Financial Accounting Case Study: Sunshine Ltd Analysis

VerifiedAdded on 2020/05/28

|10

|2863

|70

Case Study

AI Summary

This case study delves into the financial accounting practices of Sunshine Ltd, examining the manipulation of depreciation methods by the General Manager, Kam Sunshine, and the ethical dilemmas faced by the accountant, Maria Mars. The case explores the shift from straight-line to sum-of-years-digits depreciation, its impact on reported profits, and the implications for stakeholders including shareholders, creditors, suppliers, and customers. It analyzes the effects of Australian Accounting Standards Board (AASB) 116 on property, plant, and equipment accounting, highlighting issues of asset realization, carrying amounts, depreciation, and impairment losses. The study also addresses corporate governance failures, lack of transparency, and ethical breaches. The case study provides a detailed analysis of depreciation techniques and their financial implications within the context of the Sunshine Ltd case, offering valuable insights into financial reporting and ethical considerations.

Running head: FINANCIAL ACCOUNTING

Financial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Financial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ACCOUNTING 1

Executive Summary:

Shareholders of Sunshine Ltd is observed to have the accountability for attaining the profitability

related with the investments. Based on such changes inked with their investment profitability.

This has the intention to ensure that the shares are maintained within the organisation. The

major issues linked with property, plant and equipment accounting that results in asset

realization, carrying amounts ascertainment with the depreciation developments with the

impairment losses that is realised accordingly.

Executive Summary:

Shareholders of Sunshine Ltd is observed to have the accountability for attaining the profitability

related with the investments. Based on such changes inked with their investment profitability.

This has the intention to ensure that the shares are maintained within the organisation. The

major issues linked with property, plant and equipment accounting that results in asset

realization, carrying amounts ascertainment with the depreciation developments with the

impairment losses that is realised accordingly.

FINANCIAL ACCOUNTING 2

Table of Contents

1. Introduction..................................................................................................................................3

2. Ethics with Corporate Governance..............................................................................................3

3. Accountant’s Function in Altering Depreciation Methods..........................................................3

4. Stakeholders.................................................................................................................................5

5. Standard AASB 116 Effect..........................................................................................................6

6. Conclusion...................................................................................................................................7

References........................................................................................................................................8

Table of Contents

1. Introduction..................................................................................................................................3

2. Ethics with Corporate Governance..............................................................................................3

3. Accountant’s Function in Altering Depreciation Methods..........................................................3

4. Stakeholders.................................................................................................................................5

5. Standard AASB 116 Effect..........................................................................................................6

6. Conclusion...................................................................................................................................7

References........................................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ACCOUNTING 3

1. Introduction

Sunshine limited Case study has been developed and has considered that the General

Manager named Kam Sunshine is observed to manipulate the accountant of the company named

Maria Mars. The intention was to make sure that there are several developments in the

organization’s discrete incoming profit (Aasb.gov.au. 2017). This has resulted in dilemma for

Maria Mars considering the reason that the accountant has centred on renewal of her contracts

within the organization. Along with remaining aware regarding several actions that remain

unethical, the accountant has changed technique of depreciation from using method of straight

line to outskiing technique of sum-of-years digits. Due to this fact, several stakeholders

encompass the suppliers, partners, communities, government, accountant, general manager,

consumers and creditors. Maria mars has recognised a lot of ethical issues in case of

implementing depreciation techniques which is elucidated I consideration to the needs of the

organization with the impact of accounting standard “AASB 116” (Barth 2015).

2. Ethics with Corporate Governance

It is observed that ethics and governance is greatly focussed on mortality and is not to be

followed by every individual (Bushman 2014). However, ethics is deemed to be greatly effective

as the user’s confidence can get enhanced with sustaining the required quality and work level.

There are several issues related with governance of Sunshine Ltd as elaborated under:

Fault in Transparency and Integrity- Shareholders of Sunshine Ltd is observed to have

the accountability for attaining the profitability related with the investments. Based on

such changes inked with their investment profitability. This has the intention to ensure

that the shares are maintained within the organisation (Dutta and Patatoukas 2016). In

order to meet the requirements of shareholders of the Sunshine Ltd, Kam Sunshine has

elaborated that changing method of depreciation for maintaining a situation of regular

high income. This signifies lack of transparency and integrity from the side of the

company that indicates accurate information is attained by users of financial data.

