ACCT6003 Financial Accounting Processes: ChiHerbal Ltd Report

VerifiedAdded on 2023/06/10

|16

|2852

|181

Report

AI Summary

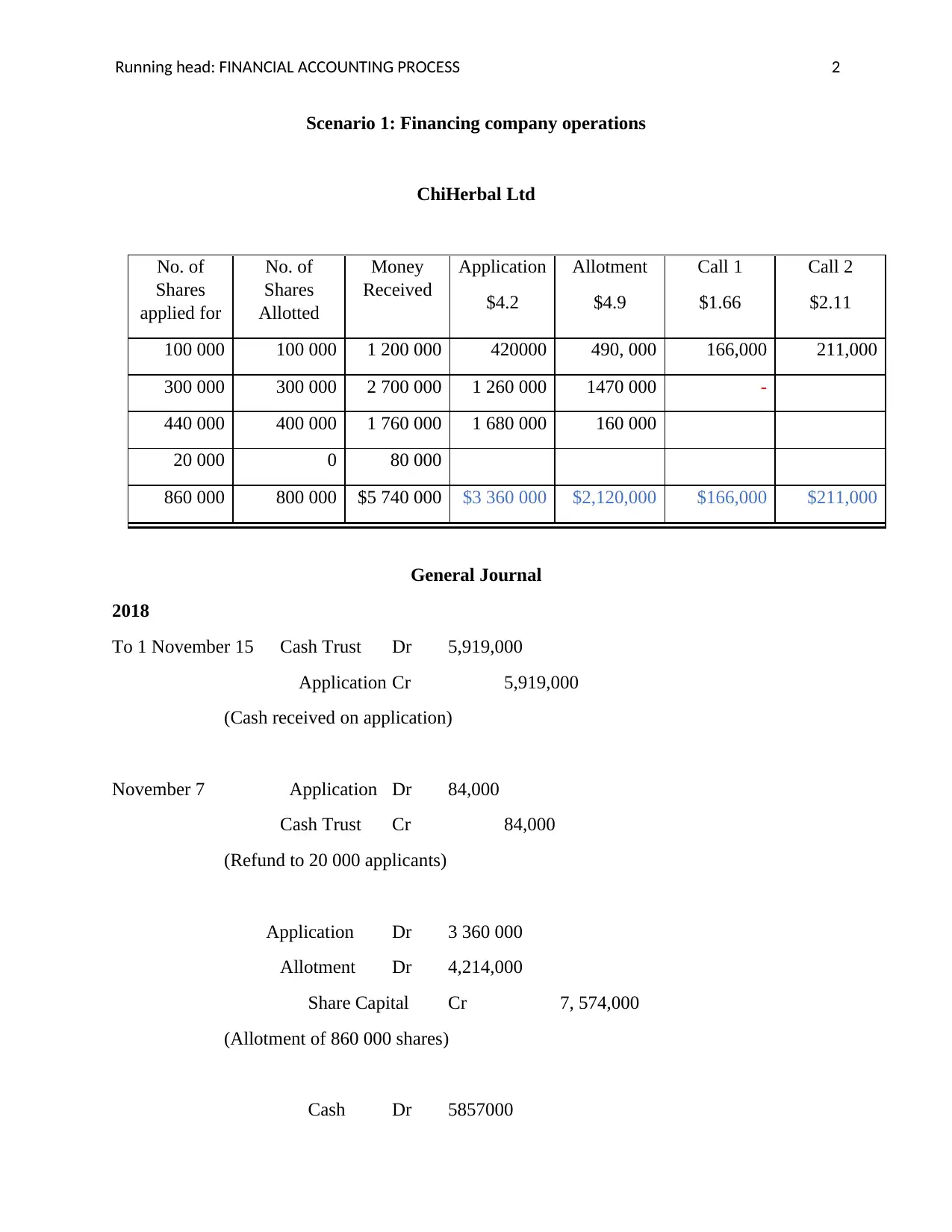

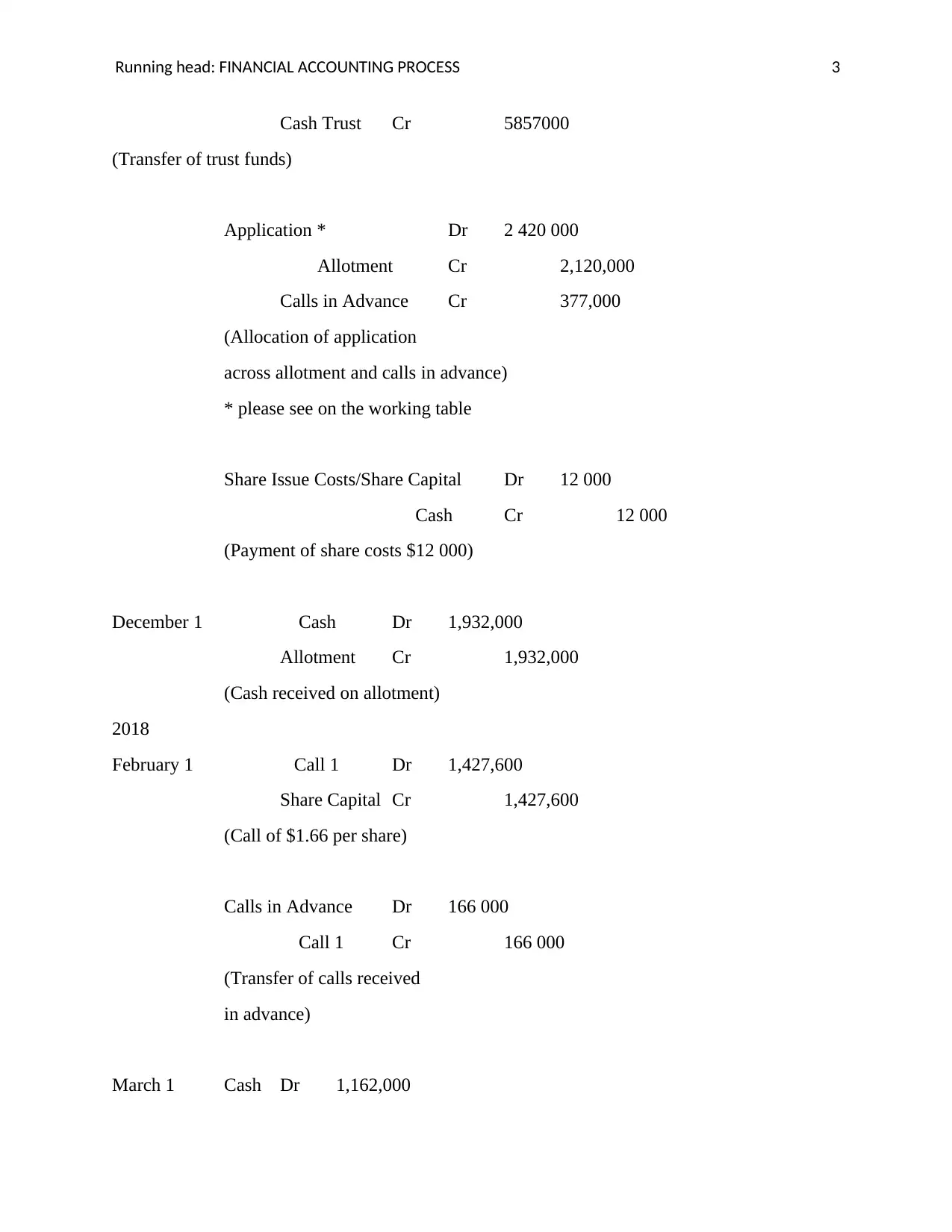

