Financial Accounting Assignment Solution for HNBS 310

VerifiedAdded on 2020/12/18

|18

|2649

|302

Homework Assignment

AI Summary

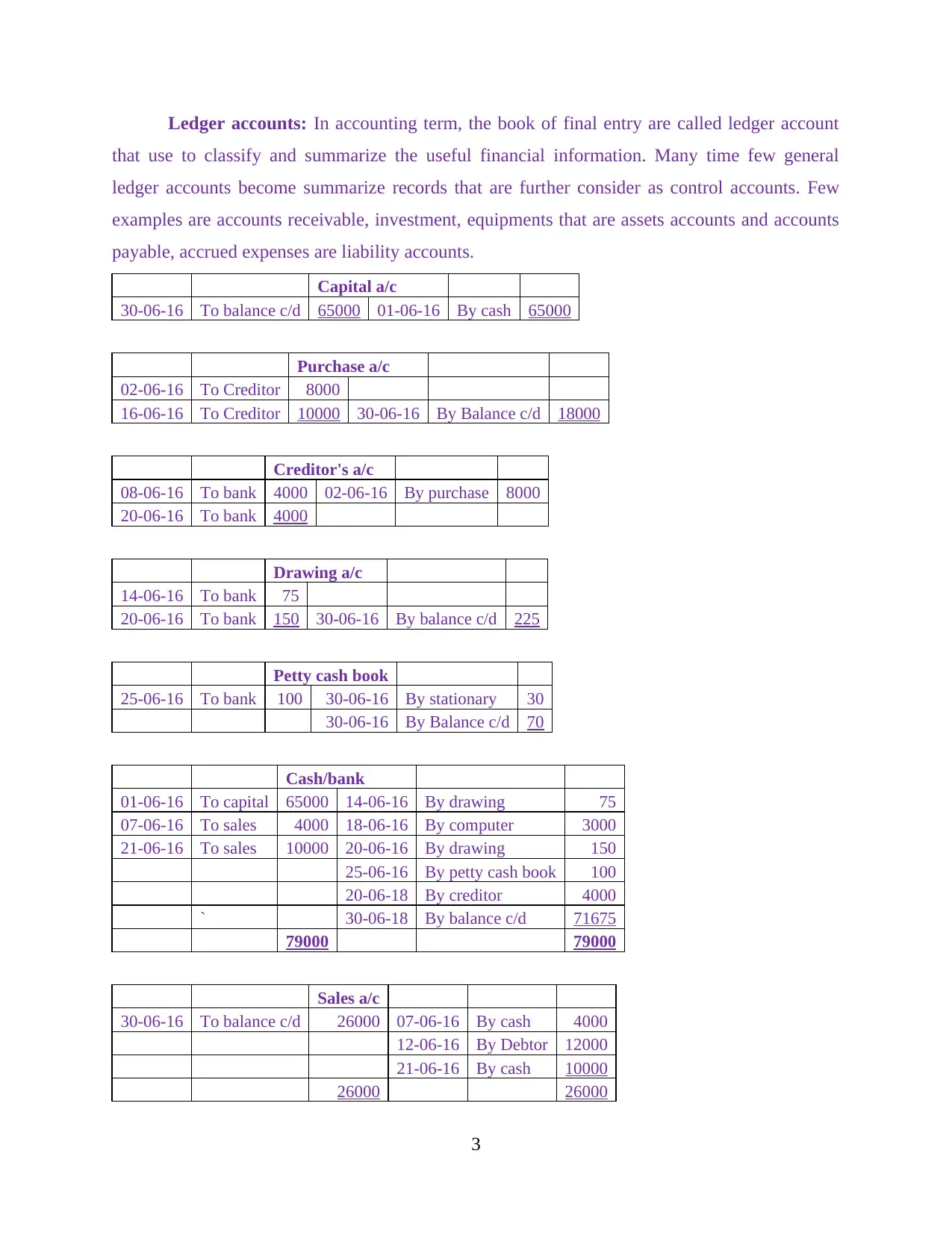

