Financial Accounting Assignment: Analysis and Calculations

VerifiedAdded on 2022/11/24

|27

|4597

|451

Homework Assignment

AI Summary

This document presents a comprehensive solution to a financial accounting assignment, addressing key concepts and practical applications. The assignment includes detailed explanations of different types of business transactions (cash and credit), bookkeeping systems (single and double-entry), and the importance of trial balances. It also features calculations and journal entries, alongside the differences between financial statements and financial reports. Furthermore, the assignment covers accounting principles (conservatism, consistency, cost, etc.), profit and loss accounts, cash flow statements, bank reconciliations, control accounts, and suspense accounts. The solution provides step-by-step calculations, comparative analyses, and theoretical explanations, making it a valuable resource for students studying financial accounting. The document is a student contribution to Desklib, a platform offering AI-based study tools.

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................3

QUESTION 1.................................................................................................................................................3

Different types of business transaction...................................................................................................3

QUESTION 2.................................................................................................................................................5

Calculation...............................................................................................................................................5

QUESTION 3...............................................................................................................................................10

Different between financial statement and financial report.................................................................10

QUESTION 4...............................................................................................................................................12

Principles of accounting.........................................................................................................................12

QUESTION 5...............................................................................................................................................14

Calculation.............................................................................................................................................14

QUESTION 6...............................................................................................................................................16

Profit and Loss Account.........................................................................................................................16

QUESTION 7...............................................................................................................................................17

Cash flow statement..............................................................................................................................17

SCENARIO 2...............................................................................................................................................18

QUESTION 1...............................................................................................................................................18

Bank Reconciliation...............................................................................................................................18

QUESTION 2...............................................................................................................................................19

Control accounts....................................................................................................................................19

QUESTION 3...............................................................................................................................................20

Suspense Account..................................................................................................................................20

QUESTION 4...............................................................................................................................................21

(a) Required to prepare updated cash book and bank reconciliation statement..................................21

QUESTION 5...............................................................................................................................................22

Journal entries.......................................................................................................................................22

CONCLUSION.............................................................................................................................................24

REFERENCES..............................................................................................................................................25

INTRODUCTION...........................................................................................................................................3

QUESTION 1.................................................................................................................................................3

Different types of business transaction...................................................................................................3

QUESTION 2.................................................................................................................................................5

Calculation...............................................................................................................................................5

QUESTION 3...............................................................................................................................................10

Different between financial statement and financial report.................................................................10

QUESTION 4...............................................................................................................................................12

Principles of accounting.........................................................................................................................12

QUESTION 5...............................................................................................................................................14

Calculation.............................................................................................................................................14

QUESTION 6...............................................................................................................................................16

Profit and Loss Account.........................................................................................................................16

QUESTION 7...............................................................................................................................................17

Cash flow statement..............................................................................................................................17

SCENARIO 2...............................................................................................................................................18

QUESTION 1...............................................................................................................................................18

Bank Reconciliation...............................................................................................................................18

QUESTION 2...............................................................................................................................................19

Control accounts....................................................................................................................................19

QUESTION 3...............................................................................................................................................20

Suspense Account..................................................................................................................................20

QUESTION 4...............................................................................................................................................21

(a) Required to prepare updated cash book and bank reconciliation statement..................................21

QUESTION 5...............................................................................................................................................22

Journal entries.......................................................................................................................................22

CONCLUSION.............................................................................................................................................24

REFERENCES..............................................................................................................................................25

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial accounting is focused with delivering information to outside parties such as

investors, bondholders, and many others. Managerial accounting offers the necessary data for

companies to function. Financial accounting offers the evaluation that is used to evaluate a

corporation's previous performance. Because management accounting is focused on

management, any study of it must begin with a basic grasp of what executives do, the

information they need to make, and the overall company context. Financial accounting is a part

of accounting that concerns with the activity of gathering, evaluating, and documenting money

transfers for a business (Halim, 2021). The intention is to consistently store, compile, and display

financial data in order to determine the issuer's financial outcomes for a specific accounting

period. As a result, financial accounting entails selecting appropriate, trustworthy, and precise

data to the individual's interested parties about its operational profit and financial condition.

Furthermore, such financial statements or filings are created in accordance with the following

structure and accountancy standards applicable to the individual's area or nation.

QUESTION 1

Different types of business transaction

Business Transactions are occurrences that lead in external technology transfers between a

company and then another company, or an independent of individuals, and have an impact on the

investor’s portfolio, obligations, and/or equity. Business transactions are recorded in the

accounting period and are assumed to take place at a distance. Each entity should keep track of

its transactions in accordance with the idea of the business. Documentation should be provided in

backing of all business transactions. The grounds element for preparing and presenting financial

statements is business transactions. Each firm, whether an independent audit or a corporation,

must recognize and document financial activity as they happen. There are mentioned two types

of business transactions such as:

Cash transaction: Cash transactions are those that are repaid in currency right away.