Infringement of Objectivity- Sunshine Ltd Company’s General Manager is deemed to

manipulate the senior manager of the organization for some personal advantage and

Maria Mars also facilitated the manager in attaining such goal (Hino 2014). The

organization has used numerous process of depreciation for the fixed assets for signifying

effect of devaluation with deprecation process. This signifies a condition in which certain

future advantages associated with asset are observed to take place. The accountant

changed the depreciation technique which took place because with some difference at the

time of total depreciation. This has led to the shareholder’s decisions for getting affected

for certain decisions by some anticipations concerning error (Hoskin, Fizzell and Cherry

2014). Maria Mars was the one to be accountable to signify accounting data in superior

manner and differences within financial statement might be reported. This is observed to

be different accountant’s work ethics which has interrupted vital objectivity principle.

3. Accountant’s Function in Altering Depreciation Methods

As elucidated by the information presented within the Sunshine Ltd case study, the

accountant has conducted an act of changing appropriate depreciation techniques to be utilised

1. Introduction

Sunshine limited Case study has been developed and has considered that the General

Manager named Kam Sunshine is observed to manipulate the accountant of the company named

Maria Mars. The intention was to make sure that there are several developments in the

organization’s discrete incoming profit (Aasb.gov.au. 2017). This has resulted in dilemma for

Maria Mars considering the reason that the accountant has centred on renewal of her contracts

within the organization. Along with remaining aware regarding several actions that remain

unethical, the accountant has changed technique of depreciation from using method of straight

line to outskiing technique of sum-of-years digits. Due to this fact, several stakeholders

encompass the suppliers, partners, communities, government, accountant, general manager,

consumers and creditors. Maria mars has recognised a lot of ethical issues in case of

implementing depreciation techniques which is elucidated I consideration to the needs of the

organization with the impact of accounting standard “AASB 116” (Barth 2015).

2. Ethics with Corporate Governance

It is observed that ethics and governance is greatly focussed on mortality and is not to be

followed by every individual (Bushman 2014). However, ethics is deemed to be greatly effective

as the user’s confidence can get enhanced with sustaining the required quality and work level.

There are several issues related with governance of Sunshine Ltd as elaborated under:

Fault in Transparency and Integrity- Shareholders of Sunshine Ltd is observed to have

the accountability for attaining the profitability related with the investments. Based on

such changes inked with their investment profitability. This has the intention to ensure

that the shares are maintained within the organisation (Dutta and Patatoukas 2016). In

order to meet the requirements of shareholders of the Sunshine Ltd, Kam Sunshine has

elaborated that changing method of depreciation for maintaining a situation of regular

high income. This signifies lack of transparency and integrity from the side of the

company that indicates accurate information is attained by users of financial data.

Infringement of Objectivity- Sunshine Ltd Company’s General Manager is deemed to

manipulate the senior manager of the organization for some personal advantage and

Maria Mars also facilitated the manager in attaining such goal (Hino 2014). The

organization has used numerous process of depreciation for the fixed assets for signifying

effect of devaluation with deprecation process. This signifies a condition in which certain

future advantages associated with asset are observed to take place. The accountant

changed the depreciation technique which took place because with some difference at the

time of total depreciation. This has led to the shareholder’s decisions for getting affected

for certain decisions by some anticipations concerning error (Hoskin, Fizzell and Cherry

2014). Maria Mars was the one to be accountable to signify accounting data in superior

manner and differences within financial statement might be reported. This is observed to

be different accountant’s work ethics which has interrupted vital objectivity principle.

3. Accountant’s Function in Altering Depreciation Methods

As elucidated by the information presented within the Sunshine Ltd case study, the

accountant has conducted an act of changing appropriate depreciation techniques to be utilised

