Financial Accounting Homework: Scenarios, Principles, and Reports

VerifiedAdded on 2022/11/25

|25

|4870

|184

Homework Assignment

AI Summary

This document presents a comprehensive solution to a financial accounting homework assignment. It begins with an overview of business transactions, single and double-entry bookkeeping, and the importance of a trial balance. The solution includes detailed journal entries, ledger accounts, and a trial balance for a given scenario. Furthermore, it differentiates between financial reports and statements, highlighting their respective users and importance. The assignment delves into key accounting principles such as accrual, conservatism, consistency, cost, economic entity, full disclosure, going concern, matching, and materiality. The solution also includes an analysis of financial statements and reports, providing insights into their preparation and usage. Finally, it covers the principles of accounting and their practical applications in financial reporting.

FINANCIAL ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

SCENARIO 1...................................................................................................................................2

Question 1....................................................................................................................................2

Question 2....................................................................................................................................3

Question 3....................................................................................................................................7

Question 4....................................................................................................................................9

Question 5..................................................................................................................................11

Question 7..................................................................................................................................12

SCENARIO 2.................................................................................................................................13

Question 2..................................................................................................................................13

Question 3..................................................................................................................................14

REFERENCES................................................................................................................................1

SCENARIO 1...................................................................................................................................2

Question 1....................................................................................................................................2

Question 2....................................................................................................................................3

Question 3....................................................................................................................................7

Question 4....................................................................................................................................9

Question 5..................................................................................................................................11

Question 7..................................................................................................................................12

SCENARIO 2.................................................................................................................................13

Question 2..................................................................................................................................13

Question 3..................................................................................................................................14

REFERENCES................................................................................................................................1

SCENARIO 1

Question 1

Business transactions:

It refers to the transactions that occur between the company and the third party and which

is recorded under organization's accounting system. These transactions are measurable in

monetary terms.

Types:

There are numerous types of accounting transactions. These are:

Purchasing goods and materials in which goods and materials are purchased by company

with respect to its business.

Sales transactions are common form under which transactions related with sales are

recorded.

Payment of wages and salaries.

Purchase of non current assets.

Accounting transactions related with payment of taxes.

Movement of cash and related transactions.

Raising of finance related transactions.

Single and double entry book keeping:

Single entry book keeping:

It is a cash oriented accounting. Under this form of book keeping single transaction for

the business transaction are recorded. Under this mode the income and expenses related with the

business are recorded in cash register. Here single entry for all the transactions are passed.

Double entry book keeping:

This concept is based on a principle that every transaction has equal and opposite effect

in at-least two different types of accounts. This is the current mode of recording transaction

(Beretta and Cencini, 2020). As per this system of book keeping the recording of transactions

starts with passing of journal entry which is followed by ledgers preparation. This will further be

carried out with the preparation of trial balance and financial statements.

Three important rules with respect to double entry bookkeeping:

Debit what comes in and credit what goes out.

Debit the receiver and credit the giver.

Question 1

Business transactions:

It refers to the transactions that occur between the company and the third party and which

is recorded under organization's accounting system. These transactions are measurable in

monetary terms.

Types:

There are numerous types of accounting transactions. These are:

Purchasing goods and materials in which goods and materials are purchased by company

with respect to its business.

Sales transactions are common form under which transactions related with sales are

recorded.

Payment of wages and salaries.

Purchase of non current assets.

Accounting transactions related with payment of taxes.

Movement of cash and related transactions.

Raising of finance related transactions.

Single and double entry book keeping:

Single entry book keeping:

It is a cash oriented accounting. Under this form of book keeping single transaction for

the business transaction are recorded. Under this mode the income and expenses related with the

business are recorded in cash register. Here single entry for all the transactions are passed.

Double entry book keeping:

This concept is based on a principle that every transaction has equal and opposite effect

in at-least two different types of accounts. This is the current mode of recording transaction

(Beretta and Cencini, 2020). As per this system of book keeping the recording of transactions

starts with passing of journal entry which is followed by ledgers preparation. This will further be

carried out with the preparation of trial balance and financial statements.

Three important rules with respect to double entry bookkeeping:

Debit what comes in and credit what goes out.

Debit the receiver and credit the giver.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

