Financial and Managerial Accounting ACC202 Assignment, July 2019

VerifiedAdded on 2022/11/14

|11

|1906

|284

Homework Assignment

AI Summary

This document presents a comprehensive solution to a Financial and Managerial Accounting assignment (ACC202), covering key aspects of accounting principles and practices. The solution includes detailed journal entries, a balance sheet, and an income statement, demonstrating the application of accounting concepts. It addresses inventory valuation using both FIFO and weighted average methods, comparing their impact on gross profit. Furthermore, the assignment delves into accounting principles such as the cost principle, conservative principle, full disclosure principle, and accrual principle, providing a real-world example using Jardine Matheson. The solution also includes a discussion on the application of these principles in the context of financial reporting standards like IFRS.

Running Head: Financial and Managerial Accounting 1

Financial and Managerial Accounting

Financial and Managerial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: Financial and Managerial Accounting

Table of Contents

Question 1.............................................................................................................................................3

A)......................................................................................................................................................3

B).......................................................................................................................................................3

C).......................................................................................................................................................3

Question 2.............................................................................................................................................4

A)......................................................................................................................................................4

B).......................................................................................................................................................6

Question 3.............................................................................................................................................7

Introduction...........................................................................................................................................7

Accounting principles and concepts......................................................................................................7

Conclusion...........................................................................................................................................10

References...........................................................................................................................................11

Table of Contents

Question 1.............................................................................................................................................3

A)......................................................................................................................................................3

B).......................................................................................................................................................3

C).......................................................................................................................................................3

Question 2.............................................................................................................................................4

A)......................................................................................................................................................4

B).......................................................................................................................................................6

Question 3.............................................................................................................................................7

Introduction...........................................................................................................................................7

Accounting principles and concepts......................................................................................................7

Conclusion...........................................................................................................................................10

References...........................................................................................................................................11

