ACCG2024 Financial Accounting: Impairment Testing Report Analysis

VerifiedAdded on 2022/09/06

|12

|1834

|22

Report

AI Summary

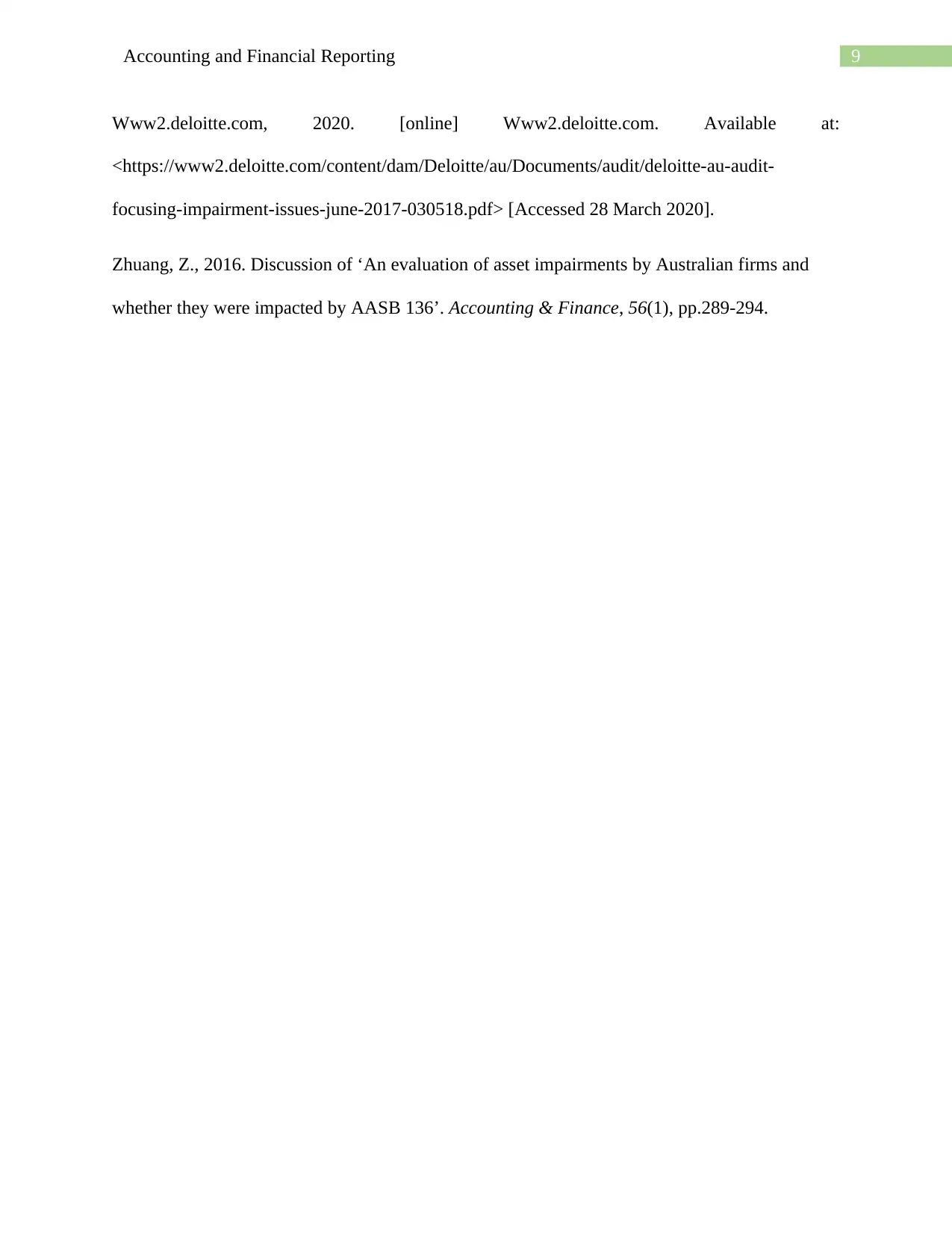

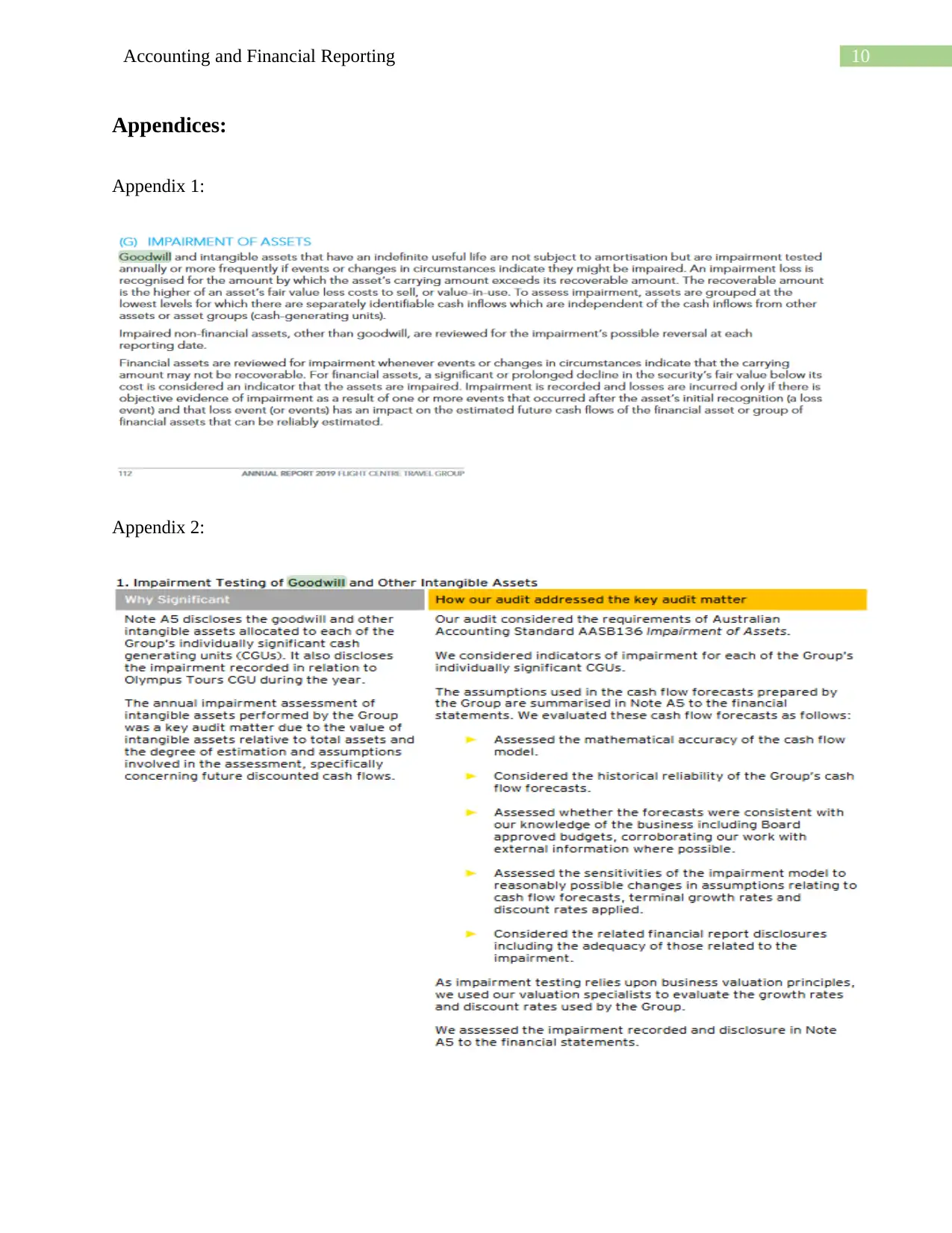

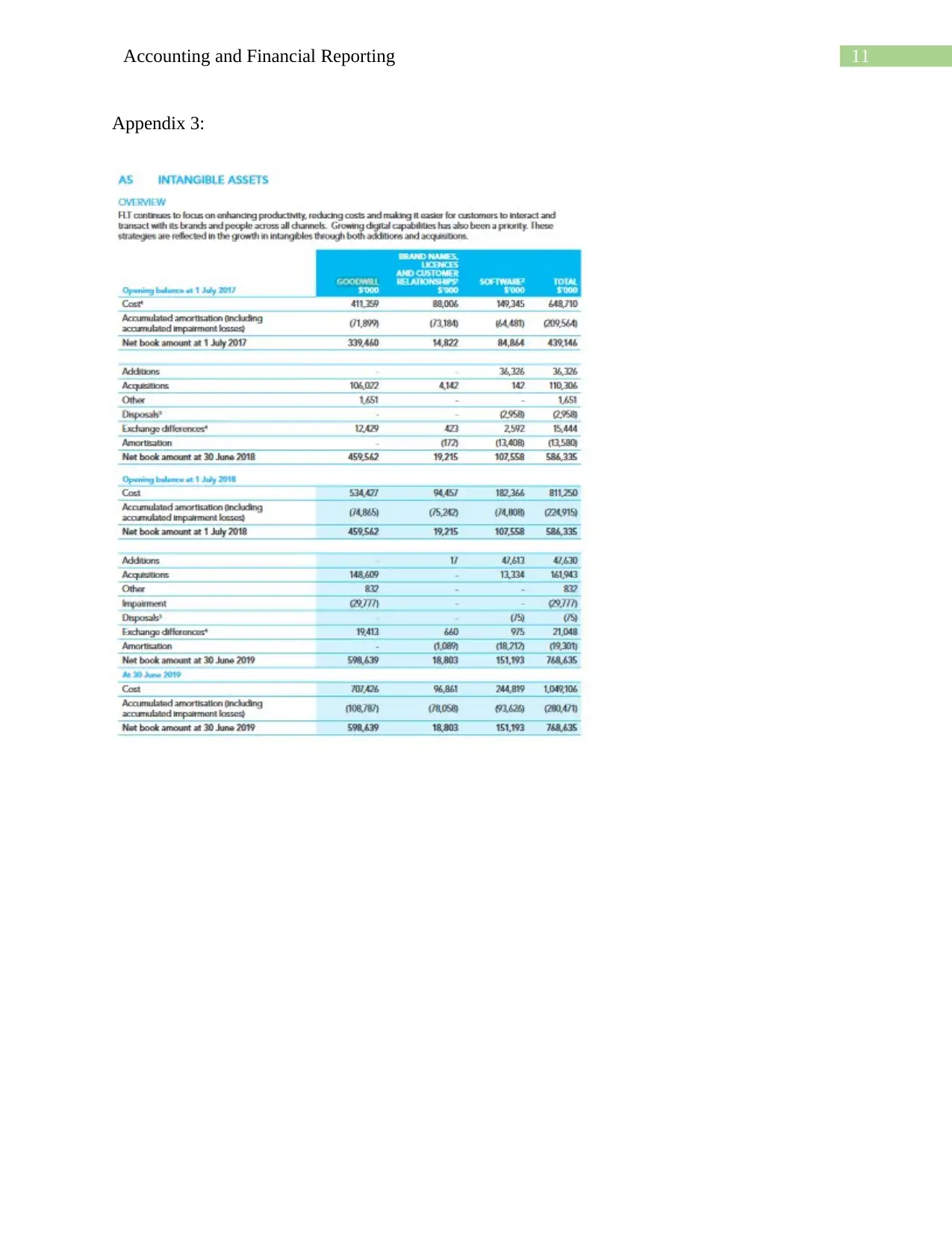

This report examines the crucial aspects of impairment testing for non-financial assets, with a focus on the Australian Accounting Standards Board (AASB) 136 guidelines. The analysis centers on Flight Centre Travel Group (FLT), an ASX-listed company, evaluating its adherence to AASB 136 in disclosing impairment losses related to goodwill and intangible assets. The report details the disclosure requirements under AASB 136, including the valuation techniques and fair value hierarchy used. It assesses FLT's compliance with these requirements, highlighting the company's handling of goodwill and intangible assets in its financial statements. Furthermore, the report identifies critical issues in impairment testing, such as the identification of cash-generating units, the selection of assumptions, and the importance of transparent disclosures. The report concludes by emphasizing key considerations for directors when reviewing impairment calculations, such as proper reconciliation, transparency, accurate identification of cash-generating units, and the careful selection of assumptions. The report uses the annual report of FLT and various sources to analyze the practical implications of impairment testing.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.