Financial Accounting Assignment: Comprehensive Analysis of Accounts

VerifiedAdded on 2022/11/24

|28

|4585

|487

Homework Assignment

AI Summary

This document presents a detailed solution to a financial accounting assignment, addressing a range of topics including different types of business transactions, single and double-entry bookkeeping, and the preparation of journal entries. The solution includes calculations, the creation of ledger accounts, and the development of a trial balance. It differentiates between financial statements and financial reports, outlines key accounting principles, and provides examples of profit and loss accounts, balance sheets, and cash flow statements. The assignment also covers scenario-based problems such as bank reconciliations, control accounts, suspense accounts, and the preparation of updated cash books and bank reconciliation statements, including associated journal entries. The assignment emphasizes the importance of understanding financial accounting concepts and applying them to solve practical problems, providing a comprehensive overview of accounting practices and financial statement analysis.

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................3

QUESTION 1.................................................................................................................................................3

Different types of business transaction...................................................................................................3

QUESTION 2.................................................................................................................................................5

Calculation...............................................................................................................................................5

QUESTION 3...............................................................................................................................................10

Different between financial statement and financial report.................................................................10

QUESTION 4...............................................................................................................................................12

Principles of accounting.........................................................................................................................12

QUESTION 5...............................................................................................................................................13

Calculation.............................................................................................................................................13

QUESTION 6...............................................................................................................................................15

Profit and Loss Account.........................................................................................................................15

QUESTION 7...............................................................................................................................................16

Cash flow statement..............................................................................................................................16

SCENARIO 2...............................................................................................................................................18

QUESTION 1...............................................................................................................................................18

Bank Reconciliation...............................................................................................................................18

QUESTION 2...............................................................................................................................................19

Control accounts....................................................................................................................................19

QUESTION 3...............................................................................................................................................20

Suspense Account..................................................................................................................................20

QUESTION 4...............................................................................................................................................21

(a) Required to prepare updated cash book and bank reconciliation statement..................................21

QUESTION 5...............................................................................................................................................23

Journal entries.......................................................................................................................................23

CONCLUSION.............................................................................................................................................25

REFERENCES..............................................................................................................................................26

INTRODUCTION...........................................................................................................................................3

QUESTION 1.................................................................................................................................................3

Different types of business transaction...................................................................................................3

QUESTION 2.................................................................................................................................................5

Calculation...............................................................................................................................................5

QUESTION 3...............................................................................................................................................10

Different between financial statement and financial report.................................................................10

QUESTION 4...............................................................................................................................................12

Principles of accounting.........................................................................................................................12

QUESTION 5...............................................................................................................................................13

Calculation.............................................................................................................................................13

QUESTION 6...............................................................................................................................................15

Profit and Loss Account.........................................................................................................................15

QUESTION 7...............................................................................................................................................16

Cash flow statement..............................................................................................................................16

SCENARIO 2...............................................................................................................................................18

QUESTION 1...............................................................................................................................................18

Bank Reconciliation...............................................................................................................................18

QUESTION 2...............................................................................................................................................19

Control accounts....................................................................................................................................19

QUESTION 3...............................................................................................................................................20

Suspense Account..................................................................................................................................20

QUESTION 4...............................................................................................................................................21

(a) Required to prepare updated cash book and bank reconciliation statement..................................21

QUESTION 5...............................................................................................................................................23

Journal entries.......................................................................................................................................23

CONCLUSION.............................................................................................................................................25

REFERENCES..............................................................................................................................................26

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial accounting is the process of recording, summarizing and analyzing a corporation's

money transfer in order to achieve an accurate image of the company's financial condition and

performance. The creation of accounting policies other than an accounting records, cash flow

statement, and profitability statement – which capture their operational efficiency over a certain

period and liquidity statements at a single point in time is the primary goal of financial

accounting. Financial accounting is a branch of accounting that assists businesses in reflecting on

their assets and debts (balance sheet), sales and costs (income statement), and working capital

(operating cash declaration) (cash flow statement). Those spaces can be utilized for both internal

and exterior reasons especially when combined.

The work is split into two categories, one with its own amount of details. Some problems,

such as the types of investments integrating single-entry and double-entry bookkeeping, balance

sheet, and its usefulness, should always be completed well before the portion can be performed.

The second section of this component aims at creating journal entries for each action, and

perhaps even the Documents and a Control Account. The contrast between an accounting records

and a financial results, including the fundamentals of accountants and the net profit margin, are

all provided in the following section.

QUESTION 1

Different types of business transaction

A financial transaction is an operation or occurrence that has an economic or functional

impact on a firm and can be quantified in terms of finances. Accounting systems are any

business activities that have a direct impact on the company's financial condition and income

reports. To guarantee comprehensive and term associated while preparing financial statements, a

bookkeeping system needs to be able to capture all company activities.

