Corporate & Financial Accounting: IFRS, Equity, Australian Banks

VerifiedAdded on 2023/06/07

|11

|2673

|460

Report

AI Summary

This report provides a comprehensive analysis of corporate and financial accounting policies, focusing on the efficiency of the accounting framework and the positive impacts of IFRS standards on organizations, particularly within the Australian banking sector. The report explores corporate regulation, examining the necessity of regulatory control over financial accounting and the limitations of management-led approaches. It delves into accounting standard settings, highlighting Australia's alignment with IFRS guidelines and the role of AASB. An equity analysis of four ASX-listed banks (NAB, CBA, ANZ, and Westpac) is presented, detailing their equity components and accounting policies. Finally, a comparative analysis assesses the debt and equity conditions of these banks, revealing Westpac's robust reporting and the consistent application of accounting principles across the institutions, referencing key legislative acts and frameworks. Desklib offers this and many other solved assignments for students.

Corporate & Financial Accounting

[Student Name]

[Student University]

[Author Note]

[Word count:]

Executive summary:

[Student Name]

[Student University]

[Author Note]

[Word count:]

Executive summary:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The report is on the financial and accounting policies. It identifies that the accounting framework

is more efficient than the management and IFRS setting has helped different types of

organizations with accurate and transparent financial information. So, the market and economy

receive positive impacts from the standards and the same is reflected in the case of the four

banks in Australia too.

1

is more efficient than the management and IFRS setting has helped different types of

organizations with accurate and transparent financial information. So, the market and economy

receive positive impacts from the standards and the same is reflected in the case of the four

banks in Australia too.

1

Introduction: 3

Discussion: 3

i) Corporate Regulation: 3

ii) Accounting Standard Setting: 5

iii) Equity analysis: 6

iv) Comparative analysis: 8

Conclusion: 9

References: 9

Websites: 10

2

Discussion: 3

i) Corporate Regulation: 3

ii) Accounting Standard Setting: 5

iii) Equity analysis: 6

iv) Comparative analysis: 8

Conclusion: 9

References: 9

Websites: 10

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction:

The report covers various dimensions of the corporate and financial accounting. Therefore the

four sections of this report are dedicated to regulations, standard settings as well as equity

analysis. In the first section, the report discusses if the financial accounting requires regulatory

control or management is adequate to deal with it. The second section deals with the accounting

standard where the IFRS and IASB are major topics. In the third section, the report identifies

four ASX listed companies and provides a discussion on the equity management. Finally, the

comparative analysis in the fourth section discusses the debt and equity conditions of the four

companies.

Discussion:

i) Corporate Regulation:

The financial accounting is defined as a process where the major aims are information

identification, information measurement, and information communication. The term information

means the specific accounting information which helps the financial judgment and decisions. As

a part of the bookkeeping process in financial accounting, the information identification is done

while the same information is extracted from the multi-entry bookkeeping system for

measurement and decisions. The final communicated or presented information covers profit/loss

and comprehensive income analysis (Henderson et al, 2015). So, the financial accounting is

focused in the areas like recorded transactions or accounting controls (bank reconciliation,

suspense accounts), financial performance in terms of profit or loss statement as well as financial

statement preparation. Again, the business environment deals with different types of

organizations (sole trader, partnerships, joint ventures, unlimited company etc). That means the

accounting regulation is required in terms of public interests (accuracy and transparency of

information) as well as for the health of the company. Moreover, the accounting regulations can

control the issues during the financial crisis as it asks for the mandatory disclosure of the

important information. In the case of the public security market, the contracts and impartial

courts are not sufficient where the non-governmental parties and their voluntary arrangements

3

The report covers various dimensions of the corporate and financial accounting. Therefore the

four sections of this report are dedicated to regulations, standard settings as well as equity

analysis. In the first section, the report discusses if the financial accounting requires regulatory

control or management is adequate to deal with it. The second section deals with the accounting

standard where the IFRS and IASB are major topics. In the third section, the report identifies

four ASX listed companies and provides a discussion on the equity management. Finally, the

comparative analysis in the fourth section discusses the debt and equity conditions of the four

companies.

