Case Study: Financial Accounting Theory and Practice (ACCT6007)

VerifiedAdded on 2022/09/14

|11

|1394

|16

Case Study

AI Summary

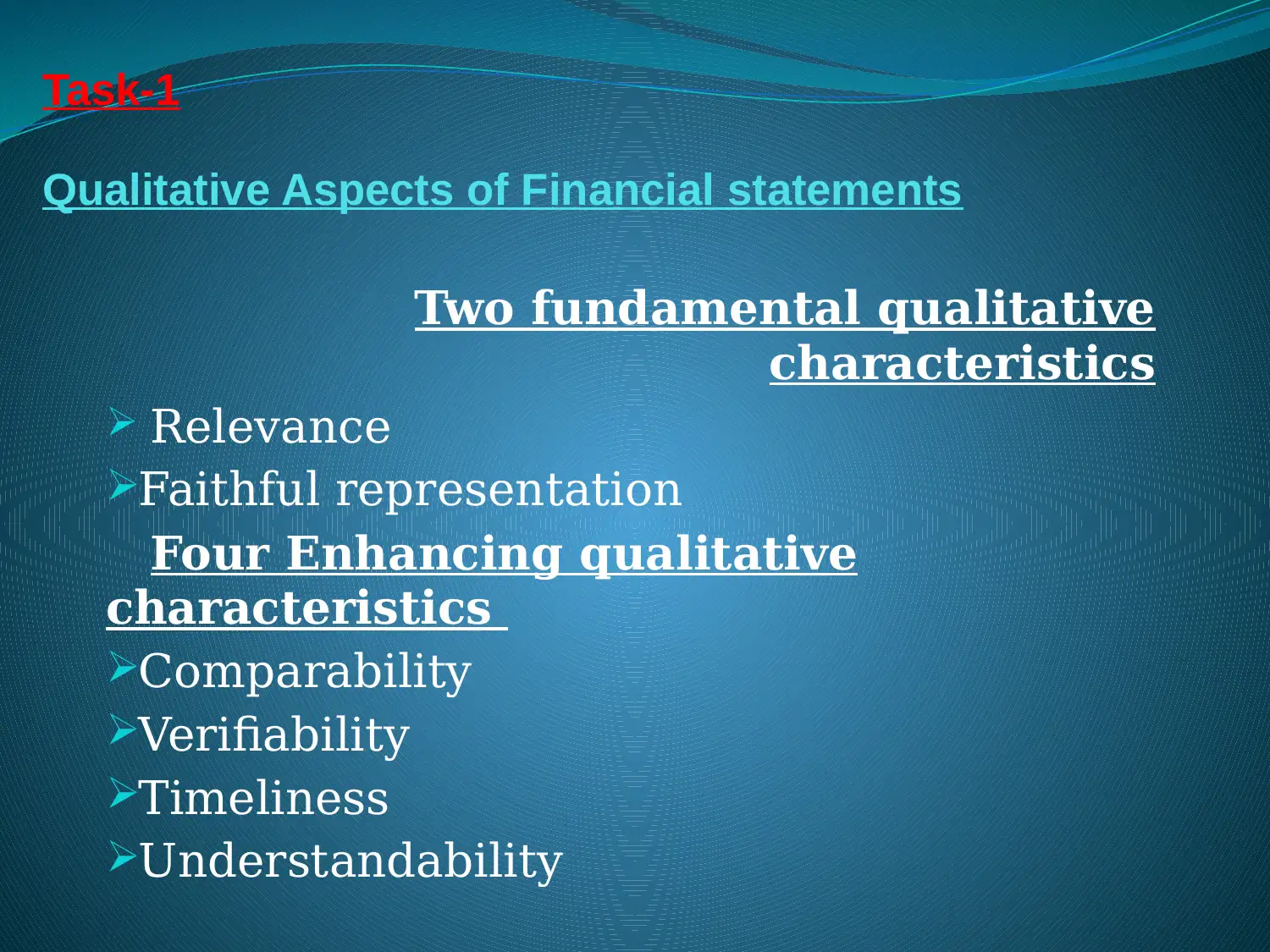

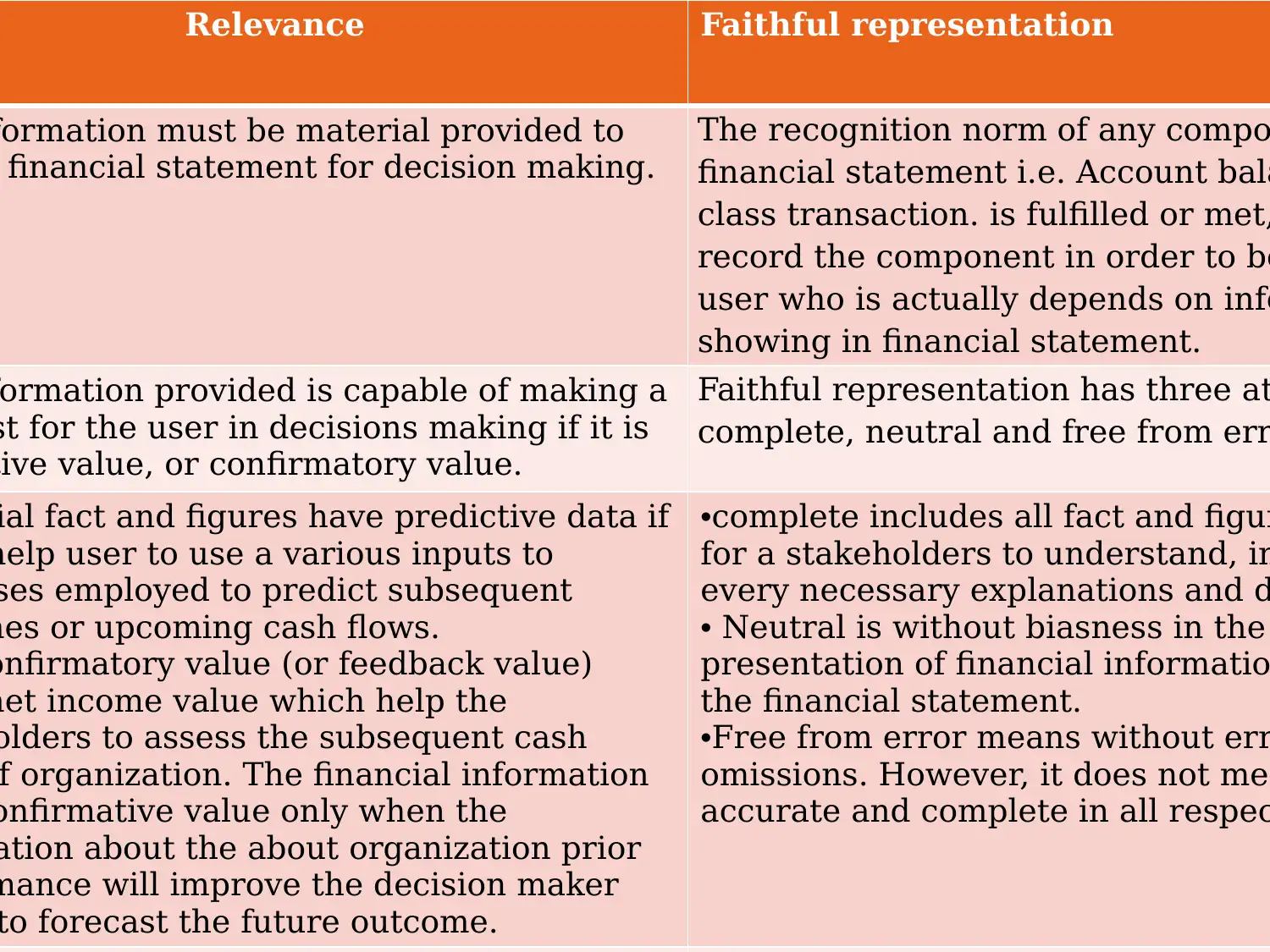

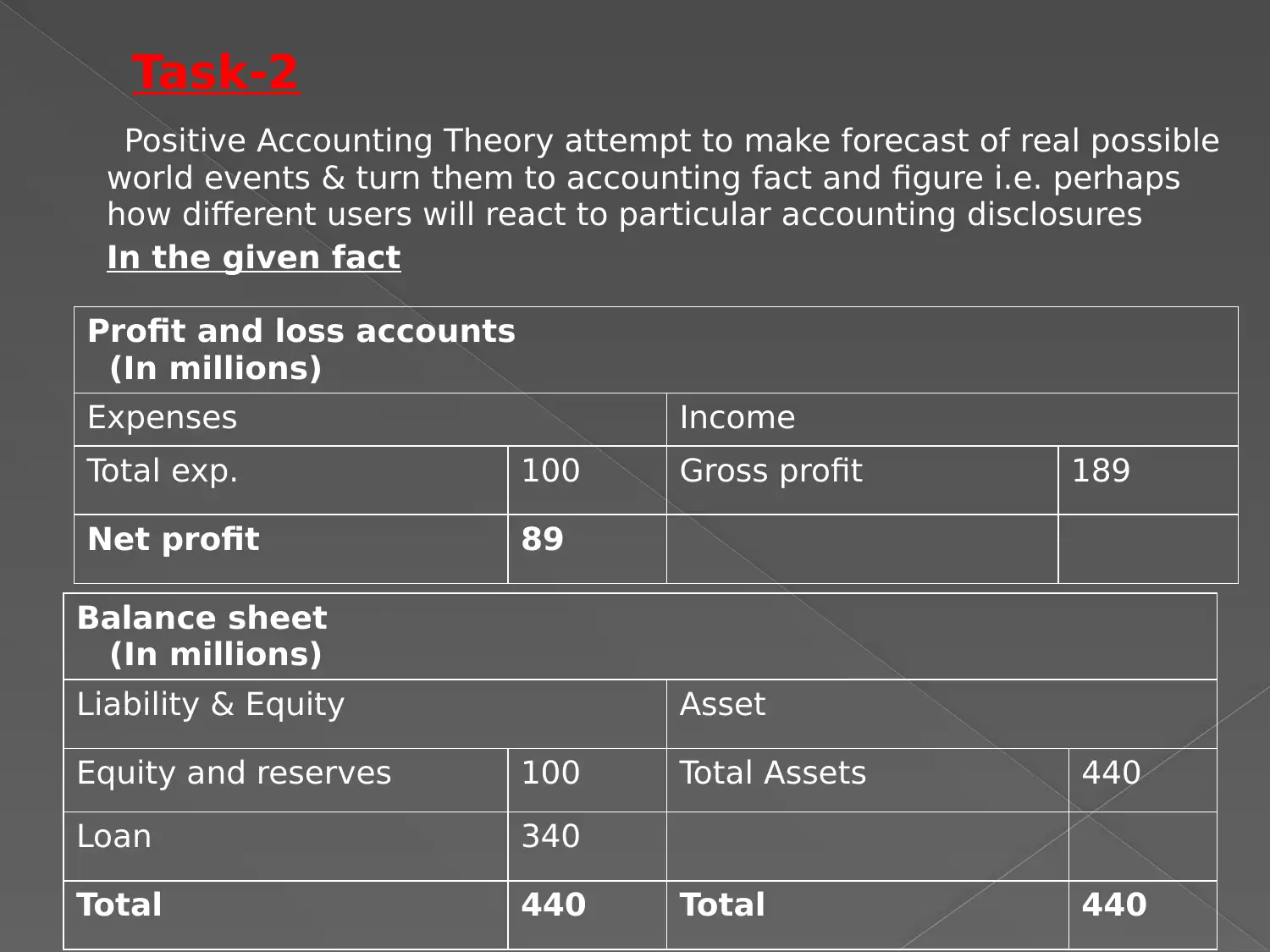

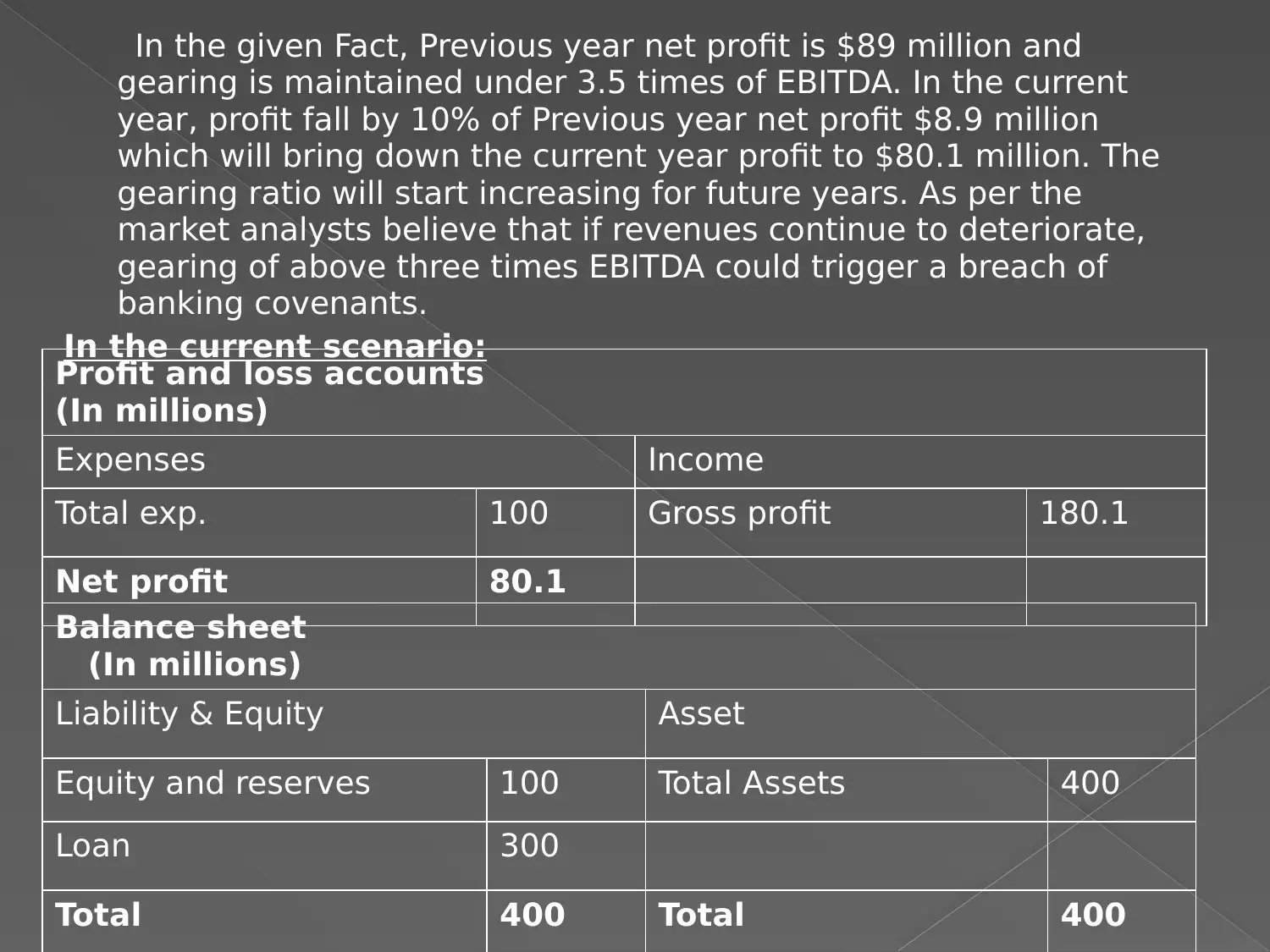

