King's Own Institute ACC701 Financial Accounting Case Study Analysis

VerifiedAdded on 2023/03/17

|9

|2759

|55

Case Study

AI Summary

This case study examines the financial accounting practices of Technology Enterprise Ltd, focusing on the accounting treatment of research and development costs related to an internally developed asset. The analysis centers on the application of AASB 138/IAS 38 for intangible assets, addressing the recognition, measurement, and disclosure requirements for these assets. The study considers the valuation of the project using present value and fair value approaches, the recognition of research costs, and the development phase of the asset. The case further explores the reduction of comparability of financial statements and the importance of adhering to accounting standards for accurate financial reporting. The report details the treatment of various costs incurred, including those related to searching, designing, and training, and their impact on the financial statements. The document also discusses the accounting for internally generated assets versus acquired intangible assets, including the treatment of goodwill. The conclusion provides recommendations for the appropriate accounting of the costs and the required disclosures.

Running head: FINANCIAL ACCOUNTING

Financial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Financial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

FINANCIAL ACCOUNTING

—_ &~ & KING’S OWN INSTITUTE* J) =

Lape ee

INDIVIDUAL ASSIGNMENT COVERSHEET

Family Name: __ Singh Given Name: _Gurwant

Student Number: _11900420 Lecturer’s Name: Andrew chew

Subject Name: _Financial accounting

Assignment Title: Individual case study

Declaration

(This declaration must be completed by the student or the assignment will not be marked.)

| certify the following:

I have read and understood the Student Academic Misconduct Policy e This assignment is my own work based

on my personal study and or research.

I have acknowledged all material and sources used in the preparation of this assignment including any

material generated in the course of my employment.

The assignment has not previously been submitted for assessment.

I have not copied in part or in whole or otherwise plagiarised the work of other students.

I have read and | understand the criteria used for assessment.

The assignment is within the word and page limits specified in the unit outline.

The use of any material in this assignment does not infringe the intellectual property / copyright of a third

party.

I understand that this assignment may undergo electronic detection for plagiarism, and an anonymous copy of

the assignment may be retained on the database and used to make comparisons with other assignments in

future.

By completing this coversheet in full and submitting this assignment electronically, | am bound by the

conditions of the KOI’s Student Academic Misconduct Policy and the declaration on this coversheet.

/_/ Signature Date

Assignment Receipt

Family Name: Given Name:(s)

Student Number: Lecturer’s Name:

Subject Name:

Assignment Title:

FINANCIAL ACCOUNTING

—_ &~ & KING’S OWN INSTITUTE* J) =

Lape ee

INDIVIDUAL ASSIGNMENT COVERSHEET

Family Name: __ Singh Given Name: _Gurwant

Student Number: _11900420 Lecturer’s Name: Andrew chew

Subject Name: _Financial accounting

Assignment Title: Individual case study

Declaration

(This declaration must be completed by the student or the assignment will not be marked.)

| certify the following:

I have read and understood the Student Academic Misconduct Policy e This assignment is my own work based

on my personal study and or research.

I have acknowledged all material and sources used in the preparation of this assignment including any

material generated in the course of my employment.

The assignment has not previously been submitted for assessment.

I have not copied in part or in whole or otherwise plagiarised the work of other students.

I have read and | understand the criteria used for assessment.

The assignment is within the word and page limits specified in the unit outline.

The use of any material in this assignment does not infringe the intellectual property / copyright of a third

party.

I understand that this assignment may undergo electronic detection for plagiarism, and an anonymous copy of

the assignment may be retained on the database and used to make comparisons with other assignments in

future.

By completing this coversheet in full and submitting this assignment electronically, | am bound by the

conditions of the KOI’s Student Academic Misconduct Policy and the declaration on this coversheet.

/_/ Signature Date

Assignment Receipt

Family Name: Given Name:(s)

Student Number: Lecturer’s Name:

Subject Name:

Assignment Title:

2

FINANCIAL ACCOUNTING

Executive Summary

The main purpose of the assessment is to analyse the business of Technology Enterprise ltd

which has undertaken research and development for developing an asset. The discussion below

shows the accounting treatments for the costs which is incurred by the business and the

disclosure which the management of the company is required to shown in the financial

statements of the business. The assessment would go into details regarding different treatments

in case an asset is internally generated or purchased through acquisition.