Running Head: Financial and Managerial Accounting

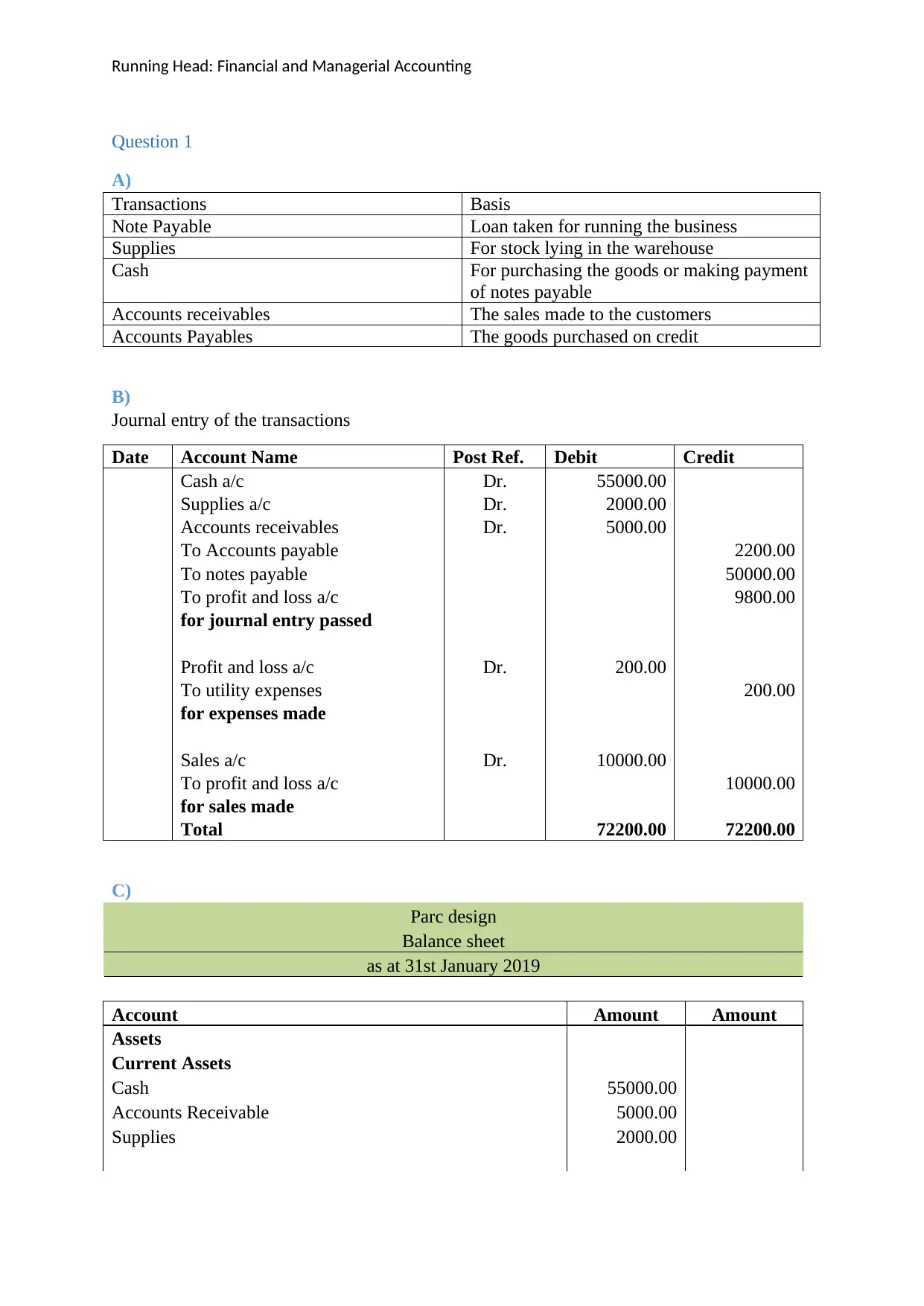

Question 1

A)

Transactions Basis

Note Payable Loan taken for running the business

Supplies For stock lying in the warehouse

Cash For purchasing the goods or making payment

of notes payable

Accounts receivables The sales made to the customers

Accounts Payables The goods purchased on credit

B)

Journal entry of the transactions

Date Account Name Post Ref. Debit Credit

Cash a/c Dr. 55000.00

Supplies a/c Dr. 2000.00

Accounts receivables Dr. 5000.00

To Accounts payable 2200.00

To notes payable 50000.00

To profit and loss a/c 9800.00

for journal entry passed

Profit and loss a/c Dr. 200.00

To utility expenses 200.00

for expenses made

Sales a/c Dr. 10000.00

To profit and loss a/c 10000.00

for sales made

Total 72200.00 72200.00

C)

Parc design

Balance sheet

as at 31st January 2019

Account Amount Amount

Assets

Current Assets

Cash 55000.00

Accounts Receivable 5000.00

Supplies 2000.00

Question 1

A)

Transactions Basis

Note Payable Loan taken for running the business

Supplies For stock lying in the warehouse

Cash For purchasing the goods or making payment

of notes payable

Accounts receivables The sales made to the customers

Accounts Payables The goods purchased on credit

B)

Journal entry of the transactions

Date Account Name Post Ref. Debit Credit

Cash a/c Dr. 55000.00

Supplies a/c Dr. 2000.00

Accounts receivables Dr. 5000.00

To Accounts payable 2200.00

To notes payable 50000.00

To profit and loss a/c 9800.00

for journal entry passed

Profit and loss a/c Dr. 200.00

To utility expenses 200.00

for expenses made

Sales a/c Dr. 10000.00

To profit and loss a/c 10000.00

for sales made

Total 72200.00 72200.00

C)

Parc design

Balance sheet

as at 31st January 2019

Account Amount Amount

Assets

Current Assets

Cash 55000.00

Accounts Receivable 5000.00

Supplies 2000.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: Financial and Managerial Accounting

