Financial Accounting Solutions: Advanced Case Studies and Analysis

VerifiedAdded on 2020/02/24

|11

|2321

|51

Homework Assignment

AI Summary

This document presents a series of financial accounting solutions addressing various scenarios. Solution-1 provides a detailed disclosure for an annual report, addressing a case against a bank involving toxic investments and class action settlements, including factors for disclosure and financial impacts. Solution-2 calculates the fair value of a leased asset (portable sound studio), creates a lease amortization schedule, and provides corresponding journal entries for Hopeful Ltd. and the return of the asset to Lessor Ltd. Solution-3 calculates Alexandra Bay's current obligation for long-service leave, including present value calculations and the required journal entry. Solution-4 presents a cash flow statement for T Pty Ltd, including adjustments and working notes for tax paid and plant & equipment. Finally, Solution-5 provides journal entries for foreign exchange transactions, covering inventory, equipment, and loan hedging, with explanations of the accounting treatments adopted under AASB 121 and forward contract hedging.

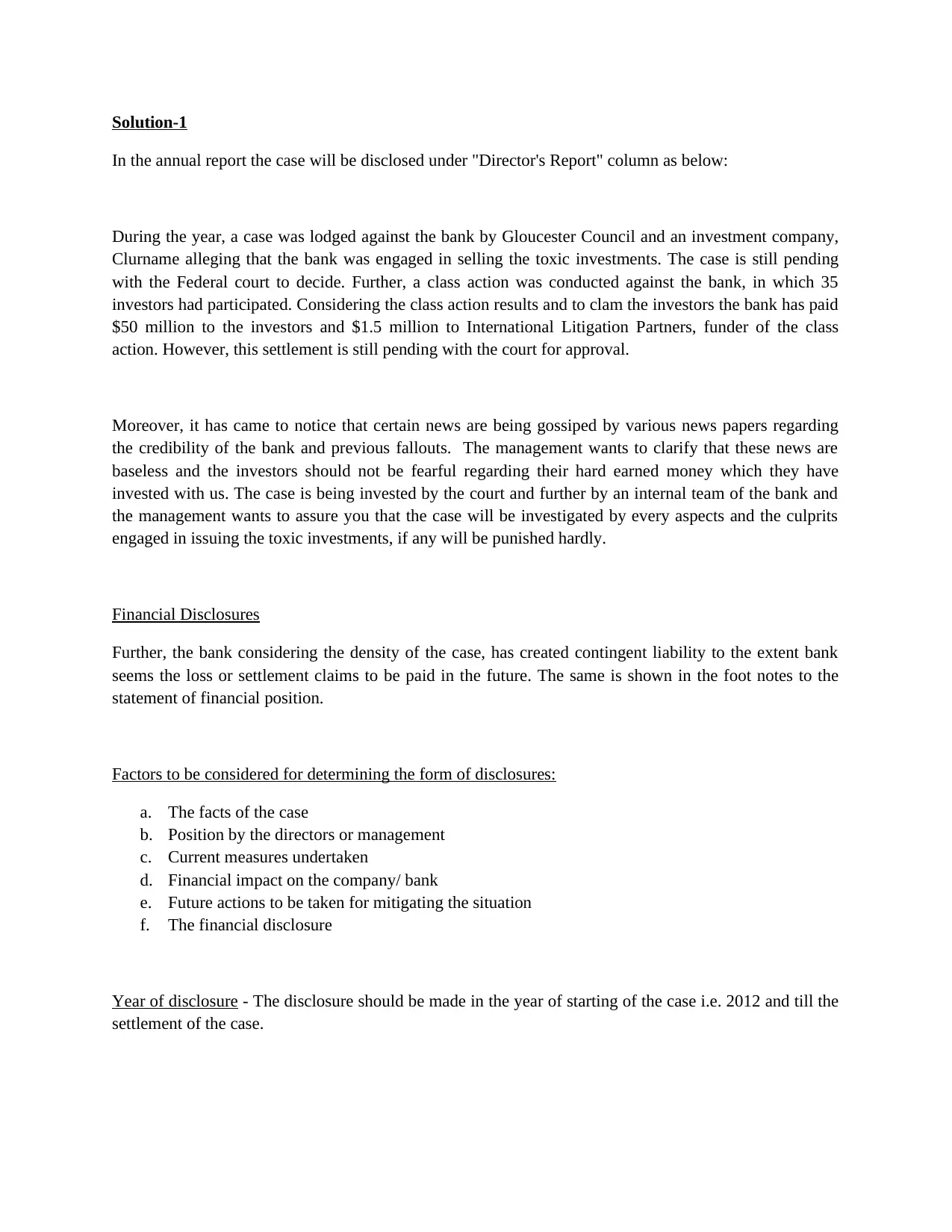

Solution-1

In the annual report the case will be disclosed under "Director's Report" column as below:

During the year, a case was lodged against the bank by Gloucester Council and an investment company,

Clurname alleging that the bank was engaged in selling the toxic investments. The case is still pending

with the Federal court to decide. Further, a class action was conducted against the bank, in which 35

investors had participated. Considering the class action results and to clam the investors the bank has paid

$50 million to the investors and $1.5 million to International Litigation Partners, funder of the class

action. However, this settlement is still pending with the court for approval.

Moreover, it has came to notice that certain news are being gossiped by various news papers regarding

the credibility of the bank and previous fallouts. The management wants to clarify that these news are

baseless and the investors should not be fearful regarding their hard earned money which they have

invested with us. The case is being invested by the court and further by an internal team of the bank and

the management wants to assure you that the case will be investigated by every aspects and the culprits

engaged in issuing the toxic investments, if any will be punished hardly.

Financial Disclosures

Further, the bank considering the density of the case, has created contingent liability to the extent bank

seems the loss or settlement claims to be paid in the future. The same is shown in the foot notes to the

statement of financial position.

Factors to be considered for determining the form of disclosures:

a. The facts of the case

b. Position by the directors or management

c. Current measures undertaken

d. Financial impact on the company/ bank

e. Future actions to be taken for mitigating the situation

f. The financial disclosure

Year of disclosure - The disclosure should be made in the year of starting of the case i.e. 2012 and till the

settlement of the case.

In the annual report the case will be disclosed under "Director's Report" column as below:

During the year, a case was lodged against the bank by Gloucester Council and an investment company,

Clurname alleging that the bank was engaged in selling the toxic investments. The case is still pending

with the Federal court to decide. Further, a class action was conducted against the bank, in which 35

investors had participated. Considering the class action results and to clam the investors the bank has paid

$50 million to the investors and $1.5 million to International Litigation Partners, funder of the class

action. However, this settlement is still pending with the court for approval.

Moreover, it has came to notice that certain news are being gossiped by various news papers regarding

the credibility of the bank and previous fallouts. The management wants to clarify that these news are

baseless and the investors should not be fearful regarding their hard earned money which they have

invested with us. The case is being invested by the court and further by an internal team of the bank and

the management wants to assure you that the case will be investigated by every aspects and the culprits

engaged in issuing the toxic investments, if any will be punished hardly.

Financial Disclosures

Further, the bank considering the density of the case, has created contingent liability to the extent bank

seems the loss or settlement claims to be paid in the future. The same is shown in the foot notes to the

statement of financial position.

