Financial Accounting Homework: Recent Developments and Statement

VerifiedAdded on 2020/02/19

|9

|1183

|42

Homework Assignment

AI Summary

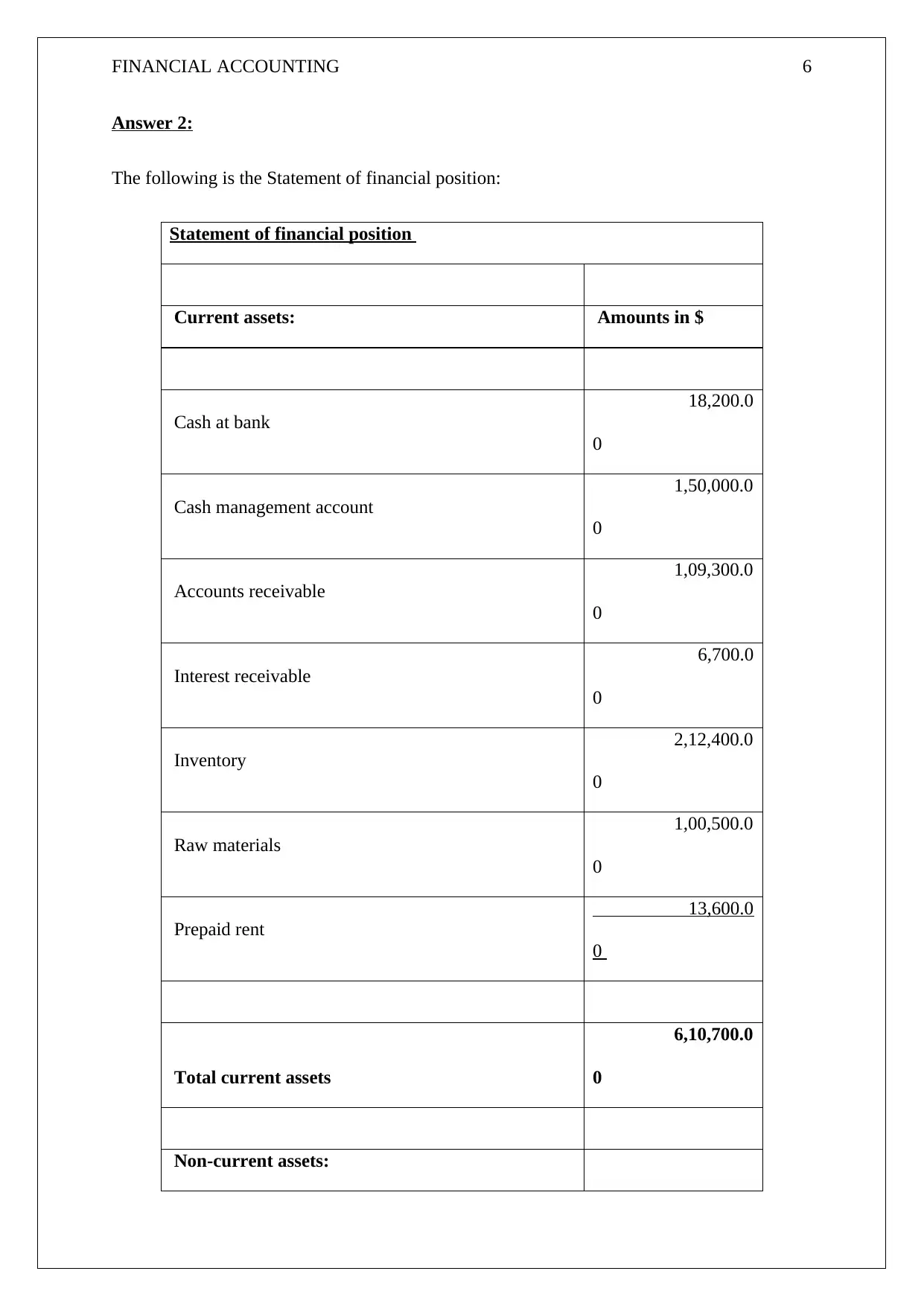

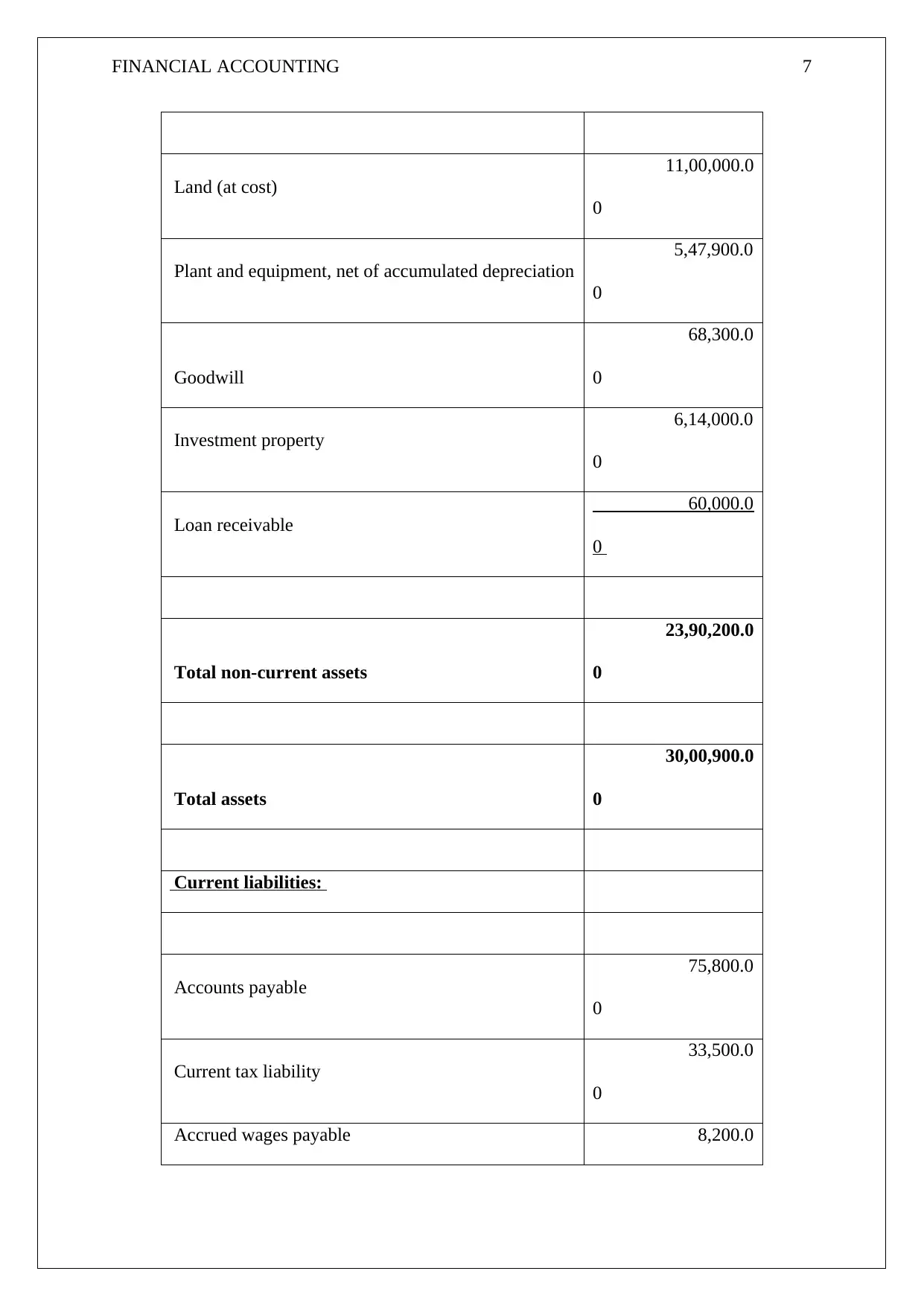

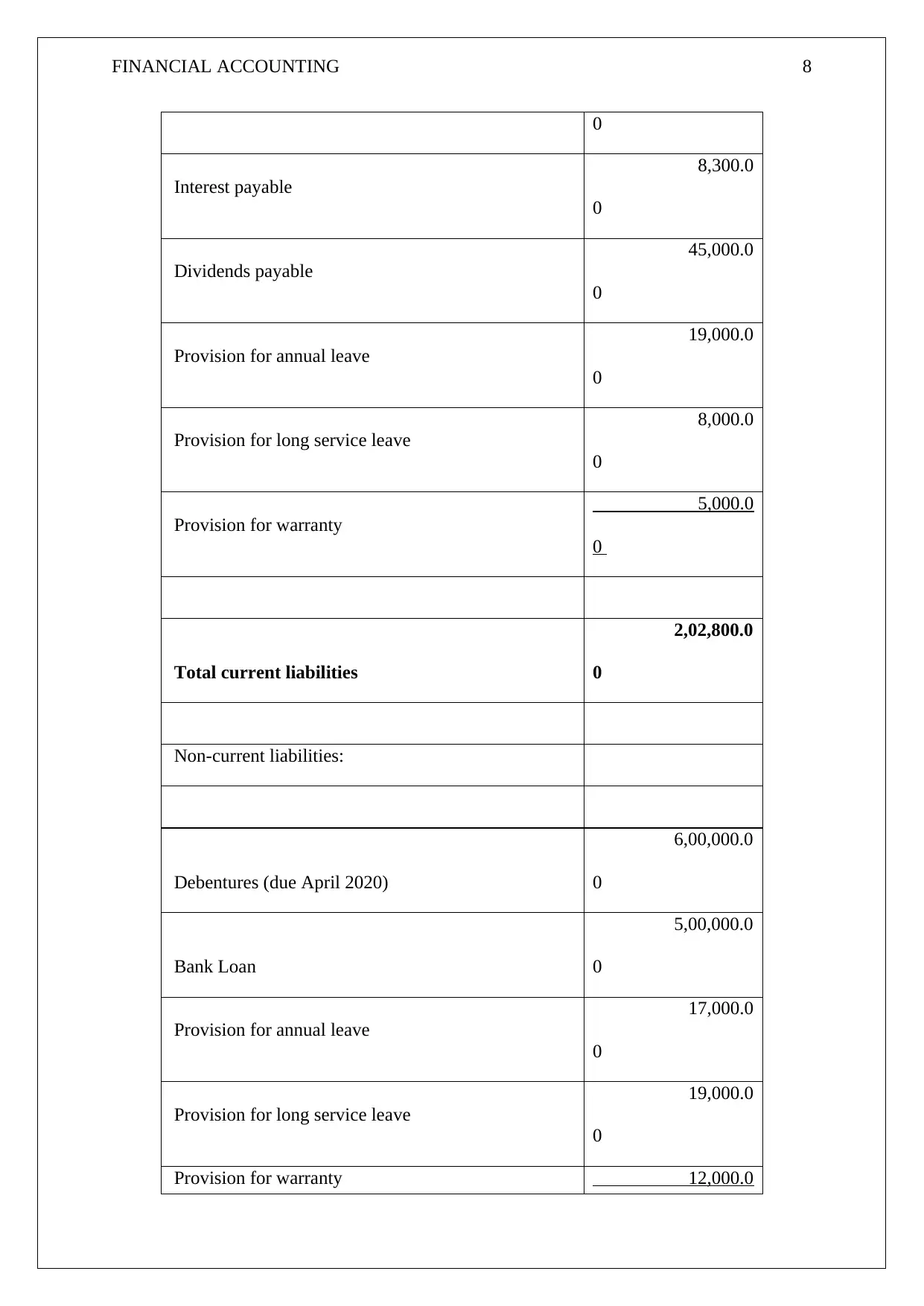

