Comprehensive Financial Accounting Report: Concepts and Application

VerifiedAdded on 2021/02/20

|28

|5695

|38

Report

AI Summary

This report delves into the core concepts of financial accounting, examining its definition, purpose, and application within the context of Fathom Financial Consulting. It elucidates the process of recording and summarizing financial transactions to produce financial statements, including the profit and loss account, balance sheet, and cash flow statement. The report also explores the roles of internal and external stakeholders, the double-entry system of bookkeeping, and the differences between financial reporting and financial statements. Furthermore, it analyzes various business transactions, the application of debit and credit recording, and provides examples to illustrate these concepts. The report includes a detailed ledger of transactions. The report aims to provide a comprehensive understanding of financial accounting principles and their practical application.

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Part (a).........................................................................................................................................3

Part (b).........................................................................................................................................6

CONCLUSION..............................................................................................................................27

REFERENCES..............................................................................................................................28

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Part (a).........................................................................................................................................3

Part (b).........................................................................................................................................6

CONCLUSION..............................................................................................................................27

REFERENCES..............................................................................................................................28

INTRODUCTION

Financial accounting is a specific branch of accounting which assist the company in

recording and summarising the financial transactions (Trucco, 2015). It is the process of

recording, summarising and reporting the business transactions resulting from several business

operations for a period of time. Company prepares its financial statements by implementing the

financial accounting system which includes profit and loss account, balance sheet, cash flow

statement and so on. For understanding of financial accounting, a company named Fathom

financial consulting is chosen which is engaged in consultancy services. This report provides

the meaning of financial accounting and its several purposes and it also explains various

stakeholders of an organisation both internal as well as external. Apart from this, it defines the

double entry system of recoding the financial transactions which helps in preparing the financial

statements. This report further explains the concepts of suspense account, control account, bank

reconciliation account and book keeping as well as it provides the differences between financial

reporting and financial statements.

MAIN BODY

Part (a)

1. Definition and meaning of financial accounting.

Financial accounting

Financial accounting is a scientific method of recording and preparing the financial

statements of an organisation (Liao, Kang, Morris and Tang, 2013). These financial statements

shows the financial health of the company which is used by the stakeholders associated with the

business to make an informed decision. Financial accounting works in contrast with the

managerial accounting . The primary financial statements prepared with the help of financial

accounting principles are profit & loss statement, balance sheet, cash flow statement and

statement of retained earnings. It is a culmination of science and art in preparing financial

accounts. They are prepared on the lines of accounting standards like IFRS , IAS, GAAP etc. all

over the world. Financial accounting uses the principle of double entry system to record its

statements. The principle is the heart of the system. Financial accounting doesn't report the

overall value of the firm , rather it provides functional financial health of the business to support

Financial accounting is a specific branch of accounting which assist the company in

recording and summarising the financial transactions (Trucco, 2015). It is the process of

recording, summarising and reporting the business transactions resulting from several business

operations for a period of time. Company prepares its financial statements by implementing the

financial accounting system which includes profit and loss account, balance sheet, cash flow

statement and so on. For understanding of financial accounting, a company named Fathom

financial consulting is chosen which is engaged in consultancy services. This report provides

the meaning of financial accounting and its several purposes and it also explains various

stakeholders of an organisation both internal as well as external. Apart from this, it defines the

double entry system of recoding the financial transactions which helps in preparing the financial

statements. This report further explains the concepts of suspense account, control account, bank

reconciliation account and book keeping as well as it provides the differences between financial

reporting and financial statements.

MAIN BODY

Part (a)

1. Definition and meaning of financial accounting.

Financial accounting

Financial accounting is a scientific method of recording and preparing the financial

statements of an organisation (Liao, Kang, Morris and Tang, 2013). These financial statements

shows the financial health of the company which is used by the stakeholders associated with the

business to make an informed decision. Financial accounting works in contrast with the

managerial accounting . The primary financial statements prepared with the help of financial

accounting principles are profit & loss statement, balance sheet, cash flow statement and

statement of retained earnings. It is a culmination of science and art in preparing financial

accounts. They are prepared on the lines of accounting standards like IFRS , IAS, GAAP etc. all

over the world. Financial accounting uses the principle of double entry system to record its

statements. The principle is the heart of the system. Financial accounting doesn't report the

overall value of the firm , rather it provides functional financial health of the business to support

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the investors in making an opinion about the firm. It is an integral part of any business. The

purpose of making financial statements are described here in as under :

Cash flow analysis : Financial statements manifest the true liquid position of the

business , primarily through cash flow statement. It helps the investors to ascertain the

liquid position of the company. It gives an assurance to the creditors that company is

solvent enough to repay their debts at any time. It assures the creditors about company's

ability to repay them at any day.

