Analysis of Financial Accounting Practices: Macquarie Group Report

VerifiedAdded on 2023/01/11

|11

|2879

|33

Report

AI Summary

This report provides a comprehensive analysis of the financial accounting practices of the Macquarie Group, an Australian multinational investment bank. It examines the company's adherence to accounting standards, including AASB and IFRS, and its compliance with the conceptual framework. The report delves into the recognition criteria for assets, liabilities, equity, revenue, and expenses, as well as the qualitative characteristics of financial reporting. It assesses the company's use of historical cost convention, risk management frameworks, and critical accounting estimates. The analysis includes the impact of AASB 9 and AASB 15, the use of both positive and normative accounting theories, and the application of accrual accounting. The report highlights the importance of relevance, faithful representation, and the use of non-financial measures for understanding the company's performance. It concludes with an assessment of how Macquarie Group enhances the qualitative characteristics of its financial reports through comparability, understandability, and verifiability, supported by data and visual representations.

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

This report presents about the financial accounting done by the Macquarie group. It

covers the fundamental accounting theories, standards which are required to be adhered while

preparing the financial report. This report has been focussed on the accounting policies being

followed by the Macquarie group along with the reporting strategies. Based on the findings, it

can be concluded that the Macquarie group has been very effective in complying with all the

relevant accounting standards and frameworks such as AASB 139. It has effectively used

qualitative characteristics for the financial reporting purpose.

This report presents about the financial accounting done by the Macquarie group. It

covers the fundamental accounting theories, standards which are required to be adhered while

preparing the financial report. This report has been focussed on the accounting policies being

followed by the Macquarie group along with the reporting strategies. Based on the findings, it

can be concluded that the Macquarie group has been very effective in complying with all the

relevant accounting standards and frameworks such as AASB 139. It has effectively used

qualitative characteristics for the financial reporting purpose.

TABLE OF CONTENTS

INTRODUCTION......................................................................................................................4

ANALYSIS................................................................................................................................4

Adherence to the objectives of the conceptual framework with its reporting........................4

Adherence with the recognition criteria for reporting assets, liabilities, equity, revenue and

expenses.................................................................................................................................5

Adherence with the qualitative enhancing characteristics of financial reporting..................7

Assessment of satisfaction of enhancing qualitative characteristics of financial report........8

CONCLUSION........................................................................................................................10

REFERENCES.........................................................................................................................11

INTRODUCTION......................................................................................................................4

ANALYSIS................................................................................................................................4

Adherence to the objectives of the conceptual framework with its reporting........................4

Adherence with the recognition criteria for reporting assets, liabilities, equity, revenue and

expenses.................................................................................................................................5

Adherence with the qualitative enhancing characteristics of financial reporting..................7

Assessment of satisfaction of enhancing qualitative characteristics of financial report........8

CONCLUSION........................................................................................................................10

REFERENCES.........................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Macquarie group is an Australian multinational investment bank having offices

globally. The MGL is headquartered in Australia and listed in Australia stock exchange

(ASX). It was founded in 1969. The company has employed over 14000 employees all

across its 30 offices around the world. The group has the total assets of $A203.2 billion and

the total of equity as on 31 march 2019 is $A18.4 billion. The company is the world’s largest

infrastructure asset manager and also it top ranked as the mergers and acquisitions (M&A)

adviser. The MGL group is having two operating groups, which are, Macquarie Asset

Management and Macquarie Capital.

For this report, Macquarie group is selected to critically analyse whether the company

has complied with all the accounting requirements. The report has put emphasis on the

accounting policies of Macquarie group. The core objective of this report is to analyse the

accounting policies and reporting strategies followed by the company. It also includes the

issues which might to suspicious. The theoretical concept of accounting framework includes

two, positive and normative theory. The former states to conduct accounting analysis on

historical data and also conclusion is drawn based on the information present currently in

hand. But the normative theory provides advises to the policy makers with respect to what

should be done which is completely based on the theoretical principles.

ANALYSIS

Adherence to the objectives of the conceptual framework with its reporting

Standards Board (AASB) is responsible for creating financial report for all types of

business entities. The significant contributing role of AASB has been considered with the

“Australian securities and investment commission at 2001”. The AASB is considered as the

basis for preparing the general purpose financial report of Macquarie group (Goodacre, Gaunt

and Henry, 2017). Also, the compliance with the Australian Accounting Standard (AAS)

makes sure that the annual report is prepared in accordance with the International Financial

Reporting Standards (IFRS) which are issued by the IASB (International Accounting

Standards Board). Historical cost convention is the basis of preparation of financial report.

The Board of the group is committed to oversight the performance and risk

management. The group heads of the company is responsible for introducing the risk

management framework to attest the key risk identified. The “Macquarie’s risk management

framework” completely includes its systems, structures, policies and processes and even

Macquarie group is an Australian multinational investment bank having offices

globally. The MGL is headquartered in Australia and listed in Australia stock exchange

(ASX). It was founded in 1969. The company has employed over 14000 employees all

across its 30 offices around the world. The group has the total assets of $A203.2 billion and

the total of equity as on 31 march 2019 is $A18.4 billion. The company is the world’s largest

infrastructure asset manager and also it top ranked as the mergers and acquisitions (M&A)

adviser. The MGL group is having two operating groups, which are, Macquarie Asset

Management and Macquarie Capital.

