Financial Accounting Assignment - Question Answers

VerifiedAdded on 2020/05/16

|12

|1173

|379

Homework Assignment

AI Summary

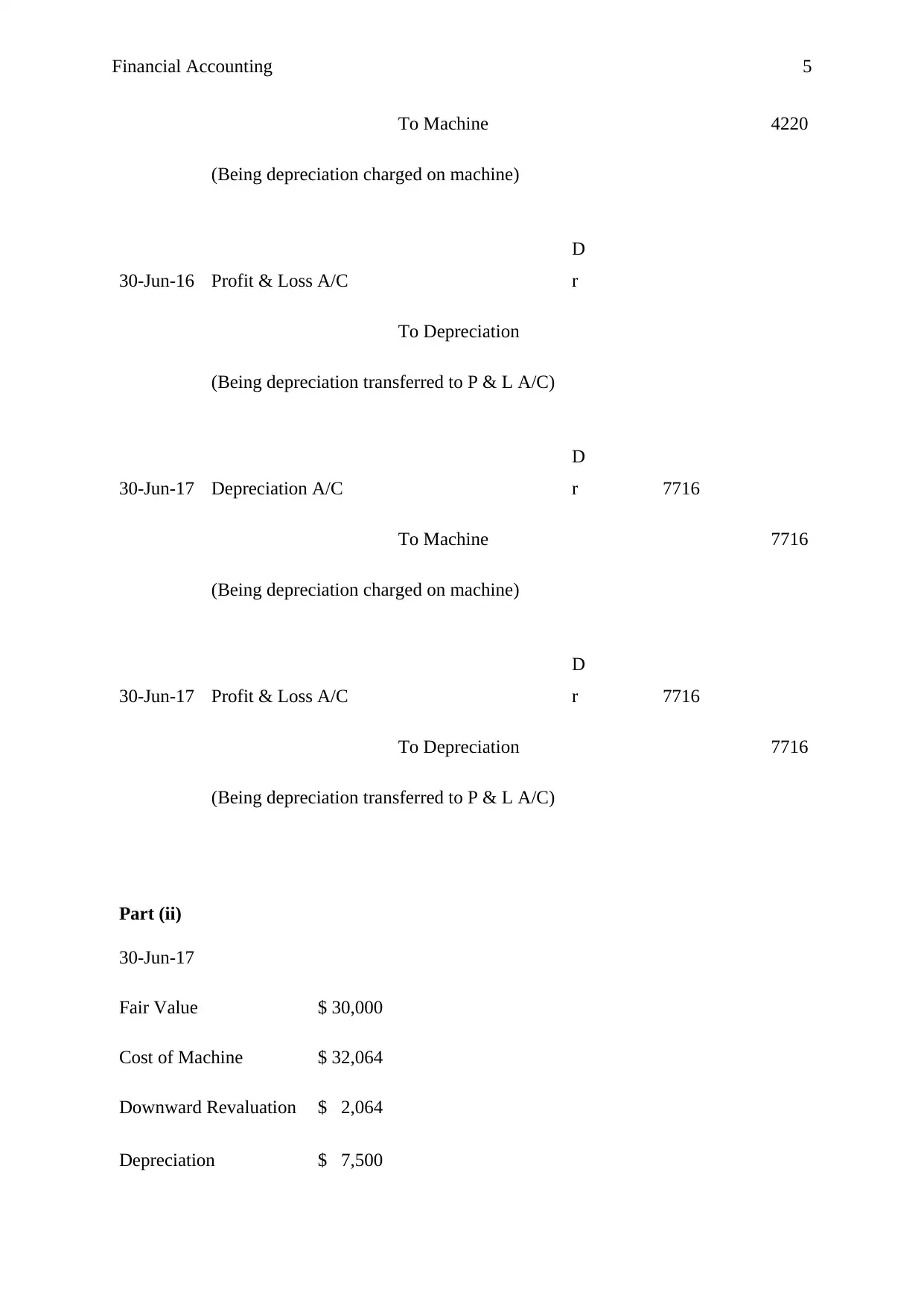

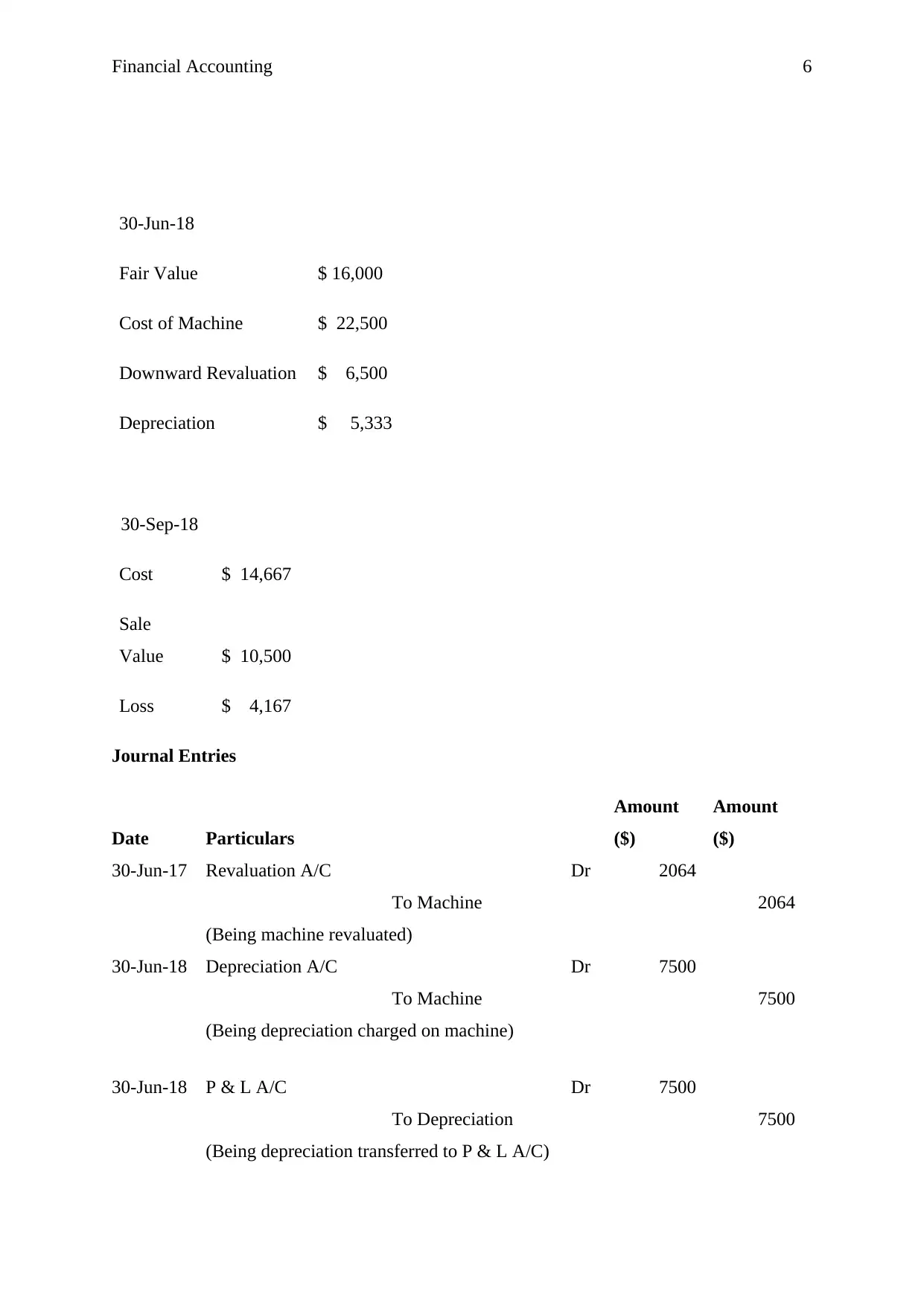