Taxation policy : Preparing financial statements based on the principles of accounting

standards and norms helps the firm in ascertaining the accurate tax liability of the

business (Whittington, 2016). It also helps the business in ensuring flow of taxes and

identify potential sources through which it can secure tax rebates. It also helps the

business from tax evasion saving it from the legal troubles.

Helps in building strategy framework : Financial statements provides quantitative as well

as qualitative data set to the management which helps them to devise future strategies.

With the help of Financial data in the hand , the management would be able to decipher

the information into valuable inputs about the target areas to focus on. And the areas

which are profitable to a business, hence designing strategies accordingly.

Beneficial to stakeholders : Through financial statements of the company its stakeholders

can analyse its profitability and potential future position. On the basis of this information

they can decide whether to invest further or withdraw their money. Its also helpful to the

government to ascertain whether the company is liquid or is walking towards sickness.

Track financial performance : A business firm through a comparison between its current

financial position and past performances can evaluate its overall performance over the

years . Keeping a track on the financial performance year to year helps the business to

identify key factors which daunted the business in the particular year and restructure that

loophole to perform better in the future.

2. Different types of internal and external stakeholders.

Stakeholder- The stakeholders can be defined as those individuals who have their interest

in the activities and functions of other companies (Trotman and Carson, 2018). Basically,

purpose of making financial statements are described here in as under :

Cash flow analysis : Financial statements manifest the true liquid position of the

business , primarily through cash flow statement. It helps the investors to ascertain the

liquid position of the company. It gives an assurance to the creditors that company is

solvent enough to repay their debts at any time. It assures the creditors about company's

ability to repay them at any day.

Taxation policy : Preparing financial statements based on the principles of accounting

standards and norms helps the firm in ascertaining the accurate tax liability of the

business (Whittington, 2016). It also helps the business in ensuring flow of taxes and

identify potential sources through which it can secure tax rebates. It also helps the

business from tax evasion saving it from the legal troubles.

Helps in building strategy framework : Financial statements provides quantitative as well

as qualitative data set to the management which helps them to devise future strategies.

With the help of Financial data in the hand , the management would be able to decipher

the information into valuable inputs about the target areas to focus on. And the areas

which are profitable to a business, hence designing strategies accordingly.

Beneficial to stakeholders : Through financial statements of the company its stakeholders

can analyse its profitability and potential future position. On the basis of this information

they can decide whether to invest further or withdraw their money. Its also helpful to the

government to ascertain whether the company is liquid or is walking towards sickness.

Track financial performance : A business firm through a comparison between its current

financial position and past performances can evaluate its overall performance over the

years . Keeping a track on the financial performance year to year helps the business to

identify key factors which daunted the business in the particular year and restructure that

loophole to perform better in the future.

2. Different types of internal and external stakeholders.

Stakeholder- The stakeholders can be defined as those individuals who have their interest

in the activities and functions of other companies (Trotman and Carson, 2018). Basically,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

objective of these stakeholders is to earn profits and revenue. There are two types of stakeholders

which are as follows:

External stakeholder.

Internal stakeholder.

These two stakeholders keep an extra site of eyes on the activities of other companies.

Description of these stakeholders is mentioned below:

External stakeholders- These stakeholders can be defined as kind of stakeholders who are

not involved in the daily activities and functions. As well as do not have any other rights

like other members of companies. These stakeholders includes government, supplier,

customer, creditors etc. The objective of all these stakeholders is common which is to

earn return on the invested capital. Herein, below some types of external stakeholders are

mentioned such as:

1. Investors- These stakeholders are associated with the investing money in the operations

and activities of business (Hiebl, 2014). The aim of these stakeholders is to get maximum

return on the invested income. For this purpose they show their interest in the financial

information of companies so that they can take decision about whether they should invest

or not. In the absence of checking the financial information of companies it can be

difficult for them to take the investment decisions.

