AC50026E Financial Accounting Report: NEXT Plc Ratio Analysis

VerifiedAdded on 2023/06/16

|12

|2412

|188

Report

AI Summary

This report provides a financial analysis of NEXT Plc using accounting ratios calculated from their 2021 annual report. It covers profitability ratios (operating profit ratio, gross profit ratio, return on capital employed), liquidity ratios (current ratio, quick ratio), efficiency ratios (debtors turnover period, fixed assets turnover), and solvency ratios (interest coverage ratio, debt to asset ratio). The interpretation of these ratios indicates a decline in financial performance in 2021 compared to previous years, particularly 2020, attributed to the global pandemic. Recommendations are made for NEXT Plc to improve its financial performance in subsequent years to regain its previous level of efficiency and effectiveness. The report concludes that while the company faced challenges in 2021, improvements are necessary to enhance its earning capacity.

Financial accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Financial accounting............................................................................................................1

Table of Contents.............................................................................................................................2

Introduction......................................................................................................................................3

Accounting Ratios and Its Calculation...................................................................................3

Interpretation....................................................................................................................................4

Recommendation....................................................................................................................6

Conclusion..............................................................................................................................6

References........................................................................................................................................7

Books & Journals...................................................................................................................7

Appendix..........................................................................................................................................8

Financial accounting............................................................................................................1

Table of Contents.............................................................................................................................2

Introduction......................................................................................................................................3

Accounting Ratios and Its Calculation...................................................................................3

Interpretation....................................................................................................................................4

Recommendation....................................................................................................................6

Conclusion..............................................................................................................................6

References........................................................................................................................................7

Books & Journals...................................................................................................................7

Appendix..........................................................................................................................................8

Introduction

In every organization, it is highly important to analyse the financial situation of the company

by carefully assessing the balancing sheet in a proper way. For this purpose, the use of

balance sheet can be utilized because all the important components of an organization that

comes in the financial capacity of an organization are included in it. In context to this report,

NEXT Plc has been taken into consideration. The annual report of this respective company

of the year 2021 are used and applied in order to calculate the accounting ratios and assess

the financial stability of the company.

Accounting Ratios and Its Calculation

Accounting Ratios can be considered as a highly valuable tool that basically helps in

making the financial decisions for the business organization in a very effective manner

(Adwan, Alhaj-Ismail and Girardone, 2020). This tool is majorly used by investors and

professionals in the finance field so that they can analyse the financial position of the

company carefully. In context to Next Plc, different ratios are explained and calculated

below:

1. Profitability Ratios: These are those ratios that helps in understanding the capacity of

the firm to create and generate earnings in accordance to the revenue by using the

financial data of the company. Several types of profitability ratios are mentioned

below:

a) Operating Profit Ratio: It is a type of ratio that helps in understanding the

capacity to earn profit and revenues out of the business operations. It is a

relationship between the operating profit & net sales.

b) Gross profit ratio: It can be defined as the difference between sales & cost of

goods sold, divided by net sales. It is usually expressed in percentage.

c) Return on Capital Employed: It is an accounting ratio used in the financial

management, valuation along with accounting. It helps in comparing the

profitability of companies for the purpose of capital used.

2. Liquidity Ratios: These are those accounting ratios that help in ascertaining the

capacity of the firm to assess ability of the firm to pay off its financial current debts

In every organization, it is highly important to analyse the financial situation of the company

by carefully assessing the balancing sheet in a proper way. For this purpose, the use of

balance sheet can be utilized because all the important components of an organization that

comes in the financial capacity of an organization are included in it. In context to this report,

NEXT Plc has been taken into consideration. The annual report of this respective company

of the year 2021 are used and applied in order to calculate the accounting ratios and assess

the financial stability of the company.

Accounting Ratios and Its Calculation

Accounting Ratios can be considered as a highly valuable tool that basically helps in

making the financial decisions for the business organization in a very effective manner

(Adwan, Alhaj-Ismail and Girardone, 2020). This tool is majorly used by investors and

professionals in the finance field so that they can analyse the financial position of the

company carefully. In context to Next Plc, different ratios are explained and calculated

below:

1. Profitability Ratios: These are those ratios that helps in understanding the capacity of

the firm to create and generate earnings in accordance to the revenue by using the

financial data of the company. Several types of profitability ratios are mentioned

below:

a) Operating Profit Ratio: It is a type of ratio that helps in understanding the

capacity to earn profit and revenues out of the business operations. It is a

relationship between the operating profit & net sales.

b) Gross profit ratio: It can be defined as the difference between sales & cost of

goods sold, divided by net sales. It is usually expressed in percentage.

c) Return on Capital Employed: It is an accounting ratio used in the financial

management, valuation along with accounting. It helps in comparing the

profitability of companies for the purpose of capital used.

2. Liquidity Ratios: These are those accounting ratios that help in ascertaining the

capacity of the firm to assess ability of the firm to pay off its financial current debts

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(Kenny and Larson, 2018). it basically helps in measuring the company’s capability to

pay back the debts and all the obligation related to it. It includes various ratios that are

mentioned below:

A) Current Ratio: It is one of the liquidity ratio that helps in measuring the capacity

of the firm to deal with the short term responsibility.

B) Quick Ratio / Acid Test Ratio: It is a ratio that helps in measuring the capability

of the business organization to utilize for the purpose to use its near cash and the

asset which don’t include inventory.

3. Efficiency Ratios (measured in Days or in Times): these are basically those ratios

that help in analysing how efficiently the company can use its assets and liabilities of

the company. The major purpose of using this ratio is basically to track the

performance of commercial and investment institutions.

a) Debtors Turnover Period : It is an accounting measure that is used by the

company in order to extend credit along with the collecting debts. This helps in

understanding the firm capability to use its assets.

b) Fixed Assets Turnover : It is the ratio that helps in utilizing the fixed assets so that

the business organization can generate high level of sales.

4. Solvency Ratios: It can be defined as an effective measure that helps in ascertaining

the company’s ability to deal with all the long-term financial obligations. it is often

used by the business leaders as they will take the decision of providing funds on the

basis of this only.

a) Interest coverage ratio: It is a ratio that specifically helps in measuring the ability

of the company to honour the payments of debts.

b) Debt to asset ratio: It is a type of leverage ratio, that helps in indicating the assets

percentage. This ratio helps in financing with the debts. A higher amount of ratio,

the greater degree of risk exists in leverage and financial.

