Financial Accounting Homework: Scenario Analysis and Principles

VerifiedAdded on 2023/01/10

|25

|4609

|89

Homework Assignment

AI Summary

This assignment solution covers key concepts in financial accounting, addressing two scenarios. Scenario 1 explores business transactions, including single and double-entry systems, journal entries, ledger accounts, trial balances, and the differences between financial statements and reports, alongside fundamental accounting principles. Scenario 2 delves into Bank Reconciliation Statements (BRS), control accounts, suspense accounts, and the distinctions between various banking transactions like standing orders and direct debits. The solution provides detailed explanations, journal entries, and analyses to enhance understanding of these core accounting principles and practices.

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Scenario 1.........................................................................................................................................4

Question 1........................................................................................................................................4

Stating different kinds of business transaction along with explaining single and double entry.

Explaining the term trial balance and its significance............................................................4

Question 2........................................................................................................................................5

1. Journal entry.......................................................................................................................5

2. Ledger accounts..................................................................................................................6

3. Trial balance.......................................................................................................................9

Question 3......................................................................................................................................10

Explaining difference between the financial statement and the report and stating the reason for

which this report are required by different users..................................................................10

Question 4......................................................................................................................................11

Explaining the fundamental principles of the accounting....................................................11

Question 5......................................................................................................................................14

Scenario 2.......................................................................................................................................16

Question 1......................................................................................................................................16

Explaining the meaning of BRS and the reason behind preparing the BRS along with its

format and importance..........................................................................................................16

Question 2......................................................................................................................................17

Explaining the meaning of control accounts and role of the control accounts in FM..........17

Question 3......................................................................................................................................18

Explaining the meaning of suspense account and the reason behind drafting suspense accounts

..............................................................................................................................................18

Question 4......................................................................................................................................19

a. Explaining the difference between standing order, direct debit, bank charges and Dishonor

of cheque..............................................................................................................................20

Question 5......................................................................................................................................21

a............................................................................................................................................21

b............................................................................................................................................23

Scenario 1.........................................................................................................................................4

Question 1........................................................................................................................................4

Stating different kinds of business transaction along with explaining single and double entry.

Explaining the term trial balance and its significance............................................................4

Question 2........................................................................................................................................5

1. Journal entry.......................................................................................................................5

2. Ledger accounts..................................................................................................................6

3. Trial balance.......................................................................................................................9

Question 3......................................................................................................................................10

Explaining difference between the financial statement and the report and stating the reason for

which this report are required by different users..................................................................10

Question 4......................................................................................................................................11

Explaining the fundamental principles of the accounting....................................................11

Question 5......................................................................................................................................14

Scenario 2.......................................................................................................................................16

Question 1......................................................................................................................................16

Explaining the meaning of BRS and the reason behind preparing the BRS along with its

format and importance..........................................................................................................16

Question 2......................................................................................................................................17

Explaining the meaning of control accounts and role of the control accounts in FM..........17

Question 3......................................................................................................................................18

Explaining the meaning of suspense account and the reason behind drafting suspense accounts

..............................................................................................................................................18

Question 4......................................................................................................................................19

a. Explaining the difference between standing order, direct debit, bank charges and Dishonor

of cheque..............................................................................................................................20

Question 5......................................................................................................................................21

a............................................................................................................................................21

b............................................................................................................................................23

REFERENCES..............................................................................................................................24

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Scenario 1

Question 1

Stating different kinds of business transaction along with explaining single and double entry.

Explaining the term trial balance and its significance

Types of business transactions

Purchase of materials and goods: It refers to the procedure which is involved in a

purchase of material of goods in which owner has to approve the invoices and verify the

goods received as per the requirement or not.

Purchasing non-current assets: It means that the assets which are use longer than a year

and owner is not see the complete value in the current accounting year.

Paying wages and salaries: In this, business transaction types, company have to pay

salary at monthly basis to the define employees.

Sales: It means that the amount which company get while sell the product and services to

their customers with an aim to increase the financial performance of a company.

Single entry- Under this system each and every accounting transaction with single entry

is recorded and centred on results of business which are reported in income statement. This type

is quite simply and that is why, anyone can maintain this system easily if the person do not have

enough knowledge with regards to the same. But under this, limited account are to be opened and

all the transaction are related to personal accounts not the real and nominal accounts.

Double entry- It means that for each transaction, amount need to be recorded in

minimum of the two accounts (Sunarya, Nurhaeni and Haris, 2017). It also requires that for all

the transactions, an amount entered as the debit must equate to amount entered as credit.

Through this entry system, both personal as well as impersonal accounts are maintained and

these are recorded as well because it helps to minimize frauds and error can be checked and

rectified easily. Moreover, it is also assist to make sure the arithmetical accuracy of a books of

account in order to reduce the chances of error and generate the exact outcome.

