Financial Accounting Comprehensive Assignment Solution: Balance Sheet

VerifiedAdded on 2023/06/14

|9

|997

|495

Homework Assignment

AI Summary

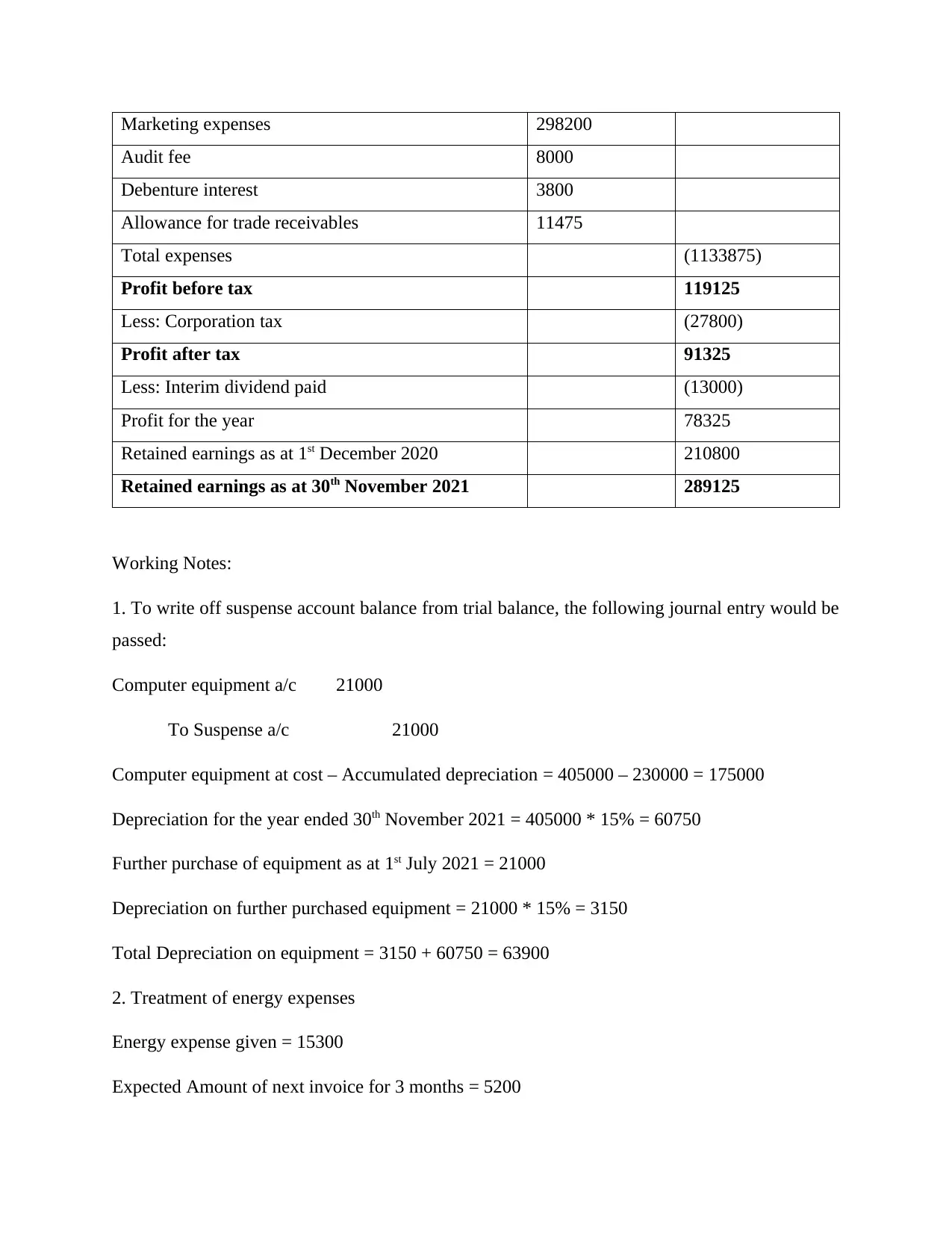

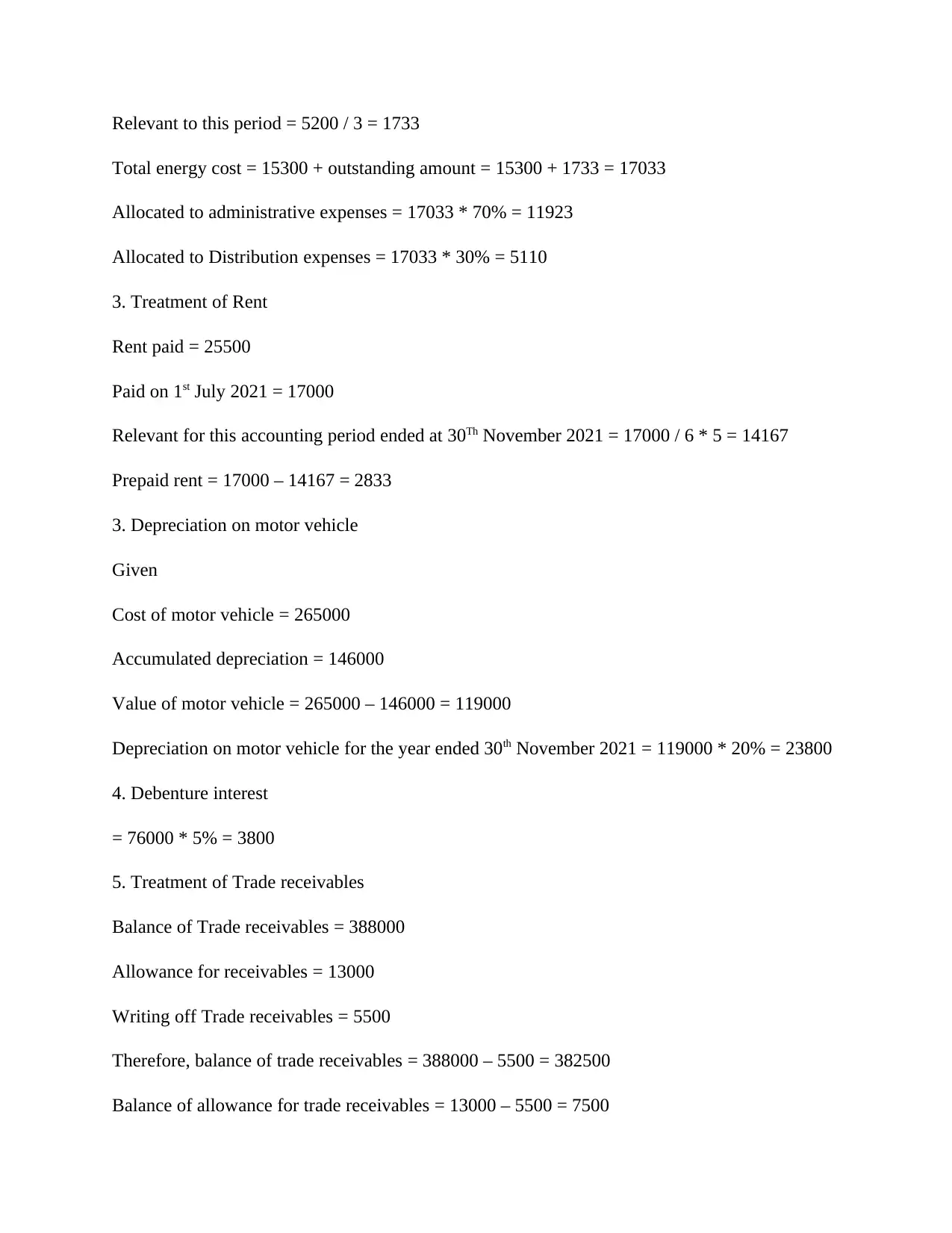

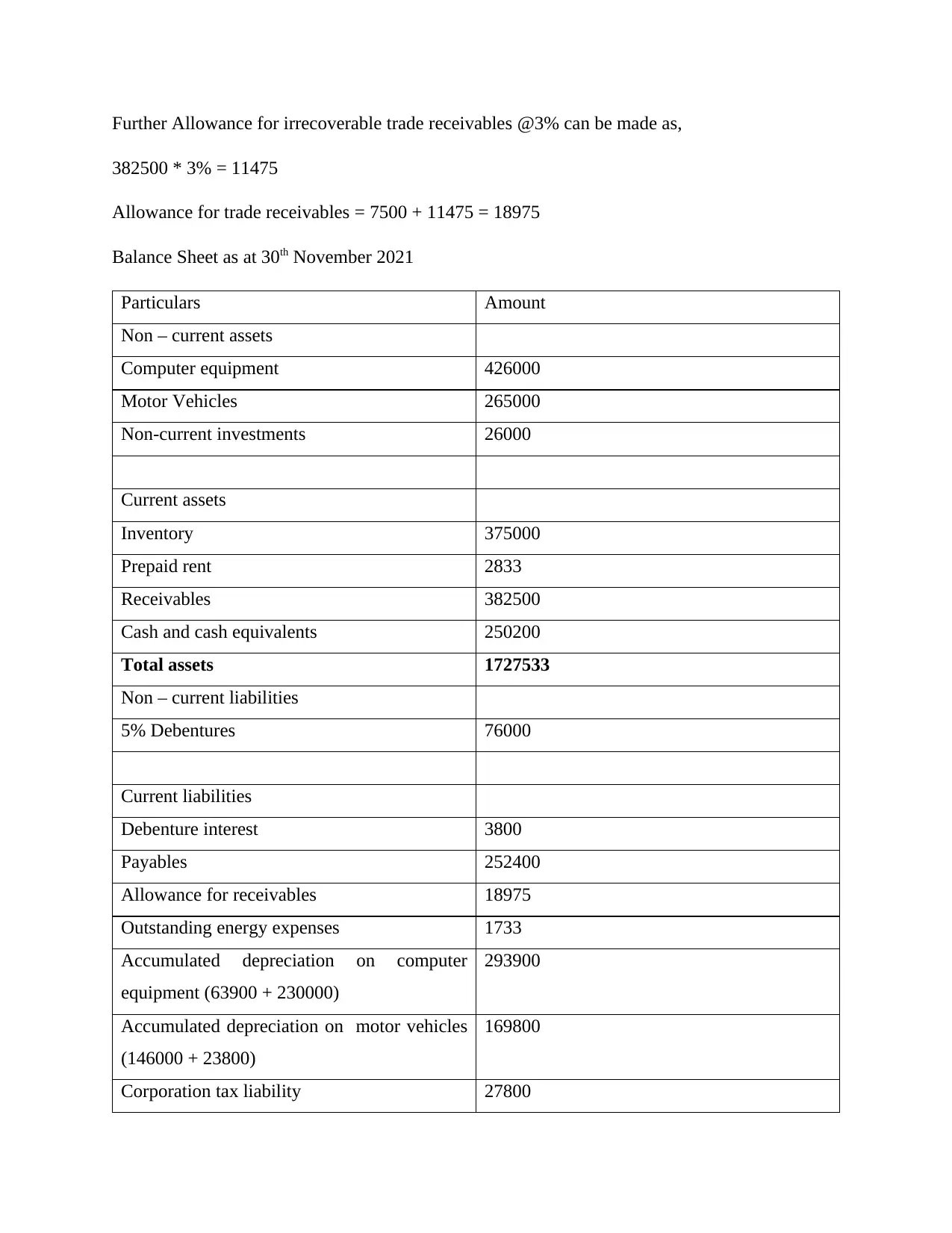

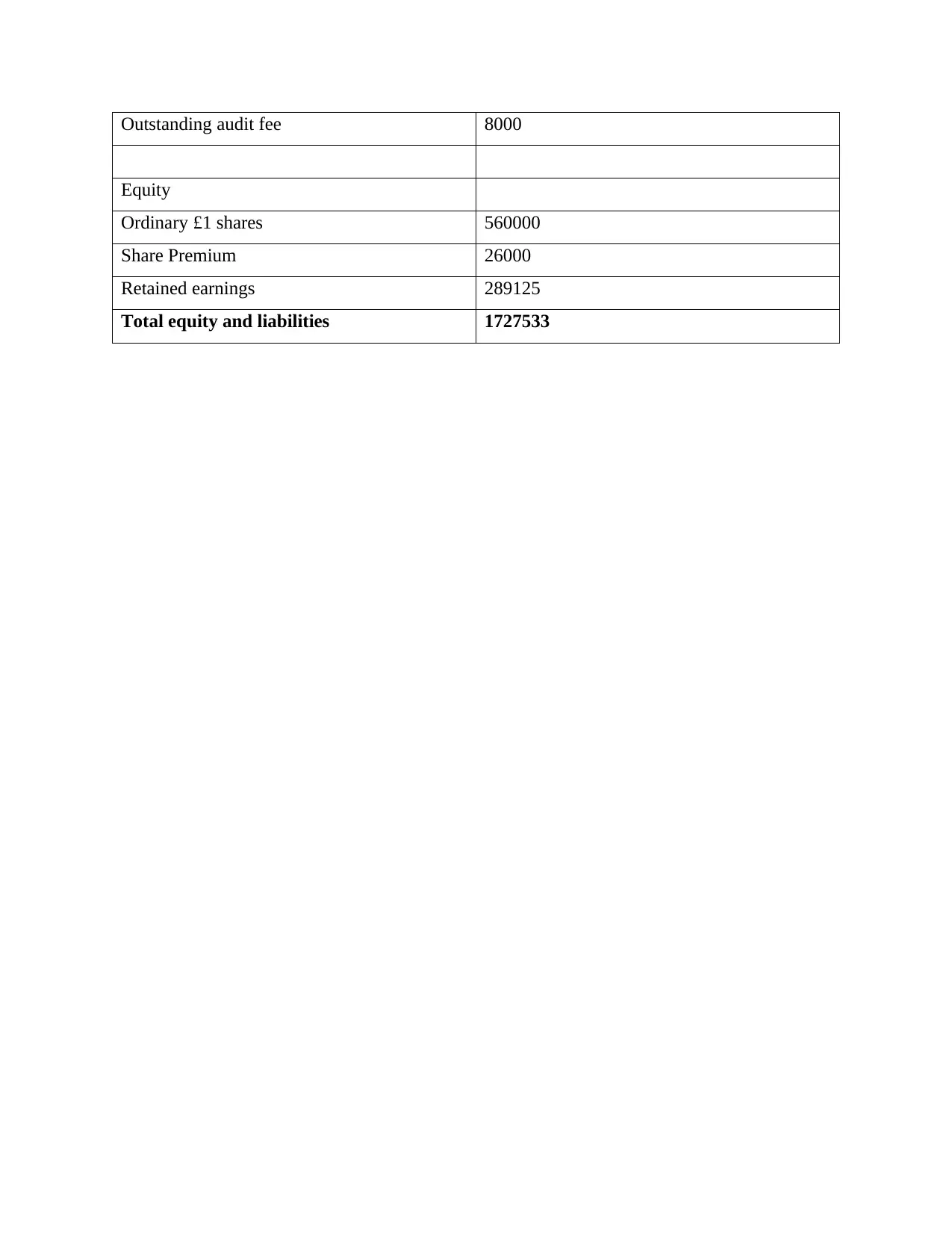

This document presents a solved assignment in Financial Accounting, featuring a comprehensive balance sheet and detailed solutions to various accounting problems. It includes calculations for cost of goods sold, administrative and distribution expenses, depreciation, debenture interest, and trade receivables. The assignment also incorporates working notes to explain the treatment of suspense accounts, energy expenses, rent, and other financial items. The final balance sheet provides a snapshot of the company's financial position, including non-current assets, current assets, non-current liabilities, current liabilities, and equity. This assignment serves as a valuable resource for students seeking to understand and master financial accounting principles, with Desklib offering additional support through similar past papers and solved examples.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.