HA2032 Corporate & Financial Accounting: Regulation, Equity & Debt

VerifiedAdded on 2023/06/04

|14

|3160

|140

Report

AI Summary

This report provides a comprehensive analysis of corporate regulation, accounting standard setting, and owners' equity within the Australian business sector, with a specific focus on the mining industry. It examines the debate surrounding the regulation of financial accounting and reporting versus voluntary disclosure by managers, highlighting the potential for manipulation in the absence of regulation. The report also discusses the role of the Australian Accounting Standards Board (AASB) in international standard setting and explores the reasons why IFRS adoption is not mandatory for all IASB member nations. Furthermore, it includes an analysis of the owners' equity position and debt management of four ASX-listed companies: Orica Limited, Rio Tinto, Fortescue Metals Group, and BHP Billiton, using financial data from their annual reports. The debt-to-equity ratios are calculated and interpreted to assess the capital structure and financial health of these organizations.

Running head: CORPORATE AND FINANCIAL ACCOUNTING

Corporate and Financial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Corporate and Financial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE AND FINANCIAL ACCOUNTING

Executive Summary:

The report is prepared to cover all the financial and regulatory aspects confronting the Australian

business sector. More specifically, it has emphasised on the mining sector of the nation by

considering Orica Limited, Rio Tinto, Fortescue Metals Group and BHP Billiton as the four key

public listed companies operating in the nation. Moreover, special emphasis has been placed on

the need for corporate regulation and voluntary disclosure of information by business managers.

The paper has shed light on the reasons that IFRS is not mandatory for all the member countries

of IASB.

Executive Summary:

The report is prepared to cover all the financial and regulatory aspects confronting the Australian

business sector. More specifically, it has emphasised on the mining sector of the nation by

considering Orica Limited, Rio Tinto, Fortescue Metals Group and BHP Billiton as the four key

public listed companies operating in the nation. Moreover, special emphasis has been placed on

the need for corporate regulation and voluntary disclosure of information by business managers.

The paper has shed light on the reasons that IFRS is not mandatory for all the member countries

of IASB.

2CORPORATE AND FINANCIAL ACCOUNTING

Table of Contents

Introduction:....................................................................................................................................3

Corporate regulation:.......................................................................................................................3

Requirement (i):...........................................................................................................................3

Accounting standard setting:...........................................................................................................5

Requirement (ii):..........................................................................................................................5

Owners’ equity:...............................................................................................................................7

Requirement (iii):.........................................................................................................................7

Requirement (iv):.........................................................................................................................8

Conclusion:....................................................................................................................................11

References:....................................................................................................................................12

Table of Contents

Introduction:....................................................................................................................................3

Corporate regulation:.......................................................................................................................3

Requirement (i):...........................................................................................................................3

Accounting standard setting:...........................................................................................................5

Requirement (ii):..........................................................................................................................5

Owners’ equity:...............................................................................................................................7

Requirement (iii):.........................................................................................................................7

Requirement (iv):.........................................................................................................................8

Conclusion:....................................................................................................................................11

References:....................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE AND FINANCIAL ACCOUNTING

Introduction:

In this report, honest attempt is taken to elaborate a concise depiction of the corporate

regulation, standard setting related to accounting and owners’ equity from the viewpoint of

accounting. The initial part of the paper would explain the need to regulate financial accounting

and reporting coupled with assigning authority to the managers in voluntary revelation of

financial information. The next part would lay stress on the functions performed by the

“Australian Accounting Standards Board (AASB)” to assist in the global process of standard

setting, which is IFRS. Along with this, a discussion would be made regarding the causes that the

member countries of IASB do not have to adopt IFRS mandatorily. Finally, the paper would

emphasise on choosing four public listed entities in ASX and analysis would be conducted with

respect to owners’ equity position and debt management.

