Management Accounting Report: Financial and Performance Analysis

VerifiedAdded on 2020/07/22

|21

|5986

|55

Report

AI Summary

This report delves into the core principles of management accounting, providing a comprehensive overview of its various facets. It begins with an introduction that discusses the importance of accounting information for decision-making in both present and future contexts. The report then explores the key differences between financial and management accounting, emphasizing their distinct objectives and user bases. Task 1 examines the critical role of decision-making in accounting. Task 2 focuses on the computation of income statements using both absorption and marginal costing methods, highlighting their impact on profitability analysis. Task 3 covers the process of preparing budgets and explores different pricing strategies. Finally, Task 4 introduces the Balance Scorecard as a systematic and strategic approach to performance management. The report concludes with a summary of the key concepts discussed and provides relevant references.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................1

TASK-1............................................................................................................................................1

Financial Accounting.............................................................................................................1

Management Accounting........................................................................................................2

Key Differences Between Financial Accounting and Management Accounting...................2

Importance of Decision Making.............................................................................................3

TASK-2 ..........................................................................................................................................6

Computation of income statement using Absorption costing method....................................9

Computation of income statement using marginal costing method.....................................10

TASK-3..........................................................................................................................................11

Process of preparing budget.................................................................................................13

Pricing strategies..................................................................................................................13

TASK-4..........................................................................................................................................14

Balance Scorecard................................................................................................................14

A systematic and strategic approach....................................................................................16

Conclusion.....................................................................................................................................17

References......................................................................................................................................18

Introduction......................................................................................................................................1

TASK-1............................................................................................................................................1

Financial Accounting.............................................................................................................1

Management Accounting........................................................................................................2

Key Differences Between Financial Accounting and Management Accounting...................2

Importance of Decision Making.............................................................................................3

TASK-2 ..........................................................................................................................................6

Computation of income statement using Absorption costing method....................................9

Computation of income statement using marginal costing method.....................................10

TASK-3..........................................................................................................................................11

Process of preparing budget.................................................................................................13

Pricing strategies..................................................................................................................13

TASK-4..........................................................................................................................................14

Balance Scorecard................................................................................................................14

A systematic and strategic approach....................................................................................16

Conclusion.....................................................................................................................................17

References......................................................................................................................................18

Introduction

Accounting fee management information solutions to discuss the company incurred in the

present and future. It also deals with inventory of various techniques. Cost estimates for

miscellaneous services are calculated by comparing the actual impact of the budget process. Also

book a different budget that helps to compare the results of real work. The provision also

includes costs, budget and a different language due to the mixture. It also deals with various

solutions that help business strategy to improve this process.

Budget management, task unit cost accounting help to give detailed information on the

various costs of business management. Through it, students can identify the tool or technology

available to analyse business costs and give economic costs organisation, provides also helps us

to understand the problem and made a series of decisions on costs and budgets.

Each organization concerned is the cost companies to reach their goals and do business

successfully. To this end, organizations must understand and classify the various costs of

overhead and any pay the interest to receive reports and budgets of the various business

processes to pay.

TASK-1

Accounting, refers to data storage and classification where simple financial transactions

and other events and interpretation of results. The machine is used to control financial

transactions, accounting and bookkeeping and Accounting confirms give a true and fair picture

of the financial position of the company in different directions.

Financial Accounting

Accounting Financial accounting in financial reporting from third parties such as

creditors, shareholders, investors, suppliers, creditors, customers etc. This is the purest form of

accounting and reporting where documents are in the system by providing consumers with

information and related materials.

Is based on the recognition of the assumptions and principles and arrangements within

the conservative and stable, and the consolidation of financial statements and other costs

of the acquisition, which includes the statement of the balance sheet of income and cash

flows from each other in line with the law on real estate, materials, fit, exercise

1

Accounting fee management information solutions to discuss the company incurred in the

present and future. It also deals with inventory of various techniques. Cost estimates for

miscellaneous services are calculated by comparing the actual impact of the budget process. Also

book a different budget that helps to compare the results of real work. The provision also

includes costs, budget and a different language due to the mixture. It also deals with various

solutions that help business strategy to improve this process.

Budget management, task unit cost accounting help to give detailed information on the

various costs of business management. Through it, students can identify the tool or technology

available to analyse business costs and give economic costs organisation, provides also helps us

to understand the problem and made a series of decisions on costs and budgets.