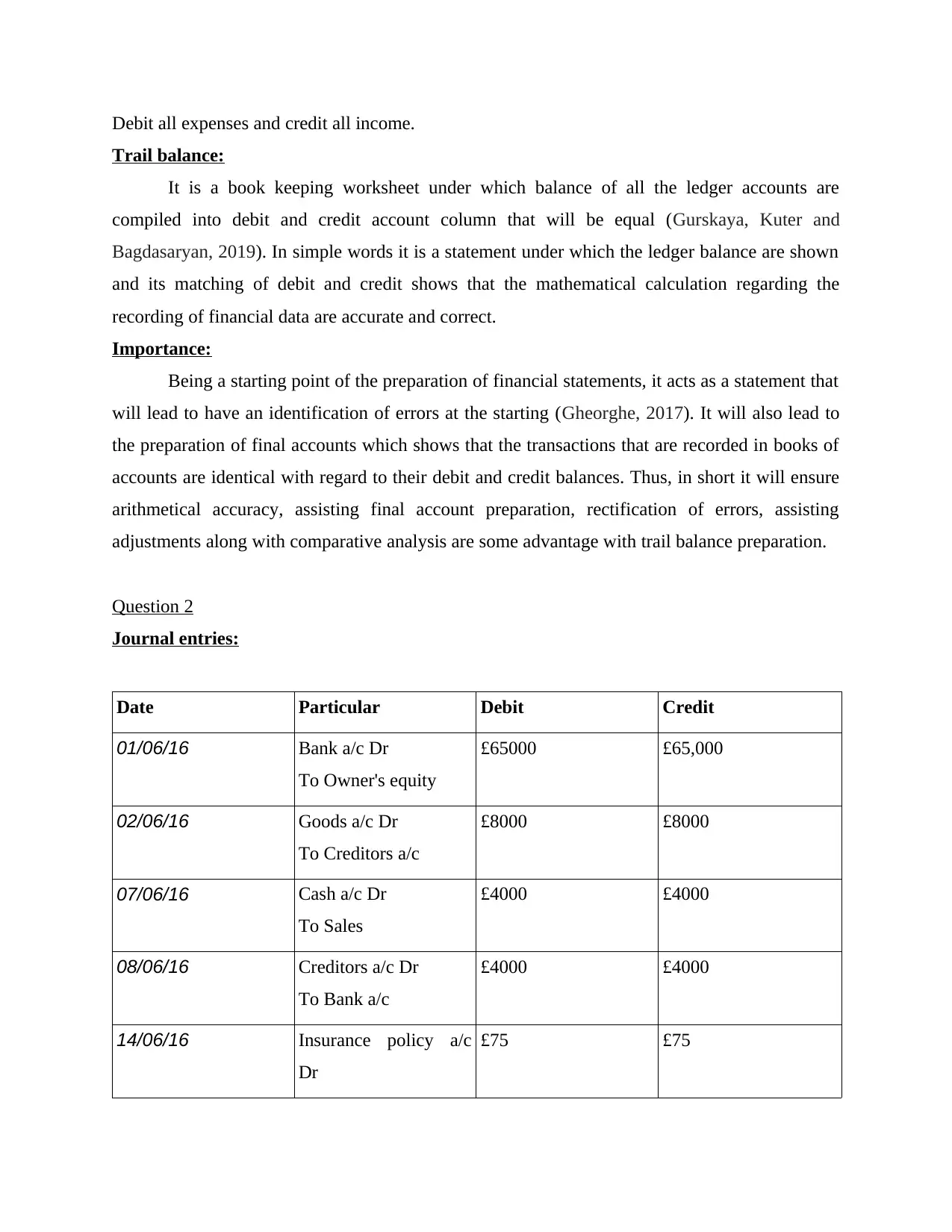

Debit all expenses and credit all income.

Trail balance:

It is a book keeping worksheet under which balance of all the ledger accounts are

compiled into debit and credit account column that will be equal (Gurskaya, Kuter and

Bagdasaryan, 2019). In simple words it is a statement under which the ledger balance are shown

and its matching of debit and credit shows that the mathematical calculation regarding the

recording of financial data are accurate and correct.

Importance:

Being a starting point of the preparation of financial statements, it acts as a statement that

will lead to have an identification of errors at the starting (Gheorghe, 2017). It will also lead to

the preparation of final accounts which shows that the transactions that are recorded in books of

accounts are identical with regard to their debit and credit balances. Thus, in short it will ensure

arithmetical accuracy, assisting final account preparation, rectification of errors, assisting

adjustments along with comparative analysis are some advantage with trail balance preparation.

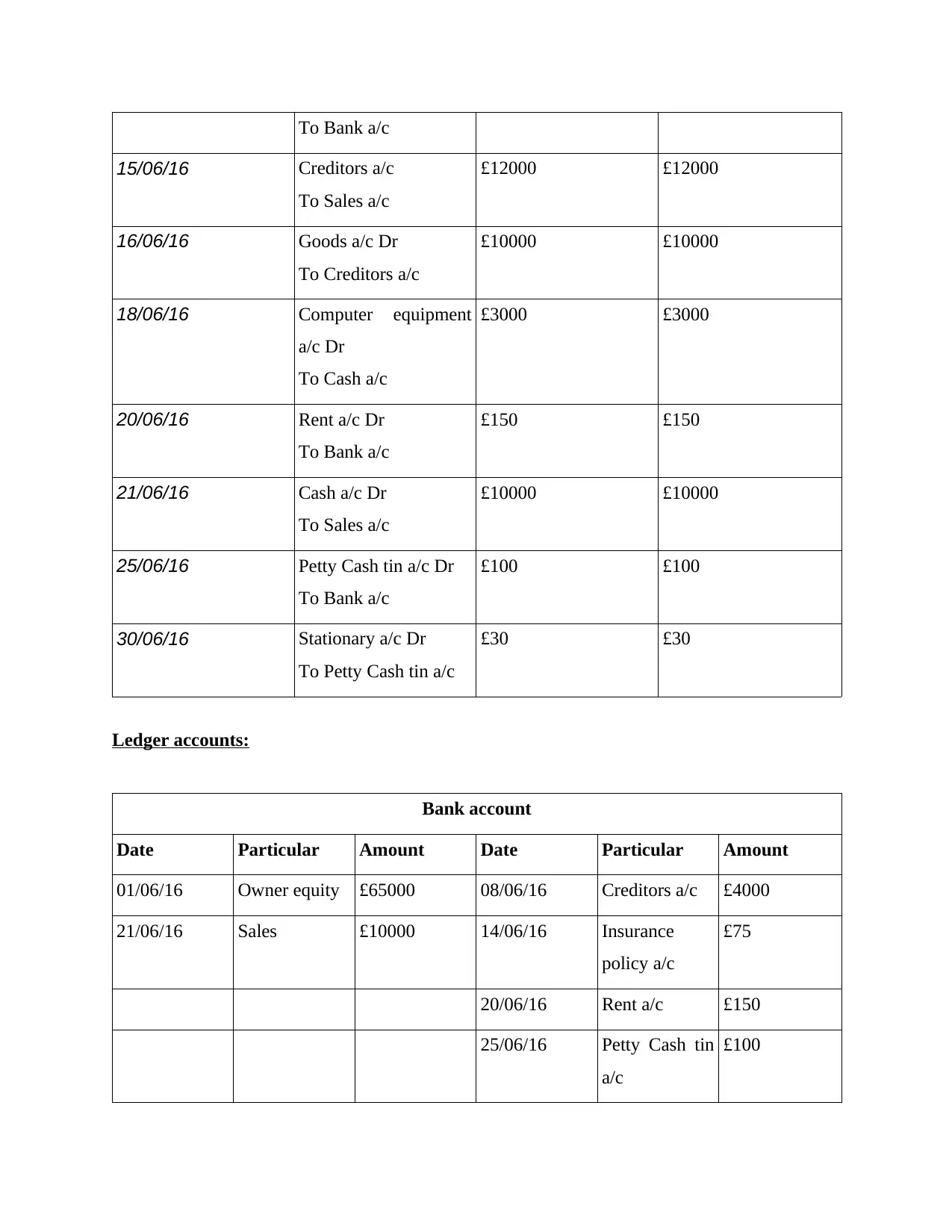

Question 2

Journal entries:

Date Particular Debit Credit

01/06/16 Bank a/c Dr

To Owner's equity

£65000 £65,000

02/06/16 Goods a/c Dr

To Creditors a/c

£8000 £8000

07/06/16 Cash a/c Dr

To Sales

£4000 £4000

08/06/16 Creditors a/c Dr

To Bank a/c

£4000 £4000

14/06/16 Insurance policy a/c

Dr

£75 £75

Trail balance:

It is a book keeping worksheet under which balance of all the ledger accounts are

compiled into debit and credit account column that will be equal (Gurskaya, Kuter and

Bagdasaryan, 2019). In simple words it is a statement under which the ledger balance are shown

and its matching of debit and credit shows that the mathematical calculation regarding the

recording of financial data are accurate and correct.

Importance:

Being a starting point of the preparation of financial statements, it acts as a statement that

will lead to have an identification of errors at the starting (Gheorghe, 2017). It will also lead to

the preparation of final accounts which shows that the transactions that are recorded in books of

accounts are identical with regard to their debit and credit balances. Thus, in short it will ensure

arithmetical accuracy, assisting final account preparation, rectification of errors, assisting

adjustments along with comparative analysis are some advantage with trail balance preparation.

Question 2

Journal entries:

Date Particular Debit Credit

01/06/16 Bank a/c Dr

To Owner's equity

£65000 £65,000

02/06/16 Goods a/c Dr

To Creditors a/c

£8000 £8000

07/06/16 Cash a/c Dr

To Sales

£4000 £4000

08/06/16 Creditors a/c Dr

To Bank a/c

£4000 £4000

14/06/16 Insurance policy a/c

Dr

£75 £75

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

To Bank a/c

15/06/16 Creditors a/c

To Sales a/c

£12000 £12000

16/06/16 Goods a/c Dr

To Creditors a/c

£10000 £10000

18/06/16 Computer equipment

a/c Dr

To Cash a/c

£3000 £3000

20/06/16 Rent a/c Dr

To Bank a/c

£150 £150

21/06/16 Cash a/c Dr

To Sales a/c

£10000 £10000

25/06/16 Petty Cash tin a/c Dr

To Bank a/c

£100 £100

30/06/16 Stationary a/c Dr

To Petty Cash tin a/c

£30 £30

Ledger accounts:

Bank account

Date Particular Amount Date Particular Amount

01/06/16 Owner equity £65000 08/06/16 Creditors a/c £4000

21/06/16 Sales £10000 14/06/16 Insurance

policy a/c

£75

20/06/16 Rent a/c £150

25/06/16 Petty Cash tin

a/c

£100

15/06/16 Creditors a/c

To Sales a/c

£12000 £12000

16/06/16 Goods a/c Dr

To Creditors a/c

£10000 £10000

18/06/16 Computer equipment

a/c Dr

To Cash a/c

£3000 £3000

20/06/16 Rent a/c Dr

To Bank a/c

£150 £150

21/06/16 Cash a/c Dr

To Sales a/c

£10000 £10000

25/06/16 Petty Cash tin a/c Dr

To Bank a/c

£100 £100

30/06/16 Stationary a/c Dr

To Petty Cash tin a/c

£30 £30

Ledger accounts:

Bank account

Date Particular Amount Date Particular Amount

01/06/16 Owner equity £65000 08/06/16 Creditors a/c £4000

21/06/16 Sales £10000 14/06/16 Insurance

policy a/c

£75

20/06/16 Rent a/c £150

25/06/16 Petty Cash tin

a/c

£100

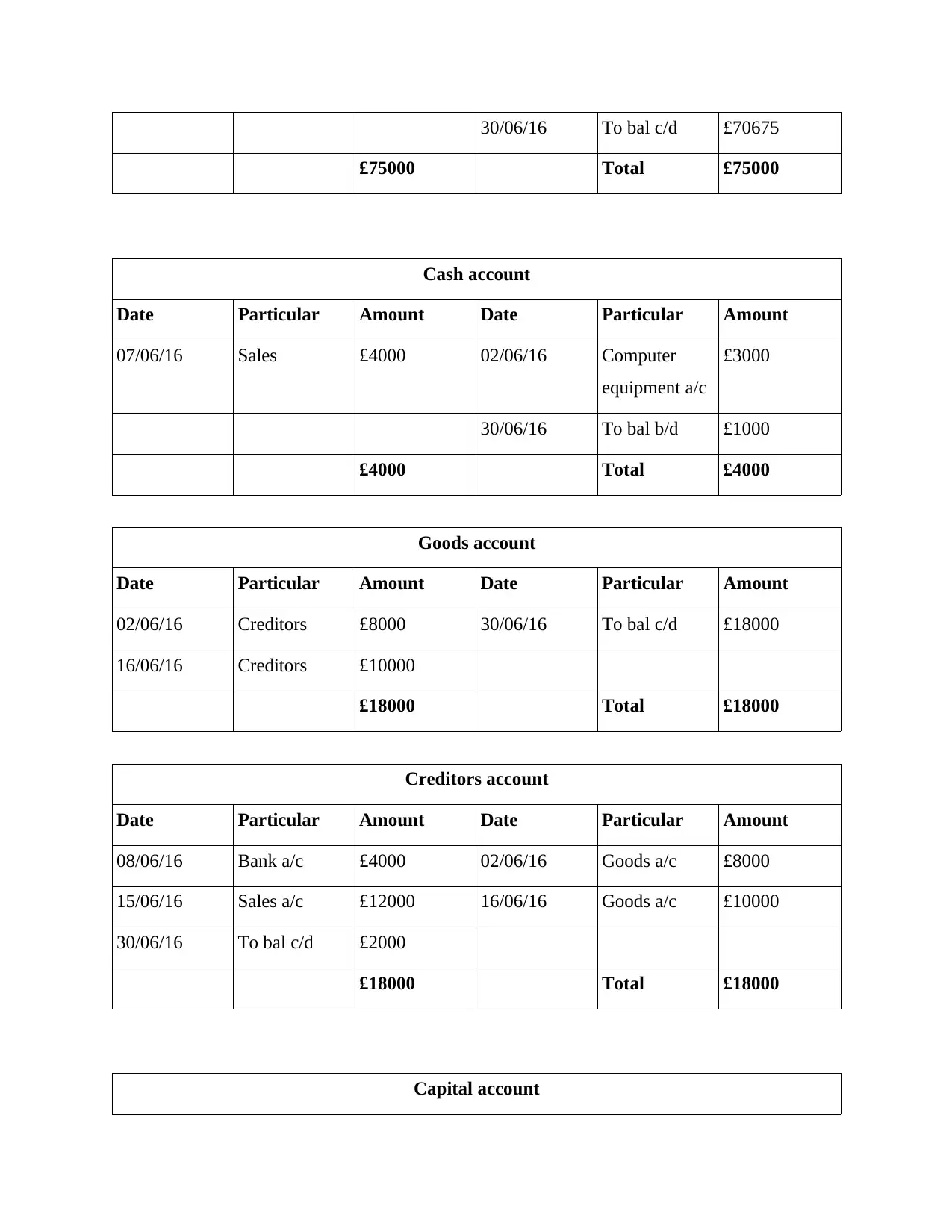

30/06/16 To bal c/d £70675

£75000 Total £75000

Cash account

Date Particular Amount Date Particular Amount

07/06/16 Sales £4000 02/06/16 Computer

equipment a/c

£3000

30/06/16 To bal b/d £1000

£4000 Total £4000

Goods account

Date Particular Amount Date Particular Amount

02/06/16 Creditors £8000 30/06/16 To bal c/d £18000

16/06/16 Creditors £10000

£18000 Total £18000

Creditors account

Date Particular Amount Date Particular Amount

08/06/16 Bank a/c £4000 02/06/16 Goods a/c £8000

15/06/16 Sales a/c £12000 16/06/16 Goods a/c £10000

30/06/16 To bal c/d £2000

£18000 Total £18000

Capital account

£75000 Total £75000

Cash account

Date Particular Amount Date Particular Amount

07/06/16 Sales £4000 02/06/16 Computer

equipment a/c

£3000

30/06/16 To bal b/d £1000

£4000 Total £4000

Goods account

Date Particular Amount Date Particular Amount

02/06/16 Creditors £8000 30/06/16 To bal c/d £18000

16/06/16 Creditors £10000

£18000 Total £18000

Creditors account

Date Particular Amount Date Particular Amount

08/06/16 Bank a/c £4000 02/06/16 Goods a/c £8000

15/06/16 Sales a/c £12000 16/06/16 Goods a/c £10000

30/06/16 To bal c/d £2000

£18000 Total £18000

Capital account

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