Corporate regulation:

Requirement (i):

Points in favour to regulate financial accounting and reporting:

There are a number of reasons due to which it has become essential to regulate financial

accounting and reporting. The primary reason is that in absence of regulation, the business

organisations would publish information that could be selective and the individuals might

manipulate such information before disclosing the same in the market (Qu et al. 2018). Hence, it

is necessary for the firms to meet certain criteria so that the public interest could be matched with

the present and prospective investors. The criteria have been established by the regulating

authorities in order to ensure that information is delivered at no or minimal cost so that the public

Introduction:

In this report, honest attempt is taken to elaborate a concise depiction of the corporate

regulation, standard setting related to accounting and owners’ equity from the viewpoint of

accounting. The initial part of the paper would explain the need to regulate financial accounting

and reporting coupled with assigning authority to the managers in voluntary revelation of

financial information. The next part would lay stress on the functions performed by the

“Australian Accounting Standards Board (AASB)” to assist in the global process of standard

setting, which is IFRS. Along with this, a discussion would be made regarding the causes that the

member countries of IASB do not have to adopt IFRS mandatorily. Finally, the paper would

emphasise on choosing four public listed entities in ASX and analysis would be conducted with

respect to owners’ equity position and debt management.

Corporate regulation:

Requirement (i):

Points in favour to regulate financial accounting and reporting:

There are a number of reasons due to which it has become essential to regulate financial

accounting and reporting. The primary reason is that in absence of regulation, the business

organisations would publish information that could be selective and the individuals might

manipulate such information before disclosing the same in the market (Qu et al. 2018). Hence, it

is necessary for the firms to meet certain criteria so that the public interest could be matched with

the present and prospective investors. The criteria have been established by the regulating

authorities in order to ensure that information is delivered at no or minimal cost so that the public

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE AND FINANCIAL ACCOUNTING

could be protected from falsified, hidden and fraudulent disclosures. Moreover, the need for true

and real accounting information is rising, as per the demand of the potential investors. When the

organisations receive investments, it is crucial to regulate authorities for intervening into the

issue so that the reporting and accounting formats meet the requirements of the investors.

When an entity views its shares listed in security market, publishing such information

would be effective in standard formats. This would assist to contrast the same with the financial

condition of the peers so that the insiders and the shareholders have same knowledge of

information (Nobes 2014). Hence, regulation is extremely vital for raising the accounting

profession standards.

Points in favour in relation voluntary revelation of financial accounting and reporting:

When the business managers receive the chance of publishing voluntary financial

information, the work would be carried out responsibly and fairly, since the managers would

perform as effective agents of their shareholders or owners. As the managers have full details of

the internal operations of the business entities, it is obvious that their actual financial health

would be known well to them. With the help of such information, the managers could provide a

variety of non-standard financial information to the various stakeholders (Higgins, Milne and

Van Grambergn 2015). This is a situation of signalling theory where the concerned entities

possess the distinctive advantage to transfer considerable information such as probable dividend

as a market signal about their growth tendencies. If the business managers reveal such financial

information, rise in stock prices is obvious, while the external parties would be assured regarding

the actual financial health of the business organisations.

could be protected from falsified, hidden and fraudulent disclosures. Moreover, the need for true

and real accounting information is rising, as per the demand of the potential investors. When the

organisations receive investments, it is crucial to regulate authorities for intervening into the

issue so that the reporting and accounting formats meet the requirements of the investors.

When an entity views its shares listed in security market, publishing such information

would be effective in standard formats. This would assist to contrast the same with the financial

condition of the peers so that the insiders and the shareholders have same knowledge of

information (Nobes 2014). Hence, regulation is extremely vital for raising the accounting

profession standards.

Points in favour in relation voluntary revelation of financial accounting and reporting:

When the business managers receive the chance of publishing voluntary financial

information, the work would be carried out responsibly and fairly, since the managers would

perform as effective agents of their shareholders or owners. As the managers have full details of

the internal operations of the business entities, it is obvious that their actual financial health

would be known well to them. With the help of such information, the managers could provide a

variety of non-standard financial information to the various stakeholders (Higgins, Milne and

Van Grambergn 2015). This is a situation of signalling theory where the concerned entities

possess the distinctive advantage to transfer considerable information such as probable dividend

as a market signal about their growth tendencies. If the business managers reveal such financial

information, rise in stock prices is obvious, while the external parties would be assured regarding

the actual financial health of the business organisations.

5CORPORATE AND FINANCIAL ACCOUNTING

On the other hand, it is noteworthy to mention that the managers would not like to reveal

information regarding the internal business operations and conditions to the different

stakeholders associated with the businesses. There are chances where they might provide

distorted information to the investors because of fear of job loss and as a result, additional funds

could be obtained. In addition, all internal information could not be disclosed publicly due to the

restrictions imposed by regulations (Nguyen and Truong 2017).