Discussion:

i) Corporate Regulation:

The financial accounting is defined as a process where the major aims are information

identification, information measurement, and information communication. The term information

means the specific accounting information which helps the financial judgment and decisions. As

a part of the bookkeeping process in financial accounting, the information identification is done

while the same information is extracted from the multi-entry bookkeeping system for

measurement and decisions. The final communicated or presented information covers profit/loss

and comprehensive income analysis (Henderson et al, 2015). So, the financial accounting is

focused in the areas like recorded transactions or accounting controls (bank reconciliation,

suspense accounts), financial performance in terms of profit or loss statement as well as financial

statement preparation. Again, the business environment deals with different types of

organizations (sole trader, partnerships, joint ventures, unlimited company etc). That means the

accounting regulation is required in terms of public interests (accuracy and transparency of

information) as well as for the health of the company. Moreover, the accounting regulations can

control the issues during the financial crisis as it asks for the mandatory disclosure of the

important information. In the case of the public security market, the contracts and impartial

courts are not sufficient where the non-governmental parties and their voluntary arrangements

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

can increase market complexities. Again, if there are no unresolved market failure issue then the

accounting regulations seem "not required" as the management can control the information.

However, there are always the risks of self-interested agents inside and outside the business

environment where the primary concerns are individual wealth and power. If the financial

accounting and reporting are under the control of management only then these self-interested

individuals will use the control as a scope to increase power. But the regulatory control

introduces complex and detail steps to deal with accounting information so for exclusive and

firm-specific benefits the regulatory framework is required. Moreover, the management

decisions and quality can fluctuate according to the business types so the market-wide effects

need a standard regulatory framework. During the financial crisis, the market needs fair value

accounting in terms of pricing patterns and cyclical financial pressure (Schaltegger and Burritt,

2017). So, to address the issues like discretion, bank transparency, cross-country loan variation,

market discipline as well as international assets the management seems inadequate. In terms of

interstate lines, the regulatory framework can deal with all the dimensions of trade securities

while establishing the public sector standard. In this context, the US-based SEC and SOX act

2002 seem significant. Again, the company type must be a factor for the content of the financial

statement. As an example, the UK uses company law to describe the size of the company where

major criteria are a financial position statement, turnover rate and a number of employees.

Moreover, the large private companies and public companies have different contents in the

financial statement (Huber, 2015). So, the reporting should be regulated considering the complex

dimensions of the financial environment.

4

accounting regulations seem "not required" as the management can control the information.

However, there are always the risks of self-interested agents inside and outside the business

environment where the primary concerns are individual wealth and power. If the financial

accounting and reporting are under the control of management only then these self-interested

individuals will use the control as a scope to increase power. But the regulatory control

introduces complex and detail steps to deal with accounting information so for exclusive and

firm-specific benefits the regulatory framework is required. Moreover, the management

decisions and quality can fluctuate according to the business types so the market-wide effects

need a standard regulatory framework. During the financial crisis, the market needs fair value

accounting in terms of pricing patterns and cyclical financial pressure (Schaltegger and Burritt,

2017). So, to address the issues like discretion, bank transparency, cross-country loan variation,

market discipline as well as international assets the management seems inadequate. In terms of

interstate lines, the regulatory framework can deal with all the dimensions of trade securities

while establishing the public sector standard. In this context, the US-based SEC and SOX act

2002 seem significant. Again, the company type must be a factor for the content of the financial

statement. As an example, the UK uses company law to describe the size of the company where

major criteria are a financial position statement, turnover rate and a number of employees.

Moreover, the large private companies and public companies have different contents in the

financial statement (Huber, 2015). So, the reporting should be regulated considering the complex

dimensions of the financial environment.

