Cost and Revenue Analysis: A Comprehensive Financial Report

VerifiedAdded on 2020/10/22

|20

|4097

|227

Homework Assignment

AI Summary

This assignment solution provides a comprehensive overview of cost and revenue analysis within a financial accounting context. It delves into internal reporting, exploring the purposes and relationships between various costing systems such as direct, absorption, and standard costing. The document examines different responsibility centers (cost, profit, and investment centers) and classifies various costing systems based on their applications, including standard, marginal, process, and budgeted costing. A key aspect is the comparison of marginal and absorption costing methods. The solution then details the recording and analysis of cost information related to materials, labor, and expenses, including the various stages of inventory and calculations using FIFO, LIFO, and weighted average methods. It also addresses cost behavior, costing systems, attribution of overhead costs, and the calculation of overhead absorption rates. Furthermore, the assignment covers variance analysis, the preparation of management reports, and the estimation of future incomes and costs for decision-making processes. It explains the impact of changing activity levels on unit costs and discusses factors influencing short-term and long-term decisions.

Costs and revenues

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

TASK 1............................................................................................................................................4

1.1 purpose of internal reporting.................................................................................................4

1.2 relationship between various costing systems.......................................................................4

1.3 explanation of various responsibility centers in organisation...............................................4

1.4 classifications and use of different types of costing system.................................................5

1.5 difference between marginal and absorption costing............................................................5

TASK 2............................................................................................................................................6

2.1 recording of cost information relating to material, labour and expenses in accordance with

the procedures of costing............................................................................................................6

2.2 analysis of cost information related to material, labour and expenses..................................6

2.3 Various stages of inventory...................................................................................................7

2.4 Calculation of cost of inventory using LIFO, FIFO and weighted average method.............7

2.5 behavior of various costs in the organisation........................................................................9

2.6 recording of cost information using various costing systems...............................................9

TASK 3..........................................................................................................................................11

3.1 attribution of overhead costs for production and service cost centres................................11

3.2 calculation of overhead absorption rate..............................................................................11

3.3 adjustment of under and over recovered costs....................................................................12

3.4 methods of allocation, apportionment and absorption of costs and implementation of

changes in these methods..........................................................................................................12

3.5 resolving queries of overhead cost data..............................................................................13

TASK 4..........................................................................................................................................13

4.1 comparison of budgeted cost with actual costs...................................................................13

4.2 analysis of variance.............................................................................................................14

4.3 information regarding variance along with suggested actions for remedies.......................14

4.4 preparation of management report .....................................................................................15

TASK 5..........................................................................................................................................16

5.1 Estimation of future incomes and costs for the decision making process...........................16

5.2 explanation of effect of changing the activity levels on unit cost.......................................17

TASK 1............................................................................................................................................4

1.1 purpose of internal reporting.................................................................................................4

1.2 relationship between various costing systems.......................................................................4

1.3 explanation of various responsibility centers in organisation...............................................4

1.4 classifications and use of different types of costing system.................................................5

1.5 difference between marginal and absorption costing............................................................5

TASK 2............................................................................................................................................6

2.1 recording of cost information relating to material, labour and expenses in accordance with

the procedures of costing............................................................................................................6

2.2 analysis of cost information related to material, labour and expenses..................................6

2.3 Various stages of inventory...................................................................................................7

2.4 Calculation of cost of inventory using LIFO, FIFO and weighted average method.............7

2.5 behavior of various costs in the organisation........................................................................9

2.6 recording of cost information using various costing systems...............................................9

TASK 3..........................................................................................................................................11

3.1 attribution of overhead costs for production and service cost centres................................11

3.2 calculation of overhead absorption rate..............................................................................11

3.3 adjustment of under and over recovered costs....................................................................12

3.4 methods of allocation, apportionment and absorption of costs and implementation of

changes in these methods..........................................................................................................12

3.5 resolving queries of overhead cost data..............................................................................13

TASK 4..........................................................................................................................................13

4.1 comparison of budgeted cost with actual costs...................................................................13

4.2 analysis of variance.............................................................................................................14

4.3 information regarding variance along with suggested actions for remedies.......................14

4.4 preparation of management report .....................................................................................15

TASK 5..........................................................................................................................................16

5.1 Estimation of future incomes and costs for the decision making process...........................16

5.2 explanation of effect of changing the activity levels on unit cost.......................................17

5.3 Calculation of effect of changing activity level on unit cost..............................................17

5.4 various factors having effect over short term and long term decision-making process......17

REFERENCES..............................................................................................................................18

5.4 various factors having effect over short term and long term decision-making process......17

REFERENCES..............................................................................................................................18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 1

1.1 purpose of internal reporting

Internal reporting is a tool of management which is used to inform the managers and

other internal users regarding internal affairs of the business (Maskell, Baggaley and Grasso,

2016). It helps the management in taking decisions regarding enhancement of internal efficiency

of the business activities like productions, inventory handling, etc.

Purpose of internal reporting:

It helps in communicating internal rule of the company with its members.

It helps the management in preventing business from frauds in the organisation.

It is also used in order to reduce the risk of happeining of errors in the business activities.

1.2 relationship between various costing systems

Direct costing, Absorption costing, marginal costing, standard costing, etc. are various

types of costing system. All the systems helps management in their decision making system. All

the costing systems are interrelated with each other (Prahlad, 2015). In absorption costing,

accountant absorbs all the cost determined by direct costing system into various departments of

the costing.