Cheque transfers are also considered cash purchases. Income and expenses and payments made

are two types of money transfers. A cash deal is a financial contract in which money is

Financial accounting is focused with delivering information to outside parties such as

investors, bondholders, and many others. Managerial accounting offers the necessary data for

companies to function. Financial accounting offers the evaluation that is used to evaluate a

corporation's previous performance. Because management accounting is focused on

management, any study of it must begin with a basic grasp of what executives do, the

information they need to make, and the overall company context. Financial accounting is a part

of accounting that concerns with the activity of gathering, evaluating, and documenting money

transfers for a business (Halim, 2021). The intention is to consistently store, compile, and display

financial data in order to determine the issuer's financial outcomes for a specific accounting

period. As a result, financial accounting entails selecting appropriate, trustworthy, and precise

data to the individual's interested parties about its operational profit and financial condition.

Furthermore, such financial statements or filings are created in accordance with the following

structure and accountancy standards applicable to the individual's area or nation.

QUESTION 1

Different types of business transaction

Business Transactions are occurrences that lead in external technology transfers between a

company and then another company, or an independent of individuals, and have an impact on the

investor’s portfolio, obligations, and/or equity. Business transactions are recorded in the

accounting period and are assumed to take place at a distance. Each entity should keep track of

its transactions in accordance with the idea of the business. Documentation should be provided in

backing of all business transactions. The grounds element for preparing and presenting financial

statements is business transactions. Each firm, whether an independent audit or a corporation,

must recognize and document financial activity as they happen. There are mentioned two types

of business transactions such as:

Cash transaction: Cash transactions are those that are repaid in currency right away.

Cheque transfers are also considered cash purchases. Income and expenses and payments made

are two types of money transfers. A cash deal is a financial contract in which money is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

exchanged at the moment the transaction takes place. In this example, cash denotes a resolution

— the payout may be in cash, debit cards cardholders, cheque transaction, or direct deposit, but it

was still considered a cash trade whether it was completed at the beginning of each month. For

contrast, for the over price of products entails the exchanging of items for money at the moment

of the sale, making it a cash deal (Kustono and Nanggala, 2020). If the purchase is paid for with

cash or a card payment card, it qualifies as a cash transaction. Both the benefits and the income

statement of bookkeeping capture money transfers in accounting system. These activities have an

instant impact on the money market fund.

Credit transaction: A credit transaction is a commercial transaction that, while having

monetary consequences, does not require the interchange of currency at the point of the issuer's

execution, but is resolved in funds at a later date. In the account books, monetary rewards lead to

formation of an assets or debt. At just the end of the tenure, this property or obligation is

removed from the records. A producer, for illustration, delivers his items to a reseller who

doesn't really paying for them right away but is given a month credit money to pay. It really is a

credit sale of products that does not include an instantaneous currency interchange but does

result in the recording of profit and the formation of a borrower, therefore it constitutes as a

financial product.

Define single entry book keeping:

A single-entry bookkeeping system, as opposed to a much more common dual

bookkeeping system, documents any financial statement with only one addition to the financial

statements. The financial statements are the focal point of a single-entry accounting system,

which focuses on the company's income. Monetary transfers and collecting payments are the

most important data to track using this technique (Bakhadirovich, 2020).

Define double entry book keeping:

The double-entry system is a method of accountancy wherein the transactions are made

in two separate entries. The most popular accounting method, which was created in the 13th

century, it's a double system. Assets are conducted in both the credit and debit accounts when

using the Dual method.

— the payout may be in cash, debit cards cardholders, cheque transaction, or direct deposit, but it

was still considered a cash trade whether it was completed at the beginning of each month. For

contrast, for the over price of products entails the exchanging of items for money at the moment

of the sale, making it a cash deal (Kustono and Nanggala, 2020). If the purchase is paid for with

cash or a card payment card, it qualifies as a cash transaction. Both the benefits and the income

statement of bookkeeping capture money transfers in accounting system. These activities have an

instant impact on the money market fund.

Credit transaction: A credit transaction is a commercial transaction that, while having

monetary consequences, does not require the interchange of currency at the point of the issuer's

execution, but is resolved in funds at a later date. In the account books, monetary rewards lead to

formation of an assets or debt. At just the end of the tenure, this property or obligation is

removed from the records. A producer, for illustration, delivers his items to a reseller who

doesn't really paying for them right away but is given a month credit money to pay. It really is a

credit sale of products that does not include an instantaneous currency interchange but does

result in the recording of profit and the formation of a borrower, therefore it constitutes as a

financial product.

Define single entry book keeping:

A single-entry bookkeeping system, as opposed to a much more common dual

bookkeeping system, documents any financial statement with only one addition to the financial

statements. The financial statements are the focal point of a single-entry accounting system,

which focuses on the company's income. Monetary transfers and collecting payments are the

most important data to track using this technique (Bakhadirovich, 2020).

Define double entry book keeping:

The double-entry system is a method of accountancy wherein the transactions are made

in two separate entries. The most popular accounting method, which was created in the 13th

century, it's a double system. Assets are conducted in both the credit and debit accounts when

using the Dual method.