4

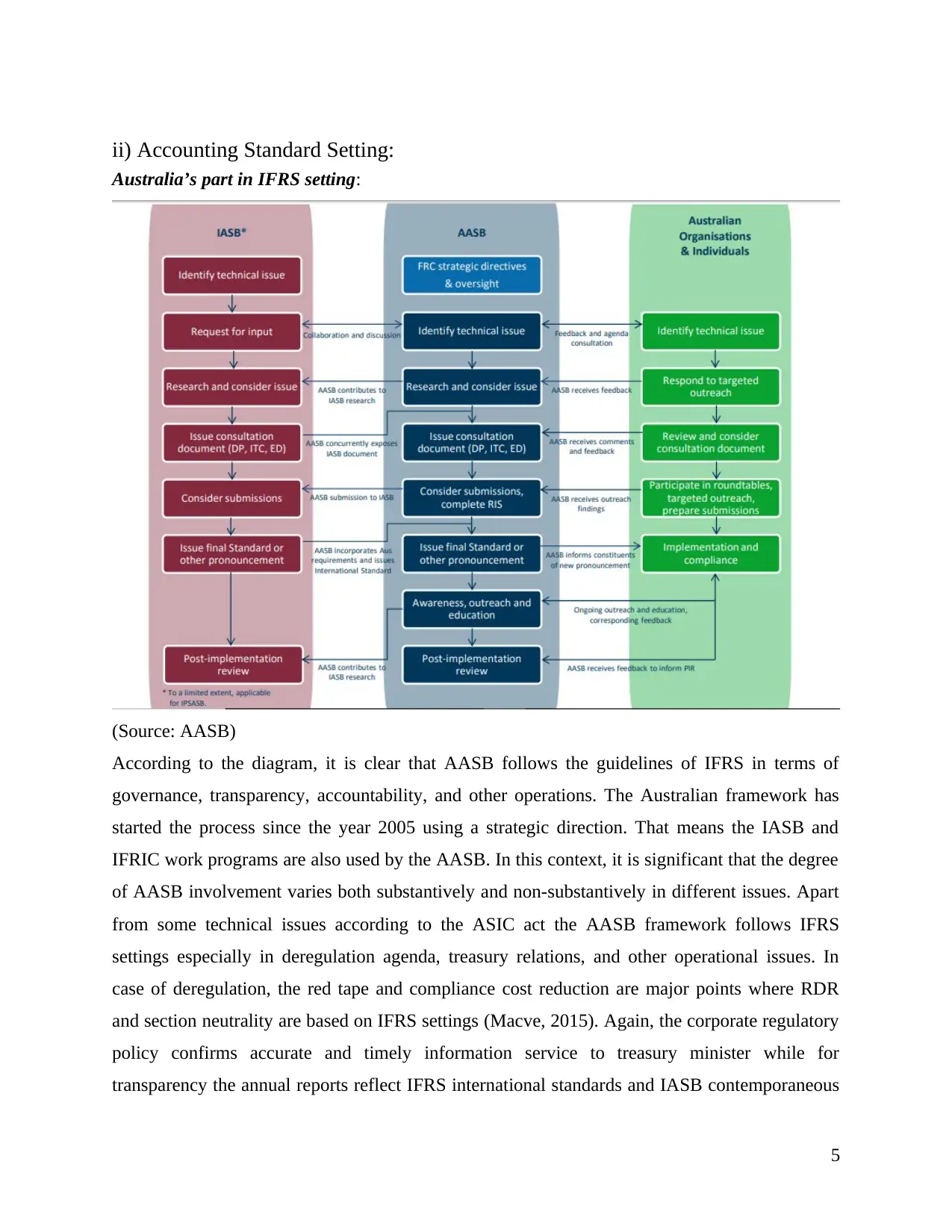

ii) Accounting Standard Setting:

Australia’s part in IFRS setting:

(Source: AASB)

According to the diagram, it is clear that AASB follows the guidelines of IFRS in terms of

governance, transparency, accountability, and other operations. The Australian framework has

started the process since the year 2005 using a strategic direction. That means the IASB and

IFRIC work programs are also used by the AASB. In this context, it is significant that the degree

of AASB involvement varies both substantively and non-substantively in different issues. Apart

from some technical issues according to the ASIC act the AASB framework follows IFRS

settings especially in deregulation agenda, treasury relations, and other operational issues. In

case of deregulation, the red tape and compliance cost reduction are major points where RDR

and section neutrality are based on IFRS settings (Macve, 2015). Again, the corporate regulatory

policy confirms accurate and timely information service to treasury minister while for

transparency the annual reports reflect IFRS international standards and IASB contemporaneous

5

Australia’s part in IFRS setting:

(Source: AASB)

According to the diagram, it is clear that AASB follows the guidelines of IFRS in terms of

governance, transparency, accountability, and other operations. The Australian framework has

started the process since the year 2005 using a strategic direction. That means the IASB and

IFRIC work programs are also used by the AASB. In this context, it is significant that the degree

of AASB involvement varies both substantively and non-substantively in different issues. Apart

from some technical issues according to the ASIC act the AASB framework follows IFRS

settings especially in deregulation agenda, treasury relations, and other operational issues. In

case of deregulation, the red tape and compliance cost reduction are major points where RDR

and section neutrality are based on IFRS settings (Macve, 2015). Again, the corporate regulatory

policy confirms accurate and timely information service to treasury minister while for

transparency the annual reports reflect IFRS international standards and IASB contemporaneous

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

domestic strategy. Apart from this, the major operational issues are dealt with PS and PGPA acts

which are influenced by the IASB framework.