Whereas in standard costing cost absorbed among various departments are compared

with the cost calculated in budgeted costing system in order to determine cost efficiency of each

level of department in the company. Hence, all the costing systems are interrelated with each

other.

1.3 explanation of various responsibility centres in organisation

Responsibilities centres helps in managing various business activities by allocating

various types of responsibilities to different departments. Company can have different

responsibility centres like cost centre. Profit centre, etc.

cost centre

This centre concerns with management of cost in the business. Its main objective is to

have better control of cost in the business activities by minimising cost wastage.

1.1 purpose of internal reporting

Internal reporting is a tool of management which is used to inform the managers and

other internal users regarding internal affairs of the business (Maskell, Baggaley and Grasso,

2016). It helps the management in taking decisions regarding enhancement of internal efficiency

of the business activities like productions, inventory handling, etc.

Purpose of internal reporting:

It helps in communicating internal rule of the company with its members.

It helps the management in preventing business from frauds in the organisation.

It is also used in order to reduce the risk of happeining of errors in the business activities.

1.2 relationship between various costing systems

Direct costing, Absorption costing, marginal costing, standard costing, etc. are various

types of costing system. All the systems helps management in their decision making system. All

the costing systems are interrelated with each other (Prahlad, 2015). In absorption costing,

accountant absorbs all the cost determined by direct costing system into various departments of

the costing.

Whereas in standard costing cost absorbed among various departments are compared

with the cost calculated in budgeted costing system in order to determine cost efficiency of each

level of department in the company. Hence, all the costing systems are interrelated with each

other.

1.3 explanation of various responsibility centres in organisation

Responsibilities centres helps in managing various business activities by allocating

various types of responsibilities to different departments. Company can have different

responsibility centres like cost centre. Profit centre, etc.

cost centre

This centre concerns with management of cost in the business. Its main objective is to

have better control of cost in the business activities by minimising cost wastage.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Profit centre

It helps management in enhancing profit of overall company. It makes different strategies

as to earn maximum amount of profit from normal course of business (Giannouli, 2015).

Investment centre

This centre advices the firm to invest its excess money in such a way so that it can earn

maximum interest in the return. It provides the best use of cash in the business and enhances the

liquidity in entity.

1.4 classifications and use of different types of costing system

Standard costing, marginal costing, process costing, budgeted costing, etc. are various

types of the costing system (Top 6 Types of Costing Systems | Cost Accounting, 2018). They all

are classified on the basis of their use in the business. Standard costing helps in determining

overall efficiency in terms of variance, process costing helps in determining cost incurred by

production department at each level of production process and with the help of budgeted costing,

management predicts the cost to be incurred by the business in future to ensure the sources of

funds availability in the company.

1.5 difference between marginal and absorption costing

Basis Marginal costing Absorption costing

Classifications It classifies costs as fixed costs

and variable cost

In this method cost is

classified as production,

distribution, selling costs, etc.

Purpose To ascertain the total cost To apportion total costs at

different levels.

Profitability It provides higher amount of

profit

Due to inclusion of fixed costs,

it gives lower profit

(Difference Between Marginal

Costing and Absorption

Costing, 2018).

It helps management in enhancing profit of overall company. It makes different strategies

as to earn maximum amount of profit from normal course of business (Giannouli, 2015).

Investment centre

This centre advices the firm to invest its excess money in such a way so that it can earn

maximum interest in the return. It provides the best use of cash in the business and enhances the

liquidity in entity.

1.4 classifications and use of different types of costing system

Standard costing, marginal costing, process costing, budgeted costing, etc. are various

types of the costing system (Top 6 Types of Costing Systems | Cost Accounting, 2018). They all

are classified on the basis of their use in the business. Standard costing helps in determining

overall efficiency in terms of variance, process costing helps in determining cost incurred by

production department at each level of production process and with the help of budgeted costing,

management predicts the cost to be incurred by the business in future to ensure the sources of

funds availability in the company.

1.5 difference between marginal and absorption costing

Basis Marginal costing Absorption costing

Classifications It classifies costs as fixed costs

and variable cost

In this method cost is

classified as production,

distribution, selling costs, etc.

Purpose To ascertain the total cost To apportion total costs at

different levels.

Profitability It provides higher amount of

profit

Due to inclusion of fixed costs,

it gives lower profit

(Difference Between Marginal

Costing and Absorption

Costing, 2018).

