ACCG224: Financial Accounting Policies and Estimates Report, S2 2019

VerifiedAdded on 2022/10/17

|9

|1716

|40

Report

AI Summary

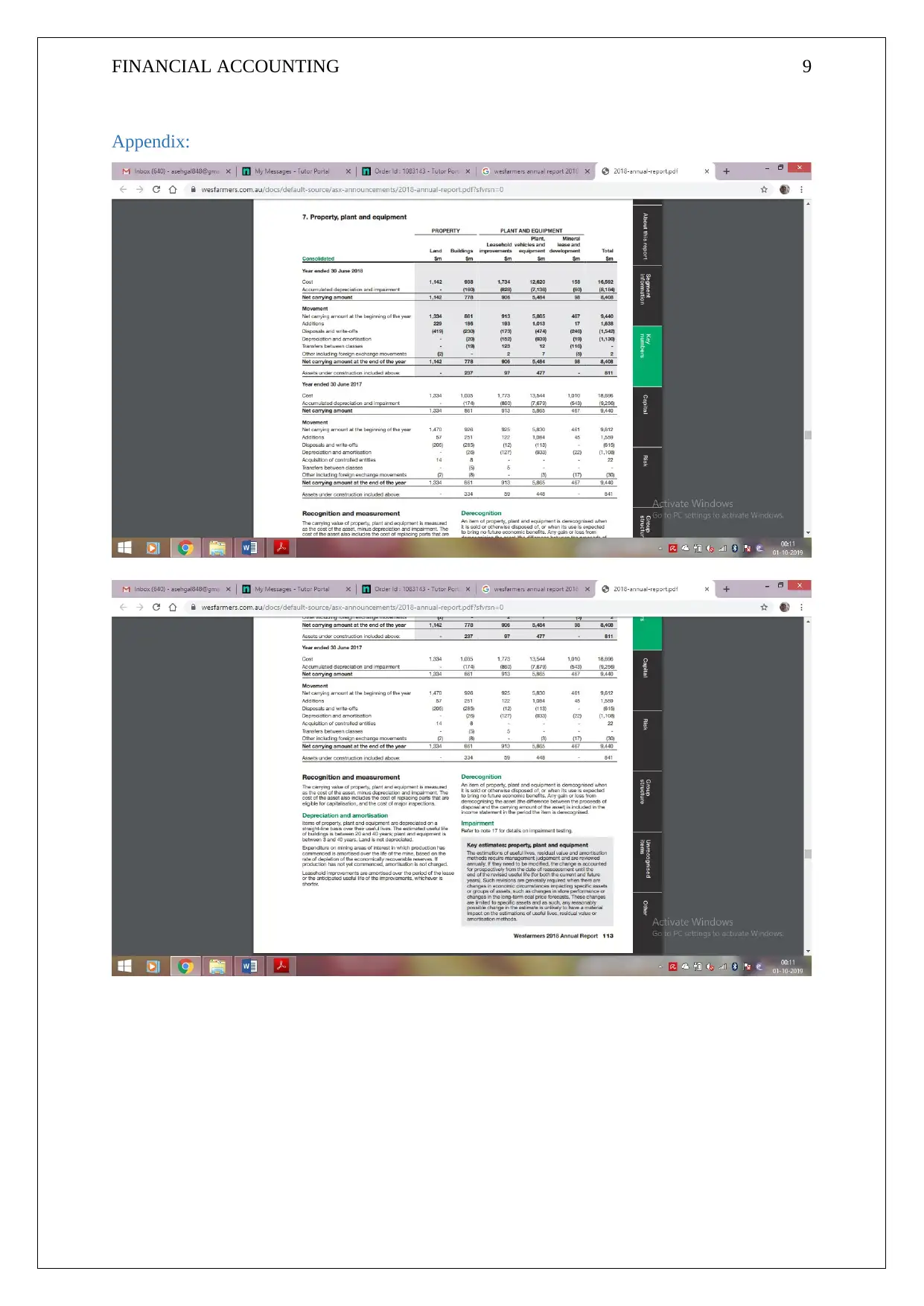

This report provides an in-depth analysis of accounting policies and estimates, specifically focusing on the requirements of AASB 108, changes in accounting policies, and their practical application within financial accounting. The report discusses the selection criteria for accounting policies and estimates, emphasizing the importance of professional judgment in financial reporting. It examines the accounting policy of Wesfarmers Limited concerning property, plant, and equipment, including depreciation methods, useful lives, and the treatment of impairments. The report also highlights potential improvements in accounting practices, such as considering legal limits on asset use and consulting external sources for determining asset values. Furthermore, it explores the impact of changes in accounting estimates on financial statements and the importance of providing relevant and reliable information to decision-makers. The report concludes by emphasizing the significance of adhering to relevant accounting standards and the need for fair disclosure in financial statements.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.