Therefore, it is beneficial to regulate financial accounting and reporting rather than

providing the managers with the authority of making voluntary disclosures, as the former would

restrict the occurrence of frauds and manipulations in the financial reports of the entities.

Accounting standard setting:

Requirement (ii):

Participation of AASB in the procedure of international standard setting;

One of the significant visions of AASB is to become the leader as national standard setter

so that it could earn fame in the global excellence centre. This is possible only when they

develop and maintain increased quality of financial reporting standards for the economic sectors

of Australia. The contribution needs to be made through leadership and talent for establishing

global financial reporting standards (Bamber and McMeeking 2016). The ways through which

AASB participates in the procedure of international standard setting constitute of the following:

IASB has formulated certain accounting standards and made amendments to those

standards and they seem to be in tandem with the Australian legislative drafting protocols

as well as the needs of “Federal Register of Legislative Instruments”.

On the other hand, it is noteworthy to mention that the managers would not like to reveal

information regarding the internal business operations and conditions to the different

stakeholders associated with the businesses. There are chances where they might provide

distorted information to the investors because of fear of job loss and as a result, additional funds

could be obtained. In addition, all internal information could not be disclosed publicly due to the

restrictions imposed by regulations (Nguyen and Truong 2017).

Therefore, it is beneficial to regulate financial accounting and reporting rather than

providing the managers with the authority of making voluntary disclosures, as the former would

restrict the occurrence of frauds and manipulations in the financial reports of the entities.

Accounting standard setting:

Requirement (ii):

Participation of AASB in the procedure of international standard setting;

One of the significant visions of AASB is to become the leader as national standard setter

so that it could earn fame in the global excellence centre. This is possible only when they

develop and maintain increased quality of financial reporting standards for the economic sectors

of Australia. The contribution needs to be made through leadership and talent for establishing

global financial reporting standards (Bamber and McMeeking 2016). The ways through which

AASB participates in the procedure of international standard setting constitute of the following:

IASB has formulated certain accounting standards and made amendments to those

standards and they seem to be in tandem with the Australian legislative drafting protocols

as well as the needs of “Federal Register of Legislative Instruments”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE AND FINANCIAL ACCOUNTING

The “Federal Register of Legislative Instruments” is used in order to file accounting

standards as well as compilations and afterwards, disclosures are made in the AASB

website within three days after finalisation (Newberry 2015).

All the significant drafts of IASB and IPSASB are used for recording responses.

Reasons that IFRS is not mandatory for the IASB member nations:

IASB is an independent and private association, which is involved in developing and

approving IFRS. The IFRS foundation strictly supervises all the operations of IASB. The IASB

has been established in 1901 in order to substitute the “International Accounting Standards

Committee (IASC)”. There are 14 IASB member countries and IASB is entirely responsible to

look after all the technical aspects associated with the foundation of IFRS. Some of the

responsibilities include full authority to develop and pursue technical agenda, which requires

consultation with the trustees as well as the public (Carnegie 2014). Along with this, it considers

the issuance and development of IFRS and exposure drafts following the procedure mentioned in

the constitution. Lastly, it takes into account the approval and issuing analyses that the IFRS

Committee has formulated.

The accounting standards vary from nation to nation. In order to bring standardisation as

well as comparability, the associations such as IASB have conducted efforts in formulating a

sole standard, which could be accepted by majority of the nations (Dyckman and Zeff 2015).

Although several efforts are made by IASB, it is still not mandatory for the member countries to

adopt IFRS due to the fact that they have their own national standards. Therefore, the progress of

IFRS is not taking place in phases.

The “Federal Register of Legislative Instruments” is used in order to file accounting

standards as well as compilations and afterwards, disclosures are made in the AASB

website within three days after finalisation (Newberry 2015).

All the significant drafts of IASB and IPSASB are used for recording responses.