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ACCOUNTING 4

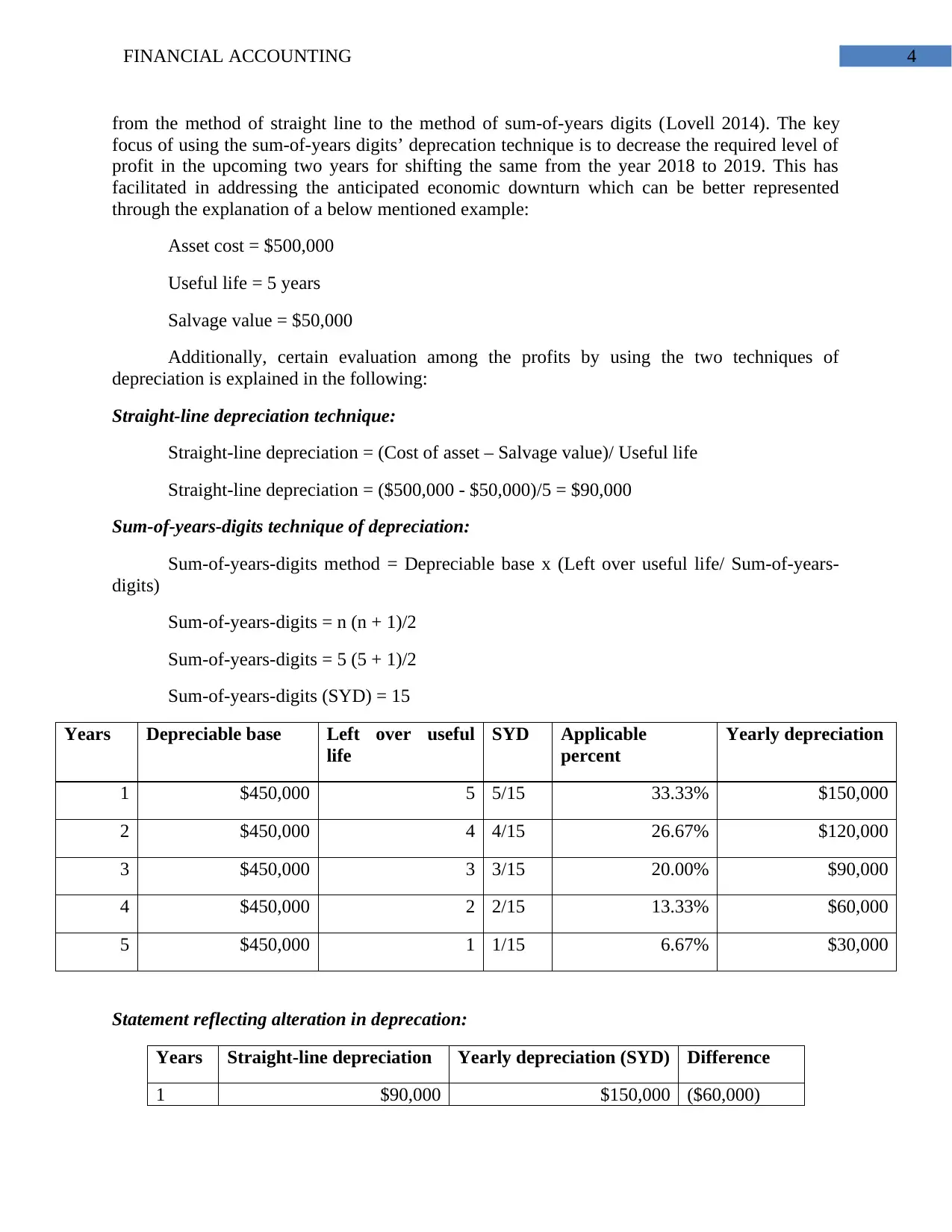

from the method of straight line to the method of sum-of-years digits (Lovell 2014). The key

focus of using the sum-of-years digits’ deprecation technique is to decrease the required level of

profit in the upcoming two years for shifting the same from the year 2018 to 2019. This has

facilitated in addressing the anticipated economic downturn which can be better represented

through the explanation of a below mentioned example:

Asset cost = $500,000

Useful life = 5 years

Salvage value = $50,000

Additionally, certain evaluation among the profits by using the two techniques of

depreciation is explained in the following:

Straight-line depreciation technique:

Straight-line depreciation = (Cost of asset – Salvage value)/ Useful life

Straight-line depreciation = ($500,000 - $50,000)/5 = $90,000

Sum-of-years-digits technique of depreciation:

Sum-of-years-digits method = Depreciable base x (Left over useful life/ Sum-of-years-

digits)

Sum-of-years-digits = n (n + 1)/2

Sum-of-years-digits = 5 (5 + 1)/2

Sum-of-years-digits (SYD) = 15

Years Depreciable base Left over useful

life

SYD Applicable

percent

Yearly depreciation

1 $450,000 5 5/15 33.33% $150,000

2 $450,000 4 4/15 26.67% $120,000

3 $450,000 3 3/15 20.00% $90,000

4 $450,000 2 2/15 13.33% $60,000

5 $450,000 1 1/15 6.67% $30,000

Statement reflecting alteration in deprecation:

Years Straight-line depreciation Yearly depreciation (SYD) Difference

1 $90,000 $150,000 ($60,000)

from the method of straight line to the method of sum-of-years digits (Lovell 2014). The key

focus of using the sum-of-years digits’ deprecation technique is to decrease the required level of

profit in the upcoming two years for shifting the same from the year 2018 to 2019. This has

facilitated in addressing the anticipated economic downturn which can be better represented

through the explanation of a below mentioned example:

Asset cost = $500,000

Useful life = 5 years

Salvage value = $50,000

Additionally, certain evaluation among the profits by using the two techniques of

depreciation is explained in the following:

Straight-line depreciation technique:

Straight-line depreciation = (Cost of asset – Salvage value)/ Useful life

Straight-line depreciation = ($500,000 - $50,000)/5 = $90,000

Sum-of-years-digits technique of depreciation:

Sum-of-years-digits method = Depreciable base x (Left over useful life/ Sum-of-years-

digits)

Sum-of-years-digits = n (n + 1)/2

Sum-of-years-digits = 5 (5 + 1)/2

Sum-of-years-digits (SYD) = 15

Years Depreciable base Left over useful

life

SYD Applicable

percent

Yearly depreciation

1 $450,000 5 5/15 33.33% $150,000

2 $450,000 4 4/15 26.67% $120,000

3 $450,000 3 3/15 20.00% $90,000

4 $450,000 2 2/15 13.33% $60,000

5 $450,000 1 1/15 6.67% $30,000

Statement reflecting alteration in deprecation:

Years Straight-line depreciation Yearly depreciation (SYD) Difference

1 $90,000 $150,000 ($60,000)

FINANCIAL ACCOUNTING 5

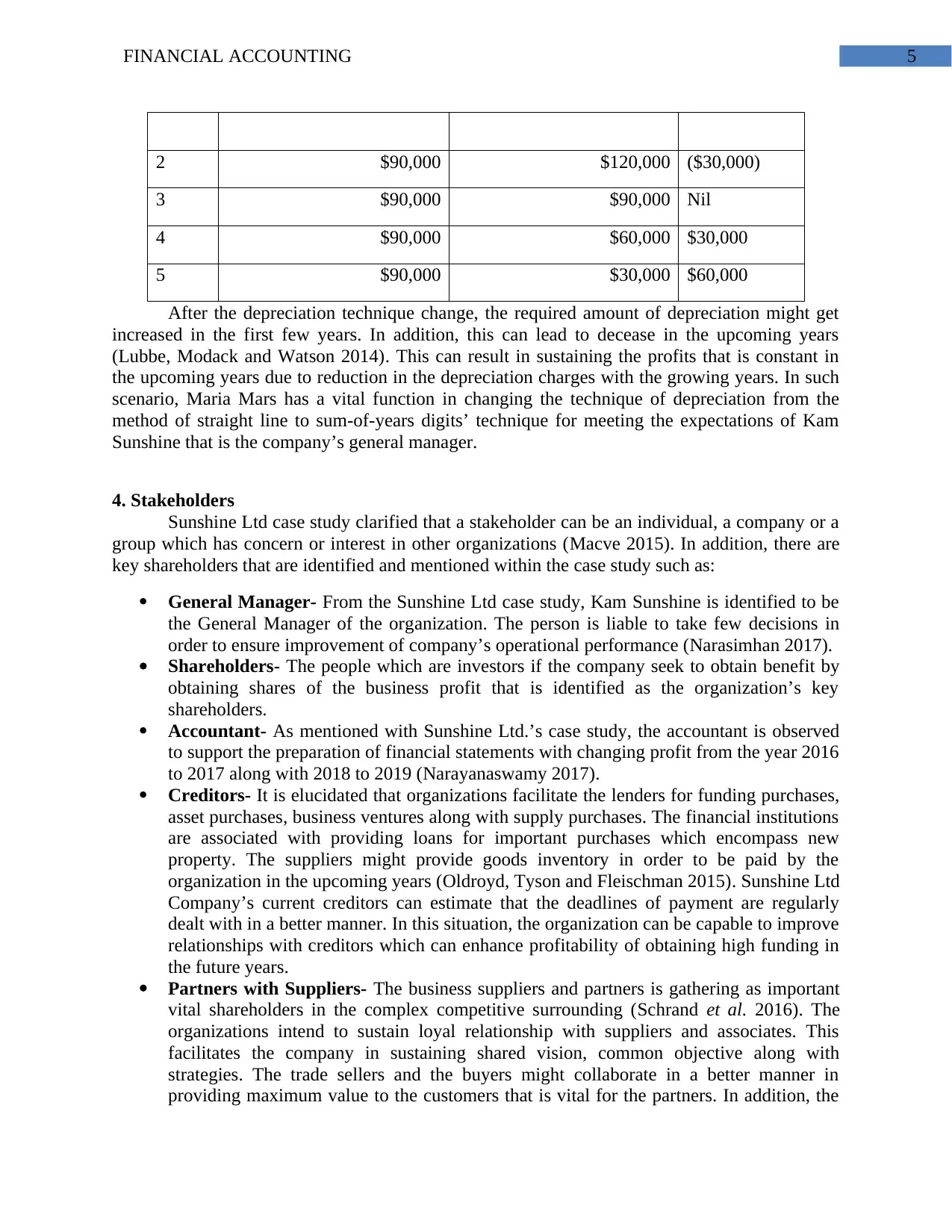

2 $90,000 $120,000 ($30,000)