FINANCIAL ACCOUNTING

Executive Summary

The main purpose of the assessment is to analyse the business of Technology Enterprise ltd

which has undertaken research and development for developing an asset. The discussion below

shows the accounting treatments for the costs which is incurred by the business and the

disclosure which the management of the company is required to shown in the financial

statements of the business. The assessment would go into details regarding different treatments

in case an asset is internally generated or purchased through acquisition.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

FINANCIAL ACCOUNTING

Table of Contents

Introduction...............................................................................................................................4

Accounting for the Project.........................................................................................................4

Reduction of Comparability of Financial Statements...............................................................5

Understanding of AASB 138/IAS 38........................................................................................6

Conclusion and Recommendation.............................................................................................6

Reference...................................................................................................................................8

FINANCIAL ACCOUNTING

Table of Contents

Introduction...............................................................................................................................4

Accounting for the Project.........................................................................................................4

Reduction of Comparability of Financial Statements...............................................................5

Understanding of AASB 138/IAS 38........................................................................................6

Conclusion and Recommendation.............................................................................................6

Reference...................................................................................................................................8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

FINANCIAL ACCOUNTING

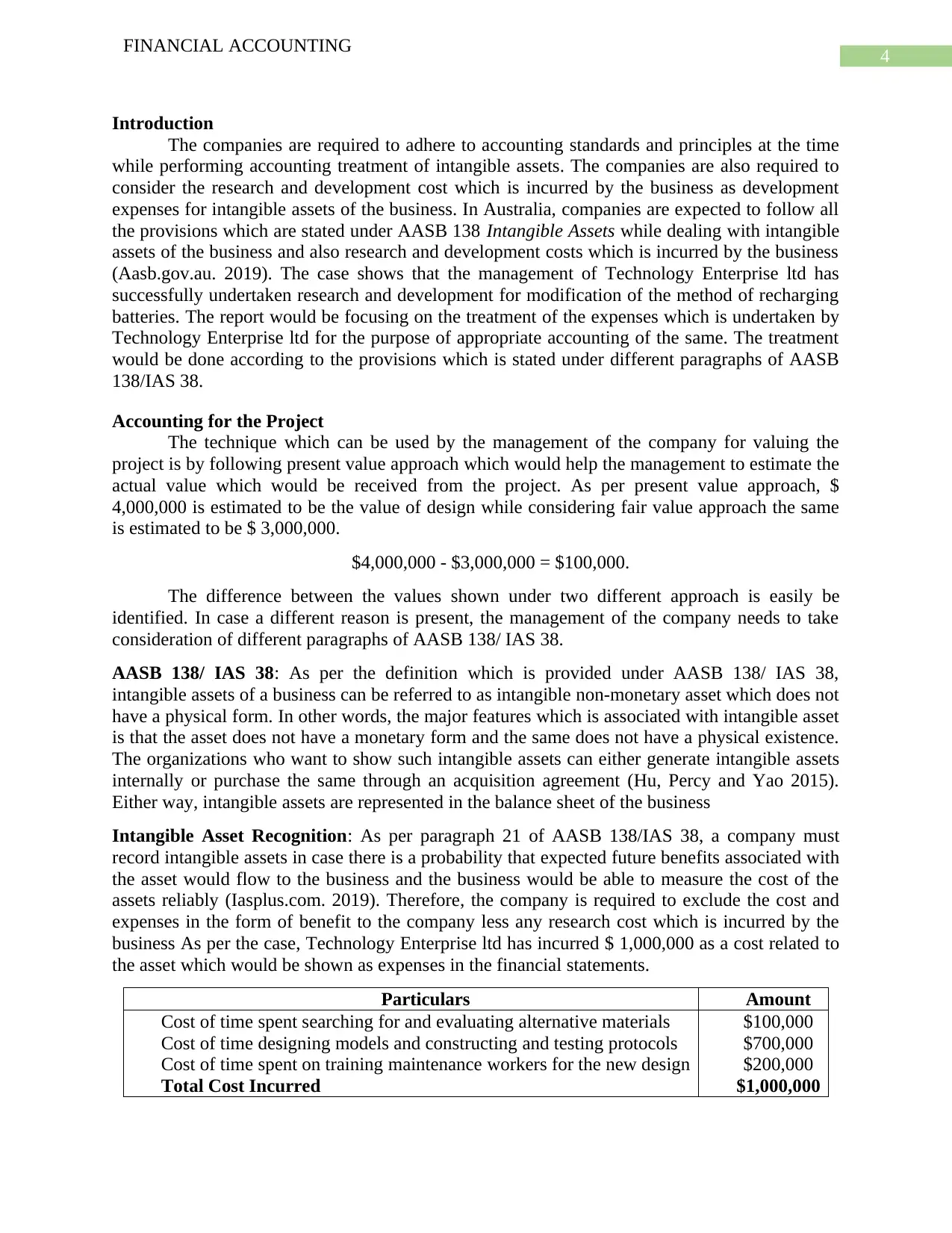

Introduction

The companies are required to adhere to accounting standards and principles at the time

while performing accounting treatment of intangible assets. The companies are also required to

consider the research and development cost which is incurred by the business as development

expenses for intangible assets of the business. In Australia, companies are expected to follow all

the provisions which are stated under AASB 138 Intangible Assets while dealing with intangible

assets of the business and also research and development costs which is incurred by the business

(Aasb.gov.au. 2019). The case shows that the management of Technology Enterprise ltd has

successfully undertaken research and development for modification of the method of recharging

batteries. The report would be focusing on the treatment of the expenses which is undertaken by

Technology Enterprise ltd for the purpose of appropriate accounting of the same. The treatment

would be done according to the provisions which is stated under different paragraphs of AASB

138/IAS 38.

Accounting for the Project

The technique which can be used by the management of the company for valuing the

project is by following present value approach which would help the management to estimate the