Interpretation

From the above calculation of all the accounting ratios, the interpretation of all the ratios is

mentioned below specifically for each type:

Operating profit ratio: Although, the operating profit margin of the year 2017 is

higher than 15% which is considered as good. In the case of critical comparison

pay back the debts and all the obligation related to it. It includes various ratios that are

mentioned below:

A) Current Ratio: It is one of the liquidity ratio that helps in measuring the capacity

of the firm to deal with the short term responsibility.

B) Quick Ratio / Acid Test Ratio: It is a ratio that helps in measuring the capability

of the business organization to utilize for the purpose to use its near cash and the

asset which don’t include inventory.

3. Efficiency Ratios (measured in Days or in Times): these are basically those ratios

that help in analysing how efficiently the company can use its assets and liabilities of

the company. The major purpose of using this ratio is basically to track the

performance of commercial and investment institutions.

a) Debtors Turnover Period : It is an accounting measure that is used by the

company in order to extend credit along with the collecting debts. This helps in

understanding the firm capability to use its assets.

b) Fixed Assets Turnover : It is the ratio that helps in utilizing the fixed assets so that

the business organization can generate high level of sales.

4. Solvency Ratios: It can be defined as an effective measure that helps in ascertaining

the company’s ability to deal with all the long-term financial obligations. it is often

used by the business leaders as they will take the decision of providing funds on the

basis of this only.

a) Interest coverage ratio: It is a ratio that specifically helps in measuring the ability

of the company to honour the payments of debts.

b) Debt to asset ratio: It is a type of leverage ratio, that helps in indicating the assets

percentage. This ratio helps in financing with the debts. A higher amount of ratio,

the greater degree of risk exists in leverage and financial.

Interpretation

From the above calculation of all the accounting ratios, the interpretation of all the ratios is

mentioned below specifically for each type:

Operating profit ratio: Although, the operating profit margin of the year 2017 is

higher than 15% which is considered as good. In the case of critical comparison

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

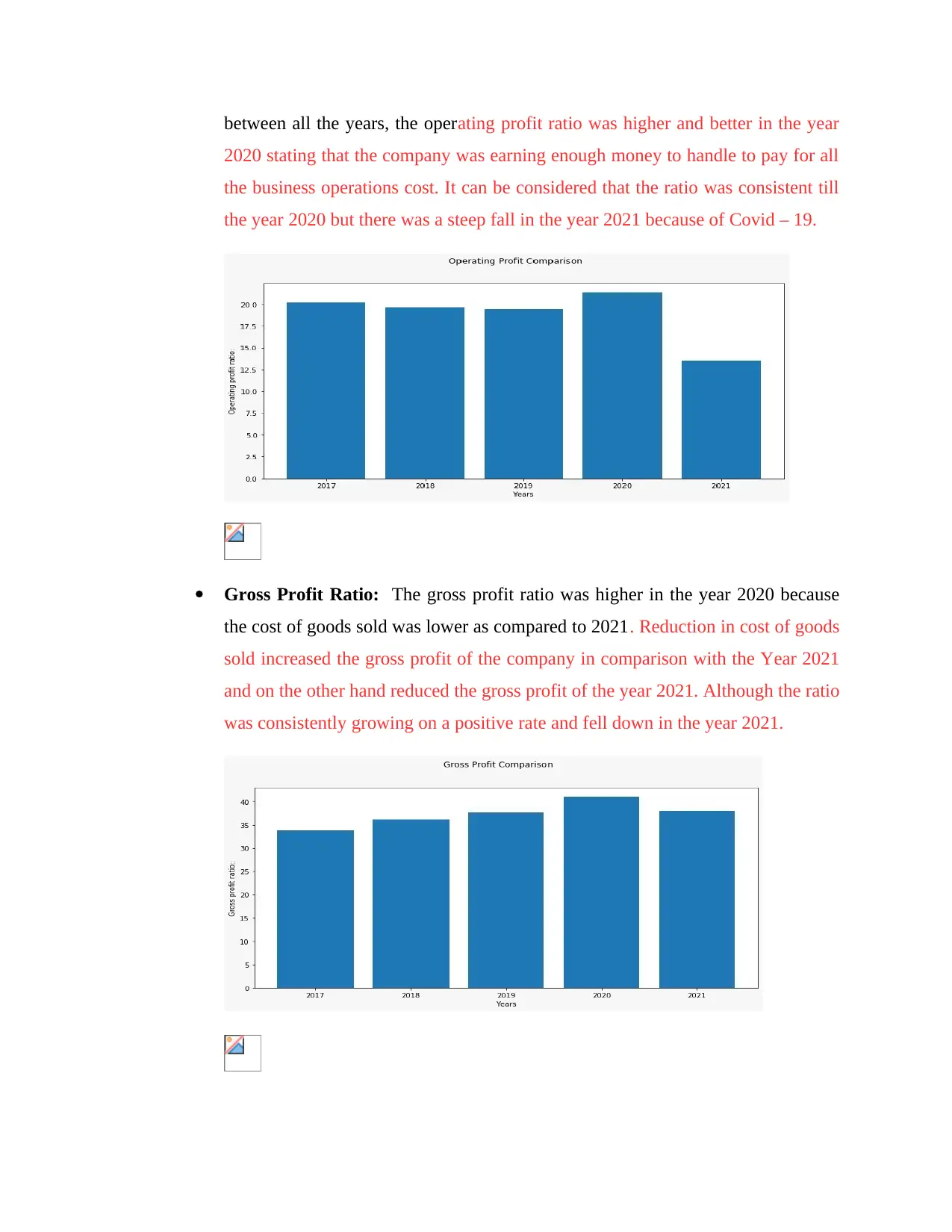

between all the years, the operating profit ratio was higher and better in the year

2020 stating that the company was earning enough money to handle to pay for all

the business operations cost. It can be considered that the ratio was consistent till

the year 2020 but there was a steep fall in the year 2021 because of Covid – 19.

Gross Profit Ratio: The gross profit ratio was higher in the year 2020 because

the cost of goods sold was lower as compared to 2021. Reduction in cost of goods

sold increased the gross profit of the company in comparison with the Year 2021

and on the other hand reduced the gross profit of the year 2021. Although the ratio

was consistently growing on a positive rate and fell down in the year 2021.