Commercial transaction: It involves most operations or exchanges that have been detectable in

cash form and have an immediate impact on employment processes. There are three indicators

on the industrial association's prosperity, liability, operations, and profitability. Business

activities are behaviors some of which are essential to management and are reflected in the firm's

Financial accounting is the process of recording, summarizing and analyzing a corporation's

money transfer in order to achieve an accurate image of the company's financial condition and

performance. The creation of accounting policies other than an accounting records, cash flow

statement, and profitability statement – which capture their operational efficiency over a certain

period and liquidity statements at a single point in time is the primary goal of financial

accounting. Financial accounting is a branch of accounting that assists businesses in reflecting on

their assets and debts (balance sheet), sales and costs (income statement), and working capital

(operating cash declaration) (cash flow statement). Those spaces can be utilized for both internal

and exterior reasons especially when combined.

The work is split into two categories, one with its own amount of details. Some problems,

such as the types of investments integrating single-entry and double-entry bookkeeping, balance

sheet, and its usefulness, should always be completed well before the portion can be performed.

The second section of this component aims at creating journal entries for each action, and

perhaps even the Documents and a Control Account. The contrast between an accounting records

and a financial results, including the fundamentals of accountants and the net profit margin, are

all provided in the following section.

QUESTION 1

Different types of business transaction

A financial transaction is an operation or occurrence that has an economic or functional

impact on a firm and can be quantified in terms of finances. Accounting systems are any

business activities that have a direct impact on the company's financial condition and income

reports. To guarantee comprehensive and term associated while preparing financial statements, a

bookkeeping system needs to be able to capture all company activities.

Commercial transaction: It involves most operations or exchanges that have been detectable in

cash form and have an immediate impact on employment processes. There are three indicators

on the industrial association's prosperity, liability, operations, and profitability. Business

activities are behaviors some of which are essential to management and are reflected in the firm's

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

journals. Trades and credit financial transactions are the two kinds of services that are

commonplace.

Cash buyer: Involving the incoming and exterior stream of money. It involves trades,

expenditures, and financial transactions, along with other things.

Credit trade: It is defined as any process in which currency is not demanded at the period of

contract.

Things purchased on credit, equities generated from the sale are just a few instance.

Certain events prompt expanded the union's requirement and have a consequence on future cash

flow, although merchandise supplied on credit strengthens the foundation's assets.

Define single entry book keeping:

All recorded corporate actions must be supported by some type of realistic evidence or

form, according to this notion. It also indicates that accountancy and financial information

should be kept separately, free of any suspicion of impropriety. Monetary accounts receivable

are handled using a single entry bookkeeping system. Only one instruction is executed by the

bookkeeper. Like the double input system, there are no card payment sides.

Define double entry book keeping:

Entrance with two doors Every monetary transaction is handled by two or more accounts in the

accounting system. A individual, for example, sold a piece of wood at a marketplace. As a result,

the monthly payment accounts will grow, but the furniture account will drop by the same

amount. In today's world, it's a key concept that encompasses books of accounts. Each monetary

transaction has an opposite and comparable effect on two separate accounts.

Explain trial balance and its importance:

It is a report that outlines a statement of all information shared all business dealings most of

which are documented in the logbook records. In this circumstance, every company holding

quantities have really been represented on the document's bank transfer section. In other regards,

a trial balance is a marketed at the ending of every accountancy year just to represent the debit

commonplace.

Cash buyer: Involving the incoming and exterior stream of money. It involves trades,

expenditures, and financial transactions, along with other things.

Credit trade: It is defined as any process in which currency is not demanded at the period of

contract.

Things purchased on credit, equities generated from the sale are just a few instance.

Certain events prompt expanded the union's requirement and have a consequence on future cash

flow, although merchandise supplied on credit strengthens the foundation's assets.

Define single entry book keeping:

All recorded corporate actions must be supported by some type of realistic evidence or

form, according to this notion. It also indicates that accountancy and financial information

should be kept separately, free of any suspicion of impropriety. Monetary accounts receivable

are handled using a single entry bookkeeping system. Only one instruction is executed by the

bookkeeper. Like the double input system, there are no card payment sides.

Define double entry book keeping:

Entrance with two doors Every monetary transaction is handled by two or more accounts in the

accounting system. A individual, for example, sold a piece of wood at a marketplace. As a result,

the monthly payment accounts will grow, but the furniture account will drop by the same

amount. In today's world, it's a key concept that encompasses books of accounts. Each monetary

transaction has an opposite and comparable effect on two separate accounts.

Explain trial balance and its importance:

It is a report that outlines a statement of all information shared all business dealings most of

which are documented in the logbook records. In this circumstance, every company holding

quantities have really been represented on the document's bank transfer section. In other regards,

a trial balance is a marketed at the ending of every accountancy year just to represent the debit

and credit sums of the entities but use a leading. In the framework of trial balance importance are

mentioned below:

Trial balance is used by employers to determine the debit and credit balances of accounts.

It is committed to the employees in mitigating risk through record submission.

It facilitates in the books of accounts by presenting essential data.