Explain trial balance and its importance

A trial balance is a chart that explains the debit and credit amounts of all accounting records,

along with the balance sheet. The cardinal standards of financial accounting are that "the

financial statement has always been equal" and "each financial transaction has an equal debit and

credit." As a result, the sum of all account balances must've been identical.

The Trial Balance report is crucial because it provides a comprehensive picture of all

accounting records. This report combines all of the Balance Sheet and Profit and Loss categories

into one report. In a comparison, you may quickly detect financial accounts that appear to be

incorrect, such as those that are either too big or too small. While running additional annual

documents like the Profit and Loss or Cash Flows, this allows you to discover and diagnose

errors. Prediction and assessment are also essential aspects of the Trial Balance reporting. To

evaluate expenditures, liabilities, and revenue, you might review of this week's accounts and one

of previous year's accounts (Antik, 2021).

QUESTION 2

Calculation

Journal entries

Date Particulars CR DR

01/06/16 Cash a/c DR

To capital a/c

65000

65000

02/06/16 Purchase a/c DR

To accounts payable a/c

8000

8000

07/06/2016 Cash a/c DR

To sales a/c

4000

4000

08/06/16 Accounts payable a/c DR

To bank a/c

4000

4000

14/06/2016 Insurance expense a/c DR

To bank a/c

75

75

A trial balance is a chart that explains the debit and credit amounts of all accounting records,

along with the balance sheet. The cardinal standards of financial accounting are that "the

financial statement has always been equal" and "each financial transaction has an equal debit and

credit." As a result, the sum of all account balances must've been identical.

The Trial Balance report is crucial because it provides a comprehensive picture of all

accounting records. This report combines all of the Balance Sheet and Profit and Loss categories

into one report. In a comparison, you may quickly detect financial accounts that appear to be

incorrect, such as those that are either too big or too small. While running additional annual

documents like the Profit and Loss or Cash Flows, this allows you to discover and diagnose

errors. Prediction and assessment are also essential aspects of the Trial Balance reporting. To

evaluate expenditures, liabilities, and revenue, you might review of this week's accounts and one

of previous year's accounts (Antik, 2021).