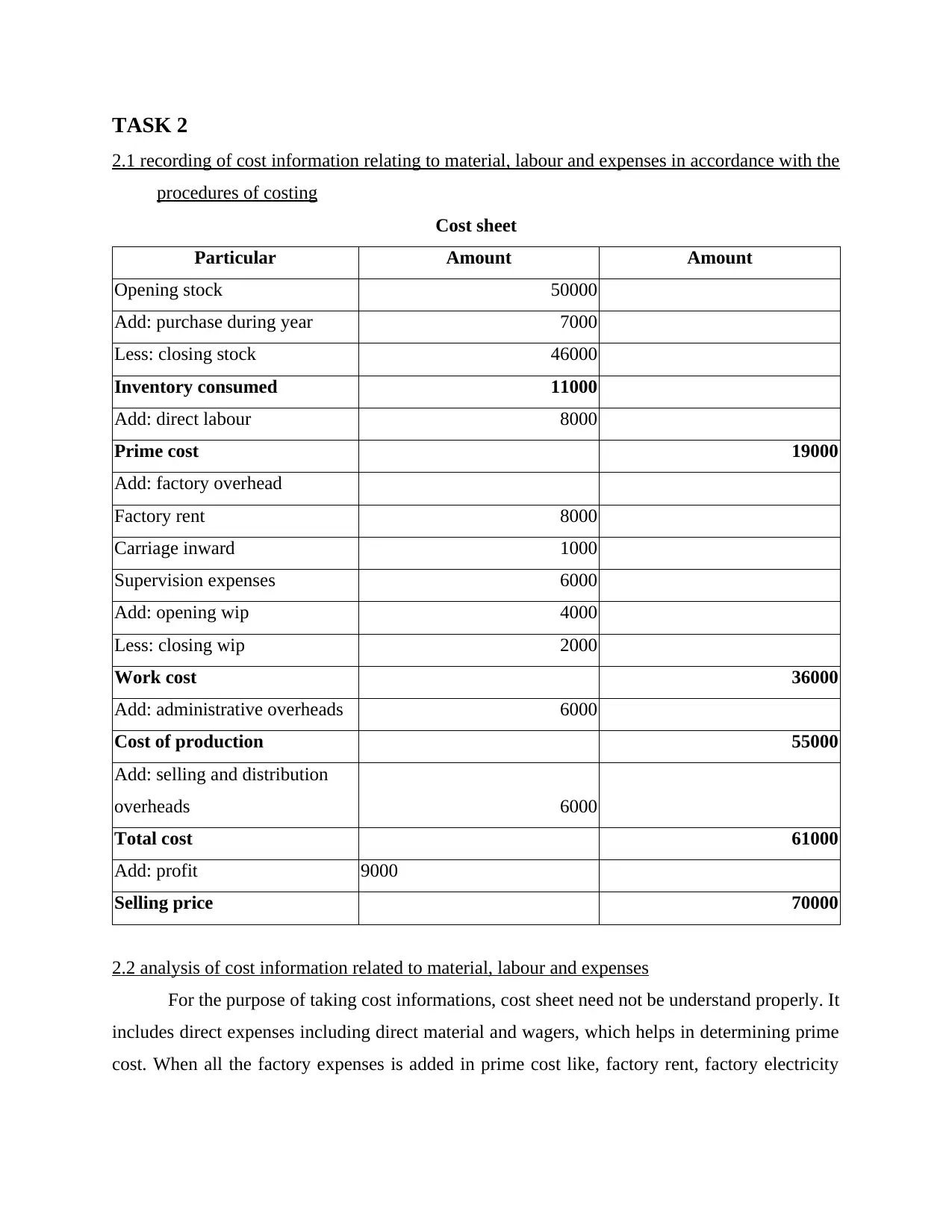

TASK 2

2.1 recording of cost information relating to material, labour and expenses in accordance with the

procedures of costing

Cost sheet

Particular Amount Amount

Opening stock 50000

Add: purchase during year 7000

Less: closing stock 46000

Inventory consumed 11000

Add: direct labour 8000

Prime cost 19000

Add: factory overhead

Factory rent 8000

Carriage inward 1000

Supervision expenses 6000

Add: opening wip 4000

Less: closing wip 2000

Work cost 36000

Add: administrative overheads 6000

Cost of production 55000

Add: selling and distribution

overheads 6000

Total cost 61000

Add: profit 9000

Selling price 70000

2.2 analysis of cost information related to material, labour and expenses

For the purpose of taking cost informations, cost sheet need not be understand properly. It

includes direct expenses including direct material and wagers, which helps in determining prime

cost. When all the factory expenses is added in prime cost like, factory rent, factory electricity

2.1 recording of cost information relating to material, labour and expenses in accordance with the

procedures of costing

Cost sheet

Particular Amount Amount

Opening stock 50000

Add: purchase during year 7000

Less: closing stock 46000

Inventory consumed 11000

Add: direct labour 8000

Prime cost 19000

Add: factory overhead

Factory rent 8000

Carriage inward 1000

Supervision expenses 6000

Add: opening wip 4000

Less: closing wip 2000

Work cost 36000

Add: administrative overheads 6000

Cost of production 55000

Add: selling and distribution

overheads 6000

Total cost 61000

Add: profit 9000

Selling price 70000

2.2 analysis of cost information related to material, labour and expenses

For the purpose of taking cost informations, cost sheet need not be understand properly. It

includes direct expenses including direct material and wagers, which helps in determining prime

cost. When all the factory expenses is added in prime cost like, factory rent, factory electricity

