Financial Accounting 1 Assignment Solution: University Name

VerifiedAdded on 2020/04/07

|19

|3449

|40

Homework Assignment

AI Summary

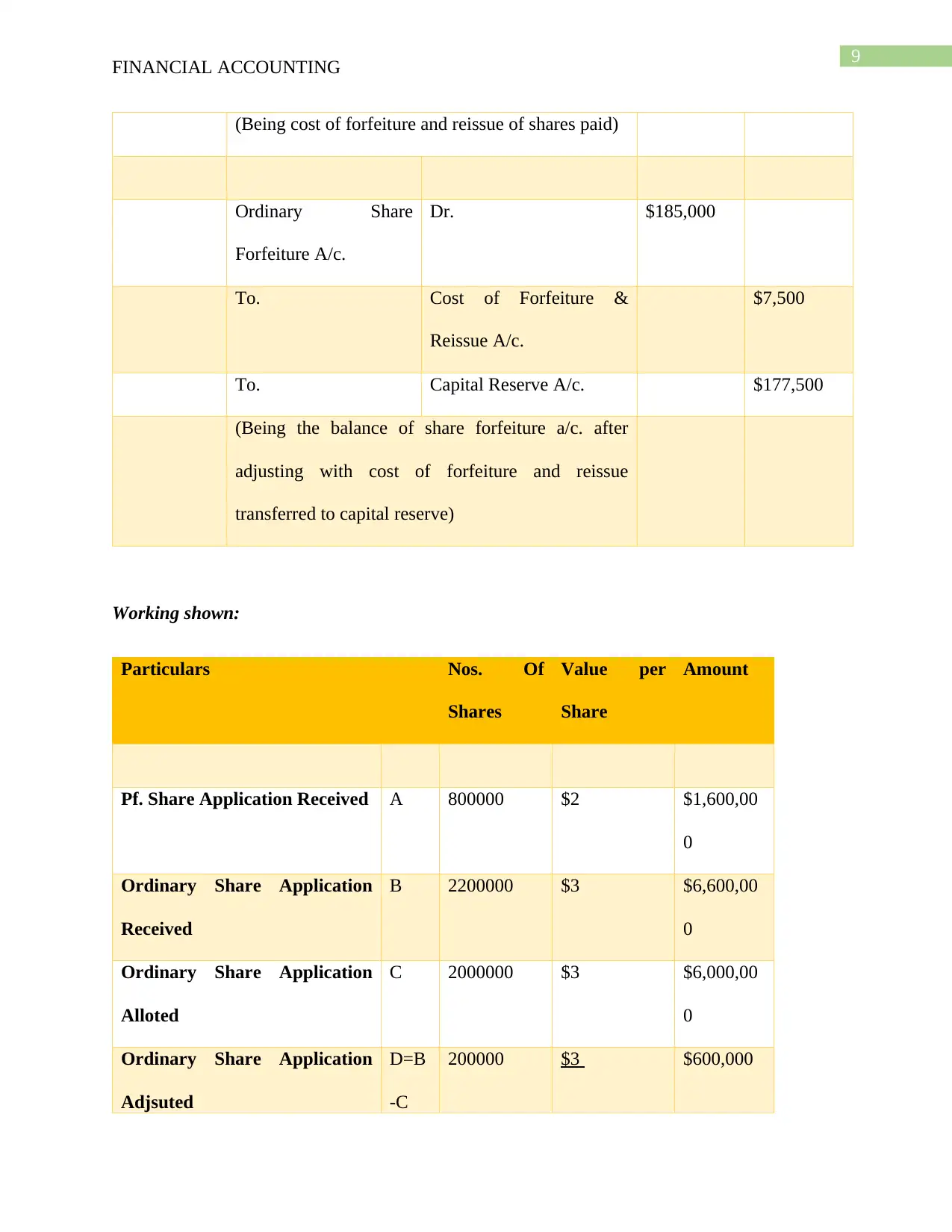

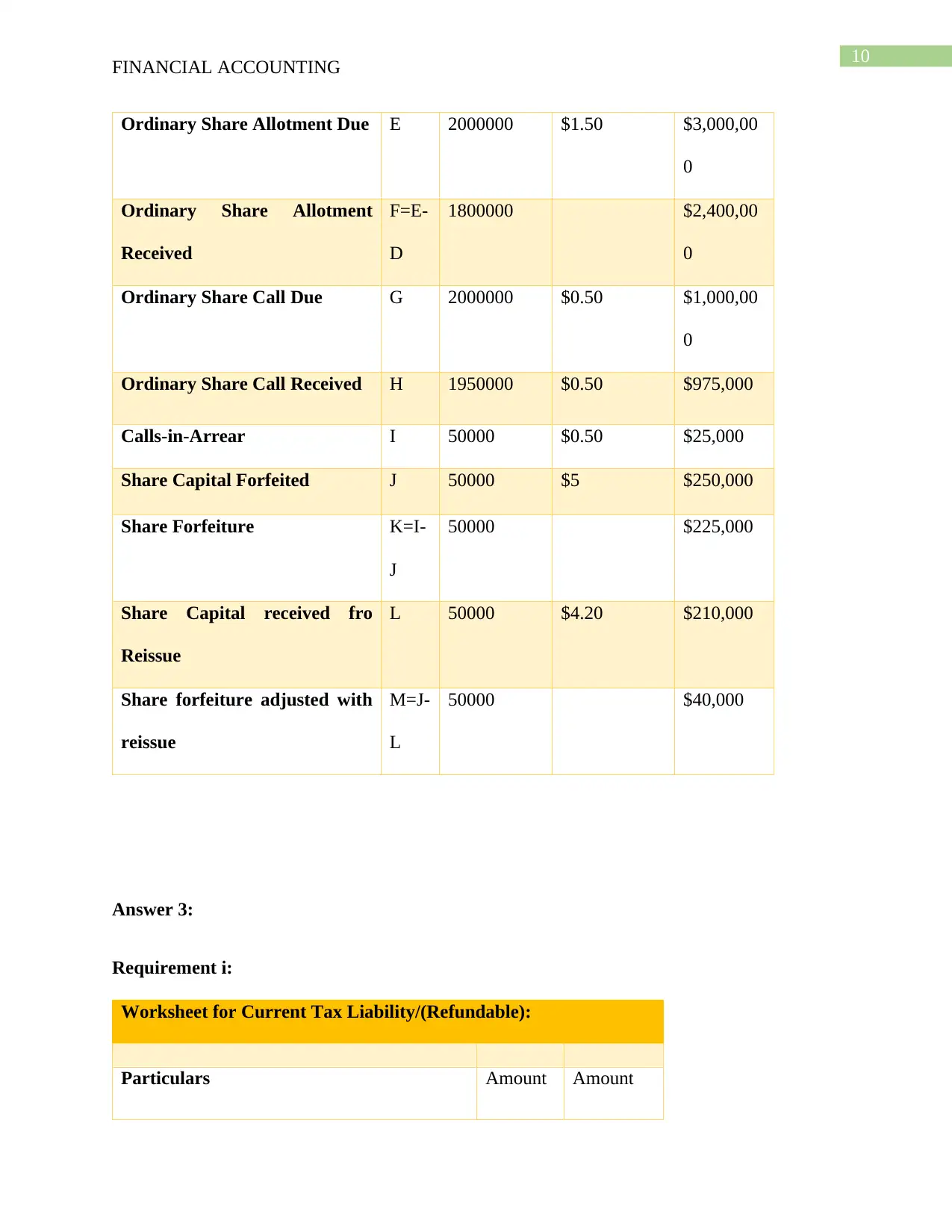

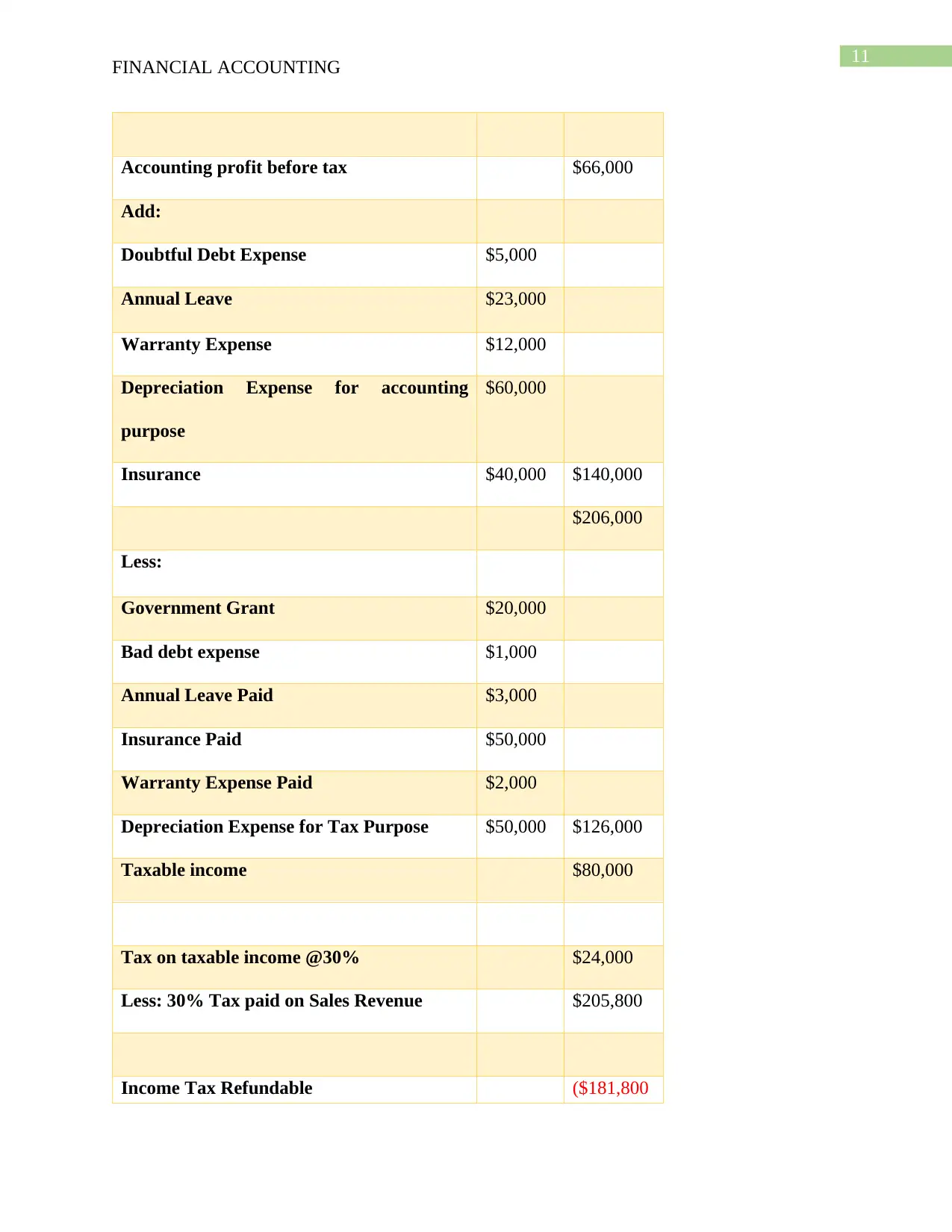

This financial accounting assignment solution covers several key areas of financial reporting and accounting practices. The solution begins with a letter to the International Accounting Standards Board (IASB) discussing the importance of effective communication and fiscal report information, with a focus on the annual reports of two banks, ANZ and Westpac. It then presents detailed journal entries for share transactions, including share applications, allotments, calls, forfeitures, and reissues, along with supporting workings. The assignment also includes comprehensive calculations and journal entries related to current and deferred tax, providing worksheets and explanations for taxable income, temporary differences, and deferred tax assets and liabilities. The solution demonstrates how to account for various expenses and revenues, including depreciation, doubtful debts, warranties, and government grants, ensuring that students gain a thorough understanding of the accounting principles involved. The assignment is designed to help students understand the complexities of financial accounting and reporting.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.