Reasons that IFRS is not mandatory for the IASB member nations:

IASB is an independent and private association, which is involved in developing and

approving IFRS. The IFRS foundation strictly supervises all the operations of IASB. The IASB

has been established in 1901 in order to substitute the “International Accounting Standards

Committee (IASC)”. There are 14 IASB member countries and IASB is entirely responsible to

look after all the technical aspects associated with the foundation of IFRS. Some of the

responsibilities include full authority to develop and pursue technical agenda, which requires

consultation with the trustees as well as the public (Carnegie 2014). Along with this, it considers

the issuance and development of IFRS and exposure drafts following the procedure mentioned in

the constitution. Lastly, it takes into account the approval and issuing analyses that the IFRS

Committee has formulated.

The accounting standards vary from nation to nation. In order to bring standardisation as

well as comparability, the associations such as IASB have conducted efforts in formulating a

sole standard, which could be accepted by majority of the nations (Dyckman and Zeff 2015).

Although several efforts are made by IASB, it is still not mandatory for the member countries to

adopt IFRS due to the fact that they have their own national standards. Therefore, the progress of

IFRS is not taking place in phases.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE AND FINANCIAL ACCOUNTING

Owners’ equity:

In this section, four public listed firms in ASX are chosen and they consist of Orica

Limited, Rio Tinto, Fortescue Metals Group and BHP Billiton.

Requirement (iii):

A balance sheet statement of an organisation includes assets, liabilities and equity and in

this segment, equity is taken into consideration. In accordance with this statement, the significant

items in equity comprise of issued capital, retained earnings and reserves (Langfield-Smith et al.

2017).

Issued capital:

As per the annual report of Orica Limited, decline in issued capital could be observed to

$1,954.40 million in 2015 from $1,975 million in 2014. After 2015, increase is significant in

both 2016 and 2017 to $2,025.30 million and $2,068.50 million respectively. For Rio Tinto, the

trend is similar like that of Orica Limited, as issued capital has declined to $220 million in 2015

from $224 million in 2014 and in 2016 and 2017; it has increased to $224 million and $230

million respectively. For Fortescue Metals Group, the trend is fluctuating over the years. This is

because issued capital has increased to $1,294 million in 2015 from $1,289 million in 2014. In

2016, it has increased again to $1,301 million with decline observed to $1,289 million in 2017.

Based on the annual report of BHP Billiton, the trend is identical to those of Orica Limited and

Rio Tinto in the year 2015. The issued capital has declined to $2,043 million in 2015 from

$2,052 million in 2014 and the capital amount in the year 2015 has remained the same in 2016

and 2017 as well. The change in issued capital is due to the intention of keeping an effective

capital structure for funding future capital projects.

Owners’ equity:

In this section, four public listed firms in ASX are chosen and they consist of Orica

Limited, Rio Tinto, Fortescue Metals Group and BHP Billiton.

Requirement (iii):

A balance sheet statement of an organisation includes assets, liabilities and equity and in

this segment, equity is taken into consideration. In accordance with this statement, the significant

items in equity comprise of issued capital, retained earnings and reserves (Langfield-Smith et al.

2017).

Issued capital:

As per the annual report of Orica Limited, decline in issued capital could be observed to

$1,954.40 million in 2015 from $1,975 million in 2014. After 2015, increase is significant in

both 2016 and 2017 to $2,025.30 million and $2,068.50 million respectively. For Rio Tinto, the

trend is similar like that of Orica Limited, as issued capital has declined to $220 million in 2015

from $224 million in 2014 and in 2016 and 2017; it has increased to $224 million and $230

million respectively. For Fortescue Metals Group, the trend is fluctuating over the years. This is

because issued capital has increased to $1,294 million in 2015 from $1,289 million in 2014. In

2016, it has increased again to $1,301 million with decline observed to $1,289 million in 2017.

Based on the annual report of BHP Billiton, the trend is identical to those of Orica Limited and

Rio Tinto in the year 2015. The issued capital has declined to $2,043 million in 2015 from

$2,052 million in 2014 and the capital amount in the year 2015 has remained the same in 2016

and 2017 as well. The change in issued capital is due to the intention of keeping an effective

capital structure for funding future capital projects.

8CORPORATE AND FINANCIAL ACCOUNTING

Retained earnings:

After issued capital, retained earnings are observed to be the next equity item for all the

chosen four organisations. Retained earnings are deemed to be the gains and losses made by an

entity from its inception after settlement of dividend payments to the shareholders (Sivathaasan

2016). In case of this item, similar trend is observed among Rio Tinto, Orica Limited and BHP

Billiton, since they have declined over the years. However, Fortescue Metals Group have

experienced rise in this item due to lower operating expenses incurred over the years resulting in

more net income.

