Preparation of Financial Records and Statements for Conga: Accounting

VerifiedAdded on 2020/10/22

|17

|4068

|228

Homework Assignment

AI Summary

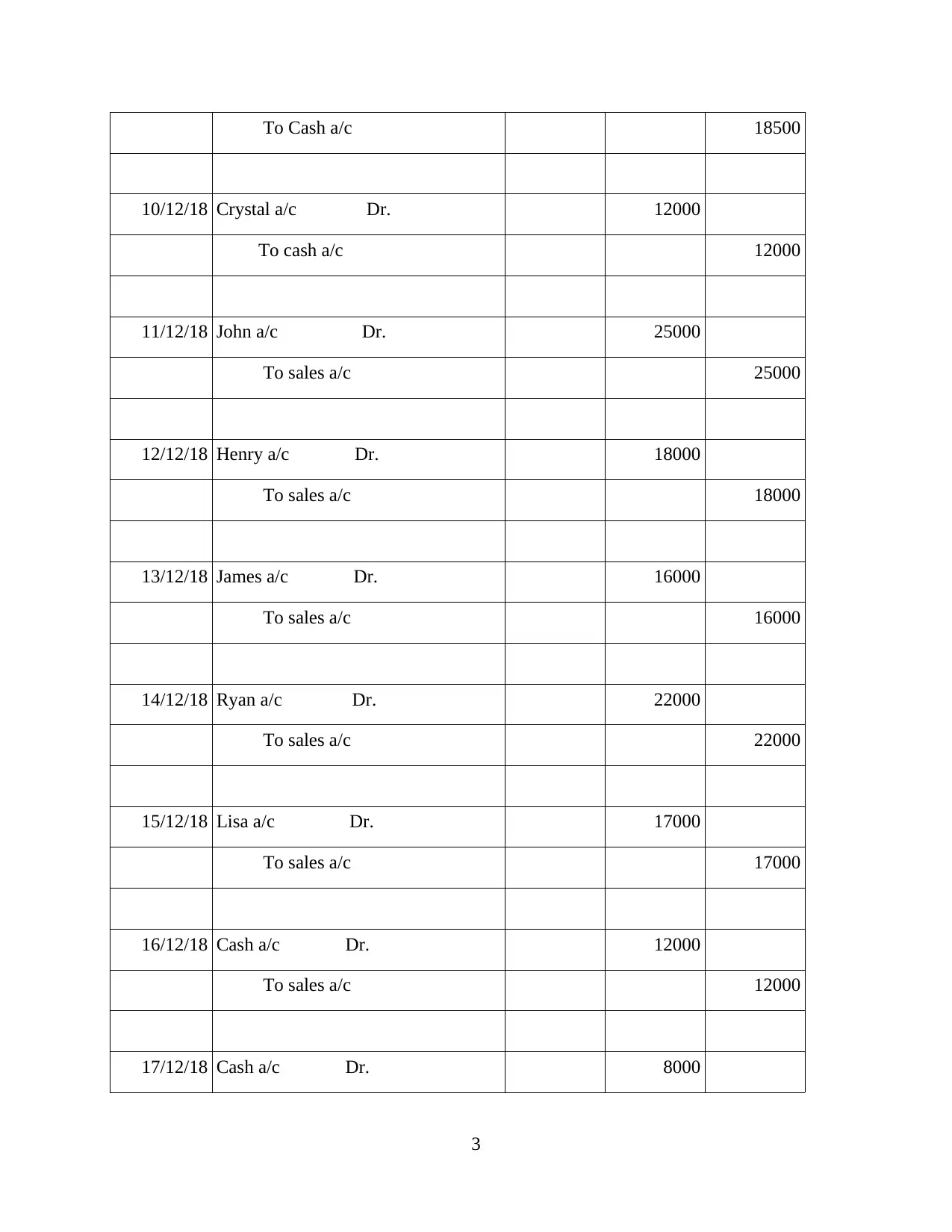