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

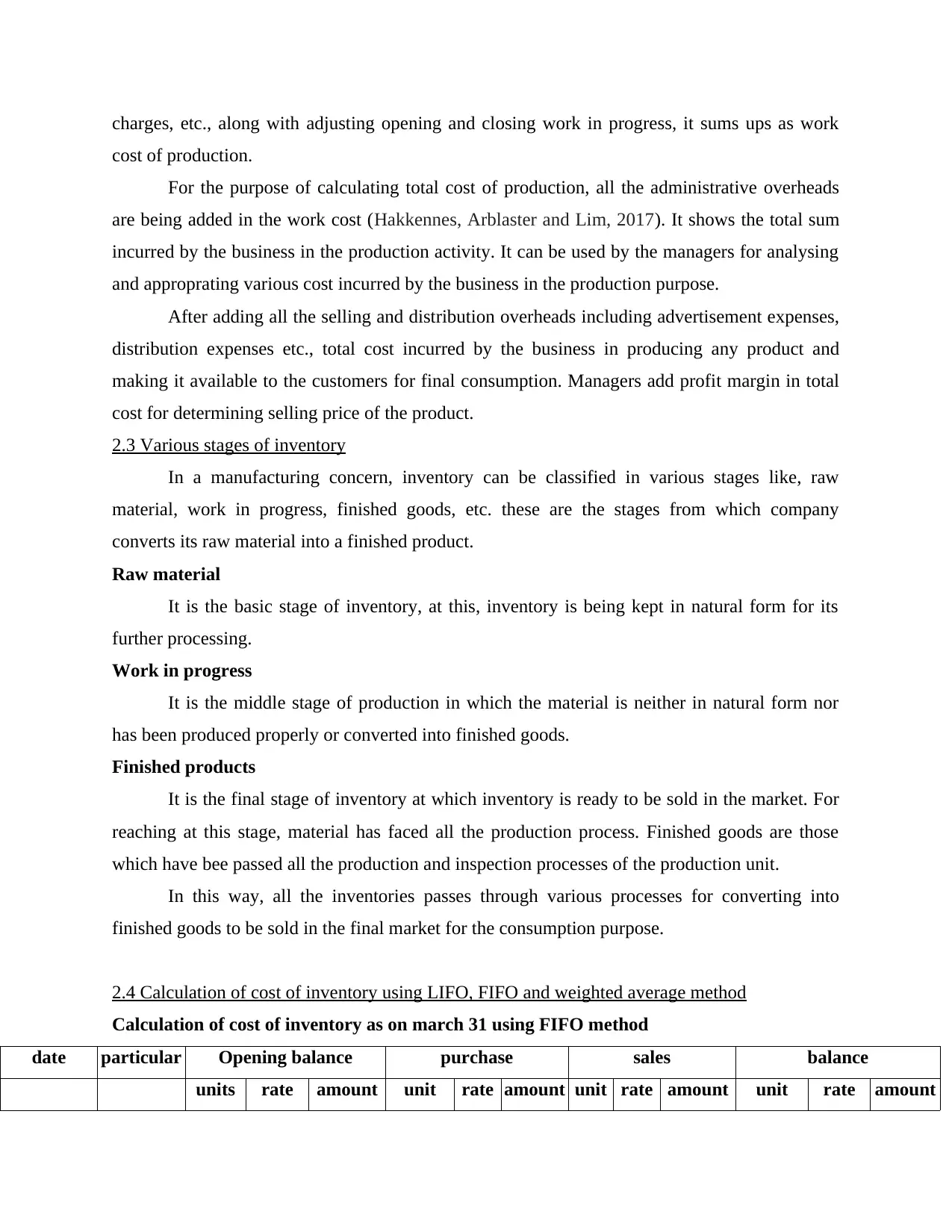

charges, etc., along with adjusting opening and closing work in progress, it sums ups as work

cost of production.

For the purpose of calculating total cost of production, all the administrative overheads

are being added in the work cost (Hakkennes, Arblaster and Lim, 2017). It shows the total sum

incurred by the business in the production activity. It can be used by the managers for analysing

and approprating various cost incurred by the business in the production purpose.

After adding all the selling and distribution overheads including advertisement expenses,

distribution expenses etc., total cost incurred by the business in producing any product and

making it available to the customers for final consumption. Managers add profit margin in total

cost for determining selling price of the product.

2.3 Various stages of inventory

In a manufacturing concern, inventory can be classified in various stages like, raw

material, work in progress, finished goods, etc. these are the stages from which company

converts its raw material into a finished product.

Raw material

It is the basic stage of inventory, at this, inventory is being kept in natural form for its

further processing.

Work in progress

It is the middle stage of production in which the material is neither in natural form nor

has been produced properly or converted into finished goods.

Finished products

It is the final stage of inventory at which inventory is ready to be sold in the market. For

reaching at this stage, material has faced all the production process. Finished goods are those

which have bee passed all the production and inspection processes of the production unit.

In this way, all the inventories passes through various processes for converting into

finished goods to be sold in the final market for the consumption purpose.

2.4 Calculation of cost of inventory using LIFO, FIFO and weighted average method

Calculation of cost of inventory as on march 31 using FIFO method

date particular Opening balance purchase sales balance

units rate amount unit rate amount unit rate amount unit rate amount

cost of production.

For the purpose of calculating total cost of production, all the administrative overheads

are being added in the work cost (Hakkennes, Arblaster and Lim, 2017). It shows the total sum

incurred by the business in the production activity. It can be used by the managers for analysing

and approprating various cost incurred by the business in the production purpose.

After adding all the selling and distribution overheads including advertisement expenses,

distribution expenses etc., total cost incurred by the business in producing any product and

making it available to the customers for final consumption. Managers add profit margin in total

cost for determining selling price of the product.

2.3 Various stages of inventory

In a manufacturing concern, inventory can be classified in various stages like, raw

material, work in progress, finished goods, etc. these are the stages from which company

converts its raw material into a finished product.

Raw material

It is the basic stage of inventory, at this, inventory is being kept in natural form for its

further processing.

Work in progress

It is the middle stage of production in which the material is neither in natural form nor

has been produced properly or converted into finished goods.