Reserves:

Finally, reserves are considered to be the final equity item. In this case, the amount of

reserves is found to be negative for Orica Limited, while the trend is fluctuating for the other

three organisations with positive reserve balance. As mentioned by Pilcher and Gilchrist (2018),

reserves are that portion of equity accumulated in excess of main issued capital. The reserve

amount is negative for Orica Limited because it has suffered business losses over the years.

However, due to the large asset base of BHP Billiton owing to diversified global

operations, it accumulates the highest amount of funds from equity shares compared to the other

three organisations having operations in the Australian mining sector.

Requirement (iv):

The debt-to-equity ratio is used for analysing the debt and equity position of the selected

organisations for gaining an insight about their capital structure (Warren and Jones 2018). It is

illustrated briefly in the form of tables as follows:

Retained earnings:

After issued capital, retained earnings are observed to be the next equity item for all the

chosen four organisations. Retained earnings are deemed to be the gains and losses made by an

entity from its inception after settlement of dividend payments to the shareholders (Sivathaasan

2016). In case of this item, similar trend is observed among Rio Tinto, Orica Limited and BHP

Billiton, since they have declined over the years. However, Fortescue Metals Group have

experienced rise in this item due to lower operating expenses incurred over the years resulting in

more net income.

Reserves:

Finally, reserves are considered to be the final equity item. In this case, the amount of

reserves is found to be negative for Orica Limited, while the trend is fluctuating for the other

three organisations with positive reserve balance. As mentioned by Pilcher and Gilchrist (2018),

reserves are that portion of equity accumulated in excess of main issued capital. The reserve

amount is negative for Orica Limited because it has suffered business losses over the years.

However, due to the large asset base of BHP Billiton owing to diversified global

operations, it accumulates the highest amount of funds from equity shares compared to the other

three organisations having operations in the Australian mining sector.

Requirement (iv):

The debt-to-equity ratio is used for analysing the debt and equity position of the selected

organisations for gaining an insight about their capital structure (Warren and Jones 2018). It is

illustrated briefly in the form of tables as follows:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE AND FINANCIAL ACCOUNTING