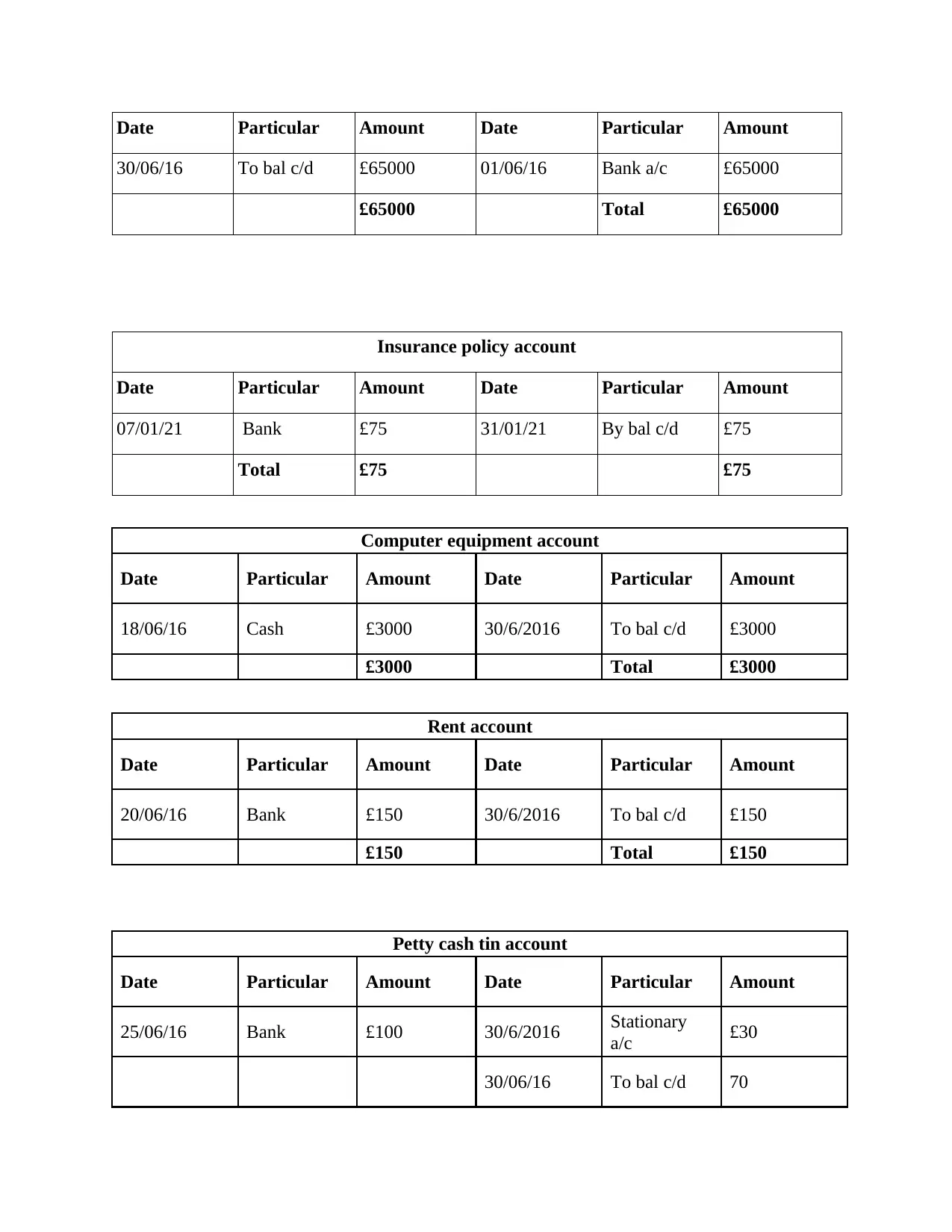

Date Particular Amount Date Particular Amount

30/06/16 To bal c/d £65000 01/06/16 Bank a/c £65000

£65000 Total £65000

Insurance policy account

Date Particular Amount Date Particular Amount

07/01/21 Bank £75 31/01/21 By bal c/d £75

Total £75 £75

Computer equipment account

Date Particular Amount Date Particular Amount

18/06/16 Cash £3000 30/6/2016 To bal c/d £3000

£3000 Total £3000

Rent account

Date Particular Amount Date Particular Amount

20/06/16 Bank £150 30/6/2016 To bal c/d £150

£150 Total £150

Petty cash tin account

Date Particular Amount Date Particular Amount

25/06/16 Bank £100 30/6/2016 Stationary

a/c £30

30/06/16 To bal c/d 70

30/06/16 To bal c/d £65000 01/06/16 Bank a/c £65000

£65000 Total £65000

Insurance policy account

Date Particular Amount Date Particular Amount

07/01/21 Bank £75 31/01/21 By bal c/d £75

Total £75 £75

Computer equipment account

Date Particular Amount Date Particular Amount

18/06/16 Cash £3000 30/6/2016 To bal c/d £3000

£3000 Total £3000

Rent account

Date Particular Amount Date Particular Amount

20/06/16 Bank £150 30/6/2016 To bal c/d £150

£150 Total £150

Petty cash tin account

Date Particular Amount Date Particular Amount

25/06/16 Bank £100 30/6/2016 Stationary

a/c £30

30/06/16 To bal c/d 70

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

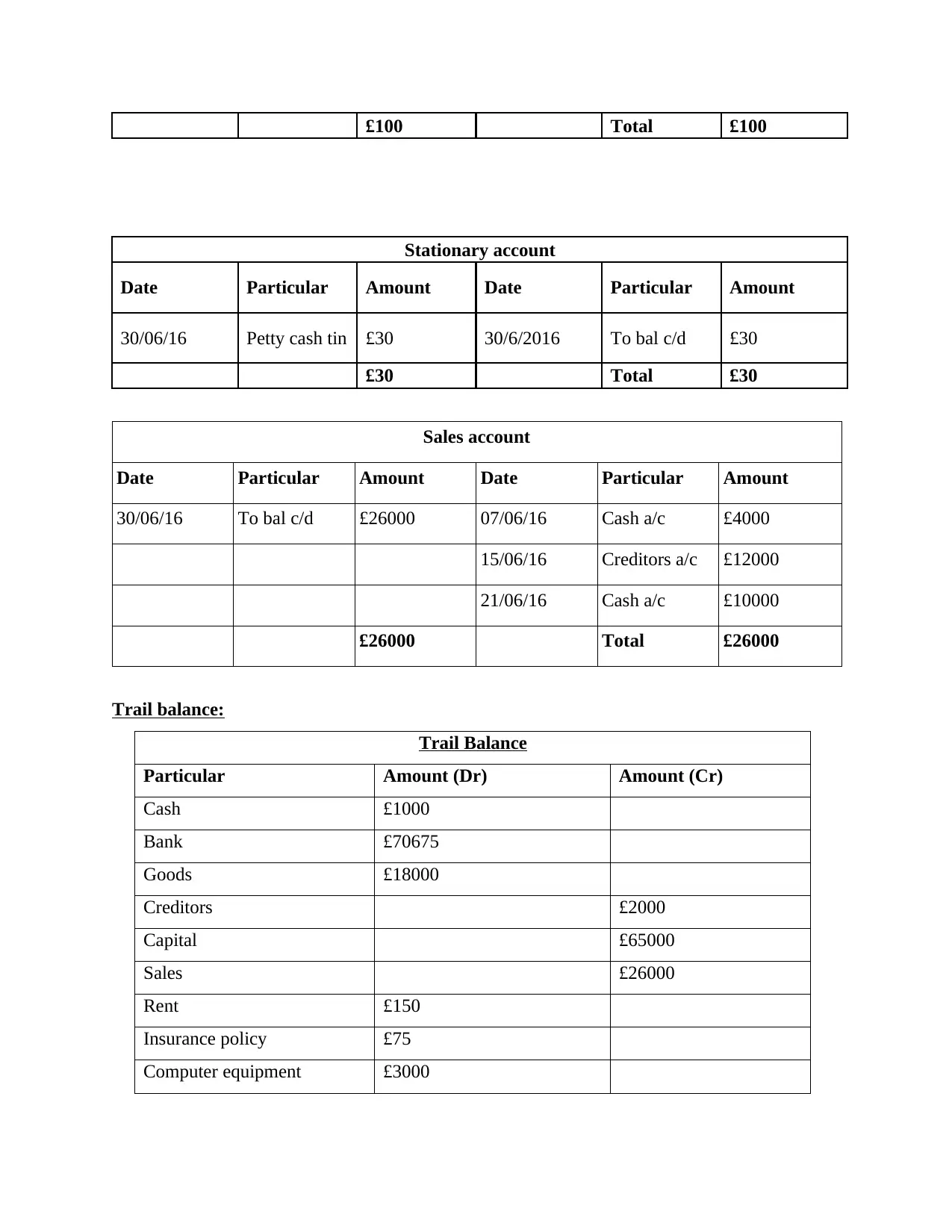

£100 Total £100

Stationary account

Date Particular Amount Date Particular Amount