Factors to be considered for determining the form of disclosures:

a. The facts of the case

b. Position by the directors or management

c. Current measures undertaken

d. Financial impact on the company/ bank

e. Future actions to be taken for mitigating the situation

f. The financial disclosure

Year of disclosure - The disclosure should be made in the year of starting of the case i.e. 2012 and till the

settlement of the case.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

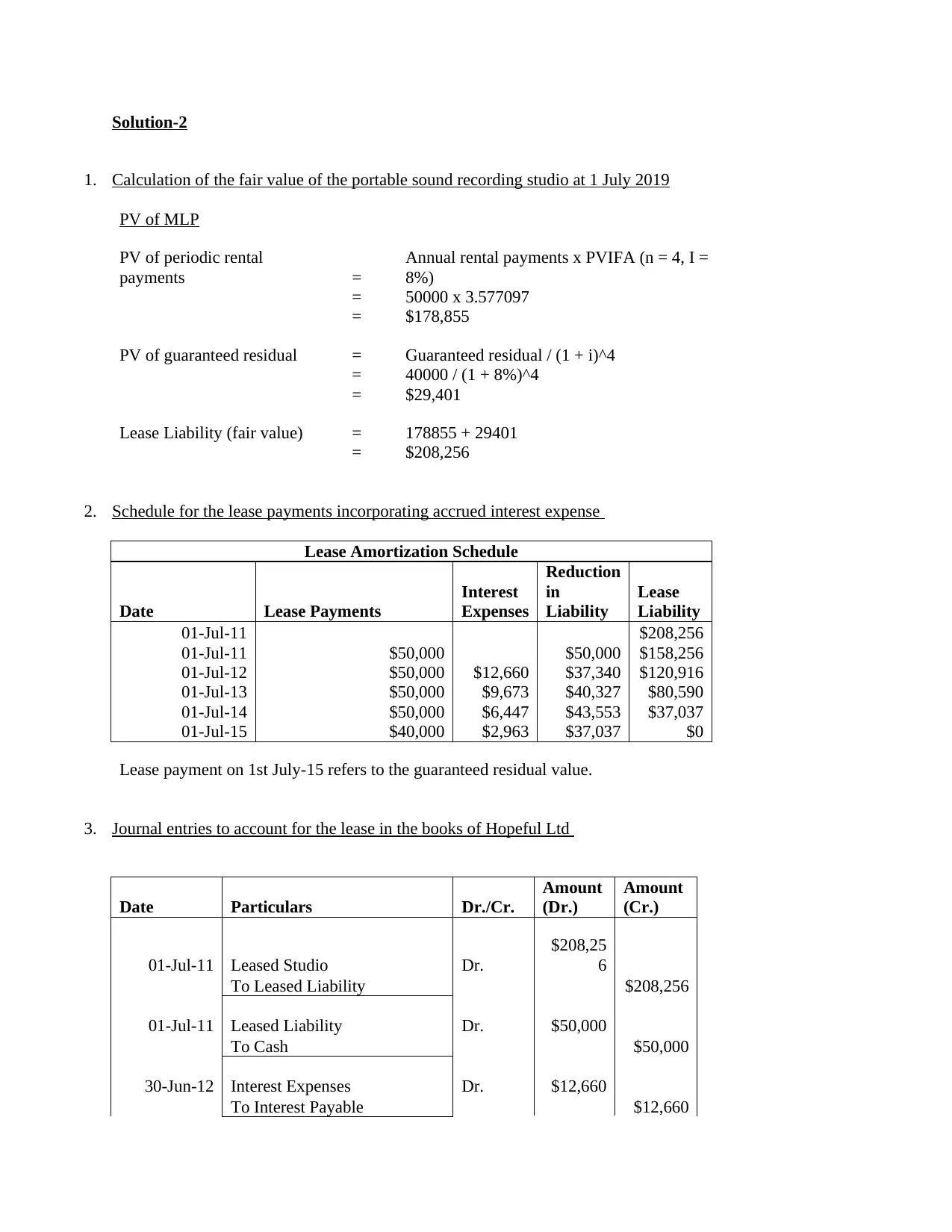

Solution-2

1. Calculation of the fair value of the portable sound recording studio at 1 July 2019

PV of MLP

PV of periodic rental

payments =

Annual rental payments x PVIFA (n = 4, I =

8%)

= 50000 x 3.577097

= $178,855

PV of guaranteed residual = Guaranteed residual / (1 + i)^4

= 40000 / (1 + 8%)^4

= $29,401

Lease Liability (fair value) = 178855 + 29401

= $208,256

2. Schedule for the lease payments incorporating accrued interest expense

Lease Amortization Schedule

Date Lease Payments

Interest

Expenses

Reduction

in

Liability

Lease

Liability

01-Jul-11 $208,256

01-Jul-11 $50,000 $50,000 $158,256

01-Jul-12 $50,000 $12,660 $37,340 $120,916

01-Jul-13 $50,000 $9,673 $40,327 $80,590

01-Jul-14 $50,000 $6,447 $43,553 $37,037

01-Jul-15 $40,000 $2,963 $37,037 $0

Lease payment on 1st July-15 refers to the guaranteed residual value.

3. Journal entries to account for the lease in the books of Hopeful Ltd

Date Particulars Dr./Cr.

Amount

(Dr.)

Amount

(Cr.)

01-Jul-11 Leased Studio Dr.

$208,25

6

To Leased Liability $208,256

01-Jul-11 Leased Liability Dr. $50,000

To Cash $50,000

30-Jun-12 Interest Expenses Dr. $12,660

To Interest Payable $12,660

1. Calculation of the fair value of the portable sound recording studio at 1 July 2019

PV of MLP

PV of periodic rental

payments =

Annual rental payments x PVIFA (n = 4, I =

8%)

= 50000 x 3.577097

= $178,855

PV of guaranteed residual = Guaranteed residual / (1 + i)^4

= 40000 / (1 + 8%)^4

= $29,401

Lease Liability (fair value) = 178855 + 29401

= $208,256

2. Schedule for the lease payments incorporating accrued interest expense

Lease Amortization Schedule

Date Lease Payments

Interest

Expenses

Reduction

in

Liability

Lease

Liability

01-Jul-11 $208,256

01-Jul-11 $50,000 $50,000 $158,256

01-Jul-12 $50,000 $12,660 $37,340 $120,916

01-Jul-13 $50,000 $9,673 $40,327 $80,590

01-Jul-14 $50,000 $6,447 $43,553 $37,037

01-Jul-15 $40,000 $2,963 $37,037 $0

Lease payment on 1st July-15 refers to the guaranteed residual value.

3. Journal entries to account for the lease in the books of Hopeful Ltd

Date Particulars Dr./Cr.

Amount

(Dr.)

Amount

(Cr.)

01-Jul-11 Leased Studio Dr.

$208,25

6

To Leased Liability $208,256

01-Jul-11 Leased Liability Dr. $50,000

To Cash $50,000

30-Jun-12 Interest Expenses Dr. $12,660

To Interest Payable $12,660

30-Jun-12

Depreciation Expenses-Leased

Studio Dr. $42,064

To Accumulated Depreciation $42,064

01-Jul-12 Leased Liability Dr. $37,340

Interest Payable Dr. $12,660

To Cash $50,000

30-Jun-13 Interest Expenses Dr. $9,673

To Interest Payable $9,673

30-Jun-13

Depreciation Expenses-Leased

Studio Dr. $42,064

To Accumulated Depreciation $42,064

4. The journal entries in the books of Hopeful Ltd for return of the asset to Lessor Ltd and the settlement of

all obligations under the lease on 1 July 2023

Hopeful Ltd. must pay difference $15,000 (40,000 - 25,000) between fair value of studio and guaranteed

residual value.

