Final Examination - Financial Accounting and Reporting, MAC001A, 2021

VerifiedAdded on 2021/07/23

|16

|3770

|93

Homework Assignment

AI Summary

This document presents a comprehensive solution to the Final Examination for the Financial Accounting and Reporting course (MAC001A) from Trimester 1, 2021. The exam covers a wide range of topics including institutional arrangements for setting accounting standards, the conceptual framework, accounting methods, lease accounting, employee benefits, financial instruments, segment reporting, corporate social responsibility, cash flow statements, comprehensive income statements, and foreign currency translation. The document includes detailed solutions to various questions, including journal entries for lease accounting and employee benefits, along with theoretical explanations and practical applications. Additional exercises and theoretical components are also included to aid in understanding the concepts. The exam emphasizes key topics such as reporting entity, stakeholder theory, creative accounting, and the difference between presentation and functional currency.

Final Exam Guideline 0121: Financial Accounting & Reporting April 2021 Page 1 of 6

FINAL EXAMINATION (Online)

TRIMESTER 1, 2021

Exam Guideline

NAME: STUDENT ID:

SUBJECT NAME: Financial Accounting and Reporting

SUBJECT CODE: MAC001A

TIME ALLOWED: 2 Hour plus 5 minutes reading time

PERMITTED MATERIALS:

• This is an Open Book exam.

INSTRUCTIONS FOR STUDENTS:

• You do not require a separate answer booklet. Please type your responses in the space

provided.

• Type your full name and ID at the top of this page.

• Answer all questions.

FINAL EXAMINATION (Online)

TRIMESTER 1, 2021

Exam Guideline

NAME: STUDENT ID:

SUBJECT NAME: Financial Accounting and Reporting

SUBJECT CODE: MAC001A

TIME ALLOWED: 2 Hour plus 5 minutes reading time

PERMITTED MATERIALS:

• This is an Open Book exam.

INSTRUCTIONS FOR STUDENTS:

• You do not require a separate answer booklet. Please type your responses in the space

provided.

• Type your full name and ID at the top of this page.

• Answer all questions.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Final Exam Guideline 0121: Financial Accounting & Reporting April 2021 Page 2 of 6

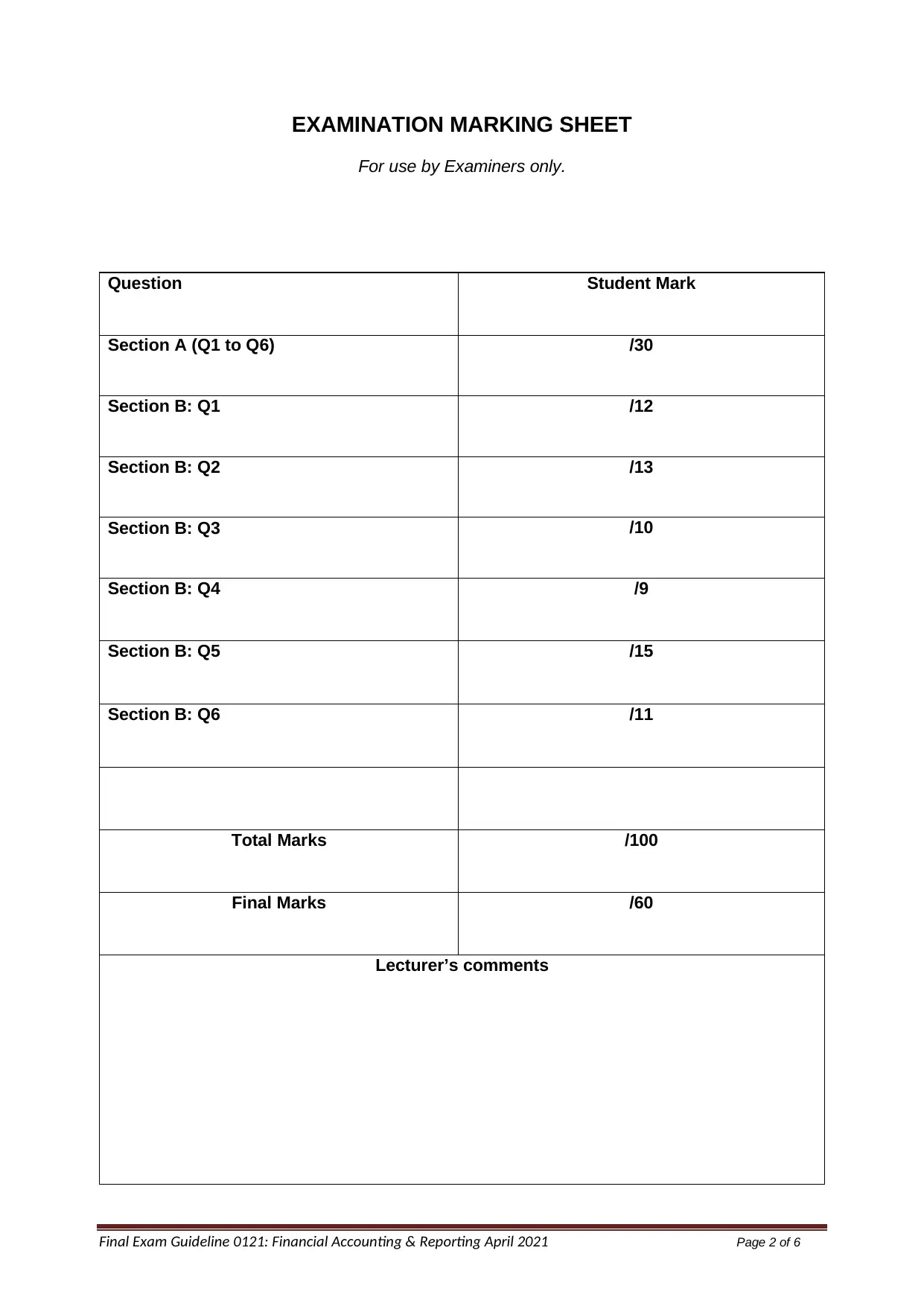

EXAMINATION MARKING SHEET

For use by Examiners only.

Question Student Mark

Section A (Q1 to Q6) /30

Section B: Q1 /12

Section B: Q2 /13

Section B: Q3 /10

Section B: Q4 /9

Section B: Q5 /15

Section B: Q6 /11

Total Marks /100

Final Marks /60

Lecturer’s comments

EXAMINATION MARKING SHEET

For use by Examiners only.

Question Student Mark

Section A (Q1 to Q6) /30

Section B: Q1 /12

Section B: Q2 /13

Section B: Q3 /10

Section B: Q4 /9

Section B: Q5 /15

Section B: Q6 /11

Total Marks /100

Final Marks /60

Lecturer’s comments

Final Exam Guideline 0121: Financial Accounting & Reporting April 2021 Page 3 of 6