2. Government- In different countries, the government act as important external stakeholder.

They establish some rules and regulations which are needed to be followed by the

companies. Eventually, the government shows the interest in the financial information of

companies for the purpose of determining about how much tax should be taken.

3. Suppliers- The suppliers provide raw material and other needed things to the companies.

They make transactions with the companies in both ways including on credit and cash.

The credit transaction depends on the reputation of firms and it is evaluated by the

financial transactions. For this purpose the suppliers show their interest in the financial

information of companies. If financial condition is weak of any company then they will

not be willing to make transaction on credit basis.

4. Creditors- These are kind of stakeholders who provide financial assistance to the

companies when they need. In return they get the interest on borrowed amount. Herein, it

is important for the creditors to evaluate the financial condition of company before giving

which are as follows:

External stakeholder.

Internal stakeholder.

These two stakeholders keep an extra site of eyes on the activities of other companies.

Description of these stakeholders is mentioned below:

External stakeholders- These stakeholders can be defined as kind of stakeholders who are

not involved in the daily activities and functions. As well as do not have any other rights

like other members of companies. These stakeholders includes government, supplier,

customer, creditors etc. The objective of all these stakeholders is common which is to

earn return on the invested capital. Herein, below some types of external stakeholders are

mentioned such as:

1. Investors- These stakeholders are associated with the investing money in the operations

and activities of business (Hiebl, 2014). The aim of these stakeholders is to get maximum

return on the invested income. For this purpose they show their interest in the financial

information of companies so that they can take decision about whether they should invest

or not. In the absence of checking the financial information of companies it can be

difficult for them to take the investment decisions.

2. Government- In different countries, the government act as important external stakeholder.

They establish some rules and regulations which are needed to be followed by the

companies. Eventually, the government shows the interest in the financial information of

companies for the purpose of determining about how much tax should be taken.

3. Suppliers- The suppliers provide raw material and other needed things to the companies.

They make transactions with the companies in both ways including on credit and cash.

The credit transaction depends on the reputation of firms and it is evaluated by the

financial transactions. For this purpose the suppliers show their interest in the financial

information of companies. If financial condition is weak of any company then they will

not be willing to make transaction on credit basis.

4. Creditors- These are kind of stakeholders who provide financial assistance to the

companies when they need. In return they get the interest on borrowed amount. Herein, it

is important for the creditors to evaluate the financial condition of company before giving

the financial services. This ensures them that any particular company will return the

borrowed amount in given time with interest.

Internal stakeholder- The internal stakeholders are those stakeholders who are available

in daily activities and operations of organisation (Lanen, Anderson and Maher, 2013).

Some common examples of these stakeholders are employees, managers etc. which are

mentioned below broad sense:

1. Employees- The employees are those who perform company's operations and activities

and get wages, salary in return. Any company's financial condition depends on the

performance of these stakeholders. The employees show their interest in the financial

information of the companies so that they can ensure about financial position of

organisation because their growth and development is linked with this.

2. Board of director (BOD)- The board of director are very important internal stakeholders

in any kind of business. This is why because they are responsible for preparation and

formulating the strategies. They show their interest in financial information of the

company, so that they can make their future plans and policies accordingly.

Part (b)

Client 1.

Business transaction- In business, there are wide range of transactions such as:

Sales- It can be defined as transfer of goods and services from seller to buyer. In return

seller get money from the buyer.

Purchase- This can be defined as acquiring goods and services from seller.

Receipt- It can be defined as a document that contains information about date of purchase

and acknowledging to person who has received money.

Payments- In general the payment means trade of value from one person to another for

products and services.

Double entry:

Manual system- This system of keeping the financial transactions of companies by hand.

Eventually, this accounting system is being used by the small business organisations.

They use this accounting system because of there small business area and transactions.

borrowed amount in given time with interest.

Internal stakeholder- The internal stakeholders are those stakeholders who are available

in daily activities and operations of organisation (Lanen, Anderson and Maher, 2013).

Some common examples of these stakeholders are employees, managers etc. which are

mentioned below broad sense:

1. Employees- The employees are those who perform company's operations and activities

and get wages, salary in return. Any company's financial condition depends on the

performance of these stakeholders. The employees show their interest in the financial

information of the companies so that they can ensure about financial position of

organisation because their growth and development is linked with this.