3 $90,000 $90,000 Nil

4 $90,000 $60,000 $30,000

5 $90,000 $30,000 $60,000

After the depreciation technique change, the required amount of depreciation might get

increased in the first few years. In addition, this can lead to decease in the upcoming years

(Lubbe, Modack and Watson 2014). This can result in sustaining the profits that is constant in

the upcoming years due to reduction in the depreciation charges with the growing years. In such

scenario, Maria Mars has a vital function in changing the technique of depreciation from the

method of straight line to sum-of-years digits’ technique for meeting the expectations of Kam

Sunshine that is the company’s general manager.

4. Stakeholders

Sunshine Ltd case study clarified that a stakeholder can be an individual, a company or a

group which has concern or interest in other organizations (Macve 2015). In addition, there are

key shareholders that are identified and mentioned within the case study such as:

General Manager- From the Sunshine Ltd case study, Kam Sunshine is identified to be

the General Manager of the organization. The person is liable to take few decisions in

order to ensure improvement of company’s operational performance (Narasimhan 2017).

Shareholders- The people which are investors if the company seek to obtain benefit by

obtaining shares of the business profit that is identified as the organization’s key

shareholders.

Accountant- As mentioned with Sunshine Ltd.’s case study, the accountant is observed

to support the preparation of financial statements with changing profit from the year 2016

to 2017 along with 2018 to 2019 (Narayanaswamy 2017).

Creditors- It is elucidated that organizations facilitate the lenders for funding purchases,

asset purchases, business ventures along with supply purchases. The financial institutions

are associated with providing loans for important purchases which encompass new

property. The suppliers might provide goods inventory in order to be paid by the

organization in the upcoming years (Oldroyd, Tyson and Fleischman 2015). Sunshine Ltd

Company’s current creditors can estimate that the deadlines of payment are regularly

dealt with in a better manner. In this situation, the organization can be capable to improve

relationships with creditors which can enhance profitability of obtaining high funding in

the future years.

Partners with Suppliers- The business suppliers and partners is gathering as important

vital shareholders in the complex competitive surrounding (Schrand et al. 2016). The

organizations intend to sustain loyal relationship with suppliers and associates. This

facilitates the company in sustaining shared vision, common objective along with

strategies. The trade sellers and the buyers might collaborate in a better manner in

providing maximum value to the customers that is vital for the partners. In addition, the

2 $90,000 $120,000 ($30,000)

3 $90,000 $90,000 Nil

4 $90,000 $60,000 $30,000

5 $90,000 $30,000 $60,000

After the depreciation technique change, the required amount of depreciation might get

increased in the first few years. In addition, this can lead to decease in the upcoming years

(Lubbe, Modack and Watson 2014). This can result in sustaining the profits that is constant in

the upcoming years due to reduction in the depreciation charges with the growing years. In such

scenario, Maria Mars has a vital function in changing the technique of depreciation from the

method of straight line to sum-of-years digits’ technique for meeting the expectations of Kam

Sunshine that is the company’s general manager.

4. Stakeholders

Sunshine Ltd case study clarified that a stakeholder can be an individual, a company or a

group which has concern or interest in other organizations (Macve 2015). In addition, there are

key shareholders that are identified and mentioned within the case study such as:

General Manager- From the Sunshine Ltd case study, Kam Sunshine is identified to be

the General Manager of the organization. The person is liable to take few decisions in

order to ensure improvement of company’s operational performance (Narasimhan 2017).

Shareholders- The people which are investors if the company seek to obtain benefit by

obtaining shares of the business profit that is identified as the organization’s key

shareholders.

Accountant- As mentioned with Sunshine Ltd.’s case study, the accountant is observed

to support the preparation of financial statements with changing profit from the year 2016

to 2017 along with 2018 to 2019 (Narayanaswamy 2017).

Creditors- It is elucidated that organizations facilitate the lenders for funding purchases,

asset purchases, business ventures along with supply purchases. The financial institutions

are associated with providing loans for important purchases which encompass new

property. The suppliers might provide goods inventory in order to be paid by the

organization in the upcoming years (Oldroyd, Tyson and Fleischman 2015). Sunshine Ltd

Company’s current creditors can estimate that the deadlines of payment are regularly

dealt with in a better manner. In this situation, the organization can be capable to improve

relationships with creditors which can enhance profitability of obtaining high funding in

the future years.