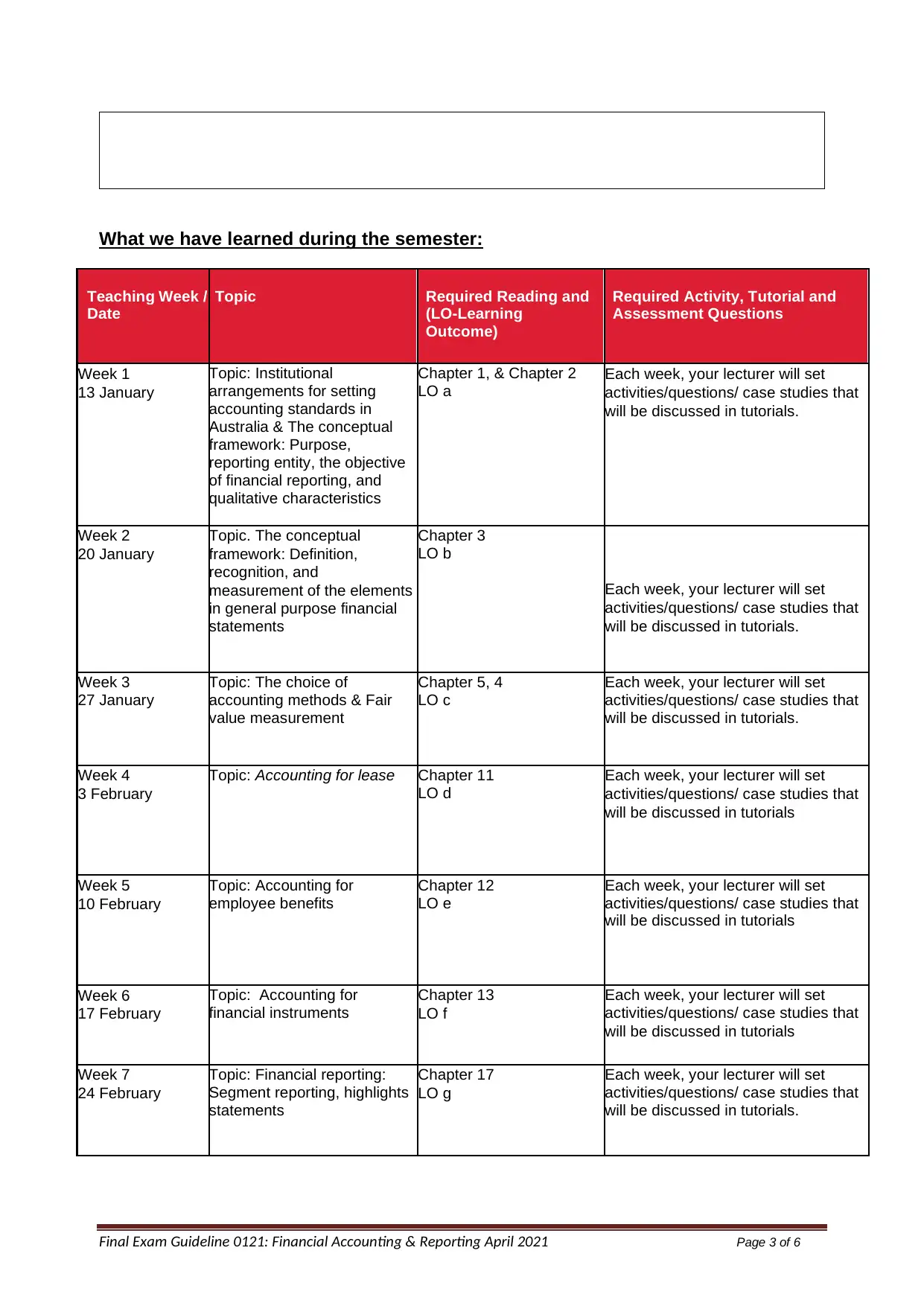

What we have learned during the semester:

Teaching Week /

Date

Topic Required Reading and

(LO-Learning

Outcome)

Required Activity, Tutorial and

Assessment Questions

Week 1

13 January

Topic: Institutional

arrangements for setting

accounting standards in

Australia & The conceptual

framework: Purpose,

reporting entity, the objective

of financial reporting, and

qualitative characteristics

Chapter 1, & Chapter 2

LO a

Each week, your lecturer will set

activities/questions/ case studies that

will be discussed in tutorials.

Week 2

20 January

Topic. The conceptual

framework: Definition,

recognition, and

measurement of the elements

in general purpose financial

statements

Chapter 3

LO b

Each week, your lecturer will set

activities/questions/ case studies that

will be discussed in tutorials.

Week 3

27 January

Topic: The choice of

accounting methods & Fair

value measurement

Chapter 5, 4

LO c

Each week, your lecturer will set

activities/questions/ case studies that

will be discussed in tutorials.

Week 4

3 February

Topic: Accounting for lease Chapter 11

LO d

Each week, your lecturer will set

activities/questions/ case studies that

will be discussed in tutorials

Week 5

10 February

Topic: Accounting for

employee benefits

Chapter 12

LO e

Each week, your lecturer will set

activities/questions/ case studies that

will be discussed in tutorials

Week 6

17 February

Topic: Accounting for

financial instruments

Chapter 13

LO f

Each week, your lecturer will set

activities/questions/ case studies that

will be discussed in tutorials

Week 7

24 February

Topic: Financial reporting:

Segment reporting, highlights

statements

Chapter 17

LO g

Each week, your lecturer will set

activities/questions/ case studies that

will be discussed in tutorials.

What we have learned during the semester:

Teaching Week /

Date

Topic Required Reading and

(LO-Learning

Outcome)

Required Activity, Tutorial and

Assessment Questions

Week 1

13 January

Topic: Institutional

arrangements for setting

accounting standards in

Australia & The conceptual

framework: Purpose,

reporting entity, the objective

of financial reporting, and

qualitative characteristics

Chapter 1, & Chapter 2

LO a

Each week, your lecturer will set

activities/questions/ case studies that

will be discussed in tutorials.

Week 2

20 January

Topic. The conceptual

framework: Definition,

recognition, and

measurement of the elements

in general purpose financial

statements

Chapter 3

LO b

Each week, your lecturer will set

activities/questions/ case studies that

will be discussed in tutorials.

Week 3

27 January

Topic: The choice of

accounting methods & Fair

value measurement

Chapter 5, 4

LO c

Each week, your lecturer will set

activities/questions/ case studies that

will be discussed in tutorials.

Week 4

3 February

Topic: Accounting for lease Chapter 11

LO d

Each week, your lecturer will set

activities/questions/ case studies that

will be discussed in tutorials

Week 5

10 February

Topic: Accounting for

employee benefits

Chapter 12

LO e

Each week, your lecturer will set

activities/questions/ case studies that

will be discussed in tutorials

Week 6

17 February

Topic: Accounting for

financial instruments

Chapter 13

LO f

Each week, your lecturer will set

activities/questions/ case studies that

will be discussed in tutorials

Week 7

24 February

Topic: Financial reporting:

Segment reporting, highlights

statements

Chapter 17

LO g

Each week, your lecturer will set

activities/questions/ case studies that

will be discussed in tutorials.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Final Exam Guideline 0121: Financial Accounting & Reporting April 2021 Page 4 of 6

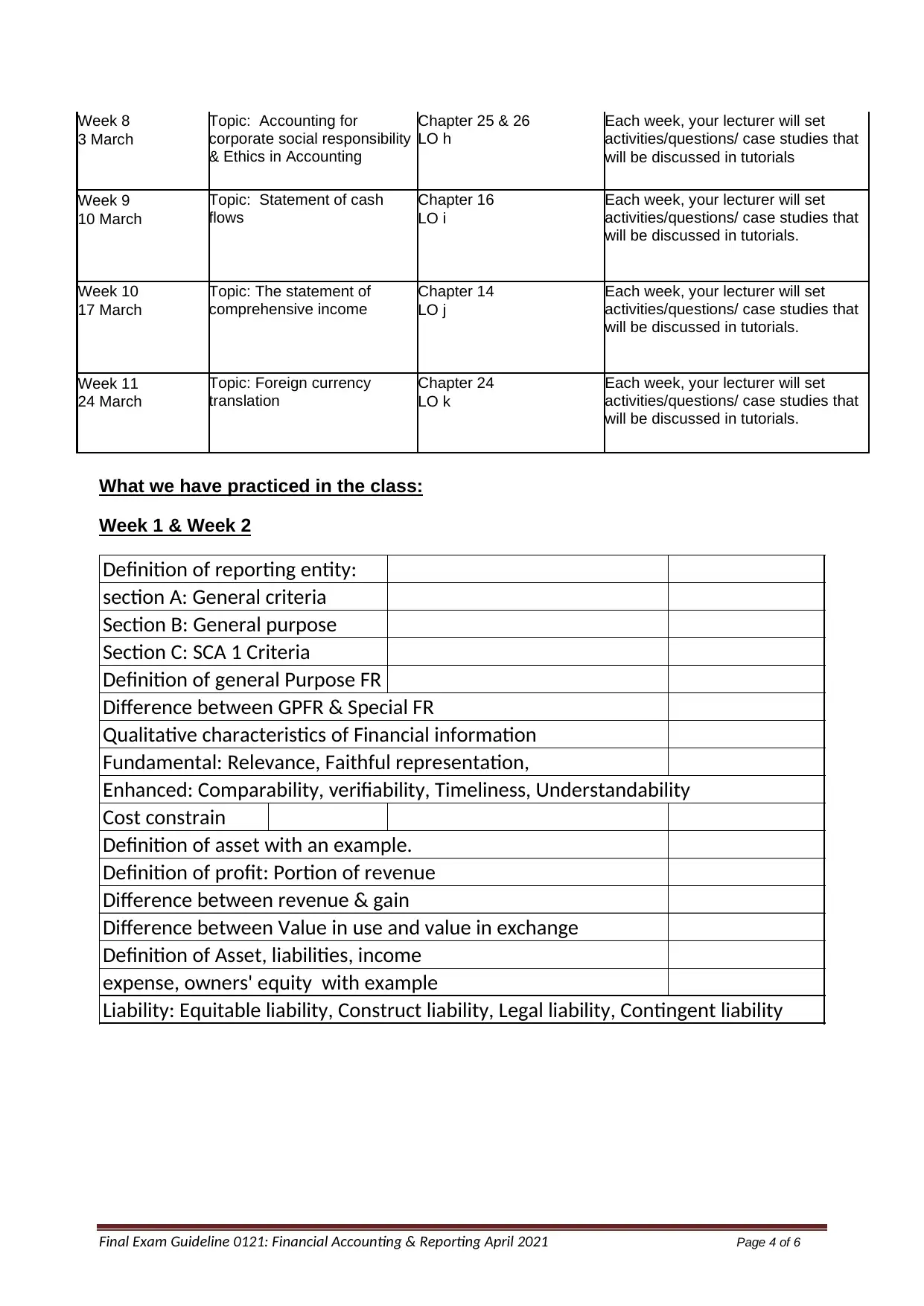

Week 8

3 March

Topic: Accounting for

corporate social responsibility

& Ethics in Accounting

Chapter 25 & 26

LO h

Each week, your lecturer will set

activities/questions/ case studies that

will be discussed in tutorials

Week 9

10 March

Topic: Statement of cash

flows

Chapter 16

LO i

Each week, your lecturer will set

activities/questions/ case studies that

will be discussed in tutorials.