Date Particulars Dr./Cr.

Amount

(Dr.)

Amount

(Cr.)

01-Jul-15 Accumulated Depreciation Dr.

$168,25

6

To Leased Studio $168,256

01-Jul-15 Leased Liability Dr. $37,037

Interest Payable Dr. $2,963

To Leased Studio $40,000

01-Jul-15 Loss on Guaranteed Residual Dr. $15,000

To Cash $15,000

Depreciation Expenses-Leased

Studio Dr. $42,064

To Accumulated Depreciation $42,064

01-Jul-12 Leased Liability Dr. $37,340

Interest Payable Dr. $12,660

To Cash $50,000

30-Jun-13 Interest Expenses Dr. $9,673

To Interest Payable $9,673

30-Jun-13

Depreciation Expenses-Leased

Studio Dr. $42,064

To Accumulated Depreciation $42,064

4. The journal entries in the books of Hopeful Ltd for return of the asset to Lessor Ltd and the settlement of

all obligations under the lease on 1 July 2023

Hopeful Ltd. must pay difference $15,000 (40,000 - 25,000) between fair value of studio and guaranteed

residual value.

Date Particulars Dr./Cr.

Amount

(Dr.)

Amount

(Cr.)

01-Jul-15 Accumulated Depreciation Dr.

$168,25

6

To Leased Studio $168,256

01-Jul-15 Leased Liability Dr. $37,037

Interest Payable Dr. $2,963

To Leased Studio $40,000

01-Jul-15 Loss on Guaranteed Residual Dr. $15,000

To Cash $15,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

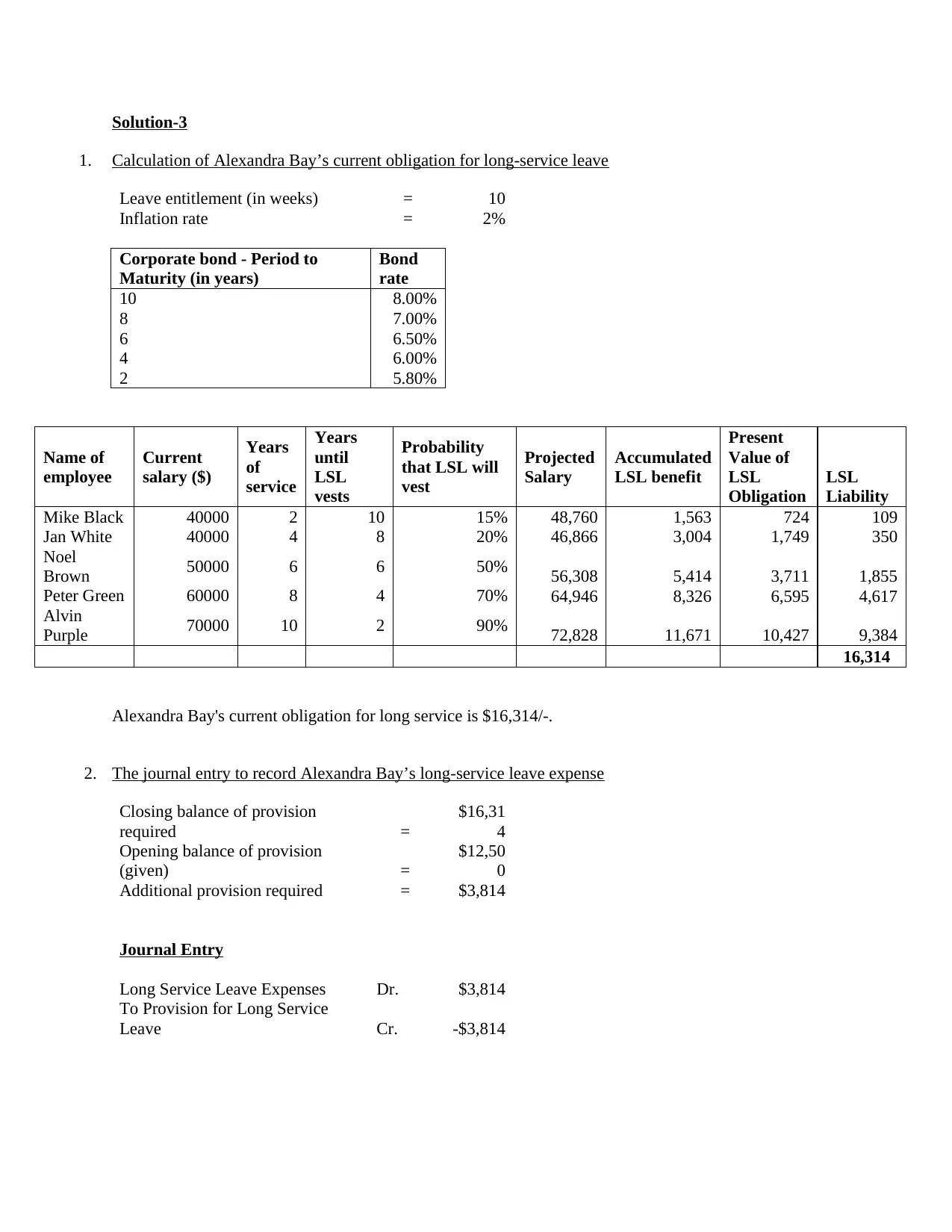

Solution-3

1. Calculation of Alexandra Bay’s current obligation for long-service leave

Leave entitlement (in weeks) = 10

Inflation rate = 2%

Corporate bond - Period to

Maturity (in years)

Bond

rate

10 8.00%

8 7.00%

6 6.50%

4 6.00%

2 5.80%

Name of

employee

Current

salary ($)

Years

of

service

Years

until

LSL

vests

Probability

that LSL will

vest

Projected

Salary

Accumulated

LSL benefit

Present

Value of

LSL

Obligation

LSL

Liability

Mike Black 40000 2 10 15% 48,760 1,563 724 109

Jan White 40000 4 8 20% 46,866 3,004 1,749 350

Noel

Brown 50000 6 6 50% 56,308 5,414 3,711 1,855

Peter Green 60000 8 4 70% 64,946 8,326 6,595 4,617

Alvin

Purple 70000 10 2 90% 72,828 11,671 10,427 9,384

16,314

Alexandra Bay's current obligation for long service is $16,314/-.

2. The journal entry to record Alexandra Bay’s long-service leave expense

Closing balance of provision

required =

$16,31

4

Opening balance of provision

(given) =

$12,50

0

Additional provision required = $3,814

Journal Entry

Long Service Leave Expenses Dr. $3,814

To Provision for Long Service

Leave Cr. -$3,814

1. Calculation of Alexandra Bay’s current obligation for long-service leave

Leave entitlement (in weeks) = 10

Inflation rate = 2%

Corporate bond - Period to

Maturity (in years)

Bond

rate

10 8.00%

8 7.00%

6 6.50%

4 6.00%

2 5.80%

Name of

employee

Current

salary ($)

Years

of

service

Years

until

LSL

vests

Probability

that LSL will

vest

Projected

Salary

Accumulated

LSL benefit

Present

Value of

LSL

Obligation

LSL

Liability

Mike Black 40000 2 10 15% 48,760 1,563 724 109

Jan White 40000 4 8 20% 46,866 3,004 1,749 350

Noel

Brown 50000 6 6 50% 56,308 5,414 3,711 1,855

Peter Green 60000 8 4 70% 64,946 8,326 6,595 4,617

Alvin

Purple 70000 10 2 90% 72,828 11,671 10,427 9,384

16,314

Alexandra Bay's current obligation for long service is $16,314/-.