IASB compulsory conditions:

The IFRS is considered as the set of international accounting standards to cover a particular type

of transactions and the accounting events in the financial statements. Moreover, the set of

standards is issued by the IASB (International accounting standard board) to determine a specific

way of accounting reports. The key goal of IFRS is to remove the complexities of an

international accounting environment with a common financial language. Therefore, the business

and accounts are more transparent in different countries and accounting environment for these

set of standards. Today, the major countries who have adopted the IFRS setting include India,

Japan, Malaysia, Russia, Canada etc. However, the IASB establishing continent of USA is a little

different in this context. Although many Asian and South American countries, as well as EU,

have adopted the IFRS but the USA cannot switch from SEC to IFRS (Carson et al, 2017). In

terms of legal complexity and financial education issues, the complete switch is not possible.

However, USA allows the IFRS information as a supplement for the SEC based financial

fillings. Similarly, the other IASB member countries allow the IFRS standard setting as a

supplement of existing financial structure to reduce the accounting policy issues Moreover, the

IASB member countries have the general idea about the IASB environment so the global

adoption of IFRS or using the same as the support is helpful for alternative comparison costs as

well as free flow of information.

iii) Equity analysis:

The report selects the big four banks (largest public sector companies) of Australia who are listed

in the ASX and belongs to the financial industry. According to the financial statement, the items

of equity (common stock, preferred stock, capital surplus, retained earnings, treasury stocks etc)

are covered with detail discussion on them. The discussion is given below:

NAB:

According to the 2017 balanced sheet, the contribute equity varies from 30,000-34,5000 million

dollars while the reserves are in the range of 190-629 million dollars in the past four years.

Again, the retained profit varies from the 15,000- 16500 million dollars which determines that

the comparative information somehow reflect the changes in interest accrual rates. The total

6

which are influenced by the IASB framework.

IASB compulsory conditions:

The IFRS is considered as the set of international accounting standards to cover a particular type

of transactions and the accounting events in the financial statements. Moreover, the set of

standards is issued by the IASB (International accounting standard board) to determine a specific

way of accounting reports. The key goal of IFRS is to remove the complexities of an

international accounting environment with a common financial language. Therefore, the business

and accounts are more transparent in different countries and accounting environment for these

set of standards. Today, the major countries who have adopted the IFRS setting include India,

Japan, Malaysia, Russia, Canada etc. However, the IASB establishing continent of USA is a little

different in this context. Although many Asian and South American countries, as well as EU,

have adopted the IFRS but the USA cannot switch from SEC to IFRS (Carson et al, 2017). In

terms of legal complexity and financial education issues, the complete switch is not possible.

However, USA allows the IFRS information as a supplement for the SEC based financial

fillings. Similarly, the other IASB member countries allow the IFRS standard setting as a

supplement of existing financial structure to reduce the accounting policy issues Moreover, the

IASB member countries have the general idea about the IASB environment so the global

adoption of IFRS or using the same as the support is helpful for alternative comparison costs as

well as free flow of information.

iii) Equity analysis:

The report selects the big four banks (largest public sector companies) of Australia who are listed

in the ASX and belongs to the financial industry. According to the financial statement, the items

of equity (common stock, preferred stock, capital surplus, retained earnings, treasury stocks etc)

are covered with detail discussion on them. The discussion is given below:

NAB:

According to the 2017 balanced sheet, the contribute equity varies from 30,000-34,5000 million

dollars while the reserves are in the range of 190-629 million dollars in the past four years.

Again, the retained profit varies from the 15,000- 16500 million dollars which determines that

the comparative information somehow reflect the changes in interest accrual rates. The total

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

equity considering the parent entity interest is varying between 48,000-51000 million dollars

while the non-controlling interest in controlled entities varies from 11-23 million dollars. The

equity changes statement ensures that treasury share adjustment in terms of insurance is fixed

while the equity-based compensation and distribution policies have flexible pattern (Bryce et al,

2015). So, the accounting policy determines that the debt instruments are majorly dependent on

the amortized cost while investment in equity instrument is not held for trading and the same has

no contingent consideration issues too. Moreover, the credit impairment covers a three-tier credit

loss model in terms of amortized costs.

