Financial Accounting Principles - Finance Assignment Solution Report

VerifiedAdded on 2020/10/22

|26

|3669

|391

Homework Assignment

AI Summary

This document provides a comprehensive solution to a financial accounting principles assignment. It begins with an introduction to financial accounting, its purpose, and an assessment of internal and external stakeholders, including employees, managers, shareholders, creditors, and government bodies. The assignment then delves into practical applications, including completing double-entry recordings, preparing a trial balance, and constructing financial statements like the statement of profit and loss and the statement of financial position for Munteanu Ltd. It also covers key accounting concepts such as consistency and prudency, the purpose of depreciation, and an evaluation of financial statements prepared by different business structures. Furthermore, the solution addresses bank reconciliation statements, the preparation of sales and purchase ledger control accounts, and the features of suspense accounts. The assignment provides detailed examples and explanations, ensuring a thorough understanding of financial accounting principles and their practical application.

Financial Accounting principles

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................1

PART A.........................................................................................................................................................1

1. Financial accounting and its purpose...................................................................................................1

2. Assessment of internal and external stakeholders who are interested in the financial information of

the organization......................................................................................................................................3

PART B.........................................................................................................................................................5

CLIENT 1...................................................................................................................................................5

1. Completing double entry recording within the relevant ledger...........................................................5

2. Trail balance at 31st January 2019......................................................................................................14

CLIENT 2.................................................................................................................................................15

(A.) Statement of profit and loss of Munteanu Ltd................................................................................15

(B.) Statement of financial position of Munteanu Ltd...........................................................................15

c.) Explanation of accounting concept: “consistency” and “prudency”.................................................17

d. Purpose of depreciation in formulating accounting statements........................................................17

e.) Evaluation of financial statements prepared by sole traders and the limited companies................18

CLIENT 3.................................................................................................................................................18

a.) Purpose of preparing the BRS...........................................................................................................18

b.) Reasons for differences in cash book and company’s statements...................................................19

c.) Term “Imprest” in petty cash system................................................................................................19

(d.) Bank reconciliation statement as at 30 September 2018................................................................19

CLIENT 4.................................................................................................................................................20

(a.) preparation of sales and purchase ledger control account.............................................................20

b.) Control account................................................................................................................................21

CLIENT 5.................................................................................................................................................21

a.) Features of suspense account..........................................................................................................21

(b.) Trial balance from the figures.........................................................................................................22

(c.) Preparation of journal entries with suspense account....................................................................22

CONCLUSION.............................................................................................................................................23

REFERENCES..............................................................................................................................................24

INTRODUCTION...........................................................................................................................................1

PART A.........................................................................................................................................................1

1. Financial accounting and its purpose...................................................................................................1

2. Assessment of internal and external stakeholders who are interested in the financial information of

the organization......................................................................................................................................3

PART B.........................................................................................................................................................5

CLIENT 1...................................................................................................................................................5

1. Completing double entry recording within the relevant ledger...........................................................5

2. Trail balance at 31st January 2019......................................................................................................14

CLIENT 2.................................................................................................................................................15

(A.) Statement of profit and loss of Munteanu Ltd................................................................................15

(B.) Statement of financial position of Munteanu Ltd...........................................................................15

c.) Explanation of accounting concept: “consistency” and “prudency”.................................................17

d. Purpose of depreciation in formulating accounting statements........................................................17

e.) Evaluation of financial statements prepared by sole traders and the limited companies................18

CLIENT 3.................................................................................................................................................18

a.) Purpose of preparing the BRS...........................................................................................................18

b.) Reasons for differences in cash book and company’s statements...................................................19

c.) Term “Imprest” in petty cash system................................................................................................19

(d.) Bank reconciliation statement as at 30 September 2018................................................................19

CLIENT 4.................................................................................................................................................20

(a.) preparation of sales and purchase ledger control account.............................................................20

b.) Control account................................................................................................................................21

CLIENT 5.................................................................................................................................................21

a.) Features of suspense account..........................................................................................................21

(b.) Trial balance from the figures.........................................................................................................22

(c.) Preparation of journal entries with suspense account....................................................................22

CONCLUSION.............................................................................................................................................23

REFERENCES..............................................................................................................................................24

INTRODUCTION

Financial accounting is the process of recording, classifying, summarizing and

monitoring financial transaction in a systematic manner in the financial statements of the

company.

Taj accountancy is a privately held company founded in the year 2010 and headquartered

in London. This is a small based financial company which offers exclusive accountancy,

business planning, company secretarial, taxation advice services and business funding to

individuals as well as to corporates.

This report highlights purpose of financial accounting and also includes internal and

external stakeholders who are interested in the financial information of the organization.

Furthermore, this report also includes recording of financial business transaction using

double entry book-keeping and extraction of trial balance. This report also includes preparation

of final accounts in compliance with principles, conventions and standards. Lastly, it also

includes reconciliation of control accounts and suspense accounts.

PART A

1. Financial accounting and its purpose.

Financial accounting is a specialized process of recording, classifying, summarizing,

controlling and monitoring the financial transactions of Taj accountancy. These financial

transactions are presented in the financial statements or reports like profit and loss income

statement, balance sheet, cash flow statement which records company's operation over a specific

period of time. Financial accounting is done to provide information to stakeholders inside or

outside the organization like management, lenders, suppliers, investors, employees, tax

authorities, government regarding the operations of business performance and its productivity

effectively and efficiently.