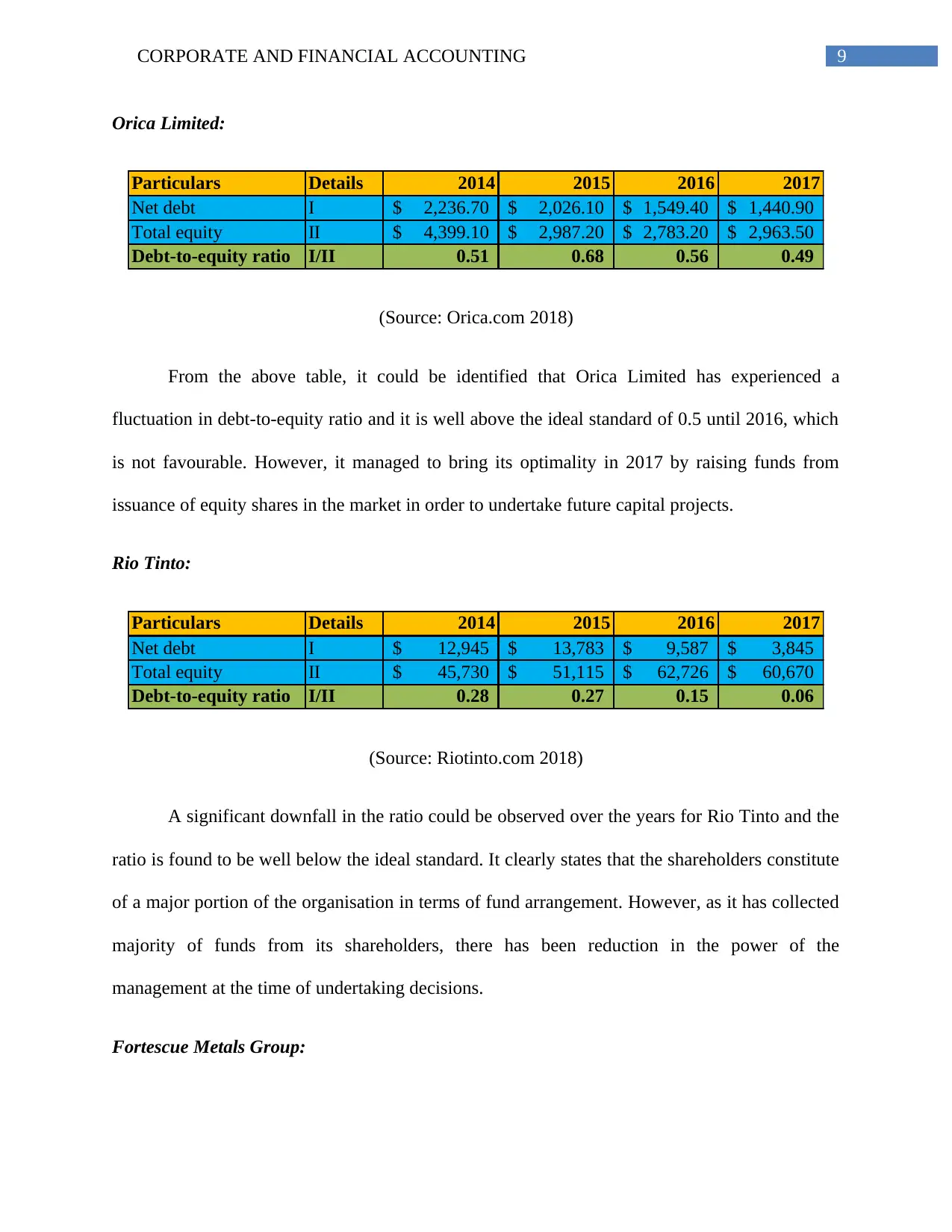

Orica Limited:

Particulars Details 2014 2015 2016 2017

Net debt I 2,236.70$ 2,026.10$ 1,549.40$ 1,440.90$

Total equity II 4,399.10$ 2,987.20$ 2,783.20$ 2,963.50$

Debt-to-equity ratio I/II 0.51 0.68 0.56 0.49

(Source: Orica.com 2018)

From the above table, it could be identified that Orica Limited has experienced a

fluctuation in debt-to-equity ratio and it is well above the ideal standard of 0.5 until 2016, which

is not favourable. However, it managed to bring its optimality in 2017 by raising funds from

issuance of equity shares in the market in order to undertake future capital projects.

Rio Tinto:

Particulars Details 2014 2015 2016 2017

Net debt I 12,945$ 13,783$ 9,587$ 3,845$

Total equity II 45,730$ 51,115$ 62,726$ 60,670$

Debt-to-equity ratio I/II 0.28 0.27 0.15 0.06

(Source: Riotinto.com 2018)

A significant downfall in the ratio could be observed over the years for Rio Tinto and the

ratio is found to be well below the ideal standard. It clearly states that the shareholders constitute

of a major portion of the organisation in terms of fund arrangement. However, as it has collected

majority of funds from its shareholders, there has been reduction in the power of the

management at the time of undertaking decisions.