For this report, Macquarie group is selected to critically analyse whether the company

has complied with all the accounting requirements. The report has put emphasis on the

accounting policies of Macquarie group. The core objective of this report is to analyse the

accounting policies and reporting strategies followed by the company. It also includes the

issues which might to suspicious. The theoretical concept of accounting framework includes

two, positive and normative theory. The former states to conduct accounting analysis on

historical data and also conclusion is drawn based on the information present currently in

hand. But the normative theory provides advises to the policy makers with respect to what

should be done which is completely based on the theoretical principles.

ANALYSIS

Adherence to the objectives of the conceptual framework with its reporting

Standards Board (AASB) is responsible for creating financial report for all types of

business entities. The significant contributing role of AASB has been considered with the

“Australian securities and investment commission at 2001”. The AASB is considered as the

basis for preparing the general purpose financial report of Macquarie group (Goodacre, Gaunt

and Henry, 2017). Also, the compliance with the Australian Accounting Standard (AAS)

makes sure that the annual report is prepared in accordance with the International Financial

Reporting Standards (IFRS) which are issued by the IASB (International Accounting

Standards Board). Historical cost convention is the basis of preparation of financial report.

The Board of the group is committed to oversight the performance and risk

management. The group heads of the company is responsible for introducing the risk

management framework to attest the key risk identified. The “Macquarie’s risk management

framework” completely includes its systems, structures, policies and processes and even

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

people within the group. The Group reviews its risk framework in a regular interval of time

which helps in enhancing its reporting and surveillance activity. It has also introduced

“Conduct Risk Management Framework” which details out the approach of managing the

conduct risk which refers to the risk of behaviour or the actions of the employees. The

preparation of the annual report in accordance with the Australian Accounting Standards

(AAS) requires the company to use certain critical accounting estimates (Cordery and

Sinclair, 2016). It also requires management of Macquarie group to exercise control and

judgement in the process of implementing the accounting policies. The notes attached with

the financial statements makes disclosure of the items which involves a higher degree of

judgement or complexity and also the items where assumptions made are significant.

The Accounting Standards which were not applicable to the current accounting year is

chosen by the organization to not apply it earlier ((Yong, Lim and Tan, 2016)). There are few

amendments and change in policies which is applicable to the organization but has not been

practiced in the current year. “The March 2019, the financial results reflect the adoption of

AASB 9 Financial Instruments (AASB 9) and also AASB 15 Revenue from contracts with

customers (AASB 15) on 1 April 2018. As allowed by AASB 9 and AASB 15, the

Consolidated Entity has not restated previously reported financial periods”. The information

for the financial years ended as on 31 March 2008–2019, the results are based on the

Australian Accounting Standards (AAS) that were adopted and implemented by the

Consolidated Entity of the Macquarie group at the reporting dates. The reporting periods have

also been restated but only to the extent as required by the accounting standards (AS). Along

with that, the financial reporting for past years may not be fully compared with another

because of the changes in accounting standards (AS) requirements.

Adherence with the recognition criteria for reporting assets, liabilities, equity, revenue and

expenses

Most of the time, while recognising assets and liabilities, the deferred income tax is

ignored or not considered. For recognising the assets and liabilities requires the estimated

value of both.

For recognising current liabilities and assets, the fair value has been considered. It is

equal to the carrying value and also the market price is the basis for deriving the fair value of

borrowings. There is no major deviation in the fair value of non-current receivables in respect

to it carrying value. The leased assets are initially recognised at the amount equal to the

which helps in enhancing its reporting and surveillance activity. It has also introduced

“Conduct Risk Management Framework” which details out the approach of managing the

conduct risk which refers to the risk of behaviour or the actions of the employees. The

preparation of the annual report in accordance with the Australian Accounting Standards

(AAS) requires the company to use certain critical accounting estimates (Cordery and

Sinclair, 2016). It also requires management of Macquarie group to exercise control and

judgement in the process of implementing the accounting policies. The notes attached with

the financial statements makes disclosure of the items which involves a higher degree of

judgement or complexity and also the items where assumptions made are significant.

The Accounting Standards which were not applicable to the current accounting year is

chosen by the organization to not apply it earlier ((Yong, Lim and Tan, 2016)). There are few

amendments and change in policies which is applicable to the organization but has not been

practiced in the current year. “The March 2019, the financial results reflect the adoption of

AASB 9 Financial Instruments (AASB 9) and also AASB 15 Revenue from contracts with

customers (AASB 15) on 1 April 2018. As allowed by AASB 9 and AASB 15, the

Consolidated Entity has not restated previously reported financial periods”. The information

for the financial years ended as on 31 March 2008–2019, the results are based on the

Australian Accounting Standards (AAS) that were adopted and implemented by the

Consolidated Entity of the Macquarie group at the reporting dates. The reporting periods have

also been restated but only to the extent as required by the accounting standards (AS). Along

with that, the financial reporting for past years may not be fully compared with another

because of the changes in accounting standards (AS) requirements.

Adherence with the recognition criteria for reporting assets, liabilities, equity, revenue and

expenses

Most of the time, while recognising assets and liabilities, the deferred income tax is

ignored or not considered. For recognising the assets and liabilities requires the estimated

value of both.