QUESTION 2

Calculation

Journal entries

Date Particulars CR DR

01/06/16 Cash a/c DR

To capital a/c

65000

65000

02/06/16 Purchase a/c DR

To accounts payable a/c

8000

8000

07/06/2016 Cash a/c DR

To sales a/c

4000

4000

08/06/16 Accounts payable a/c DR

To bank a/c

4000

4000

14/06/2016 Insurance expense a/c DR

To bank a/c

75

75

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

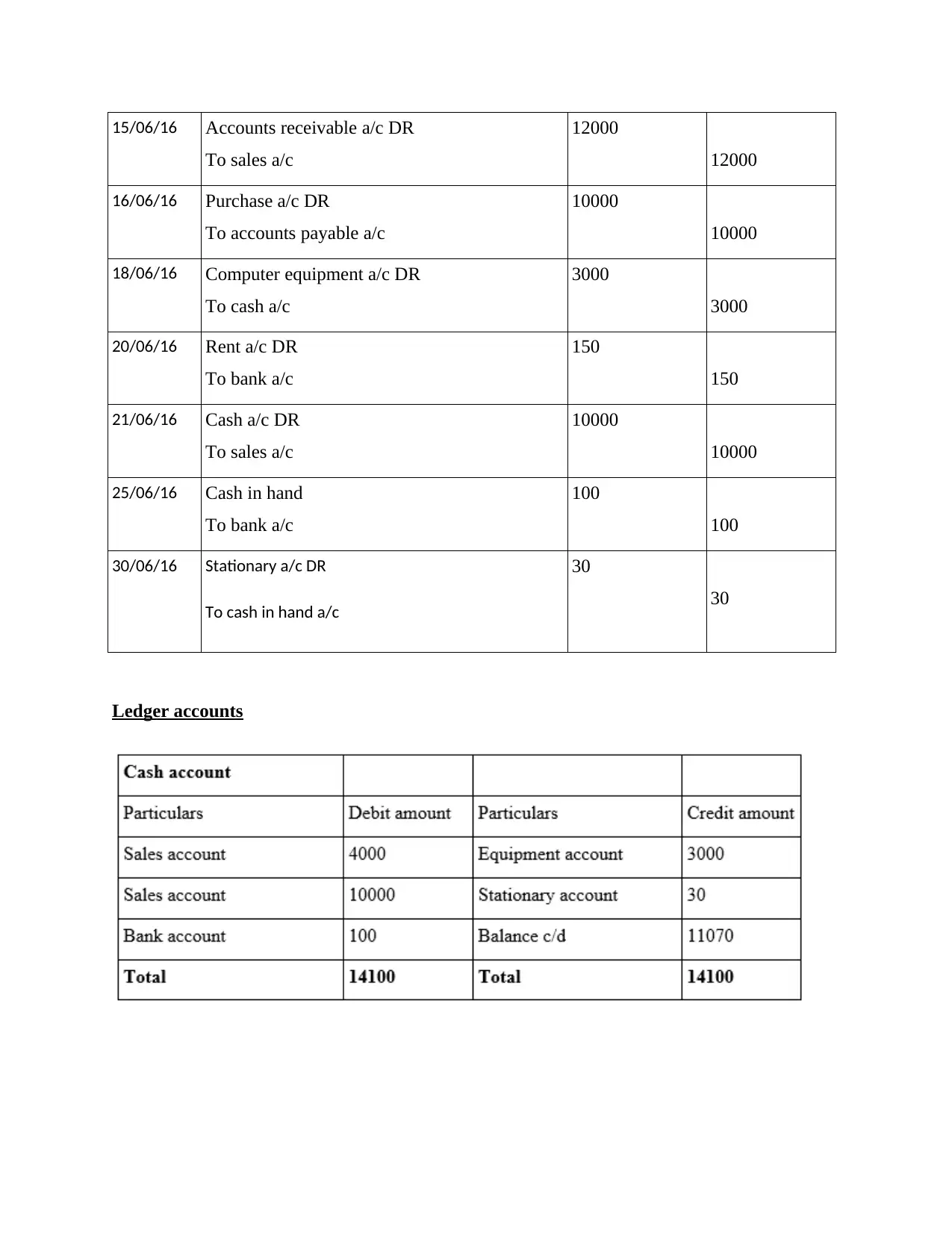

15/06/16 Accounts receivable a/c DR

To sales a/c

12000

12000

16/06/16 Purchase a/c DR

To accounts payable a/c

10000

10000

18/06/16 Computer equipment a/c DR

To cash a/c

3000

3000

20/06/16 Rent a/c DR

To bank a/c

150

150

21/06/16 Cash a/c DR

To sales a/c

10000

10000

25/06/16 Cash in hand

To bank a/c

100

100

30/06/16 Stationary a/c DR

To cash in hand a/c

30

30

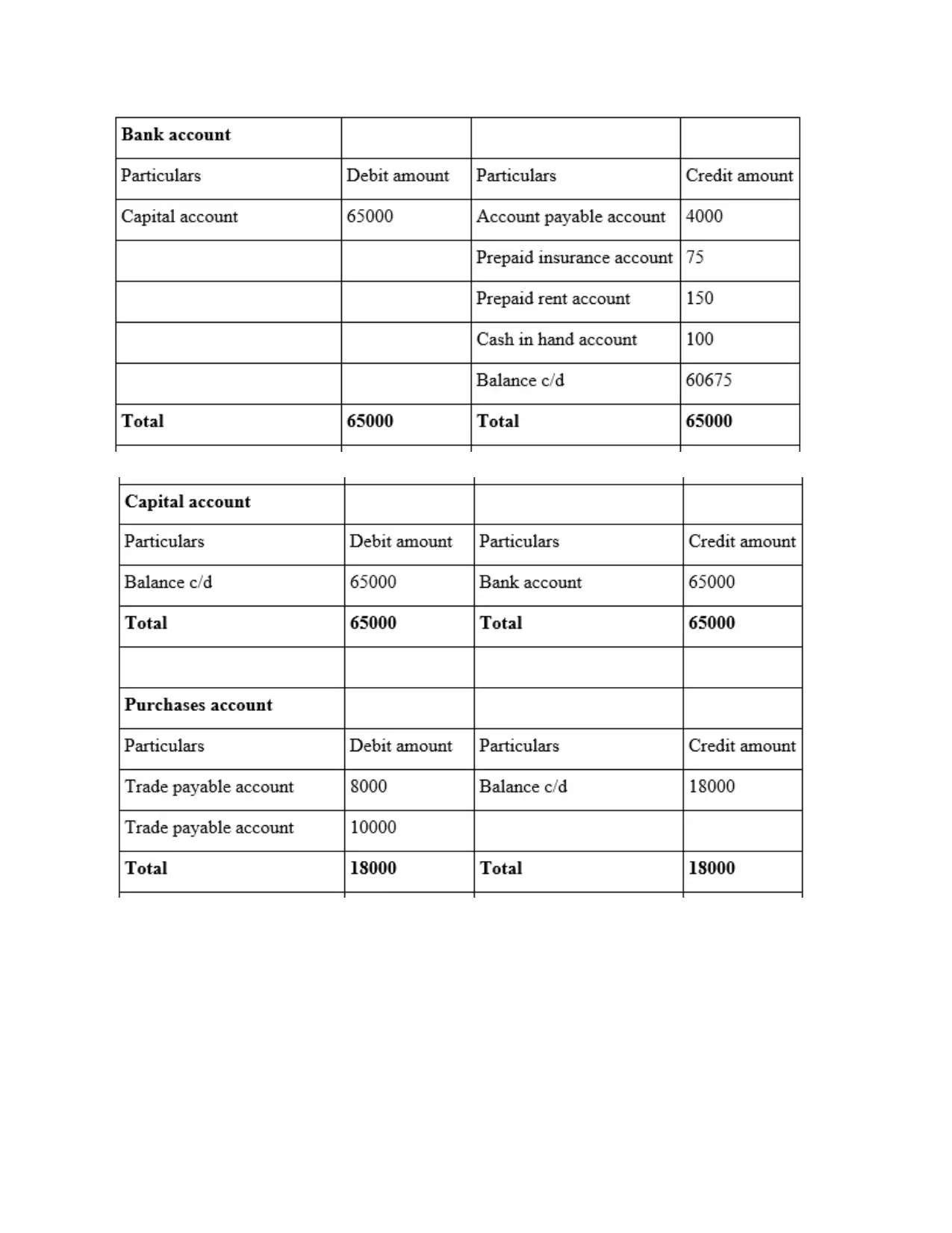

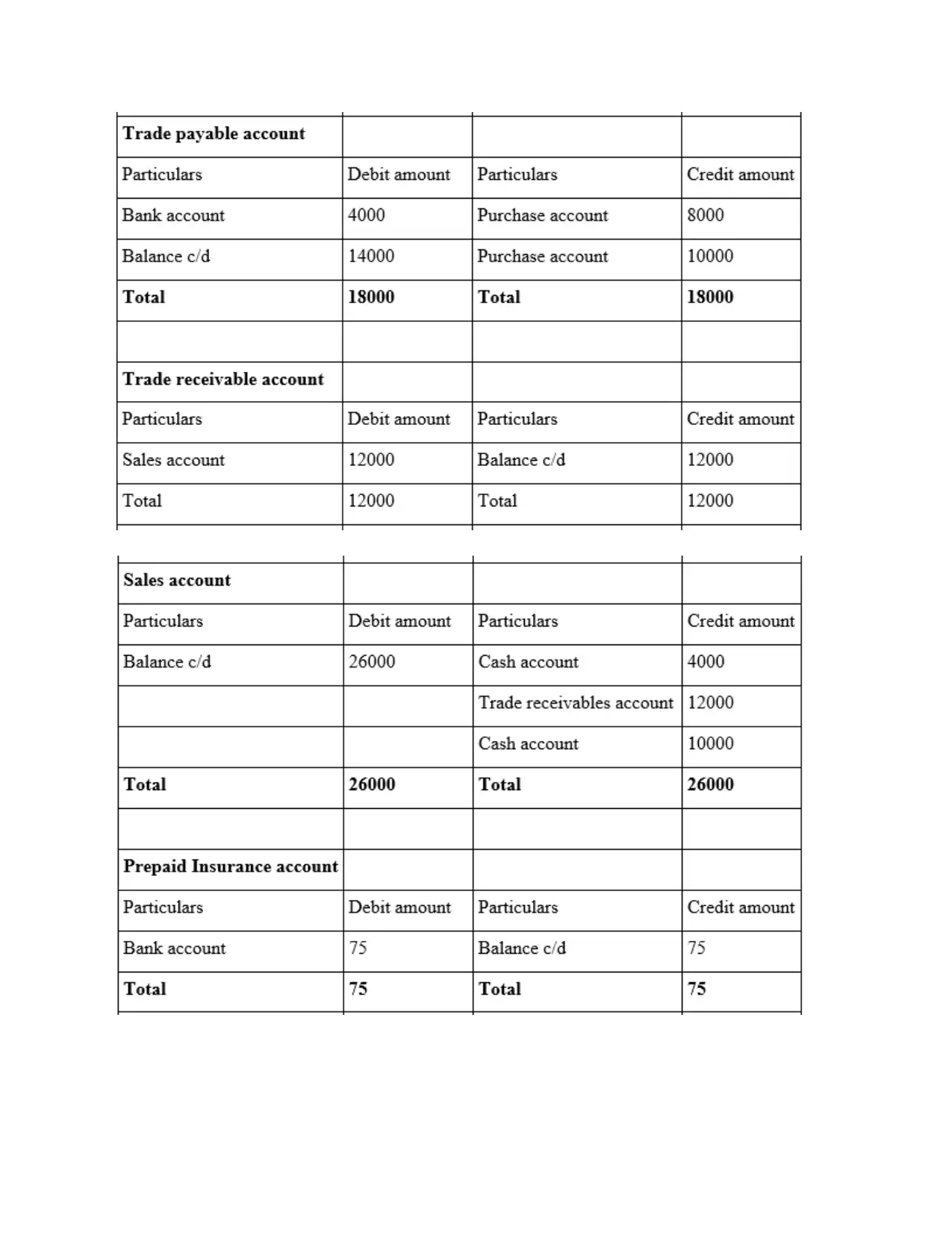

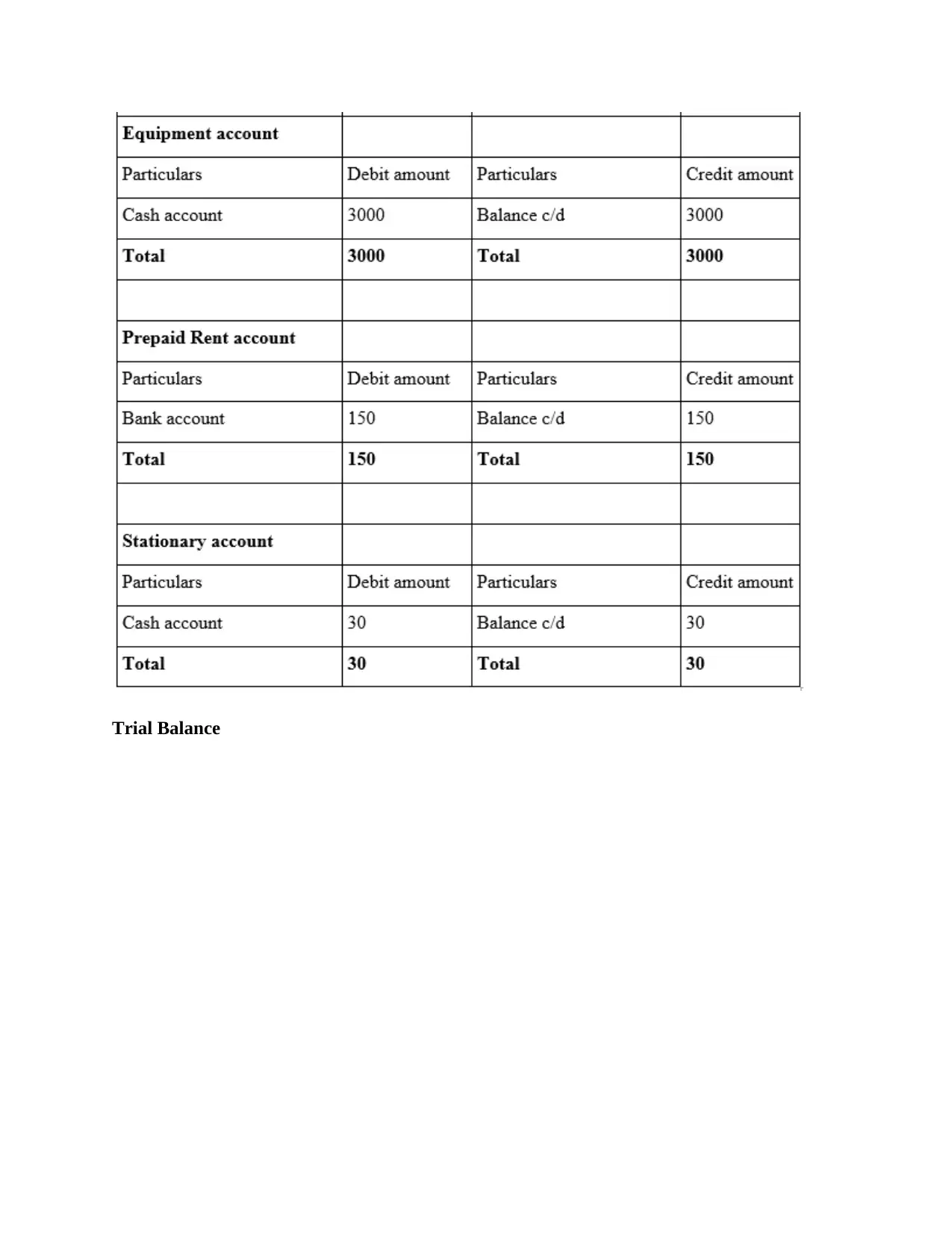

Ledger accounts

To sales a/c

12000

12000

16/06/16 Purchase a/c DR

To accounts payable a/c

10000

10000

18/06/16 Computer equipment a/c DR

To cash a/c

3000

3000

20/06/16 Rent a/c DR

To bank a/c

150

150

21/06/16 Cash a/c DR

To sales a/c

10000

10000

25/06/16 Cash in hand