2020 stating that the company was earning enough money to handle to pay for all

the business operations cost. It can be considered that the ratio was consistent till

the year 2020 but there was a steep fall in the year 2021 because of Covid – 19.

Gross Profit Ratio: The gross profit ratio was higher in the year 2020 because

the cost of goods sold was lower as compared to 2021. Reduction in cost of goods

sold increased the gross profit of the company in comparison with the Year 2021

and on the other hand reduced the gross profit of the year 2021. Although the ratio

was consistently growing on a positive rate and fell down in the year 2021.

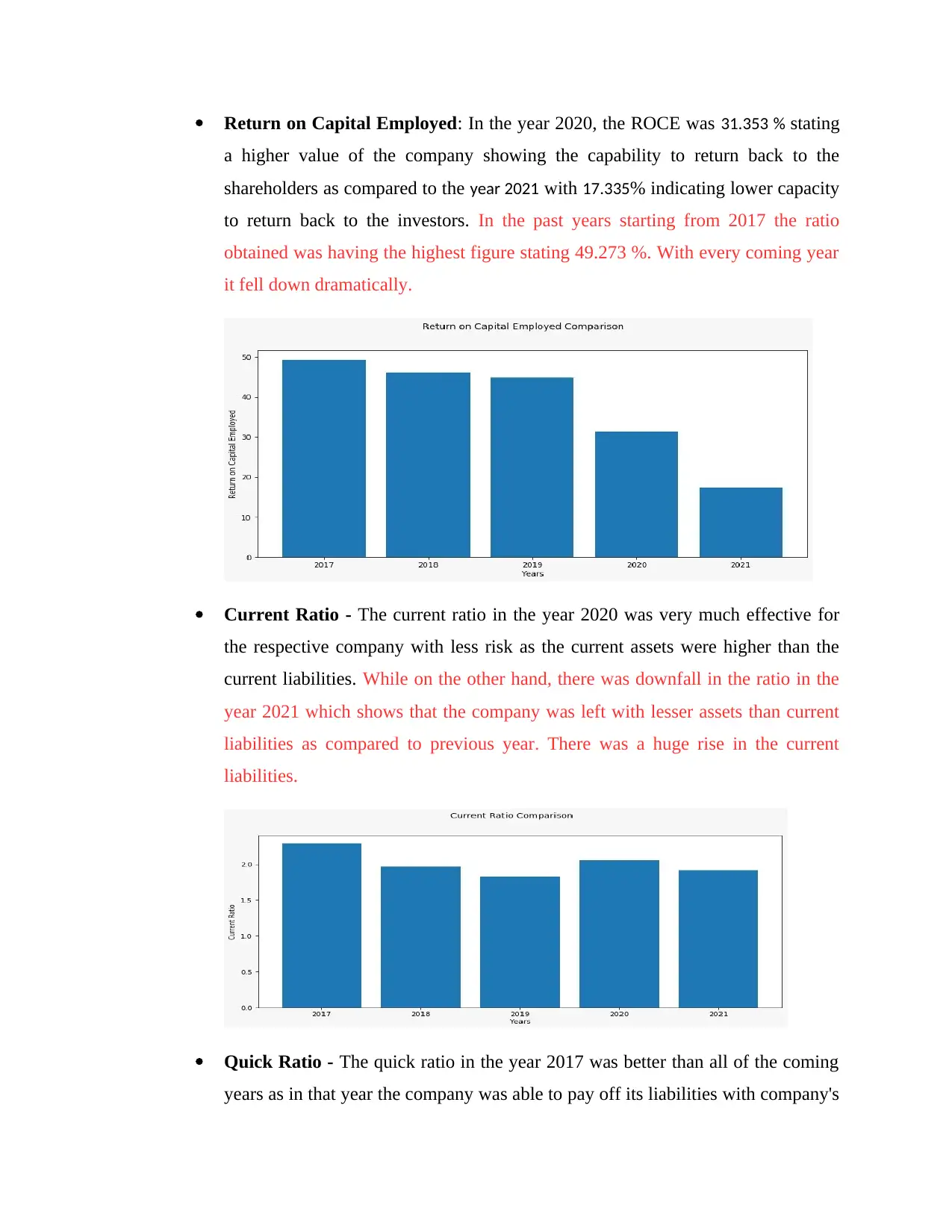

Return on Capital Employed: In the year 2020, the ROCE was 31.353 % stating

a higher value of the company showing the capability to return back to the

shareholders as compared to the year 2021 with 17.335% indicating lower capacity

to return back to the investors. In the past years starting from 2017 the ratio

obtained was having the highest figure stating 49.273 %. With every coming year

it fell down dramatically.