Financial accounting has to be performed in compliance with various accounting

principles, conventions and standards. For effective validity and credibility of financial

information company has to abide with Generally Accepted Accounting Principles ( GAAP ) .

International companies prepare financial statements in accordance with International Financial

Reporting Standards ( IFRS ) . Financial accounting is done to analyse and understand the

financial position, performance and productivity of business effectively and efficiently to take

strategic decision which helps facilitate growth of the business.

1

Financial accounting is the process of recording, classifying, summarizing and

monitoring financial transaction in a systematic manner in the financial statements of the

company.

Taj accountancy is a privately held company founded in the year 2010 and headquartered

in London. This is a small based financial company which offers exclusive accountancy,

business planning, company secretarial, taxation advice services and business funding to

individuals as well as to corporates.

This report highlights purpose of financial accounting and also includes internal and

external stakeholders who are interested in the financial information of the organization.

Furthermore, this report also includes recording of financial business transaction using

double entry book-keeping and extraction of trial balance. This report also includes preparation

of final accounts in compliance with principles, conventions and standards. Lastly, it also

includes reconciliation of control accounts and suspense accounts.

PART A

1. Financial accounting and its purpose.

Financial accounting is a specialized process of recording, classifying, summarizing,

controlling and monitoring the financial transactions of Taj accountancy. These financial

transactions are presented in the financial statements or reports like profit and loss income

statement, balance sheet, cash flow statement which records company's operation over a specific

period of time. Financial accounting is done to provide information to stakeholders inside or

outside the organization like management, lenders, suppliers, investors, employees, tax

authorities, government regarding the operations of business performance and its productivity

effectively and efficiently.

Financial accounting has to be performed in compliance with various accounting

principles, conventions and standards. For effective validity and credibility of financial

information company has to abide with Generally Accepted Accounting Principles ( GAAP ) .

International companies prepare financial statements in accordance with International Financial

Reporting Standards ( IFRS ) . Financial accounting is done to analyse and understand the

financial position, performance and productivity of business effectively and efficiently to take

strategic decision which helps facilitate growth of the business.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial accounting is a process designed to accurately determine and analyse the

activities performed by the organization in a systematic and effective manner. This allows

company to get assess to in- depth analysis of the financials of the organization and helps in

efficient allocation of resources and strategic decision making for the growth and expansion of

the business.

PURPOSE OF FINANCIAL ACCOUNTING.

Disclosure of financial position: Financial accounting main purpose is to disclose

financial position of the business for a particular period to ascertain whether the company

is making profit or loss.

Facilitate in decision making: Financial accounting helps in analysing financial

statements of the company effectively and efficiently in order to make strategic decision

making by the management for achieving desired goals and objectives of the company.

Provide information to both internal and external stakeholders: Financial accounting

statements provide information to both internal stakeholders like owners, management,

employees, and as well as to external stakeholders like investors, creditors, customers,

government, etc. to analyse financial statement and performance of the company in order

to take systematic decision.

Systematic records of financial transaction: Financial accounting is done to keep

systematic records of financial transaction of the business effectively and efficiently in

order to take fast decision for operational efficiency and productivity. This helps in better

and accurate understanding of the financial transaction (Kimmel and et.al., 2016).

Identification of unwanted financial transaction: It helps in detecting cause of any

miss-happening event and unwanted transaction which affect operational efficiency and

productivity of business.

Identification of results: Financial accounting is done to analyse and ascertain the actual

performance of the organization from the set target. This helps in analysing the results

and in case of any deviation necessary action is taken for effective working of the

organization.

Provide relevant, reliable, comparable and consistent financial information:

Financial accounting of the organization is done to provide organization with relevant

and reliable data or information to its end users which helps in taking effective decision.

2

activities performed by the organization in a systematic and effective manner. This allows

company to get assess to in- depth analysis of the financials of the organization and helps in

efficient allocation of resources and strategic decision making for the growth and expansion of

the business.

PURPOSE OF FINANCIAL ACCOUNTING.

Disclosure of financial position: Financial accounting main purpose is to disclose

financial position of the business for a particular period to ascertain whether the company

is making profit or loss.

Facilitate in decision making: Financial accounting helps in analysing financial

statements of the company effectively and efficiently in order to make strategic decision

making by the management for achieving desired goals and objectives of the company.

Provide information to both internal and external stakeholders: Financial accounting

statements provide information to both internal stakeholders like owners, management,

employees, and as well as to external stakeholders like investors, creditors, customers,

government, etc. to analyse financial statement and performance of the company in order

to take systematic decision.

Systematic records of financial transaction: Financial accounting is done to keep

systematic records of financial transaction of the business effectively and efficiently in

order to take fast decision for operational efficiency and productivity. This helps in better

and accurate understanding of the financial transaction (Kimmel and et.al., 2016).

Identification of unwanted financial transaction: It helps in detecting cause of any

miss-happening event and unwanted transaction which affect operational efficiency and

productivity of business.

Identification of results: Financial accounting is done to analyse and ascertain the actual

performance of the organization from the set target. This helps in analysing the results

and in case of any deviation necessary action is taken for effective working of the

organization.