Each organization concerned is the cost companies to reach their goals and do business

successfully. To this end, organizations must understand and classify the various costs of

overhead and any pay the interest to receive reports and budgets of the various business

processes to pay.

TASK-1

Accounting, refers to data storage and classification where simple financial transactions

and other events and interpretation of results. The machine is used to control financial

transactions, accounting and bookkeeping and Accounting confirms give a true and fair picture

of the financial position of the company in different directions.

Financial Accounting

Accounting Financial accounting in financial reporting from third parties such as

creditors, shareholders, investors, suppliers, creditors, customers etc. This is the purest form of

accounting and reporting where documents are in the system by providing consumers with

information and related materials.

Is based on the recognition of the assumptions and principles and arrangements within

the conservative and stable, and the consolidation of financial statements and other costs

of the acquisition, which includes the statement of the balance sheet of income and cash

flows from each other in line with the law on real estate, materials, fit, exercise

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Typically, the report is based on certain account calculations, so that consumers can

compare the financial situation, profitability and performance of the company during this

period. Not only external factors but internal managers should expect planning and

decision-making.

Management Accounting

Management accounting, accounting management machines also assists management to

establish, manage, forecast, plan and control the day-to-day operations of the organization

department. Quantitative and qualitative data collected and analysed for their accounts

Accounting is an area providing financial information or costs. Instead, he pulled out of

promotional materials, as well as accounting and accounting help budget, specific goals, decision

- making, and can depend on demand management, ie weekly, monthly, quarterly, etc. On the

other hand, the formation of the organization said.

Key Differences Between Financial Accounting and Management Accounting

Represents the accounting industry, which tracks each unit financial information.

Accounting is a branch of accounting records and reports financial information and

financial data packages.

Accounting users to control the internal company and external factors, when used in

internal audit and internal control.

Accounting and financial management will not reach the public is the use of the

organization, and therefore very difficult.

Only financial information in the financial statements. However, both accounting in

management, financial statements and financial statements, such as the number of

employees, the amount of raw materials used and disposed of, etc.

The accounting performance of the group, but not the expense of a specific form of

control.

Accounting focuses on providing information about business model results from users,

while financial focus on providing information to help them evaluate performance and

plan ahead.

2

compare the financial situation, profitability and performance of the company during this

period. Not only external factors but internal managers should expect planning and

decision-making.

Management Accounting

Management accounting, accounting management machines also assists management to

establish, manage, forecast, plan and control the day-to-day operations of the organization

department. Quantitative and qualitative data collected and analysed for their accounts

Accounting is an area providing financial information or costs. Instead, he pulled out of

promotional materials, as well as accounting and accounting help budget, specific goals, decision

- making, and can depend on demand management, ie weekly, monthly, quarterly, etc. On the

other hand, the formation of the organization said.

Key Differences Between Financial Accounting and Management Accounting

Represents the accounting industry, which tracks each unit financial information.

Accounting is a branch of accounting records and reports financial information and

financial data packages.

Accounting users to control the internal company and external factors, when used in

internal audit and internal control.

Accounting and financial management will not reach the public is the use of the

organization, and therefore very difficult.

Only financial information in the financial statements. However, both accounting in

management, financial statements and financial statements, such as the number of

employees, the amount of raw materials used and disposed of, etc.

The accounting performance of the group, but not the expense of a specific form of

control.

Accounting focuses on providing information about business model results from users,

while financial focus on providing information to help them evaluate performance and

plan ahead.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting is performed mainly for a specified period, usually a year. Instead made

statements according to management requirements, say quarterly and semi-annual, and

more.

Accounting is mandatory for all companies to audit. On the other hand, it is optional

because it does not.

The necessary accounting data is published and the audit report is reviewed. On the other

hand, management accounting, which requires no advertising and publishing, because it

is for internal use.

Importance of Decision Making

Controlling accounting and bookkeeping is very important, in fact, they help

organizations in different ways. Accounting also helps maintain the validity of a number of

transactions and compare the two periods of the group or two units, while the president to

facilitate the analysis of the efficiency of the statement production strategy provides an effective

political future.

Explain the different types of Management Accounting

Here we look at production units Limited pirates are as follows based on the breakdown

of costs related - information. Pirate Limited (Far, 2011).

Before going to where the issues, let us understand what the real cost. Cost words to

show how much money the company uses in creating goods and services included in the costs of

raw materials, equipment, goods, services, employment, goods, etc.

