Financial Accounting: Journal Entries, Ledgers, Trial Balance

VerifiedAdded on 2020/12/08

|23

|4103

|255

Homework Assignment

AI Summary

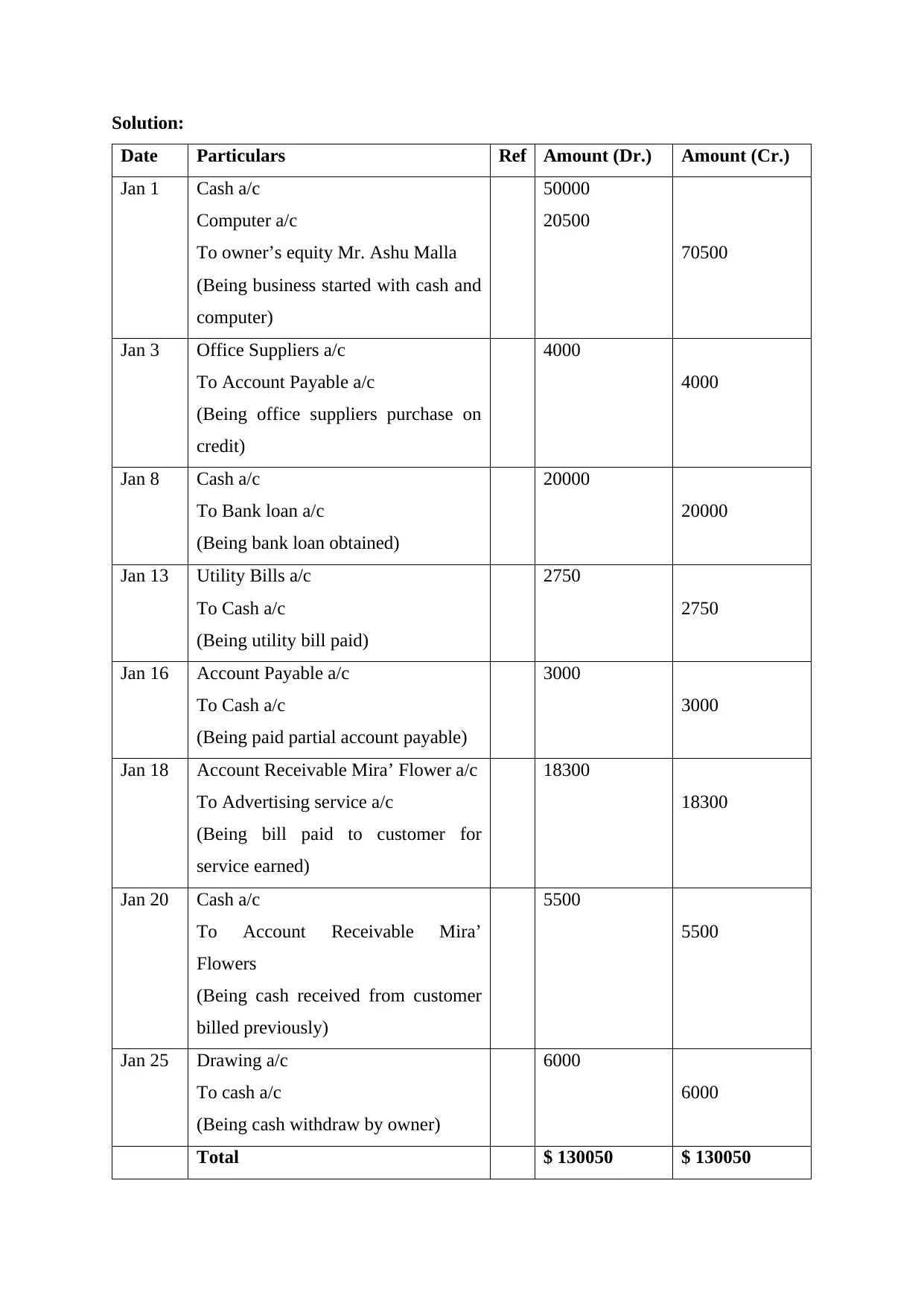

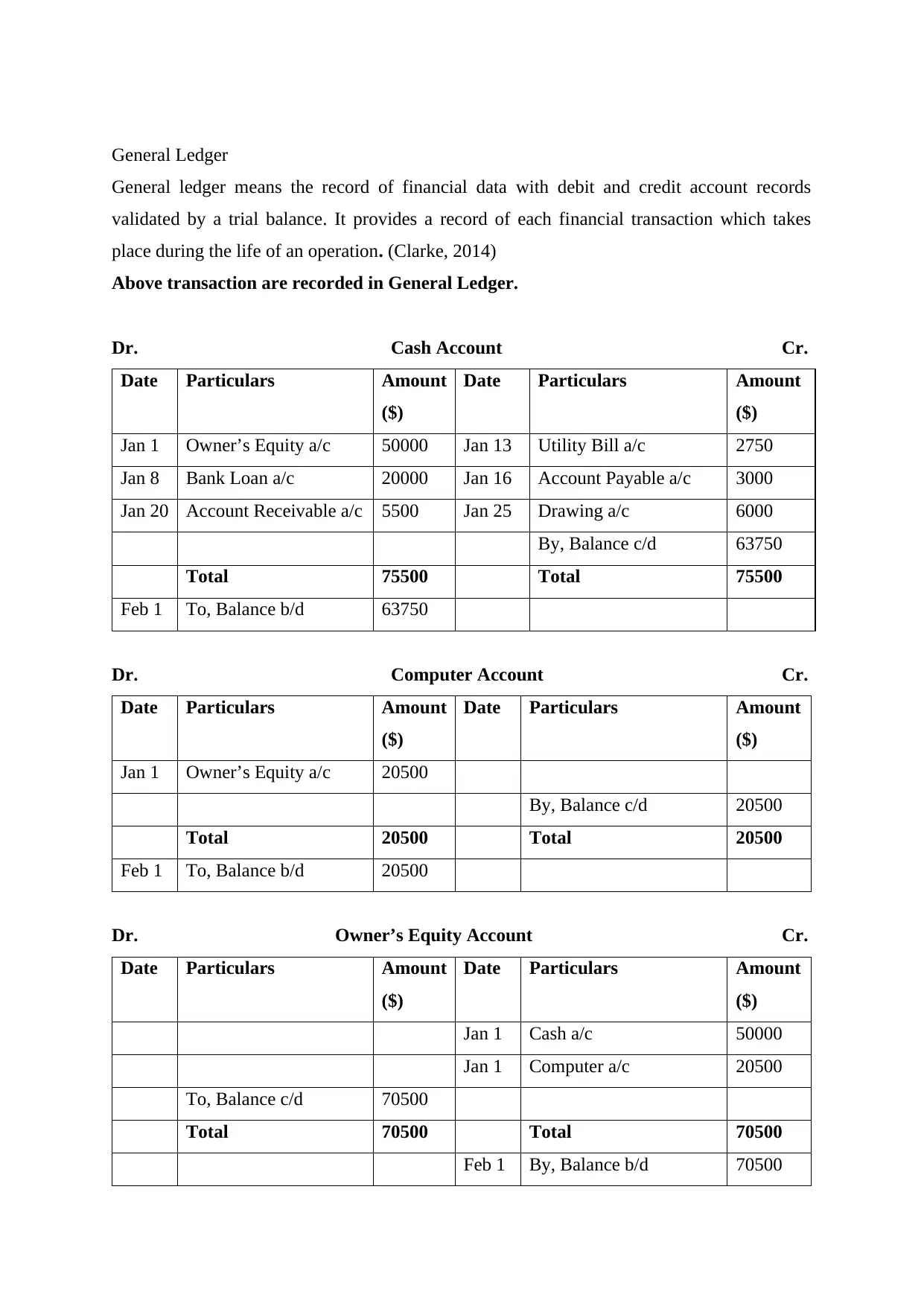