Provide relevant, reliable, comparable and consistent financial information:

Financial accounting of the organization is done to provide organization with relevant

and reliable data or information to its end users which helps in taking effective decision.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It is free of biasness and misleading information which helps company to completely rely

on such financial information for effective decision making.

2. Assessment of internal and external stakeholders who are interested in the financial

information of the organization.

Stakeholders are the group of individuals, person, banks or financial institution, corporate

who are interested in the operational efficiency of the organization. Stakeholders have concern in

the company’s financial position directly or indirectly. Primary stakeholders are directly

connected with the operation of the business and secondary stakeholders are indirectly concerned

about the financial position of the business. Stakeholders of the organization are interested in

company’s financial information which help them take strategic decision according to the

operation and finances of the organization.

Internal stakeholders are also referred to primary stakeholders which consist of

individuals, employees, owners, management, director within the organization who have

significant interest on the welfare of the company. Internal stakeholders of the Taj accountancy

are influenced by the performance of the organization and take decision accordingly. Internal

stakeholders are directly influenced by the working of the organization and helps in serving the

organization effectively.

Employees : They are part of primary internal stakeholders who are directly affected by

the success and failure of the organization. Employees of the Taj accountancy are

directly influenced by the working of the organization and they are interested in the

financial statements and reports of the organization. Employees work for remuneration,

salary, bonus which is largely dependent on the working of organization. Employees are

interested in the company who has long sustainable future with higher operational

efficiency, productivity and profitability. This helps company in taking strategic decision

whether to remain in the company for achieving greater heights or to switch to one whose

financial statements are strong and has better growth prospects (Difference Between

Internal and External Stakeholders, 2015).

Managers : Managers are responsible for taking strategic decision in order to enhance

the operational efficiency of the organization. They are directly influenced by the

operations and performance of the organization as they are primary stakeholders of the

company. Managers of the organization critically evaluate the financial statements and

3

on such financial information for effective decision making.

2. Assessment of internal and external stakeholders who are interested in the financial

information of the organization.

Stakeholders are the group of individuals, person, banks or financial institution, corporate

who are interested in the operational efficiency of the organization. Stakeholders have concern in

the company’s financial position directly or indirectly. Primary stakeholders are directly

connected with the operation of the business and secondary stakeholders are indirectly concerned

about the financial position of the business. Stakeholders of the organization are interested in

company’s financial information which help them take strategic decision according to the

operation and finances of the organization.

Internal stakeholders are also referred to primary stakeholders which consist of

individuals, employees, owners, management, director within the organization who have

significant interest on the welfare of the company. Internal stakeholders of the Taj accountancy

are influenced by the performance of the organization and take decision accordingly. Internal

stakeholders are directly influenced by the working of the organization and helps in serving the

organization effectively.

Employees : They are part of primary internal stakeholders who are directly affected by

the success and failure of the organization. Employees of the Taj accountancy are

directly influenced by the working of the organization and they are interested in the

financial statements and reports of the organization. Employees work for remuneration,

salary, bonus which is largely dependent on the working of organization. Employees are

interested in the company who has long sustainable future with higher operational

efficiency, productivity and profitability. This helps company in taking strategic decision

whether to remain in the company for achieving greater heights or to switch to one whose

financial statements are strong and has better growth prospects (Difference Between

Internal and External Stakeholders, 2015).

Managers : Managers are responsible for taking strategic decision in order to enhance

the operational efficiency of the organization. They are directly influenced by the

operations and performance of the organization as they are primary stakeholders of the

company. Managers of the organization critically evaluate the financial statements and

3

analyse whether goals and objectives of the company are achieved or not. This helps

them take effective decision accordingly. Management of the organization uses financial

statements to ensure that company has long term solvency position.

External stakeholders are also referred to as secondary stakeholders. External stakeholders

are individuals and corporate like customers, general public, rating agencies, competitors,

investment analysts, suppliers, community, investors, shareholders, government, creditors,

etc. outside the organization and are affected by the operations of business. They are

interested in financial information of the company for taking strategic decision effectively

and efficiently.

Shareholders: Shareholders of the organization have significant interest in the financial

information of the organization because they are exposed to the risk in relation to the

performance of the company. When financial position of the company is good then the

shareholders of the company will invest in that company to generate high returns whereas

if the company is not performing well then, the investor is not going to get much benefit

from the return on investment (Mosey, Kirkham and Noke, 2017). Therefore, financial

statements or information of the company is important to take strategic decision

regarding whether to invest in that company or not and helps in evaluating the return on

investment according to the current and past performance of the company. Shareholders

of the company uses financial information to determine the viability and worthiness of

the organization for future dividends, share growth and returns.

Creditors: Lenders and creditors are the banks, individual, corporate and financial

institution who lend funds for the effective working of the organization. They are part of

secondary stakeholders are not directly related with the organization. Lenders critically

evaluate the financial information and statement of the company to determine the

creditability of the company. Creditors and lenders of the company who are indirectly

related to the organization investigates and examine the financial information critically to

analyse the credit rating and determine solvency of the company. It also helps in

analysing if company makes default in payment. Creditors also require financial

statements to determine and evaluate the capability of the firm to pay back the funds and

interest attached to the loaned fund on a timely manner to the creditors.

4

them take effective decision accordingly. Management of the organization uses financial

statements to ensure that company has long term solvency position.