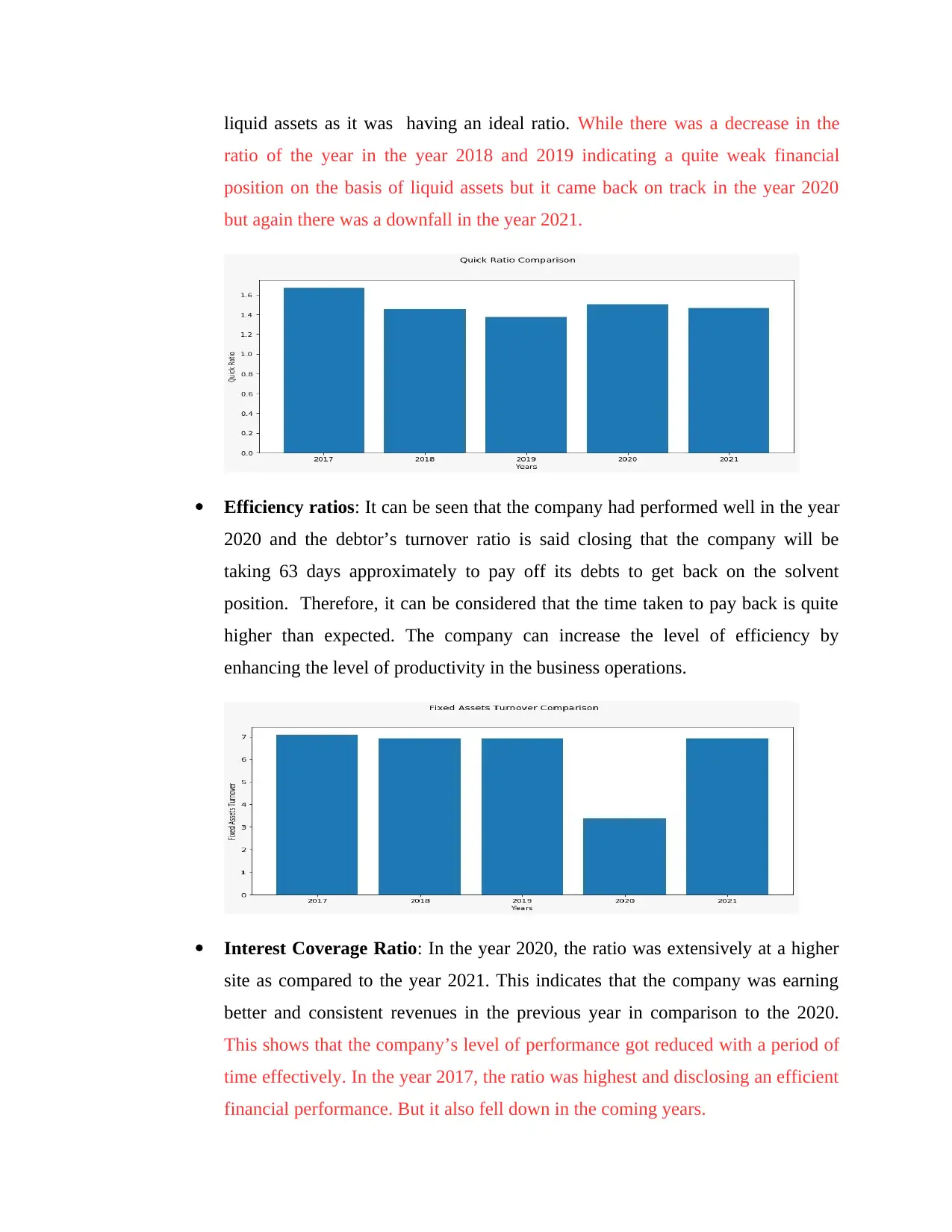

Current Ratio - The current ratio in the year 2020 was very much effective for

the respective company with less risk as the current assets were higher than the

current liabilities. While on the other hand, there was downfall in the ratio in the

year 2021 which shows that the company was left with lesser assets than current

liabilities as compared to previous year. There was a huge rise in the current

liabilities.

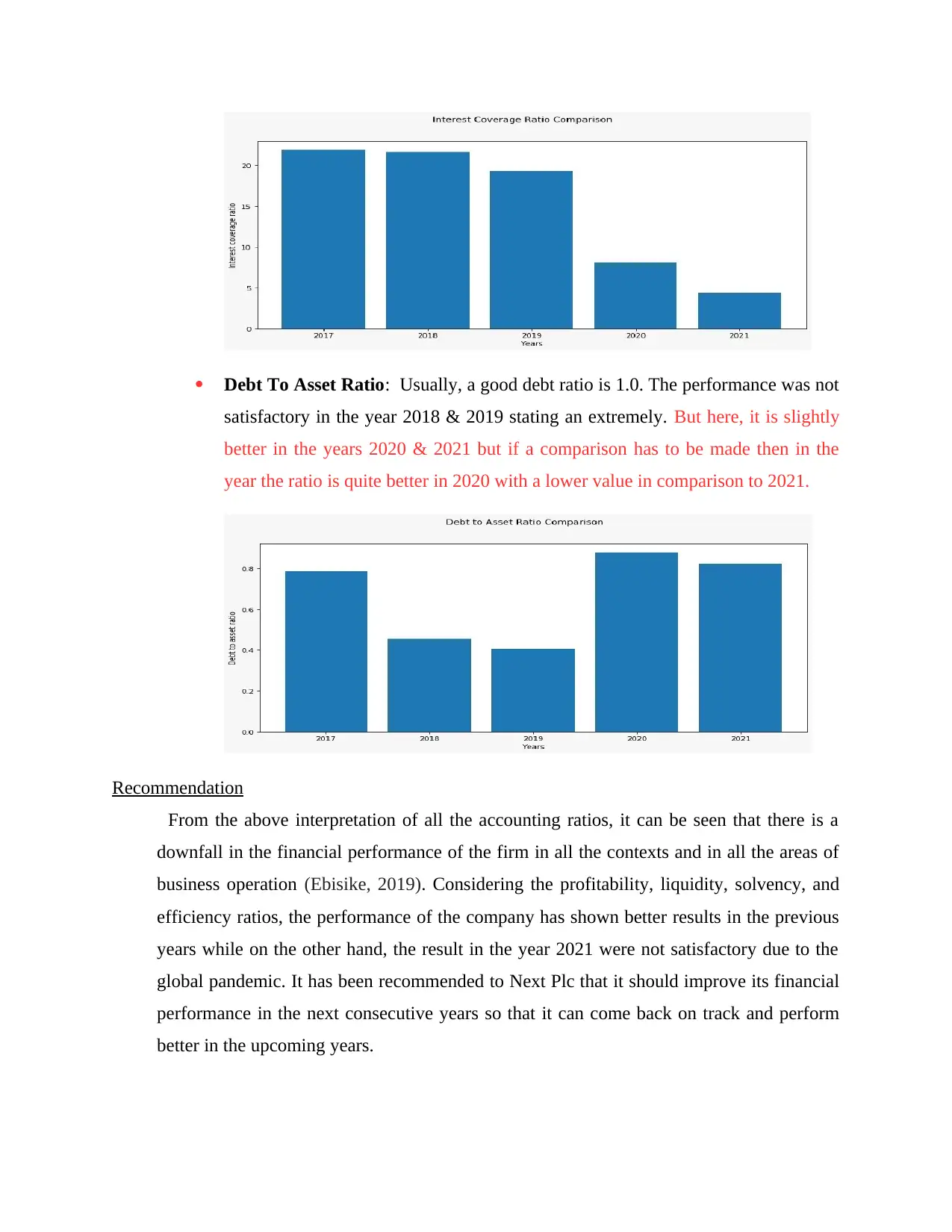

Quick Ratio - The quick ratio in the year 2017 was better than all of the coming

years as in that year the company was able to pay off its liabilities with company's

a higher value of the company showing the capability to return back to the

shareholders as compared to the year 2021 with 17.335% indicating lower capacity

to return back to the investors. In the past years starting from 2017 the ratio

obtained was having the highest figure stating 49.273 %. With every coming year

it fell down dramatically.