actual value which would be received from the project. As per present value approach, $

4,000,000 is estimated to be the value of design while considering fair value approach the same

is estimated to be $ 3,000,000.

$4,000,000 - $3,000,000 = $100,000.

The difference between the values shown under two different approach is easily be

identified. In case a different reason is present, the management of the company needs to take

consideration of different paragraphs of AASB 138/ IAS 38.

AASB 138/ IAS 38: As per the definition which is provided under AASB 138/ IAS 38,

intangible assets of a business can be referred to as intangible non-monetary asset which does not

have a physical form. In other words, the major features which is associated with intangible asset

is that the asset does not have a monetary form and the same does not have a physical existence.

The organizations who want to show such intangible assets can either generate intangible assets

internally or purchase the same through an acquisition agreement (Hu, Percy and Yao 2015).

Either way, intangible assets are represented in the balance sheet of the business

Intangible Asset Recognition: As per paragraph 21 of AASB 138/IAS 38, a company must

record intangible assets in case there is a probability that expected future benefits associated with

the asset would flow to the business and the business would be able to measure the cost of the

assets reliably (Iasplus.com. 2019). Therefore, the company is required to exclude the cost and

expenses in the form of benefit to the company less any research cost which is incurred by the

business As per the case, Technology Enterprise ltd has incurred $ 1,000,000 as a cost related to

the asset which would be shown as expenses in the financial statements.

Particulars Amount

Cost of time spent searching for and evaluating alternative materials

Cost of time designing models and constructing and testing protocols

Cost of time spent on training maintenance workers for the new design

Total Cost Incurred

$100,000

$700,000

$200,000

$1,000,000

FINANCIAL ACCOUNTING

Introduction

The companies are required to adhere to accounting standards and principles at the time

while performing accounting treatment of intangible assets. The companies are also required to

consider the research and development cost which is incurred by the business as development

expenses for intangible assets of the business. In Australia, companies are expected to follow all

the provisions which are stated under AASB 138 Intangible Assets while dealing with intangible

assets of the business and also research and development costs which is incurred by the business

(Aasb.gov.au. 2019). The case shows that the management of Technology Enterprise ltd has

successfully undertaken research and development for modification of the method of recharging

batteries. The report would be focusing on the treatment of the expenses which is undertaken by

Technology Enterprise ltd for the purpose of appropriate accounting of the same. The treatment

would be done according to the provisions which is stated under different paragraphs of AASB

138/IAS 38.

Accounting for the Project

The technique which can be used by the management of the company for valuing the

project is by following present value approach which would help the management to estimate the

actual value which would be received from the project. As per present value approach, $

4,000,000 is estimated to be the value of design while considering fair value approach the same

is estimated to be $ 3,000,000.