For recognising current liabilities and assets, the fair value has been considered. It is

equal to the carrying value and also the market price is the basis for deriving the fair value of

borrowings. There is no major deviation in the fair value of non-current receivables in respect

to it carrying value. The leased assets are initially recognised at the amount equal to the

present value of minimum lease payment or the fair value of leased assets whichever is lower

(Miah, 2017). Also, the recognition of interest in terms of finance cost is done to get a

periodic interest rate. The depreciation on the leased assets is done at the shorter of any of

this, either lease term or useful life of the asset after the initial recognition. The net interest

income is recognised using the EIR method, which is used in calculating the amortised cost

of financial instrument. Along with that, the fees and transaction cost which is an important

part of lending arrangement is shown in the profit or loss statement and is based on the

expected life of the instrument as per the expected interest rate method.

The financial statements have been prepared by the company is based on the positive

accounting theory which focusses on preparing the statements using historical cost.

Additionally, the accrual basis of accounting has been applied for recording some of the

items like accounts receivables and payables (Schroeder and et.al, 2019). Thus, the company

ahs maintained the positive accounting theory for valuing and predicting the value of the

assets at the fair value. The normative theory is also applied for preparing the annual reports

of the company. The significant amount of judgement made by the Macquarie group is in

relation to the valuing the assets and liabilities and income and expenses. It takes into

consideration the historical data along with other factors which can be considered reasonable.

AASB 9 has replaced AASB 139 which aims at addressing the financial liabilities and

asset measurements. Apart from this, expected loss impairment model is being introduced by

AASB 9 which requires the business entities to recognise the expected credit loss at the time

of recognising the assets (MGL 2019 Full year Annual report. 2019). The consolidated

entity’s shareholder’s equity has reduced by $128 million after tax and also the company’s

shareholder’s equity has fall by $20 million. It is expected that this transition will not have a

material impact on the Macquarie group minimum regulatory capital requirements and on its

classification of financial assets and liabilities as well.

AASB 15 has replaced the previous revenue recognition standard in respect to the

contract with customers. Under this standard, it is required to identify the performance

obligation with respect to the contract along with the price allocated to these obligations. The

revenue in this case is recognised only when these obligations are satisfied and this can be

only done when the control of goods and services is moved to the customers.

“The IASB has issued the revised IFRS Conceptual Framework (Framework) for

financial reporting. The Australian equivalent Conceptual Framework has not yet been

(Miah, 2017). Also, the recognition of interest in terms of finance cost is done to get a

periodic interest rate. The depreciation on the leased assets is done at the shorter of any of

this, either lease term or useful life of the asset after the initial recognition. The net interest

income is recognised using the EIR method, which is used in calculating the amortised cost

of financial instrument. Along with that, the fees and transaction cost which is an important

part of lending arrangement is shown in the profit or loss statement and is based on the

expected life of the instrument as per the expected interest rate method.

The financial statements have been prepared by the company is based on the positive

accounting theory which focusses on preparing the statements using historical cost.

Additionally, the accrual basis of accounting has been applied for recording some of the

items like accounts receivables and payables (Schroeder and et.al, 2019). Thus, the company

ahs maintained the positive accounting theory for valuing and predicting the value of the

assets at the fair value. The normative theory is also applied for preparing the annual reports

of the company. The significant amount of judgement made by the Macquarie group is in

relation to the valuing the assets and liabilities and income and expenses. It takes into

consideration the historical data along with other factors which can be considered reasonable.

AASB 9 has replaced AASB 139 which aims at addressing the financial liabilities and

asset measurements. Apart from this, expected loss impairment model is being introduced by

AASB 9 which requires the business entities to recognise the expected credit loss at the time

of recognising the assets (MGL 2019 Full year Annual report. 2019). The consolidated

entity’s shareholder’s equity has reduced by $128 million after tax and also the company’s

shareholder’s equity has fall by $20 million. It is expected that this transition will not have a

material impact on the Macquarie group minimum regulatory capital requirements and on its

classification of financial assets and liabilities as well.

AASB 15 has replaced the previous revenue recognition standard in respect to the

contract with customers. Under this standard, it is required to identify the performance

obligation with respect to the contract along with the price allocated to these obligations. The

revenue in this case is recognised only when these obligations are satisfied and this can be

only done when the control of goods and services is moved to the customers.

“The IASB has issued the revised IFRS Conceptual Framework (Framework) for

financial reporting. The Australian equivalent Conceptual Framework has not yet been

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

issued. The main objective of the Framework is to assist the IASB in developing accounting

standards and assist financial report preparers to develop accounting policies when there is no

specific or similar standard that addresses a particular issue. Amendments include the

definition and recognition criteria for assets, liabilities, income and expenses, and other

relevant financial reporting concepts. The Framework is effective for Macquarie’s annual

reporting periods beginning on 1 April 2020. The Consolidated Entity is currently analysing

the impact of the revised Framework.”

Adherence with the qualitative enhancing characteristics of financial reporting

The key decisions taken by the users is based on the relevance of the financial

information presented in the annual report of the company makes a huge difference. The

faithful and relevant representation is the fundamental characteristics of the useful financial

information. Also, the analysing the structure and content of the organization’s remuneration

report also has a great impact on increasing the relevance of the information presented.