Current Ratio - The current ratio in the year 2020 was very much effective for

the respective company with less risk as the current assets were higher than the

current liabilities. While on the other hand, there was downfall in the ratio in the

year 2021 which shows that the company was left with lesser assets than current

liabilities as compared to previous year. There was a huge rise in the current

liabilities.

Quick Ratio - The quick ratio in the year 2017 was better than all of the coming

years as in that year the company was able to pay off its liabilities with company's

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

liquid assets as it was having an ideal ratio. While there was a decrease in the

ratio of the year in the year 2018 and 2019 indicating a quite weak financial

position on the basis of liquid assets but it came back on track in the year 2020

but again there was a downfall in the year 2021.

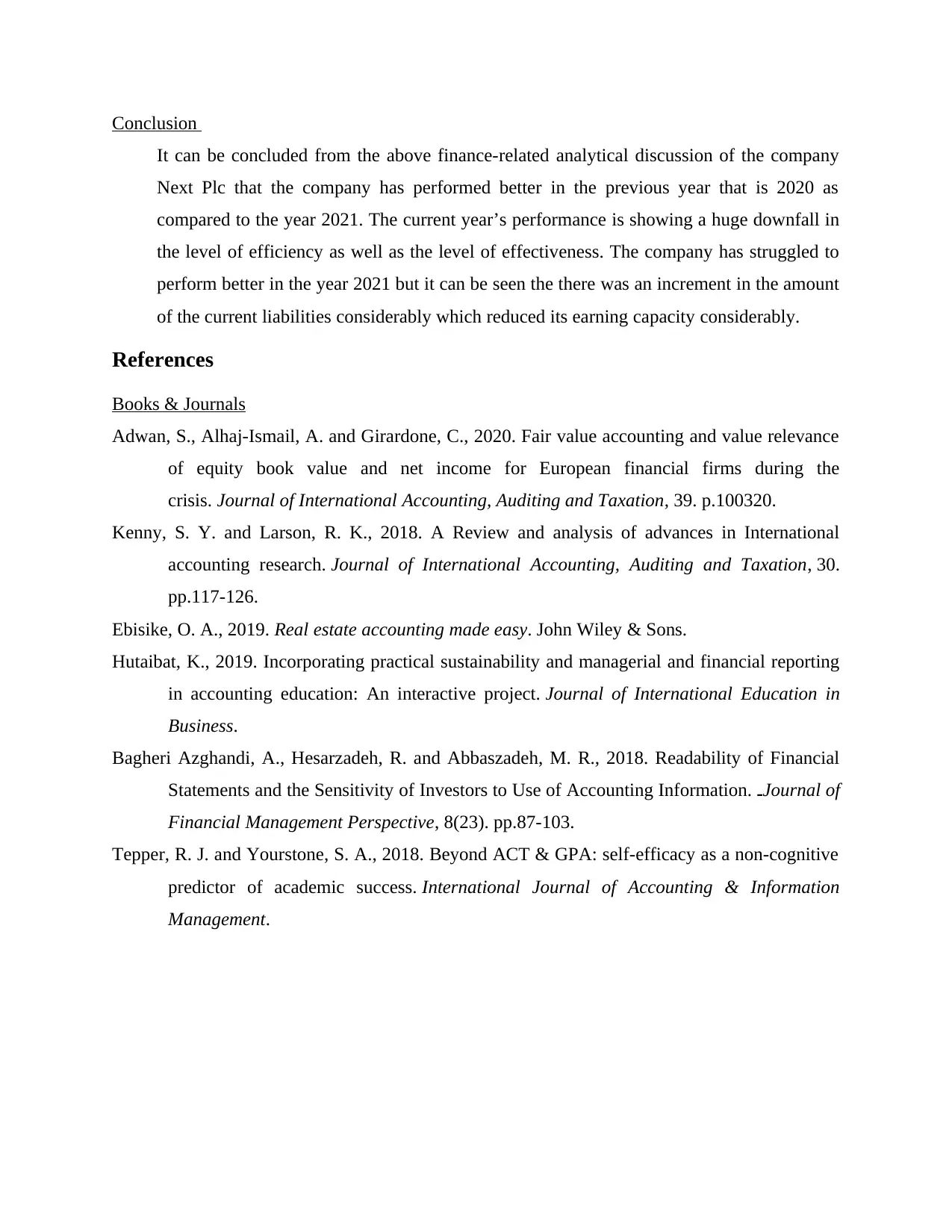

Efficiency ratios: It can be seen that the company had performed well in the year

2020 and the debtor’s turnover ratio is said closing that the company will be

taking 63 days approximately to pay off its debts to get back on the solvent

position. Therefore, it can be considered that the time taken to pay back is quite

higher than expected. The company can increase the level of efficiency by

enhancing the level of productivity in the business operations.

Interest Coverage Ratio: In the year 2020, the ratio was extensively at a higher

site as compared to the year 2021. This indicates that the company was earning

better and consistent revenues in the previous year in comparison to the 2020.

This shows that the company’s level of performance got reduced with a period of

time effectively. In the year 2017, the ratio was highest and disclosing an efficient

financial performance. But it also fell down in the coming years.

ratio of the year in the year 2018 and 2019 indicating a quite weak financial

position on the basis of liquid assets but it came back on track in the year 2020

but again there was a downfall in the year 2021.

Efficiency ratios: It can be seen that the company had performed well in the year

2020 and the debtor’s turnover ratio is said closing that the company will be

taking 63 days approximately to pay off its debts to get back on the solvent

position. Therefore, it can be considered that the time taken to pay back is quite

higher than expected. The company can increase the level of efficiency by

enhancing the level of productivity in the business operations.

Interest Coverage Ratio: In the year 2020, the ratio was extensively at a higher

site as compared to the year 2021. This indicates that the company was earning

better and consistent revenues in the previous year in comparison to the 2020.