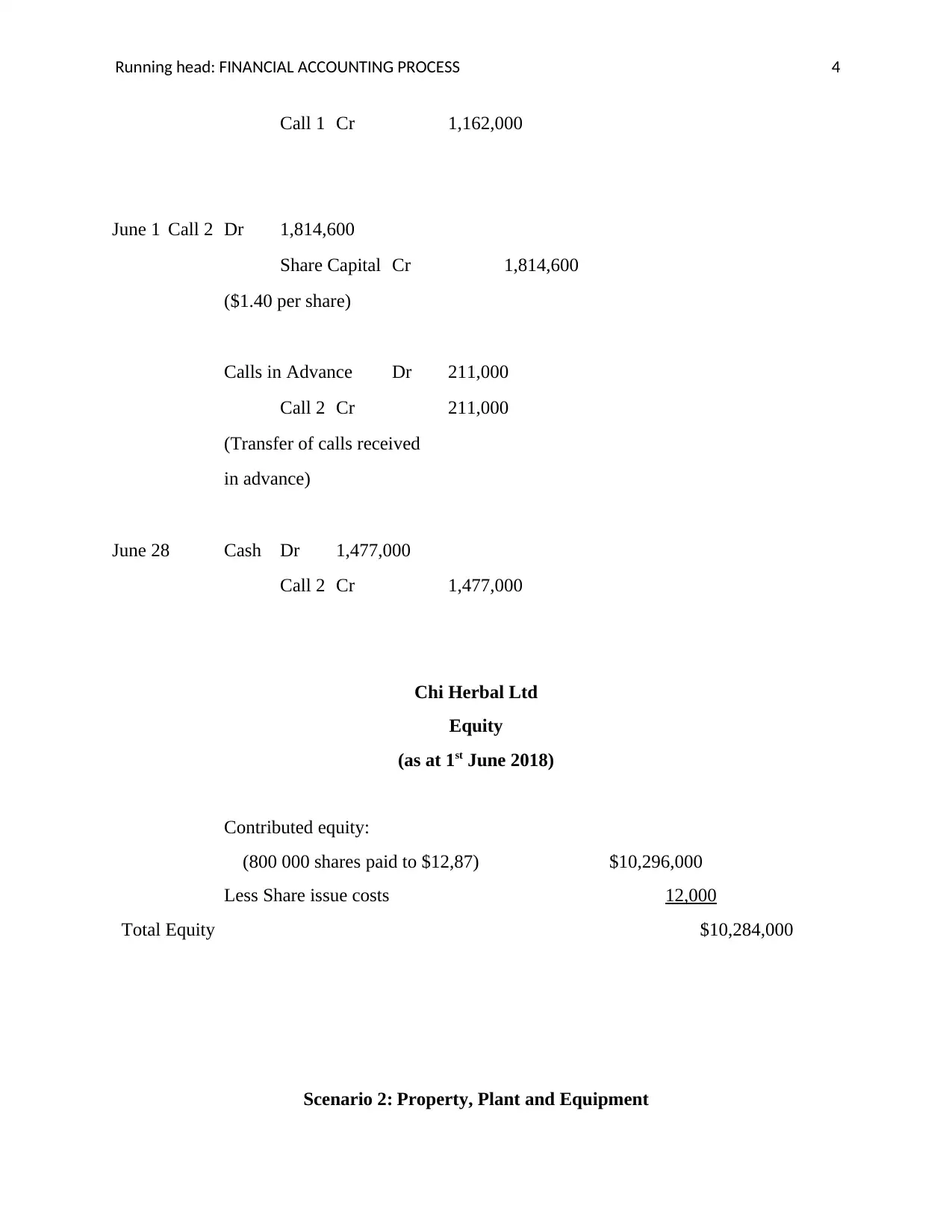

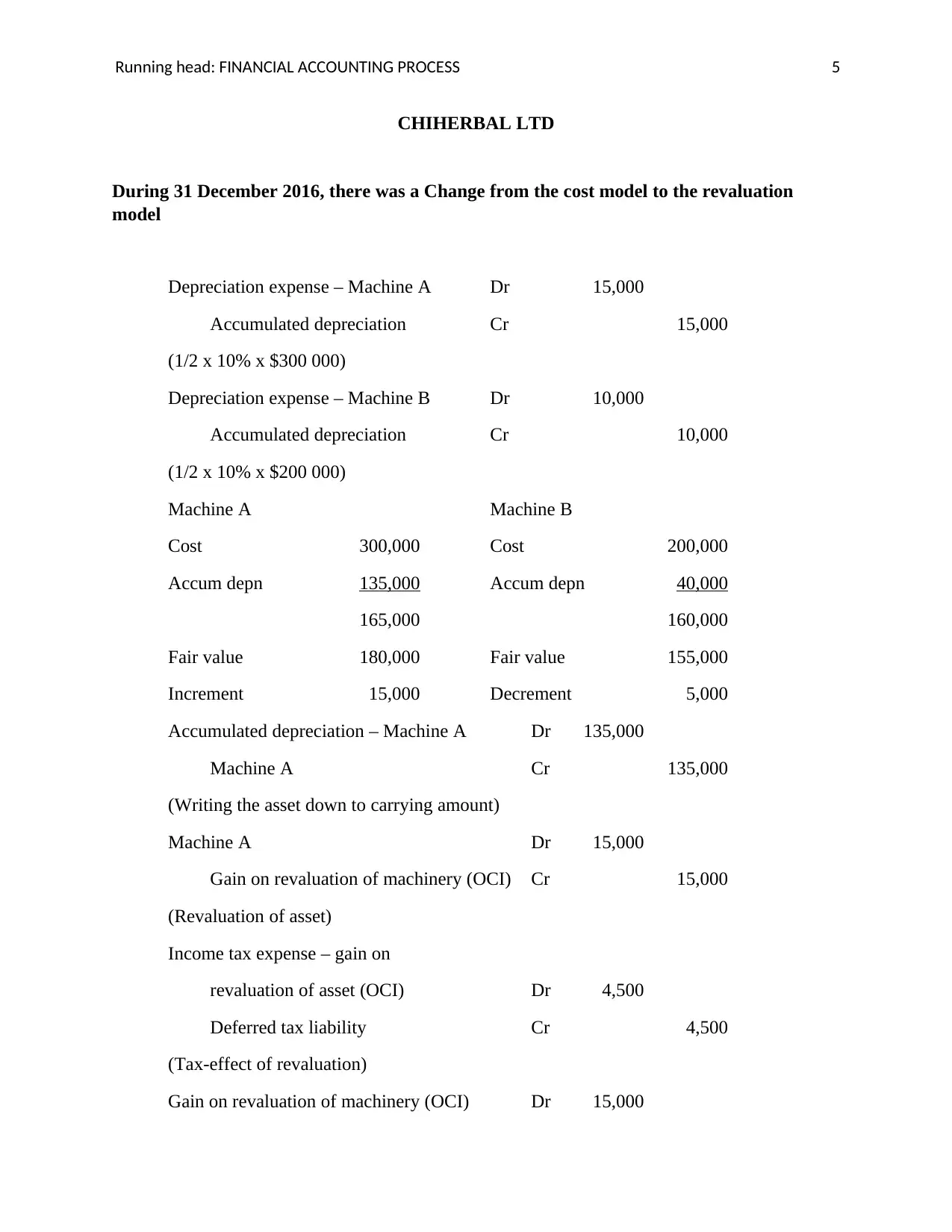

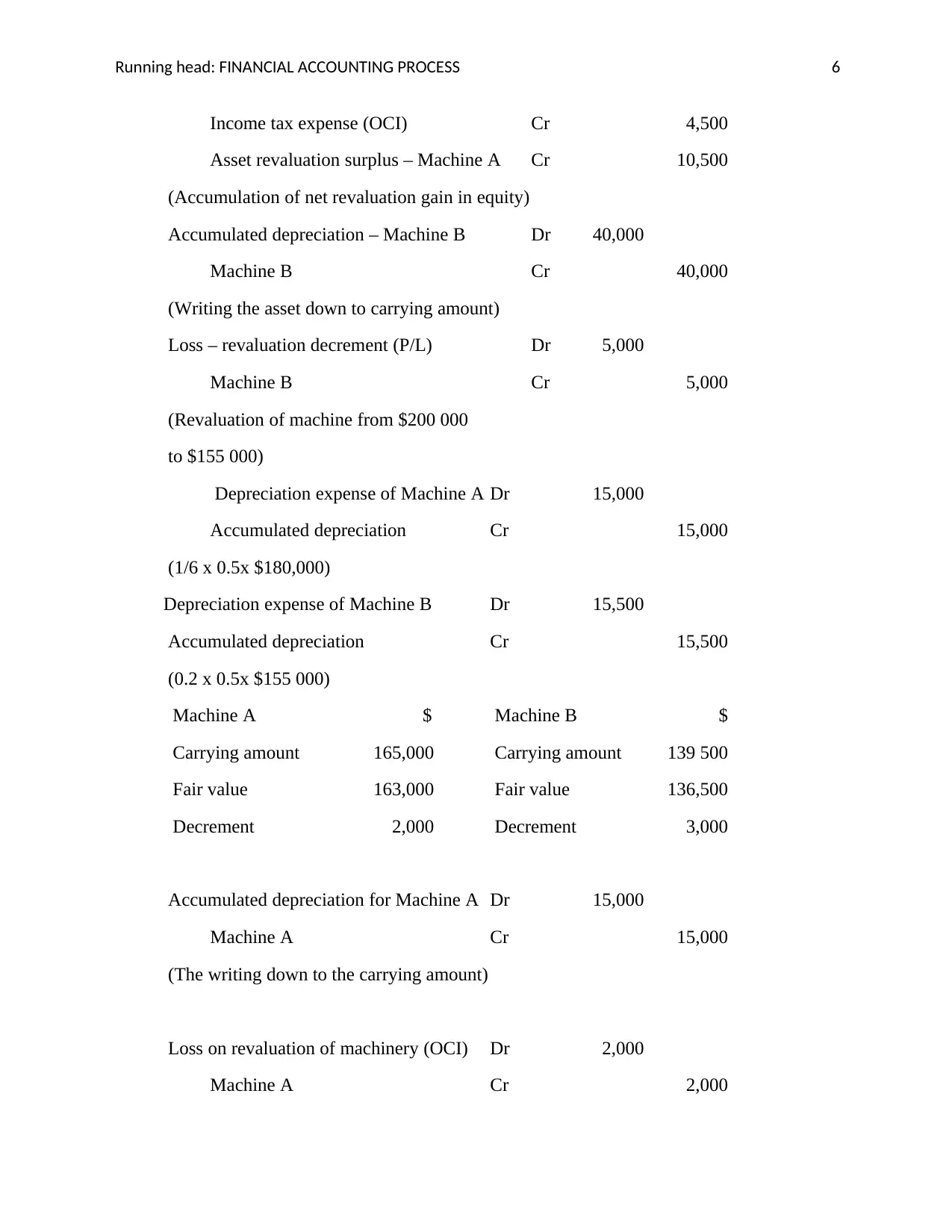

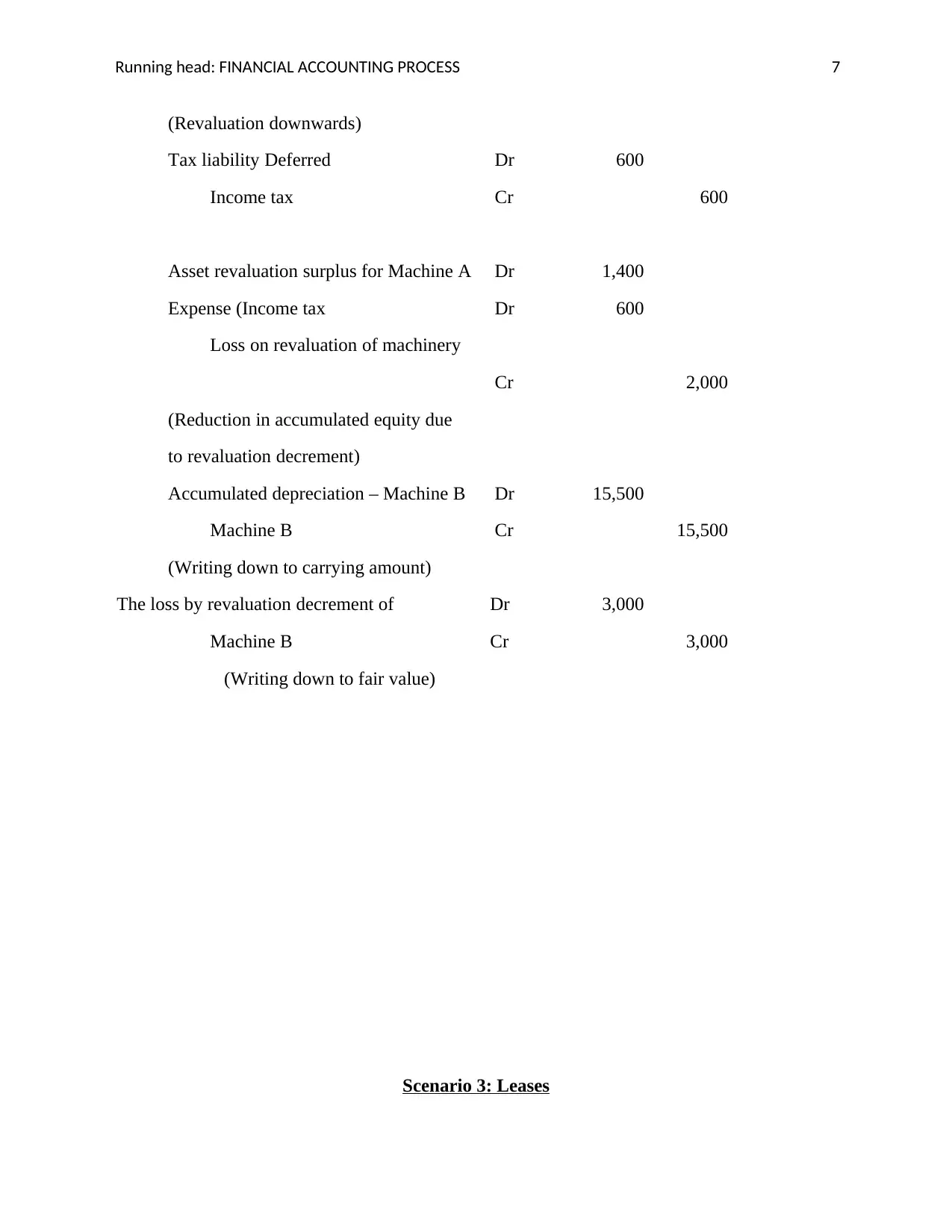

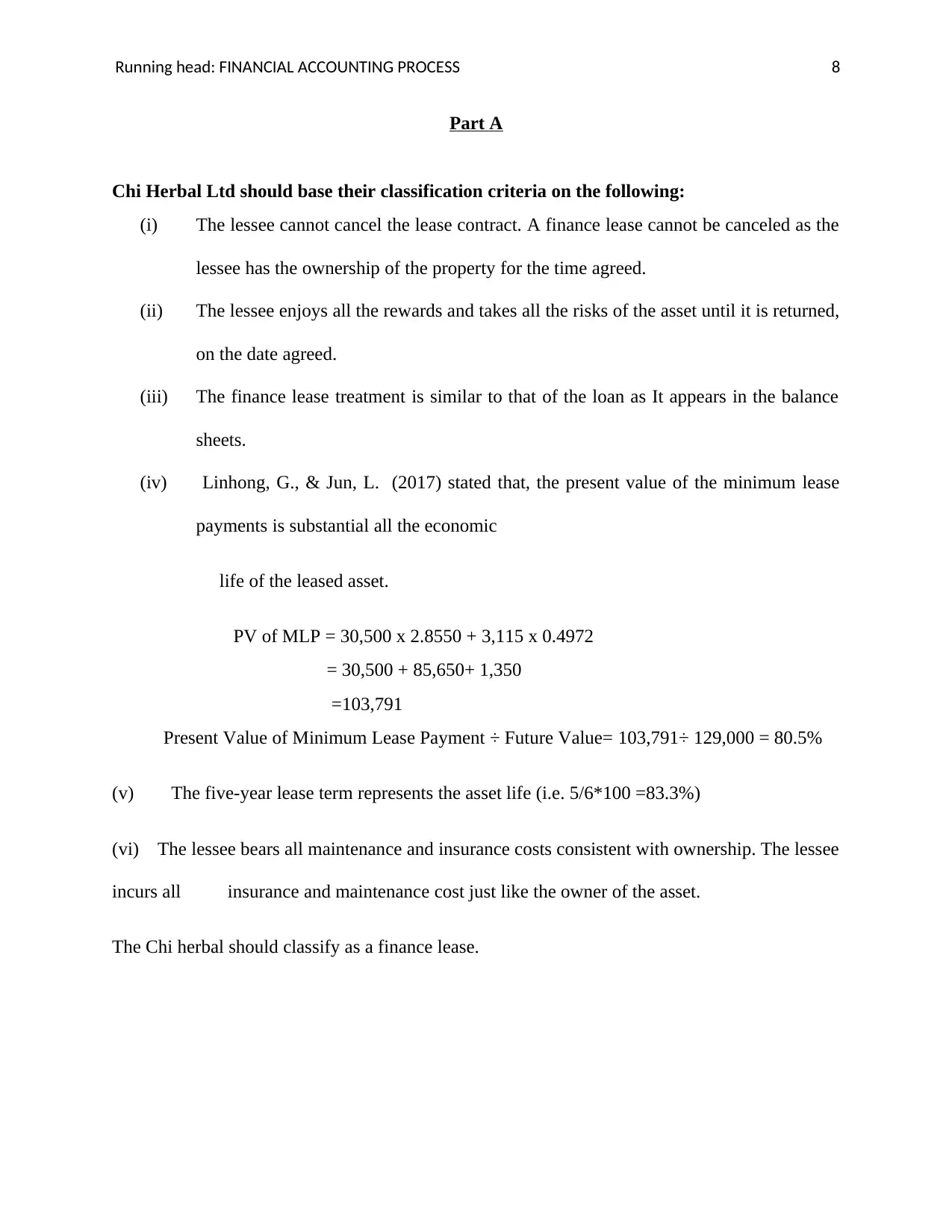

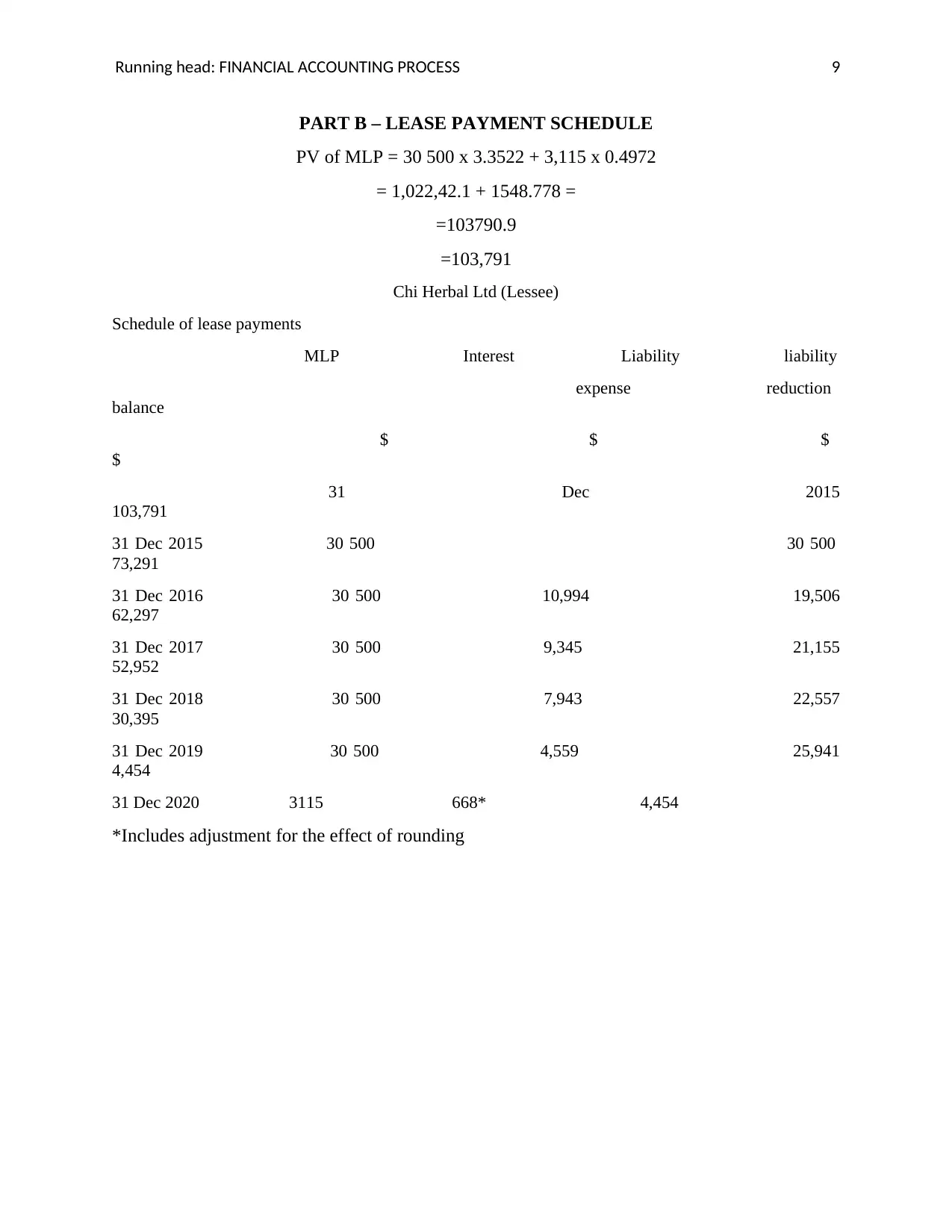