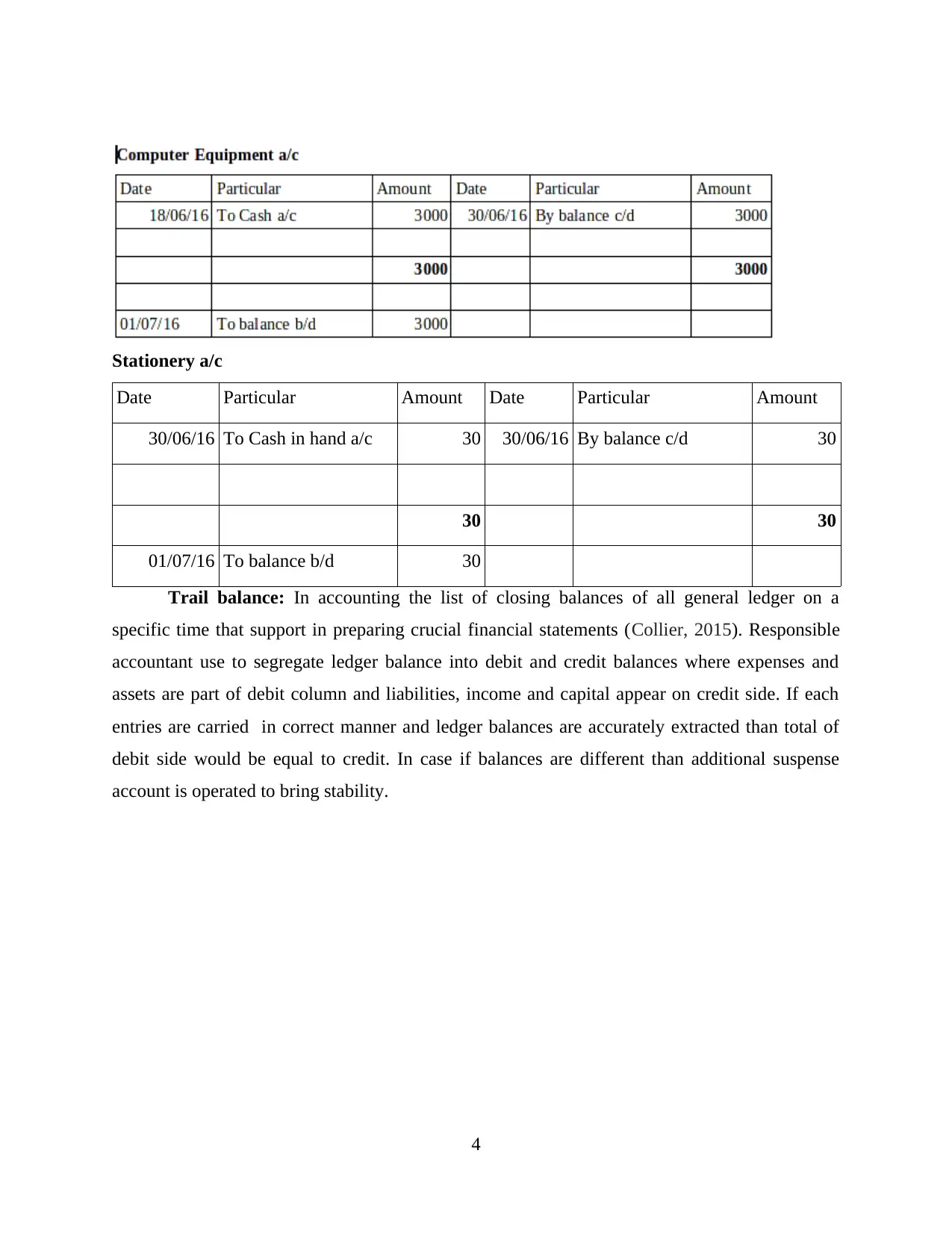

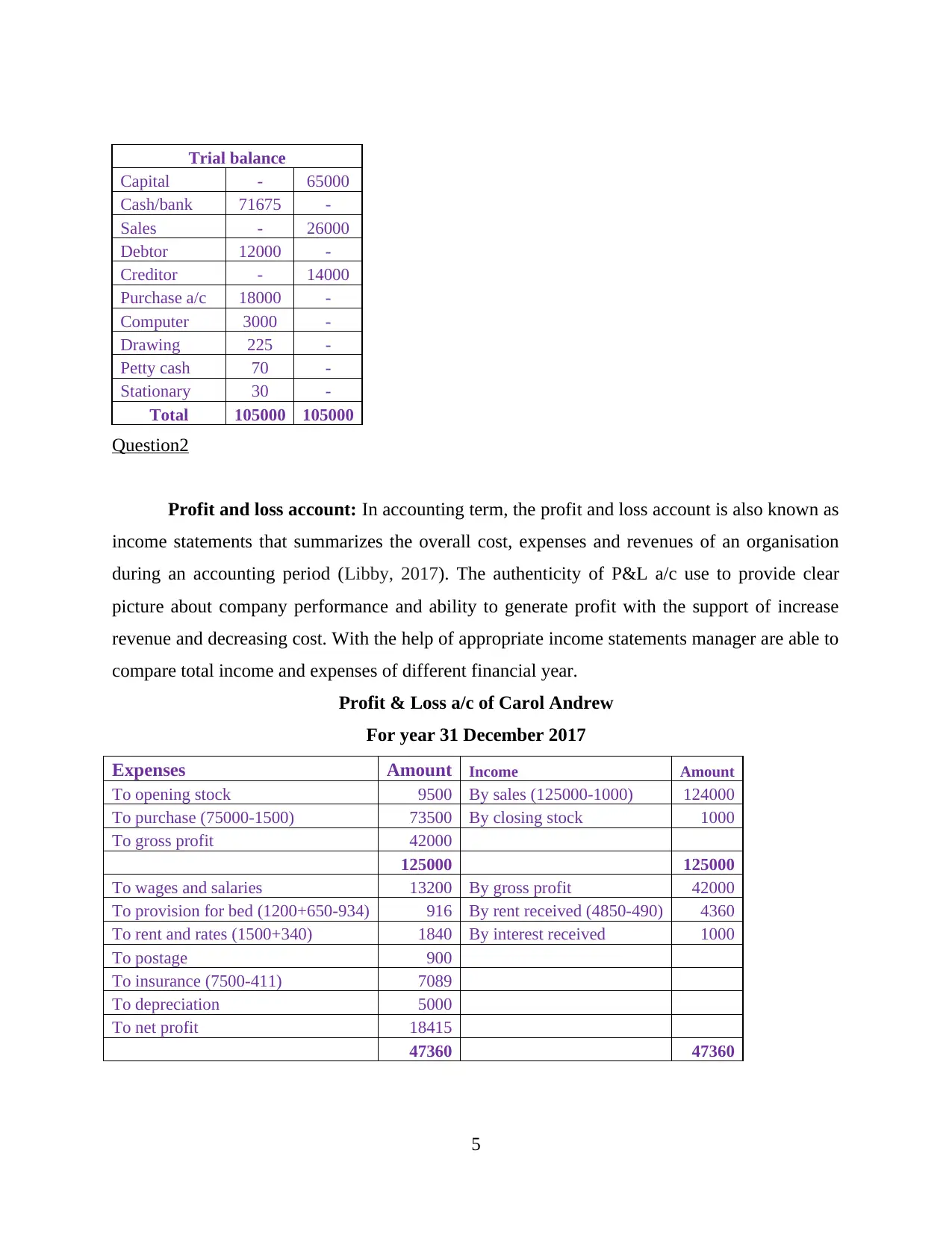

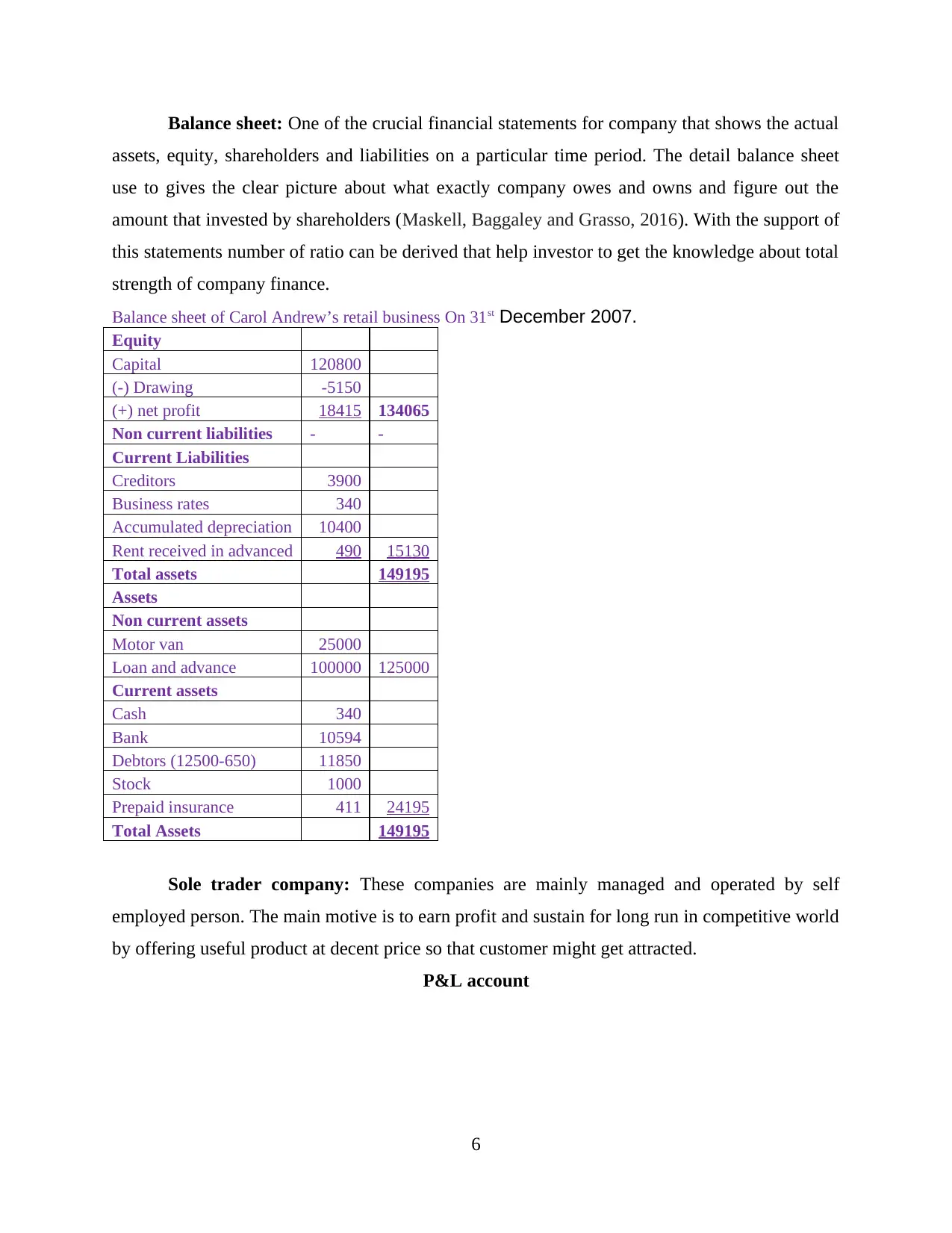

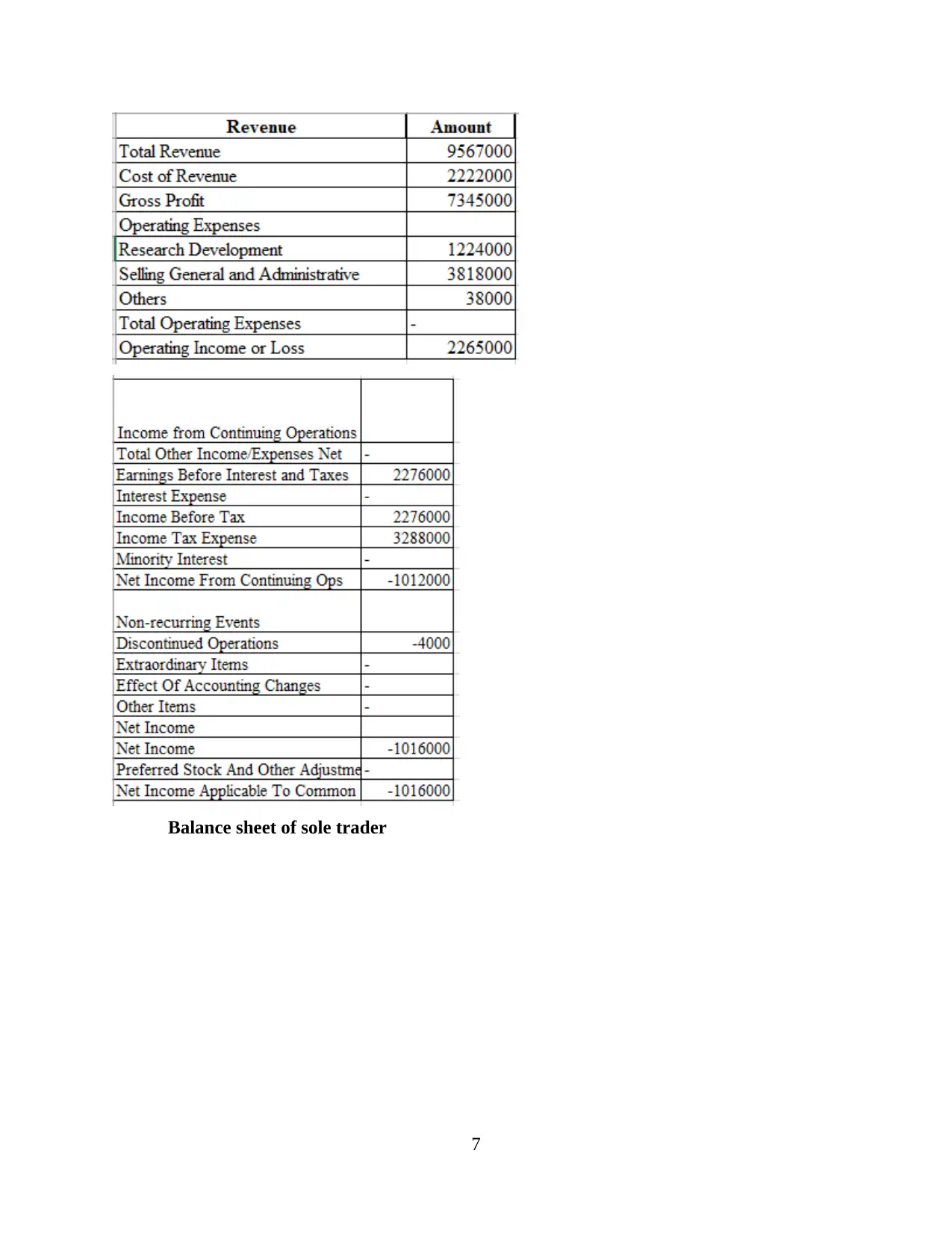