Finished products

It is the final stage of inventory at which inventory is ready to be sold in the market. For

reaching at this stage, material has faced all the production process. Finished goods are those

which have bee passed all the production and inspection processes of the production unit.

In this way, all the inventories passes through various processes for converting into

finished goods to be sold in the final market for the consumption purpose.

2.4 Calculation of cost of inventory using LIFO, FIFO and weighted average method

Calculation of cost of inventory as on march 31 using FIFO method

date particular Opening balance purchase sales balance

units rate amount unit rate amount unit rate amount unit rate amount

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

01/03/19

beginning

inventory 68 15 1020 68 15 1020

05/03/19 purchase 140 15.5 2170 68 15 1020

140 15.5 2170

09/03/19 sales 68 15 1020

26 15.5 403 114 15.5 1767

11/03/19 40 16 640 114 15.5 1767

40 16 640

16/03/19 78 16.5 1287 114 15.5 1767

40 16 640

78 16.5 1287

20/03/19 114 15.5 1767 38 16 608

2 16 32 78 16.5 1287

29/03/19 38 16 608 54 16.5 891

24 16.5 396

31/03/19

closing

stock 54 16.5 891

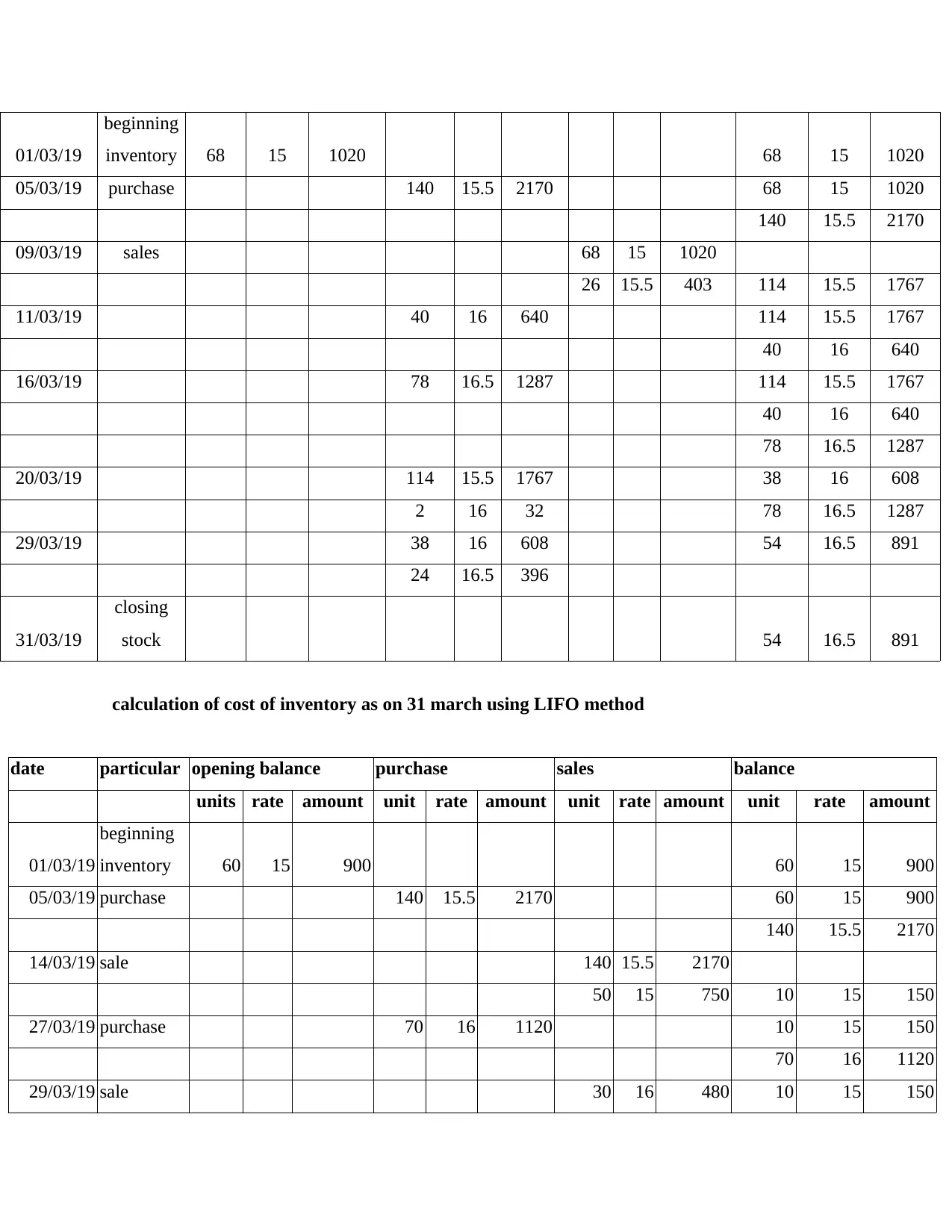

calculation of cost of inventory as on 31 march using LIFO method

date particular opening balance purchase sales balance

units rate amount unit rate amount unit rate amount unit rate amount

01/03/19

beginning

inventory 60 15 900 60 15 900

05/03/19 purchase 140 15.5 2170 60 15 900

140 15.5 2170

14/03/19 sale 140 15.5 2170

50 15 750 10 15 150

27/03/19 purchase 70 16 1120 10 15 150

70 16 1120

29/03/19 sale 30 16 480 10 15 150

beginning

inventory 68 15 1020 68 15 1020

05/03/19 purchase 140 15.5 2170 68 15 1020

140 15.5 2170

09/03/19 sales 68 15 1020

26 15.5 403 114 15.5 1767

11/03/19 40 16 640 114 15.5 1767

40 16 640

16/03/19 78 16.5 1287 114 15.5 1767

40 16 640

78 16.5 1287

20/03/19 114 15.5 1767 38 16 608

2 16 32 78 16.5 1287

29/03/19 38 16 608 54 16.5 891

24 16.5 396

31/03/19

closing

stock 54 16.5 891

calculation of cost of inventory as on 31 march using LIFO method

date particular opening balance purchase sales balance

units rate amount unit rate amount unit rate amount unit rate amount

01/03/19

beginning

inventory 60 15 900 60 15 900

05/03/19 purchase 140 15.5 2170 60 15 900

140 15.5 2170

14/03/19 sale 140 15.5 2170

50 15 750 10 15 150

27/03/19 purchase 70 16 1120 10 15 150

70 16 1120

29/03/19 sale 30 16 480 10 15 150

40 16 640

31/03/19

Closing

inventory 10 15 150

40 16 640

calculation of cost of inventory as on 31 march using Weighted average method

date particular opening balance purchase sales balance

units rate amount unit rate amount unit rate amount unit rate amount

01/03/19

beginning

inventory 60 15 900 60 15 900

05/03/19 purchase 140 15.5 2170 200 15.35 3070

14/03/19 sale 190 15.35 2916.5 10 15.35 153.5

27/03/19 purchase 70 16 1120 80

15.918

75 1273.5

29/03/19 sale 30

15.918

75

477.562

5 50

15.918

75 795.9375

31/03/19

closing

stock 50

15.918

75 795.9375

2.5 behaviour of various costs in the organisation

On the basis of behaviour, costs can be categorised into numerous categorise like fixed

cost, variable cost, semi variable cost, etc.

Fixed cost

Fixed costs are those which remains fixed over the time. It does not changes with the

change in level of production. Although, talking about per unit cost, it keeps changing.

Variable costs

As the name these costs varies over the time (Christian, 2018). However, these costs