2. The journal entry to record Alexandra Bay’s long-service leave expense

Closing balance of provision

required =

$16,31

4

Opening balance of provision

(given) =

$12,50

0

Additional provision required = $3,814

Journal Entry

Long Service Leave Expenses Dr. $3,814

To Provision for Long Service

Leave Cr. -$3,814

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

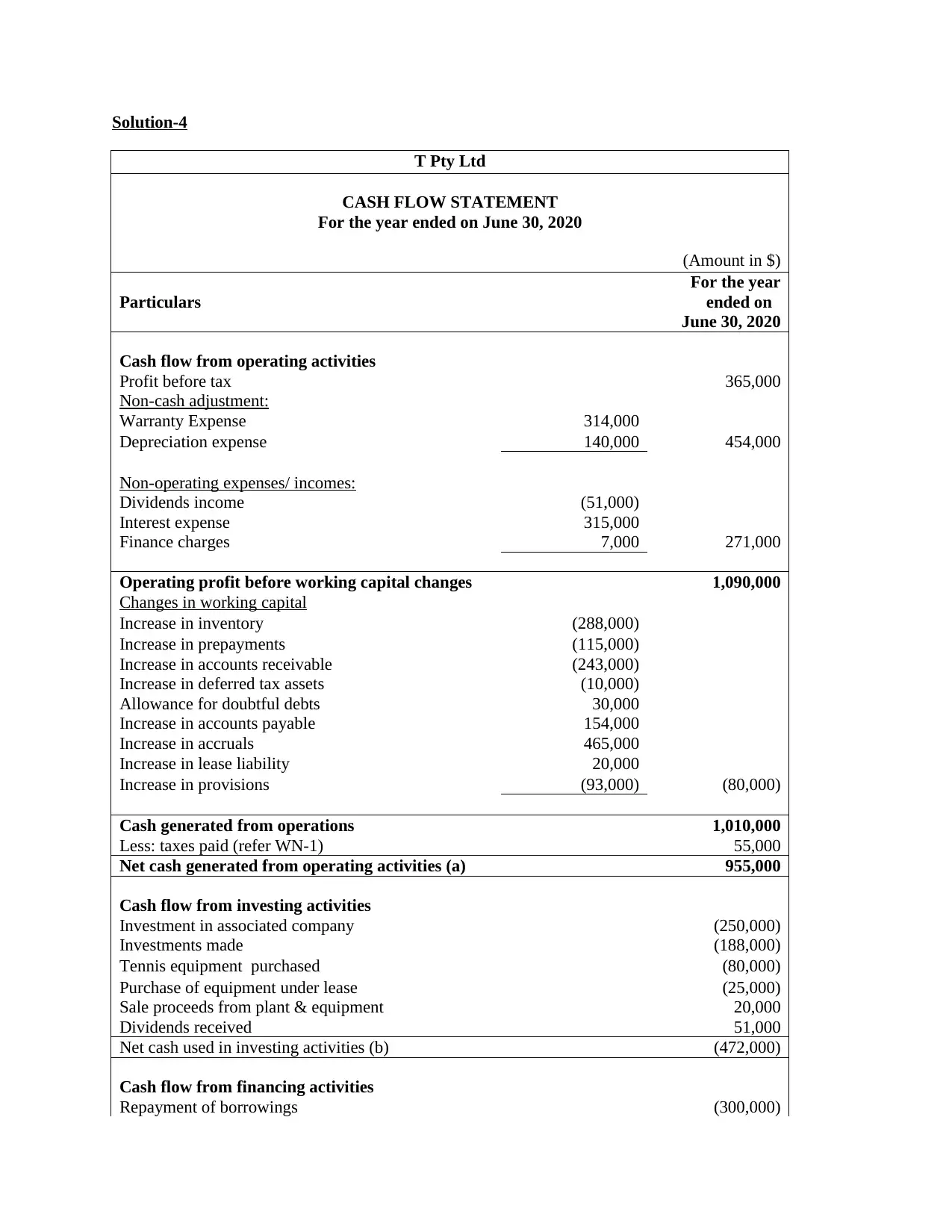

Solution-4

T Pty Ltd

CASH FLOW STATEMENT

For the year ended on June 30, 2020

(Amount in $)

Particulars

For the year

ended on

June 30, 2020

Cash flow from operating activities

Profit before tax 365,000

Non-cash adjustment:

Warranty Expense 314,000

Depreciation expense 140,000 454,000

Non-operating expenses/ incomes:

Dividends income (51,000)

Interest expense 315,000

Finance charges 7,000 271,000

Operating profit before working capital changes 1,090,000

Changes in working capital

Increase in inventory (288,000)

Increase in prepayments (115,000)

Increase in accounts receivable (243,000)

Increase in deferred tax assets (10,000)

Allowance for doubtful debts 30,000

Increase in accounts payable 154,000

Increase in accruals 465,000

Increase in lease liability 20,000

Increase in provisions (93,000) (80,000)

Cash generated from operations 1,010,000

Less: taxes paid (refer WN-1) 55,000

Net cash generated from operating activities (a) 955,000

Cash flow from investing activities

Investment in associated company (250,000)

Investments made (188,000)

Tennis equipment purchased (80,000)

Purchase of equipment under lease (25,000)

Sale proceeds from plant & equipment 20,000

Dividends received 51,000

Net cash used in investing activities (b) (472,000)

Cash flow from financing activities

Repayment of borrowings (300,000)

T Pty Ltd

CASH FLOW STATEMENT

For the year ended on June 30, 2020

(Amount in $)

Particulars

For the year

ended on

June 30, 2020

Cash flow from operating activities

Profit before tax 365,000

Non-cash adjustment:

Warranty Expense 314,000

Depreciation expense 140,000 454,000

Non-operating expenses/ incomes:

Dividends income (51,000)

Interest expense 315,000

Finance charges 7,000 271,000

Operating profit before working capital changes 1,090,000

Changes in working capital

Increase in inventory (288,000)

Increase in prepayments (115,000)

Increase in accounts receivable (243,000)

Increase in deferred tax assets (10,000)

Allowance for doubtful debts 30,000

Increase in accounts payable 154,000

Increase in accruals 465,000

Increase in lease liability 20,000

Increase in provisions (93,000) (80,000)

Cash generated from operations 1,010,000

Less: taxes paid (refer WN-1) 55,000

Net cash generated from operating activities (a) 955,000

Cash flow from investing activities

Investment in associated company (250,000)

Investments made (188,000)

Tennis equipment purchased (80,000)

Purchase of equipment under lease (25,000)

Sale proceeds from plant & equipment 20,000

Dividends received 51,000

Net cash used in investing activities (b) (472,000)

Cash flow from financing activities

Repayment of borrowings (300,000)