CBA:

According to the balance sheet, the asset and liabilities are little flat for the consecutive four

years and the shareholder equity covers three major points and they are share capital, ordinary

share capital and other equity instruments. The reserves and retained profits are other important

instruments covering the attributable equity holders and non-controlling interests. The ordinary

share capital varies from 33,000-35,000 million dollars while the reserves vary between 2500-

3100 dollars. Again, the retained profits move between 20,000-25,000 million dollars by

introducing the total shareholders' equity to 58,000-63,000 million. In terms of equity changes

the redemption, share-based payments, reinvestment plans, dividend policy are important and the

accounting policy confirms revenue profits capital reserves, asset revaluation, and cash flow

hedge reserves as the key equity instruments.

ANZ:

The remuneration report and balance sheet both provide the equity information. The types of

equity include deferred share, ordinary share, performance rights as well as the capital notes.

Moreover, the balanced sheet states that the shareholder equity in case of an ordinary share

varies between 28,000-29,000 million while reserves are highly variable (from 37-1078 million).

The retained earnings move from 27,000-29,000 million dollars. The shared capital and

attributable reserves change consistently. The major equity instruments are treasury share

adjustments as well as share acquisitions schemes and the life insurance funds. Moreover, the

reinvestment plan according to accounting policy is covered by the initial investment date rate.

The AASB instruments are followed properly in terms of insurance, leases and other operating

incomes.

WESTPAC:

7

while the non-controlling interest in controlled entities varies from 11-23 million dollars. The

equity changes statement ensures that treasury share adjustment in terms of insurance is fixed

while the equity-based compensation and distribution policies have flexible pattern (Bryce et al,

2015). So, the accounting policy determines that the debt instruments are majorly dependent on

the amortized cost while investment in equity instrument is not held for trading and the same has

no contingent consideration issues too. Moreover, the credit impairment covers a three-tier credit

loss model in terms of amortized costs.

CBA:

According to the balance sheet, the asset and liabilities are little flat for the consecutive four

years and the shareholder equity covers three major points and they are share capital, ordinary

share capital and other equity instruments. The reserves and retained profits are other important

instruments covering the attributable equity holders and non-controlling interests. The ordinary

share capital varies from 33,000-35,000 million dollars while the reserves vary between 2500-

3100 dollars. Again, the retained profits move between 20,000-25,000 million dollars by

introducing the total shareholders' equity to 58,000-63,000 million. In terms of equity changes

the redemption, share-based payments, reinvestment plans, dividend policy are important and the

accounting policy confirms revenue profits capital reserves, asset revaluation, and cash flow

hedge reserves as the key equity instruments.

ANZ:

The remuneration report and balance sheet both provide the equity information. The types of

equity include deferred share, ordinary share, performance rights as well as the capital notes.

Moreover, the balanced sheet states that the shareholder equity in case of an ordinary share

varies between 28,000-29,000 million while reserves are highly variable (from 37-1078 million).

The retained earnings move from 27,000-29,000 million dollars. The shared capital and

attributable reserves change consistently. The major equity instruments are treasury share

adjustments as well as share acquisitions schemes and the life insurance funds. Moreover, the

reinvestment plan according to accounting policy is covered by the initial investment date rate.

The AASB instruments are followed properly in terms of insurance, leases and other operating

incomes.

WESTPAC:

7

Considering the five year summary of the financial giant the total shareholder equity and non-

controlling interest varies between 41,000-61,000 million dollars. In this context, the ordinary

share increases consistently from 174 million to the 188 million dollars. However, the share is

fixed for the last two years (2016, 2017) while the share price fluctuates 34-40 million

inconsistently in terms of high, low and close types. Moreover, the capital adequacy is based on

the total equity to total asset percentage as well as the total equity to average asset percentage.