30/06/16 Petty cash tin £30 30/6/2016 To bal c/d £30

£30 Total £30

Sales account

Date Particular Amount Date Particular Amount

30/06/16 To bal c/d £26000 07/06/16 Cash a/c £4000

15/06/16 Creditors a/c £12000

21/06/16 Cash a/c £10000

£26000 Total £26000

Trail balance:

Trail Balance

Particular Amount (Dr) Amount (Cr)

Cash £1000

Bank £70675

Goods £18000

Creditors £2000

Capital £65000

Sales £26000

Rent £150

Insurance policy £75

Computer equipment £3000

Stationary account

Date Particular Amount Date Particular Amount

30/06/16 Petty cash tin £30 30/6/2016 To bal c/d £30

£30 Total £30

Sales account

Date Particular Amount Date Particular Amount

30/06/16 To bal c/d £26000 07/06/16 Cash a/c £4000

15/06/16 Creditors a/c £12000

21/06/16 Cash a/c £10000

£26000 Total £26000

Trail balance:

Trail Balance

Particular Amount (Dr) Amount (Cr)

Cash £1000

Bank £70675

Goods £18000

Creditors £2000

Capital £65000

Sales £26000

Rent £150

Insurance policy £75

Computer equipment £3000

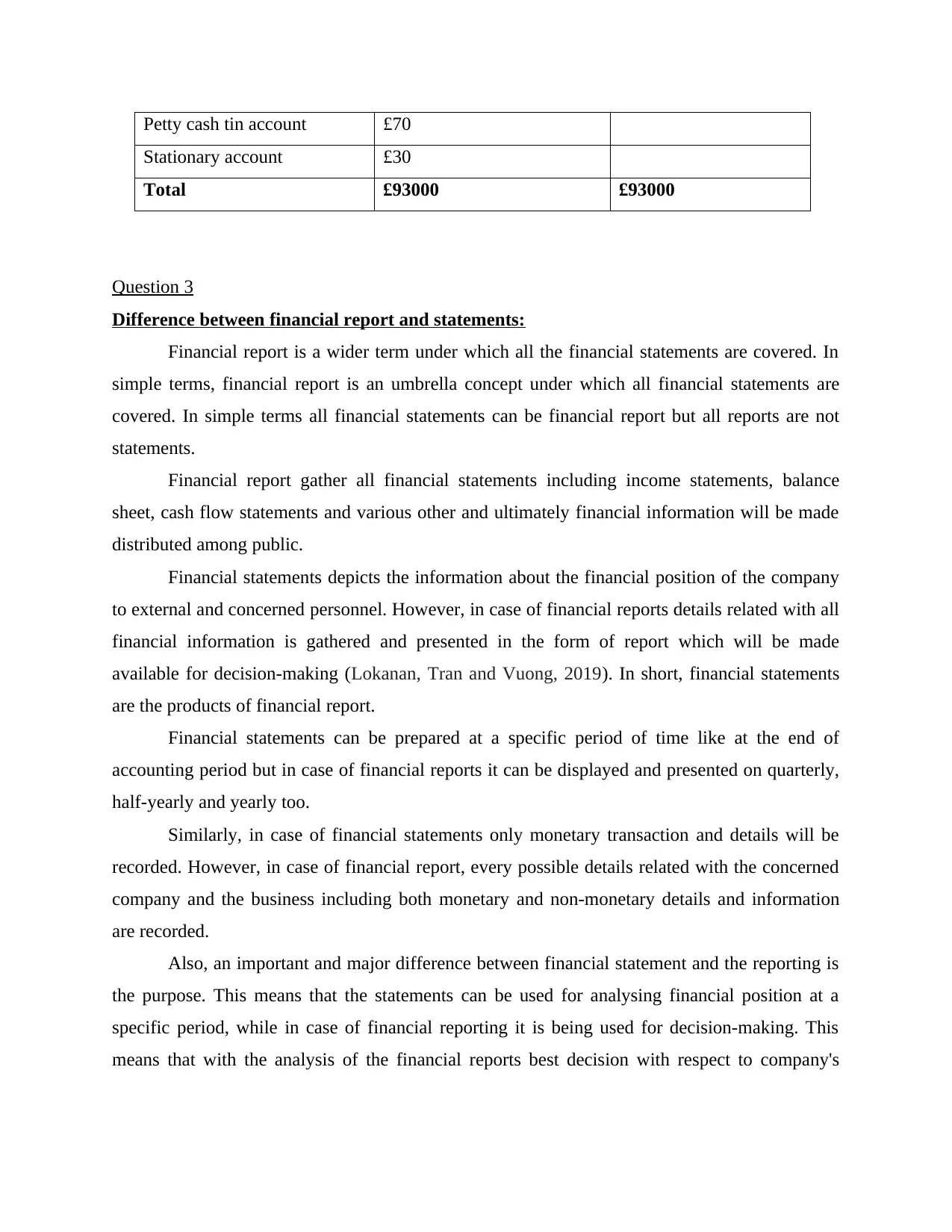

Petty cash tin account £70

Stationary account £30

Total £93000 £93000

Question 3

Difference between financial report and statements:

Financial report is a wider term under which all the financial statements are covered. In

simple terms, financial report is an umbrella concept under which all financial statements are

covered. In simple terms all financial statements can be financial report but all reports are not

statements.

