Financial Accounting Assignment: Financial Analysis and Client Cases

VerifiedAdded on 2020/10/05

|22

|4380

|420

Homework Assignment

AI Summary

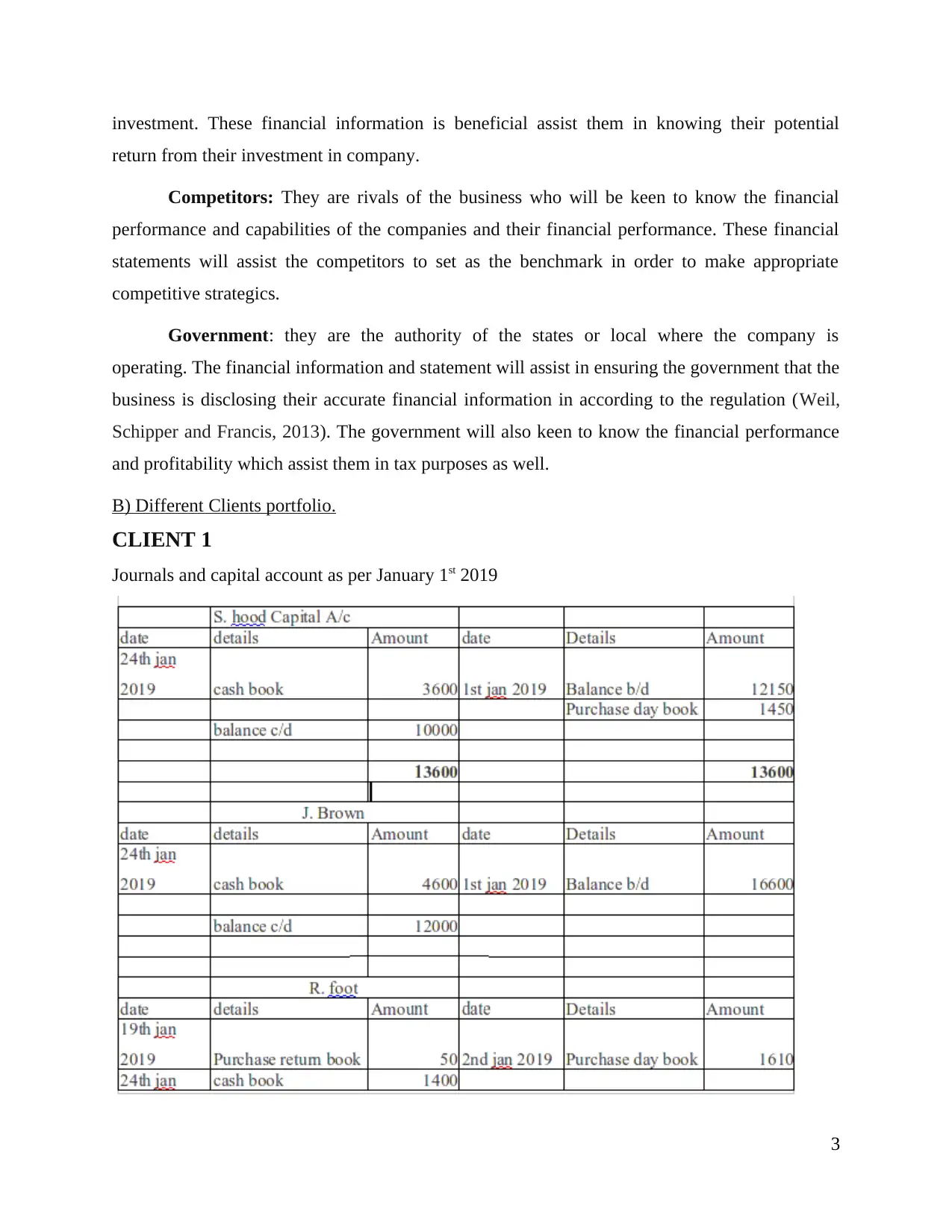

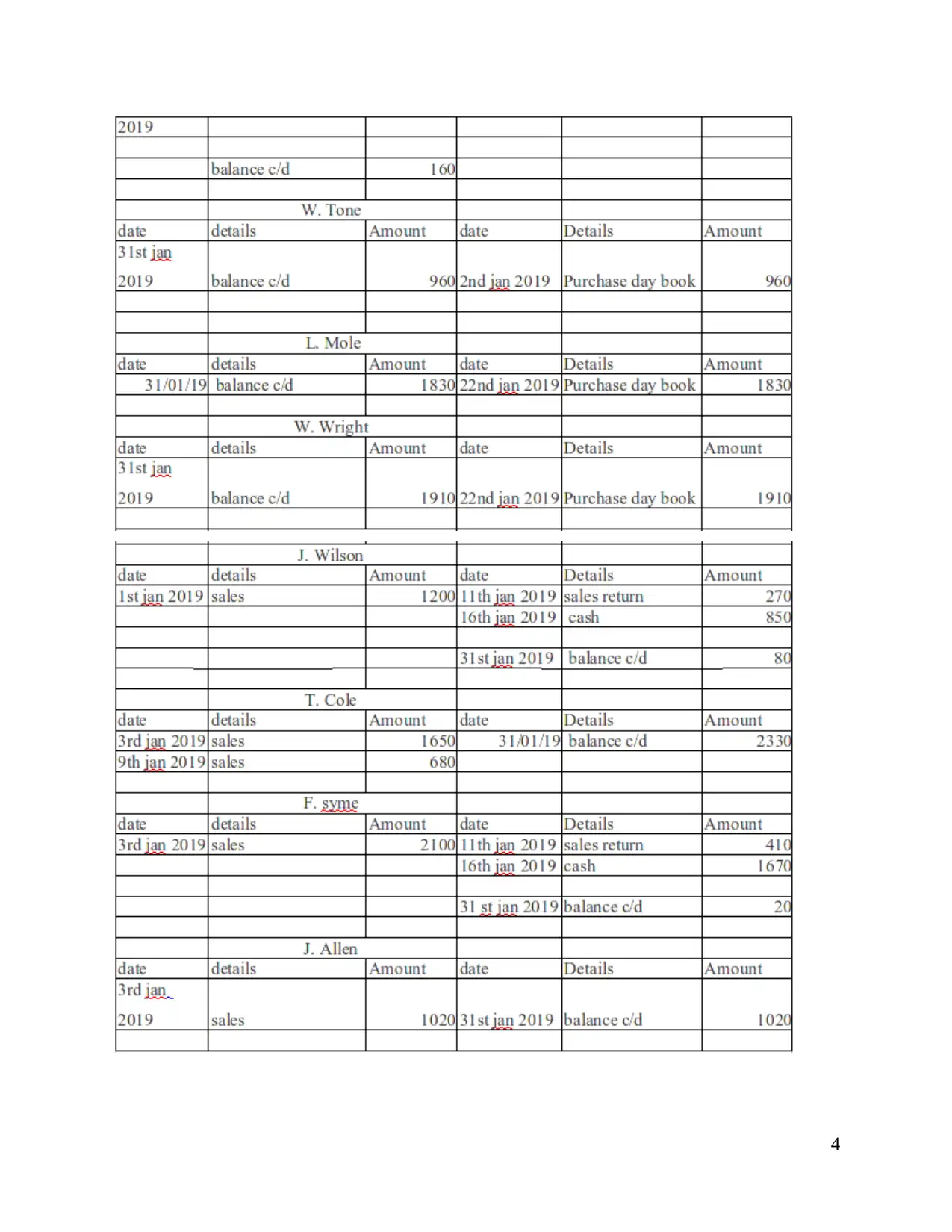