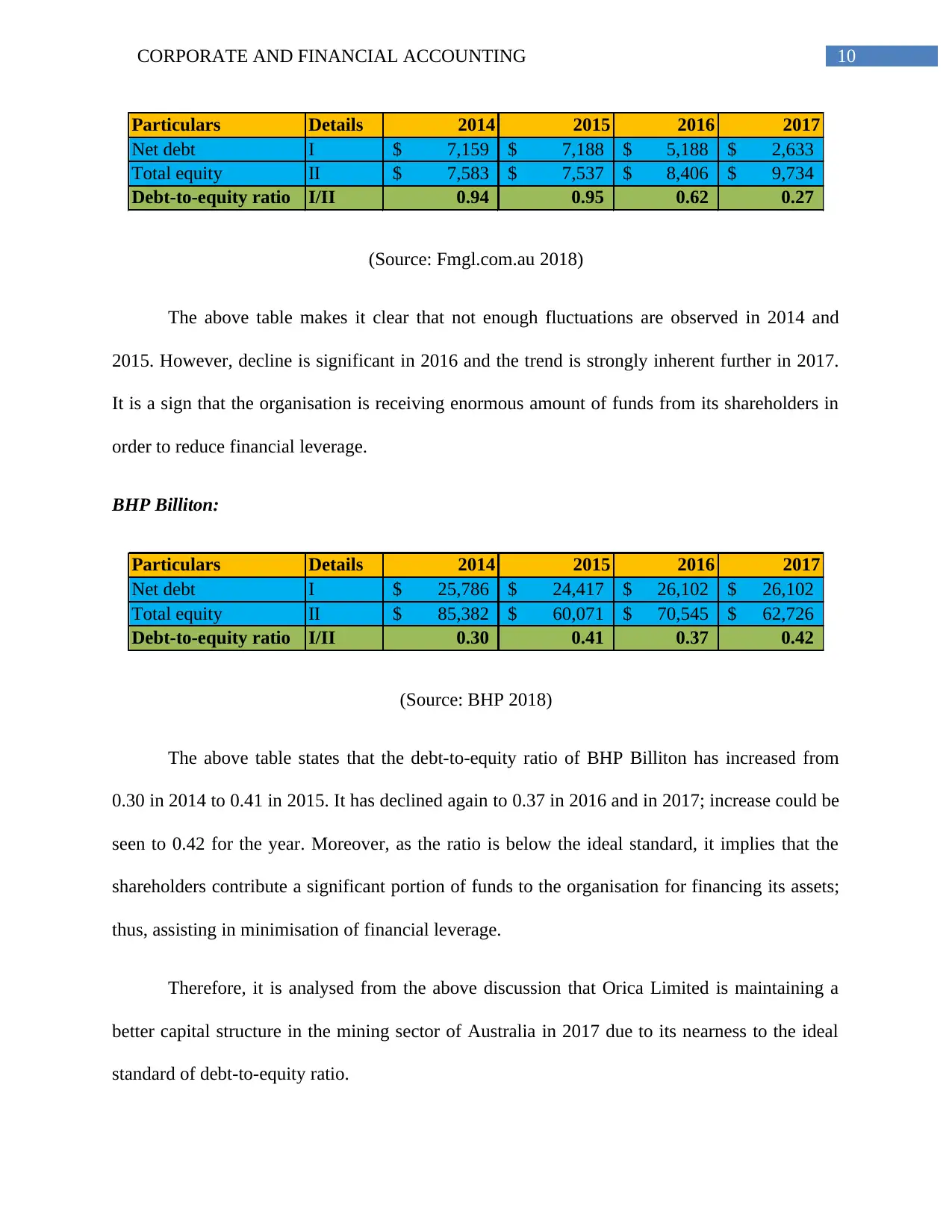

Fortescue Metals Group:

Orica Limited:

Particulars Details 2014 2015 2016 2017

Net debt I 2,236.70$ 2,026.10$ 1,549.40$ 1,440.90$

Total equity II 4,399.10$ 2,987.20$ 2,783.20$ 2,963.50$

Debt-to-equity ratio I/II 0.51 0.68 0.56 0.49

(Source: Orica.com 2018)

From the above table, it could be identified that Orica Limited has experienced a

fluctuation in debt-to-equity ratio and it is well above the ideal standard of 0.5 until 2016, which

is not favourable. However, it managed to bring its optimality in 2017 by raising funds from

issuance of equity shares in the market in order to undertake future capital projects.

Rio Tinto:

Particulars Details 2014 2015 2016 2017

Net debt I 12,945$ 13,783$ 9,587$ 3,845$

Total equity II 45,730$ 51,115$ 62,726$ 60,670$

Debt-to-equity ratio I/II 0.28 0.27 0.15 0.06

(Source: Riotinto.com 2018)

A significant downfall in the ratio could be observed over the years for Rio Tinto and the

ratio is found to be well below the ideal standard. It clearly states that the shareholders constitute

of a major portion of the organisation in terms of fund arrangement. However, as it has collected

majority of funds from its shareholders, there has been reduction in the power of the

management at the time of undertaking decisions.