Partners with Suppliers- The business suppliers and partners is gathering as important

vital shareholders in the complex competitive surrounding (Schrand et al. 2016). The

organizations intend to sustain loyal relationship with suppliers and associates. This

facilitates the company in sustaining shared vision, common objective along with

strategies. The trade sellers and the buyers might collaborate in a better manner in

providing maximum value to the customers that is vital for the partners. In addition, the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ACCOUNTING 6

trade partners are estimated to have its business operation in ethical manner for avoiding

consumer reputation hampering associated with the company (Velte and Freidank 2015).

Customers- It is gathered that organizations often employ lenders for fund business

ventures, purchases, asset acquisition and supply purchases. The organization is capable

in improving relationships with creditors that can boost profitability in obtaining funding

in future (Velte and Freidank 2015).

5. Standard AASB 116 Effect

At the end of June 30, 2015, Kam Sunshine is observed to convince the accountant in

realising the way through which profits can be decreased in the upcoming years from the years

over 2016. Go eths reason, this can lead to constant profits over the upcoming years for meeting

the shareholder’s needs (Wild 2015). Maria Mars has changed technique od deprecation from

method of straight line to the method of sum of-digits. In addition, the accountant did not

represent any changes conducted on the company’s financial statements. The Australian

Accounting Standards Board that is AASB 116 I linked with property, equipment and plant with

complied standard that is linked with periods of annual reporting that took place from 1st July,

2009. This standard has an intention to affect the accounting treatment related with plant,

property and equipment for offering vital data to the financial statement users linked with

organizational investment within the assets as well as certain developments in such investment

(Williams 2014). The major issues linked with property, plant and equipment accounting that

results in asset realization, carrying amounts ascertainment with the depreciation developments

with the impairment losses that is realised accordingly.

In the Sunshine Ltd case study, the accountant has changed technique of depreciation

from the straight line to the technique of sum-of-years digits. This theory is related with

technique of depreciation in distinguishing the tangible asset expense over a products useful life

(Lovell 2014). It is deemed that the business is getting linked with fixed or non-current set

deprecation for obtaining tax and accounting tax purposes. Accounting factors is observed to

impose an impact on the organization’s developed net income statement along with tax aspects

that is deemed to impose an impact on the organizations balance sheet statement (Lovell 2014).

However, a fraction of cost is linked with depreciation expense manner at a time where the assets

are considered to be employed. The organizations their financial reporting’s tax expenses as well

as tax aspects. The process of depreciation calculation and the years for which few assets are

depreciated might take into consideration the asset types in identical business and tax purpose

differences (Dutta and Patatoukas 2016). The regulations with accounting standards can explain

the same for it is distinct in several nations. The depreciation expense computation techniques

are numerous for this encompass method of straight line, reduction in balance and methods of

sum-of-years-digits. Taking place of despeciation expense is there at the time of asset use in the

service.

It is realised that the method of sum-of-years digits happens to be an effective technique

for asset depreciation computation (Dutta and Patatoukas 2016). The formula which is used in

depreciation value computation within this technique is elucidated under:

SYD depreciation = Depreciable base x (Left over useful life/ Sum-of-years-digits

method)

trade partners are estimated to have its business operation in ethical manner for avoiding

consumer reputation hampering associated with the company (Velte and Freidank 2015).

Customers- It is gathered that organizations often employ lenders for fund business

ventures, purchases, asset acquisition and supply purchases. The organization is capable

in improving relationships with creditors that can boost profitability in obtaining funding

in future (Velte and Freidank 2015).

5. Standard AASB 116 Effect

At the end of June 30, 2015, Kam Sunshine is observed to convince the accountant in

realising the way through which profits can be decreased in the upcoming years from the years

over 2016. Go eths reason, this can lead to constant profits over the upcoming years for meeting

the shareholder’s needs (Wild 2015). Maria Mars has changed technique od deprecation from

method of straight line to the method of sum of-digits. In addition, the accountant did not

represent any changes conducted on the company’s financial statements. The Australian

Accounting Standards Board that is AASB 116 I linked with property, equipment and plant with

complied standard that is linked with periods of annual reporting that took place from 1st July,

2009. This standard has an intention to affect the accounting treatment related with plant,

property and equipment for offering vital data to the financial statement users linked with

organizational investment within the assets as well as certain developments in such investment

(Williams 2014). The major issues linked with property, plant and equipment accounting that

results in asset realization, carrying amounts ascertainment with the depreciation developments

with the impairment losses that is realised accordingly.