$4,000,000 - $3,000,000 = $100,000.

The difference between the values shown under two different approach is easily be

identified. In case a different reason is present, the management of the company needs to take

consideration of different paragraphs of AASB 138/ IAS 38.

AASB 138/ IAS 38: As per the definition which is provided under AASB 138/ IAS 38,

intangible assets of a business can be referred to as intangible non-monetary asset which does not

have a physical form. In other words, the major features which is associated with intangible asset

is that the asset does not have a monetary form and the same does not have a physical existence.

The organizations who want to show such intangible assets can either generate intangible assets

internally or purchase the same through an acquisition agreement (Hu, Percy and Yao 2015).

Either way, intangible assets are represented in the balance sheet of the business

Intangible Asset Recognition: As per paragraph 21 of AASB 138/IAS 38, a company must

record intangible assets in case there is a probability that expected future benefits associated with

the asset would flow to the business and the business would be able to measure the cost of the

assets reliably (Iasplus.com. 2019). Therefore, the company is required to exclude the cost and

expenses in the form of benefit to the company less any research cost which is incurred by the

business As per the case, Technology Enterprise ltd has incurred $ 1,000,000 as a cost related to

the asset which would be shown as expenses in the financial statements.

Particulars Amount

Cost of time spent searching for and evaluating alternative materials

Cost of time designing models and constructing and testing protocols

Cost of time spent on training maintenance workers for the new design

Total Cost Incurred

$100,000

$700,000

$200,000

$1,000,000

5

FINANCIAL ACCOUNTING

Measurement of Intangible Assets: As per para 24 of AASB 138/IAS 38, an intangible asset

should be measured by a business initially at cost. The company therefore needs to report

regarding the internally generated asset at$ 4,000,000 as the same is stated in AASB 138/IAS 38.

The expenses which have been incurred by Technology Enterprise Ltd as a cost or time spend on

research and development would be needed to be taken into account as alternative strategies for

the purpose of analysis. As per the provisions of AASB 138/IAS 38, the research and

development expenses which is incurred by the business would be recognised in the income

statement as sunk cost of the business (Saunders and Brynjolfsson 2016).

An intangible asset can be generated by the management of the company over a certain

period of time. In case however, the business decides to acquire intangible assets by way of

acquisition or business combination than the assets would be different between total value of the

assets acquired and purchased consideration paid by the business. In such a case, the goodwill

value needs to be shown in the consolidated balance sheet of the business (Axtle-Ortiz 2013). As

per the norms of AASB 138/IAS 38, the value of acquisition is that value that the company needs

to consider and the company is needed to review the same on periodical basis in order to get the

indication of impairment (Hu, Percy and Yao, 2015).

Research Costs: As per the provisions of Paragraph 8 AASB 138/IAS 38, companies are

required to engage in planned and organised research for the purpose of gaining technical

knowledge. In the case of Technology Enterprise Ltd, the management of the company has

conducted research for the purpose of increasing the battery life and the same battery would then

be usable for a period of 10 years thus bringing about economic benefit for the business. The

company adhered to the provisions of accounting standard and conducted research for the best as

well as developed an alternative model.

Asset Development: As per the provisions which is stated under AASB 138/IAS 38, an asset is

developed when the research phase of the business is over and the management gets the results

of the research in the form of a developed asset. The provisions provides that the company can

recognise the asset just after technical feasibility of the asset is established after which the

company has the option to either use the asset or sell off the same for appropriate revenue. The

management of the company also needs to record the asset in the balance sheet of the company

and for the same purpose of appropriate accounting standard is to be applied for valuing the

assets after the process of technical feasibility test (Yallwe and Buscemi 2014). The case shows

that the management of Technology Enterprise Ltd has incurred significant amount of funds for

developing the asset. After conducting the technical feasibility test, the business is of the opinion

that the value of the asset is $ 4,000,000.