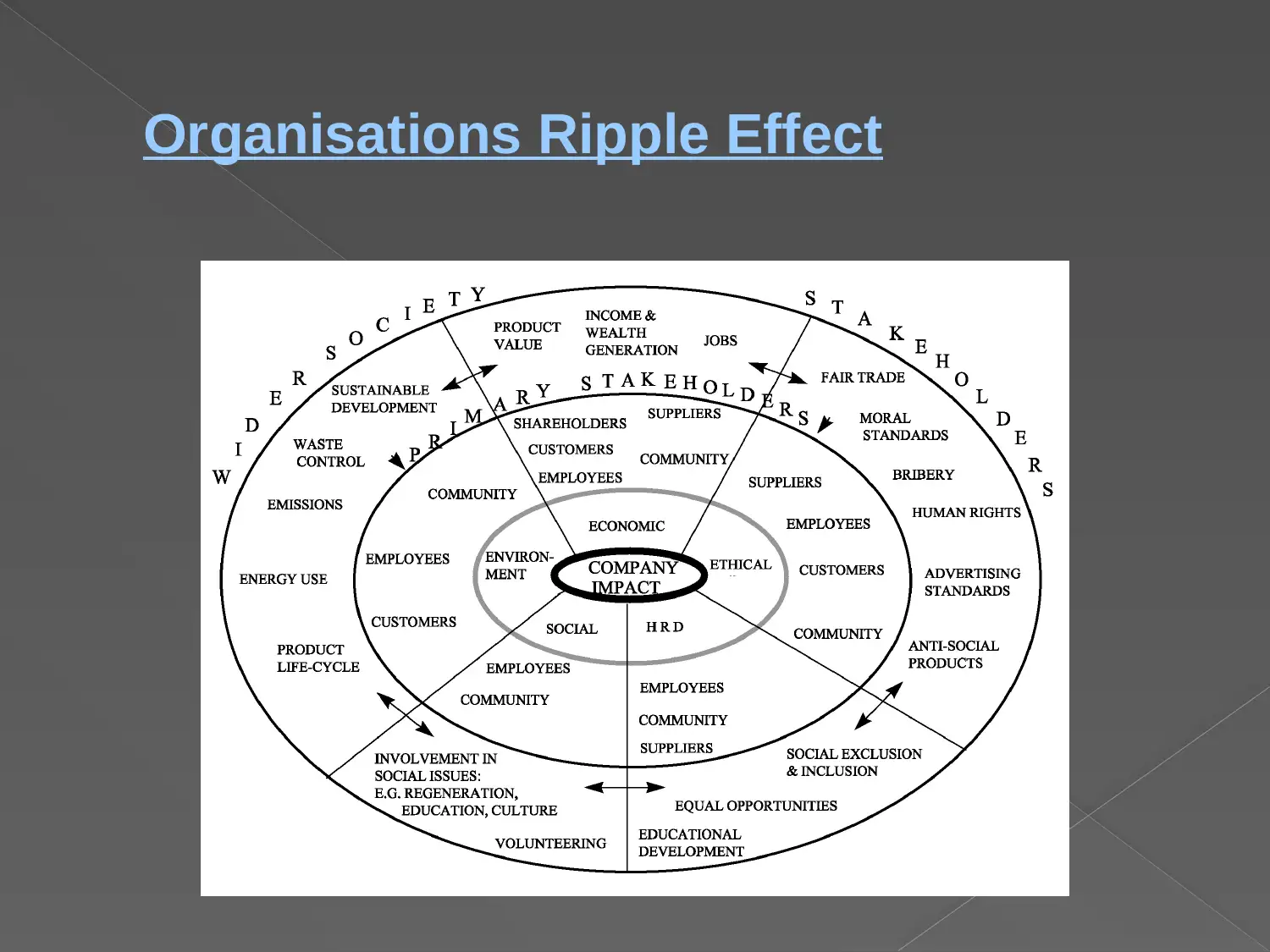

This case study, designed for ACCT6007 Financial Accounting Theory and Practice, delves into three key tasks. Task 1 examines the qualitative aspects of financial statements, including relevance, faithful representation, and enhancing characteristics, emphasizing their importance in depicting a company's financial position and the need for trade-offs in certain situations. Task 2 explores Positive Accounting Theory, analyzing how it can be applied to predict user reactions to accounting disclosures, using a scenario involving a company's declining profit and increasing gearing ratio. It also discusses the Australian government's stance on CSR, the role of market forces, and the importance of environmental disclosures, referencing a controversial coal mine project. Task 3 addresses the capture theory, where regulatory agencies favor the industry they regulate over public interest, analyzing the ripple effects of corporate social and environmental responsibilities and referencing the Australian bushfires and Amazon rainforest.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.