Financial Accounting for Corr: Financial Statements and Concepts

VerifiedAdded on 2019/12/17

|14

|4333

|109

Homework Assignment

AI Summary

This assignment focuses on the financial accounting practices of Corr, a sole trader, and the application of accounting principles. The student prepared journal entries, ledgers, a trial balance, an income statement, and a balance sheet for Corr. The assignment also assesses the usefulness of financial information, specifically examining assets, liabilities, and equity, by analyzing Domino's Pizza's annual accounts. Furthermore, it explores the application of accounting concepts such as prudence and accruals in constructing financial statements. The solution demonstrates the student's understanding of financial statement preparation and the importance of accounting principles in financial reporting.

Introduction to financial accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................3

Preparation of accounting records and financial statements for Corr, a sole trader........................3

Final account with adjustments........................................................................................................8

Explain the usefulness of information provided on assets, liabilities and equity............................9

Explain the prudence concept and accruals concept and assessing its application for Domino

Pizza...............................................................................................................................................11

CONCLUSION..................................................................................................................................12

REFERENCES...................................................................................................................................13

2

INTRODUCTION................................................................................................................................3

Preparation of accounting records and financial statements for Corr, a sole trader........................3

Final account with adjustments........................................................................................................8

Explain the usefulness of information provided on assets, liabilities and equity............................9

Explain the prudence concept and accruals concept and assessing its application for Domino

Pizza...............................................................................................................................................11

CONCLUSION..................................................................................................................................12

REFERENCES...................................................................................................................................13

2

INTRODUCTION

The art of recording, classifying, summarizing and interpreting or evaluating monetary

transaction of an enterprise is called financial accounting. It is regarded as the process of keeping

systematic records so as to ascertain business profitability and financial position at the end of

accounting year. It is very important for the managers in order to make proficient and accurate

decisions to reach success in the future. The aim of the present assignment is to prepare journal,

ledger, trial balance, income statement and balance sheet for Corr, a furniture merchandiser. In

addition to this, report will also lay emphasizes on assessing the usefulness of information reported

in Domino Pizza’s annual accounts such as assets, liabilities and equity. Furthermore, companies

prepare all the necessary accounts by complying with several concepts such as accrual, prudence

and so on. Henceforth, the report will guide the accounting principles and concepts for constructing

annual accounts.

Preparation of accounting records and financial statements for Corr, a sole trader

As per the scenario, Corr is a small sole proprietor who kept accounting records for the first

11 month ending on 31st August 2016. Its financial statement can be prepared by using following

steps, enumerated hereunder:

Journal: At the beginning stage, every monetary transaction needs to be record in journal

following dual accounting concept. It states that each transaction must be recorded in both the debit

and credit side complying with the accounting rules of personal, real and nominal accounts.

Ledger: It classify all the transactions into sub-parts, every ledger summarizes all the

transactions associated with a given element.

Trial balance: It consolidates results of all the ledger accounts either by balance or total

balance. In the former, only balance is reported in trial balance whereas later method report total of

both the debit and credit into trial balance.

Income statement: It report about total revenues and expenditures incurred by Corr in a

given duration prepared to determine net operational results either profit or loss. This statement has

two sides such as income and expenses. It provides deeper insight about the revenue generated by

the firm during the accounting year over the expenses. Income side of profitability statement

renders information about dividend and interest received during the year. On the other side,

expenses include electricity, miscellaneous expenses etc. Hence, by preparing the income statement

business unit can assess its profitability aspect.

3

The art of recording, classifying, summarizing and interpreting or evaluating monetary

transaction of an enterprise is called financial accounting. It is regarded as the process of keeping

systematic records so as to ascertain business profitability and financial position at the end of

accounting year. It is very important for the managers in order to make proficient and accurate

decisions to reach success in the future. The aim of the present assignment is to prepare journal,

ledger, trial balance, income statement and balance sheet for Corr, a furniture merchandiser. In

addition to this, report will also lay emphasizes on assessing the usefulness of information reported

in Domino Pizza’s annual accounts such as assets, liabilities and equity. Furthermore, companies

prepare all the necessary accounts by complying with several concepts such as accrual, prudence

and so on. Henceforth, the report will guide the accounting principles and concepts for constructing

annual accounts.

Preparation of accounting records and financial statements for Corr, a sole trader

As per the scenario, Corr is a small sole proprietor who kept accounting records for the first

11 month ending on 31st August 2016. Its financial statement can be prepared by using following

steps, enumerated hereunder:

Journal: At the beginning stage, every monetary transaction needs to be record in journal

following dual accounting concept. It states that each transaction must be recorded in both the debit

and credit side complying with the accounting rules of personal, real and nominal accounts.

Ledger: It classify all the transactions into sub-parts, every ledger summarizes all the

transactions associated with a given element.

Trial balance: It consolidates results of all the ledger accounts either by balance or total

balance. In the former, only balance is reported in trial balance whereas later method report total of

both the debit and credit into trial balance.

Income statement: It report about total revenues and expenditures incurred by Corr in a

given duration prepared to determine net operational results either profit or loss. This statement has

two sides such as income and expenses. It provides deeper insight about the revenue generated by

the firm during the accounting year over the expenses. Income side of profitability statement

renders information about dividend and interest received during the year. On the other side,

expenses include electricity, miscellaneous expenses etc. Hence, by preparing the income statement

business unit can assess its profitability aspect.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

