Financial Accounting Analysis: Corr's Records and Statements

VerifiedAdded on 2023/01/19

|17

|2957

|73

Homework Assignment

AI Summary

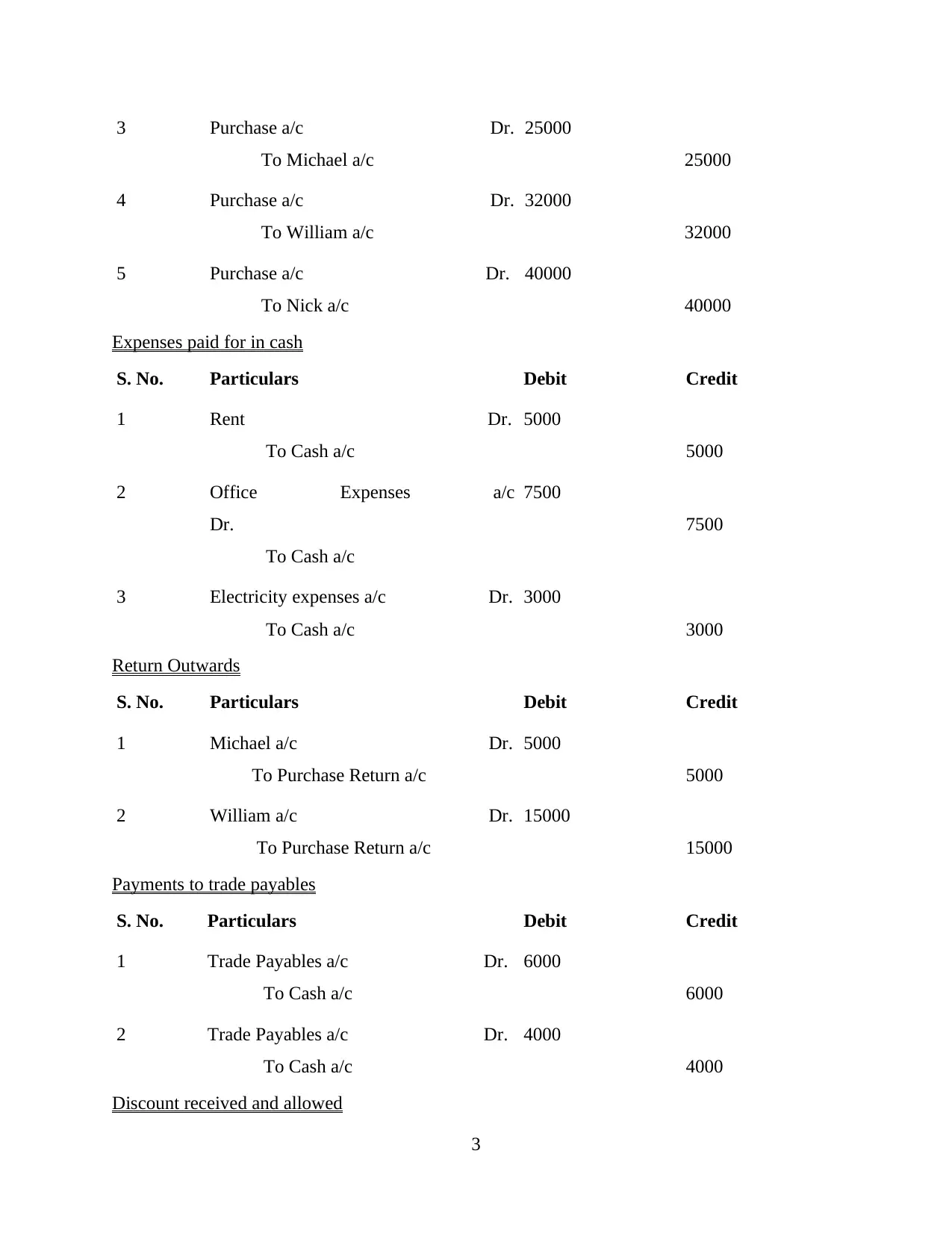