After analysing the annual report of Macquarie group, it can be said that the financial

statements and notes are prepared taking into consideration the Corporation Act 2001 which

involves adherence with the Australian Accounting Standards (Dumay and De Villiers,

2019). It presents the true and fair view of the company’s financial performance and position

as on 31 March 2019. Along with that there is a reasonable ground to believe and trust that

the Macquarie group has the ability to pay off its all debts when it becomes due. Also, it can

be seen in the annual report that the duplicate information has been avoided and the

immaterial disclosure has been disregarded as it may lead to complications. The uncertainties

with regard to certain data has been detected and disclosed specifically.

The Macquarie group has employed certain qualitative measures or non-financial

measures with the objective of measuring the efficiency and effectiveness of the business and

also managing the resource allocation. There were certain barriers in accomplishing the

authentic representation of information and for facing that, requires to acknowledge and

amend the amended standards (Hoque and et.al, 2017). These non-financial factors are very

important for understanding the relevance of disclosure. The users of the financial

information are dependent on both qualitative and quantitative factors as well for taking

better and improved decisions. In regard to this, the auditing of the annual reports of

Macquarie group has been done in accordance with its scope and nature and the qualitative

factors.

standards and assist financial report preparers to develop accounting policies when there is no

specific or similar standard that addresses a particular issue. Amendments include the

definition and recognition criteria for assets, liabilities, income and expenses, and other

relevant financial reporting concepts. The Framework is effective for Macquarie’s annual

reporting periods beginning on 1 April 2020. The Consolidated Entity is currently analysing

the impact of the revised Framework.”

Adherence with the qualitative enhancing characteristics of financial reporting

The key decisions taken by the users is based on the relevance of the financial

information presented in the annual report of the company makes a huge difference. The

faithful and relevant representation is the fundamental characteristics of the useful financial

information. Also, the analysing the structure and content of the organization’s remuneration

report also has a great impact on increasing the relevance of the information presented.

After analysing the annual report of Macquarie group, it can be said that the financial

statements and notes are prepared taking into consideration the Corporation Act 2001 which

involves adherence with the Australian Accounting Standards (Dumay and De Villiers,

2019). It presents the true and fair view of the company’s financial performance and position

as on 31 March 2019. Along with that there is a reasonable ground to believe and trust that

the Macquarie group has the ability to pay off its all debts when it becomes due. Also, it can

be seen in the annual report that the duplicate information has been avoided and the

immaterial disclosure has been disregarded as it may lead to complications. The uncertainties

with regard to certain data has been detected and disclosed specifically.

The Macquarie group has employed certain qualitative measures or non-financial

measures with the objective of measuring the efficiency and effectiveness of the business and

also managing the resource allocation. There were certain barriers in accomplishing the

authentic representation of information and for facing that, requires to acknowledge and

amend the amended standards (Hoque and et.al, 2017). These non-financial factors are very

important for understanding the relevance of disclosure. The users of the financial

information are dependent on both qualitative and quantitative factors as well for taking

better and improved decisions. In regard to this, the auditing of the annual reports of

Macquarie group has been done in accordance with its scope and nature and the qualitative

factors.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Assessment of satisfaction of enhancing qualitative characteristics of financial report

The financial report of organization has been prepared while making sure that the

information is timely, complete and available at minimum cost. The improved comparability

of the financial information, appropriateness, understandability and verifiability all these can

be done by enhancing the qualitative characteristics (Martin-Sardesai and et.al, 2017). The

data provided in the report helps the user in making comparative disclosures that assists in

proper comparison and also assist in taking proper and effective decisions. The company

reviews the operation of the business by comparing its financial data with the previous year.