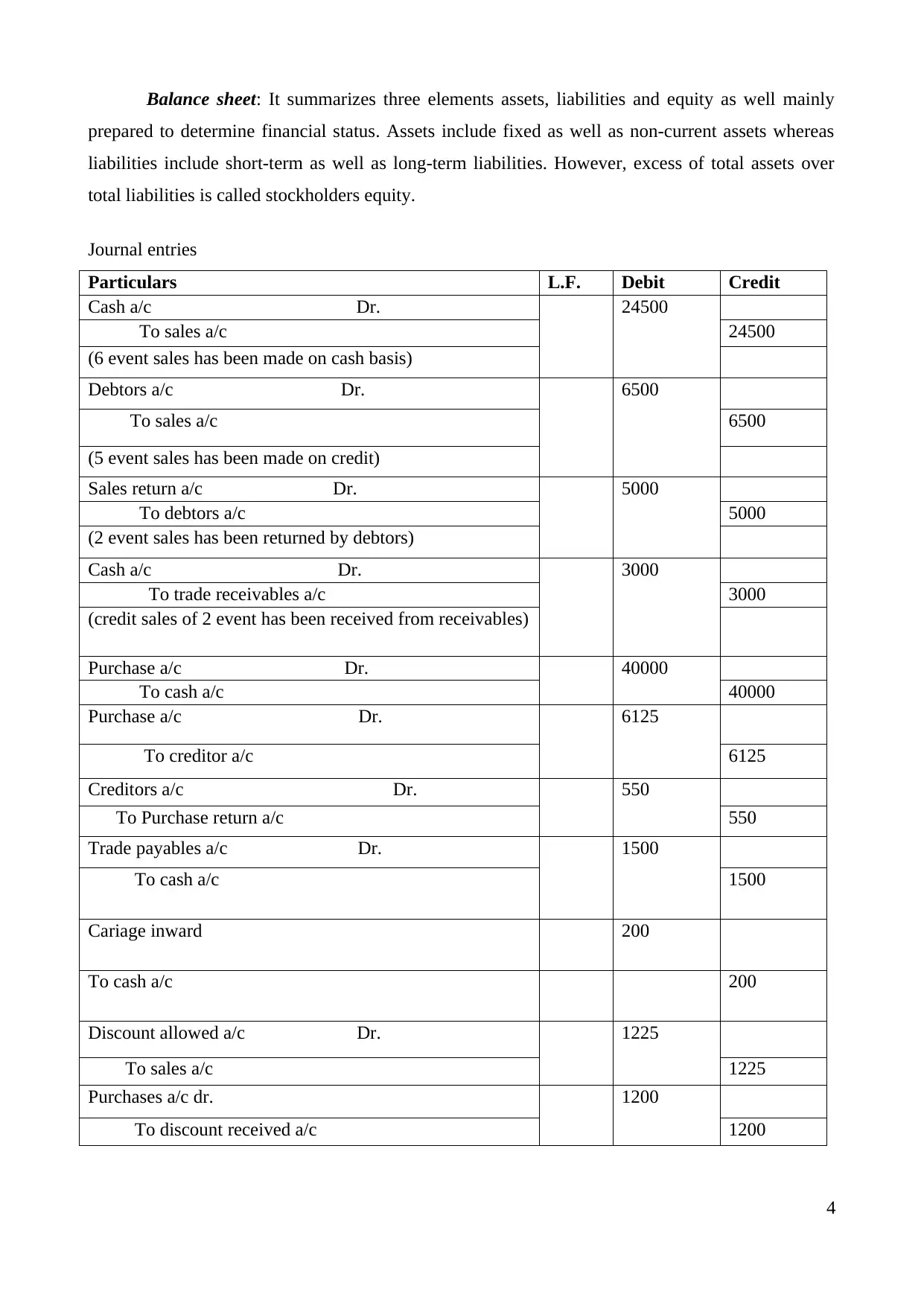

Balance sheet: It summarizes three elements assets, liabilities and equity as well mainly

prepared to determine financial status. Assets include fixed as well as non-current assets whereas

liabilities include short-term as well as long-term liabilities. However, excess of total assets over

total liabilities is called stockholders equity.

Journal entries

Particulars L.F. Debit Credit

Cash a/c Dr. 24500

To sales a/c 24500

(6 event sales has been made on cash basis)

Debtors a/c Dr. 6500

To sales a/c 6500

(5 event sales has been made on credit)

Sales return a/c Dr. 5000

To debtors a/c 5000

(2 event sales has been returned by debtors)

Cash a/c Dr. 3000

To trade receivables a/c 3000

(credit sales of 2 event has been received from receivables)

Purchase a/c Dr. 40000

To cash a/c 40000

Purchase a/c Dr. 6125

To creditor a/c 6125

Creditors a/c Dr. 550

To Purchase return a/c 550

Trade payables a/c Dr. 1500

To cash a/c 1500

Cariage inward 200

To cash a/c 200

Discount allowed a/c Dr. 1225

To sales a/c 1225

Purchases a/c dr. 1200

To discount received a/c 1200

4

prepared to determine financial status. Assets include fixed as well as non-current assets whereas

liabilities include short-term as well as long-term liabilities. However, excess of total assets over

total liabilities is called stockholders equity.

Journal entries

Particulars L.F. Debit Credit

Cash a/c Dr. 24500

To sales a/c 24500

(6 event sales has been made on cash basis)

Debtors a/c Dr. 6500

To sales a/c 6500

(5 event sales has been made on credit)

Sales return a/c Dr. 5000

To debtors a/c 5000

(2 event sales has been returned by debtors)

Cash a/c Dr. 3000

To trade receivables a/c 3000

(credit sales of 2 event has been received from receivables)

Purchase a/c Dr. 40000

To cash a/c 40000

Purchase a/c Dr. 6125

To creditor a/c 6125

Creditors a/c Dr. 550

To Purchase return a/c 550

Trade payables a/c Dr. 1500

To cash a/c 1500

Cariage inward 200

To cash a/c 200

Discount allowed a/c Dr. 1225

To sales a/c 1225

Purchases a/c dr. 1200

To discount received a/c 1200

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

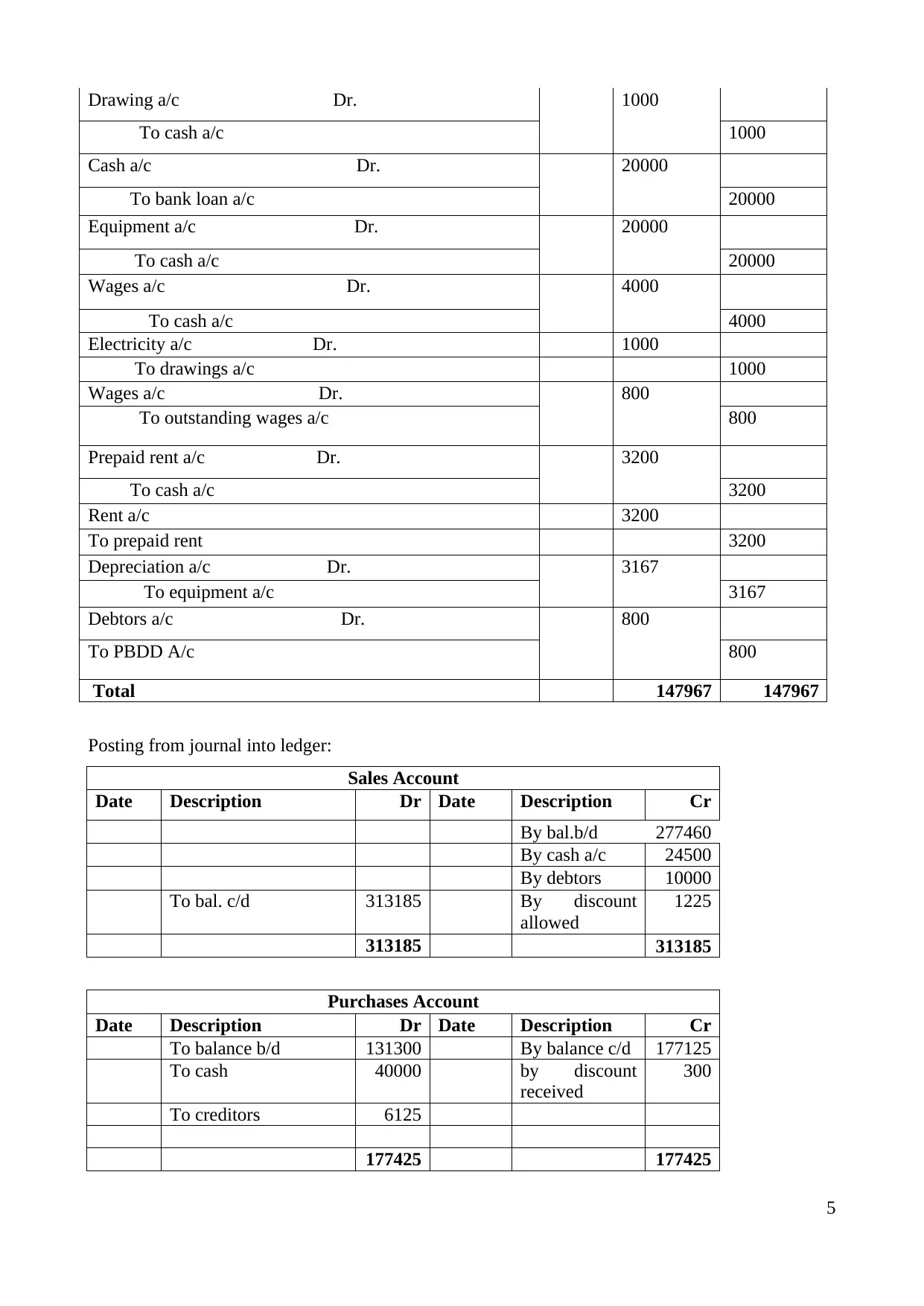

Drawing a/c Dr. 1000

To cash a/c 1000

Cash a/c Dr. 20000

To bank loan a/c 20000

Equipment a/c Dr. 20000

To cash a/c 20000

Wages a/c Dr. 4000

To cash a/c 4000

Electricity a/c Dr. 1000

To drawings a/c 1000

Wages a/c Dr. 800

To outstanding wages a/c 800

Prepaid rent a/c Dr. 3200

To cash a/c 3200

Rent a/c 3200

To prepaid rent 3200

Depreciation a/c Dr. 3167

To equipment a/c 3167

Debtors a/c Dr. 800

To PBDD A/c 800

Total 147967 147967

Posting from journal into ledger:

Sales Account

Date Description Dr Date Description Cr

By bal.b/d 277460

By cash a/c 24500

By debtors 10000

To bal. c/d 313185 By discount

allowed

1225

313185 313185

Purchases Account

Date Description Dr Date Description Cr

To balance b/d 131300 By balance c/d 177125

To cash 40000 by discount

received

300

To creditors 6125

177425 177425

5

To cash a/c 1000

Cash a/c Dr. 20000

To bank loan a/c 20000

Equipment a/c Dr. 20000

To cash a/c 20000

Wages a/c Dr. 4000

To cash a/c 4000

Electricity a/c Dr. 1000

To drawings a/c 1000

Wages a/c Dr. 800

To outstanding wages a/c 800

Prepaid rent a/c Dr. 3200

To cash a/c 3200

Rent a/c 3200

To prepaid rent 3200

Depreciation a/c Dr. 3167

To equipment a/c 3167

Debtors a/c Dr. 800

To PBDD A/c 800

Total 147967 147967

Posting from journal into ledger:

Sales Account

Date Description Dr Date Description Cr

By bal.b/d 277460

By cash a/c 24500

By debtors 10000

To bal. c/d 313185 By discount

allowed

1225

313185 313185

Purchases Account

Date Description Dr Date Description Cr

To balance b/d 131300 By balance c/d 177125

To cash 40000 by discount

received

300

To creditors 6125

177425 177425

5

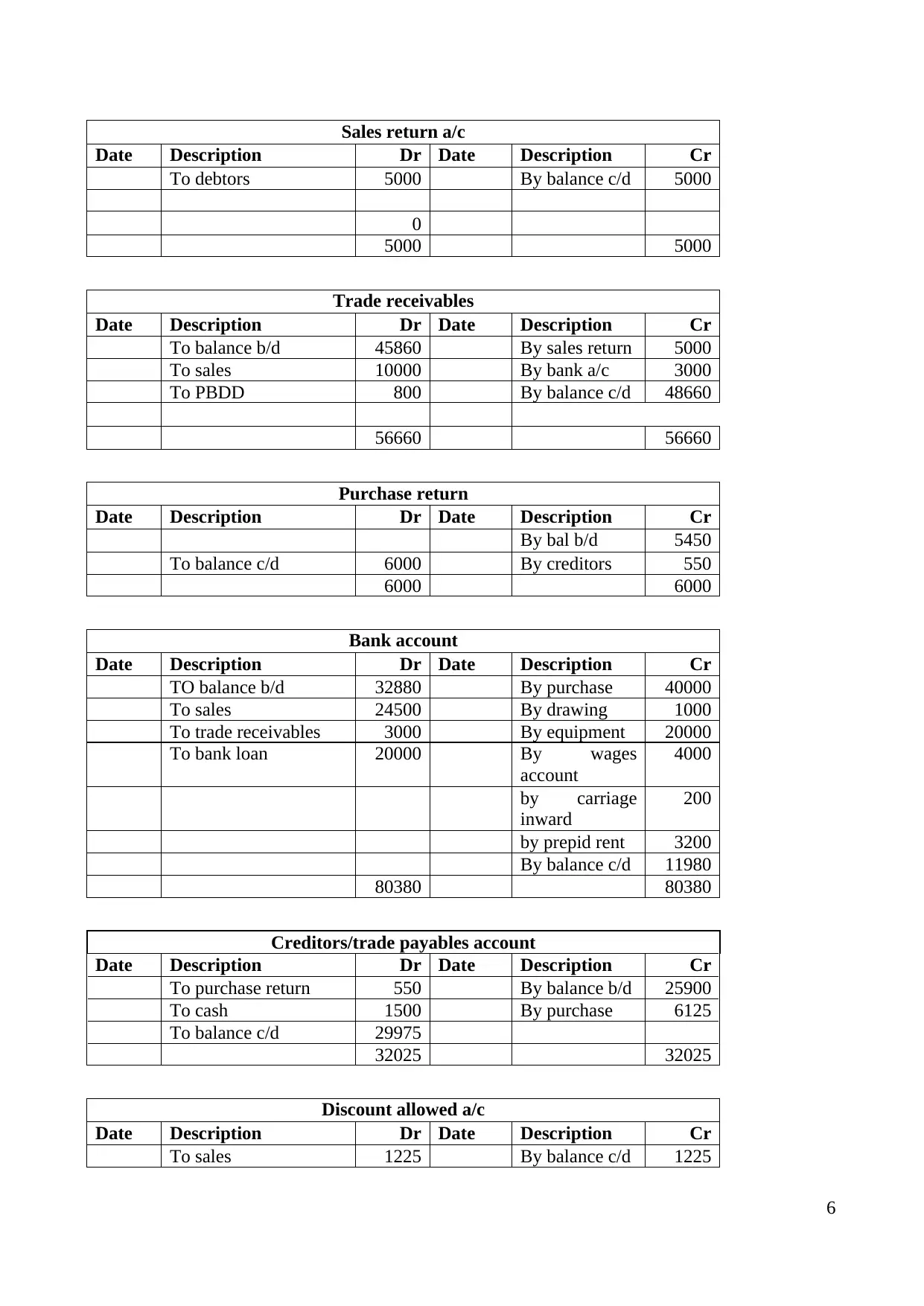

Sales return a/c

Date Description Dr Date Description Cr

To debtors 5000 By balance c/d 5000

0

5000 5000

Trade receivables

Date Description Dr Date Description Cr

To balance b/d 45860 By sales return 5000

To sales 10000 By bank a/c 3000

To PBDD 800 By balance c/d 48660

56660 56660

Purchase return

Date Description Dr Date Description Cr

By bal b/d 5450

To balance c/d 6000 By creditors 550

6000 6000

Bank account

Date Description Dr Date Description Cr

TO balance b/d 32880 By purchase 40000

To sales 24500 By drawing 1000

To trade receivables 3000 By equipment 20000

To bank loan 20000 By wages

account

4000

by carriage

inward

200

by prepid rent 3200

By balance c/d 11980

80380 80380

Creditors/trade payables account

Date Description Dr Date Description Cr

To purchase return 550 By balance b/d 25900

To cash 1500 By purchase 6125

To balance c/d 29975

32025 32025

Discount allowed a/c

Date Description Dr Date Description Cr

To sales 1225 By balance c/d 1225

6

Date Description Dr Date Description Cr

To debtors 5000 By balance c/d 5000

0

5000 5000

Trade receivables

Date Description Dr Date Description Cr

To balance b/d 45860 By sales return 5000

To sales 10000 By bank a/c 3000

To PBDD 800 By balance c/d 48660

56660 56660

Purchase return

Date Description Dr Date Description Cr

By bal b/d 5450

To balance c/d 6000 By creditors 550

6000 6000

Bank account

Date Description Dr Date Description Cr

TO balance b/d 32880 By purchase 40000

To sales 24500 By drawing 1000

To trade receivables 3000 By equipment 20000

To bank loan 20000 By wages