Cost of all three major components:

Components - direct / indirect

Work - direct / indirect

Costs - direct / indirect

These elements can be divided during production and cost.

i. Cost accounting systems

Product cost - this is the cost of manufacturing the product.

3

statements according to management requirements, say quarterly and semi-annual, and

more.

Accounting is mandatory for all companies to audit. On the other hand, it is optional

because it does not.

The necessary accounting data is published and the audit report is reviewed. On the other

hand, management accounting, which requires no advertising and publishing, because it

is for internal use.

Importance of Decision Making

Controlling accounting and bookkeeping is very important, in fact, they help

organizations in different ways. Accounting also helps maintain the validity of a number of

transactions and compare the two periods of the group or two units, while the president to

facilitate the analysis of the efficiency of the statement production strategy provides an effective

political future.

Explain the different types of Management Accounting

Here we look at production units Limited pirates are as follows based on the breakdown

of costs related - information. Pirate Limited (Far, 2011).

Before going to where the issues, let us understand what the real cost. Cost words to

show how much money the company uses in creating goods and services included in the costs of

raw materials, equipment, goods, services, employment, goods, etc.

Cost of all three major components:

Components - direct / indirect

Work - direct / indirect

Costs - direct / indirect

These elements can be divided during production and cost.

i. Cost accounting systems

Product cost - this is the cost of manufacturing the product.

3

Period costs - costs, production costs are recognized in profit or writing at different times.

The price includes the cost of goods "direct costs". Direct costs associated with direct

product manufacturing (Tyran, 1982). These costs are naturally variable costs. Direct

costs are as follows:

Direct materials - these are the property caused by the production, such as raw materials.

For example, the accumulated cost for plywood, textile fabric, wooden boards, IMDA

Tech Ltd, etc.

Direct Labour - this is the work of the production companies or set to a specific

manufacturing cost centre. For example, education, artist, saws, installation, etc.

Direct Expenses - two IAS (International Accounting Standards) costs directly part of the

cost structure. These are the costs of improvements, quality or design. For example, to

buy special equipment to update the style tables and chairs (Far, 2011).

Inventory management systems

Indirect materials - not included in the cost of direct and indirect materials imported

materials.

Wage labour costs - labour costs that are not linked directly to the production costs of

management. For example, supervisors, brooms and other techniques.

Indirect costs - costs indirect costs mainly for the factory. For example, mainly consist of

depreciation on machinery, electricity, rent, telephone bills, council tax, insurance and

other expenses.

The cost of the cost of the total cost of administrative costs and the costs of sales and

distribution, as well as economic costs.

◦ Administrative costs - is the total ownership of the administrative expenses of the

Organization. Management fees, office rent, council tax, water charges, telephone

bills, etc. (Far, 2011).

◦ Selling and distribution costs - the costs of creating a viable for the sale and

distribution of a number of death sentences product. These costs include advertising

costs, market research, salary surveys, bonus and others

4

The price includes the cost of goods "direct costs". Direct costs associated with direct

product manufacturing (Tyran, 1982). These costs are naturally variable costs. Direct

costs are as follows:

Direct materials - these are the property caused by the production, such as raw materials.

For example, the accumulated cost for plywood, textile fabric, wooden boards, IMDA

Tech Ltd, etc.

Direct Labour - this is the work of the production companies or set to a specific

manufacturing cost centre. For example, education, artist, saws, installation, etc.

Direct Expenses - two IAS (International Accounting Standards) costs directly part of the

cost structure. These are the costs of improvements, quality or design. For example, to

buy special equipment to update the style tables and chairs (Far, 2011).

Inventory management systems

Indirect materials - not included in the cost of direct and indirect materials imported

materials.

Wage labour costs - labour costs that are not linked directly to the production costs of

management. For example, supervisors, brooms and other techniques.

Indirect costs - costs indirect costs mainly for the factory. For example, mainly consist of

depreciation on machinery, electricity, rent, telephone bills, council tax, insurance and

other expenses.

The cost of the cost of the total cost of administrative costs and the costs of sales and

distribution, as well as economic costs.

◦ Administrative costs - is the total ownership of the administrative expenses of the

Organization. Management fees, office rent, council tax, water charges, telephone

bills, etc. (Far, 2011).