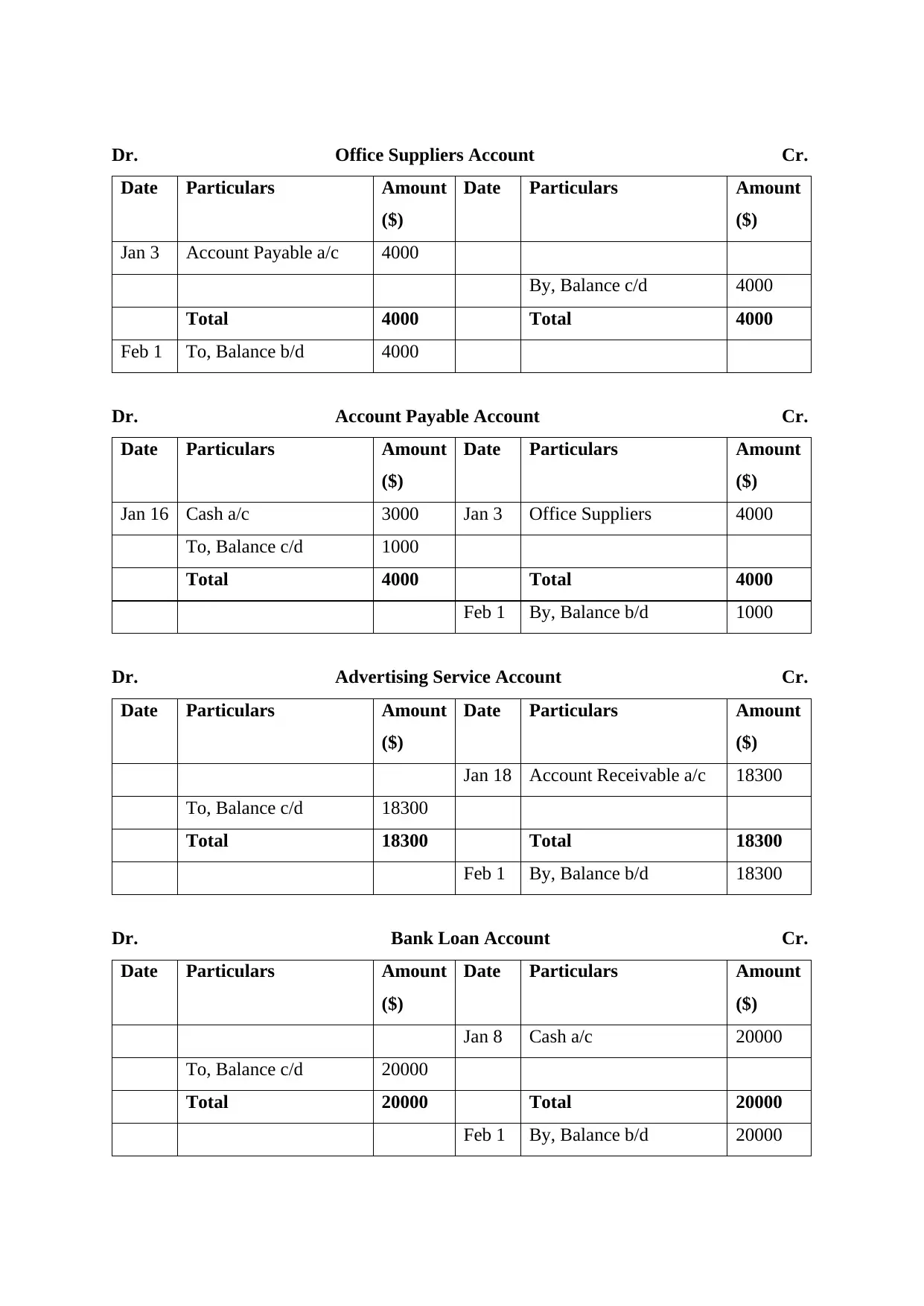

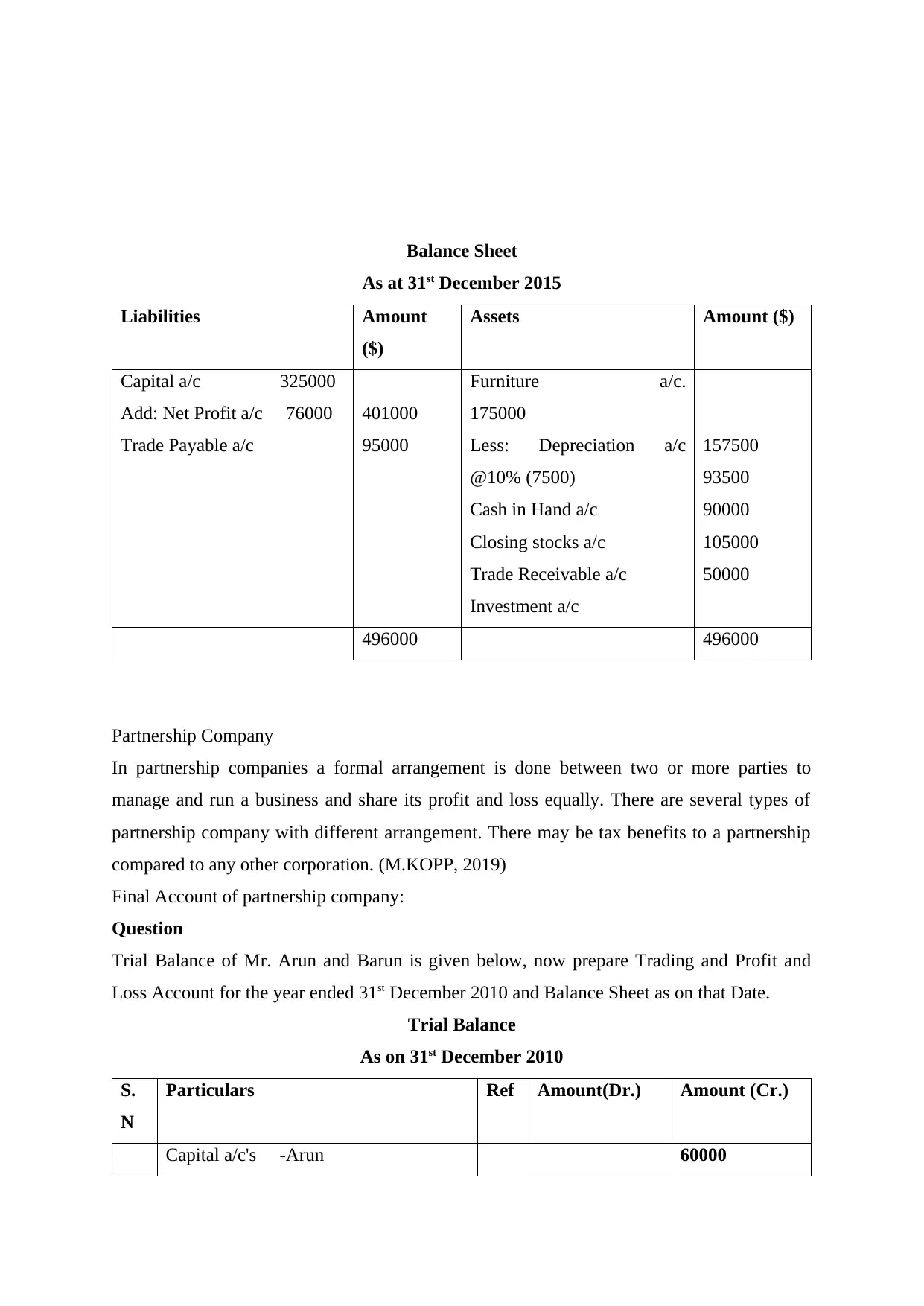

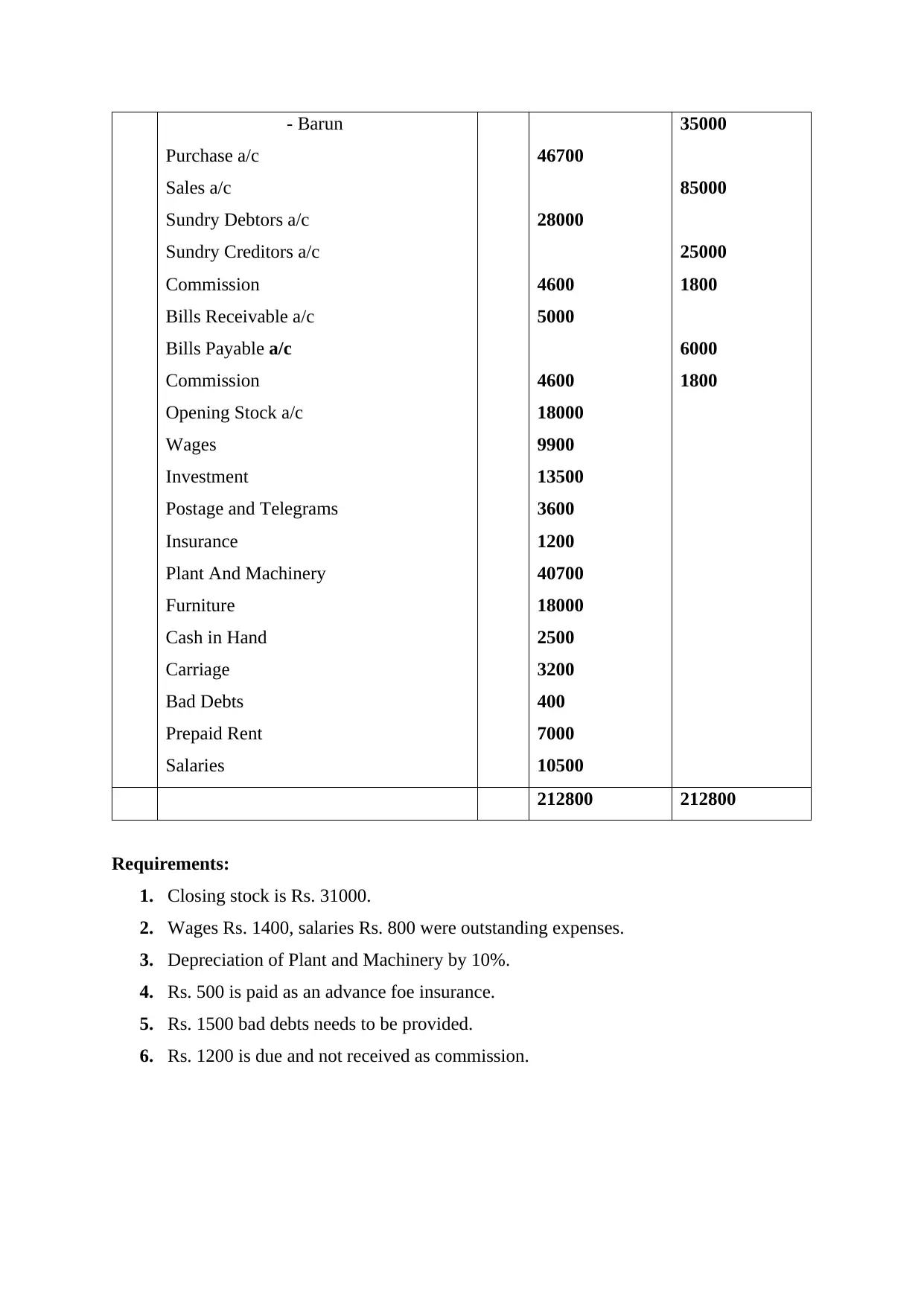

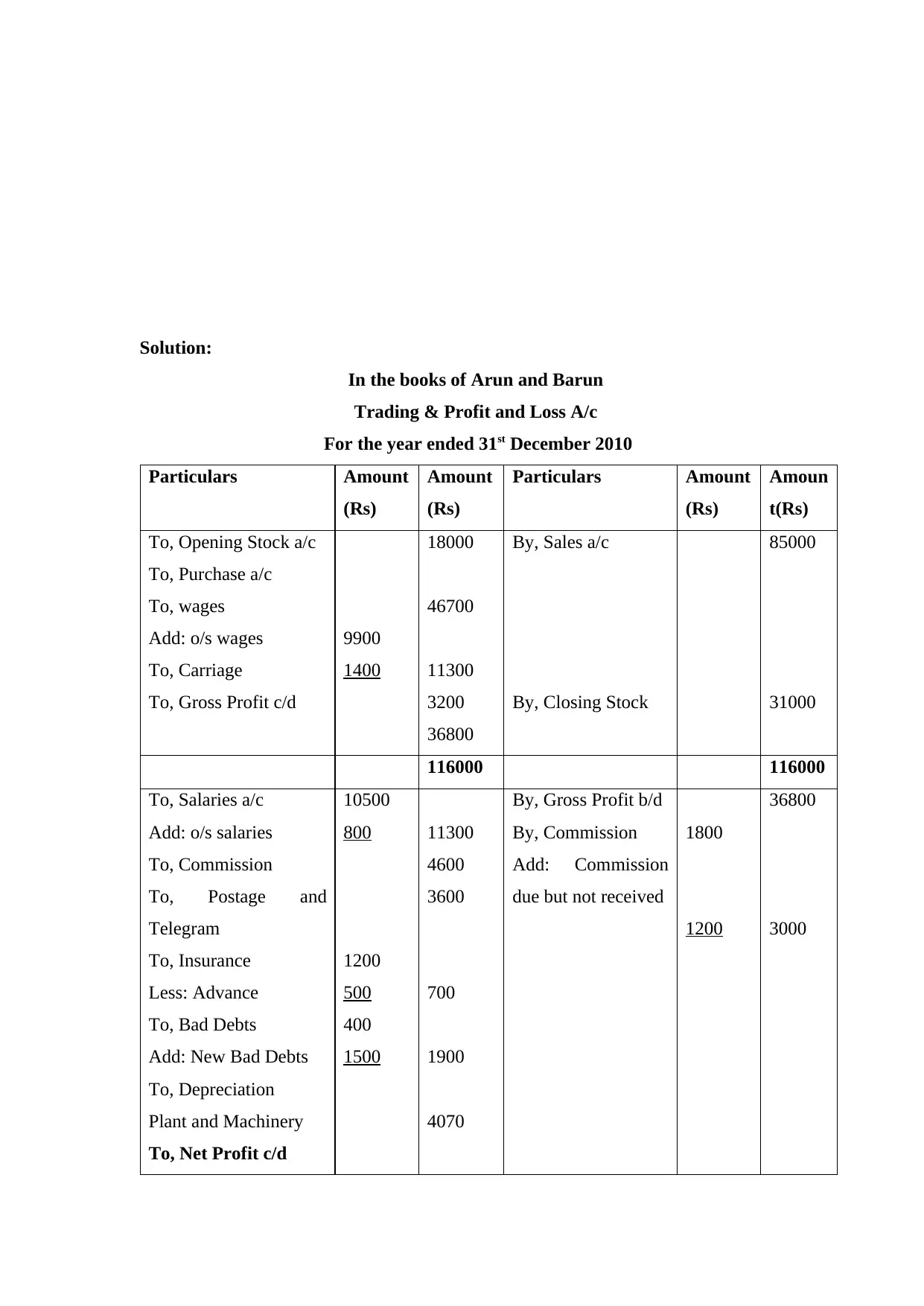

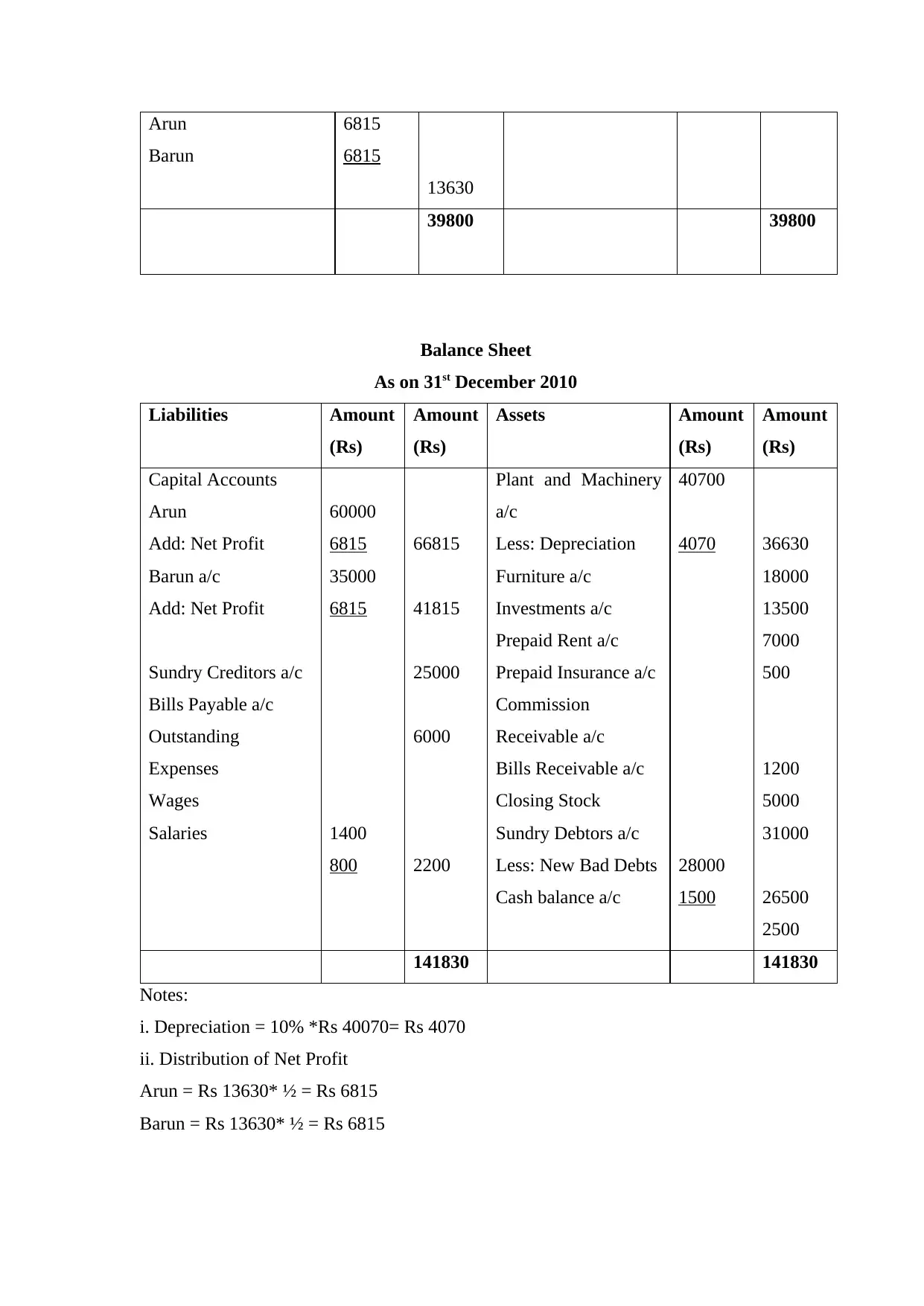

This document presents a complete solution to a financial accounting assignment, covering key concepts and practical applications. The assignment involves preparing journal entries, general ledgers, and trial balances for a consulting business, as well as constructing final accounts, including trading, profit and loss accounts, and balance sheets, for sole trader, partnership, and limited company scenarios. The solutions demonstrate the application of accounting principles, such as double-entry bookkeeping, depreciation, and adjustments for closing stock and outstanding expenses. The document provides detailed workings and financial statements for each business type, offering a valuable resource for students studying financial accounting and seeking to understand the preparation of financial reports for various business structures. The document also includes a comprehensive analysis of the trial balance and adjustments, crucial for accurate financial reporting.

1 out of 23

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.