account

4000

by carriage

inward

200

by prepid rent 3200

By balance c/d 11980

80380 80380

Creditors/trade payables account

Date Description Dr Date Description Cr

To purchase return 550 By balance b/d 25900

To cash 1500 By purchase 6125

To balance c/d 29975

32025 32025

Discount allowed a/c

Date Description Dr Date Description Cr

To sales 1225 By balance c/d 1225

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

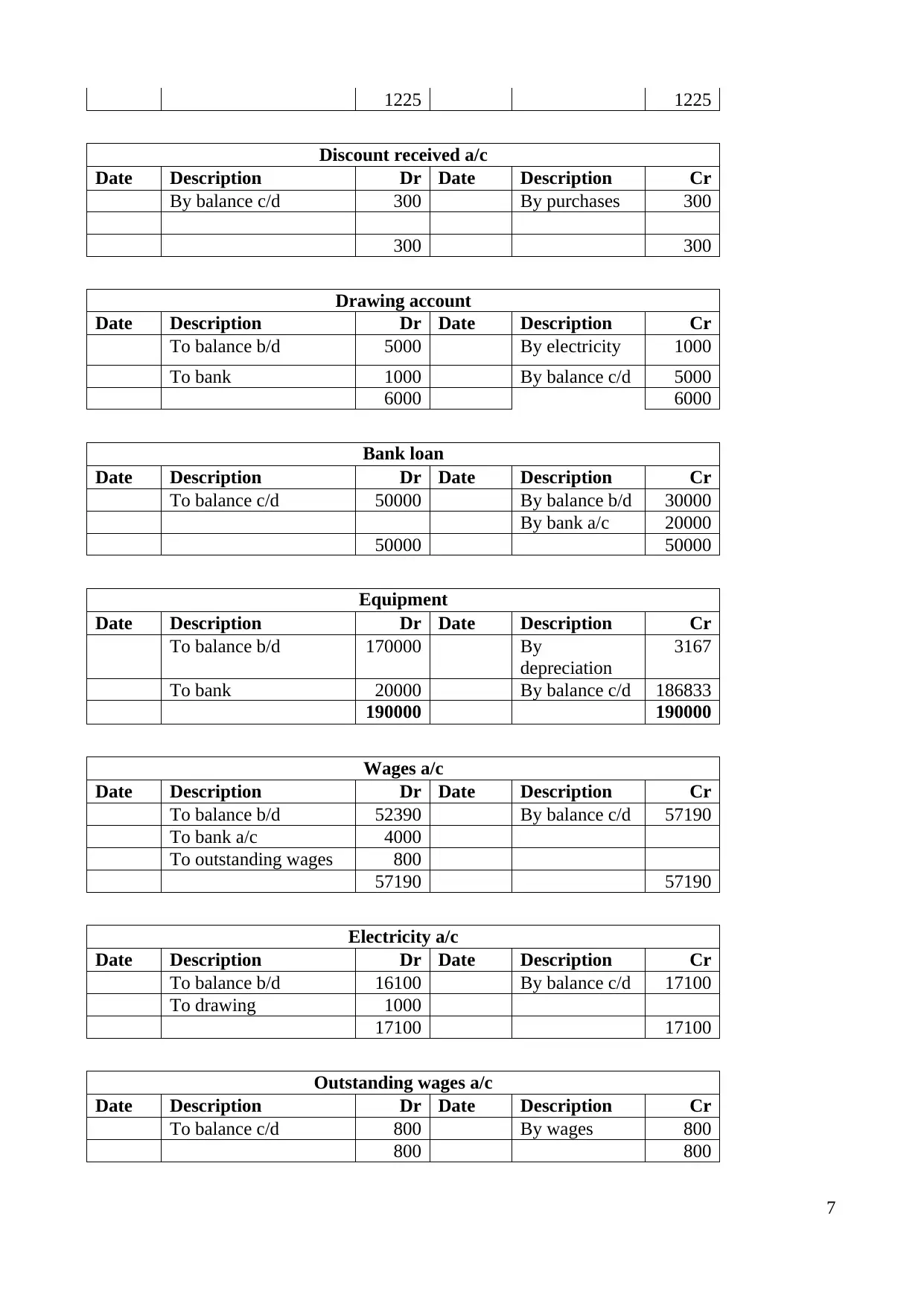

1225 1225

Discount received a/c

Date Description Dr Date Description Cr

By balance c/d 300 By purchases 300

300 300

Drawing account

Date Description Dr Date Description Cr

To balance b/d 5000 By electricity 1000

To bank 1000 By balance c/d 5000

6000 6000

Bank loan

Date Description Dr Date Description Cr

To balance c/d 50000 By balance b/d 30000

By bank a/c 20000

50000 50000

Equipment

Date Description Dr Date Description Cr

To balance b/d 170000 By

depreciation

3167

To bank 20000 By balance c/d 186833

190000 190000

Wages a/c

Date Description Dr Date Description Cr

To balance b/d 52390 By balance c/d 57190

To bank a/c 4000

To outstanding wages 800

57190 57190

Electricity a/c

Date Description Dr Date Description Cr

To balance b/d 16100 By balance c/d 17100

To drawing 1000

17100 17100

Outstanding wages a/c

Date Description Dr Date Description Cr

To balance c/d 800 By wages 800

800 800

7

Discount received a/c

Date Description Dr Date Description Cr

By balance c/d 300 By purchases 300

300 300

Drawing account

Date Description Dr Date Description Cr

To balance b/d 5000 By electricity 1000

To bank 1000 By balance c/d 5000

6000 6000

Bank loan

Date Description Dr Date Description Cr

To balance c/d 50000 By balance b/d 30000

By bank a/c 20000

50000 50000

Equipment

Date Description Dr Date Description Cr

To balance b/d 170000 By

depreciation

3167

To bank 20000 By balance c/d 186833

190000 190000

Wages a/c

Date Description Dr Date Description Cr

To balance b/d 52390 By balance c/d 57190

To bank a/c 4000

To outstanding wages 800

57190 57190

Electricity a/c

Date Description Dr Date Description Cr

To balance b/d 16100 By balance c/d 17100

To drawing 1000

17100 17100

Outstanding wages a/c

Date Description Dr Date Description Cr

To balance c/d 800 By wages 800

800 800

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

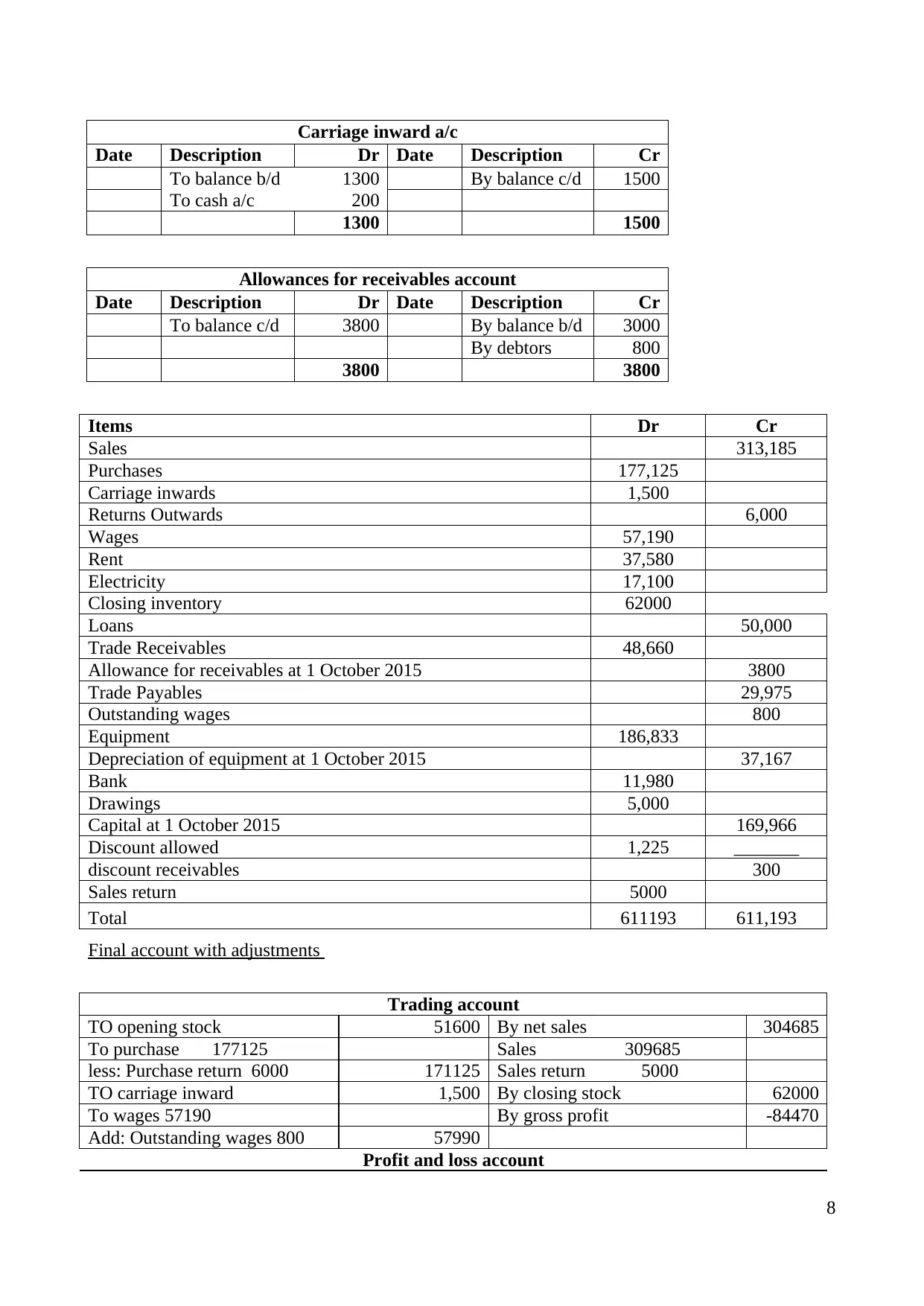

Carriage inward a/c

Date Description Dr Date Description Cr

To balance b/d 1300 By balance c/d 1500

To cash a/c 200

1300 1500

Allowances for receivables account

Date Description Dr Date Description Cr

To balance c/d 3800 By balance b/d 3000

By debtors 800

3800 3800

Items Dr Cr

Sales 313,185

Purchases 177,125

Carriage inwards 1,500

Returns Outwards 6,000

Wages 57,190

Rent 37,580