◦ Selling and distribution costs - the costs of creating a viable for the sale and

distribution of a number of death sentences product. These costs include advertising

costs, market research, salary surveys, bonus and others

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Job costing systems

Job costing: This method is the industry and are all kinds of jobs and the calculation of the cost

of each function using this method. For example, by building services that provide homes,

factories, shops and others (Lucy, 2002).The cost of assets - these costs are those associated, has

stabilized short - term financing. These include dividends, interest, long-term and short-term and

long-term loans.The additional cost can be divided into the following:Based on the behaviour-

The costs are divided on the basis of cost to the behaviour of three types, variable, fixed costs

and variable costs and a half.

iv. Price optimising systems

Price history: the cost of past and present obligations.

Where costs: costs, which have been prepared in advance for future use (Rouwendal,

2012).

There are several types of cost method of regulation. In order to successfully manage the

work under normal conditions. They are as follows:

Value of the contract: the method used to calculate the cost of the project costs or

contracts which led to bridges, buildings, construction, etc.

Valuable method: This method is used in the organization, which follows a different

process to make the final products. For example, in the textile industry to make the final

product (cloth), the following various processes such as spinning, weaving, dyeing,

folding paper, so that the costs can be calculated separately for the product (Harris,

1995).

Service price: This method is suitable for business services. For this method, the cost of

interest was prepared by the Special Services Organization (Baum, 2013).

Hackers measure limited methods of work to determine the cost of a particular job in this

case.

Limited costs: This method is used in the organization, while each unit produced. The

cost of this method was cleared from the cost of the product and the cost of fixed changes

in profitability (Harris, 1995).

5

Job costing: This method is the industry and are all kinds of jobs and the calculation of the cost

of each function using this method. For example, by building services that provide homes,

factories, shops and others (Lucy, 2002).The cost of assets - these costs are those associated, has

stabilized short - term financing. These include dividends, interest, long-term and short-term and

long-term loans.The additional cost can be divided into the following:Based on the behaviour-

The costs are divided on the basis of cost to the behaviour of three types, variable, fixed costs

and variable costs and a half.

iv. Price optimising systems

Price history: the cost of past and present obligations.

Where costs: costs, which have been prepared in advance for future use (Rouwendal,

2012).

There are several types of cost method of regulation. In order to successfully manage the

work under normal conditions. They are as follows:

Value of the contract: the method used to calculate the cost of the project costs or

contracts which led to bridges, buildings, construction, etc.

Valuable method: This method is used in the organization, which follows a different

process to make the final products. For example, in the textile industry to make the final

product (cloth), the following various processes such as spinning, weaving, dyeing,

folding paper, so that the costs can be calculated separately for the product (Harris,

1995).

Service price: This method is suitable for business services. For this method, the cost of

interest was prepared by the Special Services Organization (Baum, 2013).

Hackers measure limited methods of work to determine the cost of a particular job in this

case.

Limited costs: This method is used in the organization, while each unit produced. The

cost of this method was cleared from the cost of the product and the cost of fixed changes

in profitability (Harris, 1995).

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Fixed costs: the cost of equipment, even if the business has changed. It does not affect the

level of production (Underwood, 2006).

Variable costs: Costs vary depending on the level of production OY pirates (Czopek,

2004).

Semi - variable cost: the cost, there are two types of fixed and variable costs

characteristics.

◦ On the basis of the ability to manage: Based on the ability to control costs and are

divided into two types of control controlled by the administration and management

can not control.

◦ On the basis of time: Based on the time and costs are classified as two types of cards

original price and cost.

TASK-2

Cost Calculation Method

There are different ways to calculate the cost of production, the cost of goods sold, unit

costs and other institutions or companies the right to choose what kind of method is confirmed

by product production. Write in a way that can be classified as follows.

The following equation is obtained for marginal cost:

Marginal cost variable costs = + Fixed costs.

It accepted the recognition of excellent reception as part of the administrative costs.

Production costs are absorbed by production units. Costs may be fixed or variable, assigned to

different cost centers, which dealt with the rate of uptake (Rouwendal 2012). With this method,

the cost of recovering from the sale price of goods or services. These include technology costs

associated with manufacturing and also directly to products and services.

Based on cost absorption, the cost may be to find a solution to limited piracy

Smart Competition:

A variety of public expenditure varies in proportion to production units that direct agents,

and indirect costs of direct, which can not be transferred directly to a particular product. General

6

level of production (Underwood, 2006).

Variable costs: Costs vary depending on the level of production OY pirates (Czopek,

2004).