2. Board of director (BOD)- The board of director are very important internal stakeholders

in any kind of business. This is why because they are responsible for preparation and

formulating the strategies. They show their interest in financial information of the

company, so that they can make their future plans and policies accordingly.

Part (b)

Client 1.

Business transaction- In business, there are wide range of transactions such as:

Sales- It can be defined as transfer of goods and services from seller to buyer. In return

seller get money from the buyer.

Purchase- This can be defined as acquiring goods and services from seller.

Receipt- It can be defined as a document that contains information about date of purchase

and acknowledging to person who has received money.

Payments- In general the payment means trade of value from one person to another for

products and services.

Double entry:

Manual system- This system of keeping the financial transactions of companies by hand.

Eventually, this accounting system is being used by the small business organisations.

They use this accounting system because of there small business area and transactions.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Electronic system- This system is related to the regulating the accounting functions,

research and recording of transactions by use of computer based accounting tools (Adler,

2013). This system is used when there is huge number of transactions. It removes the

complexity from the accounting.

Debit & credit recording- There are various kind of rules and regulations to record the

debits and credit amount. In the context of double entry book keeping system, debit and

credit should be equal. As well as for each transaction total amount entered in left side

must be entered in right side.

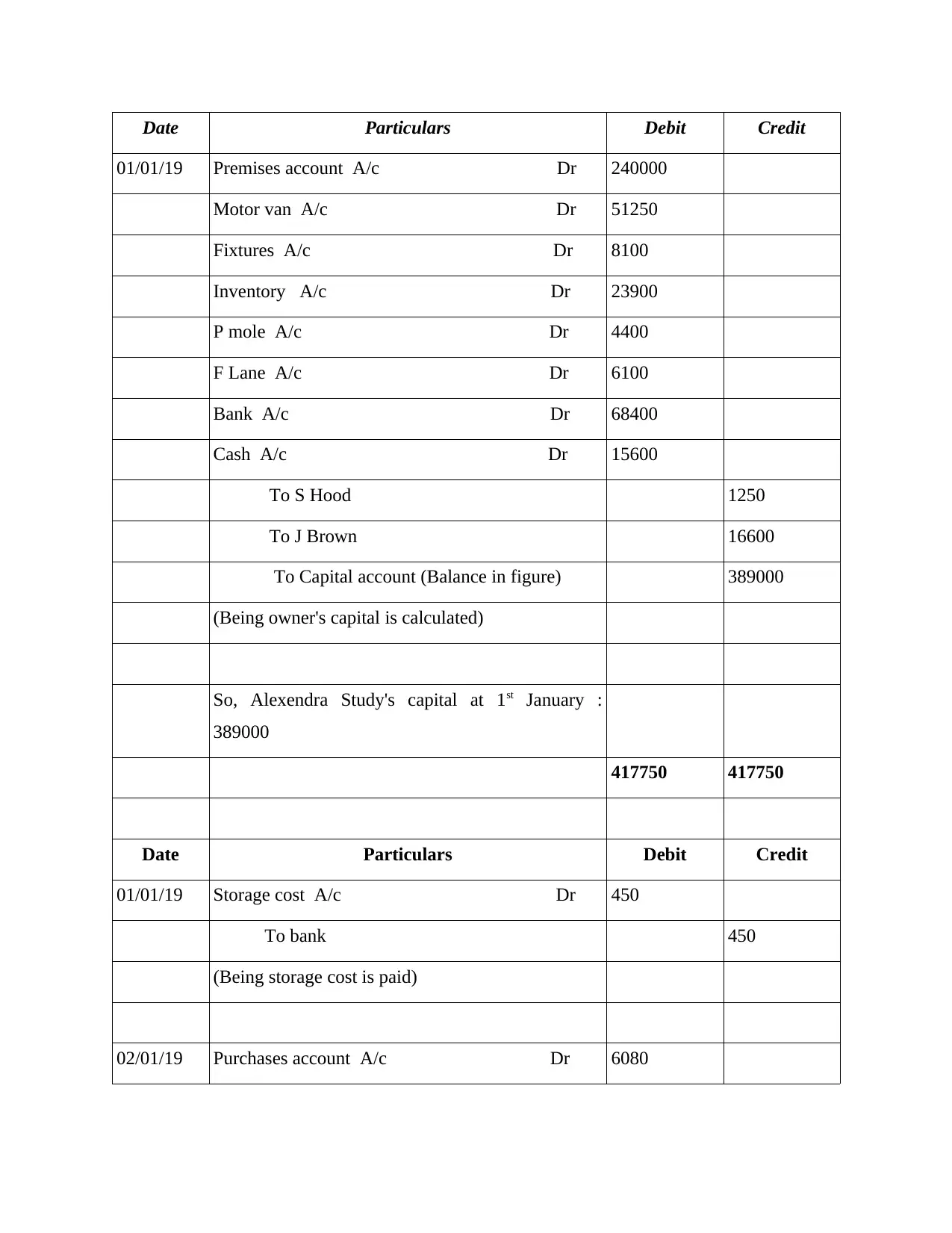

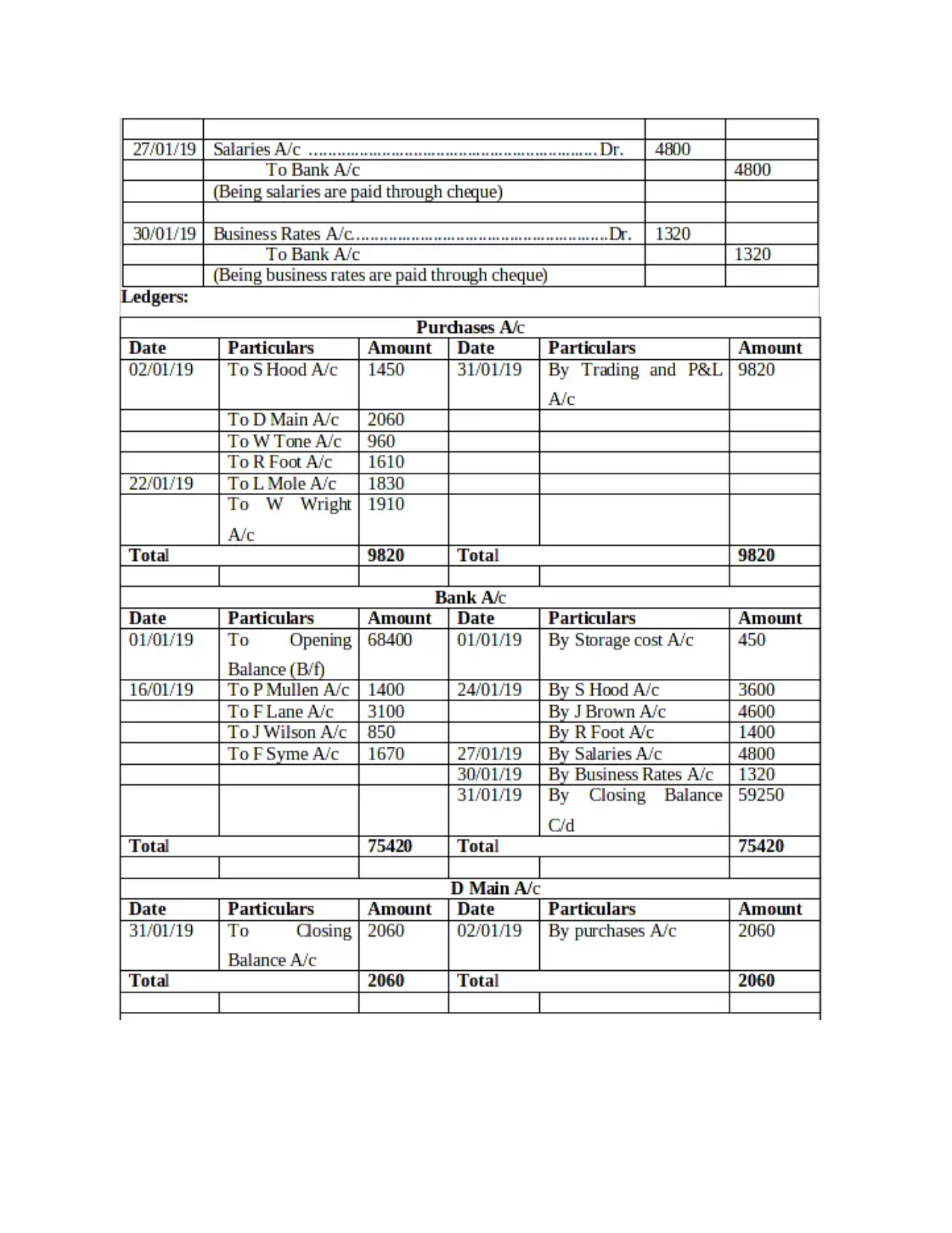

Herein, below double entry with ledgers on the basis of given data is mentioned:

research and recording of transactions by use of computer based accounting tools (Adler,

2013). This system is used when there is huge number of transactions. It removes the

complexity from the accounting.