Electricity 17,100

Closing inventory 62000

Loans 50,000

Trade Receivables 48,660

Allowance for receivables at 1 October 2015 3800

Trade Payables 29,975

Outstanding wages 800

Equipment 186,833

Depreciation of equipment at 1 October 2015 37,167

Bank 11,980

Drawings 5,000

Capital at 1 October 2015 169,966

Discount allowed 1,225 _______

discount receivables 300

Sales return 5000

Total 611193 611,193

Final account with adjustments

Trading account

TO opening stock 51600 By net sales 304685

To purchase 177125 Sales 309685

less: Purchase return 6000 171125 Sales return 5000

TO carriage inward 1,500 By closing stock 62000

To wages 57190 By gross profit -84470

Add: Outstanding wages 800 57990

Profit and loss account

8

Date Description Dr Date Description Cr

To balance b/d 1300 By balance c/d 1500

To cash a/c 200

1300 1500

Allowances for receivables account

Date Description Dr Date Description Cr

To balance c/d 3800 By balance b/d 3000

By debtors 800

3800 3800

Items Dr Cr

Sales 313,185

Purchases 177,125

Carriage inwards 1,500

Returns Outwards 6,000

Wages 57,190

Rent 37,580

Electricity 17,100

Closing inventory 62000

Loans 50,000

Trade Receivables 48,660

Allowance for receivables at 1 October 2015 3800

Trade Payables 29,975

Outstanding wages 800

Equipment 186,833

Depreciation of equipment at 1 October 2015 37,167

Bank 11,980

Drawings 5,000

Capital at 1 October 2015 169,966

Discount allowed 1,225 _______

discount receivables 300

Sales return 5000

Total 611193 611,193

Final account with adjustments

Trading account

TO opening stock 51600 By net sales 304685

To purchase 177125 Sales 309685

less: Purchase return 6000 171125 Sales return 5000

TO carriage inward 1,500 By closing stock 62000

To wages 57190 By gross profit -84470

Add: Outstanding wages 800 57990

Profit and loss account

8

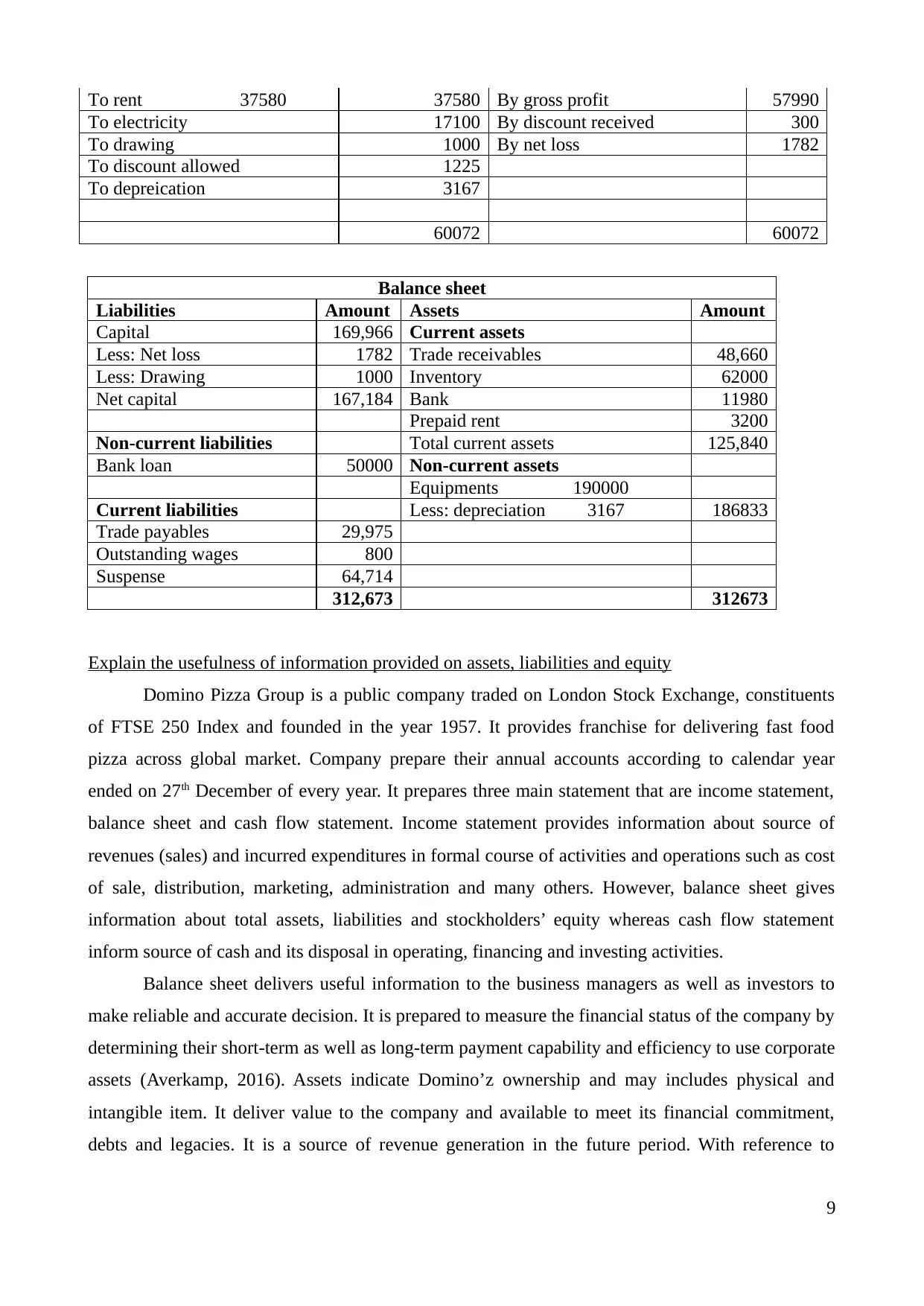

To rent 37580 37580 By gross profit 57990

To electricity 17100 By discount received 300

To drawing 1000 By net loss 1782

To discount allowed 1225

To depreication 3167

60072 60072

Balance sheet

Liabilities Amount Assets Amount

Capital 169,966 Current assets

Less: Net loss 1782 Trade receivables 48,660

Less: Drawing 1000 Inventory 62000

Net capital 167,184 Bank 11980

Prepaid rent 3200

Non-current liabilities Total current assets 125,840

Bank loan 50000 Non-current assets

Equipments 190000

Current liabilities Less: depreciation 3167 186833

Trade payables 29,975

Outstanding wages 800

Suspense 64,714

312,673 312673

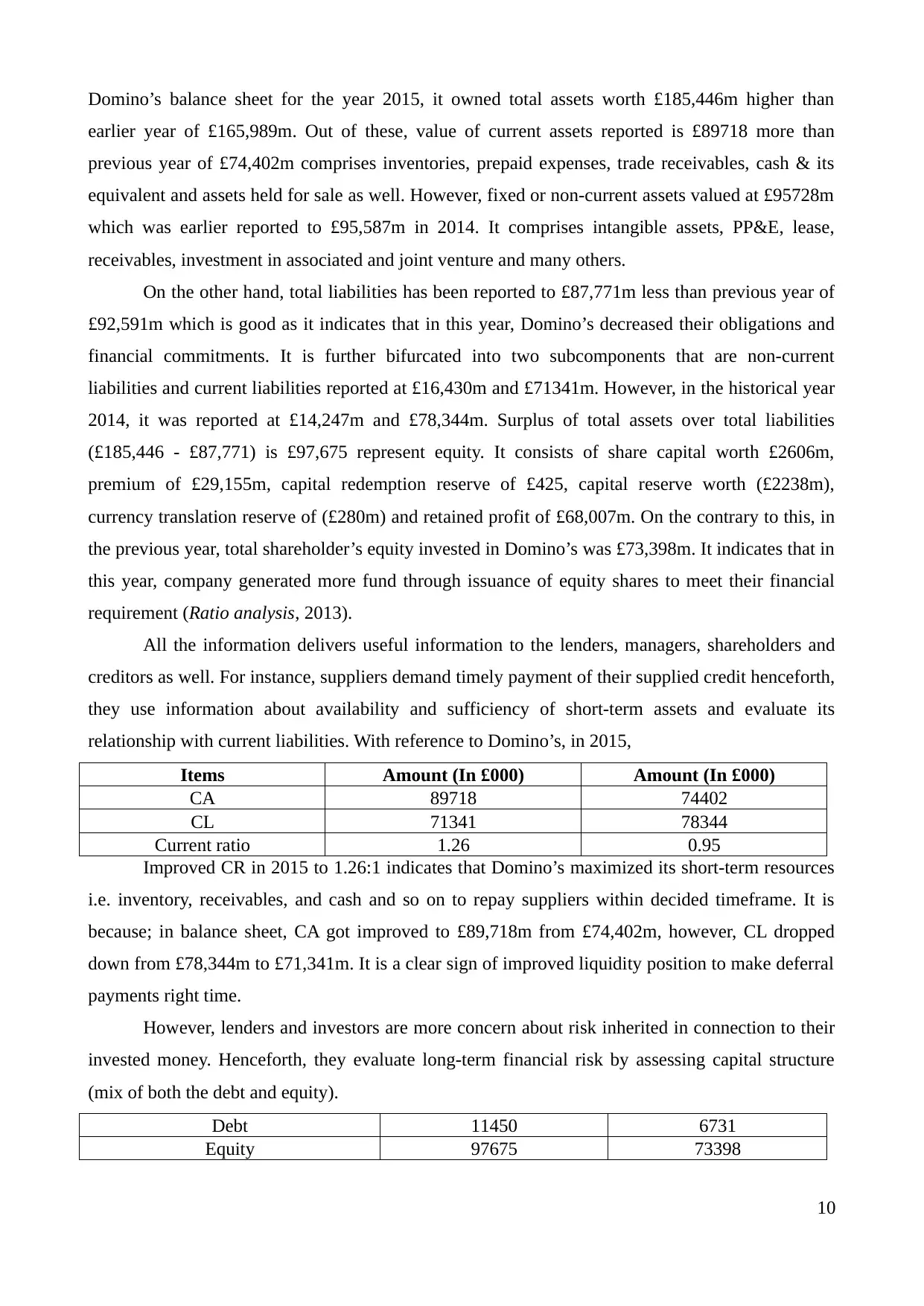

Explain the usefulness of information provided on assets, liabilities and equity

Domino Pizza Group is a public company traded on London Stock Exchange, constituents

of FTSE 250 Index and founded in the year 1957. It provides franchise for delivering fast food