This shows that the company’s level of performance got reduced with a period of

time effectively. In the year 2017, the ratio was highest and disclosing an efficient

financial performance. But it also fell down in the coming years.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Debt To Asset Ratio: Usually, a good debt ratio is 1.0. The performance was not

satisfactory in the year 2018 & 2019 stating an extremely. But here, it is slightly

better in the years 2020 & 2021 but if a comparison has to be made then in the

year the ratio is quite better in 2020 with a lower value in comparison to 2021.

Recommendation

From the above interpretation of all the accounting ratios, it can be seen that there is a

downfall in the financial performance of the firm in all the contexts and in all the areas of

business operation (Ebisike, 2019). Considering the profitability, liquidity, solvency, and

efficiency ratios, the performance of the company has shown better results in the previous

years while on the other hand, the result in the year 2021 were not satisfactory due to the

global pandemic. It has been recommended to Next Plc that it should improve its financial

performance in the next consecutive years so that it can come back on track and perform

better in the upcoming years.

satisfactory in the year 2018 & 2019 stating an extremely. But here, it is slightly

better in the years 2020 & 2021 but if a comparison has to be made then in the

year the ratio is quite better in 2020 with a lower value in comparison to 2021.

Recommendation

From the above interpretation of all the accounting ratios, it can be seen that there is a

downfall in the financial performance of the firm in all the contexts and in all the areas of

business operation (Ebisike, 2019). Considering the profitability, liquidity, solvency, and

efficiency ratios, the performance of the company has shown better results in the previous

years while on the other hand, the result in the year 2021 were not satisfactory due to the

global pandemic. It has been recommended to Next Plc that it should improve its financial

performance in the next consecutive years so that it can come back on track and perform

better in the upcoming years.

Conclusion

It can be concluded from the above finance-related analytical discussion of the company

Next Plc that the company has performed better in the previous year that is 2020 as

compared to the year 2021. The current year’s performance is showing a huge downfall in

the level of efficiency as well as the level of effectiveness. The company has struggled to

perform better in the year 2021 but it can be seen the there was an increment in the amount

of the current liabilities considerably which reduced its earning capacity considerably.

References

Books & Journals

Adwan, S., Alhaj-Ismail, A. and Girardone, C., 2020. Fair value accounting and value relevance

of equity book value and net income for European financial firms during the

crisis. Journal of International Accounting, Auditing and Taxation, 39. p.100320.

Kenny, S. Y. and Larson, R. K., 2018. A Review and analysis of advances in International

accounting research. Journal of International Accounting, Auditing and Taxation, 30.

pp.117-126.

Ebisike, O. A., 2019. Real estate accounting made easy. John Wiley & Sons.

Hutaibat, K., 2019. Incorporating practical sustainability and managerial and financial reporting

in accounting education: An interactive project. Journal of International Education in

Business.

Bagheri Azghandi, A., Hesarzadeh, R. and Abbaszadeh, M. R., 2018. Readability of Financial

Statements and the Sensitivity of Investors to Use of Accounting Information. ـJournal of

Financial Management Perspective, 8(23). pp.87-103.

Tepper, R. J. and Yourstone, S. A., 2018. Beyond ACT & GPA: self-efficacy as a non-cognitive

predictor of academic success. International Journal of Accounting & Information

Management.

It can be concluded from the above finance-related analytical discussion of the company

Next Plc that the company has performed better in the previous year that is 2020 as

compared to the year 2021. The current year’s performance is showing a huge downfall in

the level of efficiency as well as the level of effectiveness. The company has struggled to

perform better in the year 2021 but it can be seen the there was an increment in the amount

of the current liabilities considerably which reduced its earning capacity considerably.

References

Books & Journals

Adwan, S., Alhaj-Ismail, A. and Girardone, C., 2020. Fair value accounting and value relevance

of equity book value and net income for European financial firms during the

crisis. Journal of International Accounting, Auditing and Taxation, 39. p.100320.

Kenny, S. Y. and Larson, R. K., 2018. A Review and analysis of advances in International

accounting research. Journal of International Accounting, Auditing and Taxation, 30.

pp.117-126.

Ebisike, O. A., 2019. Real estate accounting made easy. John Wiley & Sons.

Hutaibat, K., 2019. Incorporating practical sustainability and managerial and financial reporting

in accounting education: An interactive project. Journal of International Education in

Business.

Bagheri Azghandi, A., Hesarzadeh, R. and Abbaszadeh, M. R., 2018. Readability of Financial

Statements and the Sensitivity of Investors to Use of Accounting Information. ـJournal of

Financial Management Perspective, 8(23). pp.87-103.

Tepper, R. J. and Yourstone, S. A., 2018. Beyond ACT & GPA: self-efficacy as a non-cognitive

