Accounting: Costing Methods and Profitability Analysis

VerifiedAdded on 2021/06/16

|7

|826

|25

Homework Assignment

AI Summary

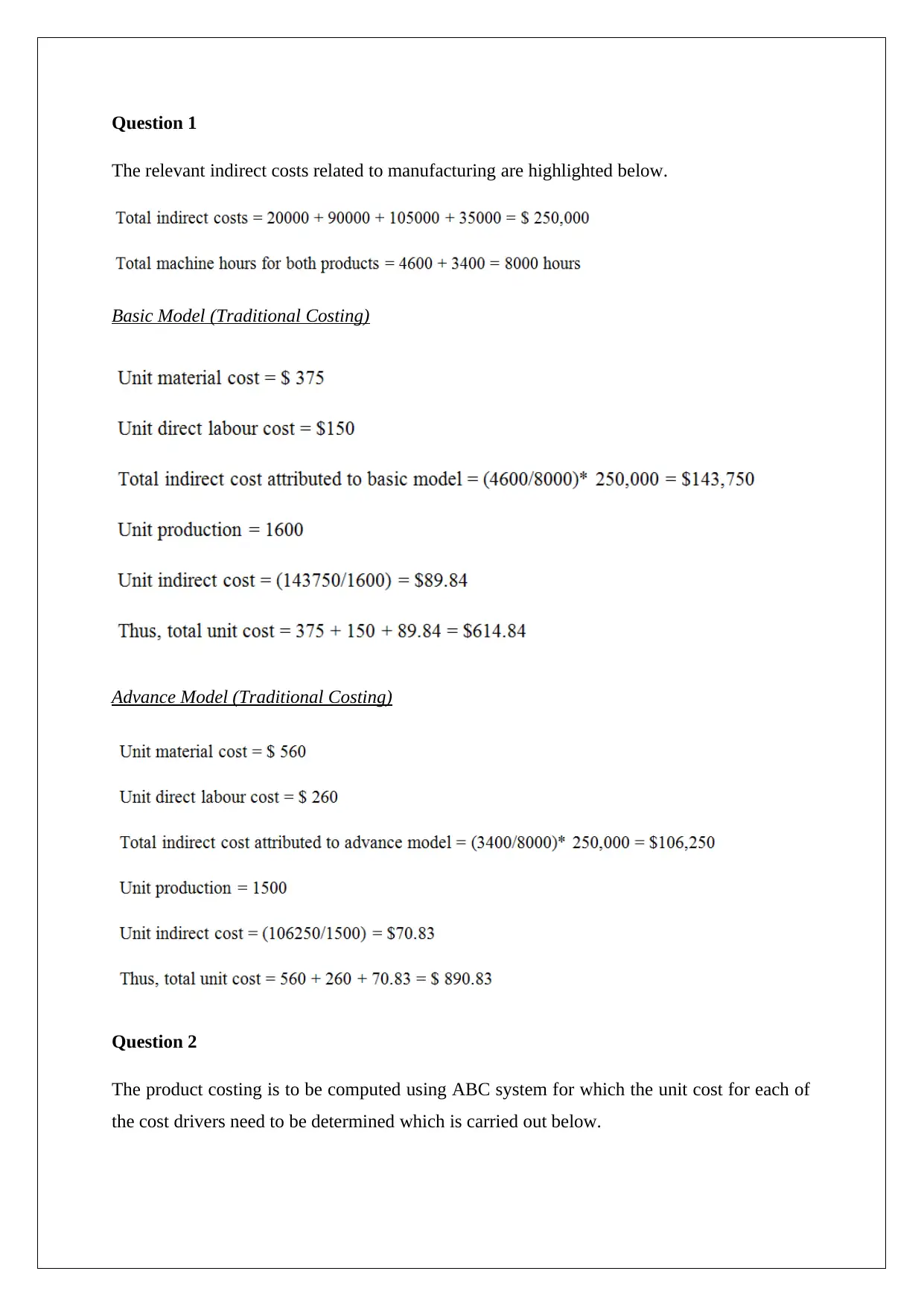

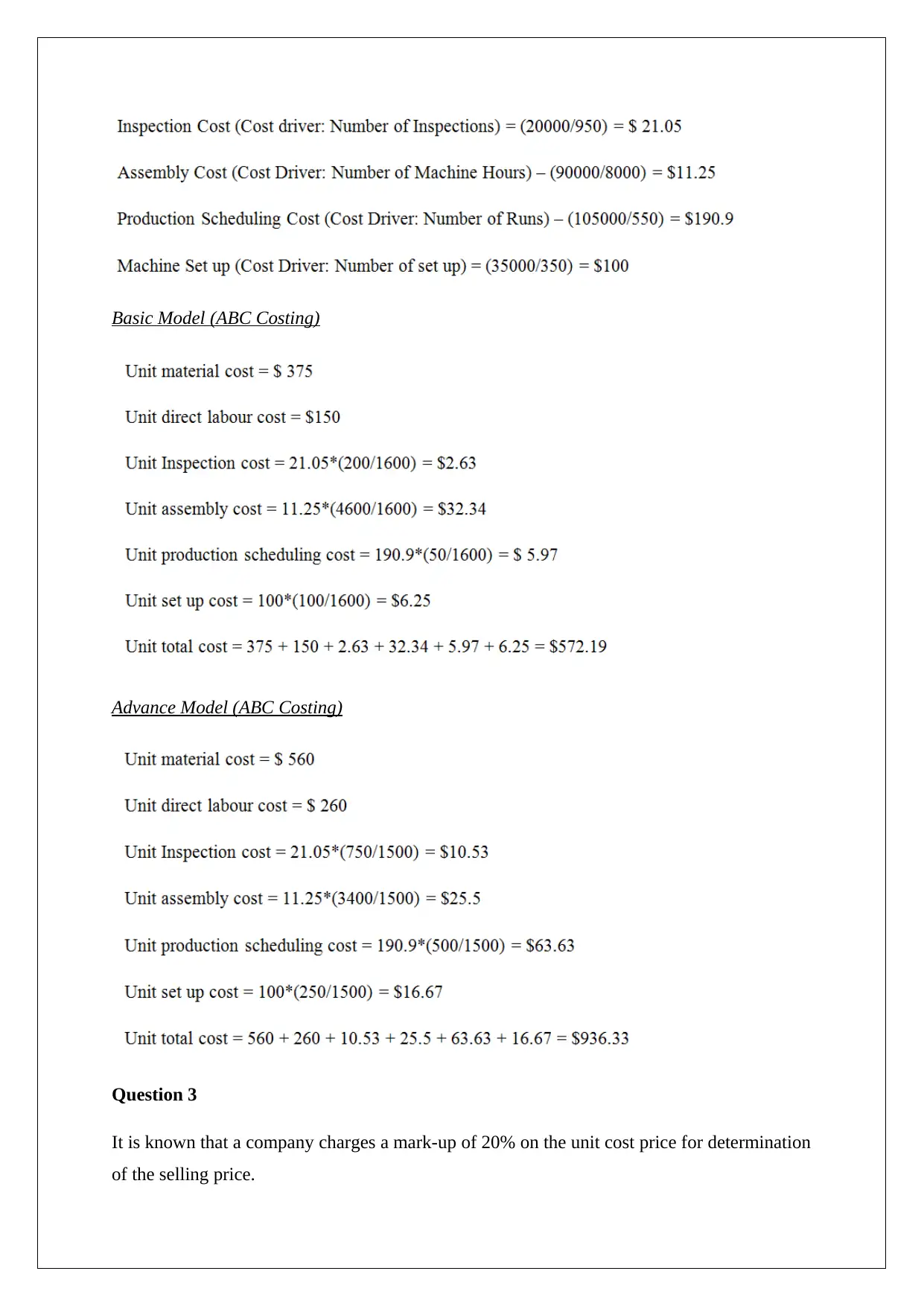

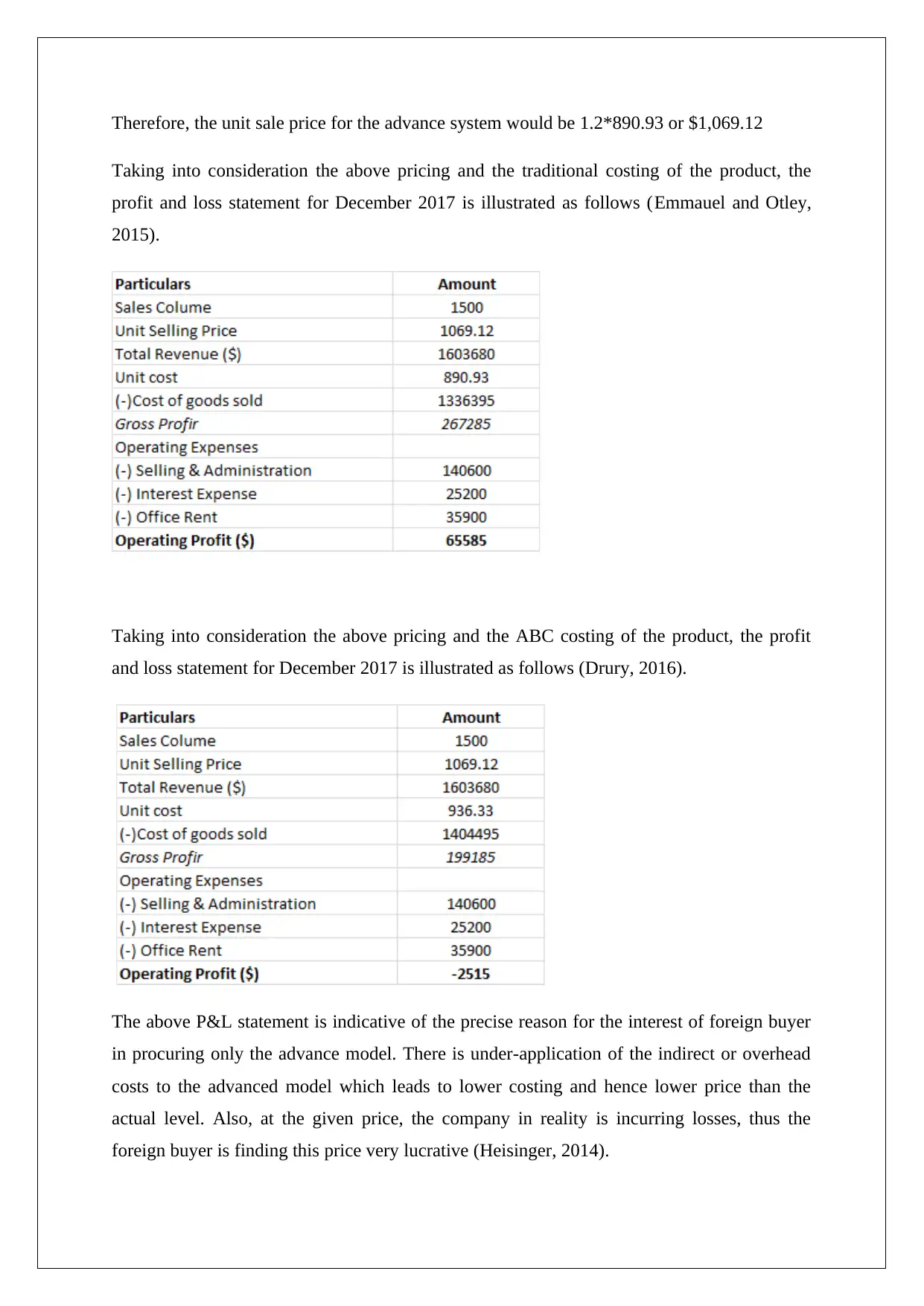

This assignment delves into the application of Activity-Based Costing (ABC) to analyze product costing and profitability. It begins by highlighting relevant indirect costs for both traditional and advanced models. The solution then demonstrates the computation of product costing using the ABC system, determining unit costs for various cost drivers. A profit and loss statement is constructed to illustrate the impact of different costing methods on pricing and profitability, explaining why a foreign buyer might be interested in a specific product model. The assignment also discusses the discrepancies between overhead costs used for cost computation and those actually incurred, providing measures to manage these variations. It further explores the benefits and limitations of the ABC system, including its accuracy in cost allocation and its complexity. The analysis uses references from established accounting texts to support its findings.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.