Semi - variable cost: the cost, there are two types of fixed and variable costs

characteristics.

◦ On the basis of the ability to manage: Based on the ability to control costs and are

divided into two types of control controlled by the administration and management

can not control.

◦ On the basis of time: Based on the time and costs are classified as two types of cards

original price and cost.

TASK-2

Cost Calculation Method

There are different ways to calculate the cost of production, the cost of goods sold, unit

costs and other institutions or companies the right to choose what kind of method is confirmed

by product production. Write in a way that can be classified as follows.

The following equation is obtained for marginal cost:

Marginal cost variable costs = + Fixed costs.

It accepted the recognition of excellent reception as part of the administrative costs.

Production costs are absorbed by production units. Costs may be fixed or variable, assigned to

different cost centers, which dealt with the rate of uptake (Rouwendal 2012). With this method,

the cost of recovering from the sale price of goods or services. These include technology costs

associated with manufacturing and also directly to products and services.

Based on cost absorption, the cost may be to find a solution to limited piracy

Smart Competition:

A variety of public expenditure varies in proportion to production units that direct agents,

and indirect costs of direct, which can not be transferred directly to a particular product. General

6

fixed costs remain constant regardless of the total output consists of rental and removal device,

insurance, office and other costs more element of the most consistent and most of them in the

output of half or semi - solid variable.

The difference between the marginal cost and the fixed and variable costs of the

product. Costs of producing an additional device called marginal cost. Other production costs

remain unchanged. It should be noted that the concept of fixed and variable costs in the short

term. And long-term, all-changing costs.

Costs can also be classified in terms of fiscal year. The benefits of the afterlife cost of

capital. These costs will be in a few years. On the other hand, the only fact costs are known to

cost year to year because of the part of the total cost. The cost-making option can also be

classified as low cost payment, unregulated cost control, cost-sharing cost difference, etc.

Normal price:

Standard costs of production costs, direct labor and related expenses directly. Contrast analysis is

an important part of the standard rate, which shows the real difference between the actual cost

and the standard cost. Some of the major languages is the difference of material costs of

changing size and labor costs variation.

Value rating:

Cost savings and cost - cost control and cost reduction is a very important tool for organizations

to work effectively. Lower costs and lower the cost of products or services a device has been

designed and manufactured. While on the other hand, cost control is to achieve goals in advance.

Producer prices - sometimes crucial to sell their products at marginal cost in the market. The cost

of welding of support for these decisions.

Absorption costing- reconstruction is another name for the absorption in the sky of the region.

Exchange of information on products in a given category. Cost breakdown per unit.

Making or buying decisions - reducing the number of times the quality control organization

decides to buy a particular part in the production of products covered. Large capacity and

decision must be made. Distribution costs help to make this decision.

7

insurance, office and other costs more element of the most consistent and most of them in the

output of half or semi - solid variable.

The difference between the marginal cost and the fixed and variable costs of the

product. Costs of producing an additional device called marginal cost. Other production costs

remain unchanged. It should be noted that the concept of fixed and variable costs in the short

term. And long-term, all-changing costs.

Costs can also be classified in terms of fiscal year. The benefits of the afterlife cost of

capital. These costs will be in a few years. On the other hand, the only fact costs are known to

cost year to year because of the part of the total cost. The cost-making option can also be

classified as low cost payment, unregulated cost control, cost-sharing cost difference, etc.

Normal price:

Standard costs of production costs, direct labor and related expenses directly. Contrast analysis is

an important part of the standard rate, which shows the real difference between the actual cost

and the standard cost. Some of the major languages is the difference of material costs of

changing size and labor costs variation.

Value rating:

Cost savings and cost - cost control and cost reduction is a very important tool for organizations

to work effectively. Lower costs and lower the cost of products or services a device has been

designed and manufactured. While on the other hand, cost control is to achieve goals in advance.

Producer prices - sometimes crucial to sell their products at marginal cost in the market. The cost

of welding of support for these decisions.

Absorption costing- reconstruction is another name for the absorption in the sky of the region.

Exchange of information on products in a given category. Cost breakdown per unit.

Making or buying decisions - reducing the number of times the quality control organization

decides to buy a particular part in the production of products covered. Large capacity and

decision must be made. Distribution costs help to make this decision.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Product diversification / expansion / stop production line - depend on the profitability of the

company’s management decided to diversify their products or not. After a certain period of time,

managers must take the initiative to develop business so that the company's competitiveness.