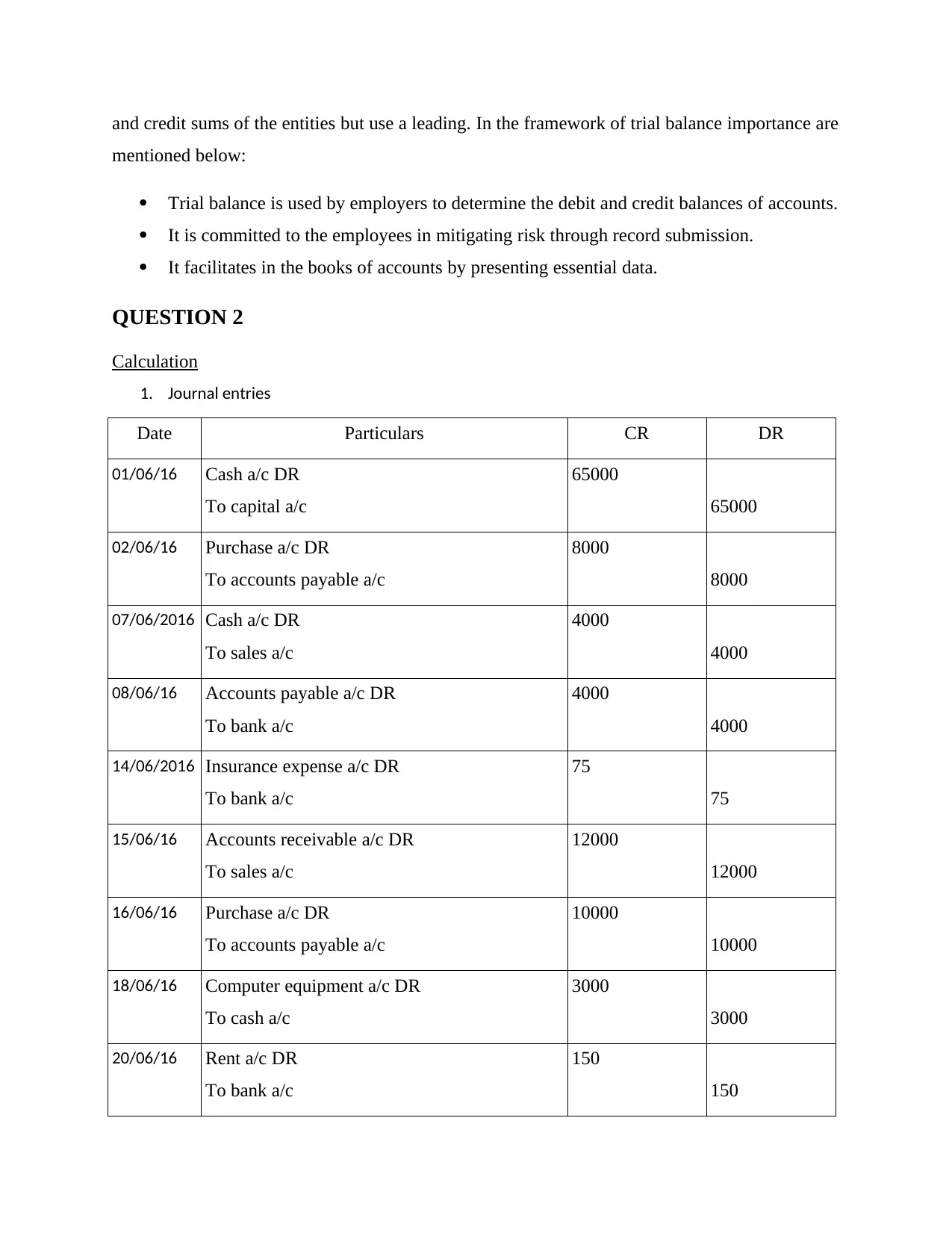

QUESTION 2

Calculation

1. Journal entries

Date Particulars CR DR

01/06/16 Cash a/c DR

To capital a/c

65000

65000

02/06/16 Purchase a/c DR

To accounts payable a/c

8000

8000

07/06/2016 Cash a/c DR

To sales a/c

4000

4000

08/06/16 Accounts payable a/c DR

To bank a/c

4000

4000

14/06/2016 Insurance expense a/c DR

To bank a/c

75

75

15/06/16 Accounts receivable a/c DR

To sales a/c

12000

12000

16/06/16 Purchase a/c DR

To accounts payable a/c

10000

10000

18/06/16 Computer equipment a/c DR

To cash a/c

3000

3000

20/06/16 Rent a/c DR

To bank a/c

150

150

mentioned below:

Trial balance is used by employers to determine the debit and credit balances of accounts.

It is committed to the employees in mitigating risk through record submission.

It facilitates in the books of accounts by presenting essential data.