Reduction of Comparability of Financial Statements

The financial statements should be comparable as the same is considered to be one of the

characteristics of financial statements. The purpose of different accounting standards and

principles is to ensure that comparability is maintained. As per the Australian Accounting

Standards Board (AASB), the applicability of both the processes can be seen are the acquisition

of intangible assets through business combination and goodwill measurement at cost value. It is

further provided in accounting standard that intangible assets can be identified as non-monetary

in nature and the same also does not physical existence. Therefore, it is clear that the valuation of

such kinds of assets is not fixed and the same depends on the benefits which can be derived from

the assets and the same varies from company to company. It is important to value intangible

FINANCIAL ACCOUNTING

Measurement of Intangible Assets: As per para 24 of AASB 138/IAS 38, an intangible asset

should be measured by a business initially at cost. The company therefore needs to report

regarding the internally generated asset at$ 4,000,000 as the same is stated in AASB 138/IAS 38.

The expenses which have been incurred by Technology Enterprise Ltd as a cost or time spend on

research and development would be needed to be taken into account as alternative strategies for

the purpose of analysis. As per the provisions of AASB 138/IAS 38, the research and

development expenses which is incurred by the business would be recognised in the income

statement as sunk cost of the business (Saunders and Brynjolfsson 2016).

An intangible asset can be generated by the management of the company over a certain

period of time. In case however, the business decides to acquire intangible assets by way of

acquisition or business combination than the assets would be different between total value of the

assets acquired and purchased consideration paid by the business. In such a case, the goodwill

value needs to be shown in the consolidated balance sheet of the business (Axtle-Ortiz 2013). As

per the norms of AASB 138/IAS 38, the value of acquisition is that value that the company needs

to consider and the company is needed to review the same on periodical basis in order to get the

indication of impairment (Hu, Percy and Yao, 2015).

Research Costs: As per the provisions of Paragraph 8 AASB 138/IAS 38, companies are

required to engage in planned and organised research for the purpose of gaining technical

knowledge. In the case of Technology Enterprise Ltd, the management of the company has

conducted research for the purpose of increasing the battery life and the same battery would then

be usable for a period of 10 years thus bringing about economic benefit for the business. The

company adhered to the provisions of accounting standard and conducted research for the best as

well as developed an alternative model.

Asset Development: As per the provisions which is stated under AASB 138/IAS 38, an asset is

developed when the research phase of the business is over and the management gets the results

of the research in the form of a developed asset. The provisions provides that the company can

recognise the asset just after technical feasibility of the asset is established after which the

company has the option to either use the asset or sell off the same for appropriate revenue. The

management of the company also needs to record the asset in the balance sheet of the company

and for the same purpose of appropriate accounting standard is to be applied for valuing the

assets after the process of technical feasibility test (Yallwe and Buscemi 2014). The case shows

that the management of Technology Enterprise Ltd has incurred significant amount of funds for

developing the asset. After conducting the technical feasibility test, the business is of the opinion

that the value of the asset is $ 4,000,000.

Reduction of Comparability of Financial Statements

The financial statements should be comparable as the same is considered to be one of the

characteristics of financial statements. The purpose of different accounting standards and

principles is to ensure that comparability is maintained. As per the Australian Accounting

Standards Board (AASB), the applicability of both the processes can be seen are the acquisition

of intangible assets through business combination and goodwill measurement at cost value. It is

further provided in accounting standard that intangible assets can be identified as non-monetary

in nature and the same also does not physical existence. Therefore, it is clear that the valuation of

such kinds of assets is not fixed and the same depends on the benefits which can be derived from

the assets and the same varies from company to company. It is important to value intangible

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

FINANCIAL ACCOUNTING

assets in the financial statements as assets relying on the benefits which is derived from the use

of asset. The company also needs to classify expenses accordingly in the financial statements of

the business.

As per the provisions of AASB 138/IAS 38, the profits which is generated from the assets

needs to be effectively recognised in the financial statements of the business in similar basis in

case the asset is acquired from acquisition (Osinski et al. 2017). The company therefore needs to

stick to the provisions which are stated under AASB 138/IAS 38 for effective recognition of the

assets and also for the purpose of capitalizing the costs which was incurred on research and

development of the asset. There is a presence of comparability features in case of intangible

assets of the business as represented by the company. An aspect of comparability should be such

that it lets the users of the financial statements make comparisons between different timelines or

different companies altogether. The comparison process can be done in case of two companies in

case of valuation, recognition and measurement of intangible assets. The process of comparison

can affect the decision-making process for both the management of the company and also for the

user of the financial statement.