In the Sunshine Ltd case study, the accountant has changed technique of depreciation

from the straight line to the technique of sum-of-years digits. This theory is related with

technique of depreciation in distinguishing the tangible asset expense over a products useful life

(Lovell 2014). It is deemed that the business is getting linked with fixed or non-current set

deprecation for obtaining tax and accounting tax purposes. Accounting factors is observed to

impose an impact on the organization’s developed net income statement along with tax aspects

that is deemed to impose an impact on the organizations balance sheet statement (Lovell 2014).

However, a fraction of cost is linked with depreciation expense manner at a time where the assets

are considered to be employed. The organizations their financial reporting’s tax expenses as well

as tax aspects. The process of depreciation calculation and the years for which few assets are

depreciated might take into consideration the asset types in identical business and tax purpose

differences (Dutta and Patatoukas 2016). The regulations with accounting standards can explain

the same for it is distinct in several nations. The depreciation expense computation techniques

are numerous for this encompass method of straight line, reduction in balance and methods of

sum-of-years-digits. Taking place of despeciation expense is there at the time of asset use in the

service.

It is realised that the method of sum-of-years digits happens to be an effective technique

for asset depreciation computation (Dutta and Patatoukas 2016). The formula which is used in

depreciation value computation within this technique is elucidated under:

SYD depreciation = Depreciable base x (Left over useful life/ Sum-of-years-digits

method)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ACCOUNTING 7

This is an effective method in explaining the process of consumption of a specific asset.

Additionally, this is also used in lack of a specific pattern within a process in which

assets ca be utilised in the upcoming years. The process of straight line deprecation

demands steady cost over the useful life of the non-current assets. This depreciation

process is better in which an assets economic realization can be carried out efficiently

during its useful life (Dutta and Patatoukas 2016).

Depreciation per year = (Cost – Residual value)/ Useful life

The organization mentioned within the case study has aa big departmental store that has a

huge members group that takes decisions focussed on regulations at the time of the

organizations emergence. This is the cause for which the company does not consider its

policy in taking few personal decisions that has direct impact on financial statement of

the organization (Dutta and Patatoukas 2016). Moreover, from Sunshine Ltd case study it

is gathered that aa few developments carried out in the organization has an impact in

taking the ultimate decision that must be represented to all the shareholders of the

organization. This is the major cause for which conducts of the accountant was not in

compliance with AASB 116 accounting standards.

6. Conclusion

As elucidated by the information presented within the Sunshine Ltd case study, the

accountant has conducted an act of changing appropriate depreciation techniques to be utilised

from the method of straight line to the method of sum-of-years digits. It is observed that ethics

and governance is greatly focussed on mortality and is not to be followed by every individual.

However, ethics is deemed to be greatly effective as the user’s confidence can get enhanced with

sustaining the required quality and work level. It is realised that the method of sum-of-years

digits happens to be an effective technique for asset depreciation computation.

This is an effective method in explaining the process of consumption of a specific asset.

Additionally, this is also used in lack of a specific pattern within a process in which

assets ca be utilised in the upcoming years. The process of straight line deprecation

demands steady cost over the useful life of the non-current assets. This depreciation

process is better in which an assets economic realization can be carried out efficiently

during its useful life (Dutta and Patatoukas 2016).

Depreciation per year = (Cost – Residual value)/ Useful life

The organization mentioned within the case study has aa big departmental store that has a

huge members group that takes decisions focussed on regulations at the time of the

organizations emergence. This is the cause for which the company does not consider its

policy in taking few personal decisions that has direct impact on financial statement of

the organization (Dutta and Patatoukas 2016). Moreover, from Sunshine Ltd case study it

is gathered that aa few developments carried out in the organization has an impact in

taking the ultimate decision that must be represented to all the shareholders of the

organization. This is the major cause for which conducts of the accountant was not in

compliance with AASB 116 accounting standards.

6. Conclusion

As elucidated by the information presented within the Sunshine Ltd case study, the

accountant has conducted an act of changing appropriate depreciation techniques to be utilised

from the method of straight line to the method of sum-of-years digits. It is observed that ethics

and governance is greatly focussed on mortality and is not to be followed by every individual.

However, ethics is deemed to be greatly effective as the user’s confidence can get enhanced with

sustaining the required quality and work level. It is realised that the method of sum-of-years

digits happens to be an effective technique for asset depreciation computation.

FINANCIAL ACCOUNTING 8

References

Aasb.gov.au., 2017. [online] Available at:

<http://www.aasb.gov.au/admin/file/content102/c3/AASB116_07-04_ERDRjun10_07-09.pdf>

[Accessed 24 Apr. 2017].

Barth, M.E., 2015. Financial accounting research, practice, and financial

accountability. Abacus, 51(4), pp.499-510.