External stakeholders are also referred to as secondary stakeholders. External stakeholders

are individuals and corporate like customers, general public, rating agencies, competitors,

investment analysts, suppliers, community, investors, shareholders, government, creditors,

etc. outside the organization and are affected by the operations of business. They are

interested in financial information of the company for taking strategic decision effectively

and efficiently.

Shareholders: Shareholders of the organization have significant interest in the financial

information of the organization because they are exposed to the risk in relation to the

performance of the company. When financial position of the company is good then the

shareholders of the company will invest in that company to generate high returns whereas

if the company is not performing well then, the investor is not going to get much benefit

from the return on investment (Mosey, Kirkham and Noke, 2017). Therefore, financial

statements or information of the company is important to take strategic decision

regarding whether to invest in that company or not and helps in evaluating the return on

investment according to the current and past performance of the company. Shareholders

of the company uses financial information to determine the viability and worthiness of

the organization for future dividends, share growth and returns.

Creditors: Lenders and creditors are the banks, individual, corporate and financial

institution who lend funds for the effective working of the organization. They are part of

secondary stakeholders are not directly related with the organization. Lenders critically

evaluate the financial information and statement of the company to determine the

creditability of the company. Creditors and lenders of the company who are indirectly

related to the organization investigates and examine the financial information critically to

analyse the credit rating and determine solvency of the company. It also helps in

analysing if company makes default in payment. Creditors also require financial

statements to determine and evaluate the capability of the firm to pay back the funds and

interest attached to the loaned fund on a timely manner to the creditors.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Government: Government bodies or tax authorities are interested in the financial

statements of the company to determine and evaluate its financial position and how they

are currently performing to compute the tax. Financial information of the company plays

a key role in evaluating the amount of tax which is to be paid to the government or tax

authority after all deductions from the profits. Government also plays key role in

formulating plans, policies and strategies for the development of the company and

economy. It helps in assessing the amount of tax payable by the company which helps in

economic growth of the company (Narayanaswamy, 2017).

Competitors: There are several rivalry competitors present in the market who offer same

range of products at the affordable price which attract large number of customers.

Competitors in the market critically evaluate the financial information and statement of

the organization to examine the financial position of the company. This helps competitors

in altering their plans and make strategic decision to gain market share in the market for

higher customer base and profitability to maintain competitive edge in the market and

survive for the longer period of time in the market. Competitors take into consideration

various financial ratios like profitability ratios which help determine the financial

position of the company. If the competitor has higher revenue, then it states that company

performs in economies of scale. Therefore, financial statements or information helps in

determining and evaluating the competitive advantage of the company which helps

competitors take strategic decision to improve their operational efficiency and

productivity to maintain competitive edge in the market and expand their business by

attracting more new customers which leads to higher profit and attaining higher market

share.