QUESTION 2

Calculation

1. Journal entries

Date Particulars CR DR

01/06/16 Cash a/c DR

To capital a/c

65000

65000

02/06/16 Purchase a/c DR

To accounts payable a/c

8000

8000

07/06/2016 Cash a/c DR

To sales a/c

4000

4000

08/06/16 Accounts payable a/c DR

To bank a/c

4000

4000

14/06/2016 Insurance expense a/c DR

To bank a/c

75

75

15/06/16 Accounts receivable a/c DR

To sales a/c

12000

12000

16/06/16 Purchase a/c DR

To accounts payable a/c

10000

10000

18/06/16 Computer equipment a/c DR

To cash a/c

3000

3000

20/06/16 Rent a/c DR

To bank a/c

150

150

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

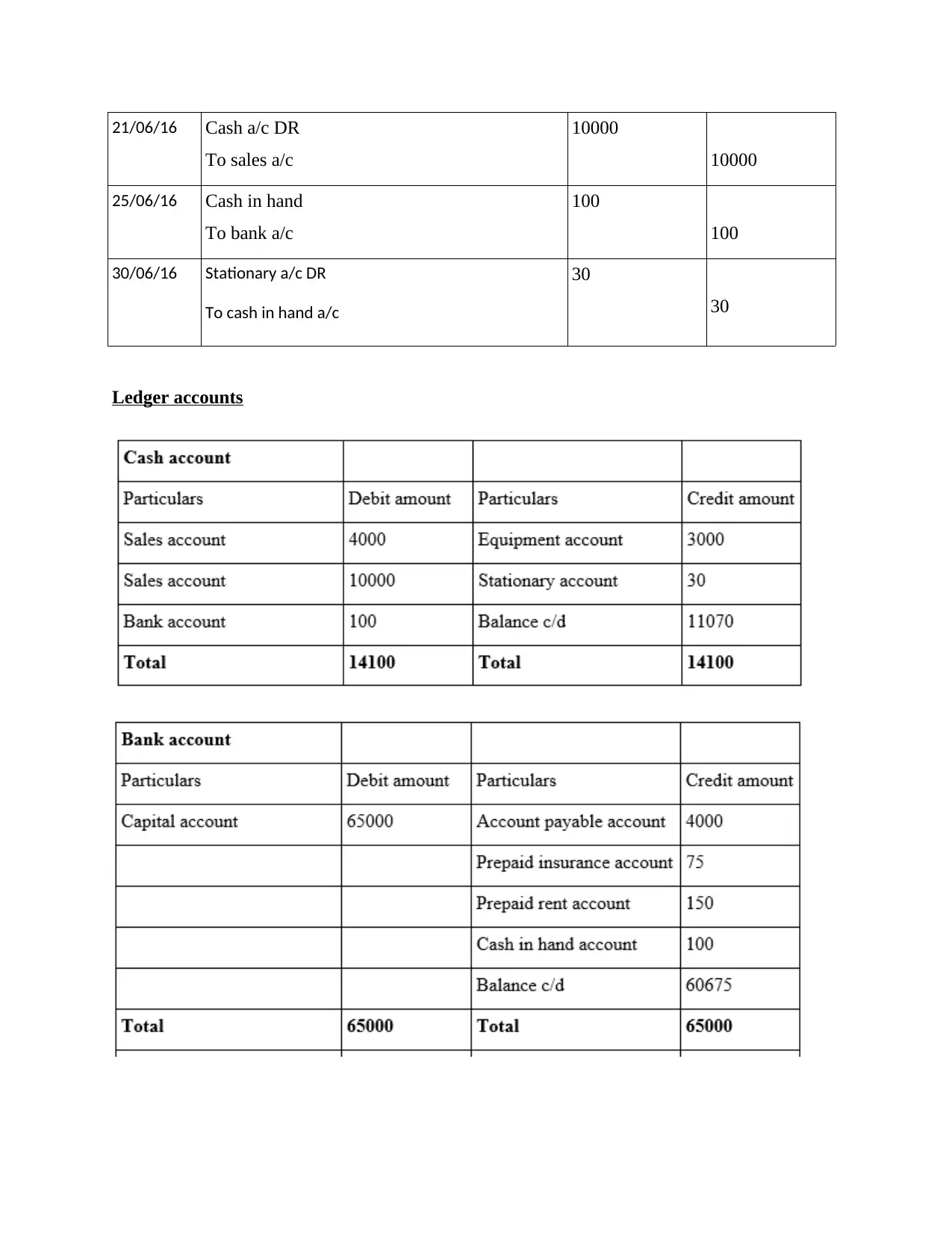

21/06/16 Cash a/c DR

To sales a/c