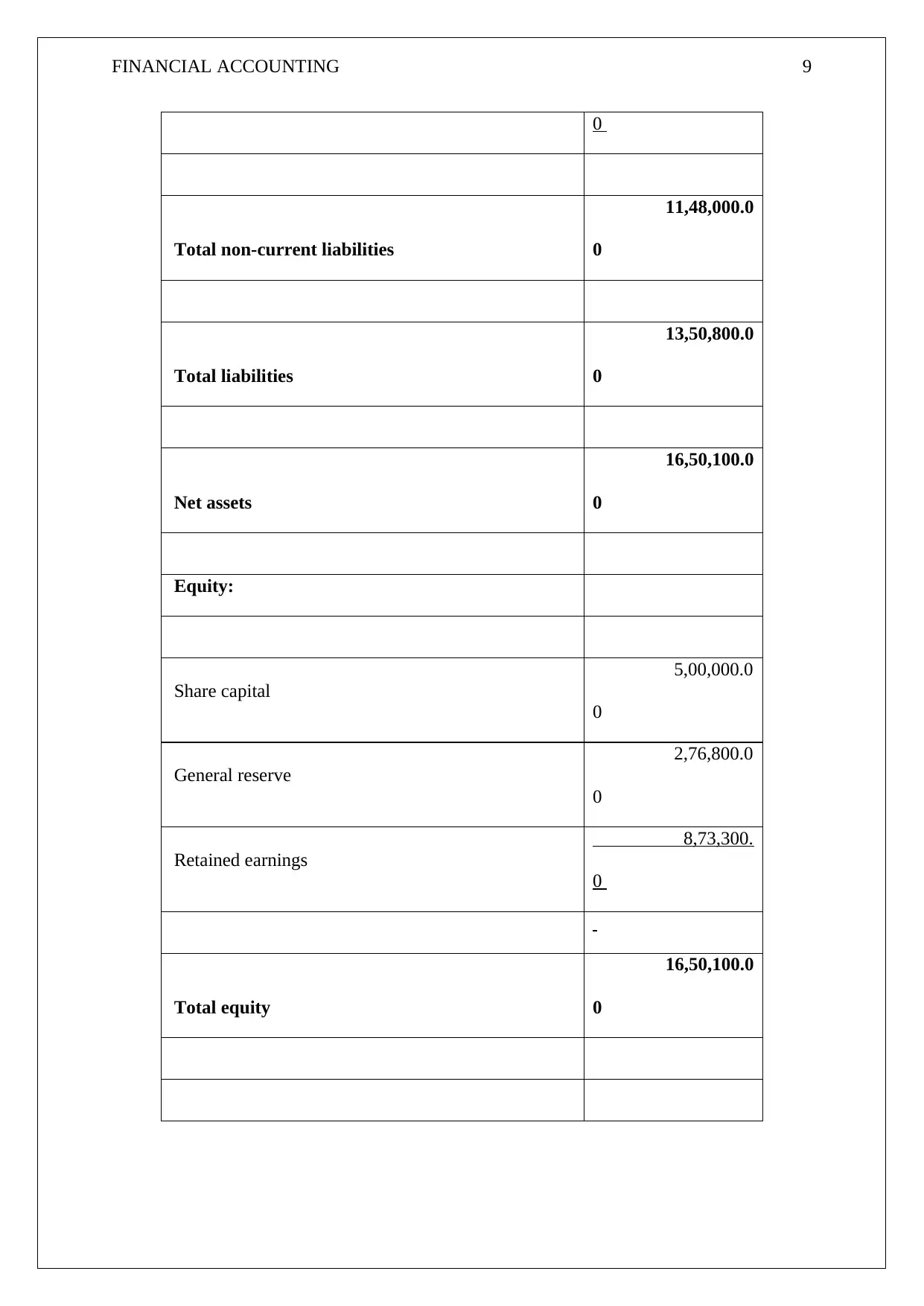

This financial accounting homework assignment provides an overview of recent developments in financial reporting, focusing on global entities, superannuation entities, share-based payments, and new standards issued by IASB, PCAOB, FASAB, and GASB. It details the implications of these updates on financial reporting practices. The assignment also includes a comprehensive statement of financial position, outlining current and non-current assets, liabilities, and equity. The statement provides a clear snapshot of the company's financial health, with detailed figures for cash, receivables, inventory, land, plant, and various liabilities such as accounts payable, tax liabilities, and provisions. The assignment is supported by references to key sources like EY, IAS plus, FASB, and IFRS.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.