PART B

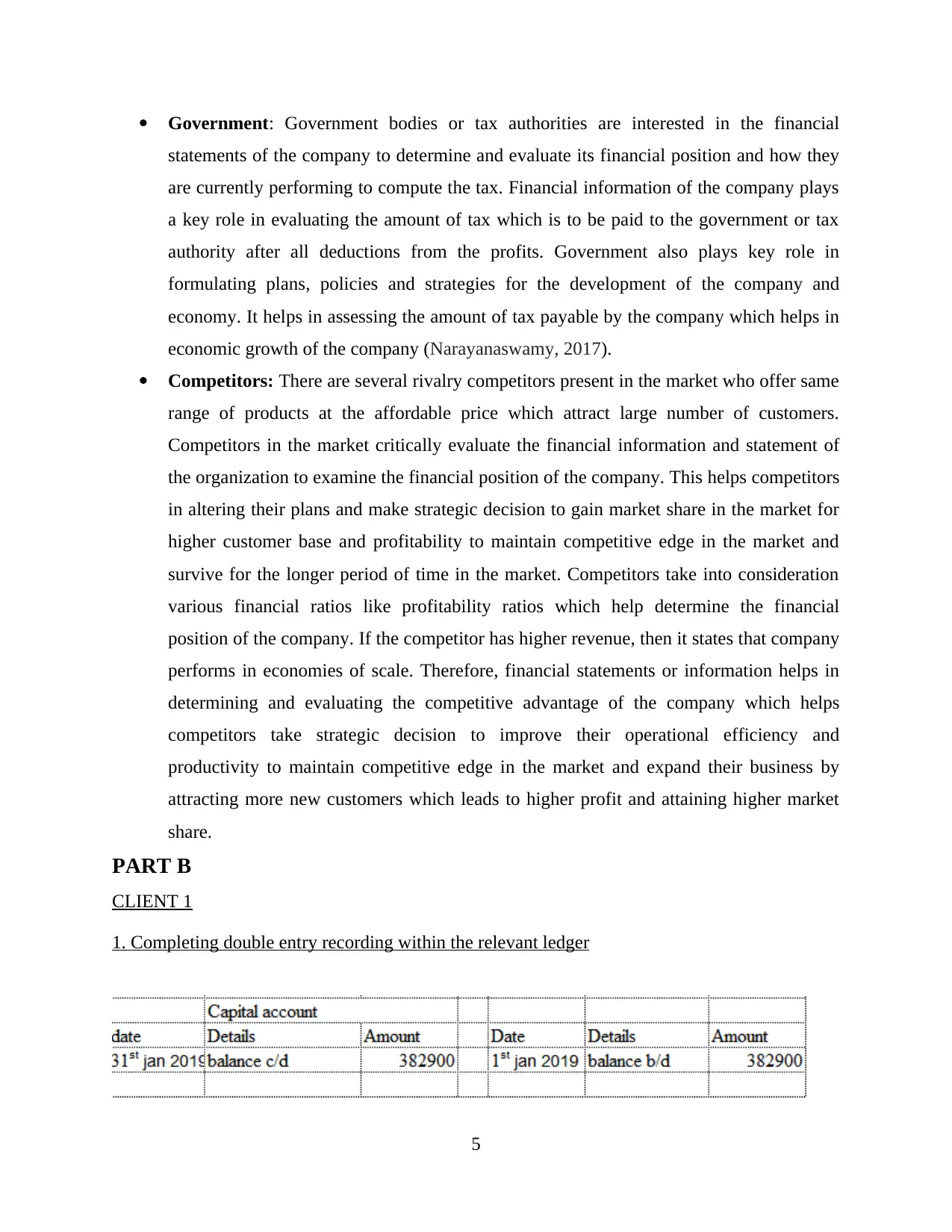

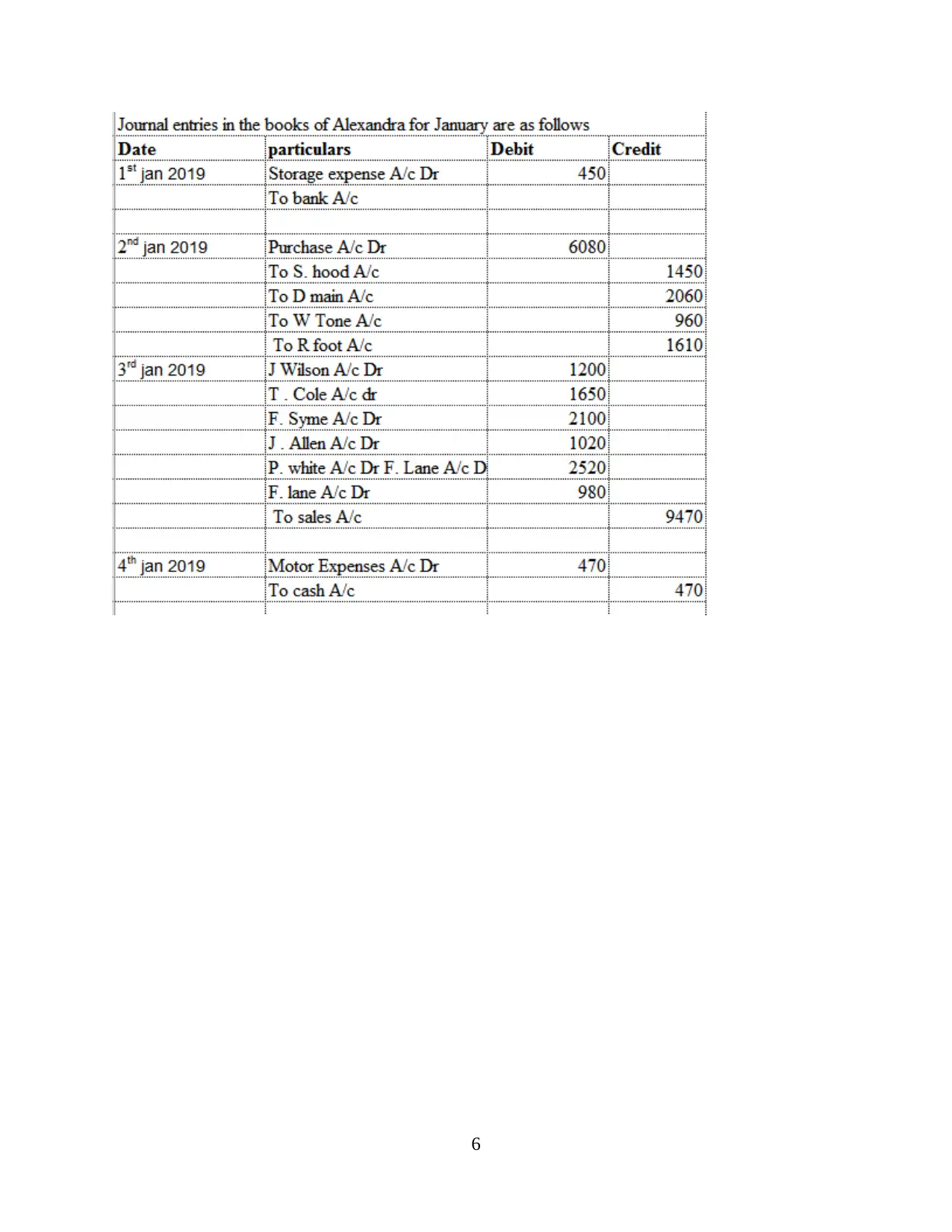

CLIENT 1

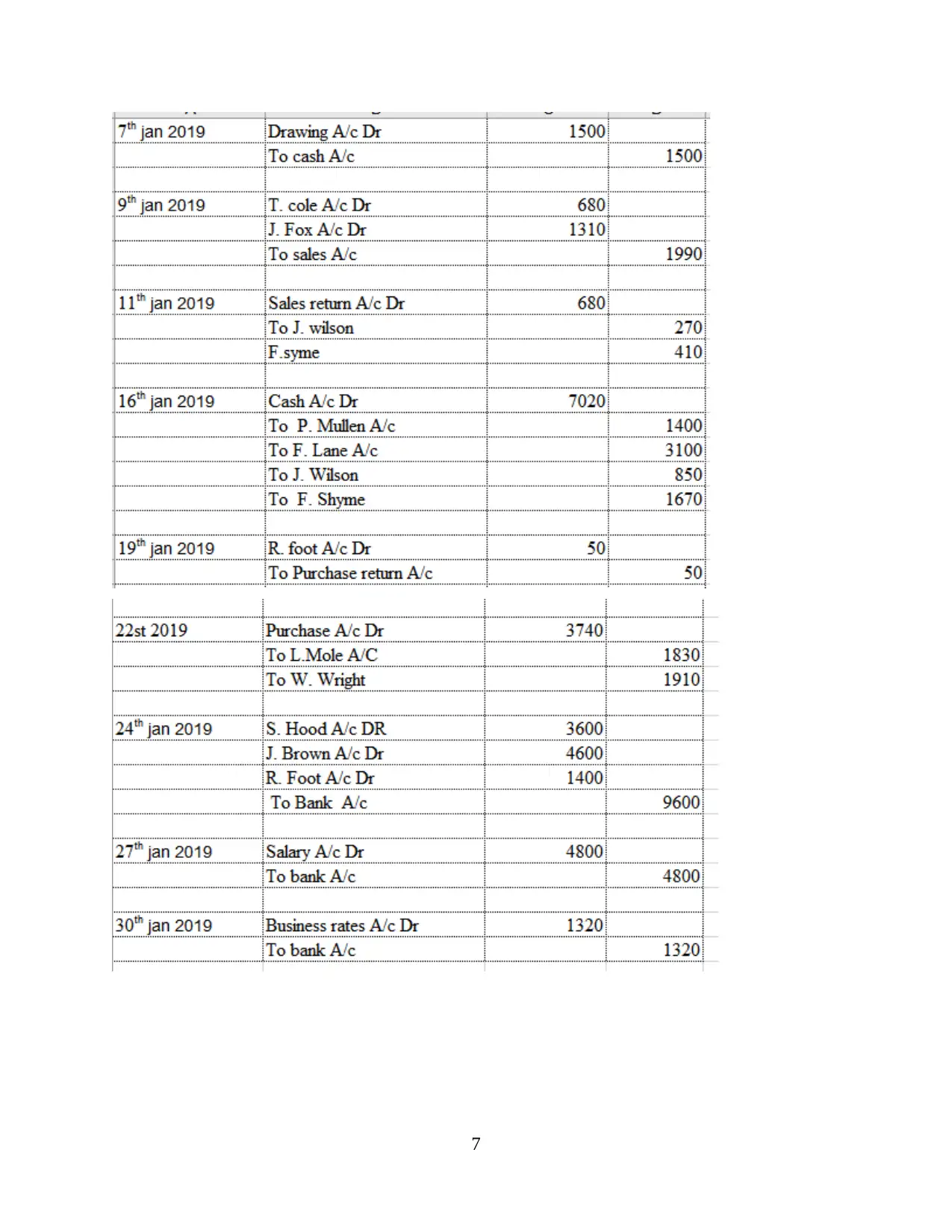

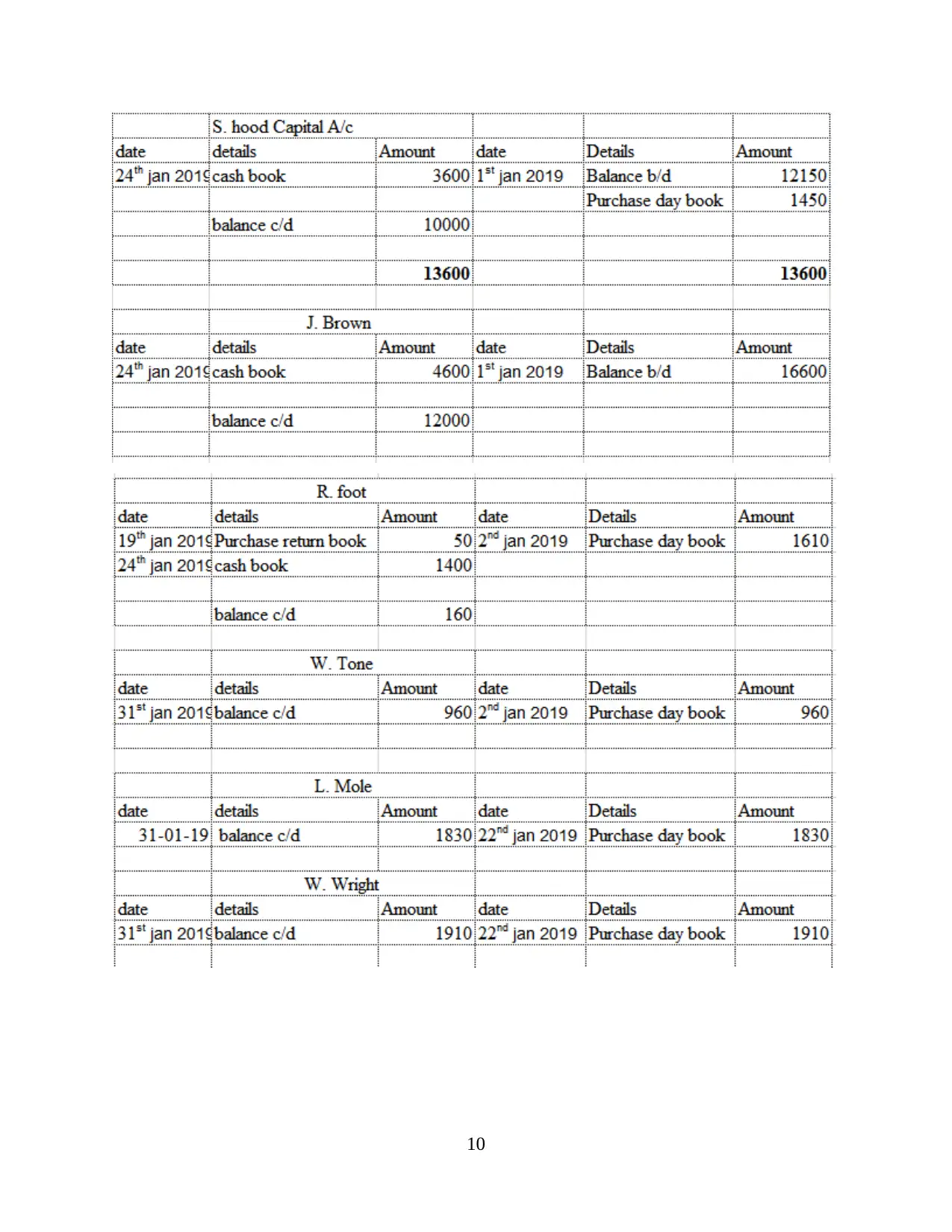

1. Completing double entry recording within the relevant ledger

5

statements of the company to determine and evaluate its financial position and how they

are currently performing to compute the tax. Financial information of the company plays

a key role in evaluating the amount of tax which is to be paid to the government or tax

authority after all deductions from the profits. Government also plays key role in

formulating plans, policies and strategies for the development of the company and

economy. It helps in assessing the amount of tax payable by the company which helps in

economic growth of the company (Narayanaswamy, 2017).

Competitors: There are several rivalry competitors present in the market who offer same

range of products at the affordable price which attract large number of customers.

Competitors in the market critically evaluate the financial information and statement of

the organization to examine the financial position of the company. This helps competitors

in altering their plans and make strategic decision to gain market share in the market for

higher customer base and profitability to maintain competitive edge in the market and

survive for the longer period of time in the market. Competitors take into consideration

various financial ratios like profitability ratios which help determine the financial

position of the company. If the competitor has higher revenue, then it states that company

performs in economies of scale. Therefore, financial statements or information helps in

determining and evaluating the competitive advantage of the company which helps

competitors take strategic decision to improve their operational efficiency and

productivity to maintain competitive edge in the market and expand their business by

attracting more new customers which leads to higher profit and attaining higher market

share.