10000

10000

25/06/16 Cash in hand

To bank a/c

100

100

30/06/16 Stationary a/c DR

To cash in hand a/c

30

30

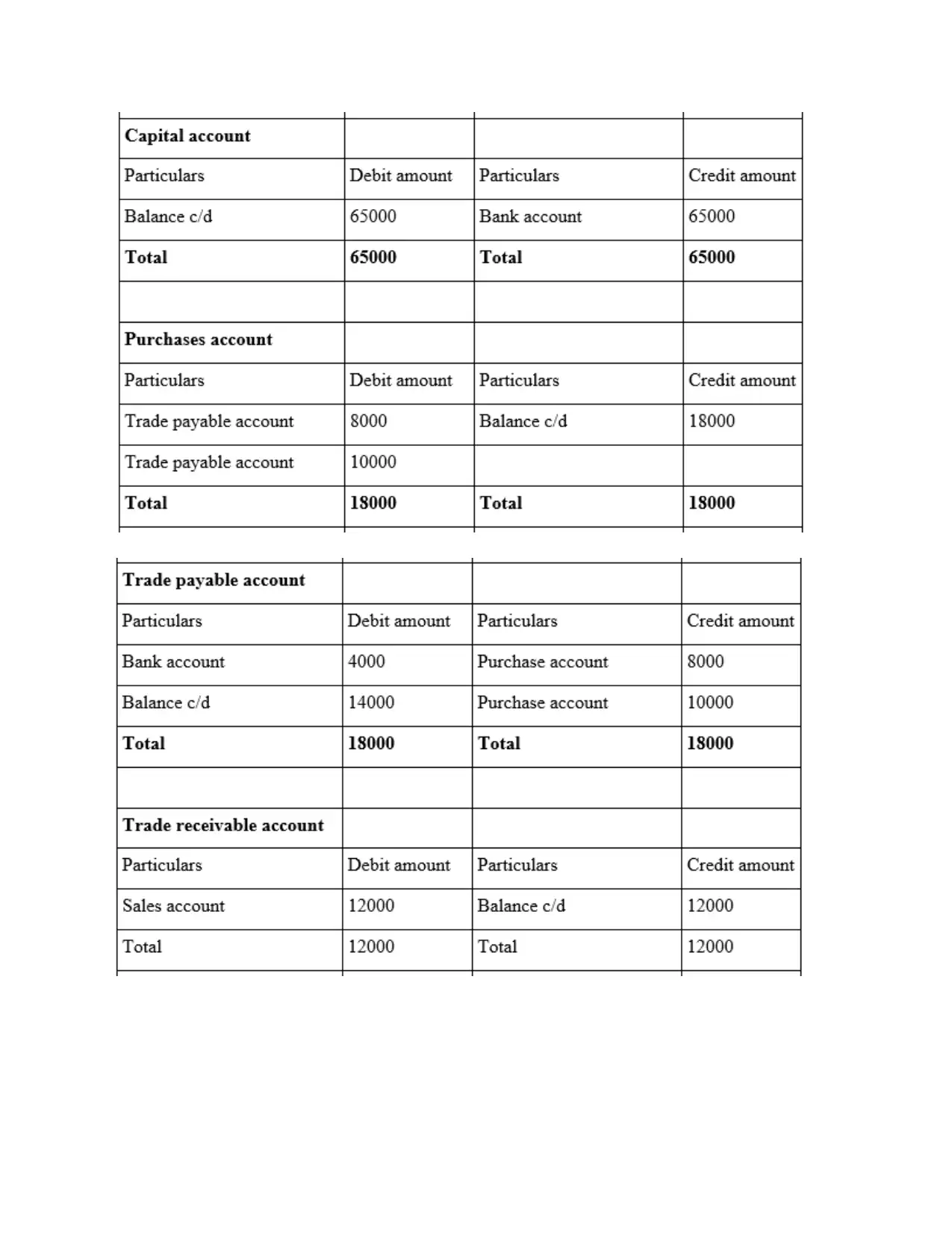

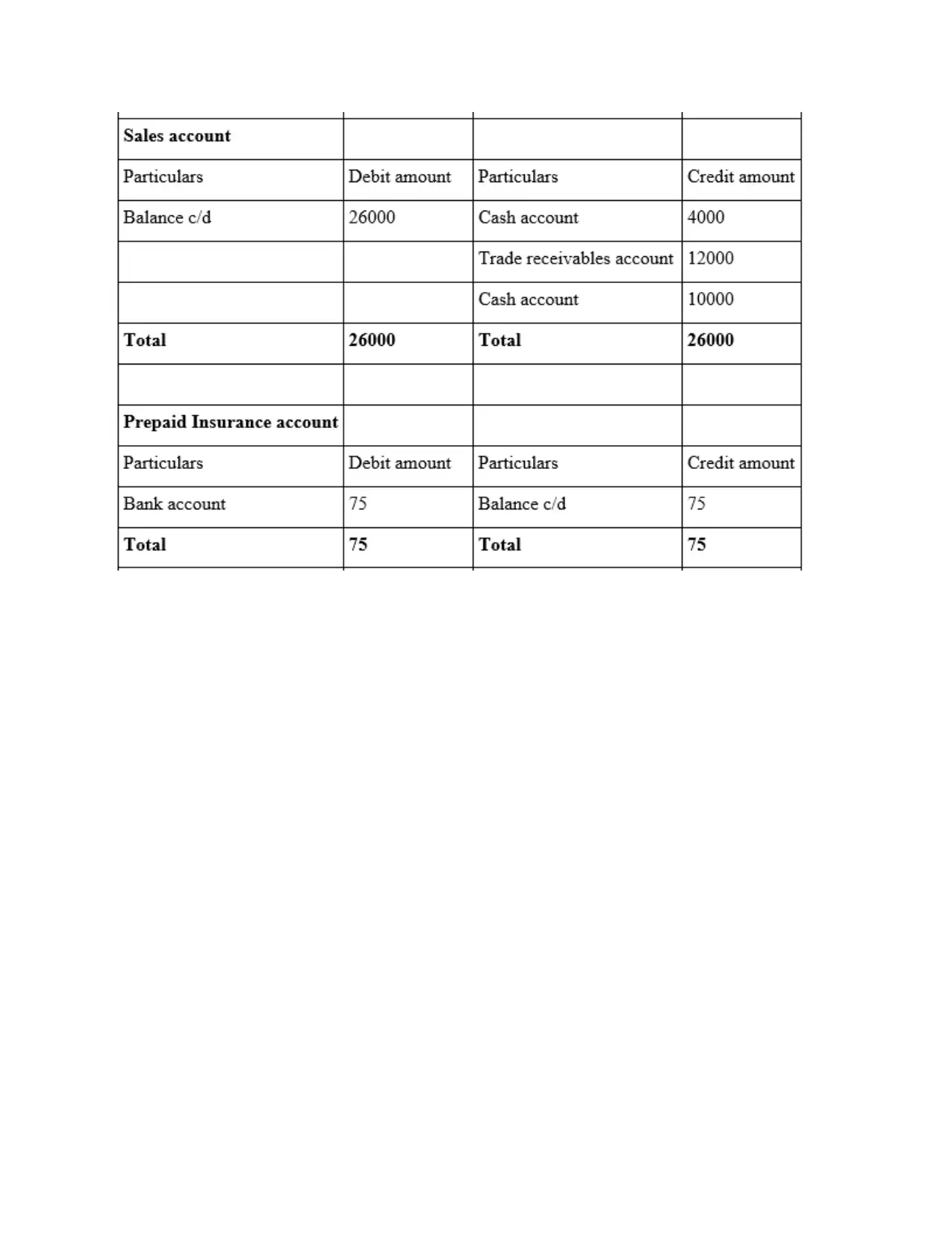

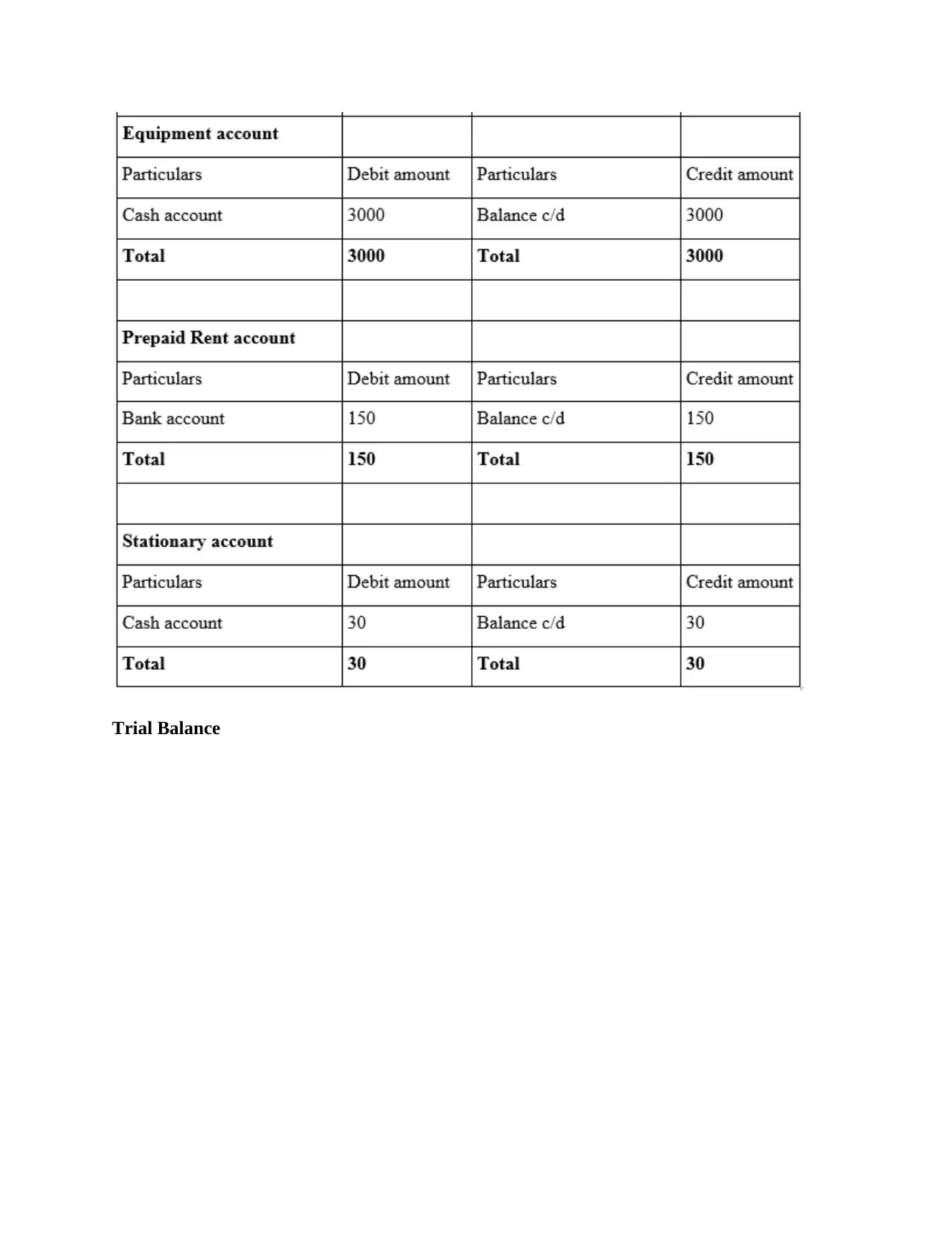

Ledger accounts

To sales a/c

10000

10000

25/06/16 Cash in hand

To bank a/c

100

100

30/06/16 Stationary a/c DR