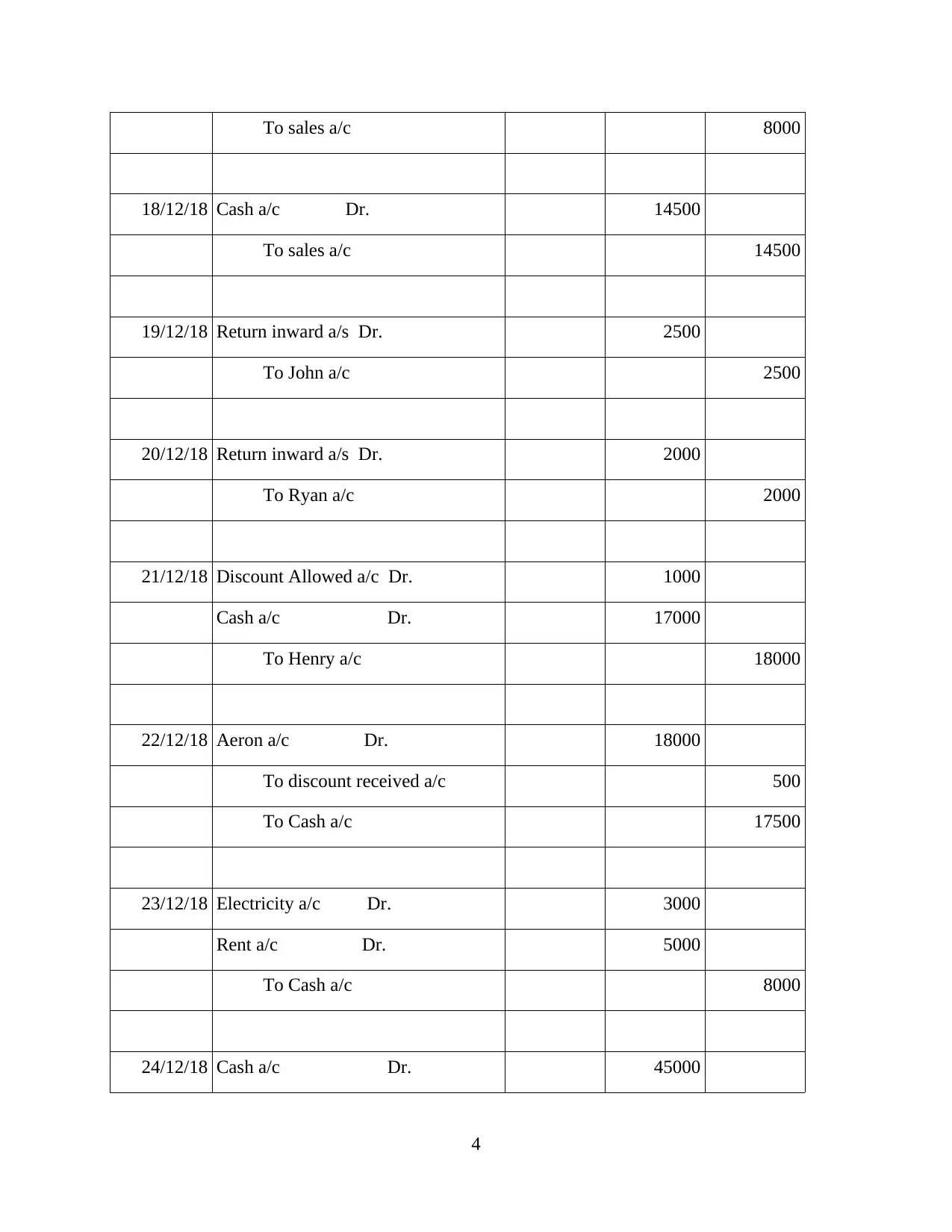

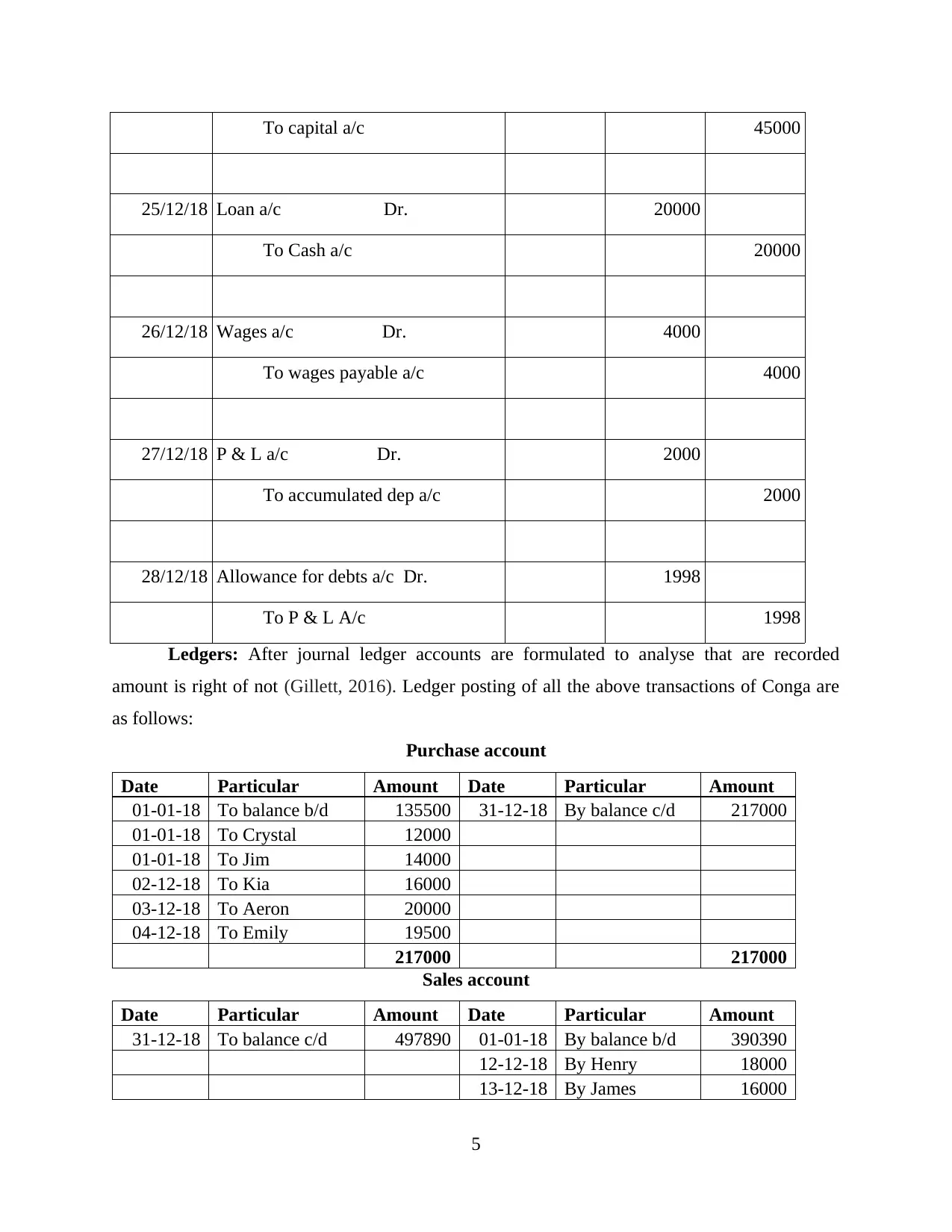

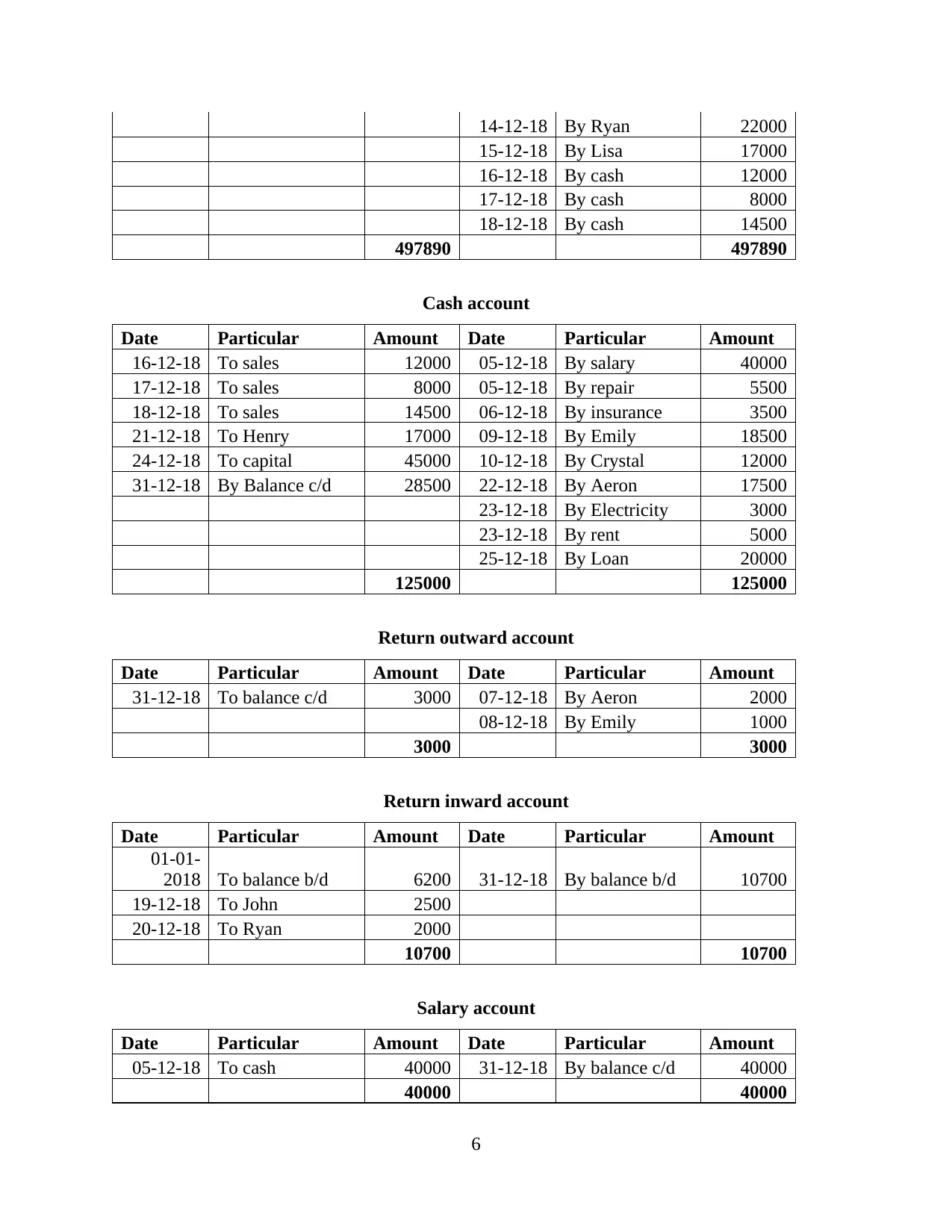

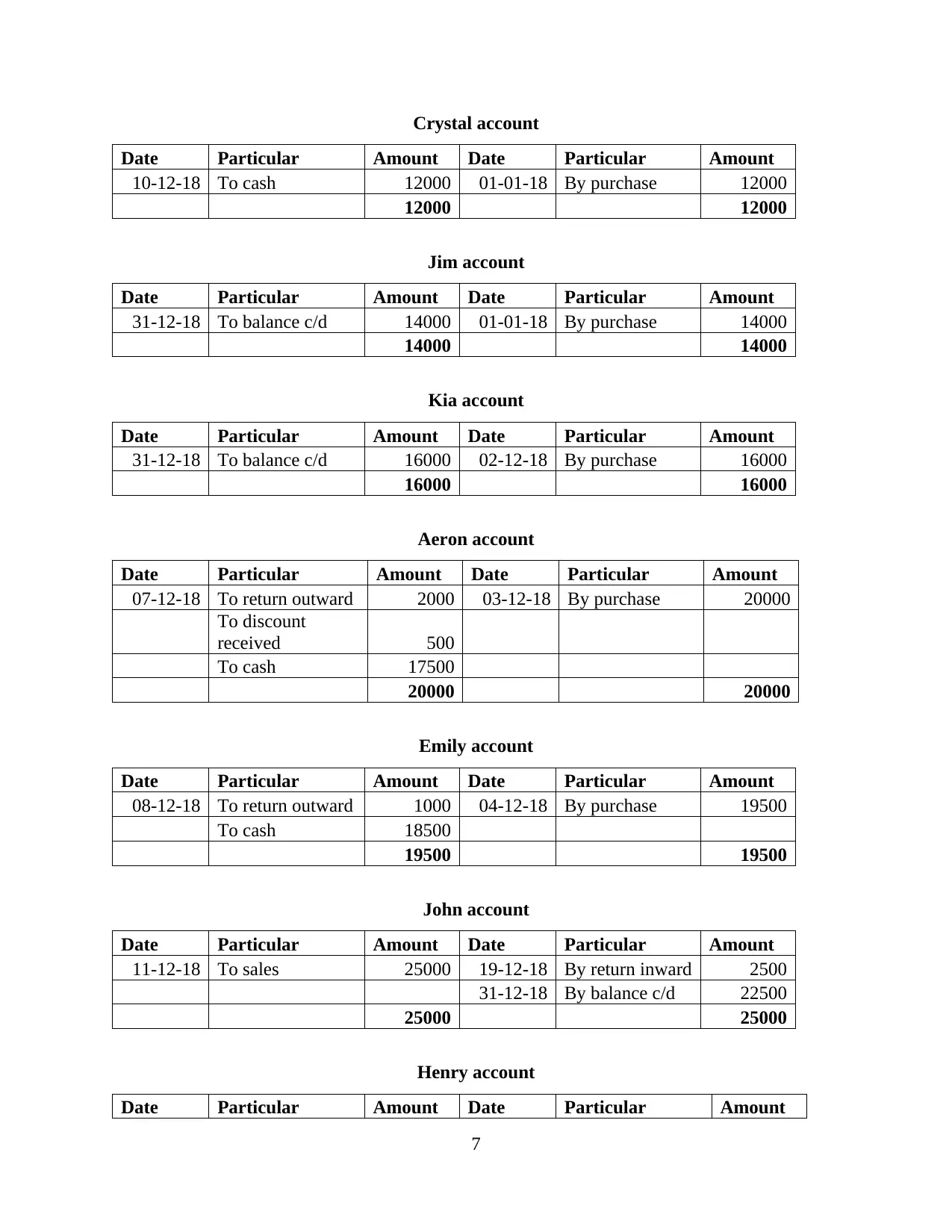

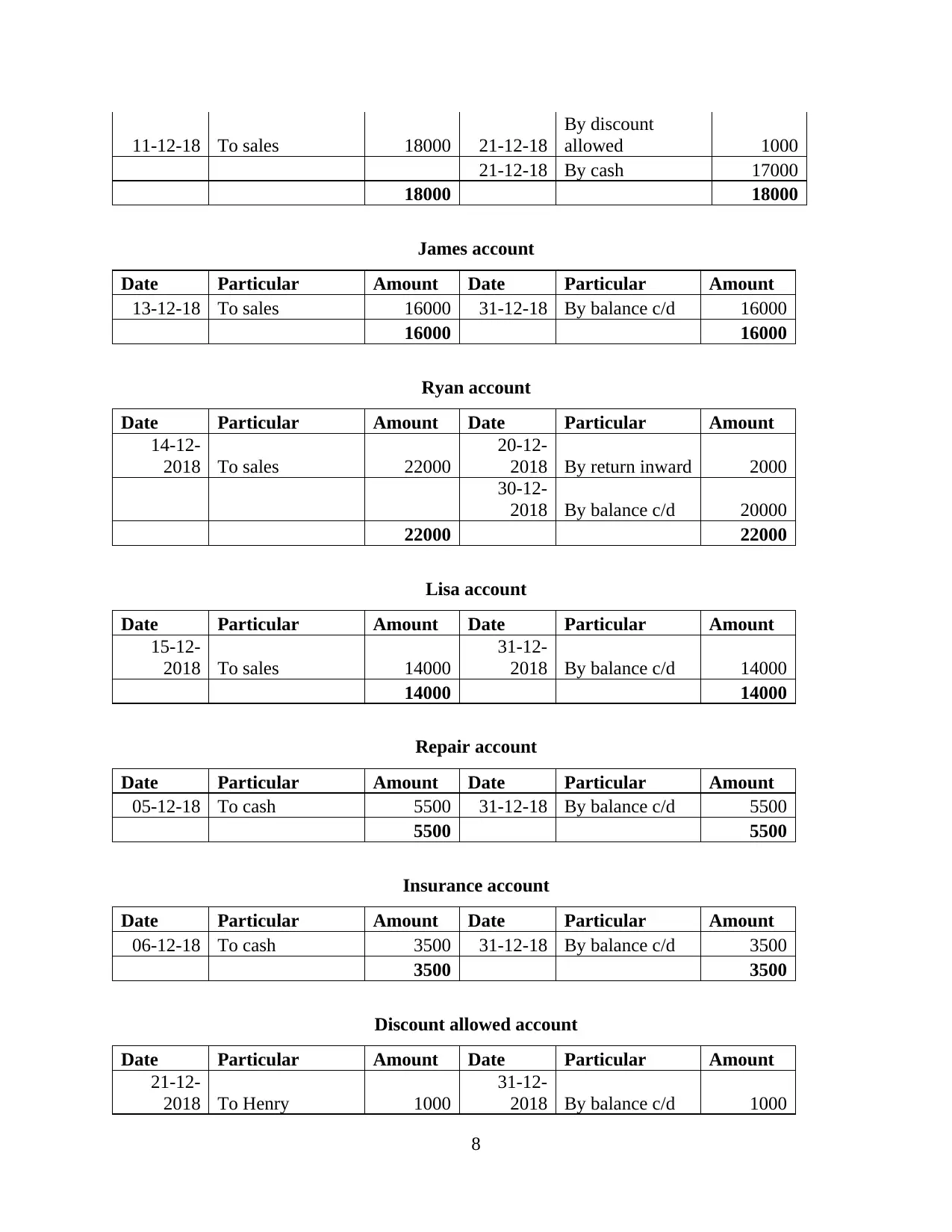

