Financial Accounting 1 Assignment: Cost Volume Profit and Break-Even

VerifiedAdded on 2023/06/07

|10

|1029

|86

Homework Assignment

AI Summary

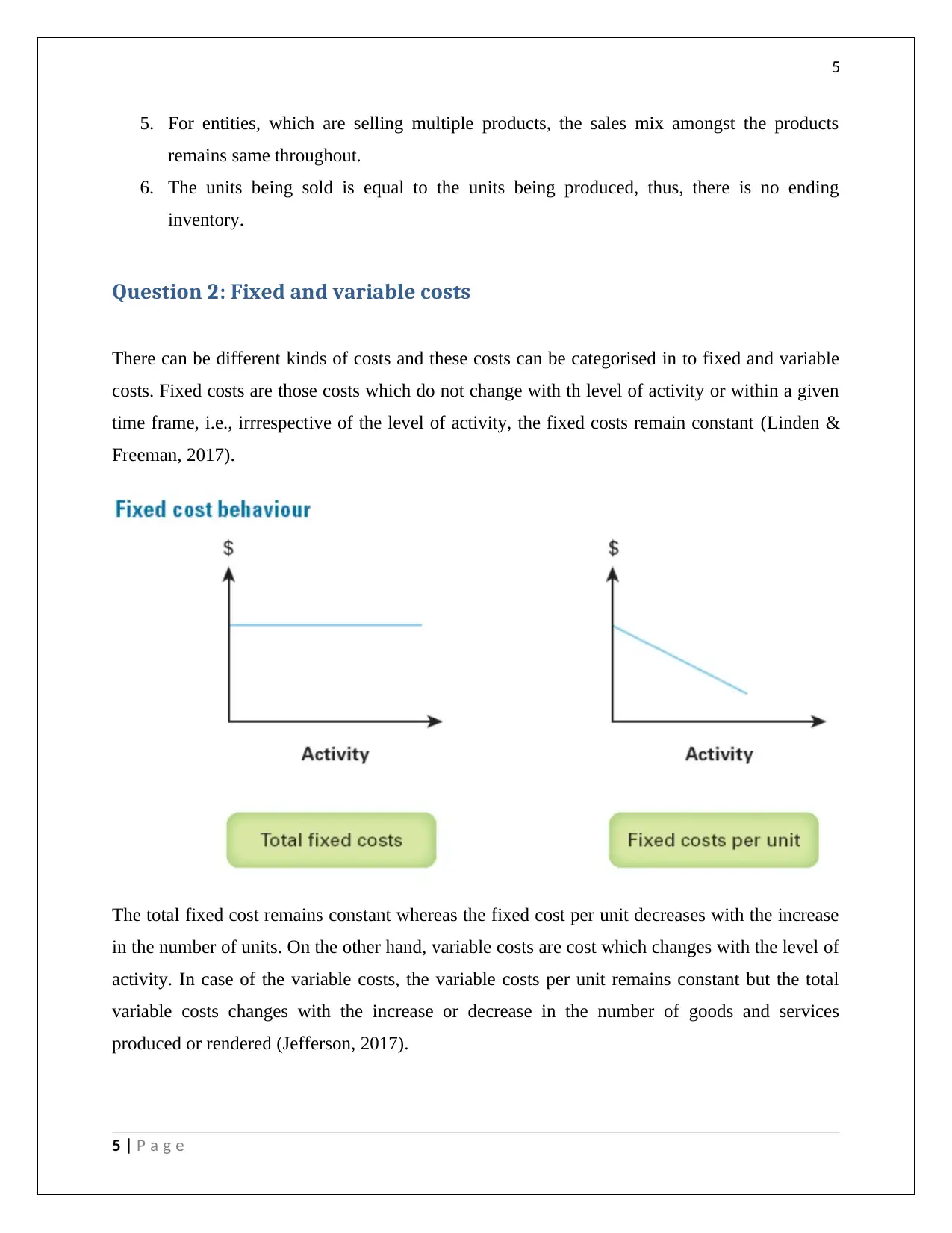

This financial accounting assignment addresses key concepts in cost-volume-profit (CVP) analysis and break-even calculations. The assignment begins with a discussion of the underlying assumptions of CVP analysis, including cost behavior classification (fixed vs. variable), constant cost behavior, and sales mix assumptions. It then differentiates between fixed and variable costs, providing examples such as rent, salaries (fixed), and direct materials, labor costs (variable). The assignment proceeds to calculate the break-even point in units for different business scenarios, using the formula: Break even point (units) = Total Fixed costs / (contribution per unit). Finally, the assignment applies break-even analysis to a specific case involving coaching sessions, calculating the number of sessions needed to cover costs. The document includes detailed calculations and references.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.