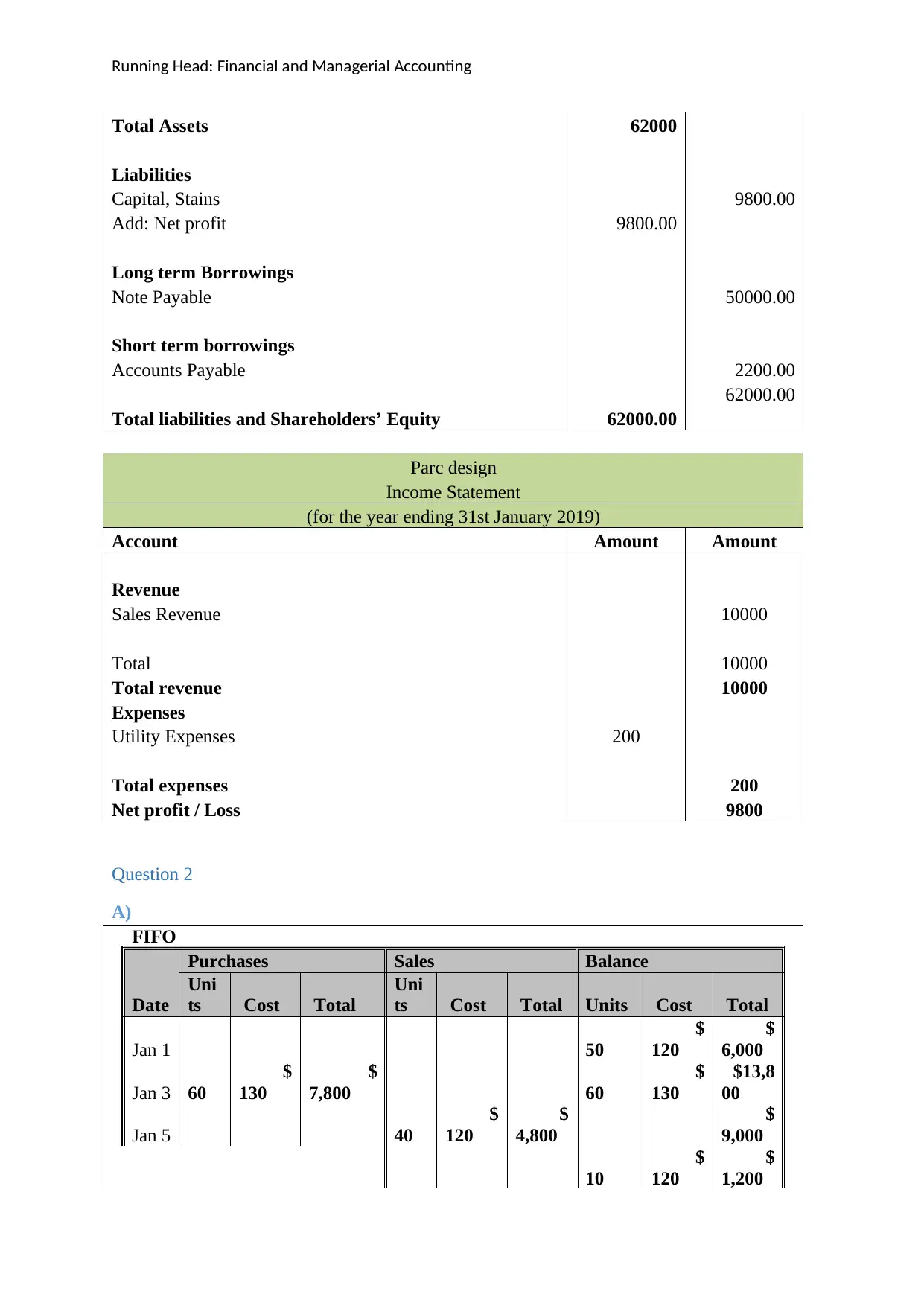

Total Assets 62000

Liabilities

Capital, Stains 9800.00

Add: Net profit 9800.00

Long term Borrowings

Note Payable 50000.00

Short term borrowings

Accounts Payable 2200.00

62000.00

Total liabilities and Shareholders’ Equity 62000.00

Parc design

Income Statement

(for the year ending 31st January 2019)

Account Amount Amount

Revenue

Sales Revenue 10000

Total 10000

Total revenue 10000

Expenses

Utility Expenses 200

Total expenses 200

Net profit / Loss 9800

Question 2

A)