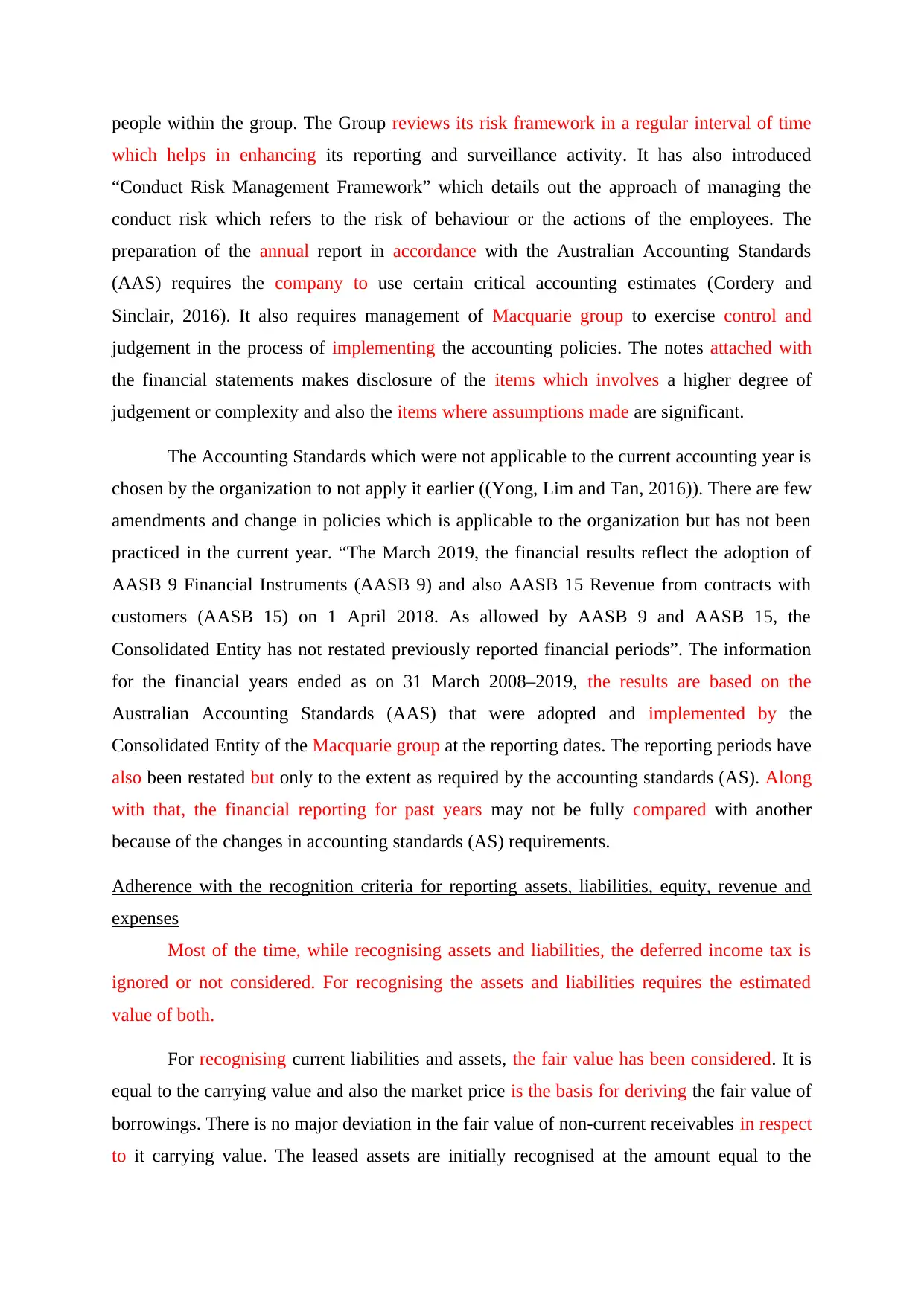

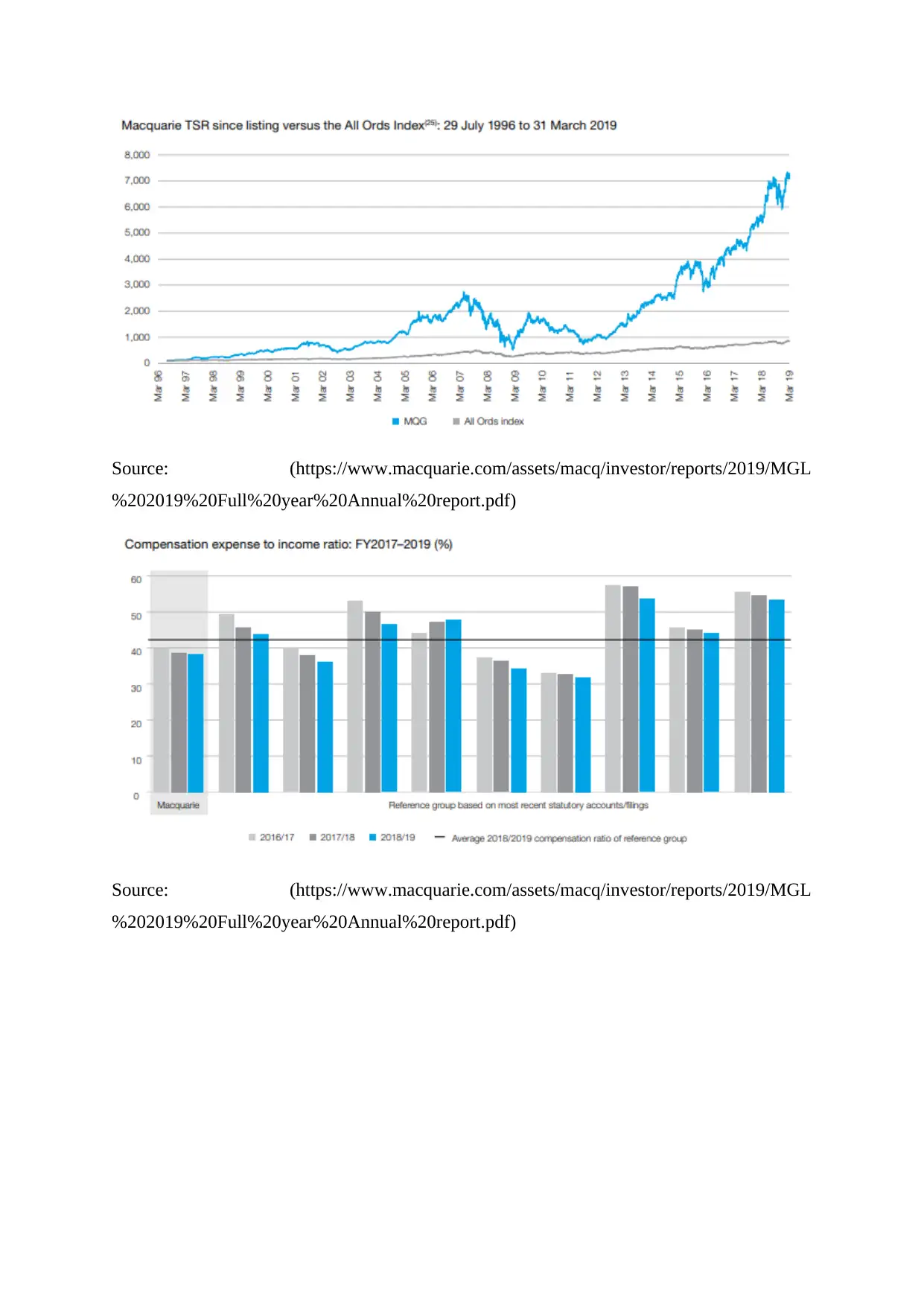

Macquarie group total shareholder return has remained strong over the long term and

has continued its strong performance at both the MSCI World Capital market index and the

All Ordinaries Accumulation since listings. This line chart depicts the clear picture of

enhancing the non-financial factors depicting total shareholder return for Macquarie vs.