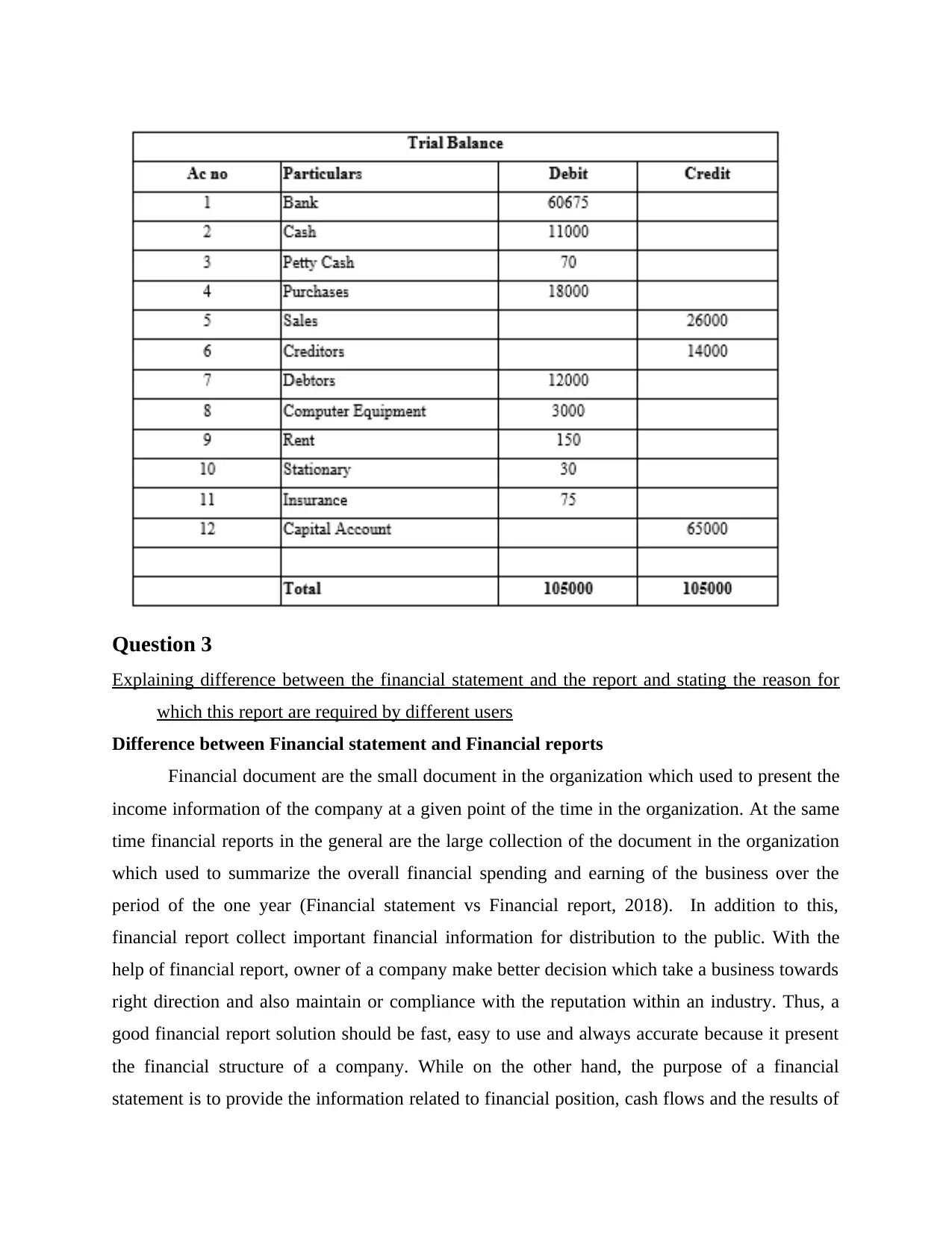

Trial balance- It is the statement that shows credits and debits in double entry books of

account with any of the disagreement reflecting an error. The purpose is to ensure that all entries

made into an entity's general ledger are properly been balanced. Further, the trial balance is also

used to prove that the value of all the debit values balance is equal to the credit balance column

and if not, then it shows the error between the nominal ledger account as well.

Question 1

Stating different kinds of business transaction along with explaining single and double entry.

Explaining the term trial balance and its significance

Types of business transactions

Purchase of materials and goods: It refers to the procedure which is involved in a

purchase of material of goods in which owner has to approve the invoices and verify the

goods received as per the requirement or not.

Purchasing non-current assets: It means that the assets which are use longer than a year

and owner is not see the complete value in the current accounting year.

Paying wages and salaries: In this, business transaction types, company have to pay

salary at monthly basis to the define employees.

Sales: It means that the amount which company get while sell the product and services to

their customers with an aim to increase the financial performance of a company.