The ratios vary from 6.4-7.9% in the five consecutive years. The ordinary share capital varies

between 33,000-34,000 million dollars while the treasury and RSP shares vary between 360-490

million dollars. Again, the retained profits vary between 15,000-26,000 million which is

inconsistent in the five year time period. In the case of accounting policies, the AAS and

corporation act 2001 is important.

iv) Comparative analysis:

After comparing the annual reports of the four financial institutions it seems that Westpac has the

best representation covering all the accounting principles. In this context, it is significant that all

the banks use the same basis of accounting principles where the banking act 1959, corporation

act 20001 and the AASB framework are important. Moreover, the WBS annual report discusses

the historical cost conventions, comparative revisions, and policy changes terms in detail. In the

case of ANZ, the AASB based lease and contracts cover both life insurance and lease issues

significantly. That means the operating income is covered by the financial instruments like

exchange rate differences, fair value movements, cash flow, and investment hedges as well as

repayment model (Beatty and Liao, 2014). The bonus option and reinvestment plan cover the

ordinary shares while the trading securities cover the government, corporate securities as well as

the equity and overall trading securities. The CBA accounting policies are IFRS framework

based which has a high influence on the AASB framework, therefore, the bank use derivative

instruments for fair value measurement. In this context, it is significant that the foreign

operations cover the expense translation, currency reserves as well as sales investments.

Therefore, the derivative instruments include fair value, cash flow, net investment hedges while

the other embedded derivatives are AFS, loans, bills and other receivables. For NAB the equity

and debt instruments are properly highlighted in the annual report and the debt instruments cover

contractual cash flows, financial asset sales while equity instruments are fair value items like

8

controlling interest varies between 41,000-61,000 million dollars. In this context, the ordinary

share increases consistently from 174 million to the 188 million dollars. However, the share is

fixed for the last two years (2016, 2017) while the share price fluctuates 34-40 million

inconsistently in terms of high, low and close types. Moreover, the capital adequacy is based on

the total equity to total asset percentage as well as the total equity to average asset percentage.

The ratios vary from 6.4-7.9% in the five consecutive years. The ordinary share capital varies

between 33,000-34,000 million dollars while the treasury and RSP shares vary between 360-490

million dollars. Again, the retained profits vary between 15,000-26,000 million which is

inconsistent in the five year time period. In the case of accounting policies, the AAS and

corporation act 2001 is important.

iv) Comparative analysis:

After comparing the annual reports of the four financial institutions it seems that Westpac has the

best representation covering all the accounting principles. In this context, it is significant that all

the banks use the same basis of accounting principles where the banking act 1959, corporation

act 20001 and the AASB framework are important. Moreover, the WBS annual report discusses

the historical cost conventions, comparative revisions, and policy changes terms in detail. In the

case of ANZ, the AASB based lease and contracts cover both life insurance and lease issues

significantly. That means the operating income is covered by the financial instruments like

exchange rate differences, fair value movements, cash flow, and investment hedges as well as

repayment model (Beatty and Liao, 2014). The bonus option and reinvestment plan cover the

ordinary shares while the trading securities cover the government, corporate securities as well as

the equity and overall trading securities. The CBA accounting policies are IFRS framework

based which has a high influence on the AASB framework, therefore, the bank use derivative

instruments for fair value measurement. In this context, it is significant that the foreign

operations cover the expense translation, currency reserves as well as sales investments.

Therefore, the derivative instruments include fair value, cash flow, net investment hedges while

the other embedded derivatives are AFS, loans, bills and other receivables. For NAB the equity

and debt instruments are properly highlighted in the annual report and the debt instruments cover

contractual cash flows, financial asset sales while equity instruments are fair value items like

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

trading items, contractual interest terms etc. Again, the ECL issues are covered by the debt

instrument loan contracts as well as financial guarantees which means the present asset value and

credit-impaired reports are important. Considering the debt and equity positions NAB, CBA and

Westpac are in good position but the ANZ has some issues with the 2017 BIS industry sales.

Conclusion:

The report confirms that finance and accounting need a standard regulatory framework to deal

with the industrial and other cross-functional issues. Therefore, the four annual reports of the

financial industry support the requirements of the accounting policies and frameworks to deal

with transparency and fair measurement issues.

References:

Beatty, A. and Liao, S., 2014. Financial accounting in the banking industry: A review of the

empirical literature. Journal of Accounting and Economics, 58(2-3), pp.339-383.

Bryce, M., Ali, M.J. and Mather, P.R., 2015. Accounting quality in the pre-/post-IFRS adoption

periods and the impact on audit committee effectiveness—Evidence from Australia. Pacific-

Basin Finance Journal, 35, pp.163-181.

Carson, E., Fargher, N. and Zhang, Y., 2017. Explaining auditors’ propensity to issue going‐

concern opinions in Australia after the global financial crisis. Accounting & Finance.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial accounting.

Pearson Higher Education AU.