Appropriate distribution of costs to launch remaining Imda Tech UK Limited

The launch the furnace directly. This method is suitable for this valuable process costs. Since

most of the costs corresponding to different shopping departments, it is the direct cost of the

organization, except for a few top shopping. In this process, the following accounting system

approved by the Ministry of different production costs measure the cost of machine production.

Therefore, the process is the best accounting estimates.

Materials - The first step is to remove the raw material production. After the first step on raw

materials and selected materials from sub-sub-sub-section includes new expenses.

Wage costs are added to the cost of staff working on the product or process - work. Wages are

divided and applied in appropriate circumstances. With the cost of various components of the

average salary can be distributed, for example, salary divided by the time to invest in product

production.

Direct costs - direct costs are those associated fully to produce specific products. These costs will

be directly charged to this process. Direct costs are no exception rent, electricity, consumption

and so on.

Costs - These costs do not participate directly in production, but overwhelmed by the absorption.

In other words, this is the indirect costs of the organization. The CEO can hire an account

maintaining machinery and equipment, etc.

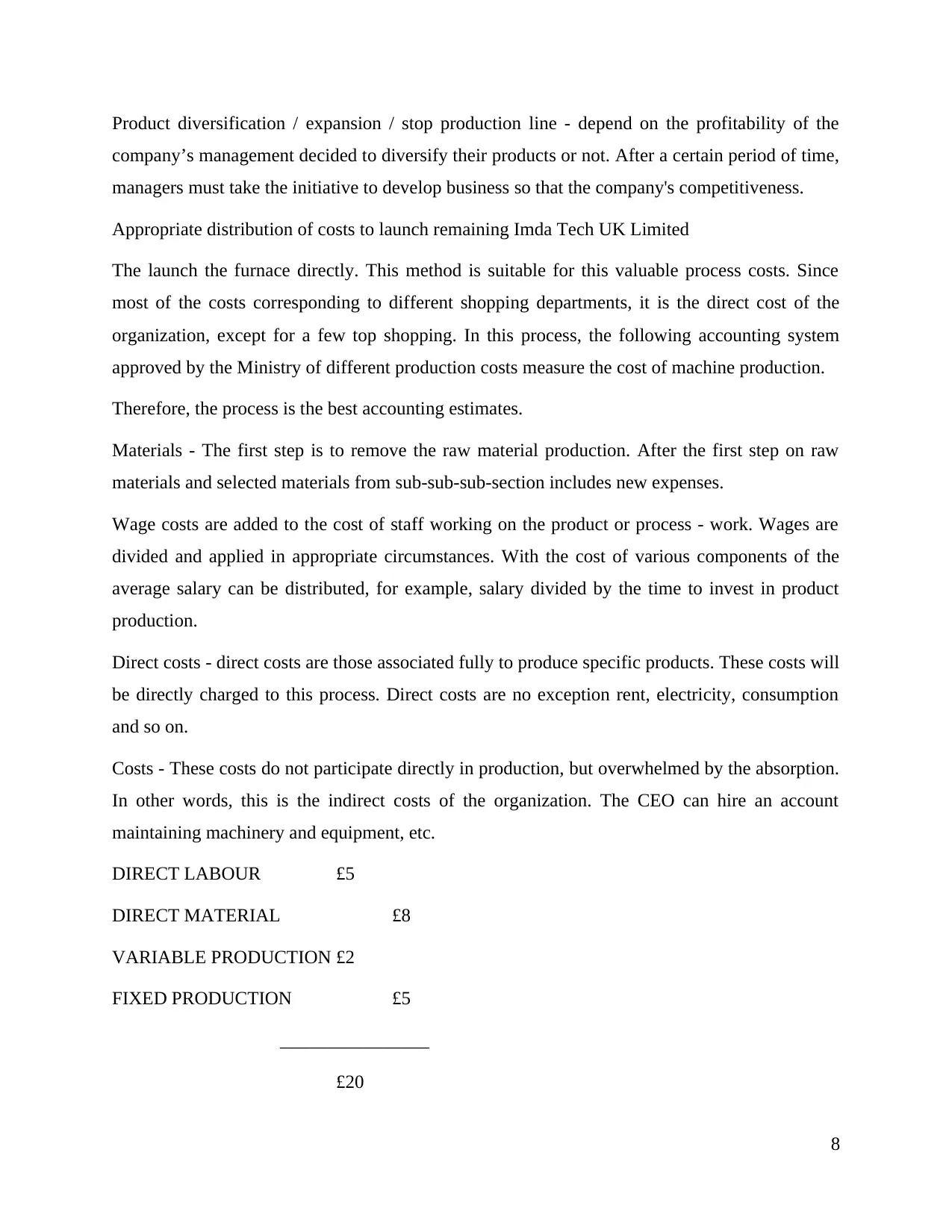

DIRECT LABOUR £5

DIRECT MATERIAL £8

VARIABLE PRODUCTION £2

FIXED PRODUCTION £5

________________

£20

8

company’s management decided to diversify their products or not. After a certain period of time,

managers must take the initiative to develop business so that the company's competitiveness.

Appropriate distribution of costs to launch remaining Imda Tech UK Limited

The launch the furnace directly. This method is suitable for this valuable process costs. Since

most of the costs corresponding to different shopping departments, it is the direct cost of the

organization, except for a few top shopping. In this process, the following accounting system

approved by the Ministry of different production costs measure the cost of machine production.

Therefore, the process is the best accounting estimates.

Materials - The first step is to remove the raw material production. After the first step on raw

materials and selected materials from sub-sub-sub-section includes new expenses.

Wage costs are added to the cost of staff working on the product or process - work. Wages are

divided and applied in appropriate circumstances. With the cost of various components of the

average salary can be distributed, for example, salary divided by the time to invest in product

production.

Direct costs - direct costs are those associated fully to produce specific products. These costs will

be directly charged to this process. Direct costs are no exception rent, electricity, consumption

and so on.

Costs - These costs do not participate directly in production, but overwhelmed by the absorption.

In other words, this is the indirect costs of the organization. The CEO can hire an account

maintaining machinery and equipment, etc.

DIRECT LABOUR £5

DIRECT MATERIAL £8

VARIABLE PRODUCTION £2

FIXED PRODUCTION £5

________________

£20

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUDGETED NORMAL OUT PUT £36000