Financial report gather all financial statements including income statements, balance

sheet, cash flow statements and various other and ultimately financial information will be made

distributed among public.

Financial statements depicts the information about the financial position of the company

to external and concerned personnel. However, in case of financial reports details related with all

financial information is gathered and presented in the form of report which will be made

available for decision-making (Lokanan, Tran and Vuong, 2019). In short, financial statements

are the products of financial report.

Financial statements can be prepared at a specific period of time like at the end of

accounting period but in case of financial reports it can be displayed and presented on quarterly,

half-yearly and yearly too.

Similarly, in case of financial statements only monetary transaction and details will be

recorded. However, in case of financial report, every possible details related with the concerned

company and the business including both monetary and non-monetary details and information

are recorded.

Also, an important and major difference between financial statement and the reporting is

the purpose. This means that the statements can be used for analysing financial position at a

specific period, while in case of financial reporting it is being used for decision-making. This

means that with the analysis of the financial reports best decision with respect to company's

Stationary account £30

Total £93000 £93000

Question 3

Difference between financial report and statements:

Financial report is a wider term under which all the financial statements are covered. In

simple terms, financial report is an umbrella concept under which all financial statements are

covered. In simple terms all financial statements can be financial report but all reports are not

statements.

Financial report gather all financial statements including income statements, balance

sheet, cash flow statements and various other and ultimately financial information will be made

distributed among public.

Financial statements depicts the information about the financial position of the company

to external and concerned personnel. However, in case of financial reports details related with all

financial information is gathered and presented in the form of report which will be made

available for decision-making (Lokanan, Tran and Vuong, 2019). In short, financial statements

are the products of financial report.

Financial statements can be prepared at a specific period of time like at the end of

accounting period but in case of financial reports it can be displayed and presented on quarterly,

half-yearly and yearly too.

Similarly, in case of financial statements only monetary transaction and details will be

recorded. However, in case of financial report, every possible details related with the concerned

company and the business including both monetary and non-monetary details and information

are recorded.

Also, an important and major difference between financial statement and the reporting is

the purpose. This means that the statements can be used for analysing financial position at a

specific period, while in case of financial reporting it is being used for decision-making. This

means that with the analysis of the financial reports best decision with respect to company's

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

betterment can be taken. These decision may either be related with the investment or of

financing.

Examples of financial statements may include Balance sheet, Income statements, cash

flow statements.

Example of financial reports includes external statements, financial notes, quarterly and

annual records, government reports.

Users:

Owners, Managers and Employees are the internal users.

Suppliers, Banks, Investors, Customers are the all counted as external users.

Importance of financial reports:

The major importance of financial report is to have an analysis of the actual money a

business have, from which sources the money come and where it will go and invested. These

reports enable the business to have an idea of overall business and its financial capabilities

(Omoolorun and Abilogun, 2017). Likewise, it is most advantageous to management because it

enables them to take decision based on the company's financial health. Also, as financial reports

may include the financial statements too so it will be used to have an analysis of the company's

financial position. It will entitle the snapshot of company's financial health in terms of delivering

information of cash flows, operations and its performance. Likewise, financial reports are useful

for company's internal as well as external stakeholders. This means that with the use of the

financial reports internal stakeholders like concerned managers will take the decision with

respect to company and its business. Similarly, its study also assist the investors to take

investment decisions. Likewise, it is also to be noted that as the financial reports include the

financial statements so it will again raise importance in terms of enabling financial performance

and position.

Question 4

Principles of accounting:

Accounting principles are the rules that the organization follows while reporting financial

information. These are the guidelines which are need to be kept and considered while recording

transactions.

Accounting principles:

financing.

Examples of financial statements may include Balance sheet, Income statements, cash

flow statements.

Example of financial reports includes external statements, financial notes, quarterly and

annual records, government reports.

Users:

Owners, Managers and Employees are the internal users.

Suppliers, Banks, Investors, Customers are the all counted as external users.

Importance of financial reports:

The major importance of financial report is to have an analysis of the actual money a

business have, from which sources the money come and where it will go and invested. These

reports enable the business to have an idea of overall business and its financial capabilities

(Omoolorun and Abilogun, 2017). Likewise, it is most advantageous to management because it

enables them to take decision based on the company's financial health. Also, as financial reports

may include the financial statements too so it will be used to have an analysis of the company's

financial position. It will entitle the snapshot of company's financial health in terms of delivering

information of cash flows, operations and its performance. Likewise, financial reports are useful

for company's internal as well as external stakeholders. This means that with the use of the

financial reports internal stakeholders like concerned managers will take the decision with

respect to company and its business. Similarly, its study also assist the investors to take

investment decisions. Likewise, it is also to be noted that as the financial reports include the

financial statements so it will again raise importance in terms of enabling financial performance

and position.

Question 4

Principles of accounting:

Accounting principles are the rules that the organization follows while reporting financial

information. These are the guidelines which are need to be kept and considered while recording

transactions.

Accounting principles:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accrual principle:

As per this principle accounting transactions will be recorded when they actually occur

rather than on the time when the payment and due will be received (Aqeel, Aws and Nawfal,

2020). This is the fundamental principle which assist that the financial statement shows the

details of all the transactions in an accounting period. This principle also assist the preparation of

financial statement in the respected accounting period. This means instead of delayed time and

lengthy process this principle suggest the recording of transaction within the respected

accounting period.