Fortescue Metals Group:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CORPORATE AND FINANCIAL ACCOUNTING

Particulars Details 2014 2015 2016 2017

Net debt I 7,159$ 7,188$ 5,188$ 2,633$

Total equity II 7,583$ 7,537$ 8,406$ 9,734$

Debt-to-equity ratio I/II 0.94 0.95 0.62 0.27

(Source: Fmgl.com.au 2018)

The above table makes it clear that not enough fluctuations are observed in 2014 and

2015. However, decline is significant in 2016 and the trend is strongly inherent further in 2017.

It is a sign that the organisation is receiving enormous amount of funds from its shareholders in

order to reduce financial leverage.

BHP Billiton:

Particulars Details 2014 2015 2016 2017

Net debt I 25,786$ 24,417$ 26,102$ 26,102$

Total equity II 85,382$ 60,071$ 70,545$ 62,726$

Debt-to-equity ratio I/II 0.30 0.41 0.37 0.42

(Source: BHP 2018)

The above table states that the debt-to-equity ratio of BHP Billiton has increased from

0.30 in 2014 to 0.41 in 2015. It has declined again to 0.37 in 2016 and in 2017; increase could be

seen to 0.42 for the year. Moreover, as the ratio is below the ideal standard, it implies that the

shareholders contribute a significant portion of funds to the organisation for financing its assets;

thus, assisting in minimisation of financial leverage.

Therefore, it is analysed from the above discussion that Orica Limited is maintaining a

better capital structure in the mining sector of Australia in 2017 due to its nearness to the ideal

standard of debt-to-equity ratio.

Particulars Details 2014 2015 2016 2017

Net debt I 7,159$ 7,188$ 5,188$ 2,633$

Total equity II 7,583$ 7,537$ 8,406$ 9,734$

Debt-to-equity ratio I/II 0.94 0.95 0.62 0.27

(Source: Fmgl.com.au 2018)

The above table makes it clear that not enough fluctuations are observed in 2014 and

2015. However, decline is significant in 2016 and the trend is strongly inherent further in 2017.

It is a sign that the organisation is receiving enormous amount of funds from its shareholders in

order to reduce financial leverage.

BHP Billiton:

Particulars Details 2014 2015 2016 2017

Net debt I 25,786$ 24,417$ 26,102$ 26,102$

Total equity II 85,382$ 60,071$ 70,545$ 62,726$

Debt-to-equity ratio I/II 0.30 0.41 0.37 0.42

(Source: BHP 2018)

The above table states that the debt-to-equity ratio of BHP Billiton has increased from

0.30 in 2014 to 0.41 in 2015. It has declined again to 0.37 in 2016 and in 2017; increase could be

seen to 0.42 for the year. Moreover, as the ratio is below the ideal standard, it implies that the

shareholders contribute a significant portion of funds to the organisation for financing its assets;

thus, assisting in minimisation of financial leverage.

Therefore, it is analysed from the above discussion that Orica Limited is maintaining a

better capital structure in the mining sector of Australia in 2017 due to its nearness to the ideal

standard of debt-to-equity ratio.

11CORPORATE AND FINANCIAL ACCOUNTING

Conclusion:

From the above assessment, it is found that there is necessity to regulate financial

accounting and reporting for ensuring accurate disclosure of financial information by preventing

fraud and other organisational malpractices. The managers should not be allowed to conduct

voluntary disclosure of financial information, as they might provide distorted figures to show

favourable financial condition of the entity owing to the fear of job loss. Moreover, it is not

mandatory for the IASB nations to adopt IFRS due to the presence of their national accounting

standards and they might encounter serious issues while converging with IFRS. Finally, it has

been evaluated that Orica Limited has maintained the optimal capital structure in the mining

sector of Australia, as it has performed closer to the industrial average.

Conclusion:

From the above assessment, it is found that there is necessity to regulate financial

accounting and reporting for ensuring accurate disclosure of financial information by preventing

fraud and other organisational malpractices. The managers should not be allowed to conduct

voluntary disclosure of financial information, as they might provide distorted figures to show

favourable financial condition of the entity owing to the fear of job loss. Moreover, it is not

mandatory for the IASB nations to adopt IFRS due to the presence of their national accounting

standards and they might encounter serious issues while converging with IFRS. Finally, it has

been evaluated that Orica Limited has maintained the optimal capital structure in the mining

sector of Australia, as it has performed closer to the industrial average.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.