Single entry- Under this system each and every accounting transaction with single entry

is recorded and centred on results of business which are reported in income statement. This type

is quite simply and that is why, anyone can maintain this system easily if the person do not have

enough knowledge with regards to the same. But under this, limited account are to be opened and

all the transaction are related to personal accounts not the real and nominal accounts.

Double entry- It means that for each transaction, amount need to be recorded in

minimum of the two accounts (Sunarya, Nurhaeni and Haris, 2017). It also requires that for all

the transactions, an amount entered as the debit must equate to amount entered as credit.

Through this entry system, both personal as well as impersonal accounts are maintained and

these are recorded as well because it helps to minimize frauds and error can be checked and

rectified easily. Moreover, it is also assist to make sure the arithmetical accuracy of a books of

account in order to reduce the chances of error and generate the exact outcome.

Trial balance- It is the statement that shows credits and debits in double entry books of

account with any of the disagreement reflecting an error. The purpose is to ensure that all entries

made into an entity's general ledger are properly been balanced. Further, the trial balance is also

used to prove that the value of all the debit values balance is equal to the credit balance column

and if not, then it shows the error between the nominal ledger account as well.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

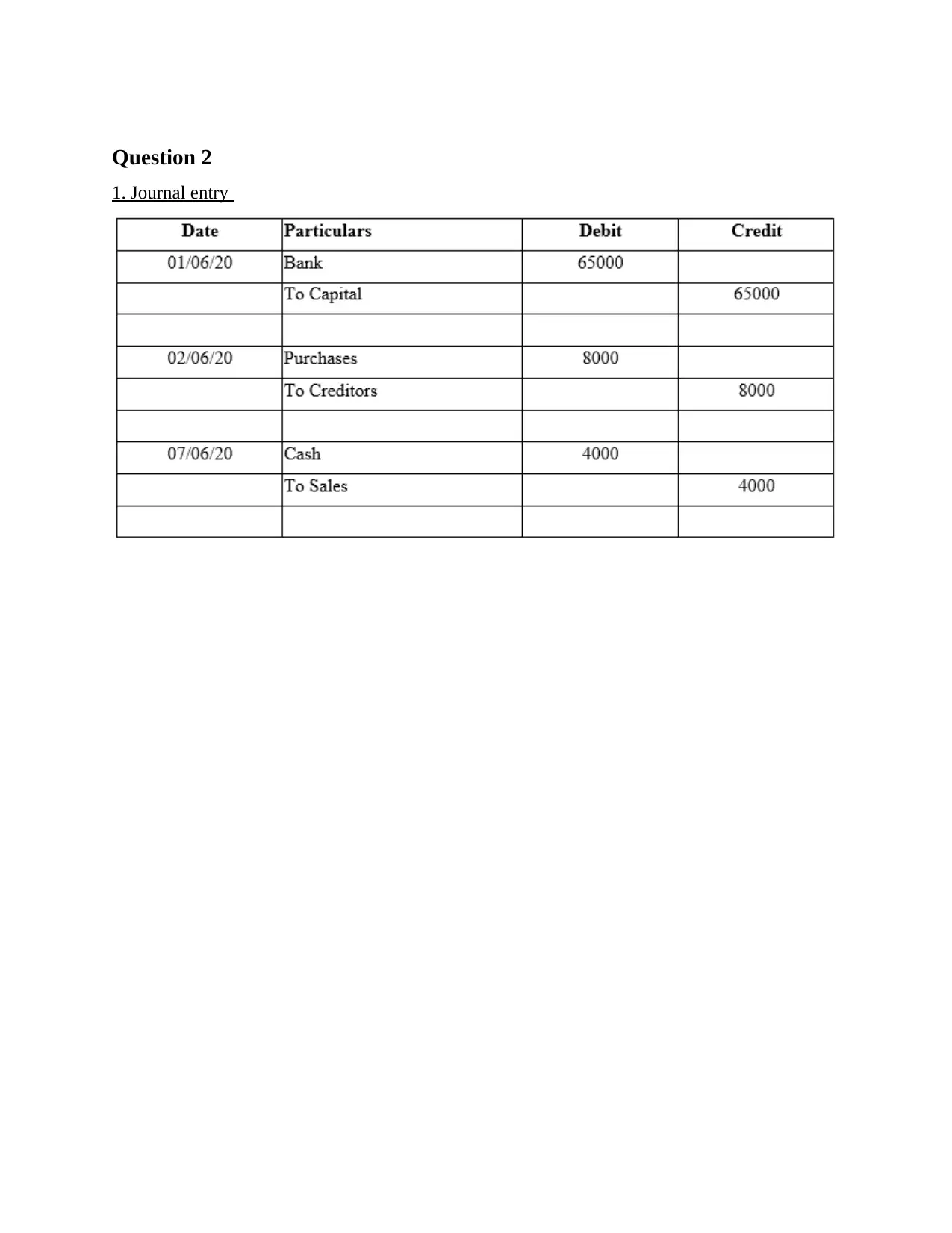