Debit & credit recording- There are various kind of rules and regulations to record the

debits and credit amount. In the context of double entry book keeping system, debit and

credit should be equal. As well as for each transaction total amount entered in left side

must be entered in right side.

Herein, below double entry with ledgers on the basis of given data is mentioned:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Date Particulars Debit Credit

01/01/19 Premises account A/c Dr 240000

Motor van A/c Dr 51250

Fixtures A/c Dr 8100

Inventory A/c Dr 23900

P mole A/c Dr 4400

F Lane A/c Dr 6100

Bank A/c Dr 68400

Cash A/c Dr 15600

To S Hood 1250

To J Brown 16600

To Capital account (Balance in figure) 389000

(Being owner's capital is calculated)

So, Alexendra Study's capital at 1st January :

389000

417750 417750

Date Particulars Debit Credit

01/01/19 Storage cost A/c Dr 450

To bank 450

(Being storage cost is paid)

02/01/19 Purchases account A/c Dr 6080

01/01/19 Premises account A/c Dr 240000

Motor van A/c Dr 51250

Fixtures A/c Dr 8100

Inventory A/c Dr 23900

P mole A/c Dr 4400

F Lane A/c Dr 6100

Bank A/c Dr 68400

Cash A/c Dr 15600

To S Hood 1250

To J Brown 16600

To Capital account (Balance in figure) 389000

(Being owner's capital is calculated)

So, Alexendra Study's capital at 1st January :

389000

417750 417750

Date Particulars Debit Credit

01/01/19 Storage cost A/c Dr 450

To bank 450

(Being storage cost is paid)

02/01/19 Purchases account A/c Dr 6080

To S Hood A/c 1450

To D Main A/c 2060

To W Tone A/c 960

To R Foot A/c 1610

(Being goods purchase on credit from different

parties)

03/01/19 J Wilson A/c Dr 1200

T Cole A/c Dr 1650

F Syme A/c Dr 2100

J Allen A/c Dr 1020

P White A/c Dr 2520

F Lane A/c Dr 980

To sales A/c 9470

04/01/19 Motor expenses A/c Dr 470

To cash A/c 470

(Being motor expenses is paid)

07/01/19 Capital A/c Dr 1500

To cash A/c 1500

(Being cash withdrawal by owner himself)

09/01/19 To Cole A/c Dr 690

To D Main A/c 2060

To W Tone A/c 960

To R Foot A/c 1610

(Being goods purchase on credit from different

parties)

03/01/19 J Wilson A/c Dr 1200

T Cole A/c Dr 1650

F Syme A/c Dr 2100

J Allen A/c Dr 1020

P White A/c Dr 2520

F Lane A/c Dr 980

To sales A/c 9470

04/01/19 Motor expenses A/c Dr 470

To cash A/c 470

(Being motor expenses is paid)

07/01/19 Capital A/c Dr 1500

To cash A/c 1500

(Being cash withdrawal by owner himself)