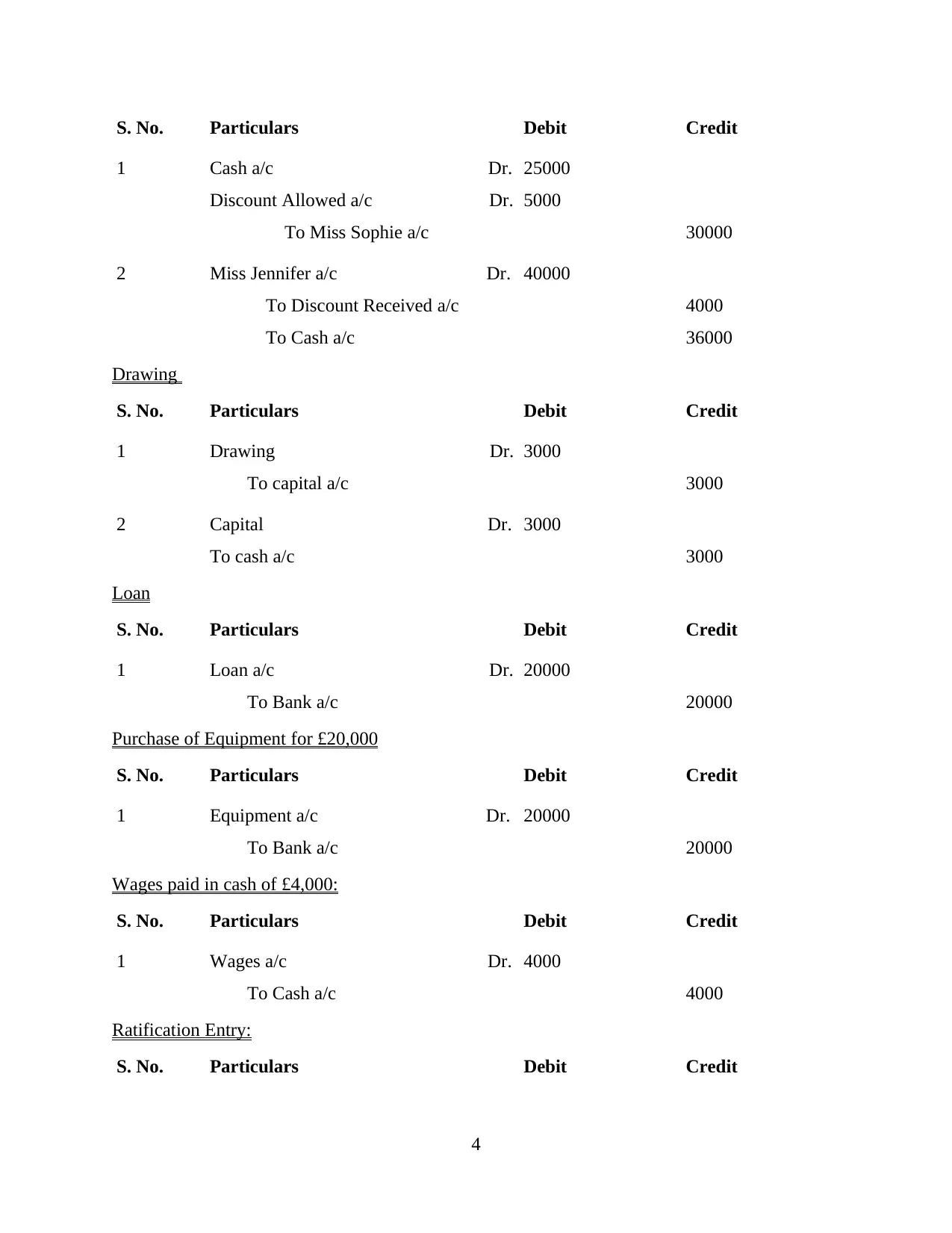

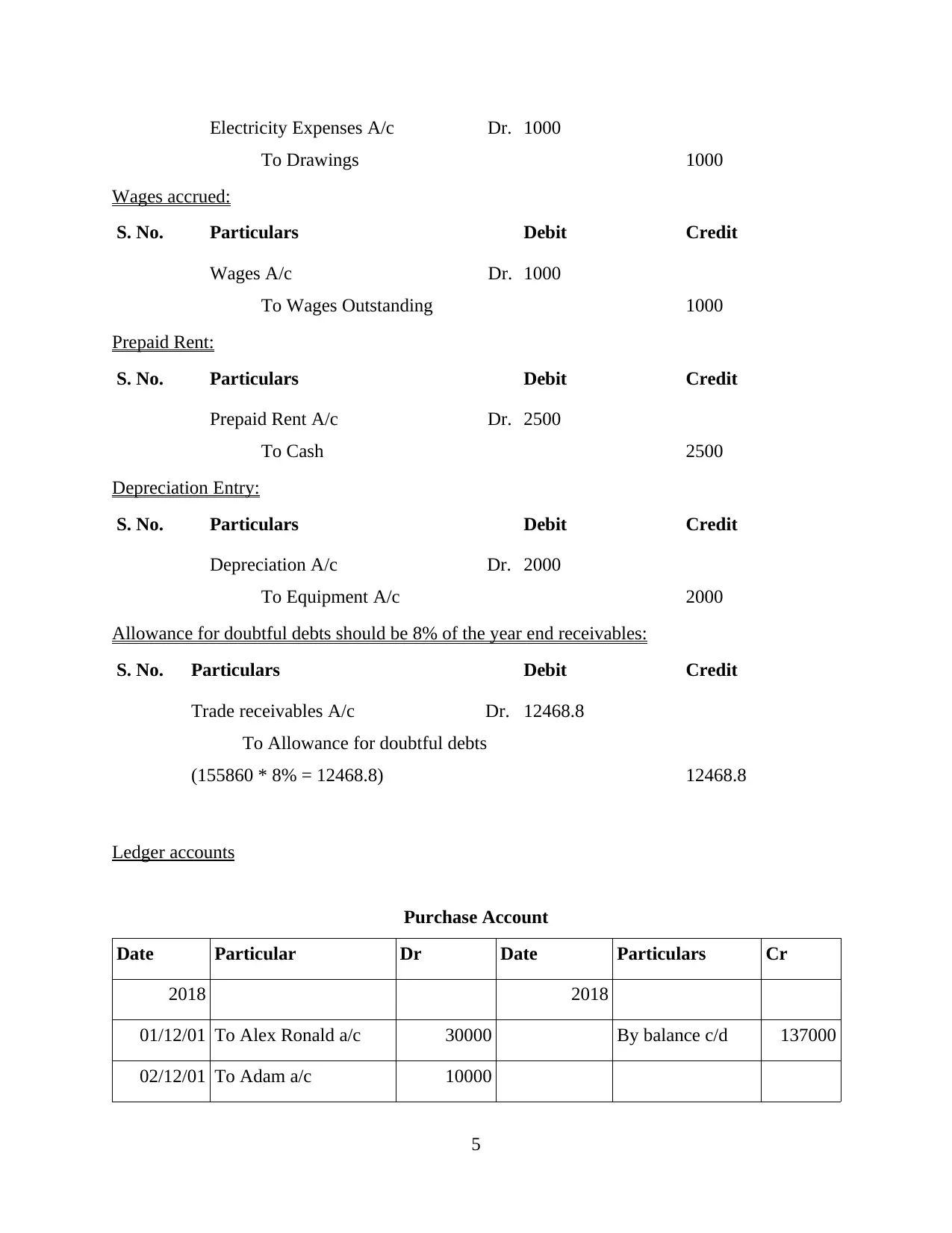

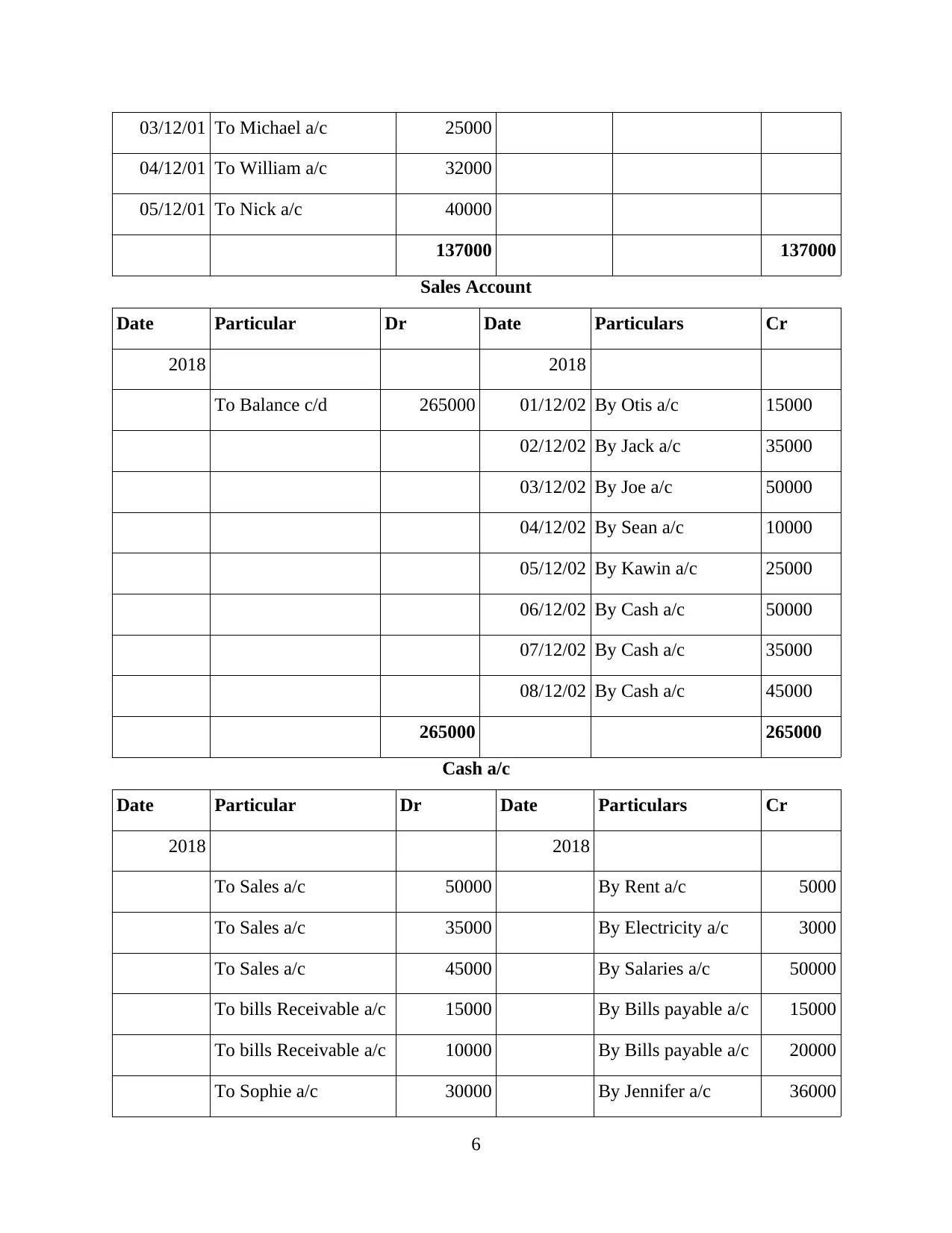

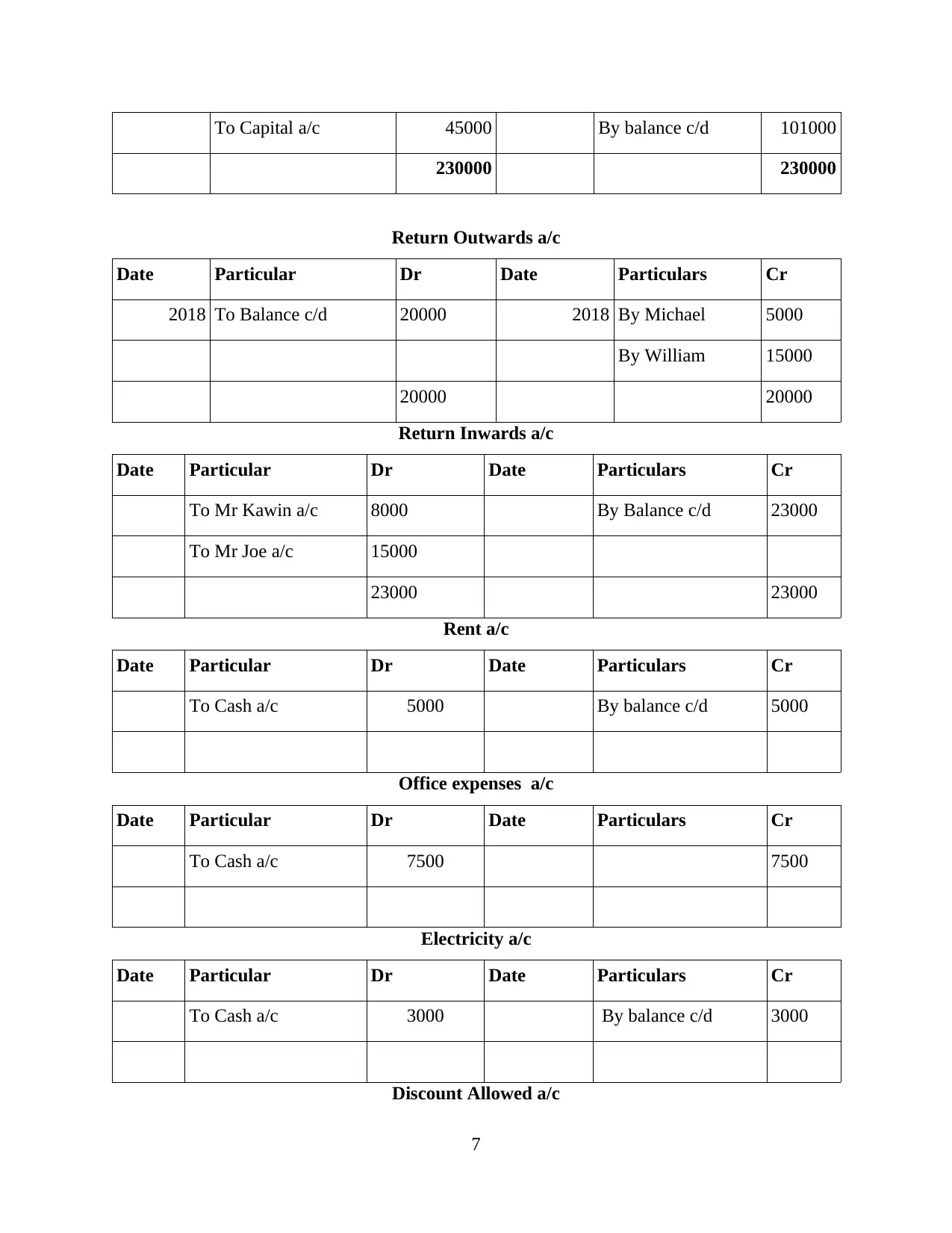