remains constant per unit for each level of production.

Semi variable cost

31/03/19

Closing

inventory 10 15 150

40 16 640

calculation of cost of inventory as on 31 march using Weighted average method

date particular opening balance purchase sales balance

units rate amount unit rate amount unit rate amount unit rate amount

01/03/19

beginning

inventory 60 15 900 60 15 900

05/03/19 purchase 140 15.5 2170 200 15.35 3070

14/03/19 sale 190 15.35 2916.5 10 15.35 153.5

27/03/19 purchase 70 16 1120 80

15.918

75 1273.5

29/03/19 sale 30

15.918

75

477.562

5 50

15.918

75 795.9375

31/03/19

closing

stock 50

15.918

75 795.9375

2.5 behaviour of various costs in the organisation

On the basis of behaviour, costs can be categorised into numerous categorise like fixed

cost, variable cost, semi variable cost, etc.

Fixed cost

Fixed costs are those which remains fixed over the time. It does not changes with the

change in level of production. Although, talking about per unit cost, it keeps changing.

Variable costs

As the name these costs varies over the time (Christian, 2018). However, these costs

remains constant per unit for each level of production.

Semi variable cost

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Semi variable costs are the combination of fixed and variable costs. A part of thses costs

remains constant over the time period, on the other hand, another part of these costs keeps

changing with the change in production level, as they remain same on per unit basis.

2.6 recording of cost information using various costing systems

Batch costing

Batch costing helps in allocating total cost of production for different batches. With this

method, management can identify cost incurred on production of each batches.

Calculation of cost for each batch Batch no. 4101

particular Department Qunatity Rate amount

Material Store department 5000 10 50000

Wages Sales department. 2000 5 10000

Purchase department 1000 4 4000

overheads 200 5 1000

Total cost

for the batch

65000

Job costing

Job costing refers to that method of costing which helps in allocating total cost on the

basis of different jobs of the department (Edwards, Sobel and Bonilha, 2018). This m,ethod is

useful for those organisations which manufacture products as per the demand of the customer or

which produces customized products.

Job costing for job no.654

Particular Department Quantity Per unit costs Amount

Direct

material

Inventory

department

50 50 2500

Direct labour Production 20 100 2000

Purchase

department

20 50 1000

remains constant over the time period, on the other hand, another part of these costs keeps

changing with the change in production level, as they remain same on per unit basis.

2.6 recording of cost information using various costing systems

Batch costing

Batch costing helps in allocating total cost of production for different batches. With this

method, management can identify cost incurred on production of each batches.

Calculation of cost for each batch Batch no. 4101

particular Department Qunatity Rate amount

Material Store department 5000 10 50000

Wages Sales department. 2000 5 10000

Purchase department 1000 4 4000

overheads 200 5 1000

Total cost

for the batch

65000

Job costing

Job costing refers to that method of costing which helps in allocating total cost on the

basis of different jobs of the department (Edwards, Sobel and Bonilha, 2018). This m,ethod is

useful for those organisations which manufacture products as per the demand of the customer or

which produces customized products.