SEPTMEBER £1500

FIXED £10000

VARIABLE %15

Reward = 0.75 * 8 * 1500 36000

Higher by 15% of the time

= 15% * 2 2400 2400

The amount of £ 91400

Computation of income statement using Absorption costing method

Income Statement using Absorption Costing Method

Particulars Amount

Units (Production) 2000

Units (sold) 1500

Sales @35 per unit 52500

9

SEPTMEBER £1500

FIXED £10000

VARIABLE %15

Reward = 0.75 * 8 * 1500 36000

Higher by 15% of the time

= 15% * 2 2400 2400

The amount of £ 91400

Computation of income statement using Absorption costing method

Income Statement using Absorption Costing Method

Particulars Amount

Units (Production) 2000

Units (sold) 1500

Sales @35 per unit 52500

9

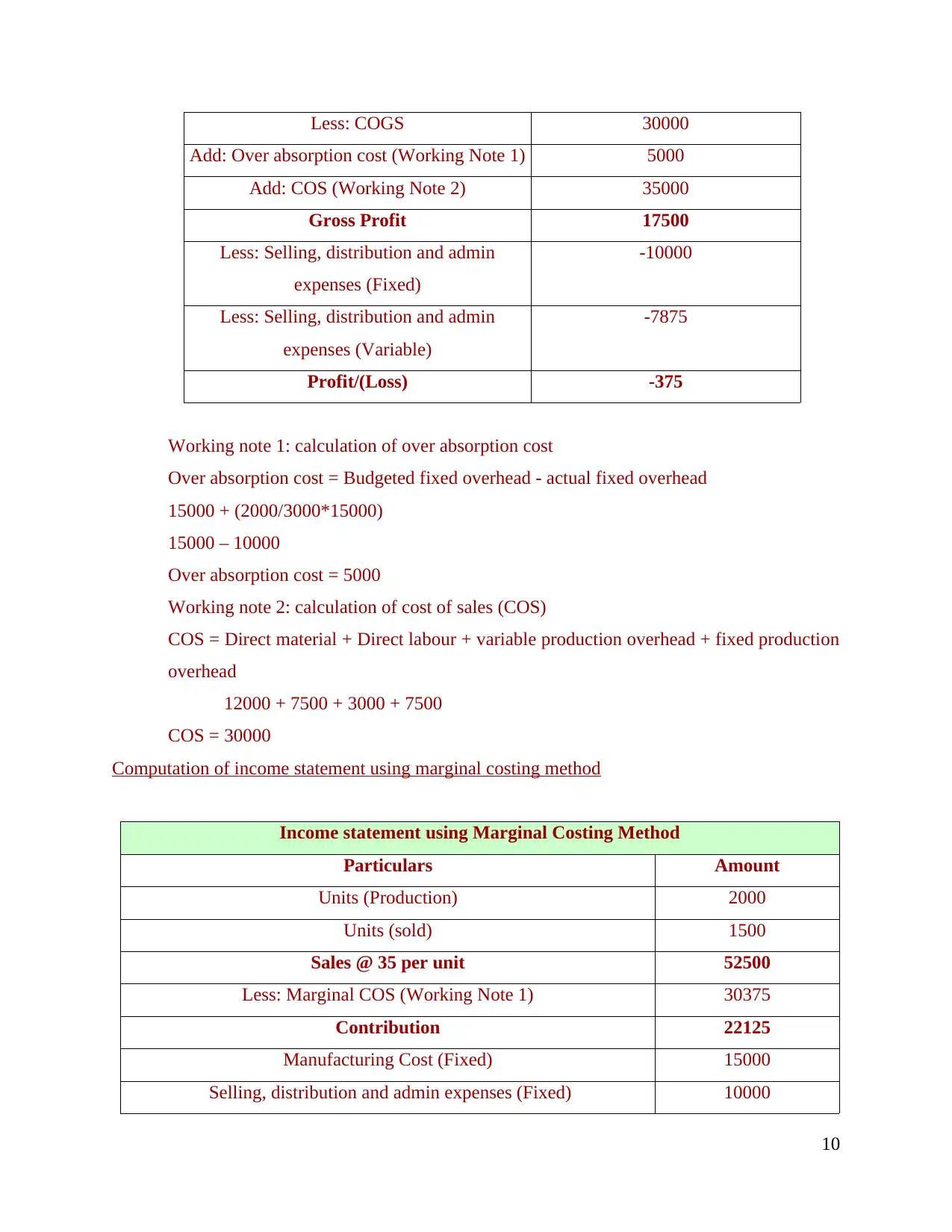

Less: COGS 30000

Add: Over absorption cost (Working Note 1) 5000

Add: COS (Working Note 2) 35000

Gross Profit 17500

Less: Selling, distribution and admin

expenses (Fixed)

-10000

Less: Selling, distribution and admin

expenses (Variable)

-7875

Profit/(Loss) -375

Working note 1: calculation of over absorption cost

Over absorption cost = Budgeted fixed overhead - actual fixed overhead

15000 + (2000/3000*15000)

15000 – 10000

Over absorption cost = 5000

Working note 2: calculation of cost of sales (COS)

COS = Direct material + Direct labour + variable production overhead + fixed production

overhead

12000 + 7500 + 3000 + 7500

COS = 30000