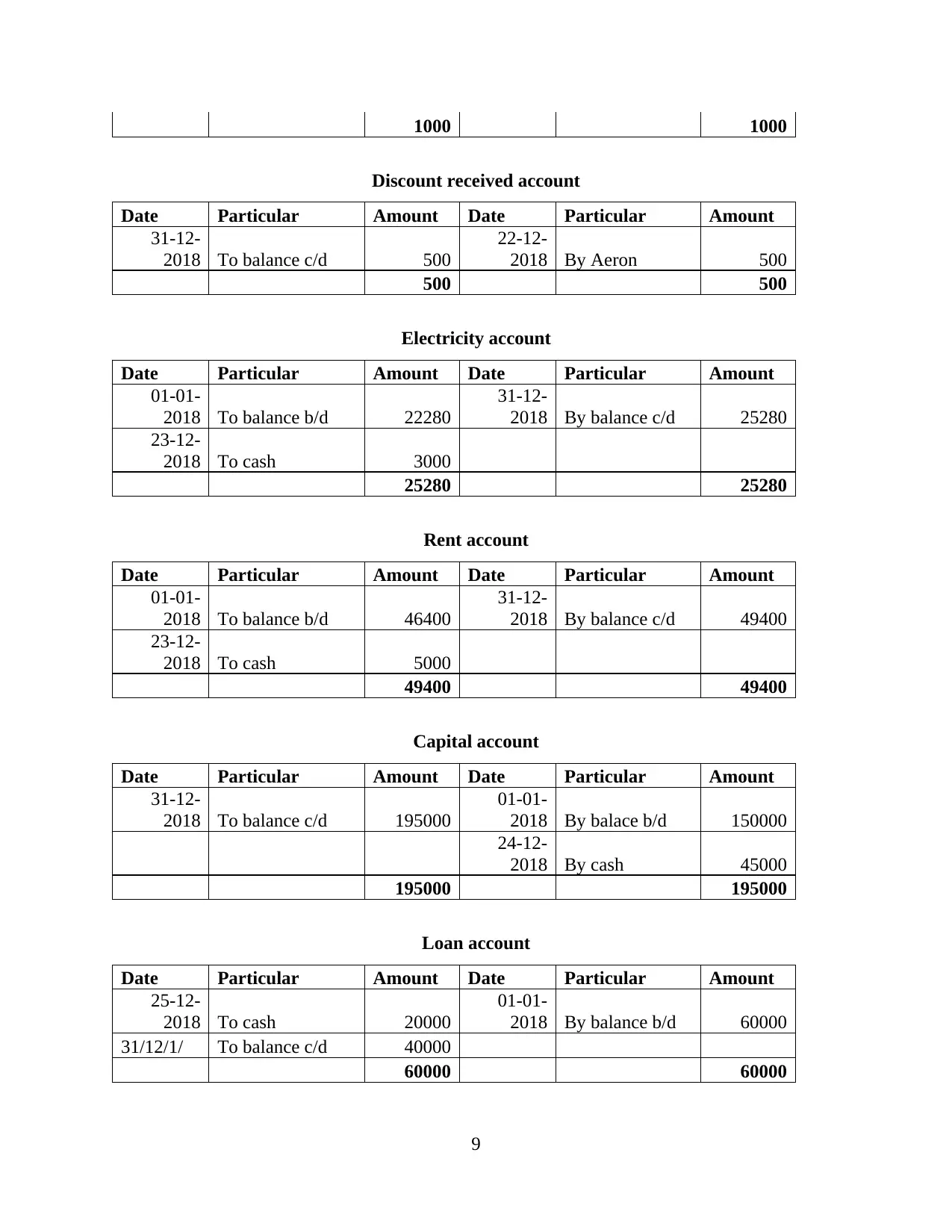

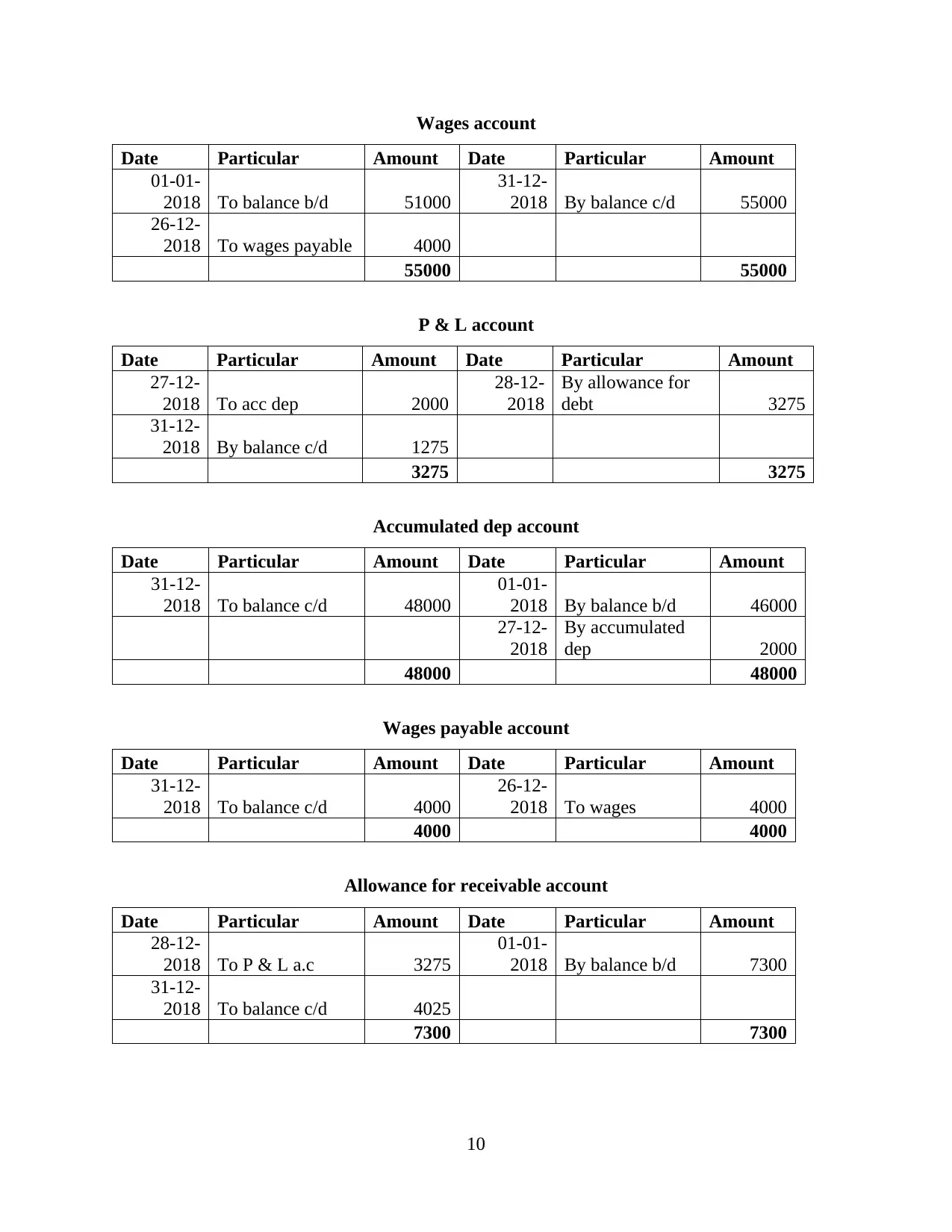

This assignment focuses on the financial accounting practices of Conga, a small UK-based toy sole trader. It provides a detailed analysis of the company's financial records, including journal entries and ledger postings. The assignment covers the preparation of financial statements, ensuring all transactions are accurately recorded. It also delves into the application of the prudence and accrual concepts within the context of Conga's financial activities. Furthermore, the report explains how Value Added Tax (VAT) is recorded in Conga's books and financial reports. The financial performance of the company is analyzed using various accounting tools and techniques. The report includes ledger accounts for purchase, sales, cash, return outward, return inward, salary, and other relevant accounts. The assignment aims to provide a comprehensive understanding of financial accounting principles and their practical application in a business setting, offering insights into financial analysis and decision-making.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.