To cash in hand a/c

30

30

Ledger accounts

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

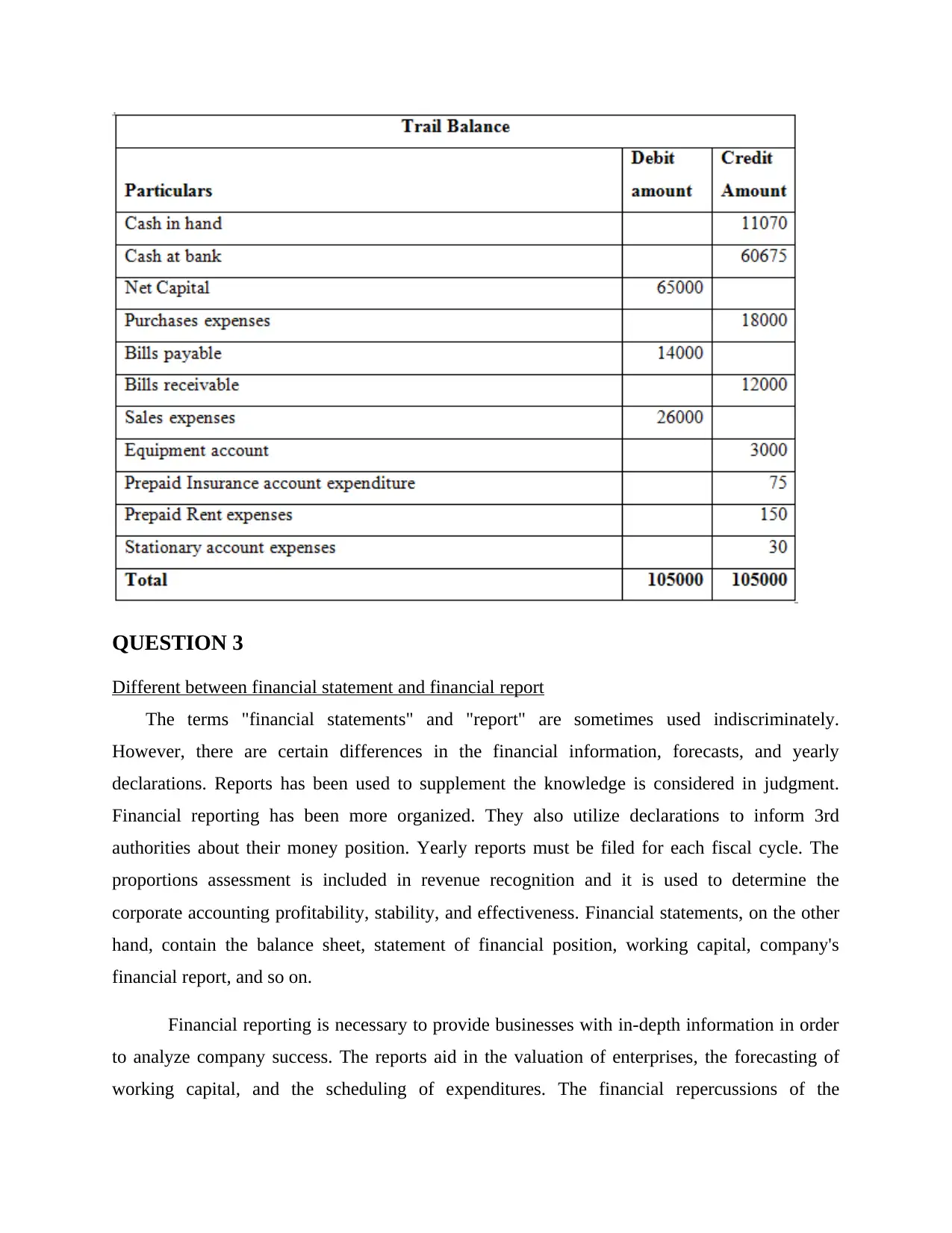

Trial Balance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUESTION 3

Different between financial statement and financial report

The terms "financial statements" and "report" are sometimes used indiscriminately.