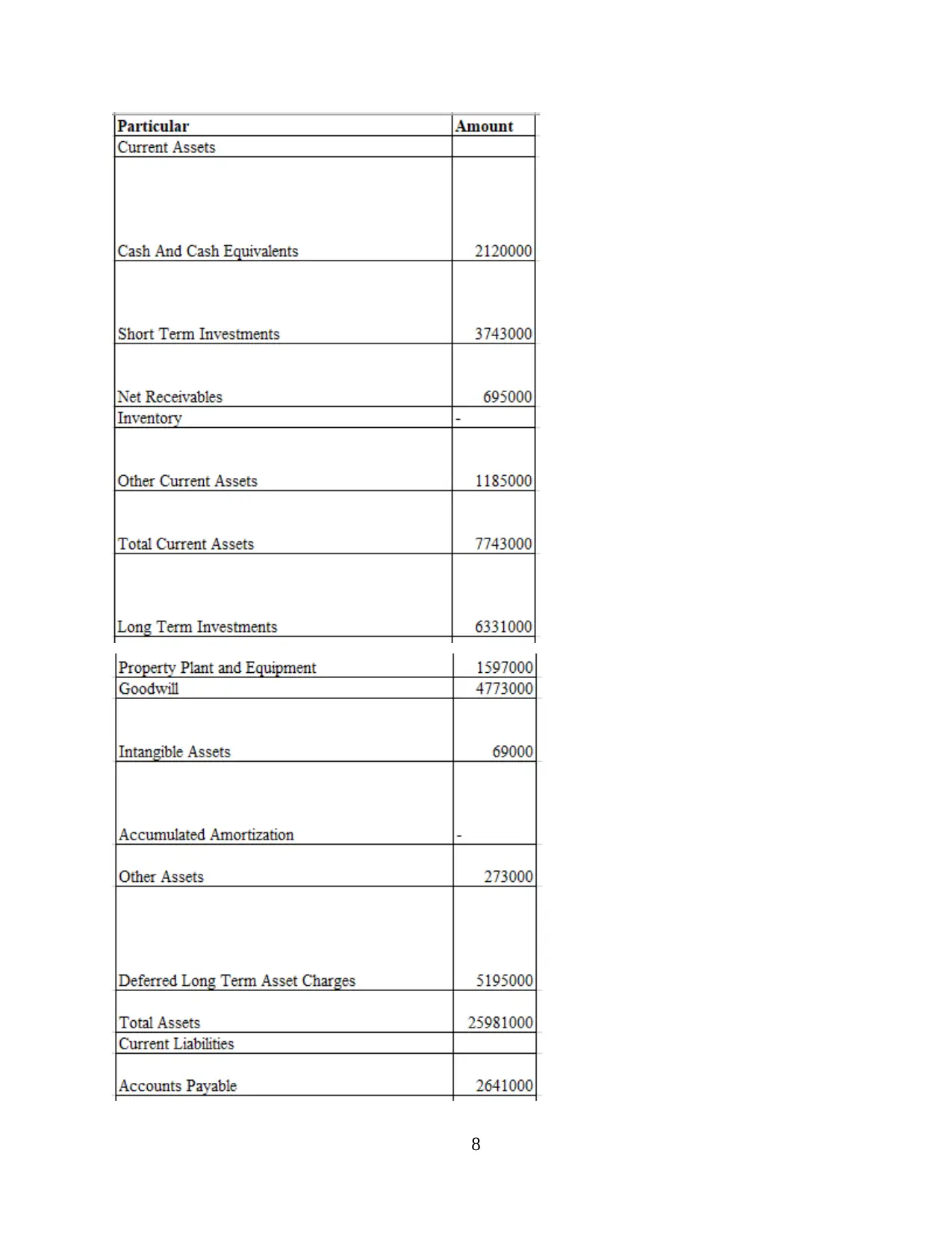

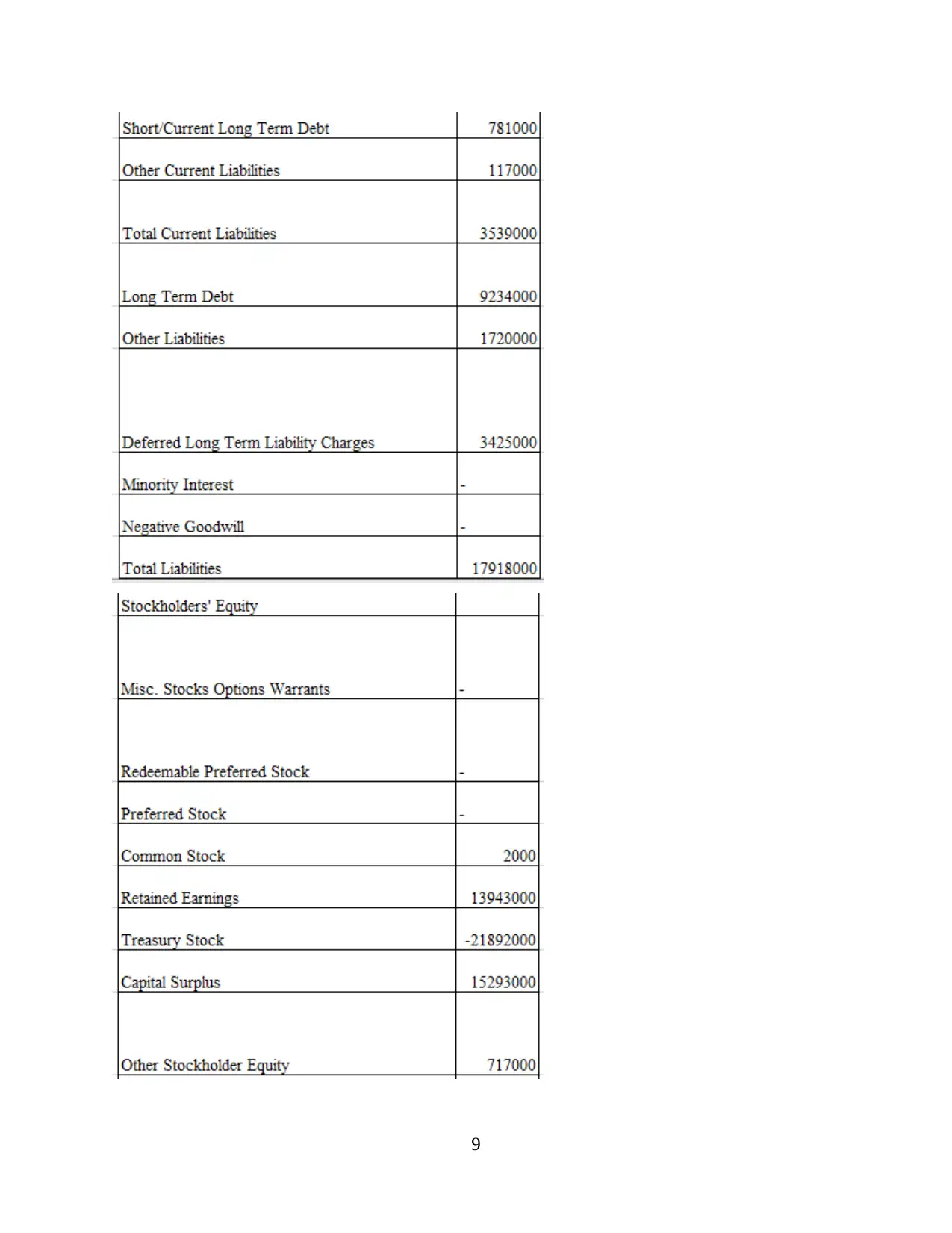

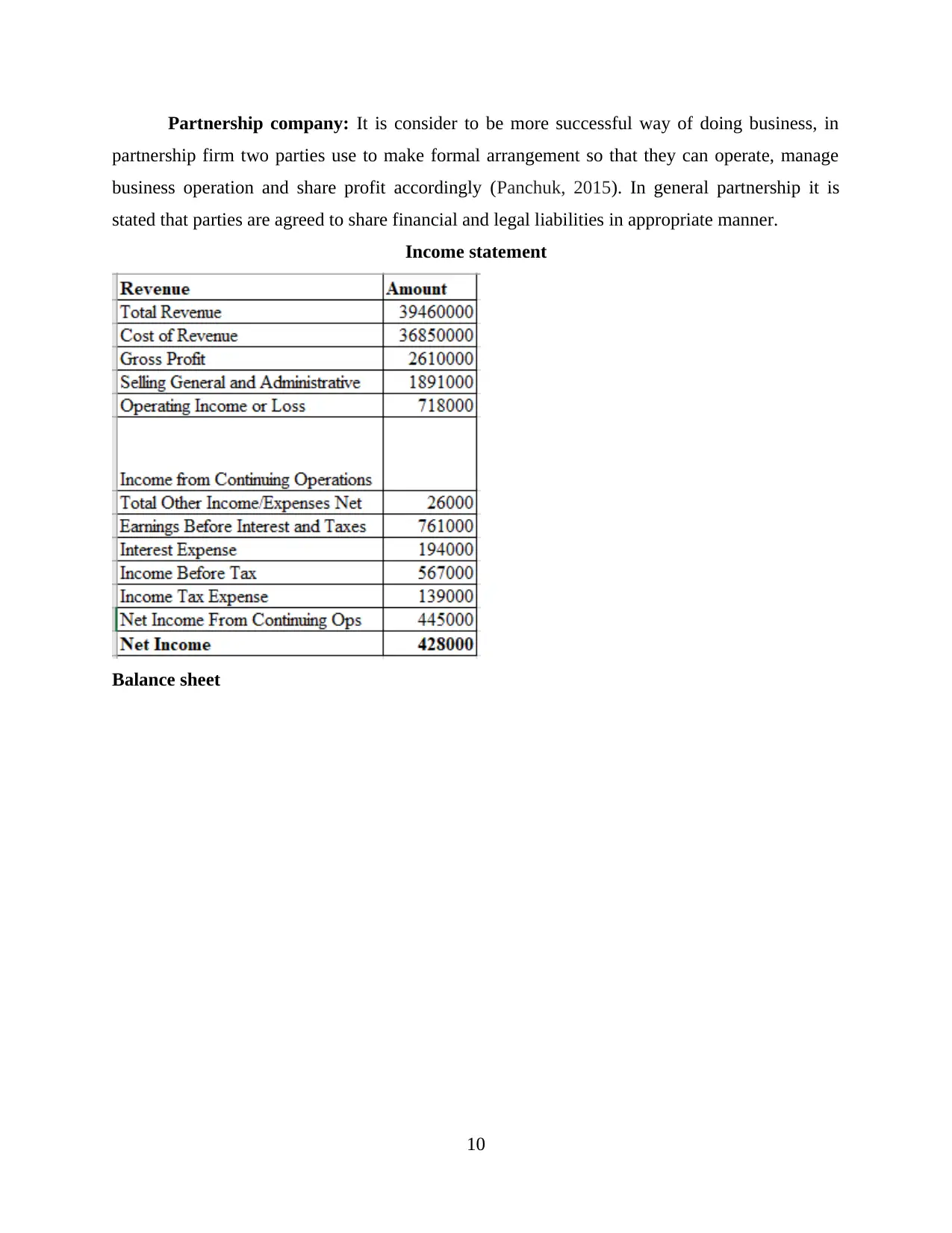

This document provides a detailed solution to a financial accounting assignment. It begins with an introduction to financial accounting, journal entries, ledger accounts, and trial balances. The solution then presents two scenarios, each with questions that involve preparing journal entries, ledger accounts, and trial balances. The first scenario covers these elements, while the second addresses a bank reconciliation and different financial terms. The document also includes profit and loss accounts, balance sheets, and discusses accounting for sole traders and partnership companies. The solution incorporates examples and explanations of key accounting concepts, such as direct debits, standing orders, bank charges, and dishonored checks, providing a comprehensive overview of the financial accounting principles and practices covered in the assignment.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.