Week 10

17 March

Topic: The statement of

comprehensive income

Chapter 14

LO j

Each week, your lecturer will set

activities/questions/ case studies that

will be discussed in tutorials.

Week 11

24 March

Topic: Foreign currency

translation

Chapter 24

LO k

Each week, your lecturer will set

activities/questions/ case studies that

will be discussed in tutorials.

What we have practiced in the class:

Week 1 & Week 2

Definition of reporting entity:

section A: General criteria

Section B: General purpose

Section C: SCA 1 Criteria

Definition of general Purpose FR

Difference between GPFR & Special FR

Qualitative characteristics of Financial information

Fundamental: Relevance, Faithful representation,

Enhanced: Comparability, verifiability, Timeliness, Understandability

Cost constrain

Definition of asset with an example.

Definition of profit: Portion of revenue

Difference between revenue & gain

Difference between Value in use and value in exchange

Definition of Asset, liabilities, income

expense, owners' equity with example

Liability: Equitable liability, Construct liability, Legal liability, Contingent liability

Week 8

3 March

Topic: Accounting for

corporate social responsibility

& Ethics in Accounting

Chapter 25 & 26

LO h

Each week, your lecturer will set

activities/questions/ case studies that

will be discussed in tutorials

Week 9

10 March

Topic: Statement of cash

flows

Chapter 16

LO i

Each week, your lecturer will set

activities/questions/ case studies that

will be discussed in tutorials.

Week 10

17 March

Topic: The statement of

comprehensive income

Chapter 14

LO j

Each week, your lecturer will set

activities/questions/ case studies that

will be discussed in tutorials.

Week 11

24 March

Topic: Foreign currency

translation

Chapter 24

LO k

Each week, your lecturer will set

activities/questions/ case studies that

will be discussed in tutorials.

What we have practiced in the class:

Week 1 & Week 2

Definition of reporting entity:

section A: General criteria

Section B: General purpose

Section C: SCA 1 Criteria

Definition of general Purpose FR

Difference between GPFR & Special FR

Qualitative characteristics of Financial information

Fundamental: Relevance, Faithful representation,

Enhanced: Comparability, verifiability, Timeliness, Understandability

Cost constrain

Definition of asset with an example.

Definition of profit: Portion of revenue

Difference between revenue & gain

Difference between Value in use and value in exchange

Definition of Asset, liabilities, income

expense, owners' equity with example

Liability: Equitable liability, Construct liability, Legal liability, Contingent liability

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Final Exam Guideline 0121: Financial Accounting & Reporting April 2021 Page 5 of 6

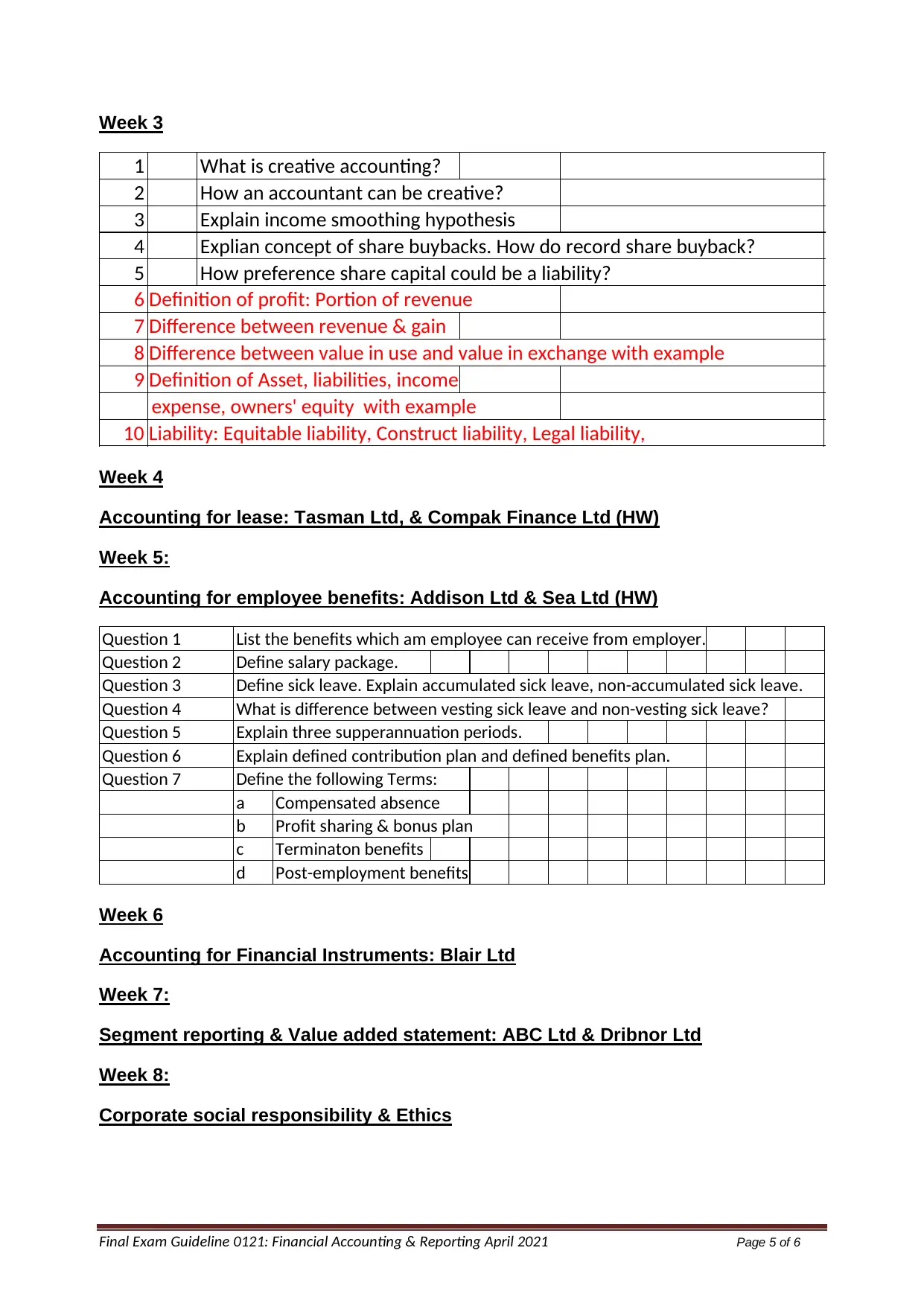

Week 3

Week 4

Accounting for lease: Tasman Ltd, & Compak Finance Ltd (HW)

Week 5:

Accounting for employee benefits: Addison Ltd & Sea Ltd (HW)

Week 6

Accounting for Financial Instruments: Blair Ltd

Week 7:

Segment reporting & Value added statement: ABC Ltd & Dribnor Ltd

Week 8:

Corporate social responsibility & Ethics

1 What is creative accounting?

2 How an accountant can be creative?

3 Explain income smoothing hypothesis

4 Explian concept of share buybacks. How do record share buyback?

5 How preference share capital could be a liability?

6 Definition of profit: Portion of revenue

7 Difference between revenue & gain

8 Difference between value in use and value in exchange with example

9 Definition of Asset, liabilities, income

expense, owners' equity with example

10 Liability: Equitable liability, Construct liability, Legal liability,

Question 1 List the benefits which am employee can receive from employer.

Question 2 Define salary package.

Question 3 Define sick leave. Explain accumulated sick leave, non-accumulated sick leave.

Question 4 What is difference between vesting sick leave and non-vesting sick leave?

Question 5 Explain three supperannuation periods.

Question 6 Explain defined contribution plan and defined benefits plan.

Question 7 Define the following Terms:

a Compensated absence

b Profit sharing & bonus plan

c Terminaton benefits

d Post-employment benefits

Week 3

Week 4

Accounting for lease: Tasman Ltd, & Compak Finance Ltd (HW)

Week 5:

Accounting for employee benefits: Addison Ltd & Sea Ltd (HW)

Week 6

Accounting for Financial Instruments: Blair Ltd

Week 7:

Segment reporting & Value added statement: ABC Ltd & Dribnor Ltd

Week 8:

Corporate social responsibility & Ethics

1 What is creative accounting?

2 How an accountant can be creative?

3 Explain income smoothing hypothesis

4 Explian concept of share buybacks. How do record share buyback?

5 How preference share capital could be a liability?

6 Definition of profit: Portion of revenue

7 Difference between revenue & gain

8 Difference between value in use and value in exchange with example

9 Definition of Asset, liabilities, income

expense, owners' equity with example

10 Liability: Equitable liability, Construct liability, Legal liability,

Question 1 List the benefits which am employee can receive from employer.

Question 2 Define salary package.

Question 3 Define sick leave. Explain accumulated sick leave, non-accumulated sick leave.

Question 4 What is difference between vesting sick leave and non-vesting sick leave?

Question 5 Explain three supperannuation periods.

Question 6 Explain defined contribution plan and defined benefits plan.