FIFO

Purchases Sales Balance

Date

Uni

ts Cost Total

Uni

ts Cost Total Units Cost Total

Jan 1 50

$

120

$

6,000

Jan 3 60

$

130

$

7,800 60

$

130

$13,8

00

Jan 5 40

$

120

$

4,800

$

9,000

10

$

120

$

1,200

Total Assets 62000

Liabilities

Capital, Stains 9800.00

Add: Net profit 9800.00

Long term Borrowings

Note Payable 50000.00

Short term borrowings

Accounts Payable 2200.00

62000.00

Total liabilities and Shareholders’ Equity 62000.00

Parc design

Income Statement

(for the year ending 31st January 2019)

Account Amount Amount

Revenue

Sales Revenue 10000

Total 10000

Total revenue 10000

Expenses

Utility Expenses 200

Total expenses 200

Net profit / Loss 9800

Question 2

A)

FIFO

Purchases Sales Balance

Date

Uni

ts Cost Total

Uni

ts Cost Total Units Cost Total

Jan 1 50

$

120

$

6,000

Jan 3 60

$

130

$

7,800 60

$

130

$13,8

00

Jan 5 40

$

120

$

4,800

$

9,000

10

$

120

$

1,200

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: Financial and Managerial Accounting

60

$

130

$

7,800

Jan

10 100

$

150

$

15,000

1

00

$

150

$15,0

00

Jan

12 10

$

120

$

1,200

20

$

130

$

2,600 40

$

130

$

5,200

1

00

$

150

$15,0

00

Jan

20 40

$

130

$

5,200

40

$

150

$

6,000 60

$

150

$

9,000

Tota

ls 160

$

22,800 150

$19,8

00 60

$

150

$

9,000

Weighted Average

Purchases Sales Balance

Date

Uni

ts Cost Total

Uni

ts Cost Total Units Cost Total

Jan 1 50

$

120

$

6,000

Jan 3 60

$

130

$

7,800 60

$

130

$

7,800

1

10

$

125

$13,8

00

Jan 5 40

$

125

$

5,000 70

$

126

$

8,800

Jan

10 100

$

150

$

15,000

1

00

$

150

$15,0

00

1

70

$

140

$23,8

00

Jan

12 30

$

140

$

4,200

1

40

$

140

$19,6

00

Jan

20 80

$

140

$11,2

00 60

$

140

$

8,400

60

$

130

$

7,800

Jan

10 100

$

150

$

15,000

1

00

$

150

$15,0

00

Jan

12 10

$

120

$

1,200

20

$

130

$

2,600 40

$

130

$

5,200

1

00

$

150

$15,0

00

Jan

20 40

$

130

$

5,200

40

$

150

$

6,000 60

$

150

$

9,000

Tota

ls 160

$

22,800 150

$19,8

00 60

$

150

$

9,000

Weighted Average

Purchases Sales Balance

Date

Uni

ts Cost Total

Uni

ts Cost Total Units Cost Total

Jan 1 50

$

120

$

6,000

Jan 3 60

$

130

$

7,800 60

$

130

$

7,800

1

10

$

125

$13,8

00

Jan 5 40

$

125

$

5,000 70

$

126

$

8,800

Jan

10 100

$

150

$

15,000

1

00

$

150

$15,0

00

1

70

$

140

$23,8

00

Jan

12 30

$

140

$

4,200

1

40

$

140

$19,6

00

Jan

20 80

$

140

$11,2

00 60

$

140

$

8,400

Running Head: Financial and Managerial Accounting

Tota

ls 160

$

22,800 150

$20,4

00 60

14

0

$

8,400

B)

The major difference in the gross profit under the FIFO method and the weighted average is

because of the change of the method of the cost per unit. Under the FIFO method which is

also known as the First in first out method the units are sold at the price in contrast to the first

units purchased, whereas in case of the weighted average cost of capital the units price is

calculated by dividing the total cost by total units. In this manner the major impact is on the

cost of goods sold. Hence the cost of goods sold is greater in FIFO method in comparison to

the weighted average cost method and so will be he profit or the loss.