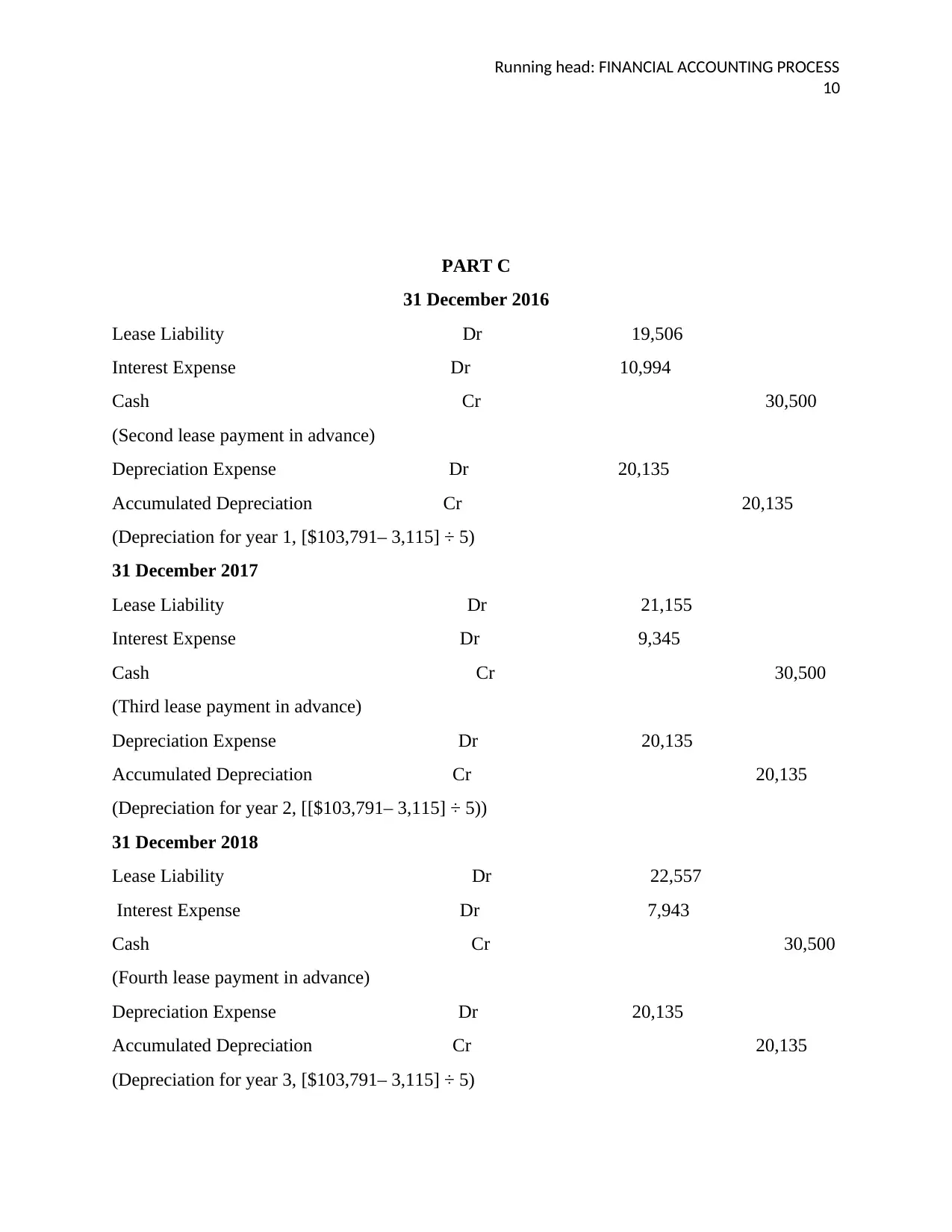

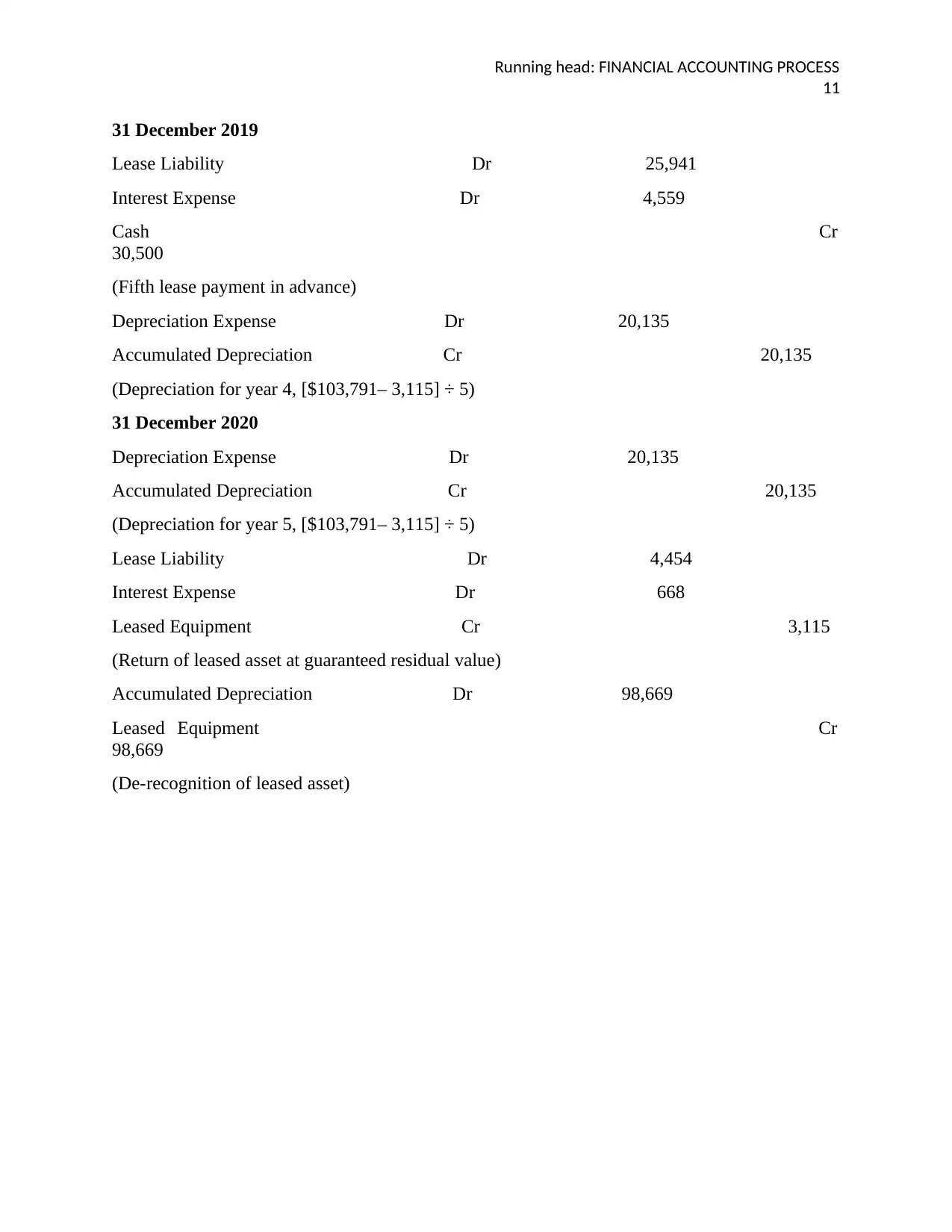

This report provides a comprehensive analysis of ChiHerbal Ltd's financial accounting processes across several scenarios. The first scenario examines the financing of company operations through share issuance, detailing the application, allotment, and call processes, including journal entries for cash received, refunds, share issuance costs, and calls in advance. The second scenario focuses on property, plant, and equipment, specifically addressing the change from the cost model to the revaluation model for Machine A and Machine B, including journal entries for depreciation, revaluation gains/losses, and deferred tax implications. The third scenario delves into lease accounting, classifying a lease as a finance lease based on several criteria, presenting a lease payment schedule, and providing journal entries for lease payments, depreciation, and the return of the leased asset. The final scenario discusses intangible assets, emphasizing the guidelines of AASB 138 regarding technical feasibility, intention to complete and sell, and the classification and measurement of intangible assets, particularly concerning a filter system project, its modification, and patenting process.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.