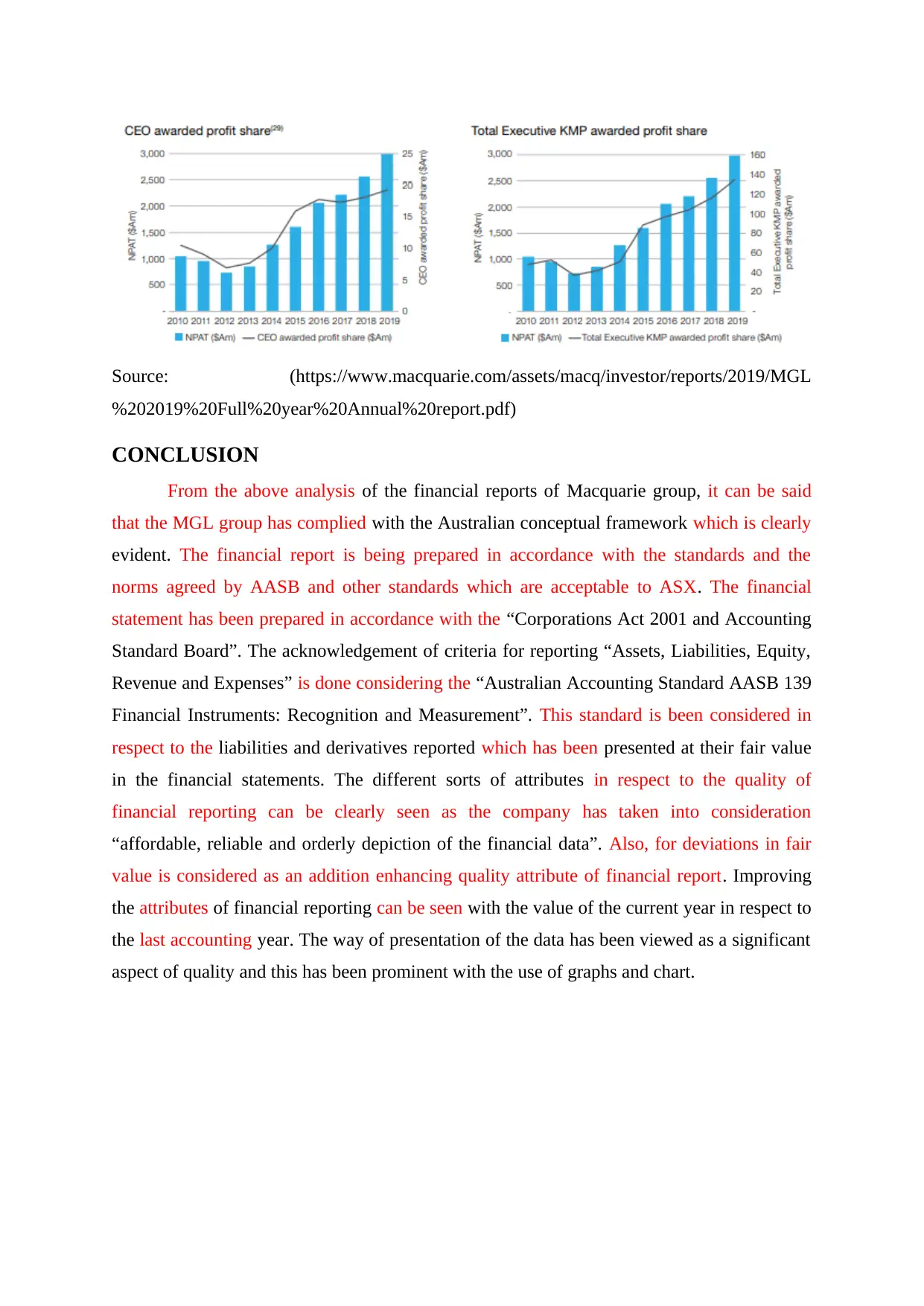

MSCI and also Macquarie vs. All Ordinaries Accumulation. The bar graph shows the fairness

of the company’s profit sharing pool. A comparison has been drawn with the international

reference group which indicates that the compensation ratio of the company is 38.3% which