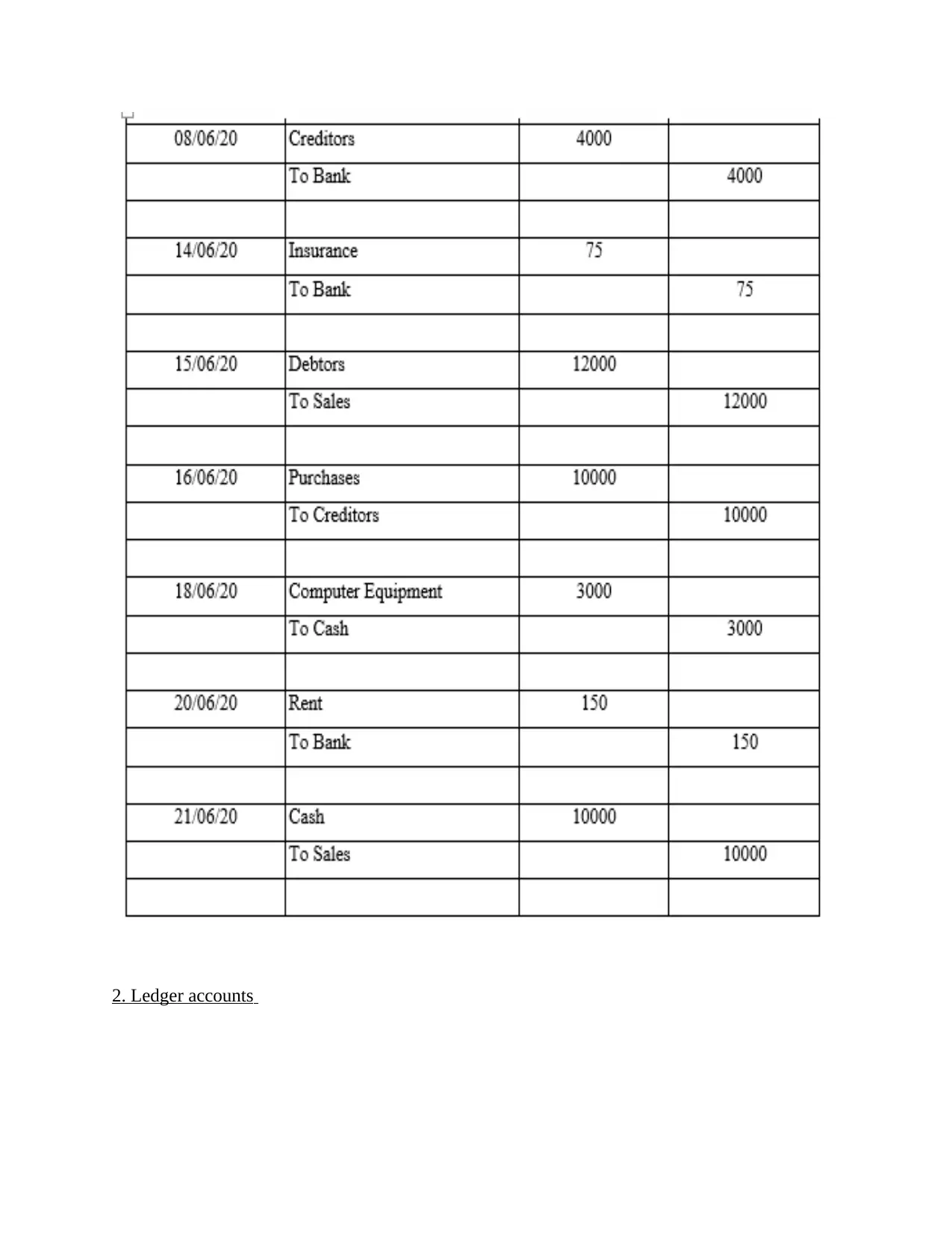

Question 2

1. Journal entry

1. Journal entry

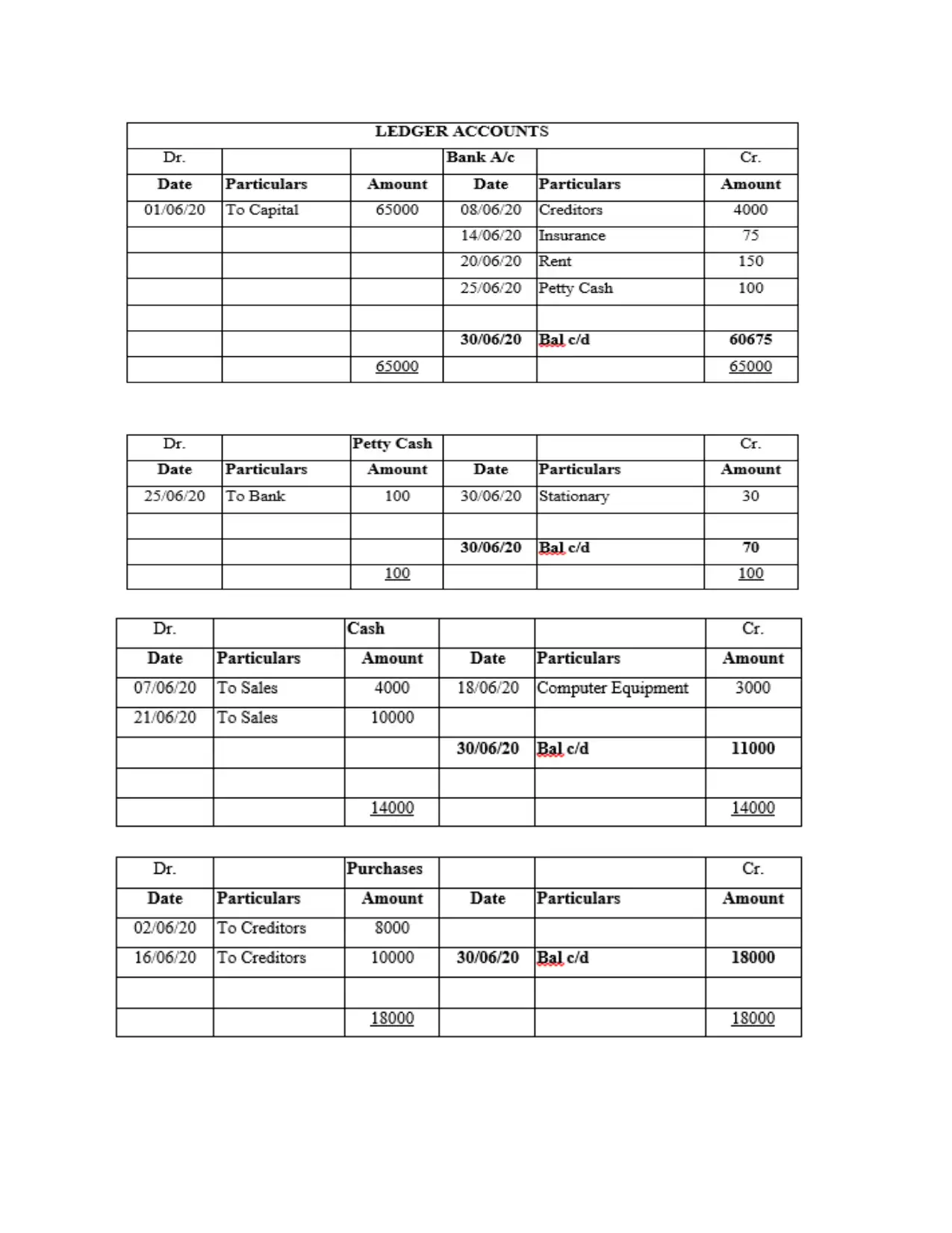

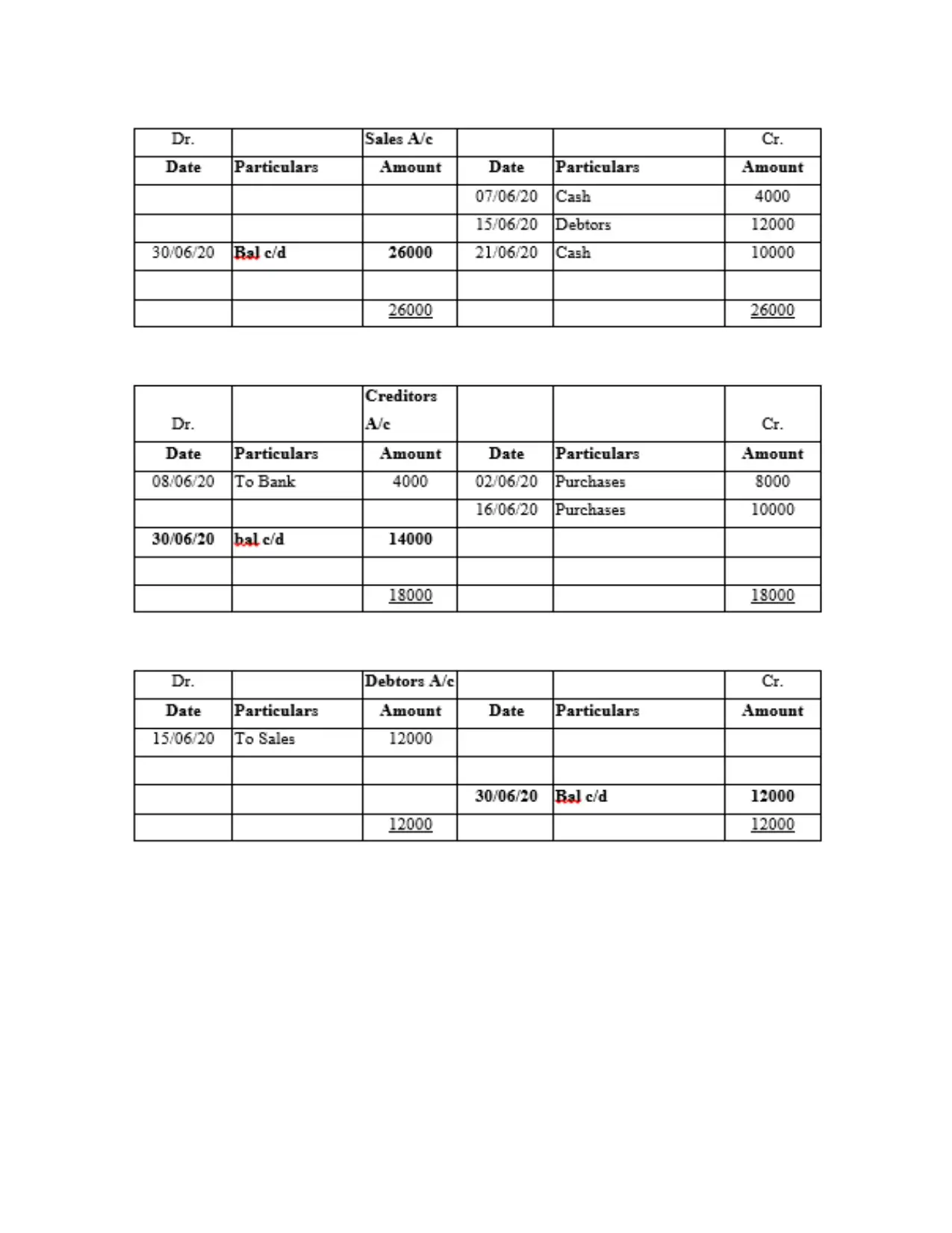

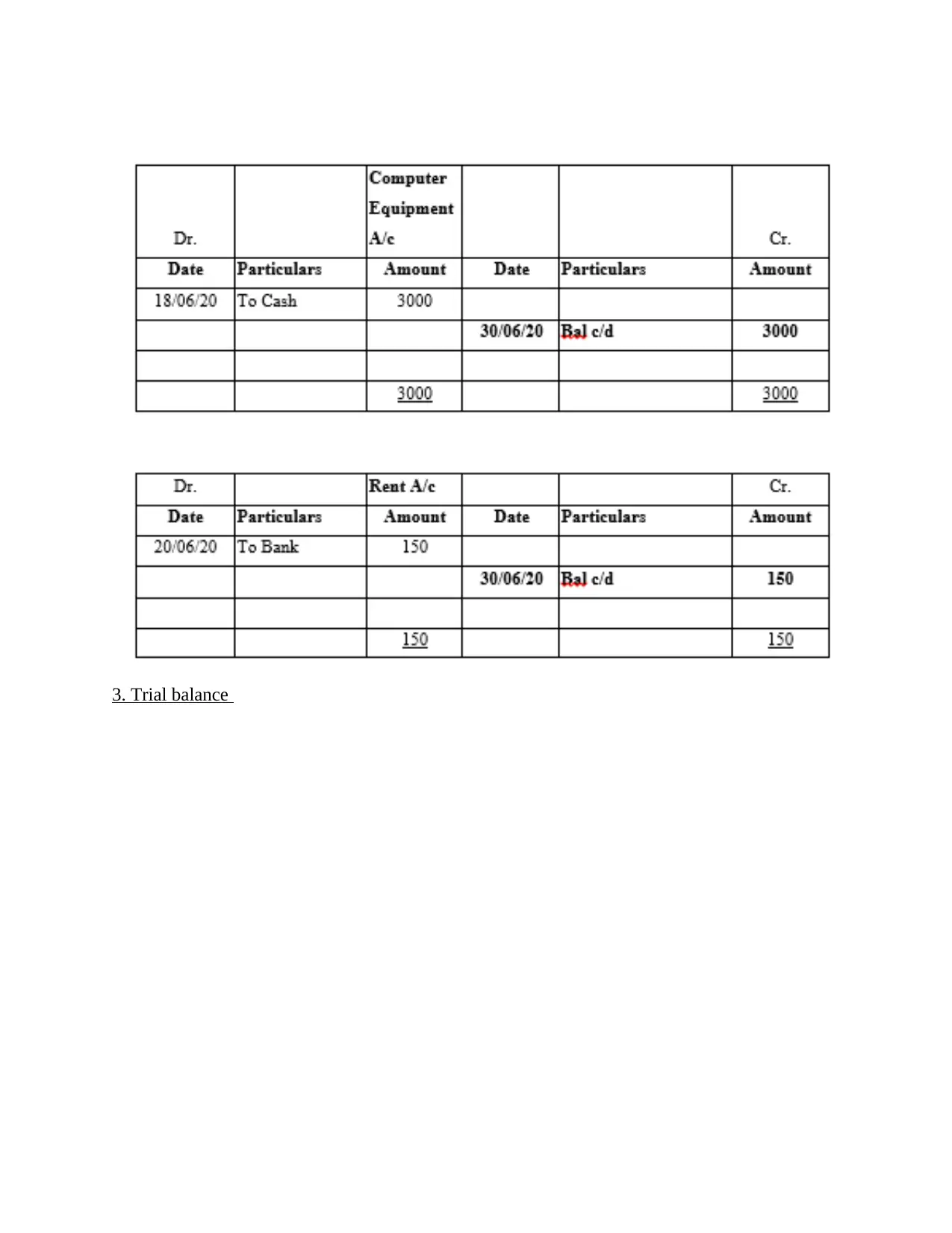

2. Ledger accounts

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3. Trial balance

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Question 3

Explaining difference between the financial statement and the report and stating the reason for

which this report are required by different users

Difference between Financial statement and Financial reports

Financial document are the small document in the organization which used to present the

income information of the company at a given point of the time in the organization. At the same

time financial reports in the general are the large collection of the document in the organization

which used to summarize the overall financial spending and earning of the business over the

period of the one year (Financial statement vs Financial report, 2018). In addition to this,

financial report collect important financial information for distribution to the public. With the

help of financial report, owner of a company make better decision which take a business towards

right direction and also maintain or compliance with the reputation within an industry. Thus, a

good financial report solution should be fast, easy to use and always accurate because it present

the financial structure of a company. While on the other hand, the purpose of a financial

statement is to provide the information related to financial position, cash flows and the results of