Tota

ls 160

$

22,800 150

$20,4

00 60

14

0

$

8,400

B)

The major difference in the gross profit under the FIFO method and the weighted average is

because of the change of the method of the cost per unit. Under the FIFO method which is

also known as the First in first out method the units are sold at the price in contrast to the first

units purchased, whereas in case of the weighted average cost of capital the units price is

calculated by dividing the total cost by total units. In this manner the major impact is on the

cost of goods sold. Hence the cost of goods sold is greater in FIFO method in comparison to

the weighted average cost method and so will be he profit or the loss.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: Financial and Managerial Accounting

Gross profit

FIFO Weighted Average

Revenues $ 8,000 $ 8,000

Cost of goods sold $ 9,000 $ 8,400

Gross profit $ (1,000) $ (400)

Question 3

Introduction

The description analyses the accounting principles and concepts by using a relevant example

named as “Jardine Matheson.” The company is a standard listed under LSE (London stock

exchange) (Jardine Matheson, 2018). This description brings out analyses of four significant

principles of accounting that are used in the formation of financial statements. As per the

GAAP (generally accepted accounting principles), it is seen that companies have to comply

with the legal requirement and compliances (Wildavsky, Lockhart, & Coughlin, 2018).

Accounting principles and concepts

Accounting principles are few rules and regulations, which a company will follow as per the

reported financial data. Principle of accounting refers to the basic and fundamental principle

including cost principle, going concern principle, full disclosure principle, and economic

entity principle (Wildavsky, Lockhart, & Coughlin, 2018).

Four important concepts

Cost principle- According to this principle, an organisation will record only assets, equity

investments, and liabilities at their book value or purchase cost. The accounting principle is

relevant from the cost perspective where cost is defined as amount spent related to cash and

cash equivalent as when it is originally obtained whether the purchase has been incurred last

year or 40 years back (Ismail, & Sori, 2017). This is the reason why amounts illustrated in the

financial statements is referred as historical cost. Asset amount is not adjusted upward

according to inflation (Jardine Matheson, 2018).

Gross profit

FIFO Weighted Average

Revenues $ 8,000 $ 8,000

Cost of goods sold $ 9,000 $ 8,400

Gross profit $ (1,000) $ (400)

Question 3

Introduction

The description analyses the accounting principles and concepts by using a relevant example

named as “Jardine Matheson.” The company is a standard listed under LSE (London stock

exchange) (Jardine Matheson, 2018). This description brings out analyses of four significant

principles of accounting that are used in the formation of financial statements. As per the

GAAP (generally accepted accounting principles), it is seen that companies have to comply

with the legal requirement and compliances (Wildavsky, Lockhart, & Coughlin, 2018).

Accounting principles and concepts

Accounting principles are few rules and regulations, which a company will follow as per the

reported financial data. Principle of accounting refers to the basic and fundamental principle

including cost principle, going concern principle, full disclosure principle, and economic

entity principle (Wildavsky, Lockhart, & Coughlin, 2018).

Four important concepts

Cost principle- According to this principle, an organisation will record only assets, equity

investments, and liabilities at their book value or purchase cost. The accounting principle is

relevant from the cost perspective where cost is defined as amount spent related to cash and

cash equivalent as when it is originally obtained whether the purchase has been incurred last

year or 40 years back (Ismail, & Sori, 2017). This is the reason why amounts illustrated in the

financial statements is referred as historical cost. Asset amount is not adjusted upward

according to inflation (Jardine Matheson, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: Financial and Managerial Accounting

For the cost principle, one has tested discounted cash flows models as being used by the

management in the assessment as checking the accuracy of calculations (Ismail, & Sori,

2017). Comparing the historical budgeting performance in relation to the actual results and

agreeing to the figures as being detailed management as being approved in order to assess the

cash flows in model (Jardine Matheson, 2018).

Conservative principle- The concept will record liabilities and expenses and financial

statements will record revenue and assets only when they are incurred. When a situation

arises, there are two acceptable alternative in order to report item where conservatism directs

accountant resulting into less net income and less amount of assets (Ismail, & Sori, 2017). It

directs the accountants to presume the future losses and risks according to environment but at

the same time, it cannot allow treat the gain same action as risk and losses. For instance- An

accountant can write the value of inventory as an amount, which is lower than the original

cost but it will not write the inventory amount as up to such higher amount as compared to its

original costs.