However, there are certain differences in the financial information, forecasts, and yearly

declarations. Reports has been used to supplement the knowledge is considered in judgment.

Financial reporting has been more organized. They also utilize declarations to inform 3rd

authorities about their money position. Yearly reports must be filed for each fiscal cycle. The

proportions assessment is included in revenue recognition and it is used to determine the

corporate accounting profitability, stability, and effectiveness. Financial statements, on the other

hand, contain the balance sheet, statement of financial position, working capital, company's

financial report, and so on.

Financial reporting is necessary to provide businesses with in-depth information in order

to analyze company success. The reports aid in the valuation of enterprises, the forecasting of

working capital, and the scheduling of expenditures. The financial repercussions of the

Different between financial statement and financial report

The terms "financial statements" and "report" are sometimes used indiscriminately.

However, there are certain differences in the financial information, forecasts, and yearly

declarations. Reports has been used to supplement the knowledge is considered in judgment.

Financial reporting has been more organized. They also utilize declarations to inform 3rd

authorities about their money position. Yearly reports must be filed for each fiscal cycle. The

proportions assessment is included in revenue recognition and it is used to determine the

corporate accounting profitability, stability, and effectiveness. Financial statements, on the other

hand, contain the balance sheet, statement of financial position, working capital, company's

financial report, and so on.

Financial reporting is necessary to provide businesses with in-depth information in order

to analyze company success. The reports aid in the valuation of enterprises, the forecasting of

working capital, and the scheduling of expenditures. The financial repercussions of the

corporation's choices are shown in the accounting in the documents. Some of these documents

are for internal use, while others are utilized by other organizations. Bankers, financiers, and

public officials scrutinize the corporate accounting records. They may also need to impose

adherence limitations on revenue recognition to other authorities in order to assure uniformity.

With each document they prepare, they should take a reasoned approach.

In the perspective of Brightstar Financial Company, there are many examples of financial

accounting, which are addressed elsewhere here:

Leader: Partners and owner make government technology to help them evaluate either to hold,

borrow, or offer so much of their properties.

Owners: Managers may even be calculated and the results. In new enterprises, although, model

is commonly consisted of skilled employees who have also been responsible the administering

the enterprise or an industry sector. They act as a means of platform independent brokers.

Executives: Those other researchers are concerned about either the intermediate and long

existence or viability. They're all over whether or not organisation can paying members' wages

and bring discounts. They may also be participating in the financial condition and outcomes in

addition to assessing client services and profession promotion opportunity.

Buyers: Unless an allowing firms have had a heavier or commitment, shoppers grow committed

in the person's capacity to sustain its appearance and establish overall quality. This necessity is

intensified in conditions at which employee’s consumers depend on something.

Funders: Equity financing is essential with institutional clients in evaluate the manufacturer's

financial performance. Independent big corporations, too, involve public data and evaluate how

well an investment is worthwhile or that it should be completed, altered, or scrapped.

While its percentage of users who’s provided government accounting is minimal, there were

some who could otherwise think critically. Investors and creditors facts would be both direct and

indirect. In almost the same method, Brightstar compiles accounting records for its subscribers.

are for internal use, while others are utilized by other organizations. Bankers, financiers, and

public officials scrutinize the corporate accounting records. They may also need to impose

adherence limitations on revenue recognition to other authorities in order to assure uniformity.

With each document they prepare, they should take a reasoned approach.

In the perspective of Brightstar Financial Company, there are many examples of financial

accounting, which are addressed elsewhere here:

Leader: Partners and owner make government technology to help them evaluate either to hold,

borrow, or offer so much of their properties.

Owners: Managers may even be calculated and the results. In new enterprises, although, model

is commonly consisted of skilled employees who have also been responsible the administering

the enterprise or an industry sector. They act as a means of platform independent brokers.

Executives: Those other researchers are concerned about either the intermediate and long

existence or viability. They're all over whether or not organisation can paying members' wages

and bring discounts. They may also be participating in the financial condition and outcomes in

addition to assessing client services and profession promotion opportunity.

Buyers: Unless an allowing firms have had a heavier or commitment, shoppers grow committed

in the person's capacity to sustain its appearance and establish overall quality. This necessity is

intensified in conditions at which employee’s consumers depend on something.

Funders: Equity financing is essential with institutional clients in evaluate the manufacturer's

financial performance. Independent big corporations, too, involve public data and evaluate how

well an investment is worthwhile or that it should be completed, altered, or scrapped.

While its percentage of users who’s provided government accounting is minimal, there were

some who could otherwise think critically. Investors and creditors facts would be both direct and

indirect. In almost the same method, Brightstar compiles accounting records for its subscribers.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.