09/01/19 To Cole A/c Dr 690

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

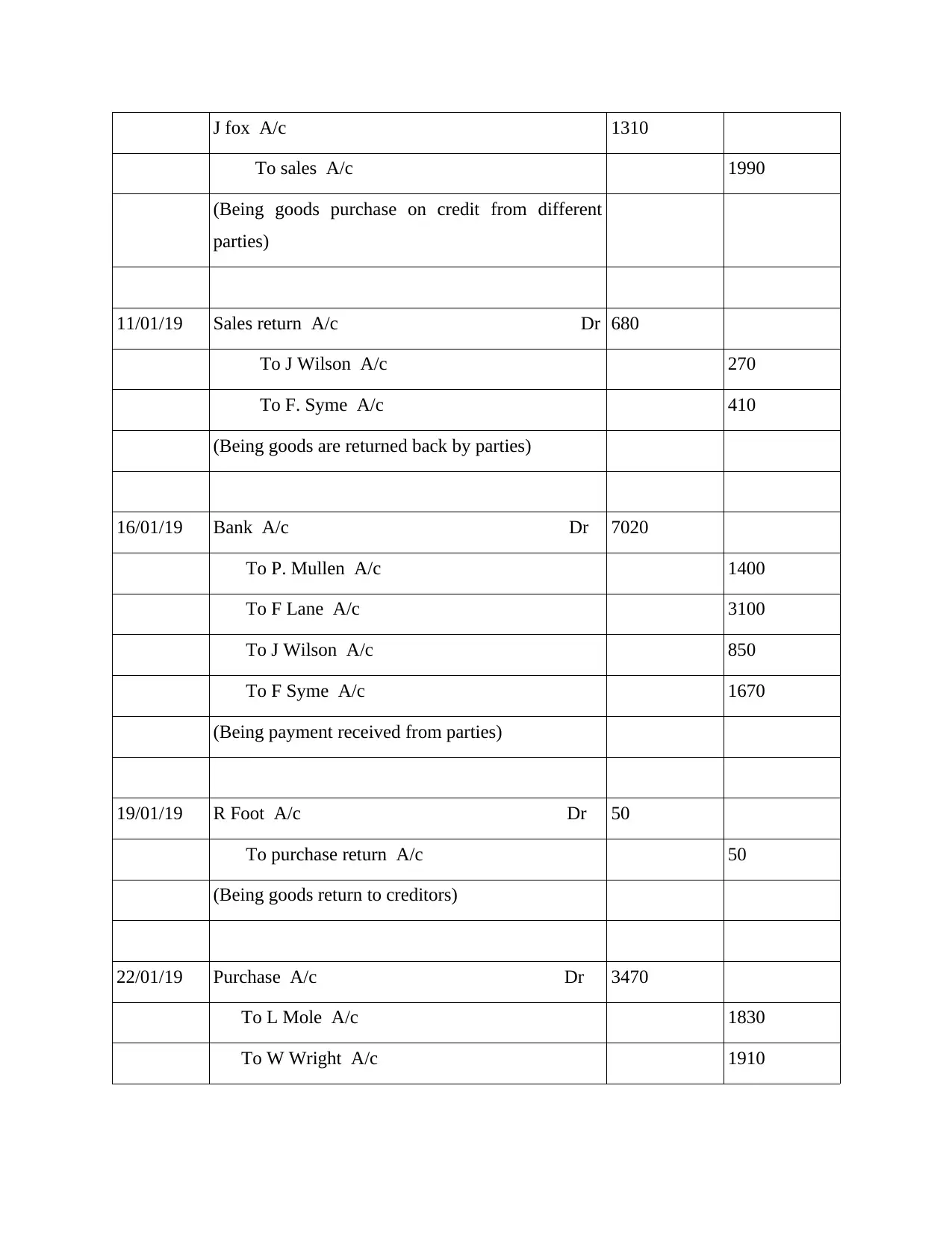

J fox A/c 1310

To sales A/c 1990

(Being goods purchase on credit from different

parties)

11/01/19 Sales return A/c Dr 680

To J Wilson A/c 270

To F. Syme A/c 410

(Being goods are returned back by parties)

16/01/19 Bank A/c Dr 7020

To P. Mullen A/c 1400

To F Lane A/c 3100

To J Wilson A/c 850

To F Syme A/c 1670

(Being payment received from parties)

19/01/19 R Foot A/c Dr 50

To purchase return A/c 50

(Being goods return to creditors)

22/01/19 Purchase A/c Dr 3470

To L Mole A/c 1830

To W Wright A/c 1910

To sales A/c 1990

(Being goods purchase on credit from different

parties)

11/01/19 Sales return A/c Dr 680

To J Wilson A/c 270

To F. Syme A/c 410

(Being goods are returned back by parties)

16/01/19 Bank A/c Dr 7020

To P. Mullen A/c 1400

To F Lane A/c 3100

To J Wilson A/c 850

To F Syme A/c 1670

(Being payment received from parties)

19/01/19 R Foot A/c Dr 50

To purchase return A/c 50

(Being goods return to creditors)