predictor of academic success. International Journal of Accounting & Information

Management.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Appendix

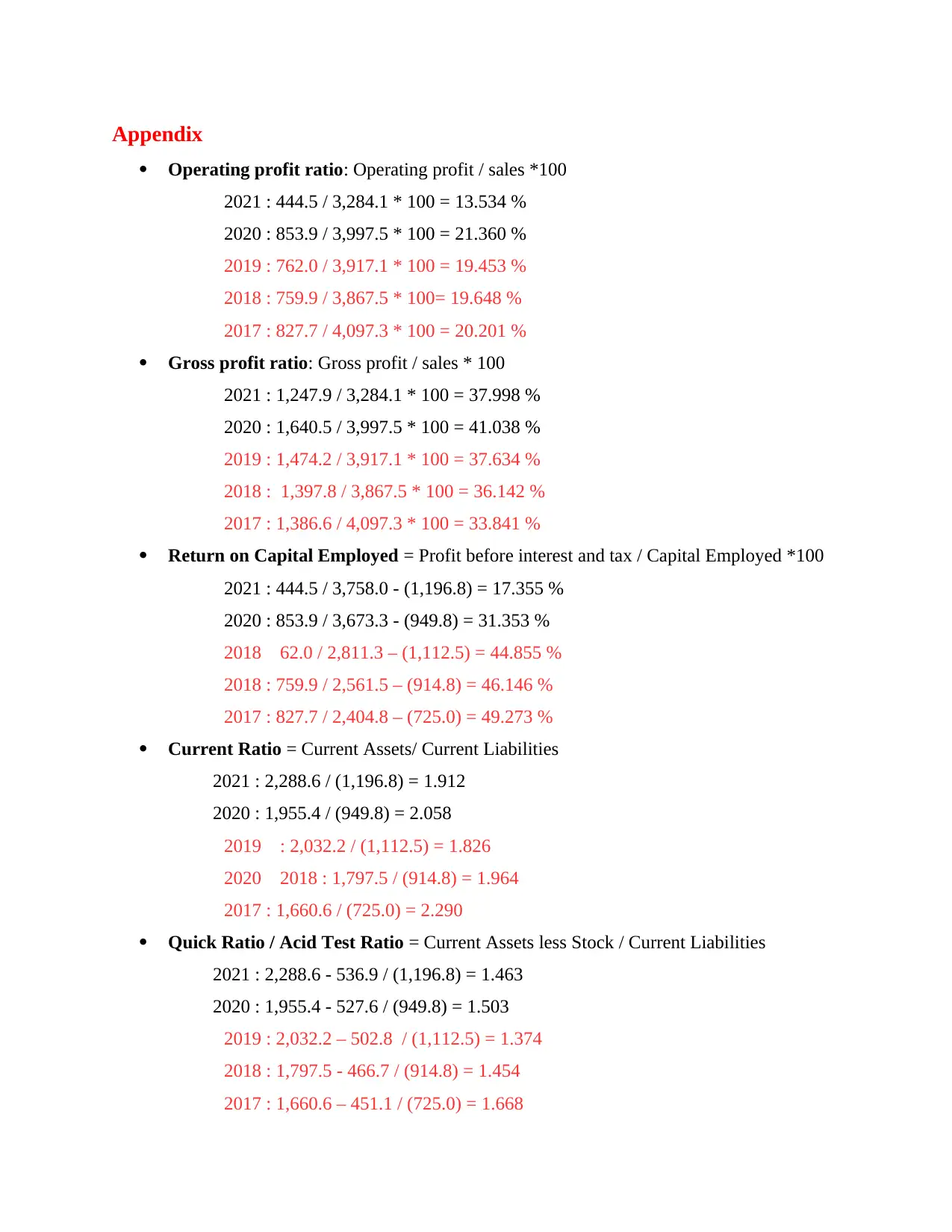

Operating profit ratio: Operating profit / sales *100

2021 : 444.5 / 3,284.1 * 100 = 13.534 %

2020 : 853.9 / 3,997.5 * 100 = 21.360 %

2019 : 762.0 / 3,917.1 * 100 = 19.453 %

2018 : 759.9 / 3,867.5 * 100= 19.648 %

2017 : 827.7 / 4,097.3 * 100 = 20.201 %

Gross profit ratio: Gross profit / sales * 100

2021 : 1,247.9 / 3,284.1 * 100 = 37.998 %

2020 : 1,640.5 / 3,997.5 * 100 = 41.038 %

2019 : 1,474.2 / 3,917.1 * 100 = 37.634 %

2018 : 1,397.8 / 3,867.5 * 100 = 36.142 %

2017 : 1,386.6 / 4,097.3 * 100 = 33.841 %

Return on Capital Employed = Profit before interest and tax / Capital Employed *100

2021 : 444.5 / 3,758.0 - (1,196.8) = 17.355 %

2020 : 853.9 / 3,673.3 - (949.8) = 31.353 %

2018 62.0 / 2,811.3 – (1,112.5) = 44.855 %

2018 : 759.9 / 2,561.5 – (914.8) = 46.146 %

2017 : 827.7 / 2,404.8 – (725.0) = 49.273 %

Current Ratio = Current Assets/ Current Liabilities

2021 : 2,288.6 / (1,196.8) = 1.912

2020 : 1,955.4 / (949.8) = 2.058

2019 : 2,032.2 / (1,112.5) = 1.826

2020 2018 : 1,797.5 / (914.8) = 1.964

2017 : 1,660.6 / (725.0) = 2.290

Quick Ratio / Acid Test Ratio = Current Assets less Stock / Current Liabilities

2021 : 2,288.6 - 536.9 / (1,196.8) = 1.463

2020 : 1,955.4 - 527.6 / (949.8) = 1.503

2019 : 2,032.2 – 502.8 / (1,112.5) = 1.374

2018 : 1,797.5 - 466.7 / (914.8) = 1.454

2017 : 1,660.6 – 451.1 / (725.0) = 1.668

Operating profit ratio: Operating profit / sales *100

2021 : 444.5 / 3,284.1 * 100 = 13.534 %

2020 : 853.9 / 3,997.5 * 100 = 21.360 %

2019 : 762.0 / 3,917.1 * 100 = 19.453 %

2018 : 759.9 / 3,867.5 * 100= 19.648 %

2017 : 827.7 / 4,097.3 * 100 = 20.201 %

Gross profit ratio: Gross profit / sales * 100

2021 : 1,247.9 / 3,284.1 * 100 = 37.998 %

2020 : 1,640.5 / 3,997.5 * 100 = 41.038 %

2019 : 1,474.2 / 3,917.1 * 100 = 37.634 %

2018 : 1,397.8 / 3,867.5 * 100 = 36.142 %

2017 : 1,386.6 / 4,097.3 * 100 = 33.841 %

Return on Capital Employed = Profit before interest and tax / Capital Employed *100