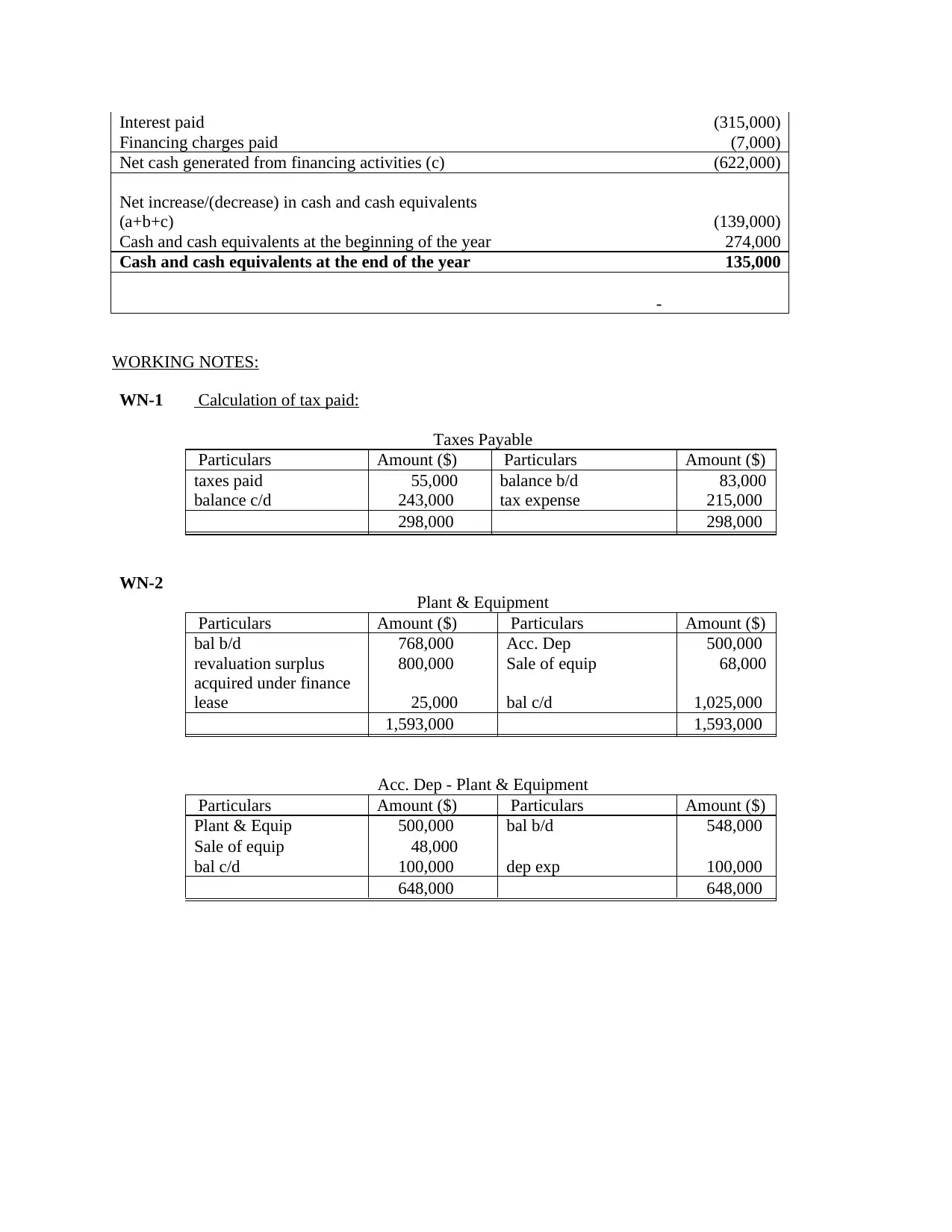

Interest paid (315,000)

Financing charges paid (7,000)

Net cash generated from financing activities (c) (622,000)

Net increase/(decrease) in cash and cash equivalents

(a+b+c) (139,000)

Cash and cash equivalents at the beginning of the year 274,000

Cash and cash equivalents at the end of the year 135,000

-

WORKING NOTES:

WN-1 Calculation of tax paid:

Taxes Payable

Particulars Amount ($) Particulars Amount ($)

taxes paid 55,000 balance b/d 83,000

balance c/d 243,000 tax expense 215,000

298,000 298,000

WN-2

Plant & Equipment

Particulars Amount ($) Particulars Amount ($)

bal b/d 768,000 Acc. Dep 500,000

revaluation surplus 800,000 Sale of equip 68,000

acquired under finance

lease 25,000 bal c/d 1,025,000

1,593,000 1,593,000

Acc. Dep - Plant & Equipment

Particulars Amount ($) Particulars Amount ($)

Plant & Equip 500,000 bal b/d 548,000

Sale of equip 48,000

bal c/d 100,000 dep exp 100,000

648,000 648,000

Financing charges paid (7,000)

Net cash generated from financing activities (c) (622,000)

Net increase/(decrease) in cash and cash equivalents

(a+b+c) (139,000)

Cash and cash equivalents at the beginning of the year 274,000

Cash and cash equivalents at the end of the year 135,000

-

WORKING NOTES:

WN-1 Calculation of tax paid:

Taxes Payable

Particulars Amount ($) Particulars Amount ($)

taxes paid 55,000 balance b/d 83,000

balance c/d 243,000 tax expense 215,000

298,000 298,000

WN-2

Plant & Equipment

Particulars Amount ($) Particulars Amount ($)

bal b/d 768,000 Acc. Dep 500,000

revaluation surplus 800,000 Sale of equip 68,000

acquired under finance

lease 25,000 bal c/d 1,025,000

1,593,000 1,593,000

Acc. Dep - Plant & Equipment

Particulars Amount ($) Particulars Amount ($)

Plant & Equip 500,000 bal b/d 548,000

Sale of equip 48,000

bal c/d 100,000 dep exp 100,000

648,000 648,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Solution-5

a. Journal Entries

Date Particulars Dr./Cr. Amount ($)

22-Apr-18 No Entry

30-Apr-18 Inventory Dr. 35,294.12

To Accounts Payable Cr. (35,294.12)

30-May-18 Accounts Payable Dr. 11,764.71

To Bank Cr. (11,682.24)

To Realised Gain on forex Cr. (82.46)

30-Jun-18 Accounts Payable Dr. 11,764.71

To Bank Cr. (11,641.44)

To Realised Gain on forex Cr. (123.26)

30-Jun-18 Accounts Payable Dr. 123.26

To Unrealised Gain on forex Cr. (123.26)

31-Jul-18 Accounts Payable Dr. 11,641.44

To Bank Cr. (11,185.68)

To Realised Gain on forex Cr. (455.76)

Month Rate Payable

22-Apr-18 8.00 37,500.00

30-Apr-18 8.50 35,294.12

31-May-18 8.56 35,046.73

30-Jun-18 8.59 34,924.33

31-Jul-18 8.94 33,557.05

Treatment adopted:

As per the generally adopted accounting norms, the inventory is recorded in the books when the title of

goods is passed. As per the contract in the given case, the title of goods is passed on 30 April, 2018, i.e.

on the date of delivery and hence, the goods are recorded as inventory on 30 April, 2018 at the prevailing

exchange rate. Further, AASB 121, “The effect of changes in foreign exchange rates”, requires to fair

value the pending liabilities and assets at the reporting date, i.e. 30 June, 2018 and respective gain or loss

to be transferred to P&L. The same has been followed. Further, the liabilities are paid off at the payment

dates and respective gain or loss due to foreign exchange fluctuations is recorded.