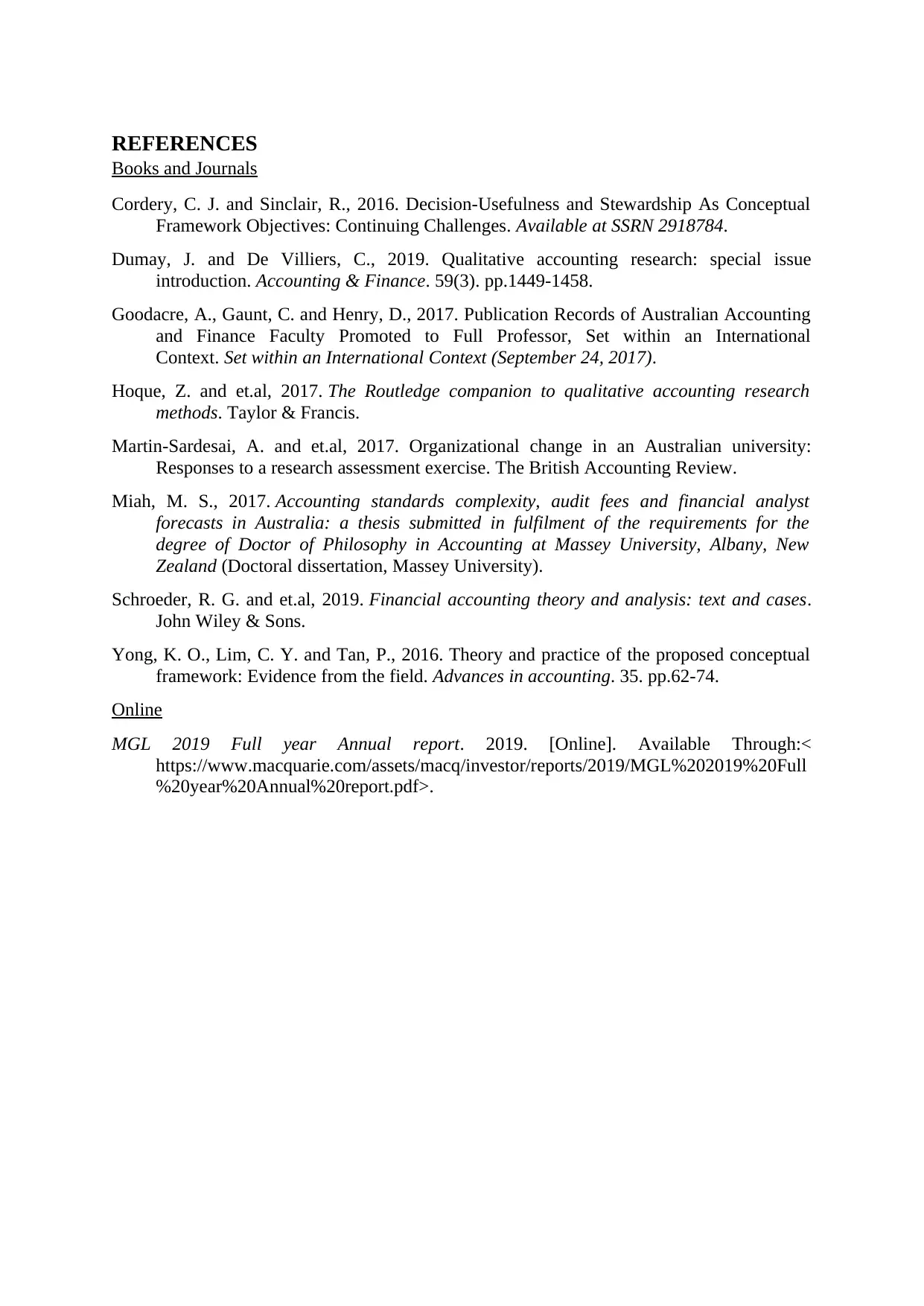

is below its peers on an average. Also, as on 31 march 2019, the board has determined the

“total awarded profit share” between CEO and total executive KMP.

The financial report of organization has been prepared while making sure that the

information is timely, complete and available at minimum cost. The improved comparability

of the financial information, appropriateness, understandability and verifiability all these can

be done by enhancing the qualitative characteristics (Martin-Sardesai and et.al, 2017). The

data provided in the report helps the user in making comparative disclosures that assists in

proper comparison and also assist in taking proper and effective decisions. The company

reviews the operation of the business by comparing its financial data with the previous year.

Macquarie group total shareholder return has remained strong over the long term and

has continued its strong performance at both the MSCI World Capital market index and the

All Ordinaries Accumulation since listings. This line chart depicts the clear picture of

enhancing the non-financial factors depicting total shareholder return for Macquarie vs.

MSCI and also Macquarie vs. All Ordinaries Accumulation. The bar graph shows the fairness

of the company’s profit sharing pool. A comparison has been drawn with the international

reference group which indicates that the compensation ratio of the company is 38.3% which

is below its peers on an average. Also, as on 31 march 2019, the board has determined the

“total awarded profit share” between CEO and total executive KMP.

Source: (https://www.macquarie.com/assets/macq/investor/reports/2019/MGL

%202019%20Full%20year%20Annual%20report.pdf)

Source: (https://www.macquarie.com/assets/macq/investor/reports/2019/MGL

%202019%20Full%20year%20Annual%20report.pdf)

%202019%20Full%20year%20Annual%20report.pdf)

Source: (https://www.macquarie.com/assets/macq/investor/reports/2019/MGL

%202019%20Full%20year%20Annual%20report.pdf)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Source: (https://www.macquarie.com/assets/macq/investor/reports/2019/MGL

%202019%20Full%20year%20Annual%20report.pdf)

CONCLUSION

From the above analysis of the financial reports of Macquarie group, it can be said

that the MGL group has complied with the Australian conceptual framework which is clearly

evident. The financial report is being prepared in accordance with the standards and the

norms agreed by AASB and other standards which are acceptable to ASX. The financial

statement has been prepared in accordance with the “Corporations Act 2001 and Accounting