As per the regulation which is stated under AASB 138/IAS 38, the companies need to

follow different rules and regulations for correct accounting treatments for different expenses

and developments. The companies are needed to consider any costs which is associated with the

business relating to research for any product or the development of the same as sunk cost. The

company would require to consider such costs in the income statement of the company rather

than capitalizing the same (Ertug and Castellucci 2015). The companies are also expected to

record expenses in appropriate books of accounts.

Understanding of AASB 138/IAS 38

The accounting standard AASB 138/IAS 38 deals with treatment of intangible assets of the

business along with research and development costs which is incurred by a business. The

standard is considered to be important as it gives direction regarding valuation of intangible

assets of a business and what disclosures needs to be provided in the financial statements to

support the treatments related to intangible assets. The accounting policy of AASB 138/IAS 38

indicates towards the crucial fact that intangible assets are identifiable as well as non-monetary

assets which do not have any physical existence. The standard provides a detailed explanation

regarding the monetary and non-monetary assets if the business. In addition to this, the standard

also provides an explanation the two methods which can be used by the business for the purpose

of generating goodwill which are internally generated and purchased through acquisition of

another company. The value of these kinds of assets on the basis of the assets created reflects

from the regulations of AASB 138/IAS 38. In addition to this, the provision of the standards also

makes it clear that intangible assets of the business initially are required to be measured at cost

and the management the company needs to report internally generated intangible assets at cost

(Saunders and Brynjolfsson 2015). The recognition of the intangible asset is done when it is

certain that benefits associated with intangible assets would flow in and the company can reliably

measure the costs of such assets. One major requirements is that the technical feasibility needs to

be established for the intangible asset before the same can be recorded as asset in the financial

reports.

FINANCIAL ACCOUNTING

assets in the financial statements as assets relying on the benefits which is derived from the use

of asset. The company also needs to classify expenses accordingly in the financial statements of

the business.

As per the provisions of AASB 138/IAS 38, the profits which is generated from the assets

needs to be effectively recognised in the financial statements of the business in similar basis in

case the asset is acquired from acquisition (Osinski et al. 2017). The company therefore needs to

stick to the provisions which are stated under AASB 138/IAS 38 for effective recognition of the

assets and also for the purpose of capitalizing the costs which was incurred on research and

development of the asset. There is a presence of comparability features in case of intangible

assets of the business as represented by the company. An aspect of comparability should be such

that it lets the users of the financial statements make comparisons between different timelines or

different companies altogether. The comparison process can be done in case of two companies in

case of valuation, recognition and measurement of intangible assets. The process of comparison

can affect the decision-making process for both the management of the company and also for the

user of the financial statement.

As per the regulation which is stated under AASB 138/IAS 38, the companies need to

follow different rules and regulations for correct accounting treatments for different expenses

and developments. The companies are needed to consider any costs which is associated with the

business relating to research for any product or the development of the same as sunk cost. The

company would require to consider such costs in the income statement of the company rather

than capitalizing the same (Ertug and Castellucci 2015). The companies are also expected to

record expenses in appropriate books of accounts.

Understanding of AASB 138/IAS 38

The accounting standard AASB 138/IAS 38 deals with treatment of intangible assets of the

business along with research and development costs which is incurred by a business. The

standard is considered to be important as it gives direction regarding valuation of intangible

assets of a business and what disclosures needs to be provided in the financial statements to

support the treatments related to intangible assets. The accounting policy of AASB 138/IAS 38

indicates towards the crucial fact that intangible assets are identifiable as well as non-monetary

assets which do not have any physical existence. The standard provides a detailed explanation

regarding the monetary and non-monetary assets if the business. In addition to this, the standard

also provides an explanation the two methods which can be used by the business for the purpose

of generating goodwill which are internally generated and purchased through acquisition of

another company. The value of these kinds of assets on the basis of the assets created reflects

from the regulations of AASB 138/IAS 38. In addition to this, the provision of the standards also

makes it clear that intangible assets of the business initially are required to be measured at cost

and the management the company needs to report internally generated intangible assets at cost

(Saunders and Brynjolfsson 2015). The recognition of the intangible asset is done when it is

certain that benefits associated with intangible assets would flow in and the company can reliably

measure the costs of such assets. One major requirements is that the technical feasibility needs to

be established for the intangible asset before the same can be recorded as asset in the financial

reports.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

FINANCIAL ACCOUNTING

Conclusion and Recommendation

The company which are engaged in preparation of the financial statements are required to

formulate the financial reports following proper accounting standards as per standards of

financial reporting, accounting policies and financial reporting regulations. The management of