To bank a/c

100

100

30/06/16 Stationary a/c DR

To cash in hand a/c

30

30

Ledger accounts

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

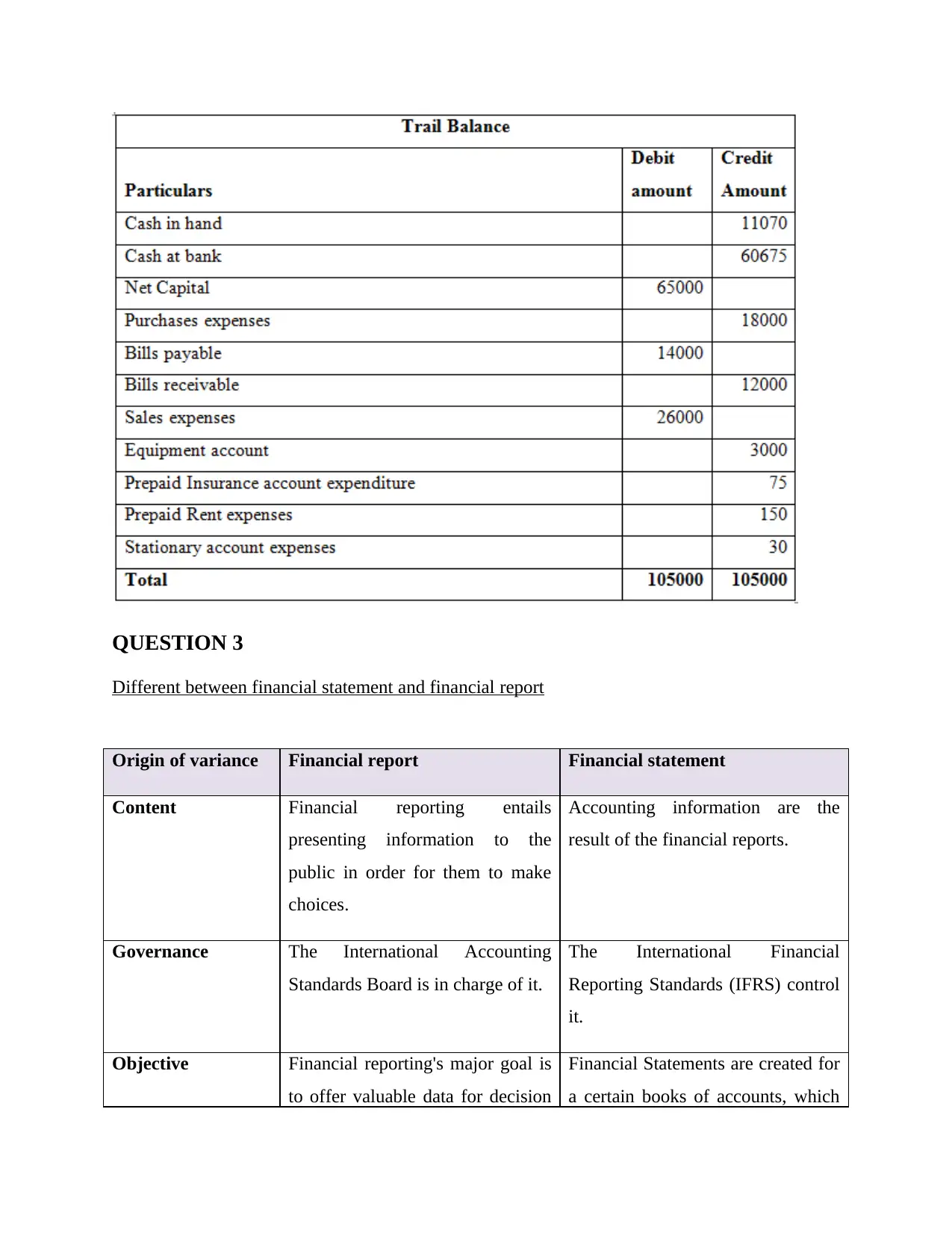

Trial Balance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

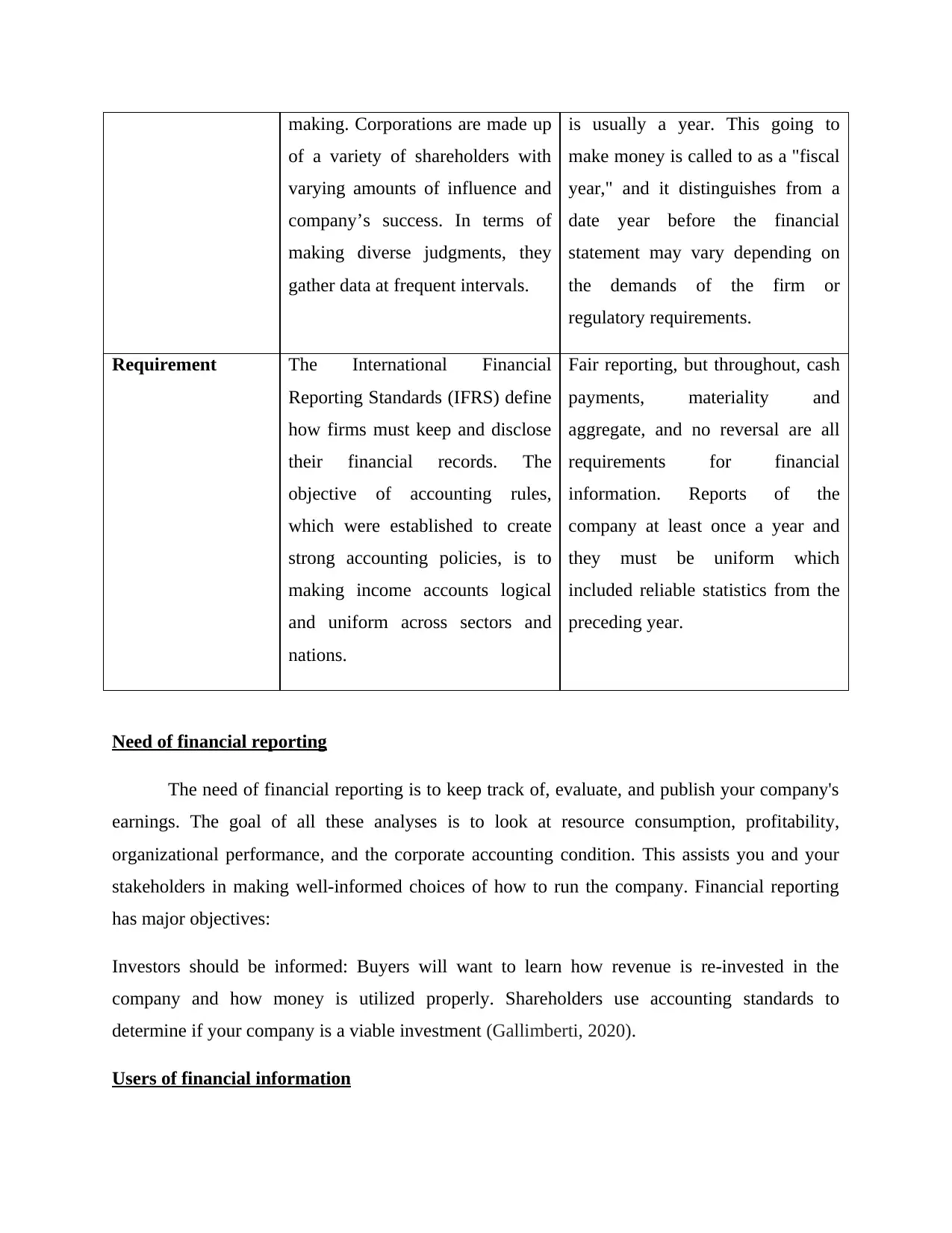

QUESTION 3

Different between financial statement and financial report

Origin of variance Financial report Financial statement

Content Financial reporting entails

presenting information to the

public in order for them to make

choices.

Accounting information are the

result of the financial reports.

Governance The International Accounting

Standards Board is in charge of it.

The International Financial

Reporting Standards (IFRS) control

it.

Objective Financial reporting's major goal is

to offer valuable data for decision

Financial Statements are created for

a certain books of accounts, which

Different between financial statement and financial report

Origin of variance Financial report Financial statement

Content Financial reporting entails

presenting information to the

public in order for them to make

choices.

Accounting information are the

result of the financial reports.

Governance The International Accounting