Explaining difference between the financial statement and the report and stating the reason for

which this report are required by different users

Difference between Financial statement and Financial reports

Financial document are the small document in the organization which used to present the

income information of the company at a given point of the time in the organization. At the same

time financial reports in the general are the large collection of the document in the organization

which used to summarize the overall financial spending and earning of the business over the

period of the one year (Financial statement vs Financial report, 2018). In addition to this,

financial report collect important financial information for distribution to the public. With the

help of financial report, owner of a company make better decision which take a business towards

right direction and also maintain or compliance with the reputation within an industry. Thus, a

good financial report solution should be fast, easy to use and always accurate because it present

the financial structure of a company. While on the other hand, the purpose of a financial

statement is to provide the information related to financial position, cash flows and the results of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

business operations. Beside this, with the help of financial statement, company make decision

regarding allocation of resources.

A financial statement in the organization used to show the current balance sheet of the

company with regard to the income of the company change in the worth or the value of the

company by looking at the income. Also, it is used to report on current status of a business and it

also estimate the things such as liquidity, debt position as well as funding of a company. The

cash flow statement of the company which used to highlight the flow or the route which is

flowing funds in the organization. Moreover, this statement is used to show the nature of cash

receipts and disbursement as well. Even cash flows do not match revenue and expenses which

was earlier shown in the income statement chart which is another useful financial statement. Last

is income statement which informs capability of a business in order to generate profit and also

determine the volume of sales and nature of various expenses as well. Overall, this is used to

determine or analyze trend within a business and make decision accordingly.

At the same time the financial report of the company used to combine the earning of the

company statement with the over all look of the net worth of the company in the context of the

different expenses and spending which is done by the company, also used to show all the thing

with a great detail with the help of evidence of different reports. Evidence document can be any

formal statement made by the management of the company in the long run such as the letter of

the CEO or the owner in the organization or can be any short prediction plan which is targeted to

increase the profit or the worth value of the company in the long run.

A financial statement of the company do not include the information in regards of the

expenses or the purchase of the item in the organization. This is not the case in the Financial

report as financial report used to show the different type of the expenses occur and different sort

of purchases which has been done in the year (YE, XU and FENG, 2016). So it is stated that the

three most common financial statement which include income statement, balance sheet,

statement of cash flows. Each statement have their own importance and that is why, there is a

need to have both the document within the report in order to make better decision.

Question 4

Explaining the fundamental principles of the accounting

Accounting principles refers to the guidelines that is been issued by IFRS and GAAP which

needs to be followed by all the organization in order to function diligently. Thus, GAAP is also

regarding allocation of resources.

A financial statement in the organization used to show the current balance sheet of the

company with regard to the income of the company change in the worth or the value of the

company by looking at the income. Also, it is used to report on current status of a business and it

also estimate the things such as liquidity, debt position as well as funding of a company. The

cash flow statement of the company which used to highlight the flow or the route which is

flowing funds in the organization. Moreover, this statement is used to show the nature of cash

receipts and disbursement as well. Even cash flows do not match revenue and expenses which

was earlier shown in the income statement chart which is another useful financial statement. Last

is income statement which informs capability of a business in order to generate profit and also

determine the volume of sales and nature of various expenses as well. Overall, this is used to

determine or analyze trend within a business and make decision accordingly.