pizza across global market. Company prepare their annual accounts according to calendar year

ended on 27th December of every year. It prepares three main statement that are income statement,

balance sheet and cash flow statement. Income statement provides information about source of

revenues (sales) and incurred expenditures in formal course of activities and operations such as cost

of sale, distribution, marketing, administration and many others. However, balance sheet gives

information about total assets, liabilities and stockholders’ equity whereas cash flow statement

inform source of cash and its disposal in operating, financing and investing activities.

Balance sheet delivers useful information to the business managers as well as investors to

make reliable and accurate decision. It is prepared to measure the financial status of the company by

determining their short-term as well as long-term payment capability and efficiency to use corporate

assets (Averkamp, 2016). Assets indicate Domino’z ownership and may includes physical and

intangible item. It deliver value to the company and available to meet its financial commitment,

debts and legacies. It is a source of revenue generation in the future period. With reference to

9

To electricity 17100 By discount received 300

To drawing 1000 By net loss 1782

To discount allowed 1225

To depreication 3167

60072 60072

Balance sheet

Liabilities Amount Assets Amount

Capital 169,966 Current assets

Less: Net loss 1782 Trade receivables 48,660

Less: Drawing 1000 Inventory 62000

Net capital 167,184 Bank 11980

Prepaid rent 3200

Non-current liabilities Total current assets 125,840

Bank loan 50000 Non-current assets

Equipments 190000

Current liabilities Less: depreciation 3167 186833

Trade payables 29,975

Outstanding wages 800

Suspense 64,714

312,673 312673

Explain the usefulness of information provided on assets, liabilities and equity

Domino Pizza Group is a public company traded on London Stock Exchange, constituents

of FTSE 250 Index and founded in the year 1957. It provides franchise for delivering fast food

pizza across global market. Company prepare their annual accounts according to calendar year

ended on 27th December of every year. It prepares three main statement that are income statement,

balance sheet and cash flow statement. Income statement provides information about source of

revenues (sales) and incurred expenditures in formal course of activities and operations such as cost

of sale, distribution, marketing, administration and many others. However, balance sheet gives

information about total assets, liabilities and stockholders’ equity whereas cash flow statement

inform source of cash and its disposal in operating, financing and investing activities.