Standards Board is in charge of it.

The International Financial

Reporting Standards (IFRS) control

it.

Objective Financial reporting's major goal is

to offer valuable data for decision

Financial Statements are created for

a certain books of accounts, which

making. Corporations are made up

of a variety of shareholders with

varying amounts of influence and

company’s success. In terms of

making diverse judgments, they

gather data at frequent intervals.

is usually a year. This going to

make money is called to as a "fiscal

year," and it distinguishes from a

date year before the financial

statement may vary depending on

the demands of the firm or

regulatory requirements.

Requirement The International Financial

Reporting Standards (IFRS) define

how firms must keep and disclose

their financial records. The

objective of accounting rules,

which were established to create

strong accounting policies, is to

making income accounts logical

and uniform across sectors and

nations.

Fair reporting, but throughout, cash

payments, materiality and

aggregate, and no reversal are all

requirements for financial

information. Reports of the

company at least once a year and

they must be uniform which

included reliable statistics from the

preceding year.

Need of financial reporting

The need of financial reporting is to keep track of, evaluate, and publish your company's

earnings. The goal of all these analyses is to look at resource consumption, profitability,

organizational performance, and the corporate accounting condition. This assists you and your

stakeholders in making well-informed choices of how to run the company. Financial reporting

has major objectives:

Investors should be informed: Buyers will want to learn how revenue is re-invested in the

company and how money is utilized properly. Shareholders use accounting standards to

determine if your company is a viable investment (Gallimberti, 2020).

Users of financial information

of a variety of shareholders with

varying amounts of influence and

company’s success. In terms of

making diverse judgments, they

gather data at frequent intervals.

is usually a year. This going to

make money is called to as a "fiscal

year," and it distinguishes from a

date year before the financial

statement may vary depending on

the demands of the firm or

regulatory requirements.

Requirement The International Financial

Reporting Standards (IFRS) define

how firms must keep and disclose

their financial records. The

objective of accounting rules,

which were established to create

strong accounting policies, is to

making income accounts logical

and uniform across sectors and

nations.

Fair reporting, but throughout, cash

payments, materiality and

aggregate, and no reversal are all

requirements for financial

information. Reports of the

company at least once a year and

they must be uniform which

included reliable statistics from the

preceding year.

Need of financial reporting

The need of financial reporting is to keep track of, evaluate, and publish your company's

earnings. The goal of all these analyses is to look at resource consumption, profitability,

organizational performance, and the corporate accounting condition. This assists you and your

stakeholders in making well-informed choices of how to run the company. Financial reporting

has major objectives:

Investors should be informed: Buyers will want to learn how revenue is re-invested in the

company and how money is utilized properly. Shareholders use accounting standards to

determine if your company is a viable investment (Gallimberti, 2020).

Users of financial information

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.