Question 7 Define the following Terms:

a Compensated absence

b Profit sharing & bonus plan

c Terminaton benefits

d Post-employment benefits

Final Exam Guideline 0121: Financial Accounting & Reporting April 2021 Page 6 of 6

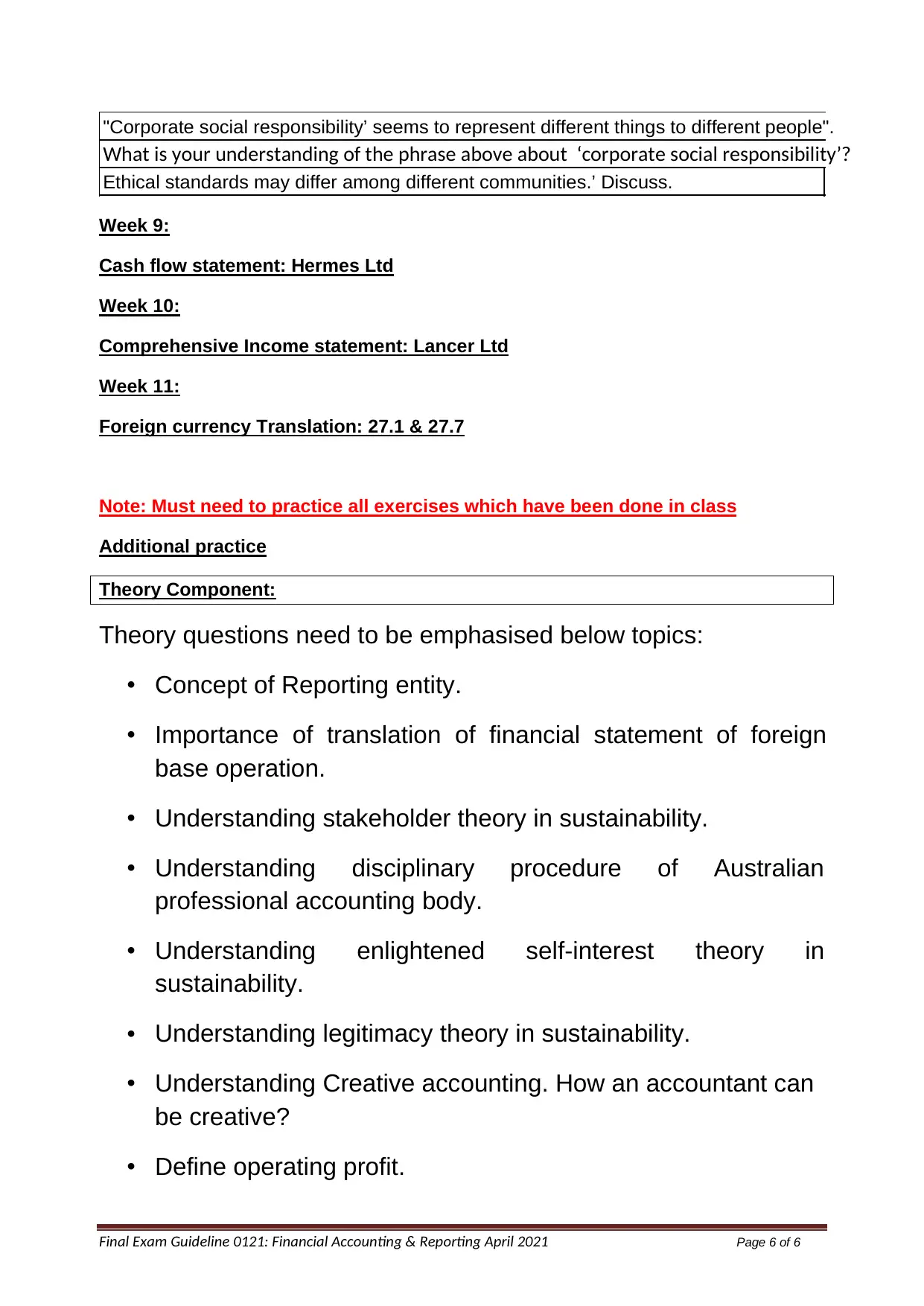

Week 9:

Cash flow statement: Hermes Ltd

Week 10:

Comprehensive Income statement: Lancer Ltd

Week 11:

Foreign currency Translation: 27.1 & 27.7

Note: Must need to practice all exercises which have been done in class

Additional practice

Theory Component:

Theory questions need to be emphasised below topics:

• Concept of Reporting entity.

• Importance of translation of financial statement of foreign

base operation.

• Understanding stakeholder theory in sustainability.

• Understanding disciplinary procedure of Australian

professional accounting body.

• Understanding enlightened self-interest theory in

sustainability.

• Understanding legitimacy theory in sustainability.

• Understanding Creative accounting. How an accountant can

be creative?

• Define operating profit.

"Corporate social responsibility’ seems to represent different things to different people".

What is your understanding of the phrase above about ‘corporate social responsibility’?

Ethical standards may differ among different communities.’ Discuss.

Week 9:

Cash flow statement: Hermes Ltd

Week 10:

Comprehensive Income statement: Lancer Ltd

Week 11:

Foreign currency Translation: 27.1 & 27.7

Note: Must need to practice all exercises which have been done in class

Additional practice

Theory Component:

Theory questions need to be emphasised below topics:

• Concept of Reporting entity.

• Importance of translation of financial statement of foreign

base operation.

• Understanding stakeholder theory in sustainability.

• Understanding disciplinary procedure of Australian

professional accounting body.

• Understanding enlightened self-interest theory in

sustainability.

• Understanding legitimacy theory in sustainability.

• Understanding Creative accounting. How an accountant can

be creative?

• Define operating profit.

"Corporate social responsibility’ seems to represent different things to different people".

What is your understanding of the phrase above about ‘corporate social responsibility’?

Ethical standards may differ among different communities.’ Discuss.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Final Exam Guideline 0121: Financial Accounting & Reporting April 2021 Page 7 of 6

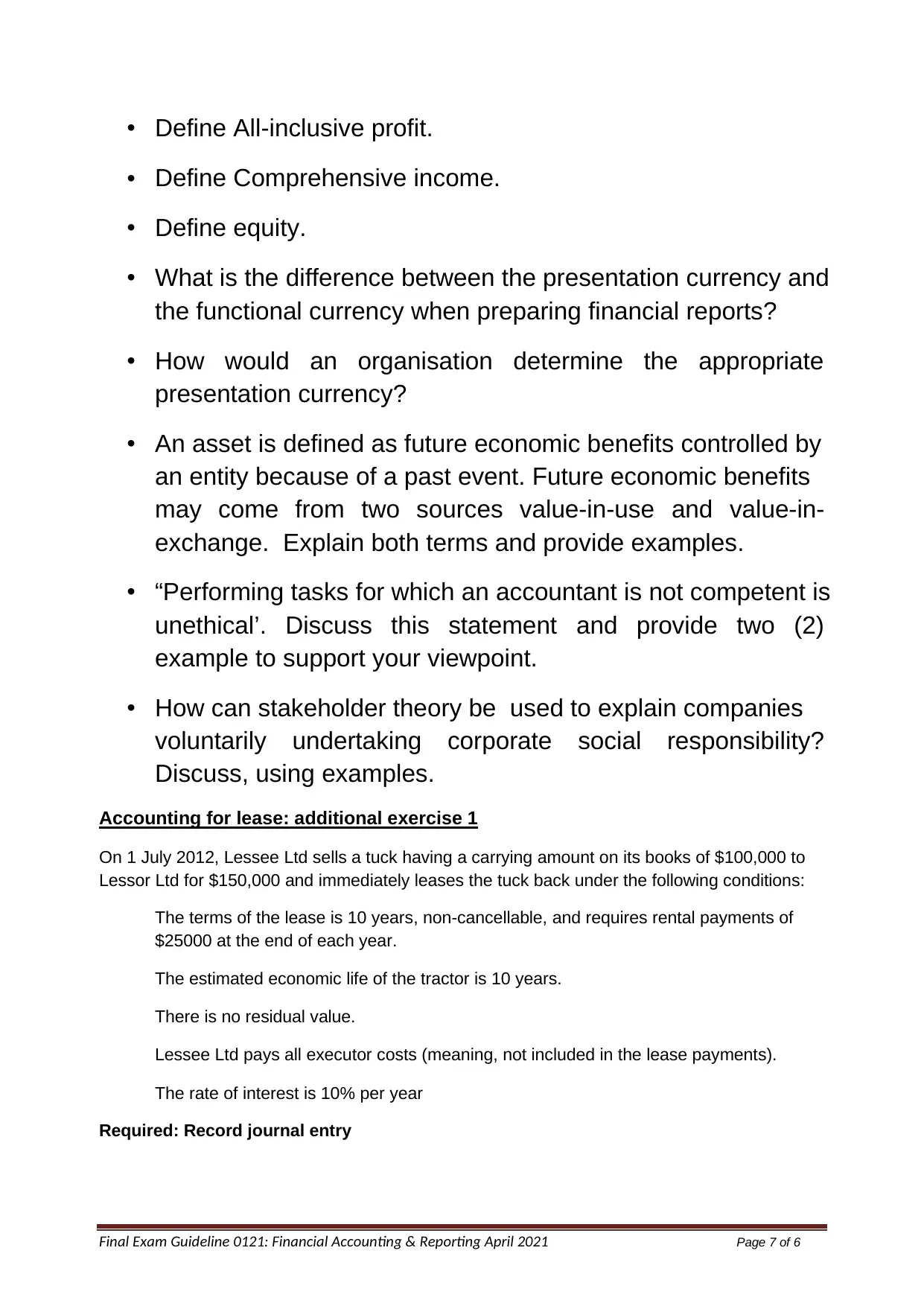

• Define All-inclusive profit.

