Financial Accounting: From Journal Entries to Balance Sheet

VerifiedAdded on 2020/02/05

|26

|5367

|167

Homework Assignment

AI Summary

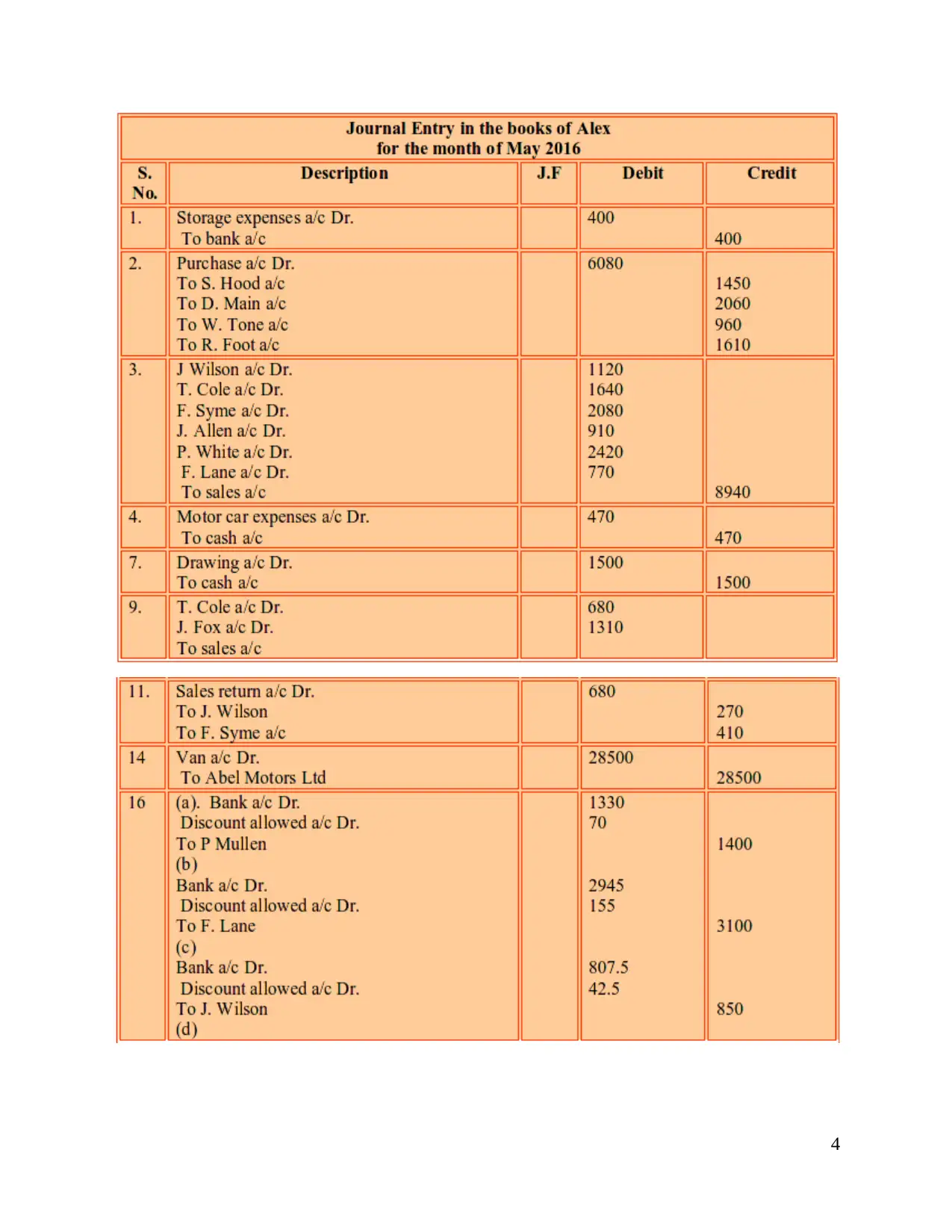

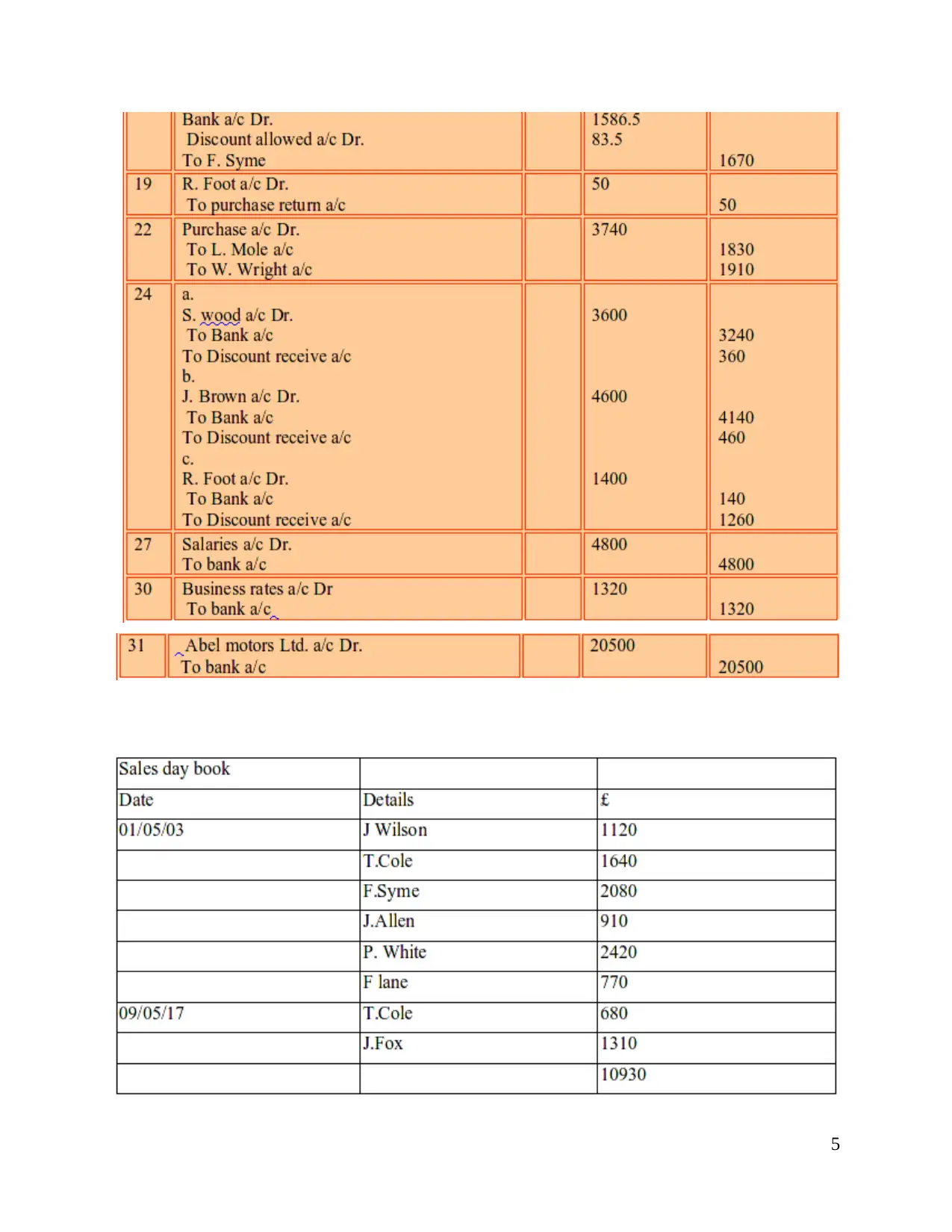