At the same time the financial report of the company used to combine the earning of the

company statement with the over all look of the net worth of the company in the context of the

different expenses and spending which is done by the company, also used to show all the thing

with a great detail with the help of evidence of different reports. Evidence document can be any

formal statement made by the management of the company in the long run such as the letter of

the CEO or the owner in the organization or can be any short prediction plan which is targeted to

increase the profit or the worth value of the company in the long run.

A financial statement of the company do not include the information in regards of the

expenses or the purchase of the item in the organization. This is not the case in the Financial

report as financial report used to show the different type of the expenses occur and different sort

of purchases which has been done in the year (YE, XU and FENG, 2016). So it is stated that the

three most common financial statement which include income statement, balance sheet,

statement of cash flows. Each statement have their own importance and that is why, there is a

need to have both the document within the report in order to make better decision.

Question 4

Explaining the fundamental principles of the accounting

Accounting principles refers to the guidelines that is been issued by IFRS and GAAP which

needs to be followed by all the organization in order to function diligently. Thus, GAAP is also

required for all the publicly traded companies and it is also implemented by non- publically

traded companies as well. There are various fundamental principles of accounting that are as

follows-

Monetary unit- Accounting require all the values that needs to be recorded in terms of the

single monetary units. It could not account for the goods such as barter system and relates to

assigning values to the items and the goods, therefore, it becomes as the problem since it is

counted as subjective (Gilfriche and et.al., 2018). On the other side, accounting has the

prescribed rules in dealing with the same. Under this principle, it is stated that business

transaction should be recorded only when they can be expressed in the term of a currency or else,

when it is non- quantifiable then it did not recorded within a business financial accounts. Thus, it

is analysed that it is generally accepted accounting principle under which a firm report their

financial position to the shareholder and it is also done in accordance with the transaction which

are expressed in better manner. Hence it is analysed that these principle will help to make

decision better and also reflect the correct financial position too.

Going concern principle- It states that the company is seen to have eternal existence

which means that once it is been formed, only manner for ending it is by the dissolution. It does

not die with a natural death as the human do. Hence, accountants assumes the principle of going

concern which implies that an entity would continue for doing the business as usual till end of

another accounting period and that there is not any information to contrary. This principle

reflects that an entity function on the credit, account for the accounts receivables and the

payables that intend in paying or receiving in future & charging depreciation by assuming that an

equipment would be used for several years.

Conservatism principle- Accountants are seen as very conservative by its nature, and so

they desire to hope for best and prepared for worst. It is been displayed in rules that they had

created for their own profession. One of central tenets of an accounting is the conservatism

principle which depicts that when there is any doubt about an amount of an expected outflow &

inflows, an organization must state for lowest possible sales and highest chances of cost (Dignath

and et.al., 2019). In fact, it could be seen that an accountant values inventory at the lower cost or

the market price . On the other side, it helps an entity in getting prepared for any type of

uncertainty or financial crises in the future.

traded companies as well. There are various fundamental principles of accounting that are as

follows-

Monetary unit- Accounting require all the values that needs to be recorded in terms of the

single monetary units. It could not account for the goods such as barter system and relates to

assigning values to the items and the goods, therefore, it becomes as the problem since it is

counted as subjective (Gilfriche and et.al., 2018). On the other side, accounting has the

prescribed rules in dealing with the same. Under this principle, it is stated that business

transaction should be recorded only when they can be expressed in the term of a currency or else,

when it is non- quantifiable then it did not recorded within a business financial accounts. Thus, it

is analysed that it is generally accepted accounting principle under which a firm report their

financial position to the shareholder and it is also done in accordance with the transaction which

are expressed in better manner. Hence it is analysed that these principle will help to make

decision better and also reflect the correct financial position too.

Going concern principle- It states that the company is seen to have eternal existence

which means that once it is been formed, only manner for ending it is by the dissolution. It does

not die with a natural death as the human do. Hence, accountants assumes the principle of going

concern which implies that an entity would continue for doing the business as usual till end of

another accounting period and that there is not any information to contrary. This principle

reflects that an entity function on the credit, account for the accounts receivables and the

payables that intend in paying or receiving in future & charging depreciation by assuming that an

equipment would be used for several years.

Conservatism principle- Accountants are seen as very conservative by its nature, and so

they desire to hope for best and prepared for worst. It is been displayed in rules that they had

created for their own profession. One of central tenets of an accounting is the conservatism

principle which depicts that when there is any doubt about an amount of an expected outflow &

inflows, an organization must state for lowest possible sales and highest chances of cost (Dignath

and et.al., 2019). In fact, it could be seen that an accountant values inventory at the lower cost or

the market price . On the other side, it helps an entity in getting prepared for any type of

uncertainty or financial crises in the future.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.