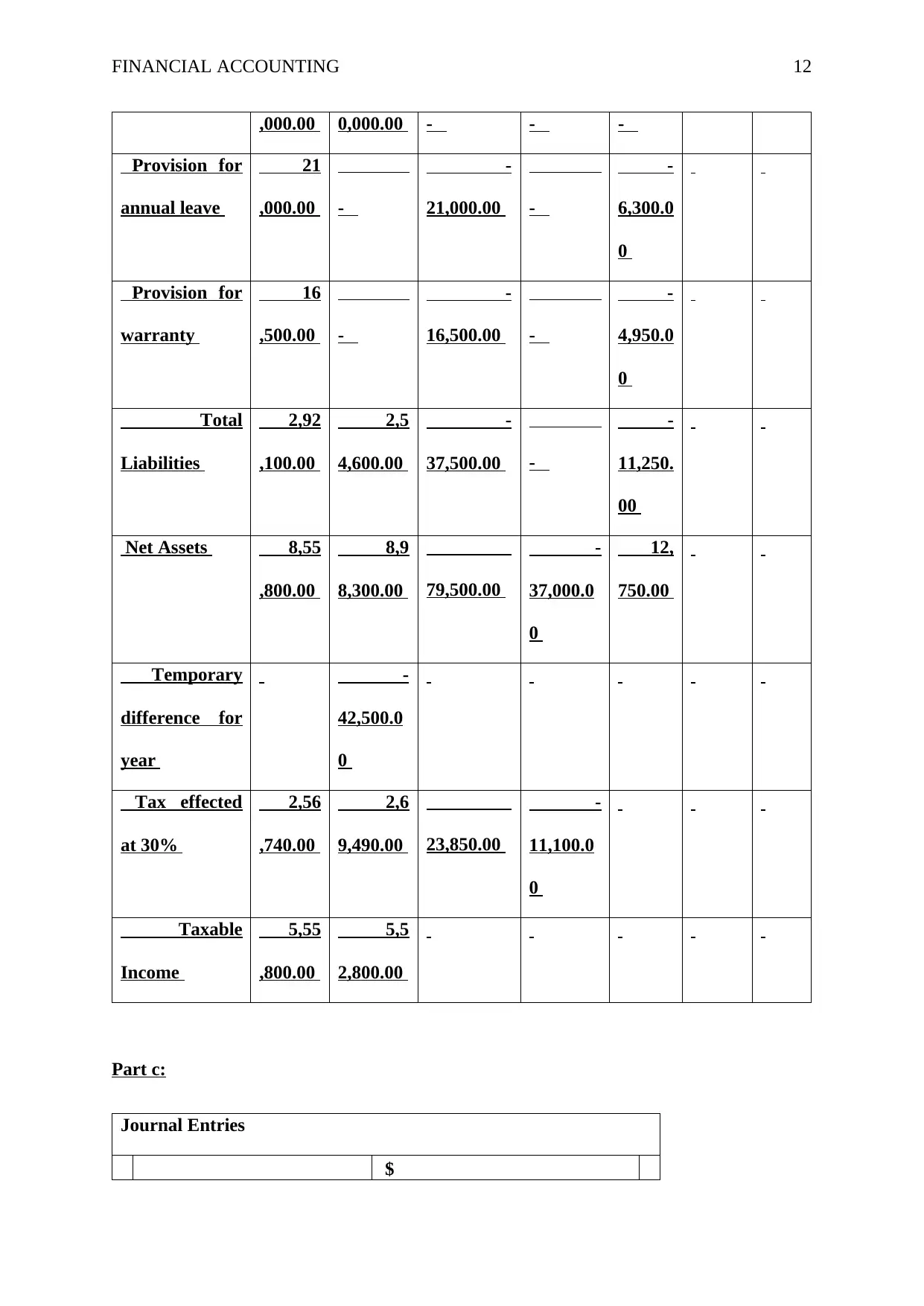

This document presents a comprehensive solution to a financial accounting homework assignment. The solution addresses various aspects of financial accounting, including changes in accounting policies and estimates as per IAS 8, accounting for share capital transactions, calculation of taxable income and deferred taxes, and accounting for asset revaluations and impairments. The assignment covers topics such as depreciation, fair value measurement, journal entries, and financial statement disclosures, offering detailed explanations and calculations for each question. It also includes analysis of fraudulent activities, share forfeiture, and impairment losses, providing a complete overview of the topics covered in the financial accounting module.

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.