a. Journal Entries

Date Particulars Dr./Cr. Amount ($)

22-Apr-18 No Entry

30-Apr-18 Inventory Dr. 35,294.12

To Accounts Payable Cr. (35,294.12)

30-May-18 Accounts Payable Dr. 11,764.71

To Bank Cr. (11,682.24)

To Realised Gain on forex Cr. (82.46)

30-Jun-18 Accounts Payable Dr. 11,764.71

To Bank Cr. (11,641.44)

To Realised Gain on forex Cr. (123.26)

30-Jun-18 Accounts Payable Dr. 123.26

To Unrealised Gain on forex Cr. (123.26)

31-Jul-18 Accounts Payable Dr. 11,641.44

To Bank Cr. (11,185.68)

To Realised Gain on forex Cr. (455.76)

Month Rate Payable

22-Apr-18 8.00 37,500.00

30-Apr-18 8.50 35,294.12

31-May-18 8.56 35,046.73

30-Jun-18 8.59 34,924.33

31-Jul-18 8.94 33,557.05

Treatment adopted:

As per the generally adopted accounting norms, the inventory is recorded in the books when the title of

goods is passed. As per the contract in the given case, the title of goods is passed on 30 April, 2018, i.e.

on the date of delivery and hence, the goods are recorded as inventory on 30 April, 2018 at the prevailing

exchange rate. Further, AASB 121, “The effect of changes in foreign exchange rates”, requires to fair

value the pending liabilities and assets at the reporting date, i.e. 30 June, 2018 and respective gain or loss

to be transferred to P&L. The same has been followed. Further, the liabilities are paid off at the payment

dates and respective gain or loss due to foreign exchange fluctuations is recorded.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

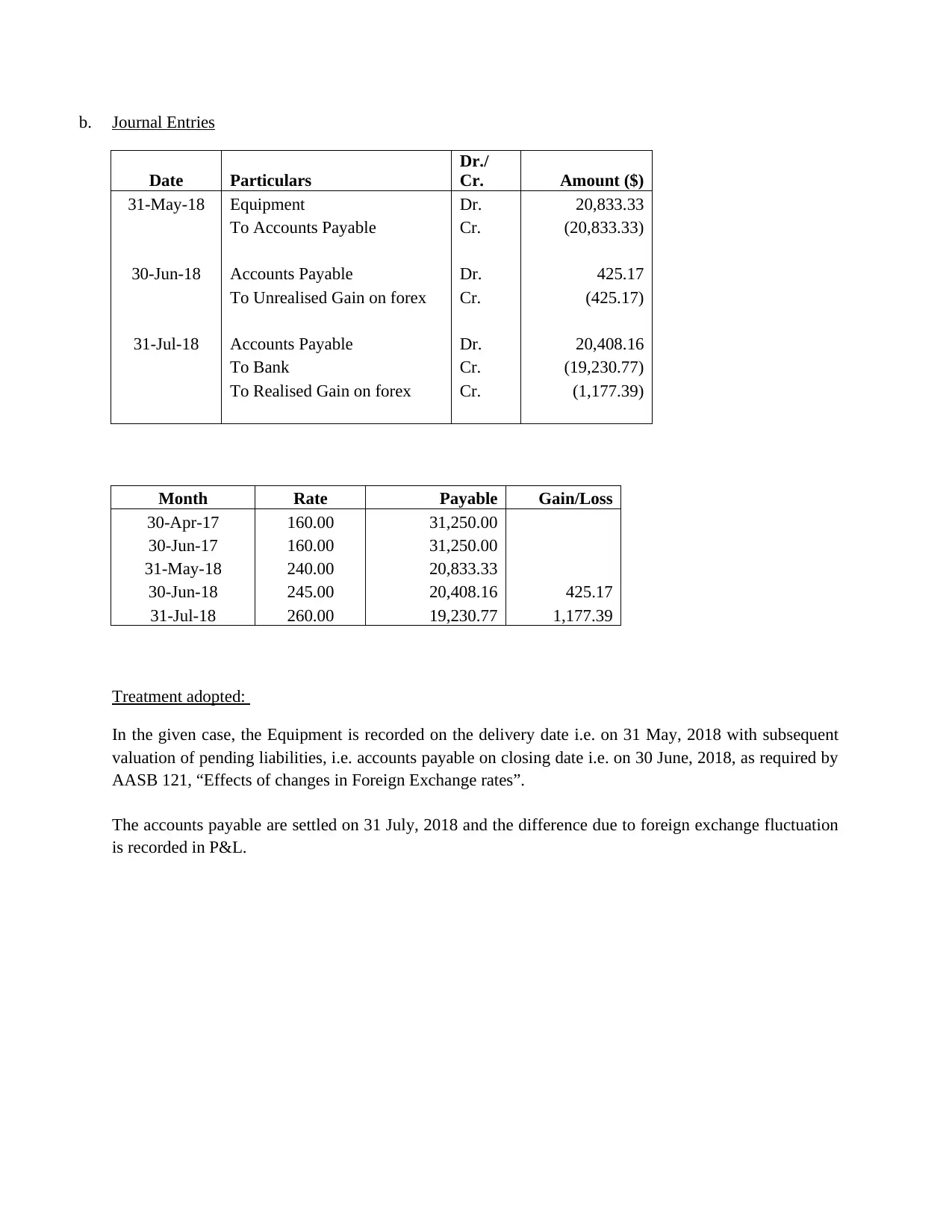

b. Journal Entries

Date Particulars

Dr./

Cr. Amount ($)

31-May-18 Equipment Dr. 20,833.33

To Accounts Payable Cr. (20,833.33)

30-Jun-18 Accounts Payable Dr. 425.17

To Unrealised Gain on forex Cr. (425.17)

31-Jul-18 Accounts Payable Dr. 20,408.16

To Bank Cr. (19,230.77)

To Realised Gain on forex Cr. (1,177.39)

Month Rate Payable Gain/Loss

30-Apr-17 160.00 31,250.00

30-Jun-17 160.00 31,250.00

31-May-18 240.00 20,833.33

30-Jun-18 245.00 20,408.16 425.17

31-Jul-18 260.00 19,230.77 1,177.39

Treatment adopted:

In the given case, the Equipment is recorded on the delivery date i.e. on 31 May, 2018 with subsequent

valuation of pending liabilities, i.e. accounts payable on closing date i.e. on 30 June, 2018, as required by

AASB 121, “Effects of changes in Foreign Exchange rates”.

The accounts payable are settled on 31 July, 2018 and the difference due to foreign exchange fluctuation

is recorded in P&L.

Date Particulars

Dr./

Cr. Amount ($)

31-May-18 Equipment Dr. 20,833.33

To Accounts Payable Cr. (20,833.33)

30-Jun-18 Accounts Payable Dr. 425.17

To Unrealised Gain on forex Cr. (425.17)

31-Jul-18 Accounts Payable Dr. 20,408.16

To Bank Cr. (19,230.77)

To Realised Gain on forex Cr. (1,177.39)

Month Rate Payable Gain/Loss

30-Apr-17 160.00 31,250.00

30-Jun-17 160.00 31,250.00

31-May-18 240.00 20,833.33

30-Jun-18 245.00 20,408.16 425.17

31-Jul-18 260.00 19,230.77 1,177.39

Treatment adopted:

In the given case, the Equipment is recorded on the delivery date i.e. on 31 May, 2018 with subsequent

valuation of pending liabilities, i.e. accounts payable on closing date i.e. on 30 June, 2018, as required by

AASB 121, “Effects of changes in Foreign Exchange rates”.