Balance sheet delivers useful information to the business managers as well as investors to

make reliable and accurate decision. It is prepared to measure the financial status of the company by

determining their short-term as well as long-term payment capability and efficiency to use corporate

assets (Averkamp, 2016). Assets indicate Domino’z ownership and may includes physical and

intangible item. It deliver value to the company and available to meet its financial commitment,

debts and legacies. It is a source of revenue generation in the future period. With reference to

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

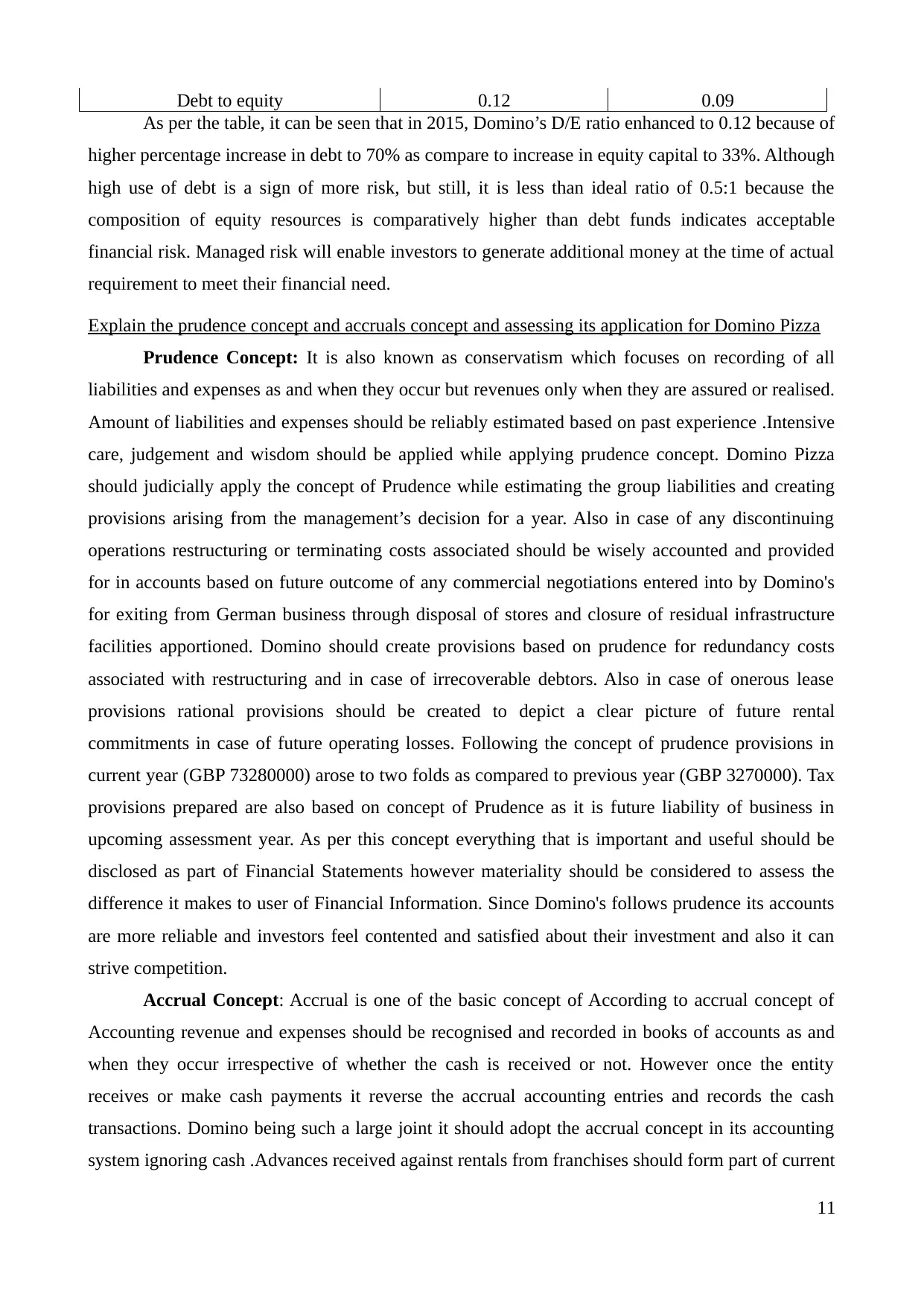

Domino’s balance sheet for the year 2015, it owned total assets worth £185,446m higher than

earlier year of £165,989m. Out of these, value of current assets reported is £89718 more than

previous year of £74,402m comprises inventories, prepaid expenses, trade receivables, cash & its

equivalent and assets held for sale as well. However, fixed or non-current assets valued at £95728m

which was earlier reported to £95,587m in 2014. It comprises intangible assets, PP&E, lease,

receivables, investment in associated and joint venture and many others.

On the other hand, total liabilities has been reported to £87,771m less than previous year of

£92,591m which is good as it indicates that in this year, Domino’s decreased their obligations and

financial commitments. It is further bifurcated into two subcomponents that are non-current

liabilities and current liabilities reported at £16,430m and £71341m. However, in the historical year

2014, it was reported at £14,247m and £78,344m. Surplus of total assets over total liabilities

(£185,446 - £87,771) is £97,675 represent equity. It consists of share capital worth £2606m,

premium of £29,155m, capital redemption reserve of £425, capital reserve worth (£2238m),

currency translation reserve of (£280m) and retained profit of £68,007m. On the contrary to this, in

the previous year, total shareholder’s equity invested in Domino’s was £73,398m. It indicates that in

this year, company generated more fund through issuance of equity shares to meet their financial

requirement (Ratio analysis, 2013).

All the information delivers useful information to the lenders, managers, shareholders and

creditors as well. For instance, suppliers demand timely payment of their supplied credit henceforth,

they use information about availability and sufficiency of short-term assets and evaluate its

relationship with current liabilities. With reference to Domino’s, in 2015,

Items Amount (In £000) Amount (In £000)

CA 89718 74402

CL 71341 78344

Current ratio 1.26 0.95

Improved CR in 2015 to 1.26:1 indicates that Domino’s maximized its short-term resources

i.e. inventory, receivables, and cash and so on to repay suppliers within decided timeframe. It is

because; in balance sheet, CA got improved to £89,718m from £74,402m, however, CL dropped

down from £78,344m to £71,341m. It is a clear sign of improved liquidity position to make deferral

payments right time.

However, lenders and investors are more concern about risk inherited in connection to their

invested money. Henceforth, they evaluate long-term financial risk by assessing capital structure

(mix of both the debt and equity).

Debt 11450 6731

Equity 97675 73398

10

earlier year of £165,989m. Out of these, value of current assets reported is £89718 more than

previous year of £74,402m comprises inventories, prepaid expenses, trade receivables, cash & its

equivalent and assets held for sale as well. However, fixed or non-current assets valued at £95728m

which was earlier reported to £95,587m in 2014. It comprises intangible assets, PP&E, lease,

receivables, investment in associated and joint venture and many others.

On the other hand, total liabilities has been reported to £87,771m less than previous year of

£92,591m which is good as it indicates that in this year, Domino’s decreased their obligations and

financial commitments. It is further bifurcated into two subcomponents that are non-current

liabilities and current liabilities reported at £16,430m and £71341m. However, in the historical year

2014, it was reported at £14,247m and £78,344m. Surplus of total assets over total liabilities

(£185,446 - £87,771) is £97,675 represent equity. It consists of share capital worth £2606m,

premium of £29,155m, capital redemption reserve of £425, capital reserve worth (£2238m),

currency translation reserve of (£280m) and retained profit of £68,007m. On the contrary to this, in

the previous year, total shareholder’s equity invested in Domino’s was £73,398m. It indicates that in

this year, company generated more fund through issuance of equity shares to meet their financial

requirement (Ratio analysis, 2013).

All the information delivers useful information to the lenders, managers, shareholders and

creditors as well. For instance, suppliers demand timely payment of their supplied credit henceforth,

they use information about availability and sufficiency of short-term assets and evaluate its

relationship with current liabilities. With reference to Domino’s, in 2015,

Items Amount (In £000) Amount (In £000)

CA 89718 74402

CL 71341 78344

Current ratio 1.26 0.95

Improved CR in 2015 to 1.26:1 indicates that Domino’s maximized its short-term resources

i.e. inventory, receivables, and cash and so on to repay suppliers within decided timeframe. It is

because; in balance sheet, CA got improved to £89,718m from £74,402m, however, CL dropped

down from £78,344m to £71,341m. It is a clear sign of improved liquidity position to make deferral

payments right time.