2021 : 444.5 / 3,758.0 - (1,196.8) = 17.355 %

2020 : 853.9 / 3,673.3 - (949.8) = 31.353 %

2018 62.0 / 2,811.3 – (1,112.5) = 44.855 %

2018 : 759.9 / 2,561.5 – (914.8) = 46.146 %

2017 : 827.7 / 2,404.8 – (725.0) = 49.273 %

Current Ratio = Current Assets/ Current Liabilities

2021 : 2,288.6 / (1,196.8) = 1.912

2020 : 1,955.4 / (949.8) = 2.058

2019 : 2,032.2 / (1,112.5) = 1.826

2020 2018 : 1,797.5 / (914.8) = 1.964

2017 : 1,660.6 / (725.0) = 2.290

Quick Ratio / Acid Test Ratio = Current Assets less Stock / Current Liabilities

2021 : 2,288.6 - 536.9 / (1,196.8) = 1.463

2020 : 1,955.4 - 527.6 / (949.8) = 1.503

2019 : 2,032.2 – 502.8 / (1,112.5) = 1.374

2018 : 1,797.5 - 466.7 / (914.8) = 1.454

2017 : 1,660.6 – 451.1 / (725.0) = 1.668

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

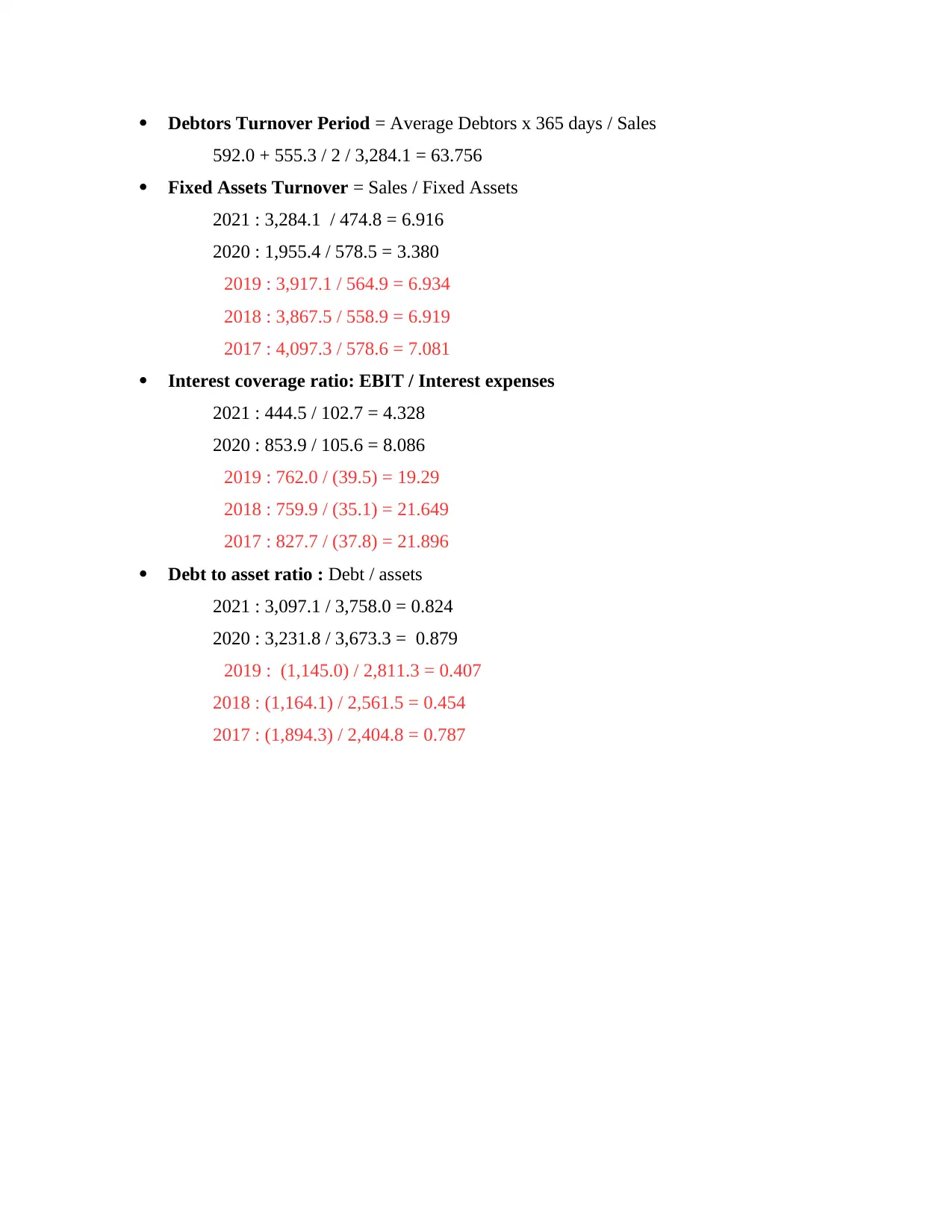

Debtors Turnover Period = Average Debtors x 365 days / Sales

592.0 + 555.3 / 2 / 3,284.1 = 63.756

Fixed Assets Turnover = Sales / Fixed Assets

2021 : 3,284.1 / 474.8 = 6.916

2020 : 1,955.4 / 578.5 = 3.380

2019 : 3,917.1 / 564.9 = 6.934

2018 : 3,867.5 / 558.9 = 6.919

2017 : 4,097.3 / 578.6 = 7.081

Interest coverage ratio: EBIT / Interest expenses

2021 : 444.5 / 102.7 = 4.328

2020 : 853.9 / 105.6 = 8.086

2019 : 762.0 / (39.5) = 19.29

2018 : 759.9 / (35.1) = 21.649

2017 : 827.7 / (37.8) = 21.896

Debt to asset ratio : Debt / assets

2021 : 3,097.1 / 3,758.0 = 0.824

2020 : 3,231.8 / 3,673.3 = 0.879

2019 : (1,145.0) / 2,811.3 = 0.407

2018 : (1,164.1) / 2,561.5 = 0.454

2017 : (1,894.3) / 2,404.8 = 0.787

592.0 + 555.3 / 2 / 3,284.1 = 63.756

Fixed Assets Turnover = Sales / Fixed Assets

2021 : 3,284.1 / 474.8 = 6.916

2020 : 1,955.4 / 578.5 = 3.380

2019 : 3,917.1 / 564.9 = 6.934

2018 : 3,867.5 / 558.9 = 6.919

2017 : 4,097.3 / 578.6 = 7.081

Interest coverage ratio: EBIT / Interest expenses

2021 : 444.5 / 102.7 = 4.328

2020 : 853.9 / 105.6 = 8.086

2019 : 762.0 / (39.5) = 19.29

2018 : 759.9 / (35.1) = 21.649

2017 : 827.7 / (37.8) = 21.896

Debt to asset ratio : Debt / assets

2021 : 3,097.1 / 3,758.0 = 0.824

2020 : 3,231.8 / 3,673.3 = 0.879

2019 : (1,145.0) / 2,811.3 = 0.407

2018 : (1,164.1) / 2,561.5 = 0.454

2017 : (1,894.3) / 2,404.8 = 0.787

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.