Comprehensive Financial Accounting Assignment: Solutions Provided

VerifiedAdded on 2023/06/13

|6

|912

|201

Homework Assignment

AI Summary

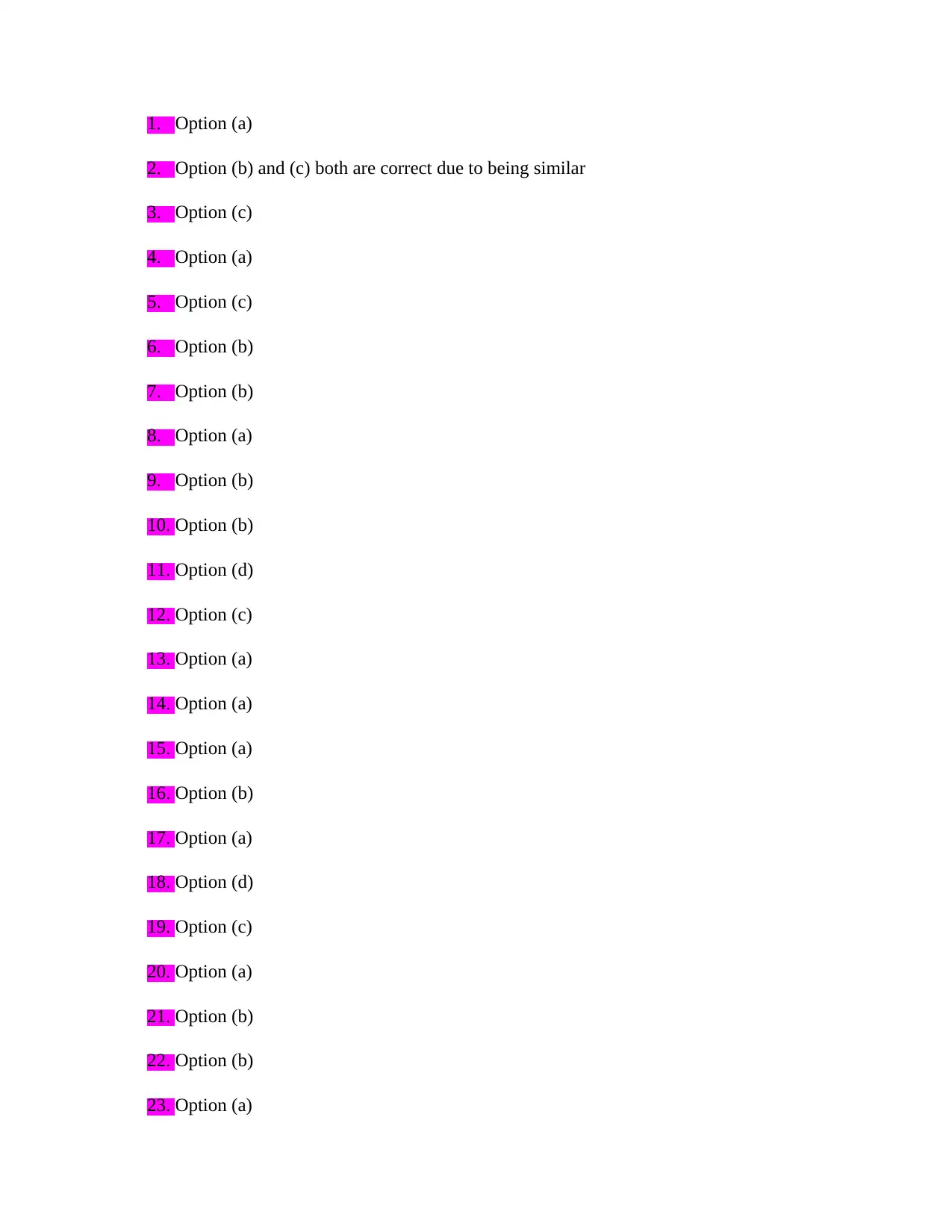

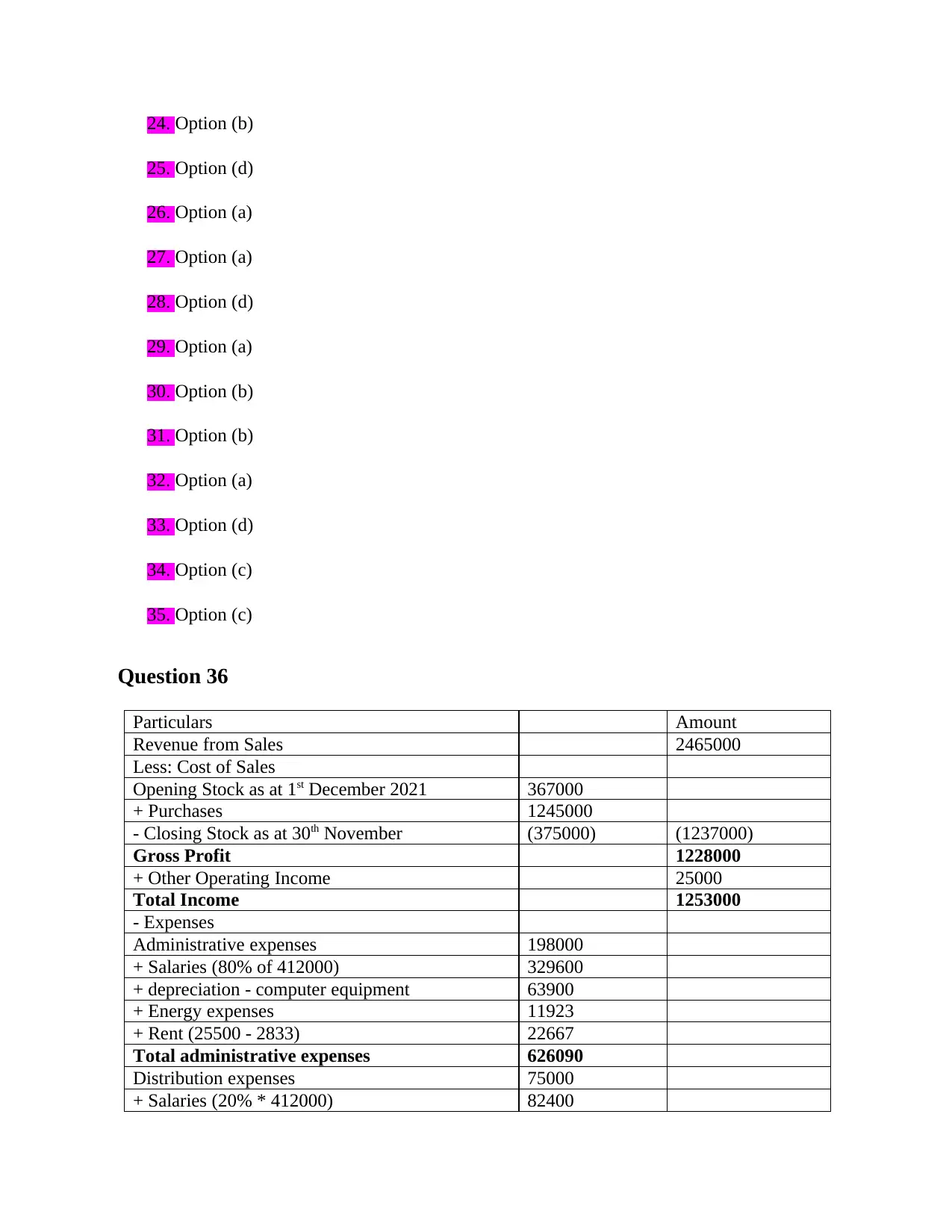

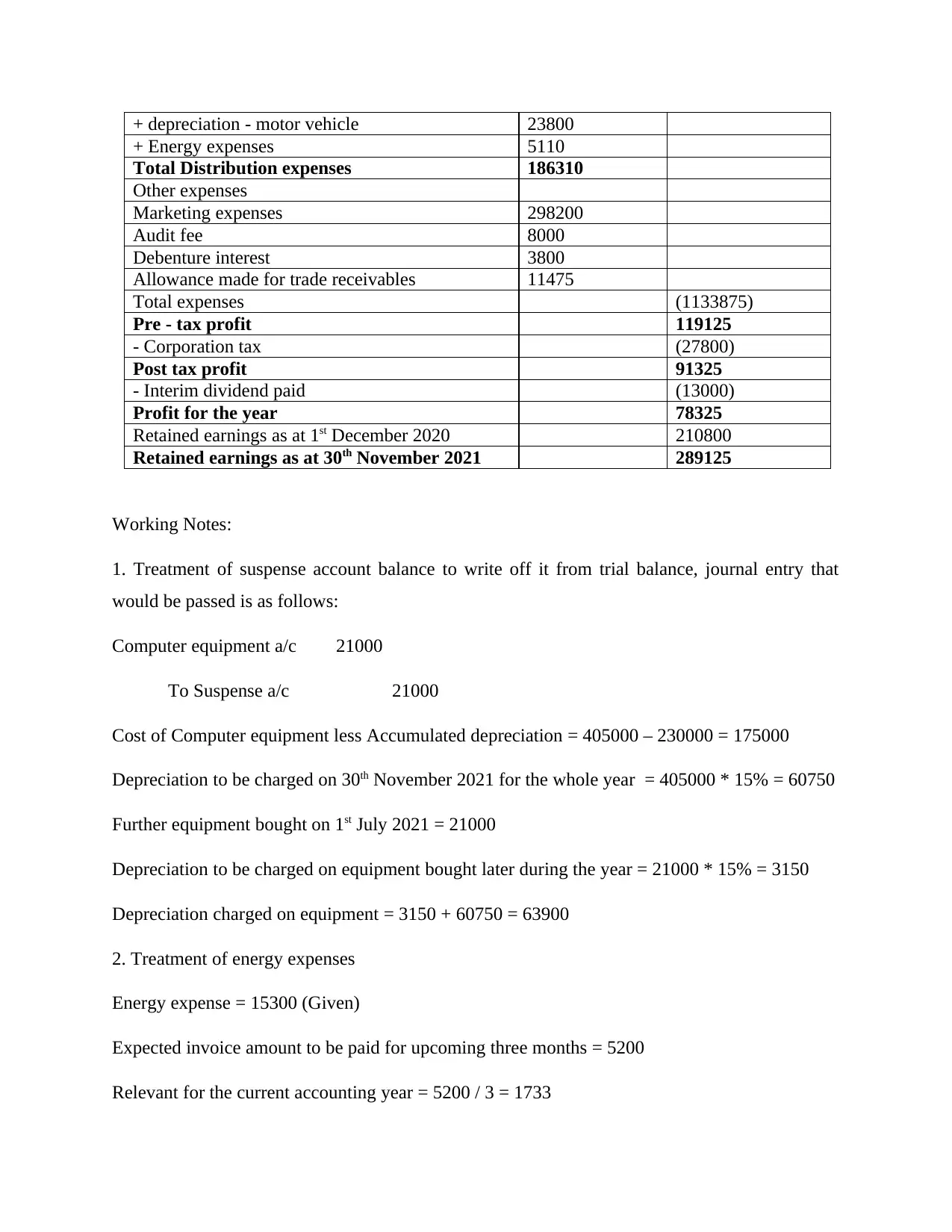