PART B

CLIENT 1

1. Completing double entry recording within the relevant ledger

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

6

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

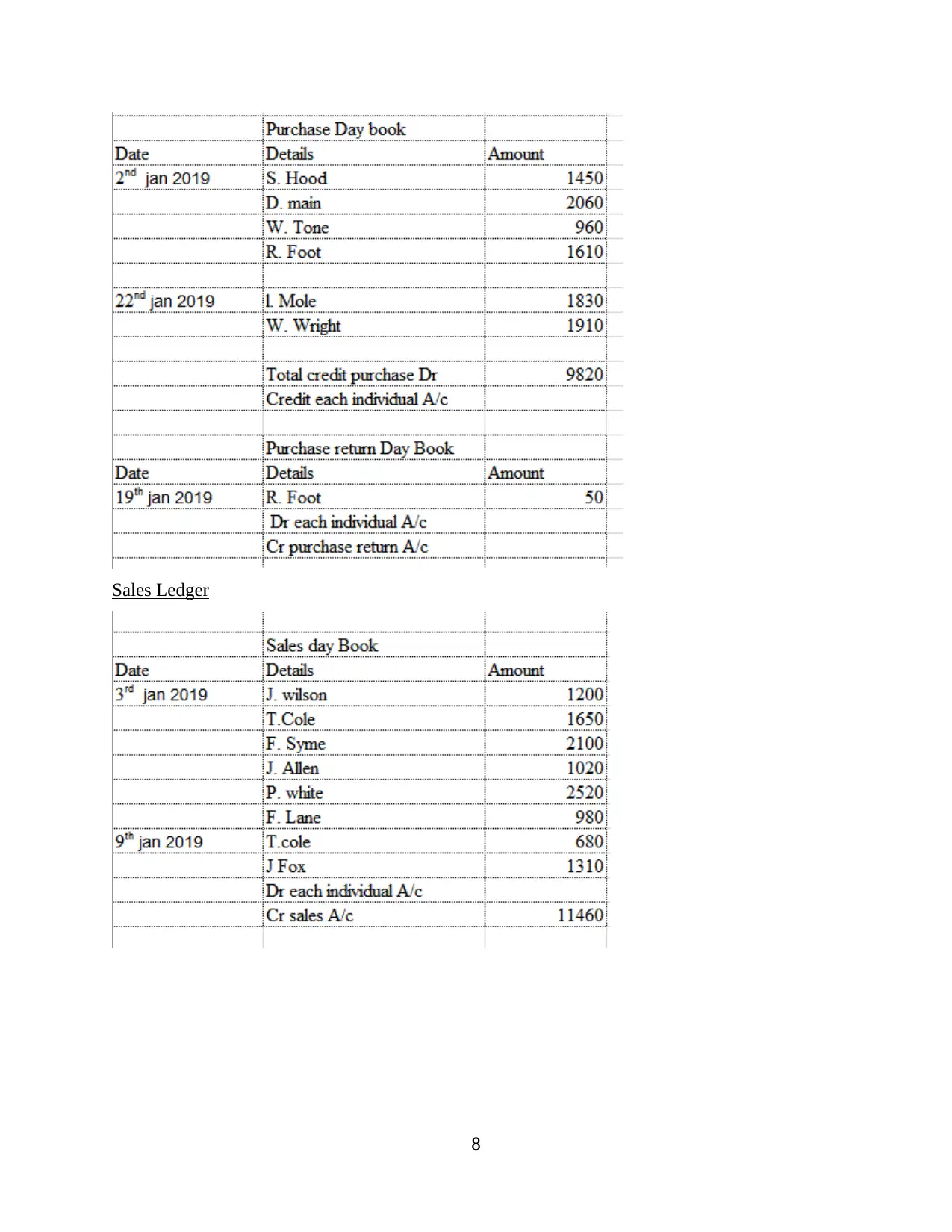

Sales Ledger

8

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

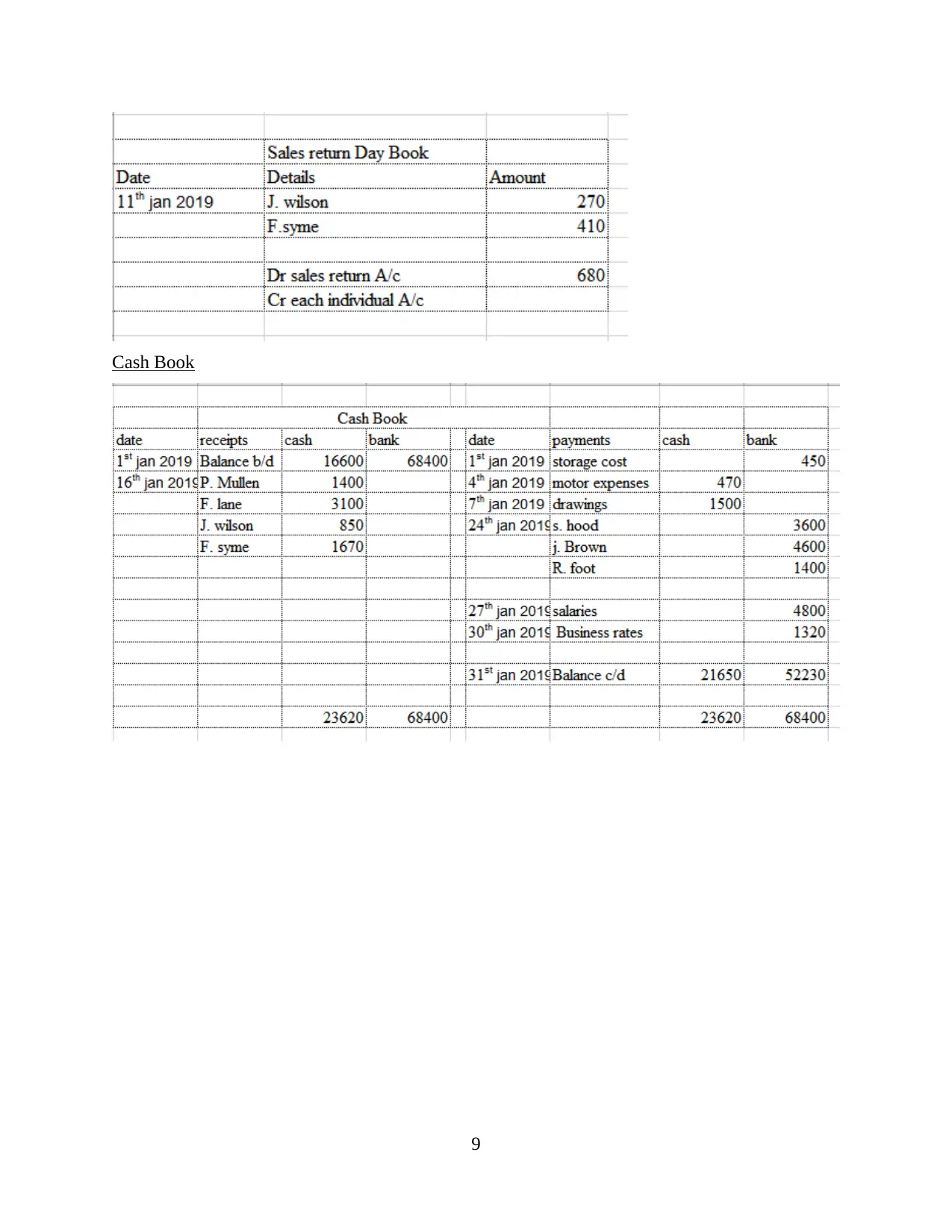

Cash Book

9

9

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.