Conservatism principle:

This principle suggest that the expenses and liabilities are need to be recorded when they

have occurred. However, revenue and assets will be recorded only when there is surety related

with its occurrence. In short this principle focus on recording losses and expenses on early basis

rather than income. The concept related with this principle is that there may be delay in the

occurrence of revenue and profits, however expenses and liabilities occurred at the actual time.

Thus, recording of expenses at the actual time will predict a true image of company's financial

position.

Consistency principle:

As per this principle once a method of accounting and recording will be adopted then it

will needed to be carried out consistently (Shaw, 2021). This continuity will be carried out until

new and better principle will come across. This means that there will be no shuffling and shifting

of methods again and again.

Cost principle:

As per this principle the assets, liabilities and equity investments need to be recorded on

its original purchased cost. However, this principle is less valid because the host of accounting

standards shows that the assets and liabilities need to be recorded at face value.

Economic entity principle:

As per this principle the transactions of business and the owners will be recorded

separately. This principle prevent intermingling of business and its owner's transactions. This

will also safeguard the facing of difficulties when the accounts of the business will be audited.

Full disclosure principle:

As per this principle accounting transactions will be recorded when they actually occur

rather than on the time when the payment and due will be received (Aqeel, Aws and Nawfal,

2020). This is the fundamental principle which assist that the financial statement shows the

details of all the transactions in an accounting period. This principle also assist the preparation of

financial statement in the respected accounting period. This means instead of delayed time and

lengthy process this principle suggest the recording of transaction within the respected

accounting period.

Conservatism principle:

This principle suggest that the expenses and liabilities are need to be recorded when they

have occurred. However, revenue and assets will be recorded only when there is surety related

with its occurrence. In short this principle focus on recording losses and expenses on early basis

rather than income. The concept related with this principle is that there may be delay in the

occurrence of revenue and profits, however expenses and liabilities occurred at the actual time.

Thus, recording of expenses at the actual time will predict a true image of company's financial

position.

Consistency principle:

As per this principle once a method of accounting and recording will be adopted then it

will needed to be carried out consistently (Shaw, 2021). This continuity will be carried out until

new and better principle will come across. This means that there will be no shuffling and shifting

of methods again and again.

Cost principle:

As per this principle the assets, liabilities and equity investments need to be recorded on

its original purchased cost. However, this principle is less valid because the host of accounting

standards shows that the assets and liabilities need to be recorded at face value.

Economic entity principle:

As per this principle the transactions of business and the owners will be recorded

separately. This principle prevent intermingling of business and its owner's transactions. This

will also safeguard the facing of difficulties when the accounts of the business will be audited.

Full disclosure principle:

According to this principle, every relevant information related with the financial

statements need to be disclosed fully (Comandaru and et.al., 2020). This means that the

information that is required for understanding financial statements need to be disclosed fully.

This principle is based on the fact that the reader of the financial statements can understood them

fully and adequately.

Going concern principle:

This principle shows that the business will run continuously (Kumar, 2020). This means

that the business will continue for unforeseeable future. Various changes in terms of coming and

going of stakeholders and owners will occur but the business will be continue for long period.

Matching principle:

As per this principle recording of revenue will be match with the same recording of

expenses. This means that the revenue will be justified with relevant expenses (Basic accounting

principles, 2021). This is based on accrual concept in which transactions will be recorded on

actual occurrence. Cash basis is not applicable as per this principle.

Materiality principle:

All the material information must be recorded. This means that the material and

important information will need to be recorded (Bardford, 2020). This principle also states that

all transactions must be recorded in accounting records so that the most relevant decision will be

taken by the reader with respect to concerned business.

Monetary unit principle:

As per this principle only those transactions will be recorded which has monetary value

and can be determined in monetary terms. Thus, as per this principle it would be easy to record

the purchase of fixed asset rather then recording the value that it deliver towards the company.

Reliability principle:

Only those informations that can be proven and reliable are the part of recording. This

means that reliable and relevant information will need to be recorded (Guliyev and

Hajiyev,2020). This is the basis of auditing. The best example of this principle is the recording of

expenses based on invoice related with the sale or purchase of products and goods to or from

supplier .

Revenue recognition principle:

statements need to be disclosed fully (Comandaru and et.al., 2020). This means that the

information that is required for understanding financial statements need to be disclosed fully.

This principle is based on the fact that the reader of the financial statements can understood them

fully and adequately.

Going concern principle:

This principle shows that the business will run continuously (Kumar, 2020). This means

that the business will continue for unforeseeable future. Various changes in terms of coming and

going of stakeholders and owners will occur but the business will be continue for long period.

Matching principle:

As per this principle recording of revenue will be match with the same recording of

expenses. This means that the revenue will be justified with relevant expenses (Basic accounting

principles, 2021). This is based on accrual concept in which transactions will be recorded on

actual occurrence. Cash basis is not applicable as per this principle.

Materiality principle:

All the material information must be recorded. This means that the material and

important information will need to be recorded (Bardford, 2020). This principle also states that

all transactions must be recorded in accounting records so that the most relevant decision will be

taken by the reader with respect to concerned business.

Monetary unit principle:

As per this principle only those transactions will be recorded which has monetary value

and can be determined in monetary terms. Thus, as per this principle it would be easy to record

the purchase of fixed asset rather then recording the value that it deliver towards the company.

Reliability principle:

Only those informations that can be proven and reliable are the part of recording. This

means that reliable and relevant information will need to be recorded (Guliyev and

Hajiyev,2020). This is the basis of auditing. The best example of this principle is the recording of

expenses based on invoice related with the sale or purchase of products and goods to or from

supplier .

Revenue recognition principle:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.