Computation of income statement using marginal costing method

Income statement using Marginal Costing Method

Particulars Amount

Units (Production) 2000

Units (sold) 1500

Sales @ 35 per unit 52500

Less: Marginal COS (Working Note 1) 30375

Contribution 22125

Manufacturing Cost (Fixed) 15000

Selling, distribution and admin expenses (Fixed) 10000

10

Add: Over absorption cost (Working Note 1) 5000

Add: COS (Working Note 2) 35000

Gross Profit 17500

Less: Selling, distribution and admin

expenses (Fixed)

-10000

Less: Selling, distribution and admin

expenses (Variable)

-7875

Profit/(Loss) -375

Working note 1: calculation of over absorption cost

Over absorption cost = Budgeted fixed overhead - actual fixed overhead

15000 + (2000/3000*15000)

15000 – 10000

Over absorption cost = 5000

Working note 2: calculation of cost of sales (COS)

COS = Direct material + Direct labour + variable production overhead + fixed production

overhead

12000 + 7500 + 3000 + 7500

COS = 30000

Computation of income statement using marginal costing method

Income statement using Marginal Costing Method

Particulars Amount

Units (Production) 2000

Units (sold) 1500

Sales @ 35 per unit 52500

Less: Marginal COS (Working Note 1) 30375

Contribution 22125

Manufacturing Cost (Fixed) 15000

Selling, distribution and admin expenses (Fixed) 10000

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.