Job costing for job no.654

Particular Department Quantity Per unit costs Amount

Direct

material

Inventory

department

50 50 2500

Direct labour Production 20 100 2000

Purchase

department

20 50 1000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Overheads 2000

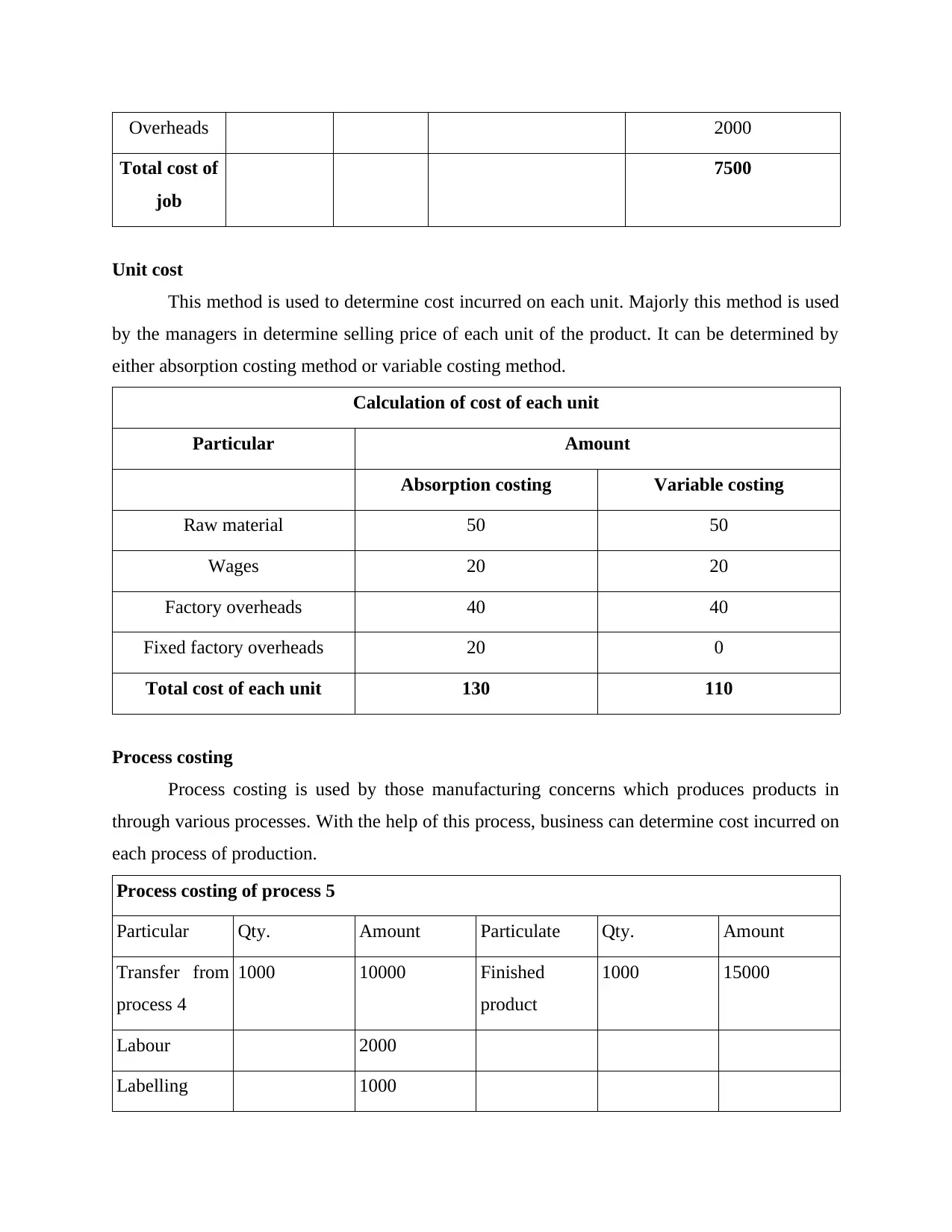

Total cost of

job

7500

Unit cost

This method is used to determine cost incurred on each unit. Majorly this method is used

by the managers in determine selling price of each unit of the product. It can be determined by

either absorption costing method or variable costing method.

Calculation of cost of each unit

Particular Amount

Absorption costing Variable costing

Raw material 50 50

Wages 20 20

Factory overheads 40 40

Fixed factory overheads 20 0

Total cost of each unit 130 110

Process costing

Process costing is used by those manufacturing concerns which produces products in

through various processes. With the help of this process, business can determine cost incurred on

each process of production.

Process costing of process 5

Particular Qty. Amount Particulate Qty. Amount

Transfer from

process 4

1000 10000 Finished

product

1000 15000

Labour 2000

Labelling 1000

Total cost of

job

7500

Unit cost

This method is used to determine cost incurred on each unit. Majorly this method is used

by the managers in determine selling price of each unit of the product. It can be determined by

either absorption costing method or variable costing method.

Calculation of cost of each unit

Particular Amount

Absorption costing Variable costing

Raw material 50 50

Wages 20 20

Factory overheads 40 40

Fixed factory overheads 20 0

Total cost of each unit 130 110

Process costing

Process costing is used by those manufacturing concerns which produces products in

through various processes. With the help of this process, business can determine cost incurred on

each process of production.