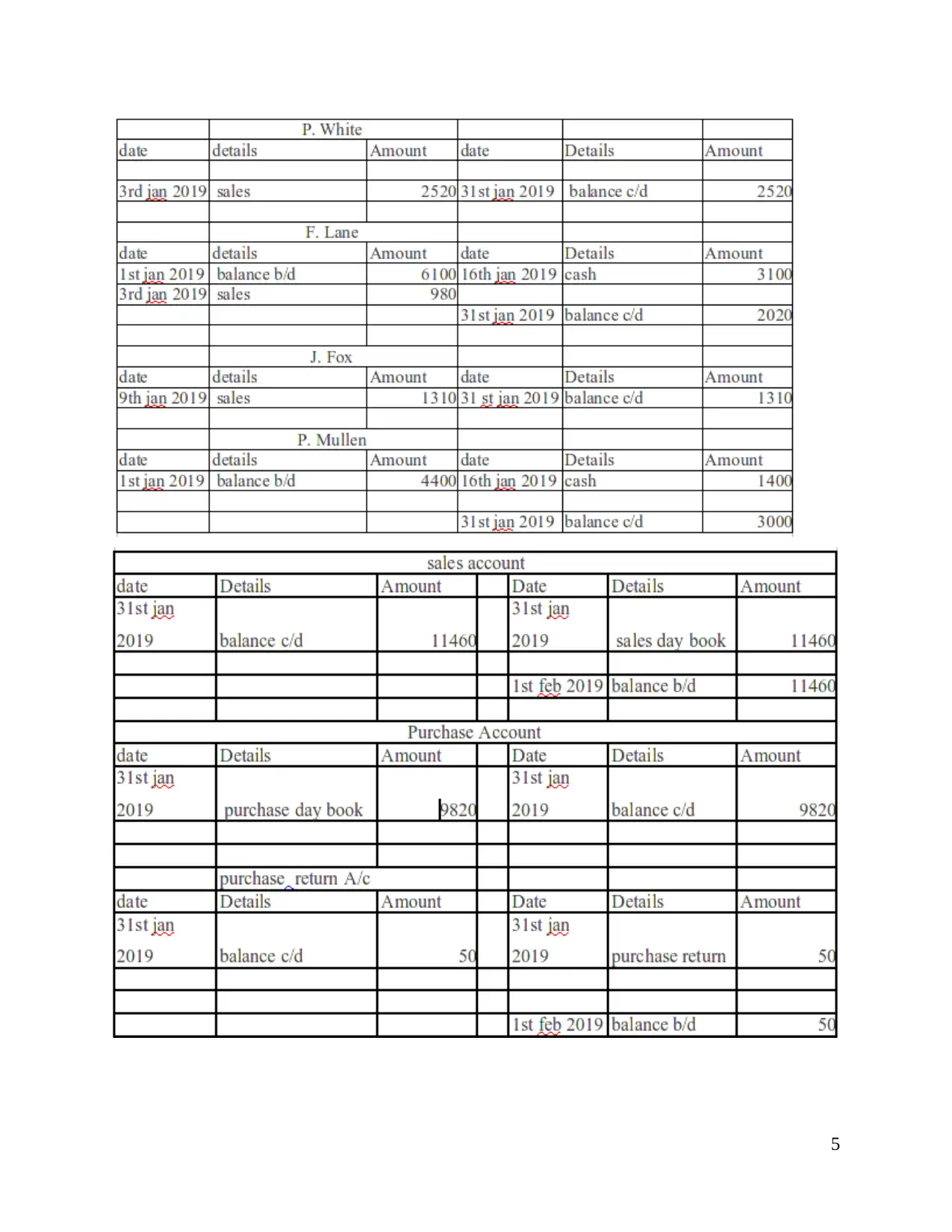

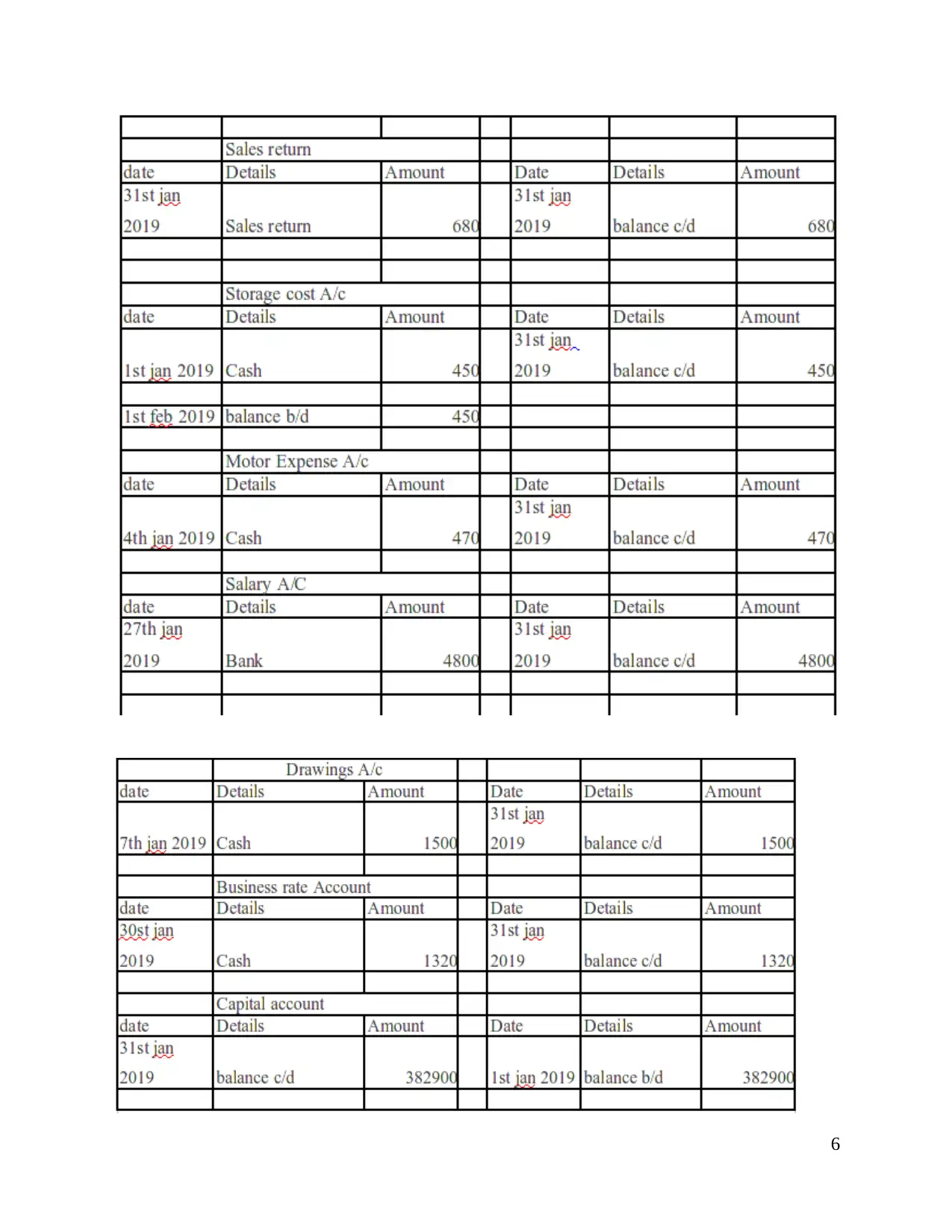

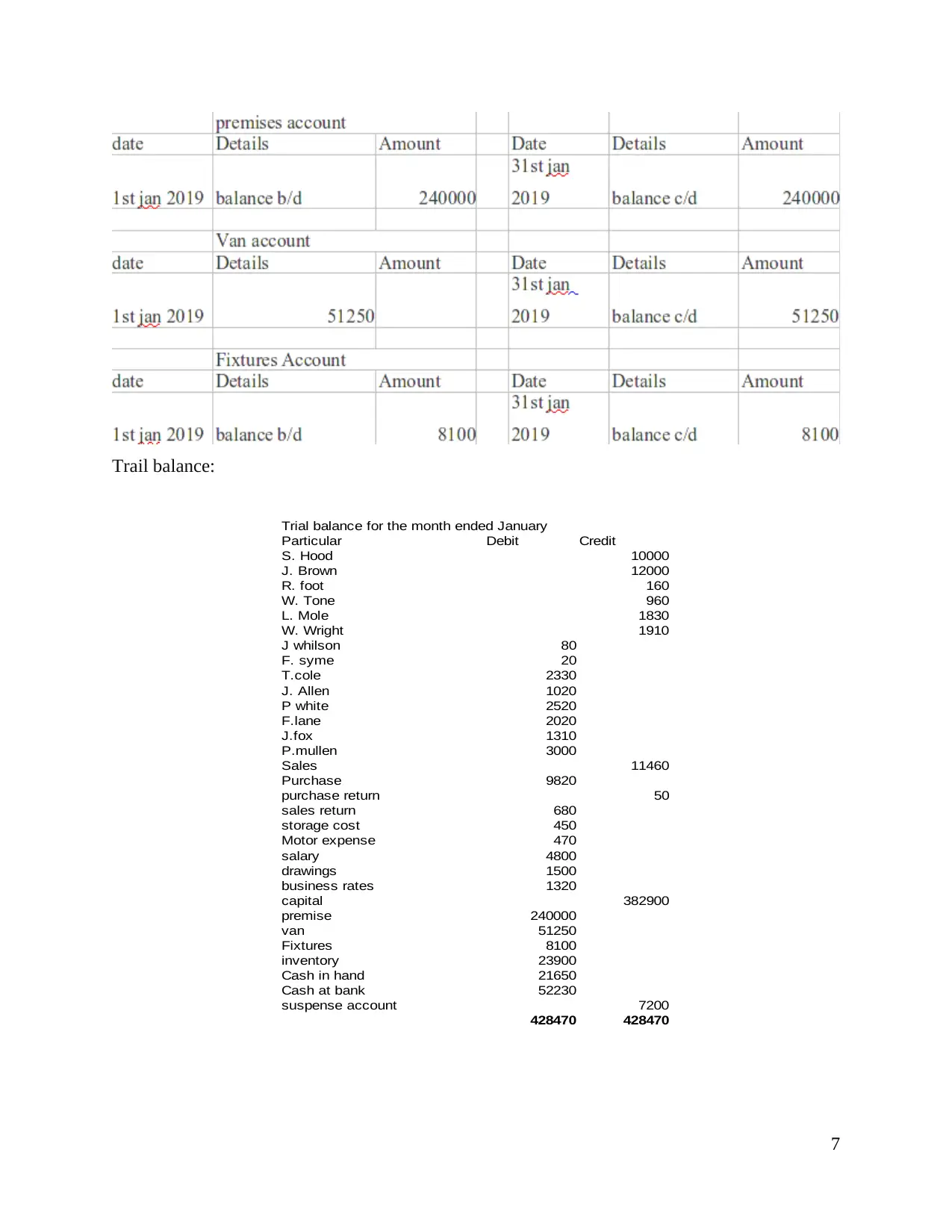

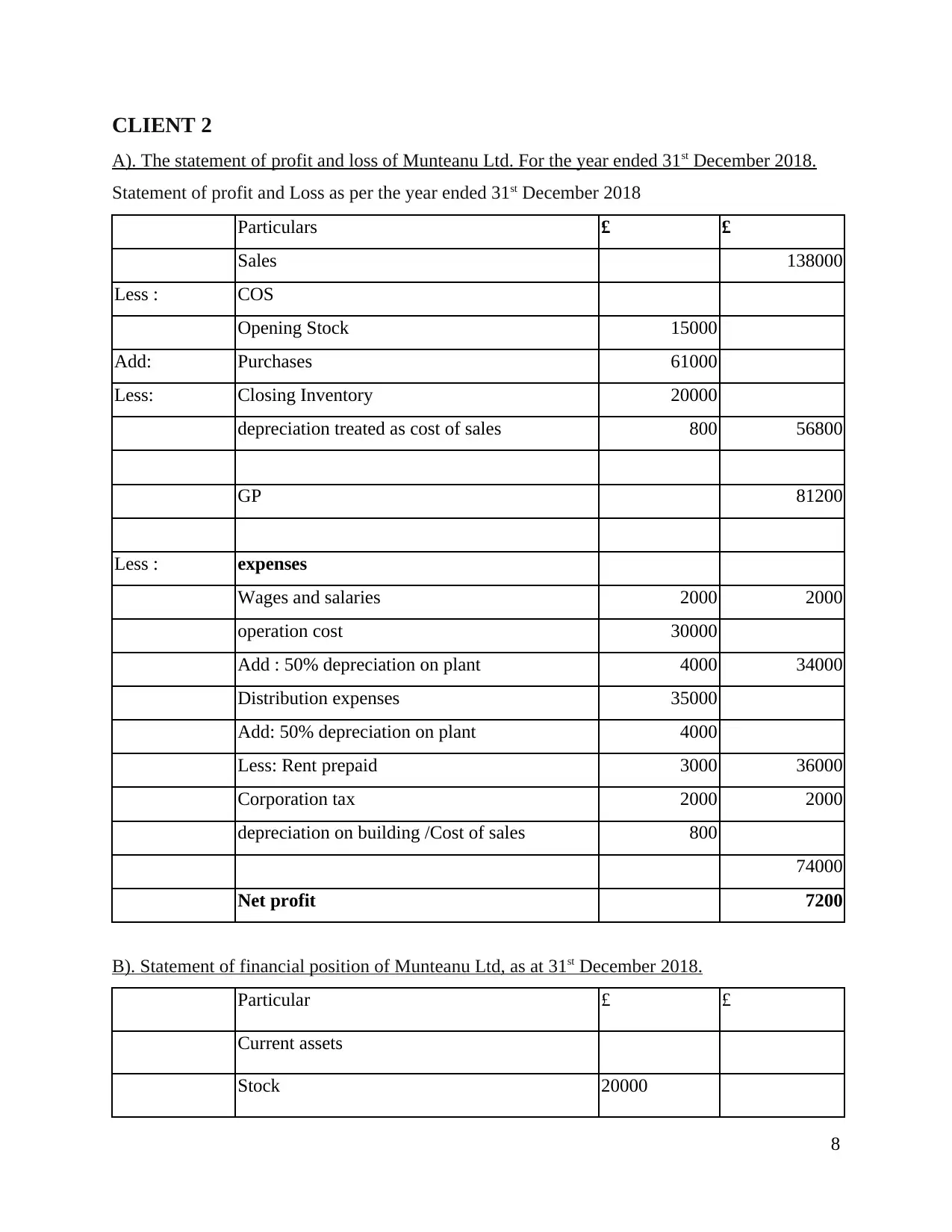

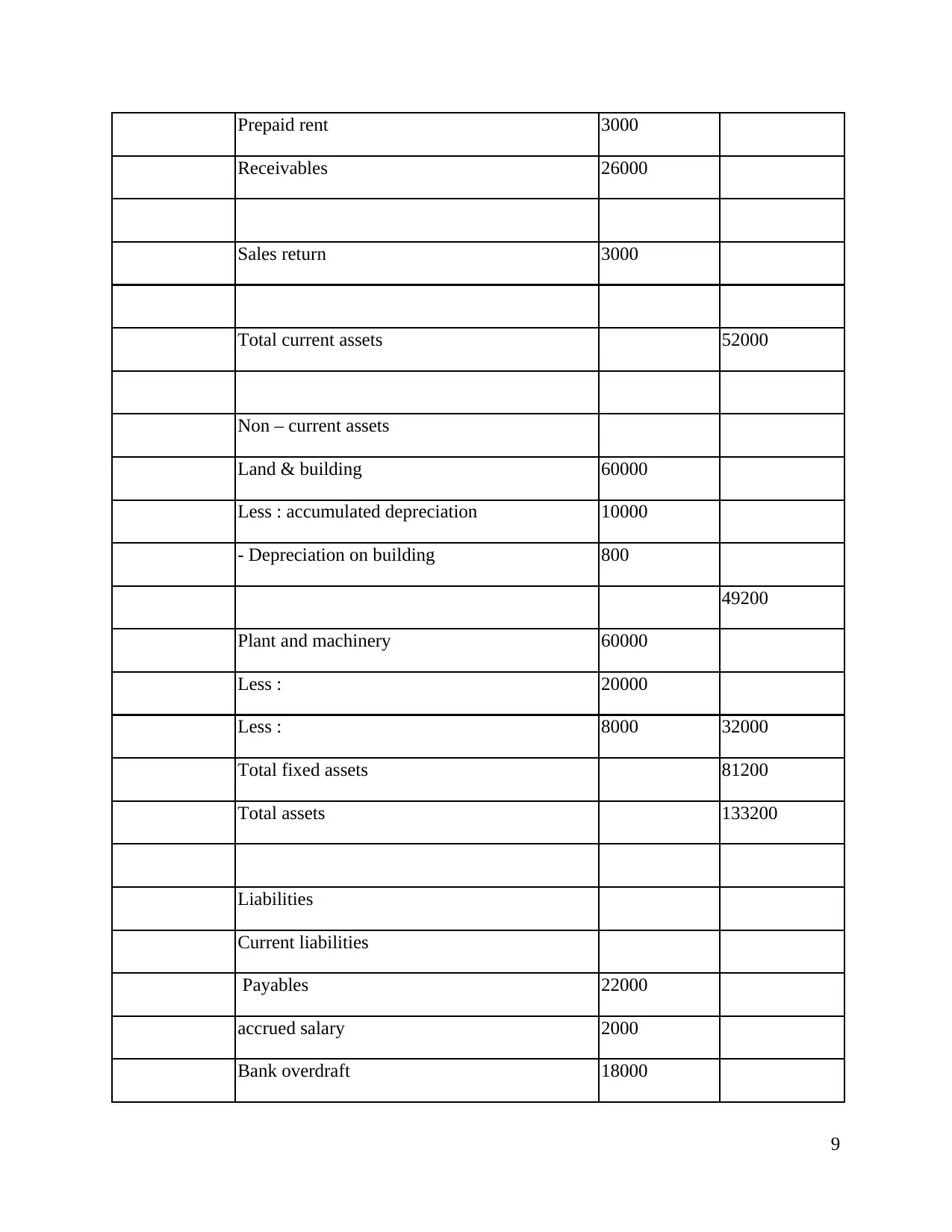

This financial accounting assignment provides a comprehensive overview of key concepts and practical applications. It begins with an introduction to financial accounting and its purpose, followed by an analysis of internal and external stakeholders of Marks and Spencer. The assignment then delves into various client portfolios, including journals, capital accounts, and trial balances. It includes the statement of profit and loss and statement of financial position for Munteanu Ltd. The assignment further explores accounting concepts such as consistency and prudency, the purpose of depreciation, and the differences between financial statements of sole traders and limited companies. It also covers bank reconciliation statements, areas causing deviations in bank records, the term "imprest" in petty cash statements, and updates to a cash book and bank reconciliation statement for Burcu Ltd. The assignment concludes with an examination of purchase ledger accounts and suspense accounts, and a trial balance using a control account.

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.