Technology Enterprise ltd can addresses the concerns of the shareholders of the business by

providing appropriate disclosures in the financial reports of the business relating to treatments or

valuation of assets. The management of Technology Enterprise Ltd needs to assess the financial

viability of the assets before reporting the same in the annual reports of the business. The

company needs to strengthen certain rules and regulations regarding disclosures which are to be

provided in the annual report of the business. These financial disclosures regarding the assets

play vital role in the interpretation of the financial information regarding the assets and

liabilities.

FINANCIAL ACCOUNTING

Conclusion and Recommendation

The company which are engaged in preparation of the financial statements are required to

formulate the financial reports following proper accounting standards as per standards of

financial reporting, accounting policies and financial reporting regulations. The management of

Technology Enterprise ltd can addresses the concerns of the shareholders of the business by

providing appropriate disclosures in the financial reports of the business relating to treatments or

valuation of assets. The management of Technology Enterprise Ltd needs to assess the financial

viability of the assets before reporting the same in the annual reports of the business. The

company needs to strengthen certain rules and regulations regarding disclosures which are to be

provided in the annual report of the business. These financial disclosures regarding the assets

play vital role in the interpretation of the financial information regarding the assets and

liabilities.

8

FINANCIAL ACCOUNTING

Reference

Aasb.gov.au. 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB138_08-15_COMPoct15_01-18.pdf

[Accessed 7 May 2019].

Axtle-Ortiz, M.A., 2013. Perceiving the value of intangible assets in context. Journal of

Business Research, 66(3), pp.417-424.

Ertug, G. and Castellucci, F., 2015. Who shall get more? How intangible assets and aspiration

levels affect the valuation of resource providers. Strategic Organization, 13(1), pp.6-31.

Hu, F., Percy, M. and Yao, D., 2015. Asset revaluations and earnings management: Evidence

from Australian companies. Corporate Ownership and Control, 13(1), pp.930-939.

Iasplus.com. 2019. IAS 38 — Intangible Assets. [online] Available at: https://www.iasplus

Osinski, M., Selig, P.M., Matos, F. and Roman, D.J., 2017. Methods of evaluation of intangible

assets and intellectual capital. Journal of Intellectual Capital, 18(3), pp.470-485.

Saunders, A. and Brynjolfsson, E., 2015. Valuing IT-related intangible assets. MIS Quarterly,

Forthcoming.

Saunders, A. and Brynjolfsson, E., 2016. Valuing Information Technology Related Intangible

Assets. Mis Quarterly, 40(1).

Yallwe, A.H. and Buscemi, A., 2014. An era of intangible assets. Journal of Applied Finance

and Banking, 4(5), p.17.

FINANCIAL ACCOUNTING

Reference

Aasb.gov.au. 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB138_08-15_COMPoct15_01-18.pdf

[Accessed 7 May 2019].

Axtle-Ortiz, M.A., 2013. Perceiving the value of intangible assets in context. Journal of

Business Research, 66(3), pp.417-424.

Ertug, G. and Castellucci, F., 2015. Who shall get more? How intangible assets and aspiration

levels affect the valuation of resource providers. Strategic Organization, 13(1), pp.6-31.

Hu, F., Percy, M. and Yao, D., 2015. Asset revaluations and earnings management: Evidence

from Australian companies. Corporate Ownership and Control, 13(1), pp.930-939.

Iasplus.com. 2019. IAS 38 — Intangible Assets. [online] Available at: https://www.iasplus

Osinski, M., Selig, P.M., Matos, F. and Roman, D.J., 2017. Methods of evaluation of intangible

assets and intellectual capital. Journal of Intellectual Capital, 18(3), pp.470-485.

Saunders, A. and Brynjolfsson, E., 2015. Valuing IT-related intangible assets. MIS Quarterly,

Forthcoming.

Saunders, A. and Brynjolfsson, E., 2016. Valuing Information Technology Related Intangible

Assets. Mis Quarterly, 40(1).

Yallwe, A.H. and Buscemi, A., 2014. An era of intangible assets. Journal of Applied Finance

and Banking, 4(5), p.17.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.