Process costing of process 5

Particular Qty. Amount Particulate Qty. Amount

Transfer from

process 4

1000 10000 Finished

product

1000 15000

Labour 2000

Labelling 1000

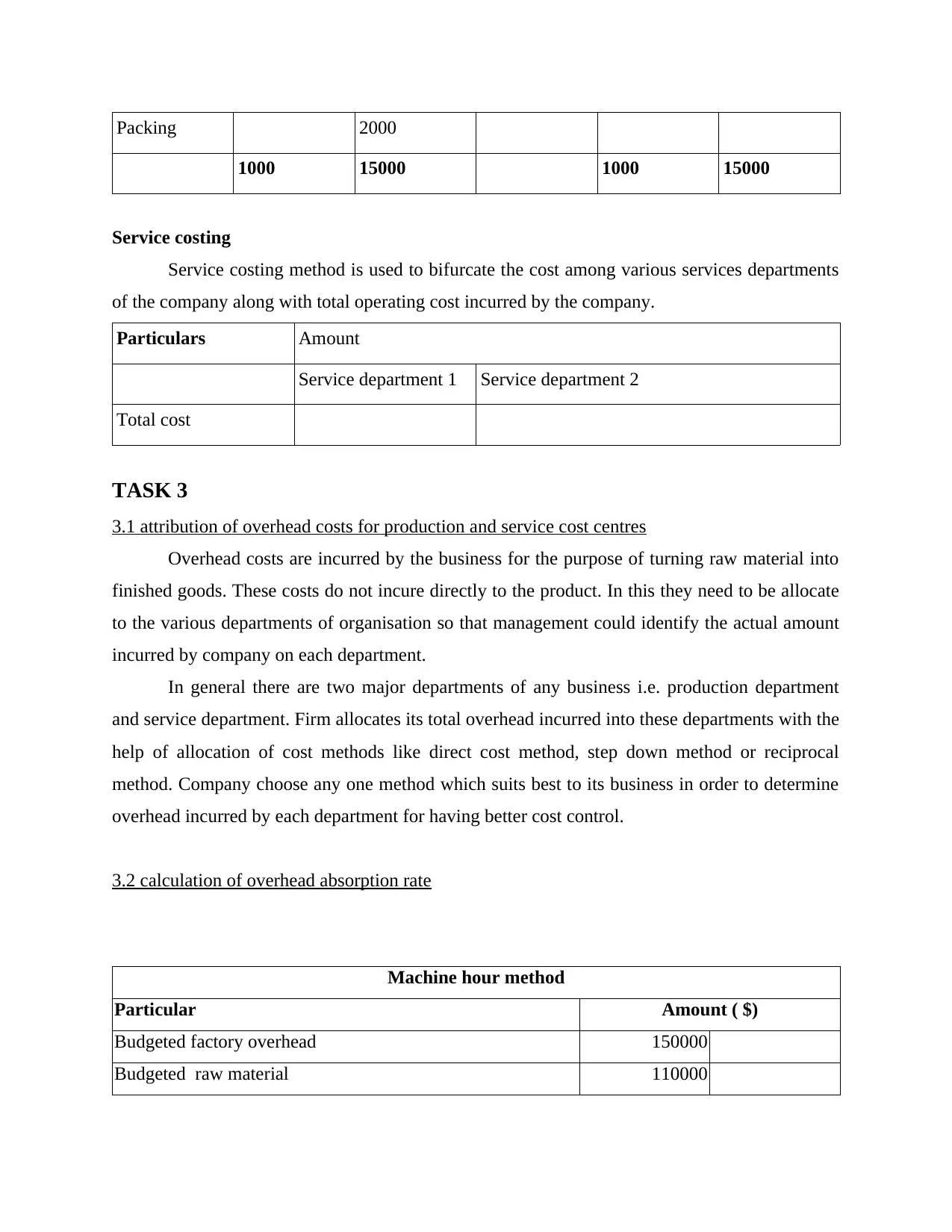

Packing 2000

1000 15000 1000 15000

Service costing

Service costing method is used to bifurcate the cost among various services departments

of the company along with total operating cost incurred by the company.

Particulars Amount

Service department 1 Service department 2

Total cost

TASK 3

3.1 attribution of overhead costs for production and service cost centres

Overhead costs are incurred by the business for the purpose of turning raw material into

finished goods. These costs do not incure directly to the product. In this they need to be allocate

to the various departments of organisation so that management could identify the actual amount

incurred by company on each department.

In general there are two major departments of any business i.e. production department

and service department. Firm allocates its total overhead incurred into these departments with the

help of allocation of cost methods like direct cost method, step down method or reciprocal

method. Company choose any one method which suits best to its business in order to determine

overhead incurred by each department for having better cost control.

3.2 calculation of overhead absorption rate

Machine hour method

Particular Amount ( $)

Budgeted factory overhead 150000

Budgeted raw material 110000

1000 15000 1000 15000

Service costing

Service costing method is used to bifurcate the cost among various services departments

of the company along with total operating cost incurred by the company.

Particulars Amount

Service department 1 Service department 2

Total cost

TASK 3

3.1 attribution of overhead costs for production and service cost centres

Overhead costs are incurred by the business for the purpose of turning raw material into

finished goods. These costs do not incure directly to the product. In this they need to be allocate

to the various departments of organisation so that management could identify the actual amount

incurred by company on each department.

In general there are two major departments of any business i.e. production department

and service department. Firm allocates its total overhead incurred into these departments with the

help of allocation of cost methods like direct cost method, step down method or reciprocal

method. Company choose any one method which suits best to its business in order to determine

overhead incurred by each department for having better cost control.

3.2 calculation of overhead absorption rate

Machine hour method

Particular Amount ( $)

Budgeted factory overhead 150000

Budgeted raw material 110000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.