The company simply applies appropriate measurement simplified approach in order to expect

credit losses. It is seen from the annual reports of Jardine Matheson, it expected its loss

allowance for the trade debtors and the contract assets. In order to measure expected credit

losses, the company estimates its shared credit risk, trade receivable, contract assets, and also

the past due for it (Jardine Matheson, 2018). The expected loss is based on the historical

payment sales profiles and its corresponding for the historical credit losses. The historical

loss will reflect the adjustment of forward looking data and current fluctuation on the factors

of macro-economic factors.

Full disclosure principle- Certain information is quite important for the investors and lenders

with the use of financial statements. In order to accomplish this principle, financial

For the cost principle, one has tested discounted cash flows models as being used by the

management in the assessment as checking the accuracy of calculations (Ismail, & Sori,

2017). Comparing the historical budgeting performance in relation to the actual results and

agreeing to the figures as being detailed management as being approved in order to assess the

cash flows in model (Jardine Matheson, 2018).

Conservative principle- The concept will record liabilities and expenses and financial

statements will record revenue and assets only when they are incurred. When a situation

arises, there are two acceptable alternative in order to report item where conservatism directs

accountant resulting into less net income and less amount of assets (Ismail, & Sori, 2017). It

directs the accountants to presume the future losses and risks according to environment but at

the same time, it cannot allow treat the gain same action as risk and losses. For instance- An

accountant can write the value of inventory as an amount, which is lower than the original

cost but it will not write the inventory amount as up to such higher amount as compared to its

original costs.

The company simply applies appropriate measurement simplified approach in order to expect

credit losses. It is seen from the annual reports of Jardine Matheson, it expected its loss

allowance for the trade debtors and the contract assets. In order to measure expected credit

losses, the company estimates its shared credit risk, trade receivable, contract assets, and also

the past due for it (Jardine Matheson, 2018). The expected loss is based on the historical

payment sales profiles and its corresponding for the historical credit losses. The historical

loss will reflect the adjustment of forward looking data and current fluctuation on the factors

of macro-economic factors.

Full disclosure principle- Certain information is quite important for the investors and lenders

with the use of financial statements. In order to accomplish this principle, financial

Running Head: Financial and Managerial Accounting

statements maintain notes to accounts “footnotes” as being attached to the financial data. It is

a concept inclusive of appropriate information alongside within the financial statements about

the data, which affect reader’s understanding of the financial Statements. The concept covers

specifying the enormous number of data disclosures (Ismail, & Sori, 2017).

This concept is purely useful for the investors to analyse the performance of the company.

The group analyses underlying profits in the internal financial reporting to differentiate

between non-trading items and the ongoing performance for business. The company

announced several additional disclosures made in the financial statements as mainly on the

revenue form the contracts and impairment of debtors (Flood, 2015). IFRS 17 in regards to

insurance contracts have comprehensive policies and standards as a fundamental overhauling

insurance recognition, accounting, disclosures, and presentation. It needs insurance of

contract liabilities as being reported balance sheet by using the current assumption at the

reporting time. The company discloses the presentation in corporate governance disclosing

cross reference from the financial reporting and audited (Jardine Matheson, 2018).

Accrual principle- This concept states that accounting transactions must be recorded as per

the accounting periods when it is incurred rather than periods and its associated cash

generated (Sikka, 2017). It is crucial to form financial statements as shown if happened in the

fiscal period rather than recording artificial cash revenues just to accelerate the estimated

cash flows (Sikka, 2017). This principle is used to record expense for which the company has

paid for through which incorporated lengthy delaying caused to the payment, which is

associated with supplier invoice (Jardine Matheson, 2018).

With the changes in the accounting policies, there is an adoption of IFRS 9 inclusive of

financial instrument and also IFRS 15 “revenue from the contracts with the customers” in the

financial statements. Residences and revenue from the hotels branding and management

statements maintain notes to accounts “footnotes” as being attached to the financial data. It is

a concept inclusive of appropriate information alongside within the financial statements about

the data, which affect reader’s understanding of the financial Statements. The concept covers

specifying the enormous number of data disclosures (Ismail, & Sori, 2017).

This concept is purely useful for the investors to analyse the performance of the company.