The accounts payable are settled on 31 July, 2018 and the difference due to foreign exchange fluctuation

is recorded in P&L.

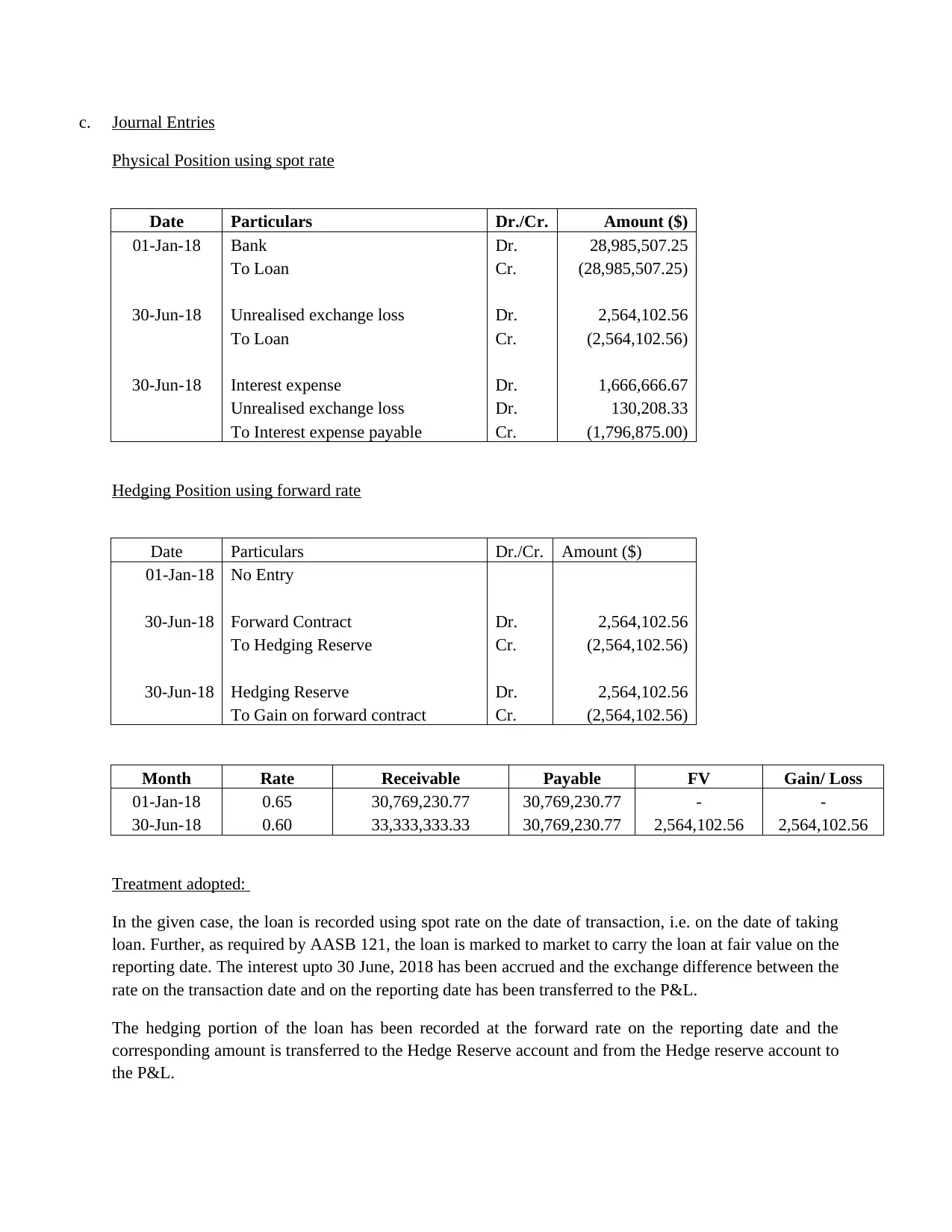

c. Journal Entries

Physical Position using spot rate

Date Particulars Dr./Cr. Amount ($)

01-Jan-18 Bank Dr. 28,985,507.25

To Loan Cr. (28,985,507.25)

30-Jun-18 Unrealised exchange loss Dr. 2,564,102.56

To Loan Cr. (2,564,102.56)

30-Jun-18 Interest expense Dr. 1,666,666.67

Unrealised exchange loss Dr. 130,208.33

To Interest expense payable Cr. (1,796,875.00)

Hedging Position using forward rate

Date Particulars Dr./Cr. Amount ($)

01-Jan-18 No Entry

30-Jun-18 Forward Contract Dr. 2,564,102.56

To Hedging Reserve Cr. (2,564,102.56)

30-Jun-18 Hedging Reserve Dr. 2,564,102.56

To Gain on forward contract Cr. (2,564,102.56)

Month Rate Receivable Payable FV Gain/ Loss

01-Jan-18 0.65 30,769,230.77 30,769,230.77 - -

30-Jun-18 0.60 33,333,333.33 30,769,230.77 2,564,102.56 2,564,102.56

Treatment adopted:

In the given case, the loan is recorded using spot rate on the date of transaction, i.e. on the date of taking

loan. Further, as required by AASB 121, the loan is marked to market to carry the loan at fair value on the

reporting date. The interest upto 30 June, 2018 has been accrued and the exchange difference between the

rate on the transaction date and on the reporting date has been transferred to the P&L.

The hedging portion of the loan has been recorded at the forward rate on the reporting date and the

corresponding amount is transferred to the Hedge Reserve account and from the Hedge reserve account to

the P&L.

Physical Position using spot rate

Date Particulars Dr./Cr. Amount ($)

01-Jan-18 Bank Dr. 28,985,507.25

To Loan Cr. (28,985,507.25)

30-Jun-18 Unrealised exchange loss Dr. 2,564,102.56

To Loan Cr. (2,564,102.56)

30-Jun-18 Interest expense Dr. 1,666,666.67

Unrealised exchange loss Dr. 130,208.33

To Interest expense payable Cr. (1,796,875.00)

Hedging Position using forward rate

Date Particulars Dr./Cr. Amount ($)

01-Jan-18 No Entry

30-Jun-18 Forward Contract Dr. 2,564,102.56

To Hedging Reserve Cr. (2,564,102.56)

30-Jun-18 Hedging Reserve Dr. 2,564,102.56

To Gain on forward contract Cr. (2,564,102.56)

Month Rate Receivable Payable FV Gain/ Loss

01-Jan-18 0.65 30,769,230.77 30,769,230.77 - -

30-Jun-18 0.60 33,333,333.33 30,769,230.77 2,564,102.56 2,564,102.56

Treatment adopted:

In the given case, the loan is recorded using spot rate on the date of transaction, i.e. on the date of taking

loan. Further, as required by AASB 121, the loan is marked to market to carry the loan at fair value on the

reporting date. The interest upto 30 June, 2018 has been accrued and the exchange difference between the

rate on the transaction date and on the reporting date has been transferred to the P&L.