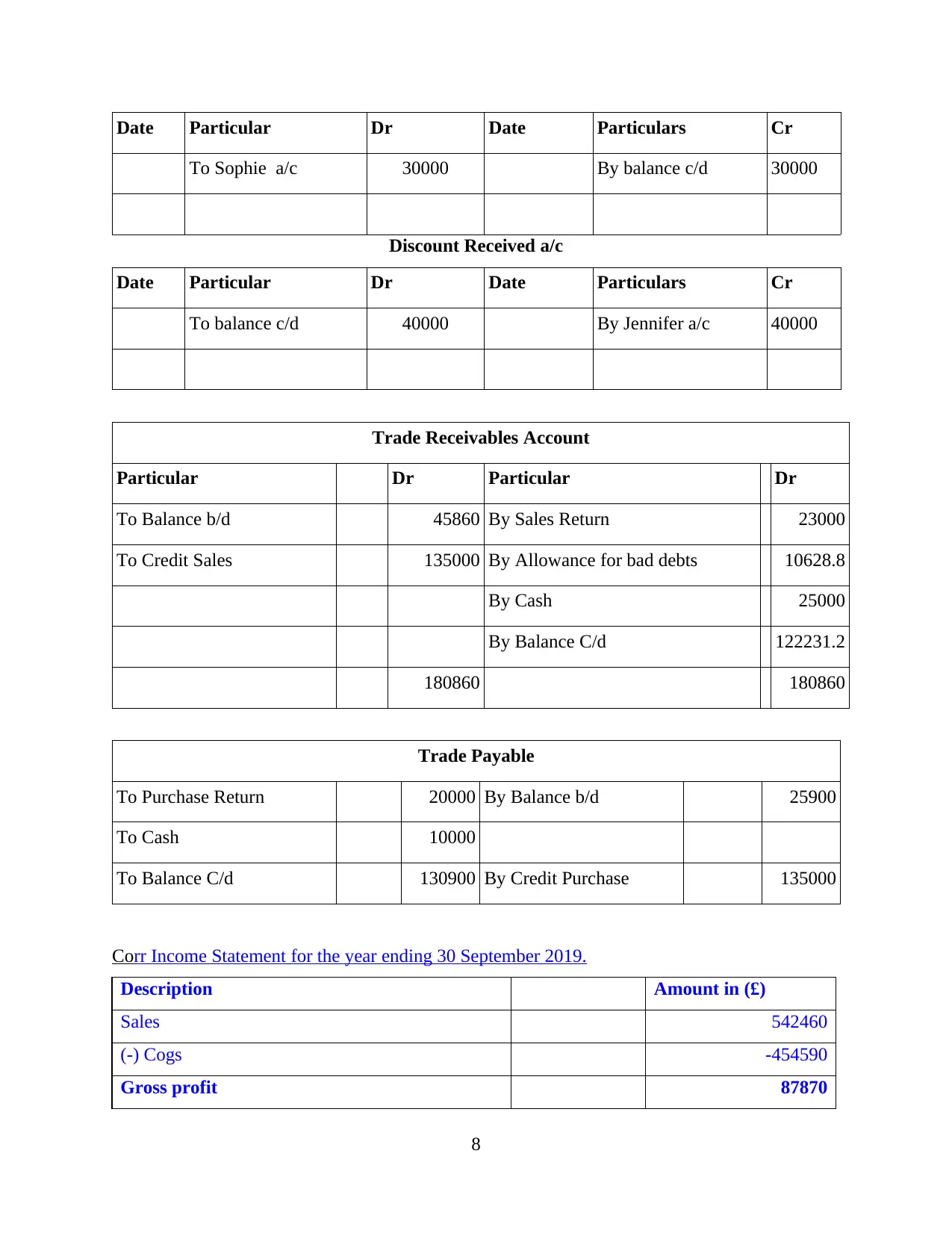

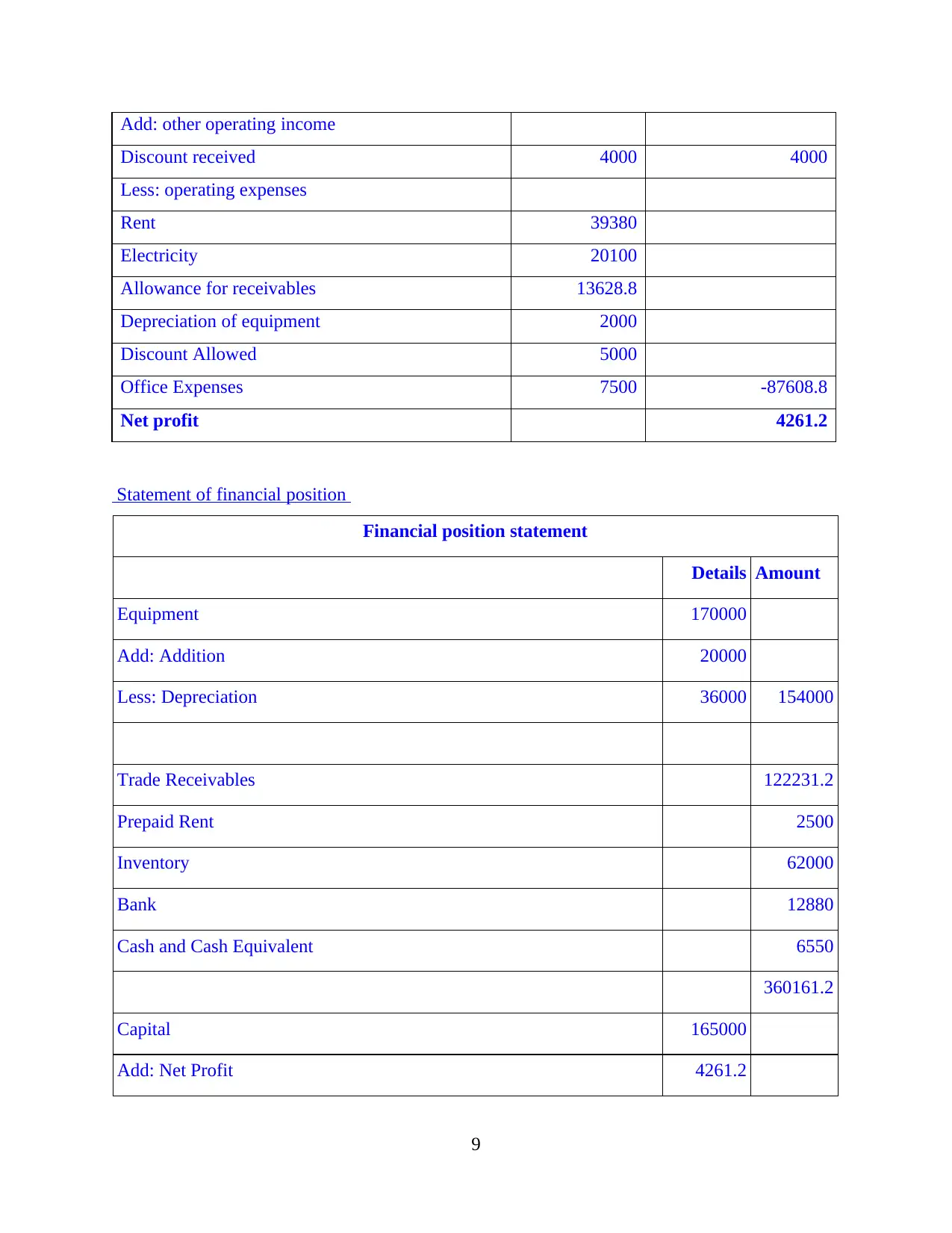

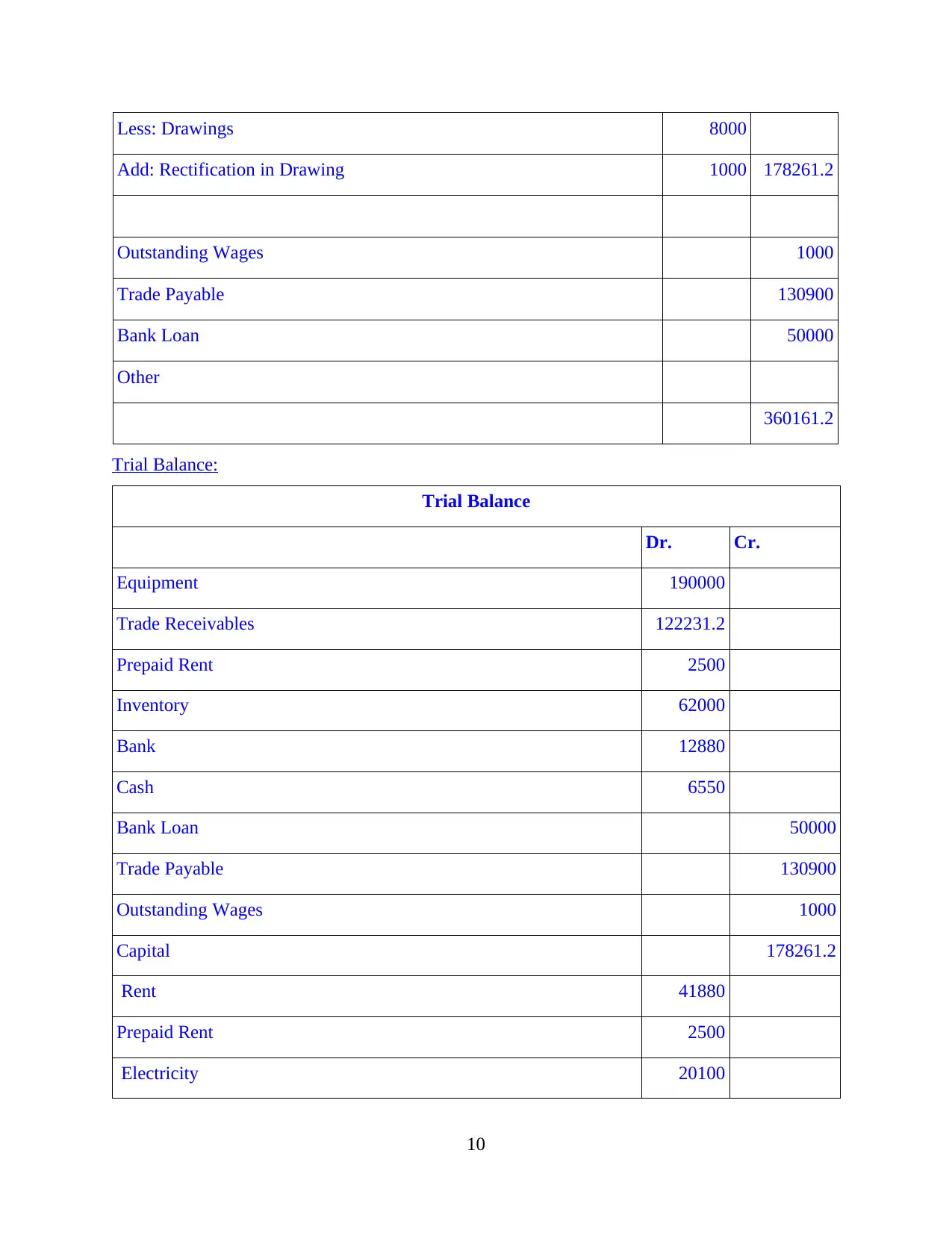

This assignment provides a comprehensive overview of financial accounting principles through a case study of Corr, a sole trader company. It begins with detailed journal entries for various transactions, including sales, purchases, returns, receipts, and payments. These entries are then used to create ledger accounts, which are summarized in an income statement and a statement of financial position. The assignment also includes a trial balance to ensure the accuracy of the accounting process. Furthermore, it explores the importance of asset reporting and the differences between cash flow and profit. The report concludes with an analysis of the financial data, providing insights into Corr's financial performance and position. The document covers various aspects of accounting like tangible and intangible assets, current and fixed assets. The assignment also explains the causes of differences in cash accounts and profit.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.