Standard Board”. The acknowledgement of criteria for reporting “Assets, Liabilities, Equity,

Revenue and Expenses” is done considering the “Australian Accounting Standard AASB 139

Financial Instruments: Recognition and Measurement”. This standard is been considered in

respect to the liabilities and derivatives reported which has been presented at their fair value

in the financial statements. The different sorts of attributes in respect to the quality of

financial reporting can be clearly seen as the company has taken into consideration

“affordable, reliable and orderly depiction of the financial data”. Also, for deviations in fair

value is considered as an addition enhancing quality attribute of financial report. Improving

the attributes of financial reporting can be seen with the value of the current year in respect to

the last accounting year. The way of presentation of the data has been viewed as a significant

aspect of quality and this has been prominent with the use of graphs and chart.

%202019%20Full%20year%20Annual%20report.pdf)

CONCLUSION

From the above analysis of the financial reports of Macquarie group, it can be said

that the MGL group has complied with the Australian conceptual framework which is clearly

evident. The financial report is being prepared in accordance with the standards and the

norms agreed by AASB and other standards which are acceptable to ASX. The financial

statement has been prepared in accordance with the “Corporations Act 2001 and Accounting

Standard Board”. The acknowledgement of criteria for reporting “Assets, Liabilities, Equity,

Revenue and Expenses” is done considering the “Australian Accounting Standard AASB 139

Financial Instruments: Recognition and Measurement”. This standard is been considered in

respect to the liabilities and derivatives reported which has been presented at their fair value

in the financial statements. The different sorts of attributes in respect to the quality of

financial reporting can be clearly seen as the company has taken into consideration

“affordable, reliable and orderly depiction of the financial data”. Also, for deviations in fair

value is considered as an addition enhancing quality attribute of financial report. Improving

the attributes of financial reporting can be seen with the value of the current year in respect to

the last accounting year. The way of presentation of the data has been viewed as a significant

aspect of quality and this has been prominent with the use of graphs and chart.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Cordery, C. J. and Sinclair, R., 2016. Decision-Usefulness and Stewardship As Conceptual

Framework Objectives: Continuing Challenges. Available at SSRN 2918784.

Dumay, J. and De Villiers, C., 2019. Qualitative accounting research: special issue

introduction. Accounting & Finance. 59(3). pp.1449-1458.

Goodacre, A., Gaunt, C. and Henry, D., 2017. Publication Records of Australian Accounting

and Finance Faculty Promoted to Full Professor, Set within an International

Context. Set within an International Context (September 24, 2017).

Hoque, Z. and et.al, 2017. The Routledge companion to qualitative accounting research

methods. Taylor & Francis.

Martin-Sardesai, A. and et.al, 2017. Organizational change in an Australian university:

Responses to a research assessment exercise. The British Accounting Review.

Miah, M. S., 2017. Accounting standards complexity, audit fees and financial analyst

forecasts in Australia: a thesis submitted in fulfilment of the requirements for the

degree of Doctor of Philosophy in Accounting at Massey University, Albany, New

Zealand (Doctoral dissertation, Massey University).

Schroeder, R. G. and et.al, 2019. Financial accounting theory and analysis: text and cases.

John Wiley & Sons.

Yong, K. O., Lim, C. Y. and Tan, P., 2016. Theory and practice of the proposed conceptual

framework: Evidence from the field. Advances in accounting. 35. pp.62-74.

Online

MGL 2019 Full year Annual report. 2019. [Online]. Available Through:<

https://www.macquarie.com/assets/macq/investor/reports/2019/MGL%202019%20Full

%20year%20Annual%20report.pdf>.

Books and Journals

Cordery, C. J. and Sinclair, R., 2016. Decision-Usefulness and Stewardship As Conceptual

Framework Objectives: Continuing Challenges. Available at SSRN 2918784.

Dumay, J. and De Villiers, C., 2019. Qualitative accounting research: special issue

introduction. Accounting & Finance. 59(3). pp.1449-1458.

Goodacre, A., Gaunt, C. and Henry, D., 2017. Publication Records of Australian Accounting

and Finance Faculty Promoted to Full Professor, Set within an International

Context. Set within an International Context (September 24, 2017).

Hoque, Z. and et.al, 2017. The Routledge companion to qualitative accounting research

methods. Taylor & Francis.

Martin-Sardesai, A. and et.al, 2017. Organizational change in an Australian university:

Responses to a research assessment exercise. The British Accounting Review.

Miah, M. S., 2017. Accounting standards complexity, audit fees and financial analyst

forecasts in Australia: a thesis submitted in fulfilment of the requirements for the

degree of Doctor of Philosophy in Accounting at Massey University, Albany, New

Zealand (Doctoral dissertation, Massey University).

Schroeder, R. G. and et.al, 2019. Financial accounting theory and analysis: text and cases.

John Wiley & Sons.

Yong, K. O., Lim, C. Y. and Tan, P., 2016. Theory and practice of the proposed conceptual

framework: Evidence from the field. Advances in accounting. 35. pp.62-74.

Online

MGL 2019 Full year Annual report. 2019. [Online]. Available Through:<

https://www.macquarie.com/assets/macq/investor/reports/2019/MGL%202019%20Full

%20year%20Annual%20report.pdf>.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.