The group analyses underlying profits in the internal financial reporting to differentiate

between non-trading items and the ongoing performance for business. The company

announced several additional disclosures made in the financial statements as mainly on the

revenue form the contracts and impairment of debtors (Flood, 2015). IFRS 17 in regards to

insurance contracts have comprehensive policies and standards as a fundamental overhauling

insurance recognition, accounting, disclosures, and presentation. It needs insurance of

contract liabilities as being reported balance sheet by using the current assumption at the

reporting time. The company discloses the presentation in corporate governance disclosing

cross reference from the financial reporting and audited (Jardine Matheson, 2018).

Accrual principle- This concept states that accounting transactions must be recorded as per

the accounting periods when it is incurred rather than periods and its associated cash

generated (Sikka, 2017). It is crucial to form financial statements as shown if happened in the

fiscal period rather than recording artificial cash revenues just to accelerate the estimated

cash flows (Sikka, 2017). This principle is used to record expense for which the company has

paid for through which incorporated lengthy delaying caused to the payment, which is

associated with supplier invoice (Jardine Matheson, 2018).

With the changes in the accounting policies, there is an adoption of IFRS 9 inclusive of

financial instrument and also IFRS 15 “revenue from the contracts with the customers” in the

financial statements. Residences and revenue from the hotels branding and management

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: Financial and Managerial Accounting

comprises of gross fees as being earned from branding. This management fees is determined

by relevant contract, accounting performance of hotels, operating and sales expense of

residences. Residences and hotel invoices is according to terms of contracts and fees that are

payable when being invoiced (Jardine Matheson, 2018).

Conclusion

From the above discussion, it is seen that financial statements are prepared as per the IFRS

(International Financial Reporting Standards) including IASB (International Accounting

Standards Board). The statements are prepared on the basis of going concern and also under

the historical costing convention while disclosing the accounting procedures and policies.

comprises of gross fees as being earned from branding. This management fees is determined

by relevant contract, accounting performance of hotels, operating and sales expense of

residences. Residences and hotel invoices is according to terms of contracts and fees that are

payable when being invoiced (Jardine Matheson, 2018).

Conclusion

From the above discussion, it is seen that financial statements are prepared as per the IFRS

(International Financial Reporting Standards) including IASB (International Accounting

Standards Board). The statements are prepared on the basis of going concern and also under

the historical costing convention while disclosing the accounting procedures and policies.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: Financial and Managerial Accounting

References

Flood, J. M. (2015). Wiley GAAP 2016: Interpretation and Application of Generally

Accepted Accounting Principles. John Wiley & Sons.

Ismail, N., & Sori, Z. M. (2017). A closer look at accounting for Islamic financial

institutions. In SHS Web of Conferences (Vol. 34, p. 07004). EDP Sciences.

Jardine Matheson, (2018). Annual Report 2018. Retrieved from:

https://www.jardines.com/assets/files/Investors/Reports/matheson/jm-ar2018.pdf

Sikka, P. (2017, December). Accounting and taxation: Conjoined twins or separate siblings?.

In Accounting forum (Vol. 41, No. 4, pp. 390-405). Taylor & Francis.

Wildavsky, A., Lockhart, C., & Coughlin, R. M. (2018). Accounting for the Environment 1.

In Culture and Social Theory (pp. 85-112). Routledge.

References

Flood, J. M. (2015). Wiley GAAP 2016: Interpretation and Application of Generally

Accepted Accounting Principles. John Wiley & Sons.

Ismail, N., & Sori, Z. M. (2017). A closer look at accounting for Islamic financial

institutions. In SHS Web of Conferences (Vol. 34, p. 07004). EDP Sciences.

Jardine Matheson, (2018). Annual Report 2018. Retrieved from:

https://www.jardines.com/assets/files/Investors/Reports/matheson/jm-ar2018.pdf

Sikka, P. (2017, December). Accounting and taxation: Conjoined twins or separate siblings?.

In Accounting forum (Vol. 41, No. 4, pp. 390-405). Taylor & Francis.

Wildavsky, A., Lockhart, C., & Coughlin, R. M. (2018). Accounting for the Environment 1.

In Culture and Social Theory (pp. 85-112). Routledge.

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.