Bushman, R.M., 2014. Thoughts on financial accounting and the banking industry. Journal of

Accounting and Economics, 58(2), pp.384-395.

Dutta, S. and Patatoukas, P.N., 2016. Identifying Conditional Conservatism in Financial

Accounting Data: Theory and Evidence. The Accounting Review.

Hino, S., 2014. Accounting Methods and Financial Viability for Not-for-profit Organizations.

13(2), pp.27-37.

Hoskin, R.E., Fizzell, M.R. and Cherry, D.C., 2014. Financial Accounting: a user perspective.

Wiley Global Education.

Lovell, H., 2014. Climate change, markets and standards: the case of financial

accounting. Economy and Society, 43(2), pp.260-284.

Lubbe, I., Modack, G. and Watson, A., 2014. Financial Accounting GAAP Principles. OUP

Catalogue.

Macve, R., 2015. A Conceptual Framework for Financial Accounting and Reporting: Vision,

Tool, Or Threat?. Routledge.

Narasimhan, M.S., 2017. Financial Accounting Regulations.

Narayanaswamy, R., 2017. Financial accounting: a managerial perspective. PHI Learning Pvt.

Ltd..

Oldroyd, D., Tyson, T.N. and Fleischman, R.K., 2015. American ideology, socialism and

financial accounting theory: A counter view. Critical Perspectives on Accounting, 27, pp.209-

218.

Schrand, C.M., Armstrong, C.S., Taylor, D.J., Verrecchia, R.E., Wagenhofer, A., Casey, R.J.,

Gao, F., Kirschenheiter, M.T., Li, S., Pandit, S. and Hribar, P., 2016. Journal of Financial

Reporting A Publication of the Financial Accounting and Reporting Section of the American

Accounting Association.

Velte, P. and Freidank, C.C., 2015. The link between in-and external rotation of the auditor and

the quality of financial accounting and external audit. European Journal of Law and

Economics, 40(2), pp.225-246.

Wild, J., 2015. Financial accounting fundamentals. McGraw-Hill Higher Education.

References

Aasb.gov.au., 2017. [online] Available at:

<http://www.aasb.gov.au/admin/file/content102/c3/AASB116_07-04_ERDRjun10_07-09.pdf>

[Accessed 24 Apr. 2017].

Barth, M.E., 2015. Financial accounting research, practice, and financial

accountability. Abacus, 51(4), pp.499-510.

Bushman, R.M., 2014. Thoughts on financial accounting and the banking industry. Journal of

Accounting and Economics, 58(2), pp.384-395.

Dutta, S. and Patatoukas, P.N., 2016. Identifying Conditional Conservatism in Financial

Accounting Data: Theory and Evidence. The Accounting Review.

Hino, S., 2014. Accounting Methods and Financial Viability for Not-for-profit Organizations.

13(2), pp.27-37.

Hoskin, R.E., Fizzell, M.R. and Cherry, D.C., 2014. Financial Accounting: a user perspective.

Wiley Global Education.

Lovell, H., 2014. Climate change, markets and standards: the case of financial

accounting. Economy and Society, 43(2), pp.260-284.

Lubbe, I., Modack, G. and Watson, A., 2014. Financial Accounting GAAP Principles. OUP

Catalogue.

Macve, R., 2015. A Conceptual Framework for Financial Accounting and Reporting: Vision,

Tool, Or Threat?. Routledge.

Narasimhan, M.S., 2017. Financial Accounting Regulations.

Narayanaswamy, R., 2017. Financial accounting: a managerial perspective. PHI Learning Pvt.

Ltd..

Oldroyd, D., Tyson, T.N. and Fleischman, R.K., 2015. American ideology, socialism and

financial accounting theory: A counter view. Critical Perspectives on Accounting, 27, pp.209-

218.

Schrand, C.M., Armstrong, C.S., Taylor, D.J., Verrecchia, R.E., Wagenhofer, A., Casey, R.J.,

Gao, F., Kirschenheiter, M.T., Li, S., Pandit, S. and Hribar, P., 2016. Journal of Financial

Reporting A Publication of the Financial Accounting and Reporting Section of the American

Accounting Association.

Velte, P. and Freidank, C.C., 2015. The link between in-and external rotation of the auditor and

the quality of financial accounting and external audit. European Journal of Law and

Economics, 40(2), pp.225-246.

Wild, J., 2015. Financial accounting fundamentals. McGraw-Hill Higher Education.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ACCOUNTING 9

Williams, J., 2014. Financial accounting. McGraw-Hill Higher Education.

Williams, J., 2014. Financial accounting. McGraw-Hill Higher Education.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.