22/01/19 Purchase A/c Dr 3470

To L Mole A/c 1830

To W Wright A/c 1910

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

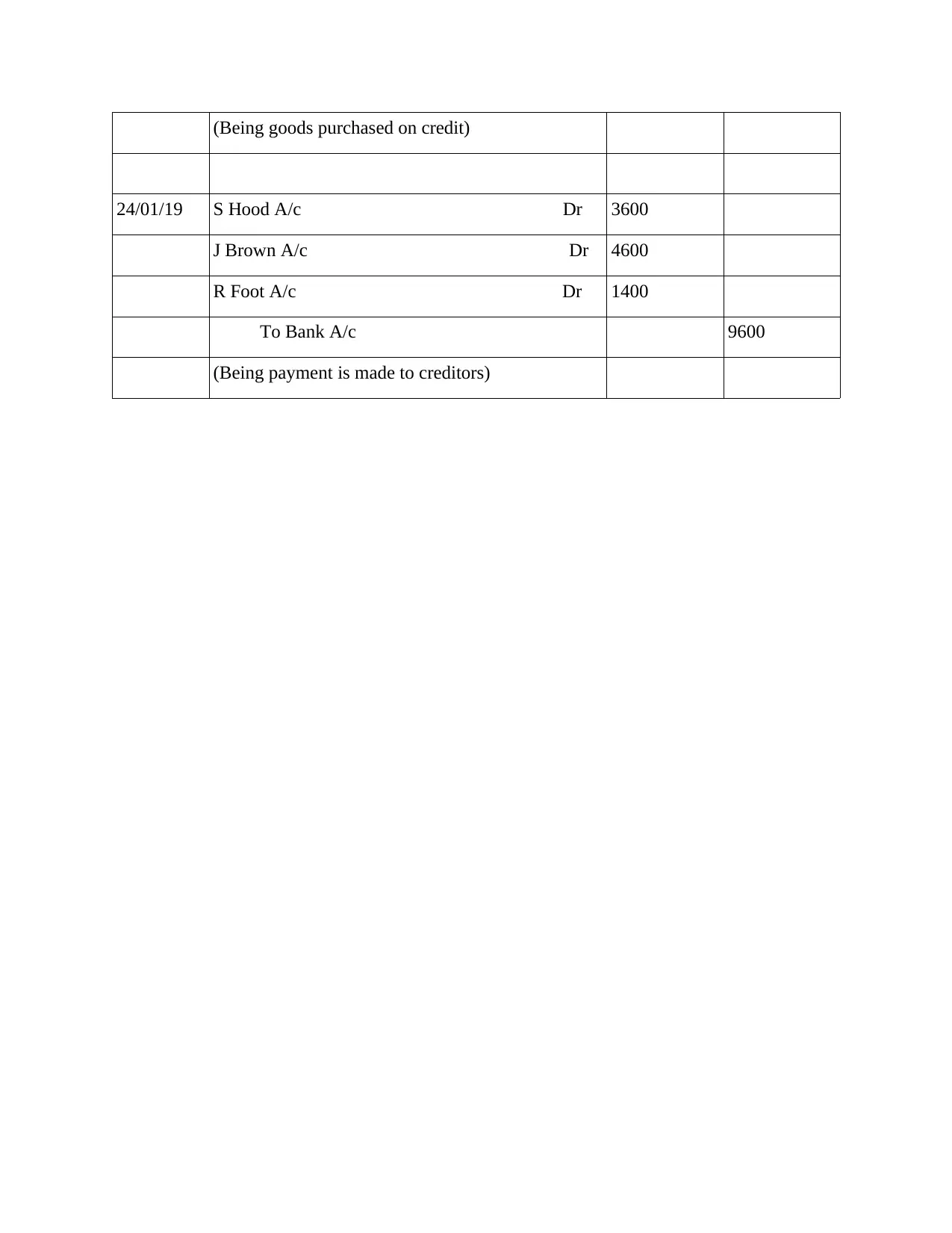

(Being goods purchased on credit)

24/01/19 S Hood A/c Dr 3600

J Brown A/c Dr 4600

R Foot A/c Dr 1400

To Bank A/c 9600

(Being payment is made to creditors)

24/01/19 S Hood A/c Dr 3600

J Brown A/c Dr 4600

R Foot A/c Dr 1400

To Bank A/c 9600

(Being payment is made to creditors)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.