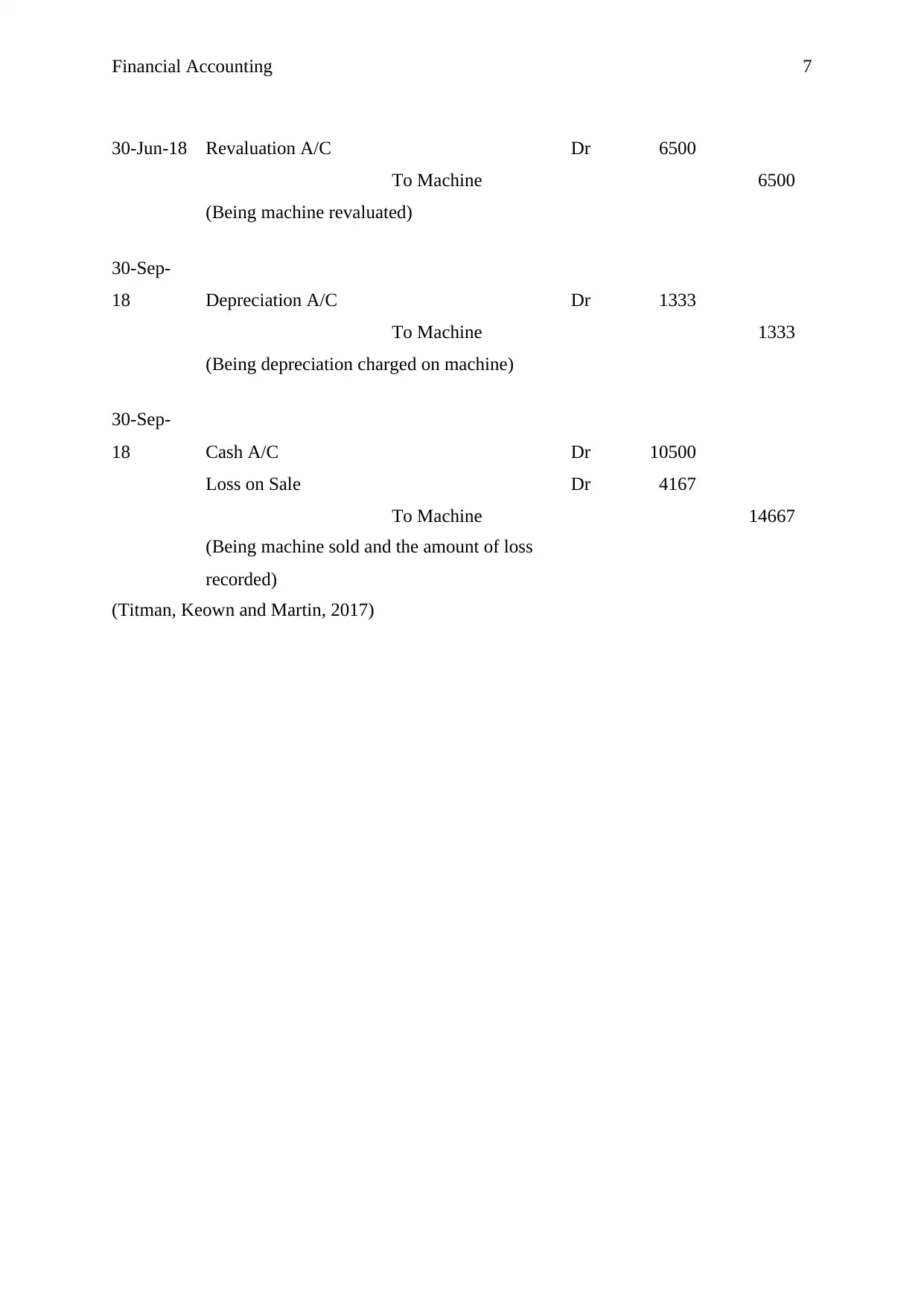

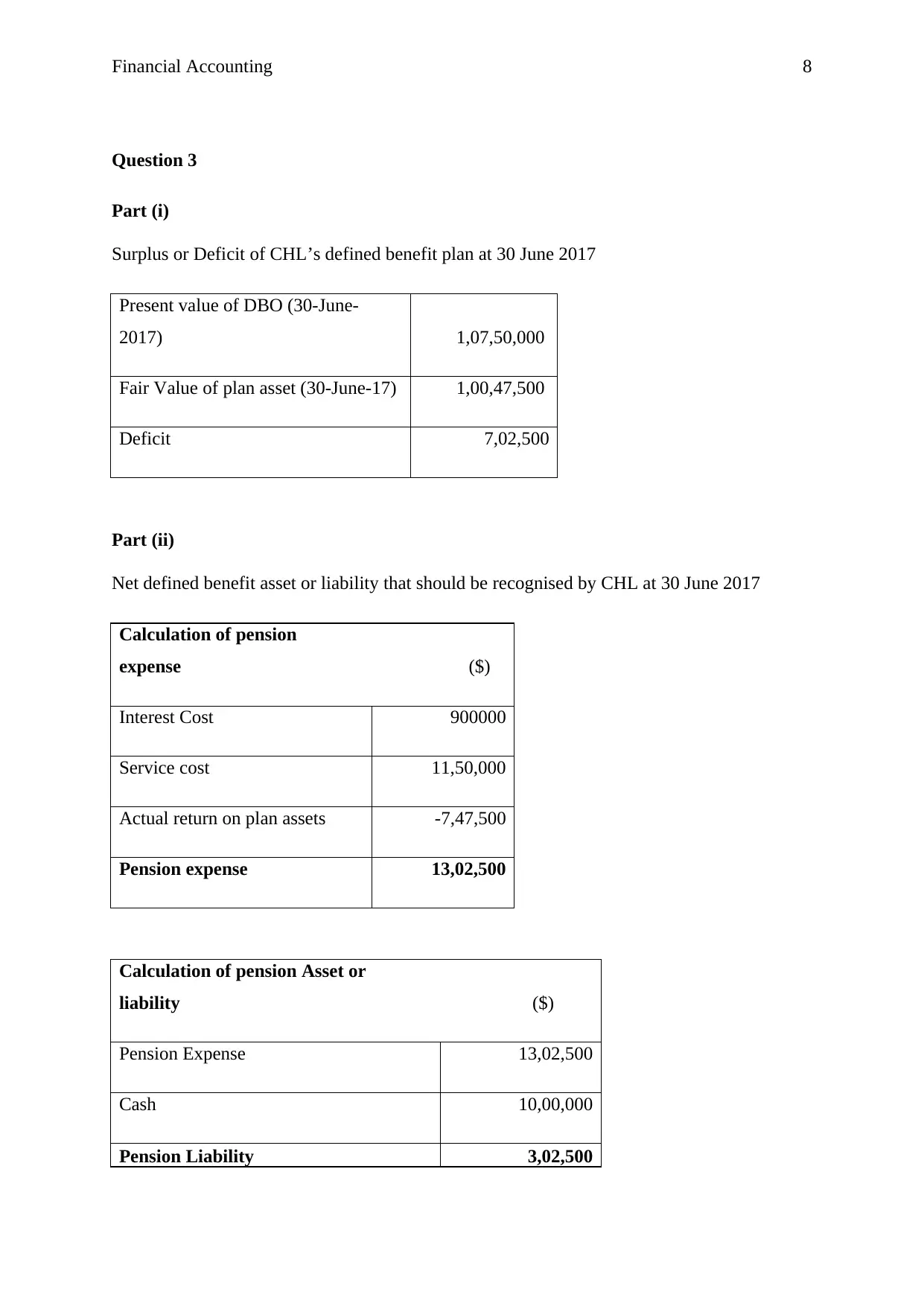

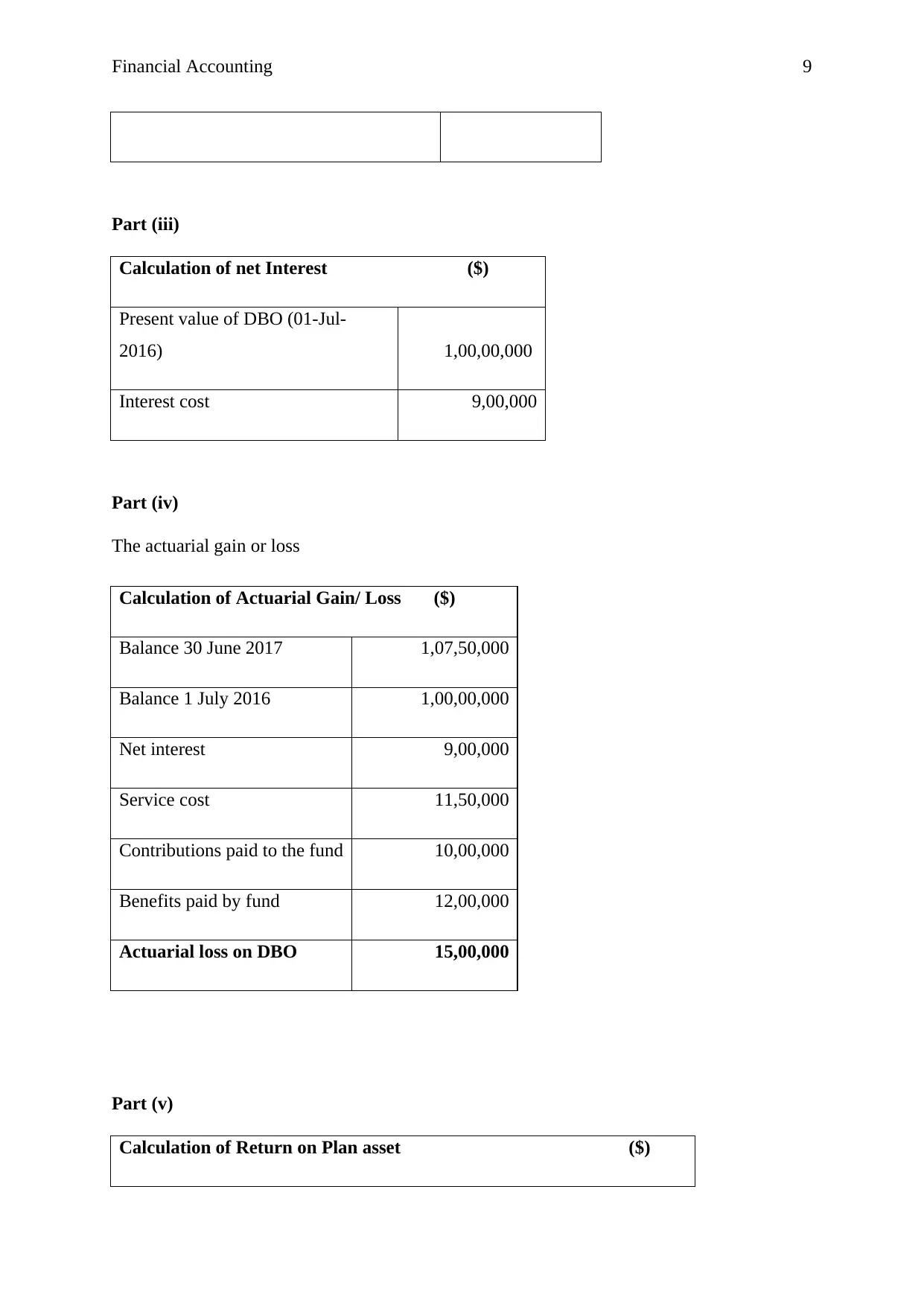

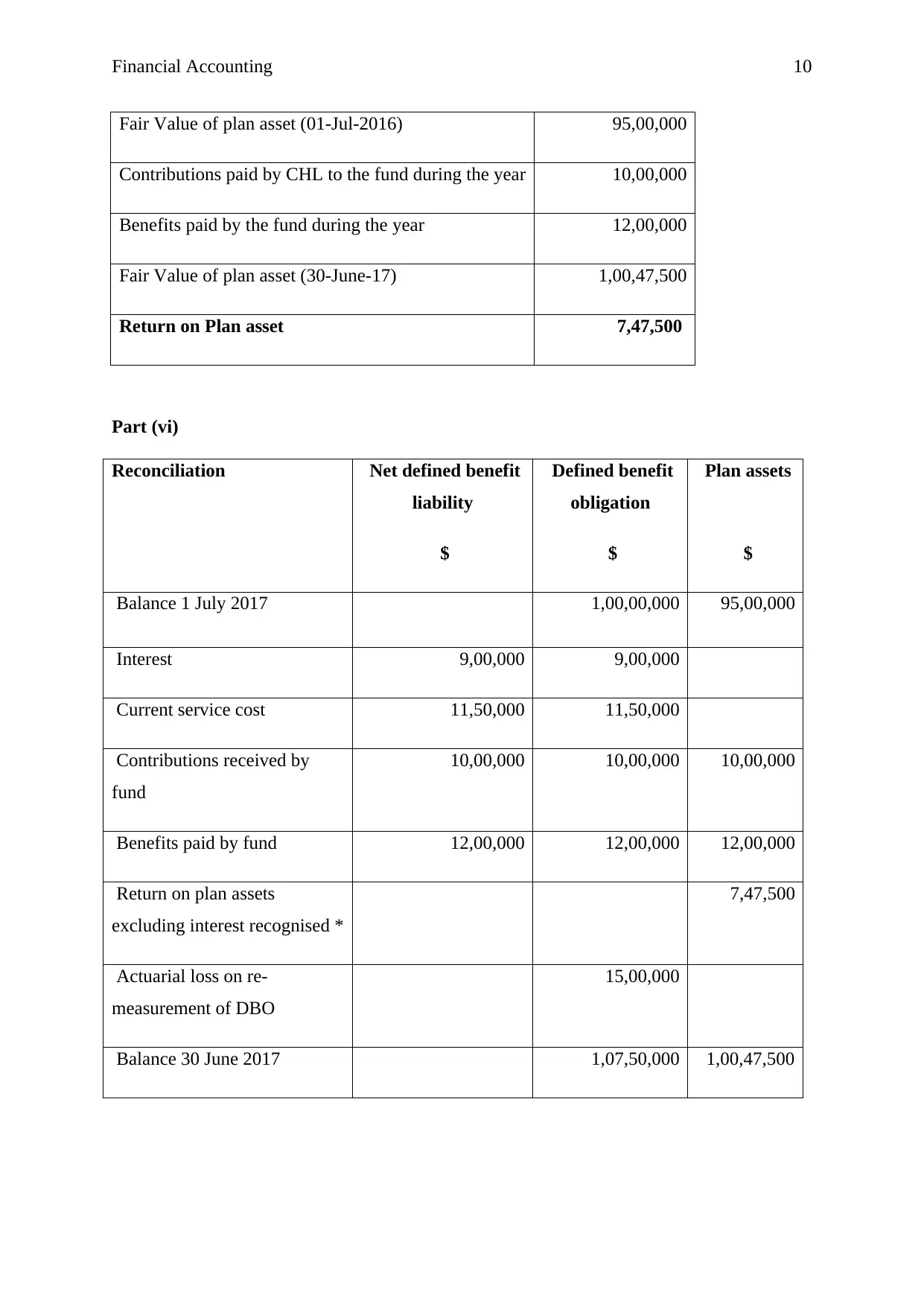

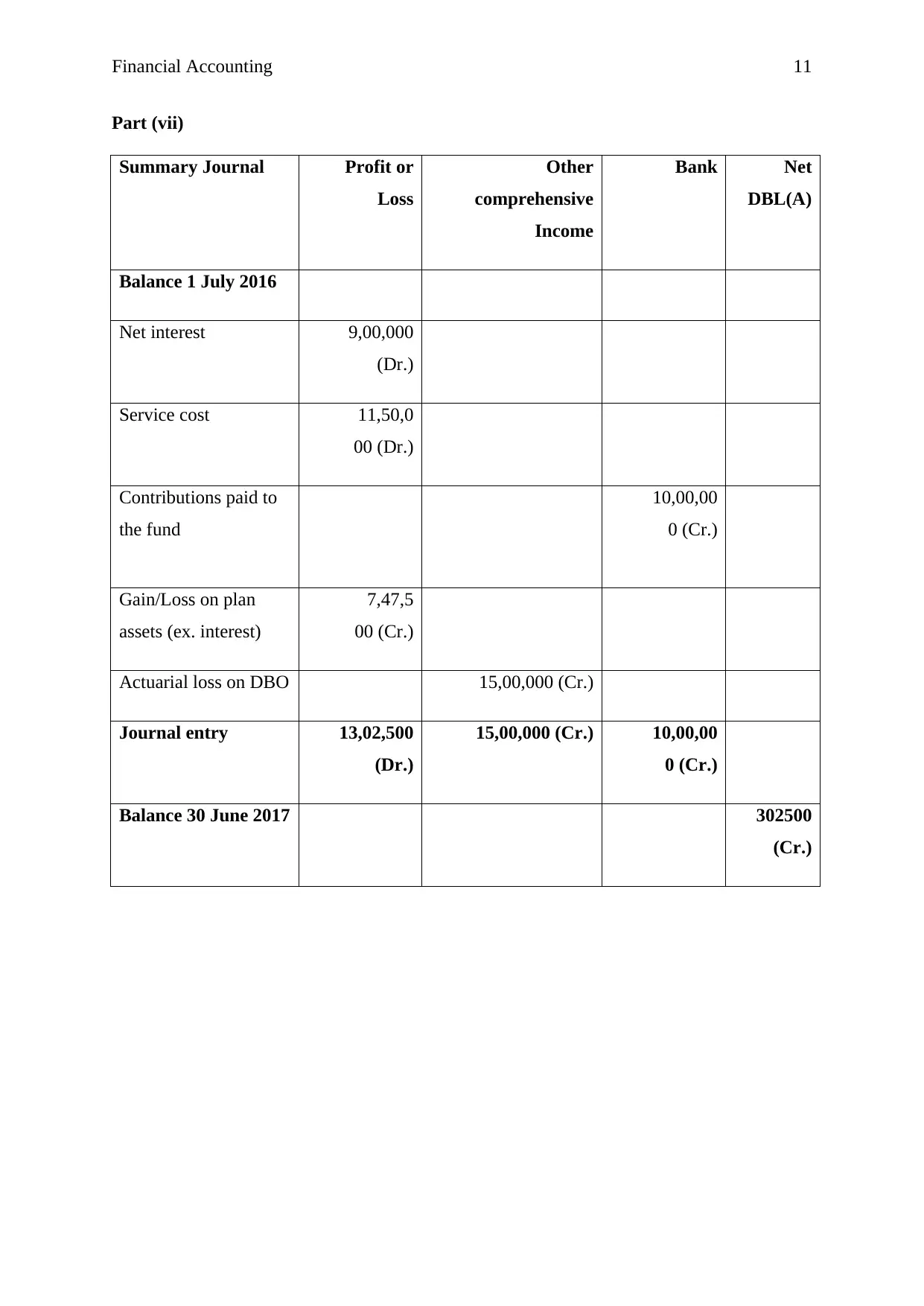

This financial accounting assignment solution addresses key concepts in financial reporting, including fair value accounting, depreciation, and pension accounting. Question 1 explores the application of fair value to assets without an active market, referencing AASB 13 and considering valuation methods based on similar assets or expert assumptions. Question 2 presents depreciation calculations using the straight-line method, along with journal entries for depreciation and revaluation of a printing machine. It also covers the sale of an asset. Question 3 delves into pension accounting, calculating the surplus or deficit of a defined benefit plan, pension expense, and net interest. It includes the calculation of actuarial gains or losses, return on plan assets, and a reconciliation of the net defined benefit liability, accompanied by relevant journal entries. The solution references accounting standards and provides detailed calculations and explanations to enhance understanding of these core financial accounting topics.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.