• Define Comprehensive income.

• Define equity.

• What is the difference between the presentation currency and

the functional currency when preparing financial reports?

• How would an organisation determine the appropriate

presentation currency?

• An asset is defined as future economic benefits controlled by

an entity because of a past event. Future economic benefits

may come from two sources value-in-use and value-in-

exchange. Explain both terms and provide examples.

• “Performing tasks for which an accountant is not competent is

unethical’. Discuss this statement and provide two (2)

example to support your viewpoint.

• How can stakeholder theory be used to explain companies

voluntarily undertaking corporate social responsibility?

Discuss, using examples.

Accounting for lease: additional exercise 1

On 1 July 2012, Lessee Ltd sells a tuck having a carrying amount on its books of $100,000 to

Lessor Ltd for $150,000 and immediately leases the tuck back under the following conditions:

The terms of the lease is 10 years, non-cancellable, and requires rental payments of

$25000 at the end of each year.

The estimated economic life of the tractor is 10 years.

There is no residual value.

Lessee Ltd pays all executor costs (meaning, not included in the lease payments).

The rate of interest is 10% per year

Required: Record journal entry

• Define All-inclusive profit.

• Define Comprehensive income.

• Define equity.

• What is the difference between the presentation currency and

the functional currency when preparing financial reports?

• How would an organisation determine the appropriate

presentation currency?

• An asset is defined as future economic benefits controlled by

an entity because of a past event. Future economic benefits

may come from two sources value-in-use and value-in-

exchange. Explain both terms and provide examples.

• “Performing tasks for which an accountant is not competent is

unethical’. Discuss this statement and provide two (2)

example to support your viewpoint.

• How can stakeholder theory be used to explain companies

voluntarily undertaking corporate social responsibility?

Discuss, using examples.

Accounting for lease: additional exercise 1

On 1 July 2012, Lessee Ltd sells a tuck having a carrying amount on its books of $100,000 to

Lessor Ltd for $150,000 and immediately leases the tuck back under the following conditions:

The terms of the lease is 10 years, non-cancellable, and requires rental payments of

$25000 at the end of each year.

The estimated economic life of the tractor is 10 years.

There is no residual value.

Lessee Ltd pays all executor costs (meaning, not included in the lease payments).

The rate of interest is 10% per year

Required: Record journal entry

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Final Exam Guideline 0121: Financial Accounting & Reporting April 2021 Page 8 of 6

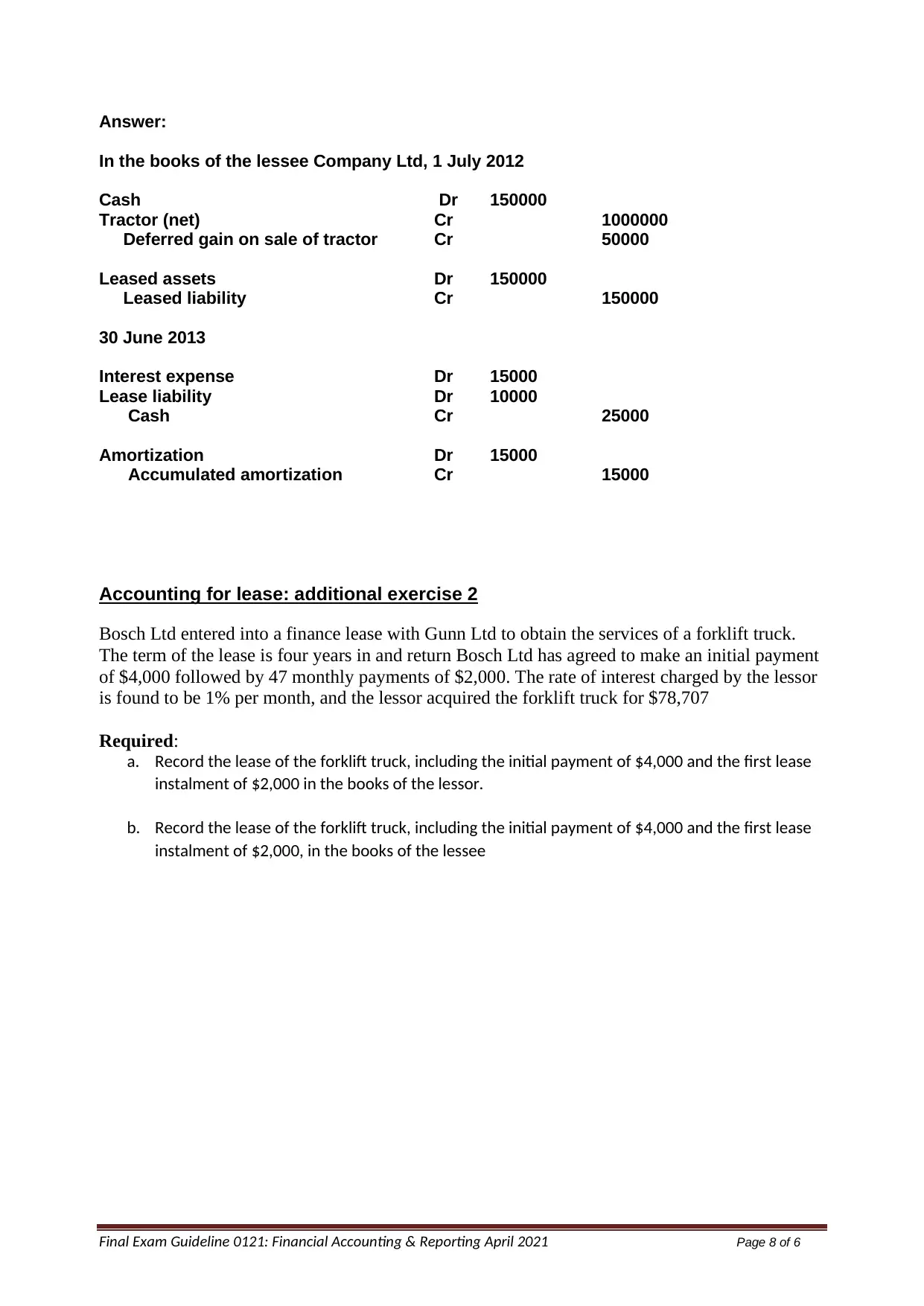

Answer:

In the books of the lessee Company Ltd, 1 July 2012

Cash Dr 150000

Tractor (net) Cr 1000000

Deferred gain on sale of tractor Cr 50000

Leased assets Dr 150000

Leased liability Cr 150000

30 June 2013

Interest expense Dr 15000

Lease liability Dr 10000

Cash Cr 25000

Amortization Dr 15000

Accumulated amortization Cr 15000

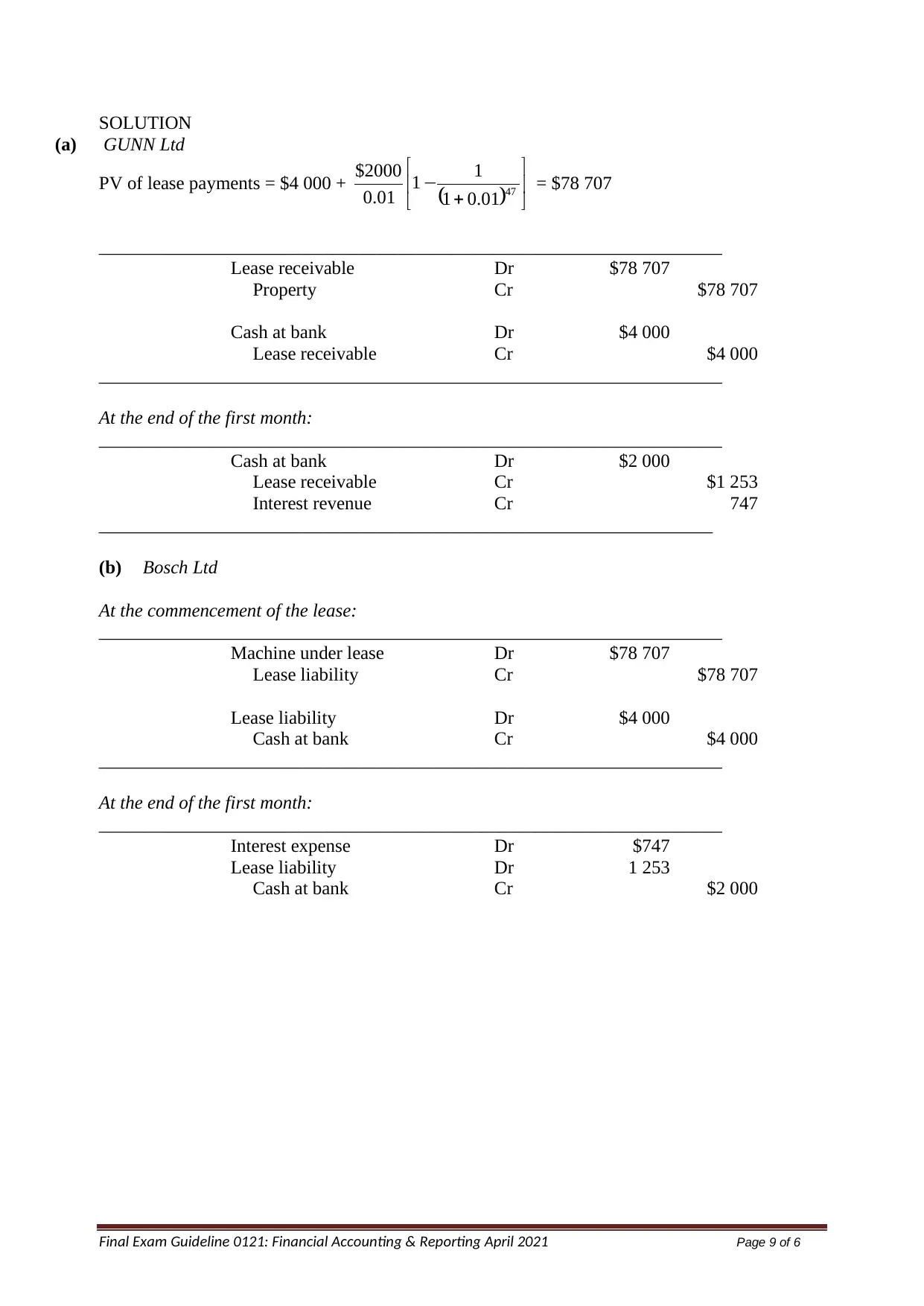

Accounting for lease: additional exercise 2

Bosch Ltd entered into a finance lease with Gunn Ltd to obtain the services of a forklift truck.

The term of the lease is four years in and return Bosch Ltd has agreed to make an initial payment

of $4,000 followed by 47 monthly payments of $2,000. The rate of interest charged by the lessor

is found to be 1% per month, and the lessor acquired the forklift truck for $78,707

Required:

a. Record the lease of the forklift truck, including the initial payment of $4,000 and the first lease

instalment of $2,000 in the books of the lessor.

b. Record the lease of the forklift truck, including the initial payment of $4,000 and the first lease

instalment of $2,000, in the books of the lessee

Answer:

In the books of the lessee Company Ltd, 1 July 2012

Cash Dr 150000

Tractor (net) Cr 1000000

Deferred gain on sale of tractor Cr 50000

Leased assets Dr 150000

Leased liability Cr 150000

30 June 2013

Interest expense Dr 15000

Lease liability Dr 10000

Cash Cr 25000

Amortization Dr 15000

Accumulated amortization Cr 15000

Accounting for lease: additional exercise 2

Bosch Ltd entered into a finance lease with Gunn Ltd to obtain the services of a forklift truck.

The term of the lease is four years in and return Bosch Ltd has agreed to make an initial payment

of $4,000 followed by 47 monthly payments of $2,000. The rate of interest charged by the lessor

is found to be 1% per month, and the lessor acquired the forklift truck for $78,707

Required:

a. Record the lease of the forklift truck, including the initial payment of $4,000 and the first lease

instalment of $2,000 in the books of the lessor.

b. Record the lease of the forklift truck, including the initial payment of $4,000 and the first lease

instalment of $2,000, in the books of the lessee

Final Exam Guideline 0121: Financial Accounting & Reporting April 2021 Page 9 of 6

SOLUTION

(a) GUNN Ltd

PV of lease payments = $4 000 + ( )

+

− 47

01.01

1

1

01.0

2000$ = $78 707

___________________________________________________________________

Lease receivable Dr $78 707

Property Cr $78 707

Cash at bank Dr $4 000

Lease receivable Cr $4 000

___________________________________________________________________

At the end of the first month:

___________________________________________________________________

Cash at bank Dr $2 000

Lease receivable Cr $1 253

Interest revenue Cr 747

__________________________________________________________________

(b) Bosch Ltd

At the commencement of the lease:

___________________________________________________________________

Machine under lease Dr $78 707

Lease liability Cr $78 707

Lease liability Dr $4 000

Cash at bank Cr $4 000

___________________________________________________________________

At the end of the first month:

___________________________________________________________________

Interest expense Dr $747

Lease liability Dr 1 253

Cash at bank Cr $2 000

SOLUTION

(a) GUNN Ltd

PV of lease payments = $4 000 + ( )

+

− 47

01.01

1

1

01.0

2000$ = $78 707

___________________________________________________________________

Lease receivable Dr $78 707

Property Cr $78 707

Cash at bank Dr $4 000

Lease receivable Cr $4 000

___________________________________________________________________

At the end of the first month:

___________________________________________________________________

Cash at bank Dr $2 000

Lease receivable Cr $1 253

Interest revenue Cr 747

__________________________________________________________________

(b) Bosch Ltd

At the commencement of the lease:

___________________________________________________________________

Machine under lease Dr $78 707

Lease liability Cr $78 707

Lease liability Dr $4 000

Cash at bank Cr $4 000

___________________________________________________________________

At the end of the first month:

___________________________________________________________________

Interest expense Dr $747

Lease liability Dr 1 253

Cash at bank Cr $2 000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Final Exam Guideline 0121: Financial Accounting & Reporting April 2021 Page 10 of 6

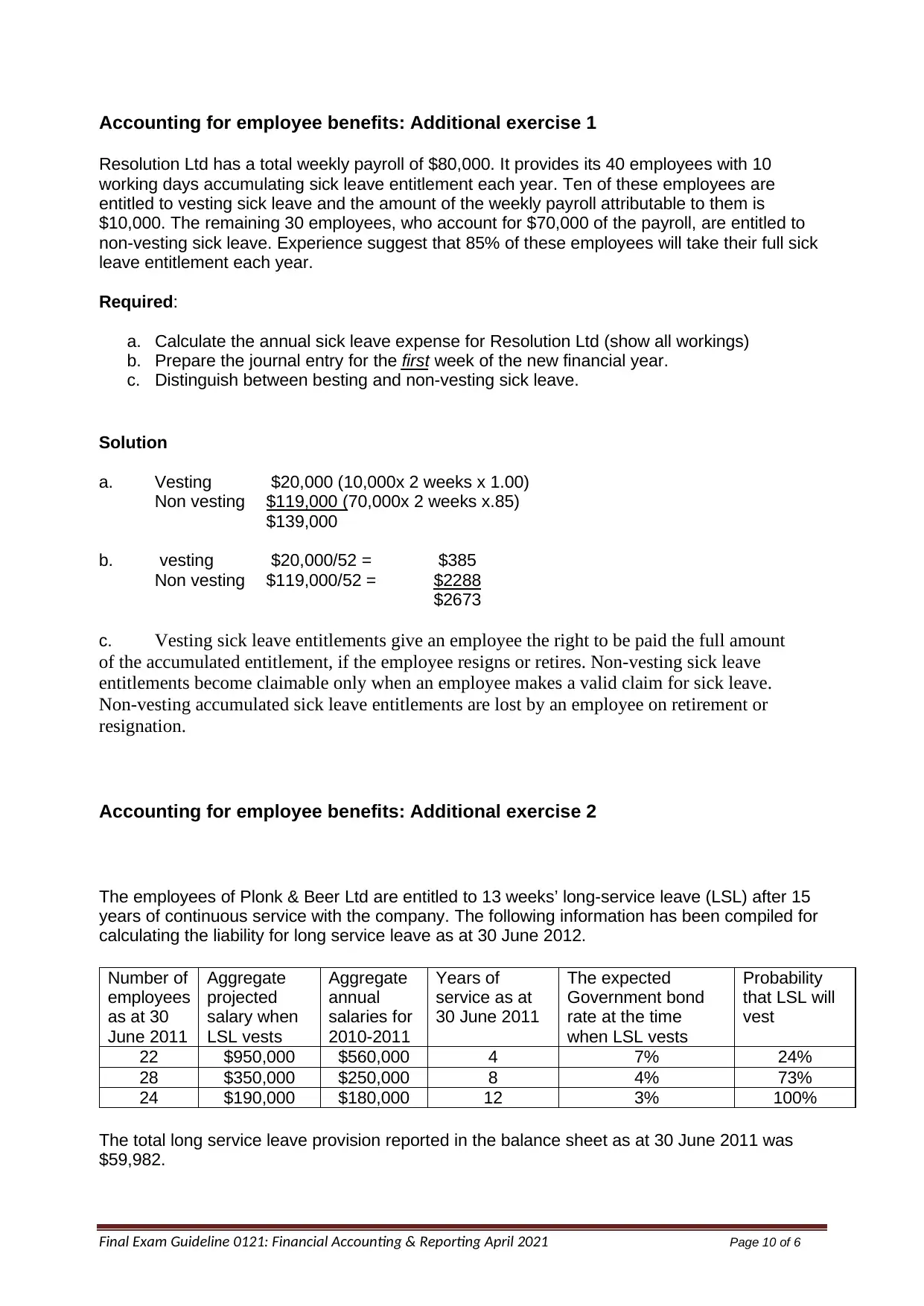

Accounting for employee benefits: Additional exercise 1

Resolution Ltd has a total weekly payroll of $80,000. It provides its 40 employees with 10

working days accumulating sick leave entitlement each year. Ten of these employees are

entitled to vesting sick leave and the amount of the weekly payroll attributable to them is

$10,000. The remaining 30 employees, who account for $70,000 of the payroll, are entitled to

non-vesting sick leave. Experience suggest that 85% of these employees will take their full sick

leave entitlement each year.