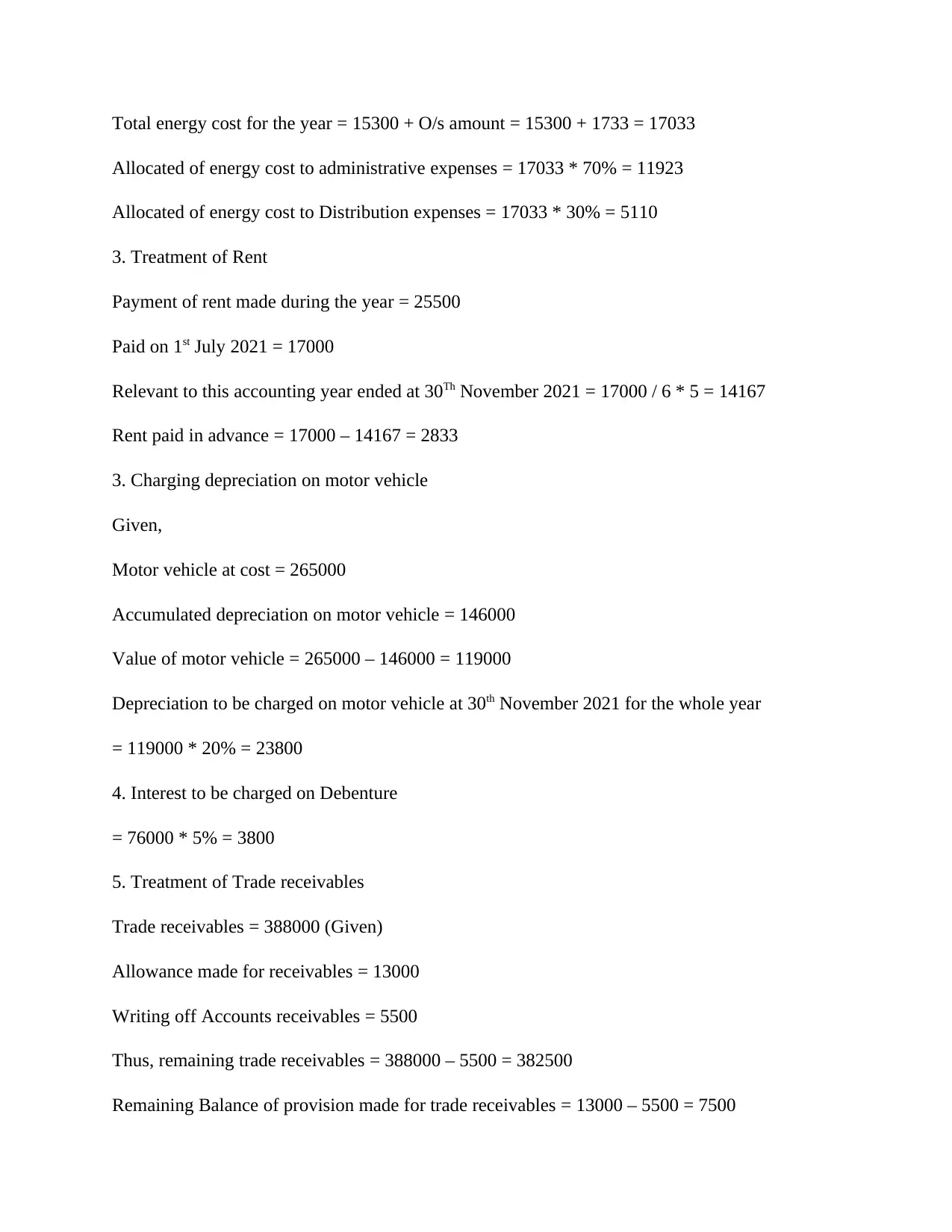

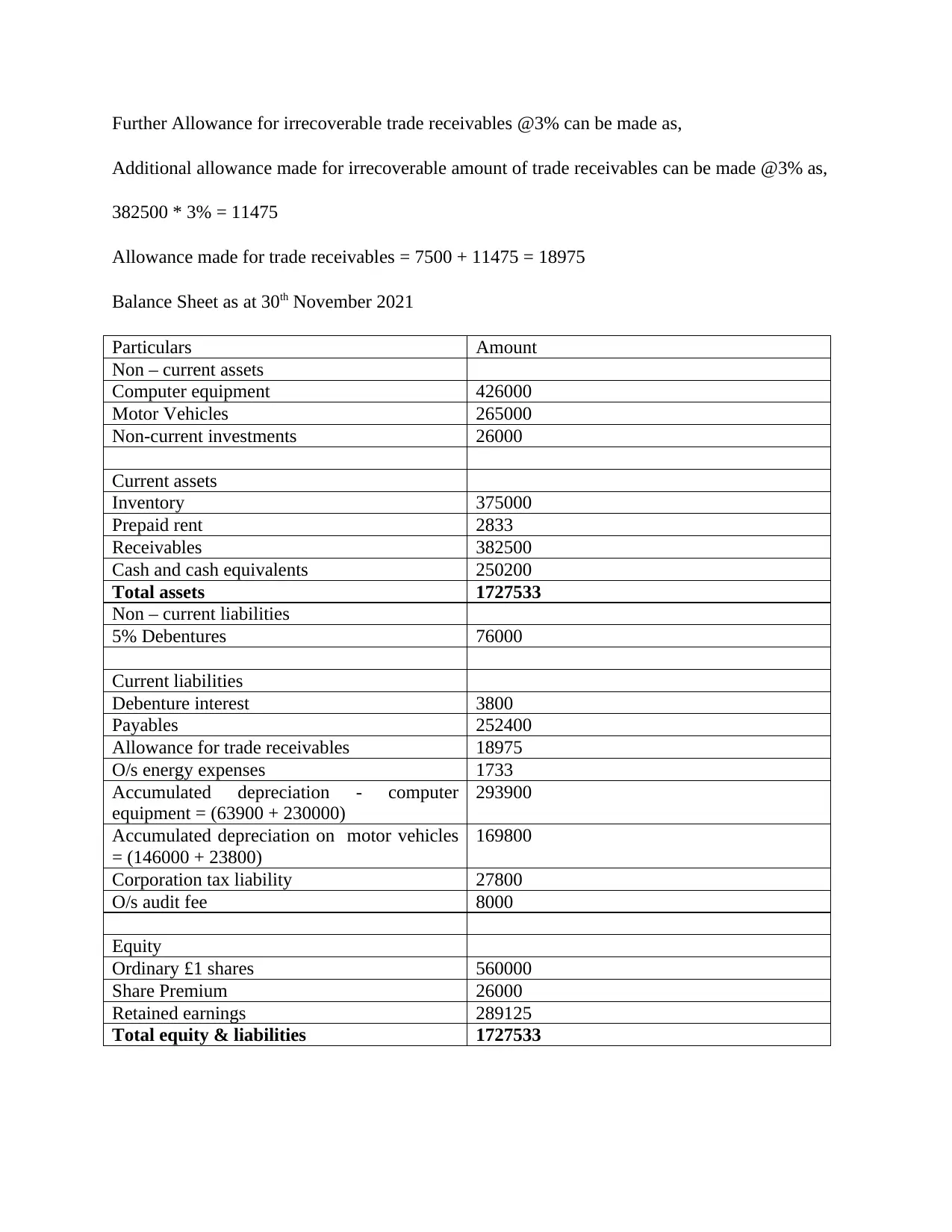

This document presents a solved financial accounting assignment, beginning with answers to multiple-choice questions covering fundamental accounting concepts. It then provides a detailed solution to a comprehensive problem involving the preparation of an income statement and balance sheet. The solution includes meticulous working notes that explain the treatment of various items such as suspense account balances, energy expenses, rent payments, depreciation on motor vehicles and computer equipment, debenture interest, and trade receivables. The income statement calculates gross profit, total income, pre-tax profit, post-tax profit, and retained earnings. The balance sheet categorizes assets into non-current and current, and liabilities into non-current and current, ultimately balancing equity and liabilities with total assets. This assignment solution is designed to aid students in understanding and applying financial accounting principles.

1 out of 6

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.