However, lenders and investors are more concern about risk inherited in connection to their

invested money. Henceforth, they evaluate long-term financial risk by assessing capital structure

(mix of both the debt and equity).

Debt 11450 6731

Equity 97675 73398

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Debt to equity 0.12 0.09

As per the table, it can be seen that in 2015, Domino’s D/E ratio enhanced to 0.12 because of

higher percentage increase in debt to 70% as compare to increase in equity capital to 33%. Although

high use of debt is a sign of more risk, but still, it is less than ideal ratio of 0.5:1 because the

composition of equity resources is comparatively higher than debt funds indicates acceptable

financial risk. Managed risk will enable investors to generate additional money at the time of actual

requirement to meet their financial need.

Explain the prudence concept and accruals concept and assessing its application for Domino Pizza

Prudence Concept: It is also known as conservatism which focuses on recording of all

liabilities and expenses as and when they occur but revenues only when they are assured or realised.

Amount of liabilities and expenses should be reliably estimated based on past experience .Intensive

care, judgement and wisdom should be applied while applying prudence concept. Domino Pizza

should judicially apply the concept of Prudence while estimating the group liabilities and creating

provisions arising from the management’s decision for a year. Also in case of any discontinuing

operations restructuring or terminating costs associated should be wisely accounted and provided

for in accounts based on future outcome of any commercial negotiations entered into by Domino's

for exiting from German business through disposal of stores and closure of residual infrastructure

facilities apportioned. Domino should create provisions based on prudence for redundancy costs

associated with restructuring and in case of irrecoverable debtors. Also in case of onerous lease

provisions rational provisions should be created to depict a clear picture of future rental

commitments in case of future operating losses. Following the concept of prudence provisions in

current year (GBP 73280000) arose to two folds as compared to previous year (GBP 3270000). Tax

provisions prepared are also based on concept of Prudence as it is future liability of business in

upcoming assessment year. As per this concept everything that is important and useful should be

disclosed as part of Financial Statements however materiality should be considered to assess the

difference it makes to user of Financial Information. Since Domino's follows prudence its accounts

are more reliable and investors feel contented and satisfied about their investment and also it can

strive competition.

Accrual Concept: Accrual is one of the basic concept of According to accrual concept of

Accounting revenue and expenses should be recognised and recorded in books of accounts as and

when they occur irrespective of whether the cash is received or not. However once the entity

receives or make cash payments it reverse the accrual accounting entries and records the cash

transactions. Domino being such a large joint it should adopt the accrual concept in its accounting

system ignoring cash .Advances received against rentals from franchises should form part of current

11

As per the table, it can be seen that in 2015, Domino’s D/E ratio enhanced to 0.12 because of

higher percentage increase in debt to 70% as compare to increase in equity capital to 33%. Although

high use of debt is a sign of more risk, but still, it is less than ideal ratio of 0.5:1 because the

composition of equity resources is comparatively higher than debt funds indicates acceptable

financial risk. Managed risk will enable investors to generate additional money at the time of actual

requirement to meet their financial need.

Explain the prudence concept and accruals concept and assessing its application for Domino Pizza

Prudence Concept: It is also known as conservatism which focuses on recording of all

liabilities and expenses as and when they occur but revenues only when they are assured or realised.

Amount of liabilities and expenses should be reliably estimated based on past experience .Intensive

care, judgement and wisdom should be applied while applying prudence concept. Domino Pizza

should judicially apply the concept of Prudence while estimating the group liabilities and creating

provisions arising from the management’s decision for a year. Also in case of any discontinuing

operations restructuring or terminating costs associated should be wisely accounted and provided

for in accounts based on future outcome of any commercial negotiations entered into by Domino's

for exiting from German business through disposal of stores and closure of residual infrastructure

facilities apportioned. Domino should create provisions based on prudence for redundancy costs

associated with restructuring and in case of irrecoverable debtors. Also in case of onerous lease

provisions rational provisions should be created to depict a clear picture of future rental

commitments in case of future operating losses. Following the concept of prudence provisions in

current year (GBP 73280000) arose to two folds as compared to previous year (GBP 3270000). Tax

provisions prepared are also based on concept of Prudence as it is future liability of business in

upcoming assessment year. As per this concept everything that is important and useful should be

disclosed as part of Financial Statements however materiality should be considered to assess the

difference it makes to user of Financial Information. Since Domino's follows prudence its accounts

are more reliable and investors feel contented and satisfied about their investment and also it can

strive competition.

Accrual Concept: Accrual is one of the basic concept of According to accrual concept of

Accounting revenue and expenses should be recognised and recorded in books of accounts as and

when they occur irrespective of whether the cash is received or not. However once the entity

receives or make cash payments it reverse the accrual accounting entries and records the cash

transactions. Domino being such a large joint it should adopt the accrual concept in its accounting

system ignoring cash .Advances received against rentals from franchises should form part of current

11

period as cash received in advance related to current year should form part of financial statements

of relevant period. Accrual concept should be used by Domino's even in statutory dues such as

pension payments, royalties, franchise fees, rental income and also franchisee rebates should be

recognised on accrual basis on expected entitlement which has been earned up to the balance sheet

date. Following a accrual concept of accounting it gives Domino's a advantage that the financial

statements reflect all the expenses associated with related revenues for a particular accounting

period which depicts a clear picture to investors and potential investors who rely on financial

information to generate best outcome of their investments. Domino's being largely into retail

business do not promote or accept credit for their products delivered to customers therefore accrual

is necessary to be followed n every transaction an organisation undertakes. As and when the invoice

is sent to customer transaction is to be recorded by Domino whether the cash is immediately

received or not. It will help management to make better decisions Accrual should always be used in

combination with various other accounting policies. It ensures that Financial statements fairly

present the each year's activity with the help of matching concept of revenues and related expenses.

Profits generated for Domino's are mixture of both cash as well as accrual transaction entered into.

CONCLUSION

From the above report, it has been concluded that financial reports provide deeper insight to

stakeholders about the financial health and performance of an organization. Besides this, it can be

inferred from the report that accounting principles and concepts help manager in recording the

business protractions in the best possible. Further, it can be inferred that reports which are created

according the global accounting principles facilitate better transparency and comparison. It can be

seen in the report accrual concept helps in presenting the fair view of the statements in front of the

stakeholders.

12

of relevant period. Accrual concept should be used by Domino's even in statutory dues such as

pension payments, royalties, franchise fees, rental income and also franchisee rebates should be

recognised on accrual basis on expected entitlement which has been earned up to the balance sheet

date. Following a accrual concept of accounting it gives Domino's a advantage that the financial

statements reflect all the expenses associated with related revenues for a particular accounting

period which depicts a clear picture to investors and potential investors who rely on financial

information to generate best outcome of their investments. Domino's being largely into retail

business do not promote or accept credit for their products delivered to customers therefore accrual

is necessary to be followed n every transaction an organisation undertakes. As and when the invoice

is sent to customer transaction is to be recorded by Domino whether the cash is immediately

received or not. It will help management to make better decisions Accrual should always be used in

combination with various other accounting policies. It ensures that Financial statements fairly

present the each year's activity with the help of matching concept of revenues and related expenses.

Profits generated for Domino's are mixture of both cash as well as accrual transaction entered into.

CONCLUSION

From the above report, it has been concluded that financial reports provide deeper insight to

stakeholders about the financial health and performance of an organization. Besides this, it can be

inferred from the report that accounting principles and concepts help manager in recording the

business protractions in the best possible. Further, it can be inferred that reports which are created

according the global accounting principles facilitate better transparency and comparison. It can be

seen in the report accrual concept helps in presenting the fair view of the statements in front of the

stakeholders.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.