The hedging portion of the loan has been recorded at the forward rate on the reporting date and the

corresponding amount is transferred to the Hedge Reserve account and from the Hedge reserve account to

the P&L.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

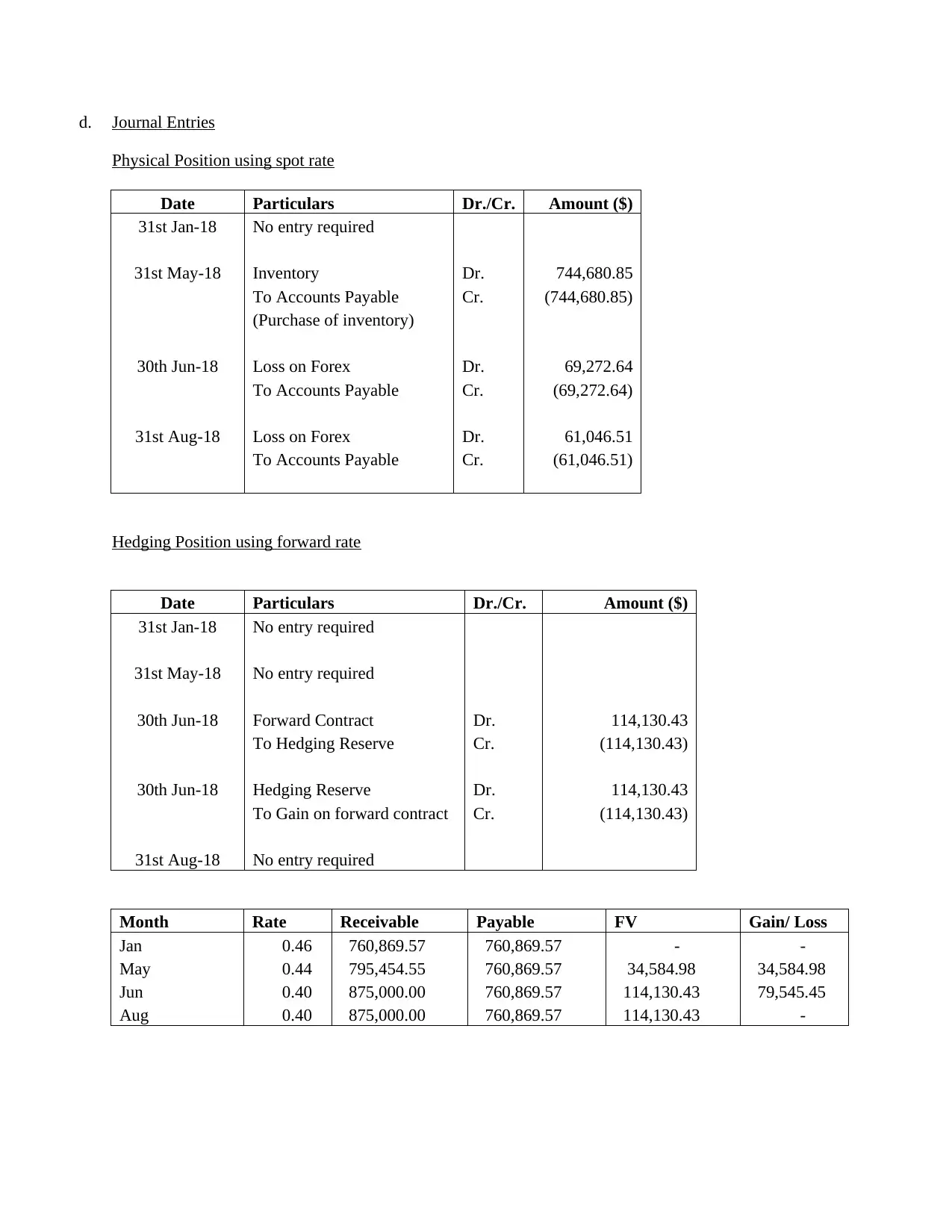

d. Journal Entries

Physical Position using spot rate

Date Particulars Dr./Cr. Amount ($)

31st Jan-18 No entry required

31st May-18 Inventory Dr. 744,680.85

To Accounts Payable Cr. (744,680.85)

(Purchase of inventory)

30th Jun-18 Loss on Forex Dr. 69,272.64

To Accounts Payable Cr. (69,272.64)

31st Aug-18 Loss on Forex Dr. 61,046.51

To Accounts Payable Cr. (61,046.51)

Hedging Position using forward rate

Date Particulars Dr./Cr. Amount ($)

31st Jan-18 No entry required

31st May-18 No entry required

30th Jun-18 Forward Contract Dr. 114,130.43

To Hedging Reserve Cr. (114,130.43)

30th Jun-18 Hedging Reserve Dr. 114,130.43

To Gain on forward contract Cr. (114,130.43)

31st Aug-18 No entry required

Month Rate Receivable Payable FV Gain/ Loss

Jan 0.46 760,869.57 760,869.57 - -

May 0.44 795,454.55 760,869.57 34,584.98 34,584.98

Jun 0.40 875,000.00 760,869.57 114,130.43 79,545.45

Aug 0.40 875,000.00 760,869.57 114,130.43 -

Physical Position using spot rate

Date Particulars Dr./Cr. Amount ($)

31st Jan-18 No entry required

31st May-18 Inventory Dr. 744,680.85

To Accounts Payable Cr. (744,680.85)

(Purchase of inventory)

30th Jun-18 Loss on Forex Dr. 69,272.64

To Accounts Payable Cr. (69,272.64)

31st Aug-18 Loss on Forex Dr. 61,046.51

To Accounts Payable Cr. (61,046.51)

Hedging Position using forward rate

Date Particulars Dr./Cr. Amount ($)

31st Jan-18 No entry required

31st May-18 No entry required

30th Jun-18 Forward Contract Dr. 114,130.43

To Hedging Reserve Cr. (114,130.43)

30th Jun-18 Hedging Reserve Dr. 114,130.43

To Gain on forward contract Cr. (114,130.43)

31st Aug-18 No entry required

Month Rate Receivable Payable FV Gain/ Loss

Jan 0.46 760,869.57 760,869.57 - -

May 0.44 795,454.55 760,869.57 34,584.98 34,584.98

Jun 0.40 875,000.00 760,869.57 114,130.43 79,545.45

Aug 0.40 875,000.00 760,869.57 114,130.43 -

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Treatment adopted:

The inventory is recorded on the date of delivery (as title and possession of the goods is passed on the

date of delivery) using the spot rate prevailing on the transaction date. Then, the amount payable to

vendor, i.e. accounts payable is marked to market on the reporting date and finally settled on 31st August,

2018 by paying off the liability at the prevailing spot rate and differences arising due to foreign exchange

fluctuations are recorded in P&L.

The treatment of hedging portion is that the contract is valued on the reporting date i.e. 30th June, 2018 at

the forward rates prevailing on 30th June and corresponding amount is transferred to the P&L through

Hedging Reserve.

The inventory is recorded on the date of delivery (as title and possession of the goods is passed on the

date of delivery) using the spot rate prevailing on the transaction date. Then, the amount payable to

vendor, i.e. accounts payable is marked to market on the reporting date and finally settled on 31st August,

2018 by paying off the liability at the prevailing spot rate and differences arising due to foreign exchange

fluctuations are recorded in P&L.

The treatment of hedging portion is that the contract is valued on the reporting date i.e. 30th June, 2018 at

the forward rates prevailing on 30th June and corresponding amount is transferred to the P&L through

Hedging Reserve.

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.