Huber, D., 2015. ON THE HEGEMONY OF FINANCIAL ACCOUNTING RESEARCH: A

SURVEY OF ACCOUNTING RESEARCH SEEN FROM A GLOBAL PERSPECTIVE.

Journal of Theoretical Accounting Research, 11(1).

Macve, R., 2015. A Conceptual Framework for Financial Accounting and Reporting: Vision,

Tool, Or Threat?. Routledge.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues, concepts,

and practice. Routledge.

9

instrument loan contracts as well as financial guarantees which means the present asset value and

credit-impaired reports are important. Considering the debt and equity positions NAB, CBA and

Westpac are in good position but the ANZ has some issues with the 2017 BIS industry sales.

Conclusion:

The report confirms that finance and accounting need a standard regulatory framework to deal

with the industrial and other cross-functional issues. Therefore, the four annual reports of the

financial industry support the requirements of the accounting policies and frameworks to deal

with transparency and fair measurement issues.

References:

Beatty, A. and Liao, S., 2014. Financial accounting in the banking industry: A review of the

empirical literature. Journal of Accounting and Economics, 58(2-3), pp.339-383.

Bryce, M., Ali, M.J. and Mather, P.R., 2015. Accounting quality in the pre-/post-IFRS adoption

periods and the impact on audit committee effectiveness—Evidence from Australia. Pacific-

Basin Finance Journal, 35, pp.163-181.

Carson, E., Fargher, N. and Zhang, Y., 2017. Explaining auditors’ propensity to issue going‐

concern opinions in Australia after the global financial crisis. Accounting & Finance.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial accounting.

Pearson Higher Education AU.

Huber, D., 2015. ON THE HEGEMONY OF FINANCIAL ACCOUNTING RESEARCH: A

SURVEY OF ACCOUNTING RESEARCH SEEN FROM A GLOBAL PERSPECTIVE.

Journal of Theoretical Accounting Research, 11(1).

Macve, R., 2015. A Conceptual Framework for Financial Accounting and Reporting: Vision,

Tool, Or Threat?. Routledge.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues, concepts,

and practice. Routledge.

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Websites:

http://www.accountingtechniciansireland.ie/Files/Documents_and_Forms/

Advanced_Financial_Accounting_Sample_Chapter.pdf

http://public.kenan-flagler.unc.edu/faculty/bushmanr/bushman_and_landsman_abr_3-2010.pdf

https://www.aasb.gov.au/About-the-AASB/The-standard-setting-process.aspx

https://static.treasury.gov.au/uploads/sites/1/2017/06/AASB_Statement_of_Intent.docx

https://www.iasplus.com/en/resources/ifrs-topics/adoption-of-ifrs

https://www.investopedia.com/terms/i/ifrs.asp

https://capital.nab.com.au/docs/NAB-2017-annual-financial-report.pdf

https://www.commbank.com.au/content/dam/commbank/about-us/shareholders/pdfs/annual-

reports/annual_report_2017_14_aug_2017.pdf

https://shareholder.anz.com/sites/default/files/2017_anz_annual_report.pdf

https://www.westpac.com.au/content/dam/public/wbc/documents/pdf/aw/ic/

2017_Westpac_Annual_Report_Web_ready_&_Bookmarked.pdf

10

http://www.accountingtechniciansireland.ie/Files/Documents_and_Forms/

Advanced_Financial_Accounting_Sample_Chapter.pdf

http://public.kenan-flagler.unc.edu/faculty/bushmanr/bushman_and_landsman_abr_3-2010.pdf

https://www.aasb.gov.au/About-the-AASB/The-standard-setting-process.aspx

https://static.treasury.gov.au/uploads/sites/1/2017/06/AASB_Statement_of_Intent.docx

https://www.iasplus.com/en/resources/ifrs-topics/adoption-of-ifrs

https://www.investopedia.com/terms/i/ifrs.asp

https://capital.nab.com.au/docs/NAB-2017-annual-financial-report.pdf

https://www.commbank.com.au/content/dam/commbank/about-us/shareholders/pdfs/annual-

reports/annual_report_2017_14_aug_2017.pdf

https://shareholder.anz.com/sites/default/files/2017_anz_annual_report.pdf

https://www.westpac.com.au/content/dam/public/wbc/documents/pdf/aw/ic/

2017_Westpac_Annual_Report_Web_ready_&_Bookmarked.pdf

10

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.