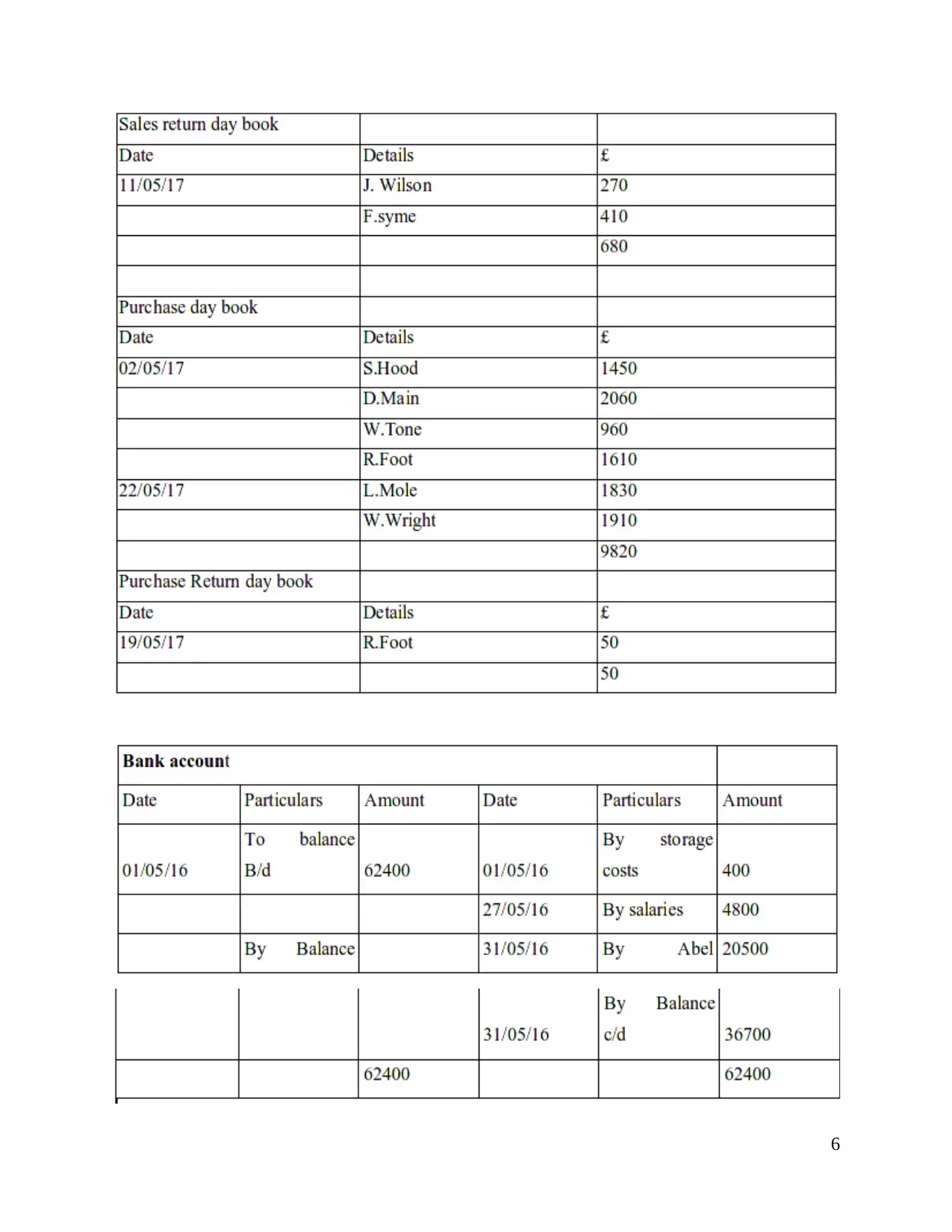

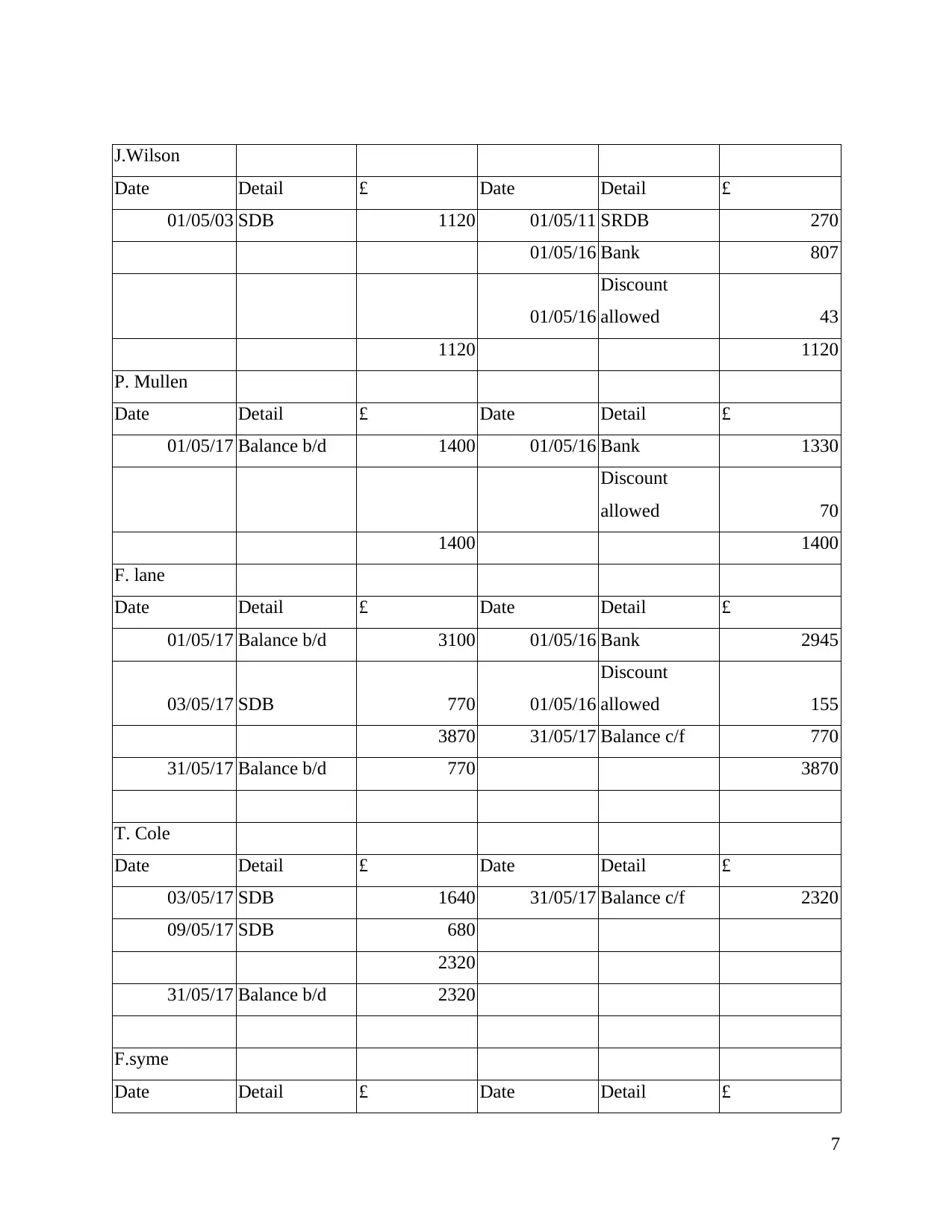

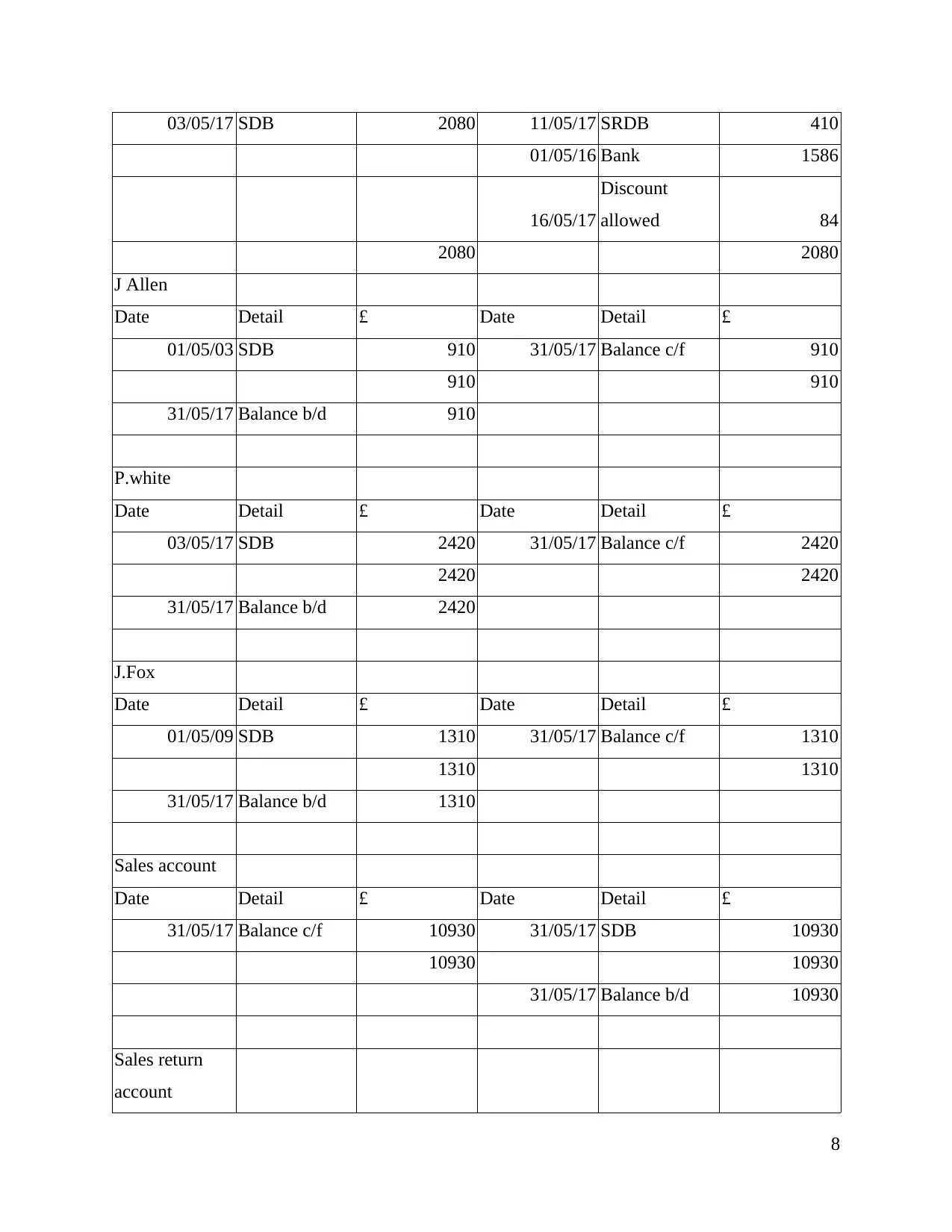

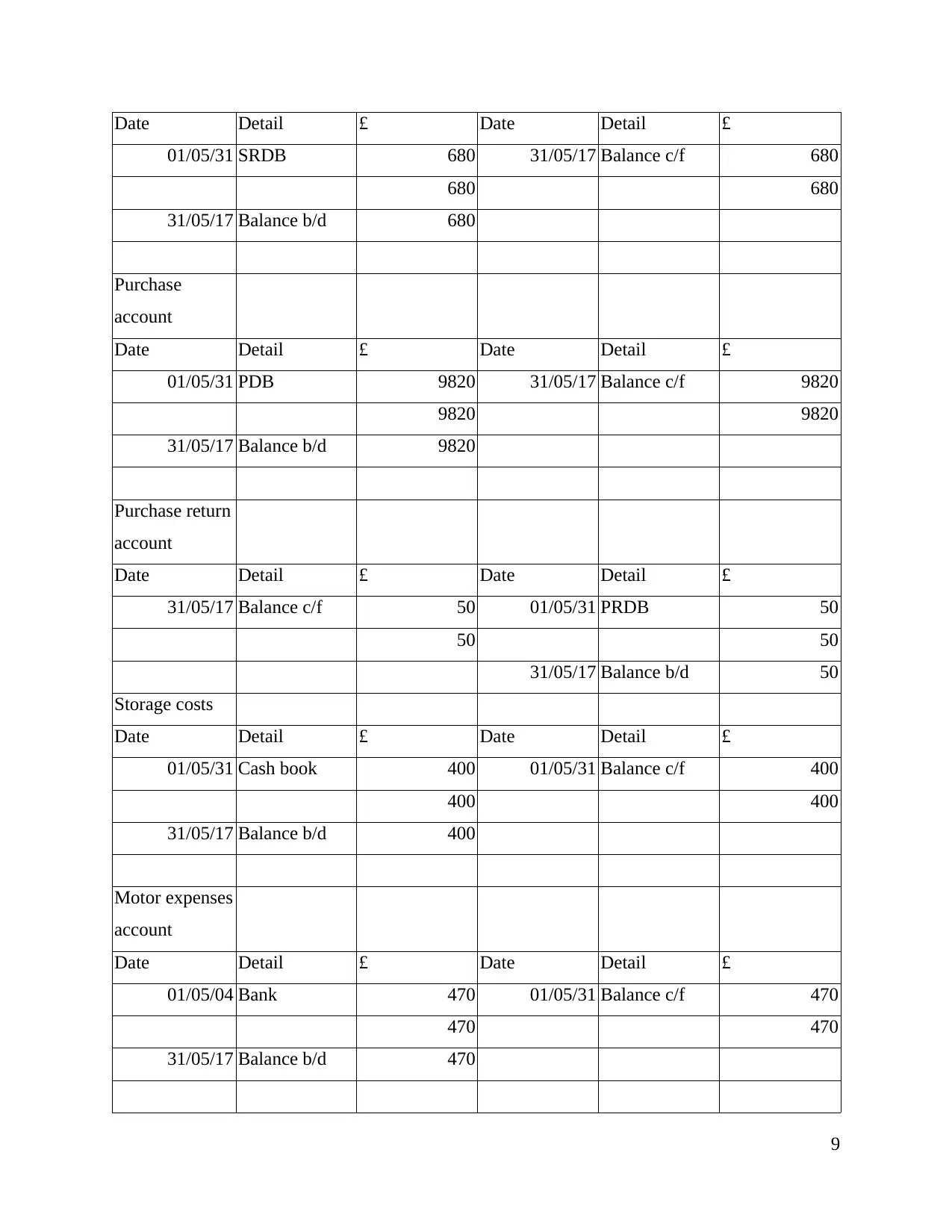

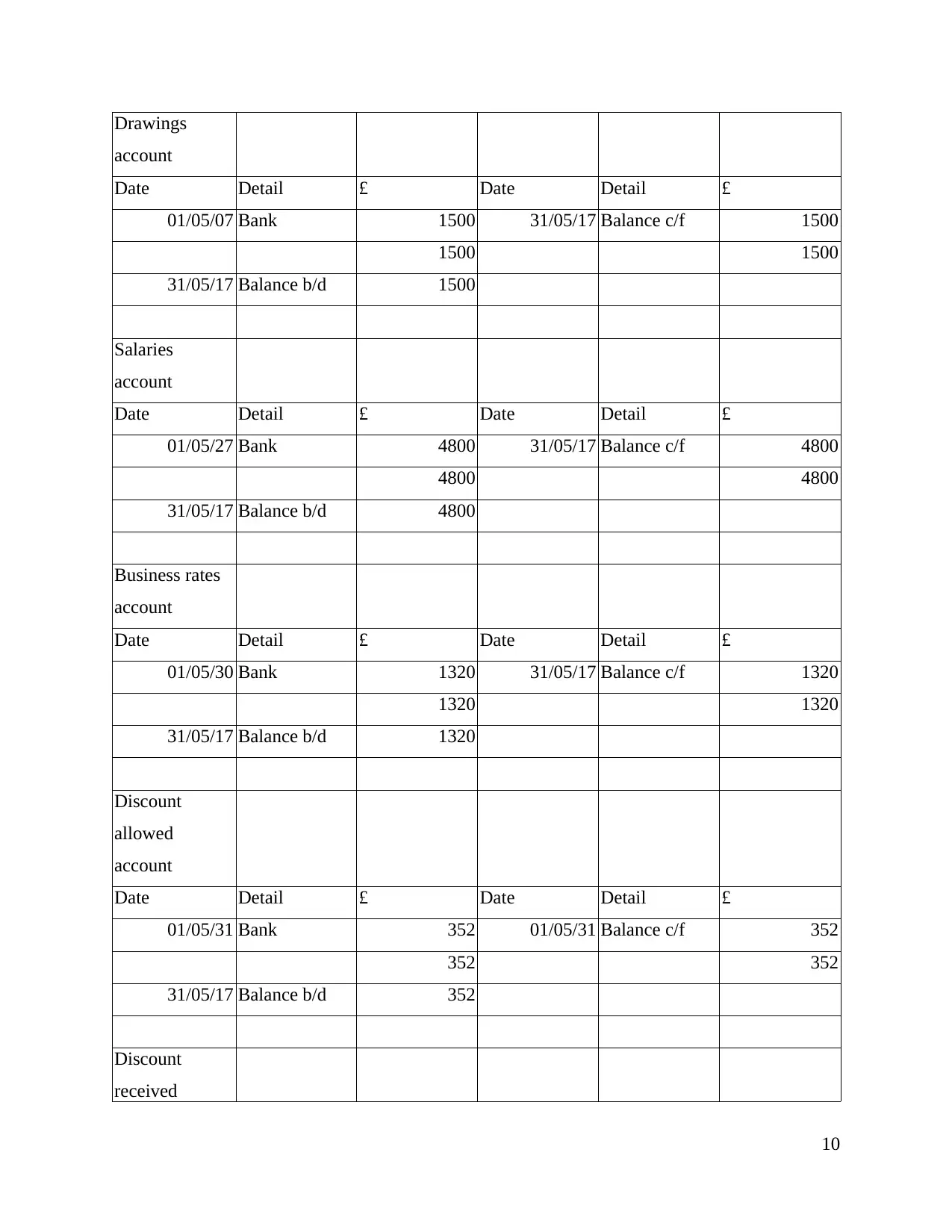

This document provides a comprehensive overview of financial accounting, starting with fundamental concepts and principles. It delves into the practical aspects of accounting, including the creation of journal entries, the maintenance of ledger accounts, and the preparation of profit and loss statements and balance sheets. The assignment covers important topics such as bank reconciliation statements, suspense accounts, and control accounts. It also discusses the regulatory framework of financial accounting, including the role of the Financial Accounting Standards Board (FASB) and the application of International Accounting Standards (IAS). Furthermore, the document explains accounting rules, principles, and conventions, including going concern, materiality, and consistency. The document includes examples of ledger accounts for different transactions, such as sales, purchases, and expenses. Desklib offers this assignment to aid students in understanding financial accounting.

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.