Required:

a. Calculate the annual sick leave expense for Resolution Ltd (show all workings)

b. Prepare the journal entry for the first week of the new financial year.

c. Distinguish between besting and non-vesting sick leave.

Accounting for employee benefits: Additional exercise 2

The employees of Plonk & Beer Ltd are entitled to 13 weeks’ long-service leave (LSL) after 15

years of continuous service with the company. The following information has been compiled for

calculating the liability for long service leave as at 30 June 2012.

Number of

employees

as at 30

June 2011

Aggregate

projected

salary when

LSL vests

Aggregate

annual

salaries for

2010-2011

Years of

service as at

30 June 2011

The expected

Government bond

rate at the time

when LSL vests

Probability

that LSL will

vest

22 $950,000 $560,000 4 7% 24%

28 $350,000 $250,000 8 4% 73%

24 $190,000 $180,000 12 3% 100%

The total long service leave provision reported in the balance sheet as at 30 June 2011 was

$59,982.

Solution

a. Vesting $20,000 (10,000x 2 weeks x 1.00)

Non vesting $119,000 (70,000x 2 weeks x.85)

$139,000

b. vesting $20,000/52 = $385

Non vesting $119,000/52 = $2288

$2673

c. Vesting sick leave entitlements give an employee the right to be paid the full amount

of the accumulated entitlement, if the employee resigns or retires. Non-vesting sick leave

entitlements become claimable only when an employee makes a valid claim for sick leave.

Non-vesting accumulated sick leave entitlements are lost by an employee on retirement or

resignation.

Accounting for employee benefits: Additional exercise 1

Resolution Ltd has a total weekly payroll of $80,000. It provides its 40 employees with 10

working days accumulating sick leave entitlement each year. Ten of these employees are

entitled to vesting sick leave and the amount of the weekly payroll attributable to them is

$10,000. The remaining 30 employees, who account for $70,000 of the payroll, are entitled to

non-vesting sick leave. Experience suggest that 85% of these employees will take their full sick

leave entitlement each year.

Required:

a. Calculate the annual sick leave expense for Resolution Ltd (show all workings)

b. Prepare the journal entry for the first week of the new financial year.

c. Distinguish between besting and non-vesting sick leave.

Accounting for employee benefits: Additional exercise 2

The employees of Plonk & Beer Ltd are entitled to 13 weeks’ long-service leave (LSL) after 15

years of continuous service with the company. The following information has been compiled for

calculating the liability for long service leave as at 30 June 2012.

Number of

employees

as at 30

June 2011

Aggregate

projected

salary when

LSL vests

Aggregate

annual

salaries for

2010-2011

Years of

service as at

30 June 2011

The expected

Government bond

rate at the time

when LSL vests

Probability

that LSL will

vest

22 $950,000 $560,000 4 7% 24%

28 $350,000 $250,000 8 4% 73%

24 $190,000 $180,000 12 3% 100%

The total long service leave provision reported in the balance sheet as at 30 June 2011 was

$59,982.

Solution

a. Vesting $20,000 (10,000x 2 weeks x 1.00)

Non vesting $119,000 (70,000x 2 weeks x.85)

$139,000

b. vesting $20,000/52 = $385

Non vesting $119,000/52 = $2288

$2673

c. Vesting sick leave entitlements give an employee the right to be paid the full amount

of the accumulated entitlement, if the employee resigns or retires. Non-vesting sick leave

entitlements become claimable only when an employee makes a valid claim for sick leave.

Non-vesting accumulated sick leave entitlements are lost by an employee on retirement or

resignation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Final Exam Guideline 0121: Financial Accounting & Reporting April 2021 Page 11 of 6

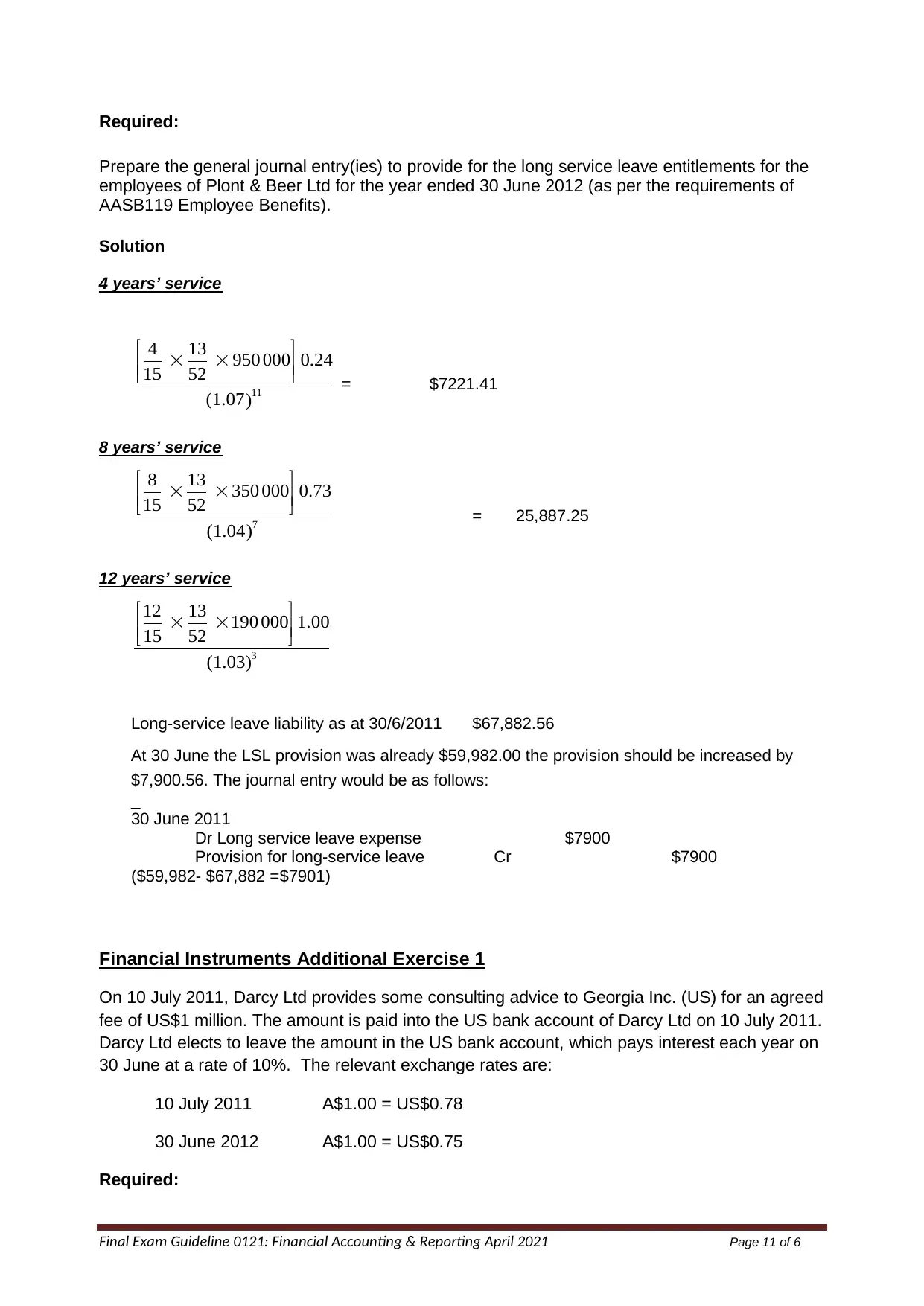

Required:

Prepare the general journal entry(ies) to provide for the long service leave entitlements for the

employees of Plont & Beer Ltd for the year ended 30 June 2012 (as per the requirements of

AASB119 Employee Benefits).

Financial Instruments Additional Exercise 1

On 10 July 2011, Darcy Ltd provides some consulting advice to Georgia Inc. (US) for an agreed

fee of US$1 million. The amount is paid into the US bank account of Darcy Ltd on 10 July 2011.

Darcy Ltd elects to leave the amount in the US bank account, which pays interest each year on

30 June at a rate of 10%. The relevant exchange rates are:

10 July 2011 A$1.00 = US$0.78

30 June 2012 A$1.00 = US$0.75

Required:

Solution

4 years’ service

)(1.07

0.24000950

52

13

15

4

11

= $7221.41

8 years’ service

)(1.04

0.73000350

52

13

15

8

7

= 25,887.25

12 years’ service

)(1.03

1.00000190

52

13

15

12

3

Long-service leave liability as at 30/6/2011 $67,882.56

At 30 June the LSL provision was already $59,982.00 the provision should be increased by

$7,900.56. The journal entry would be as follows:

_

30 June 2011

Dr Long service leave expense $7900

Provision for long-service leave Cr $7900

($59,982- $67,882 =$7901)

Required:

Prepare the general journal entry(ies) to provide for the long service leave entitlements for the

employees of Plont & Beer Ltd for the year ended 30 June 2012 (as per the requirements of

AASB119 Employee Benefits).

Financial Instruments Additional Exercise 1

On 10 July 2011, Darcy Ltd provides some consulting advice to Georgia Inc. (US) for an agreed

fee of US$1 million. The amount is paid into the US bank account of Darcy Ltd on 10 July 2011.

Darcy Ltd elects to leave the amount in the US bank account, which pays interest each year on

30 June at a rate of 10%. The relevant exchange rates are:

10 July 2011 A$1.00 = US$0.78

30 June 2012 A$1.00 = US$0.75

Required:

Solution

4 years’ service

)(1.07

0.24000950

52

13

15

4

11

= $7221.41

8 years’ service

)(1.04

0.73000350

52

13

15

8

7

= 25,887.25

12 years’ service

)(1.03

1.00000190

52

13

15

12

3

Long-service leave liability as at 30/6/2011 $67,882.56

At 30 June the LSL provision was already $59,982.00 the provision should be increased by

$7,900.56. The journal entry would be as follows:

_

30 June 2011

Dr Long service leave expense $7900

Provision for long-service leave Cr $7900

($59,982- $67,882 =$7901)

Final Exam Guideline 0121: Financial Accounting & Reporting April 2021 Page 12 of 6

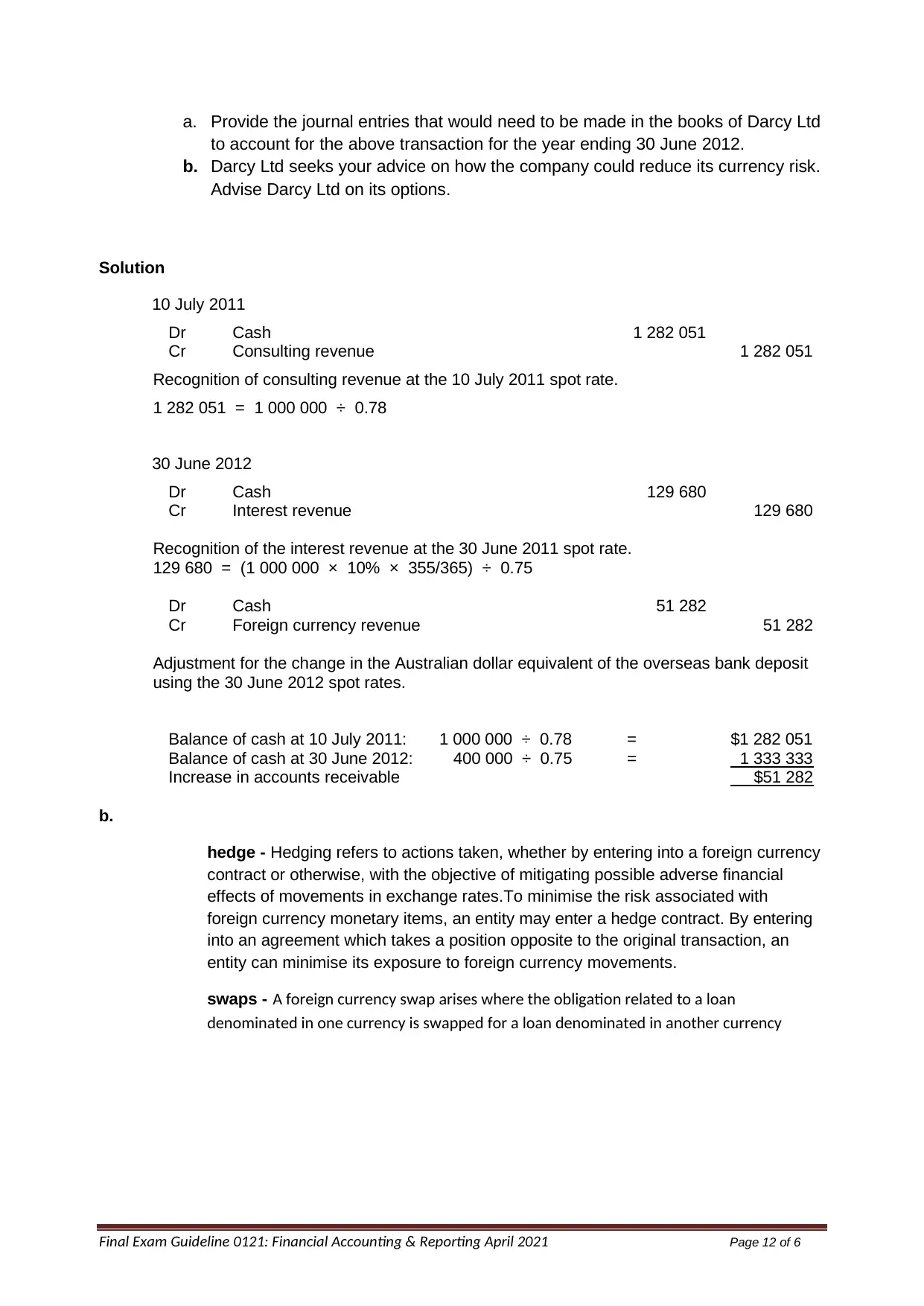

a. Provide the journal entries that would need to be made in the books of Darcy Ltd

to account for the above transaction for the year ending 30 June 2012.

b. Darcy Ltd seeks your advice on how the company could reduce its currency risk.

Advise Darcy Ltd on its options.

Solution

10 July 2011

Dr Cash 1 282 051

Cr Consulting revenue 1 282 051

Recognition of consulting revenue at the 10 July 2011 spot rate.

1 282 051 = 1 000 000 ÷ 0.78

30 June 2012

Dr Cash 129 680

Cr Interest revenue 129 680

Recognition of the interest revenue at the 30 June 2011 spot rate.

129 680 = (1 000 000 × 10% × 355/365) ÷ 0.75

Dr Cash 51 282

Cr Foreign currency revenue 51 282

Adjustment for the change in the Australian dollar equivalent of the overseas bank deposit

using the 30 June 2012 spot rates.

Balance of cash at 10 July 2011: 1 000 000 ÷ 0.78 = $1 282 051

Balance of cash at 30 June 2012: 400 000 ÷ 0.75 = 1 333 333

Increase in accounts receivable $51 282

b.

hedge - Hedging refers to actions taken, whether by entering into a foreign currency

contract or otherwise, with the objective of mitigating possible adverse financial

effects of movements in exchange rates.To minimise the risk associated with

foreign currency monetary items, an entity may enter a hedge contract. By entering

into an agreement which takes a position opposite to the original transaction, an

entity can minimise its exposure to foreign currency movements.

swaps - A foreign currency swap arises where the obligation related to a loan

denominated in one currency is swapped for a loan denominated in another currency

a. Provide the journal entries that would need to be made in the books of Darcy Ltd

to account for the above transaction for the year ending 30 June 2012.

b. Darcy Ltd seeks your advice on how the company could reduce its currency risk.

Advise Darcy Ltd on its options.

Solution

10 July 2011

Dr Cash 1 282 051

Cr Consulting revenue 1 282 051

Recognition of consulting revenue at the 10 July 2011 spot rate.

1 282 051 = 1 000 000 ÷ 0.78

30 June 2012

Dr Cash 129 680

Cr Interest revenue 129 680

Recognition of the interest revenue at the 30 June 2011 spot rate.

129 680 = (1 000 000 × 10% × 355/365) ÷ 0.75

Dr Cash 51 282

Cr Foreign currency revenue 51 282

Adjustment for the change in the Australian dollar equivalent of the overseas bank deposit

using the 30 June 2012 spot rates.

Balance of cash at 10 July 2011: 1 000 000 ÷ 0.78 = $1 282 051

Balance of cash at 30 June 2012: 400 000 ÷ 0.75 = 1 333 333

Increase in accounts receivable $51 282

b.

hedge - Hedging refers to actions taken, whether by entering into a foreign currency

contract or otherwise, with the objective of mitigating possible adverse financial

effects of movements in exchange rates.To minimise the risk associated with

foreign currency monetary items, an entity may enter a hedge contract. By entering

into an agreement which takes a position opposite to the original transaction, an

entity can minimise its exposure to foreign currency movements.

swaps - A foreign currency swap arises where the obligation related to a loan

denominated in one currency is swapped for a loan denominated in another currency

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.