Financial Accounting Principles: A Detailed Client Portfolio Review

VerifiedAdded on 2024/06/07

|28

|2406

|157

Report

AI Summary

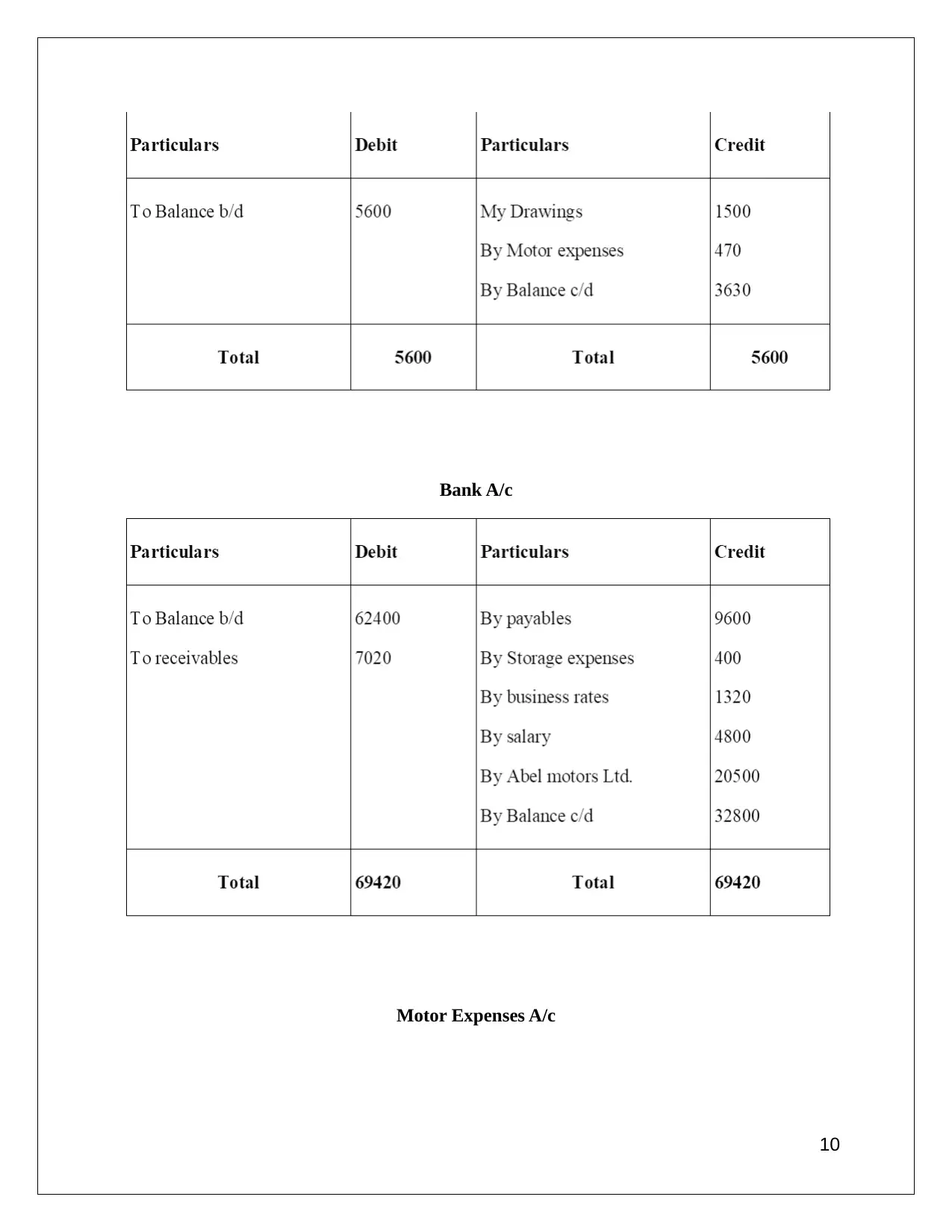

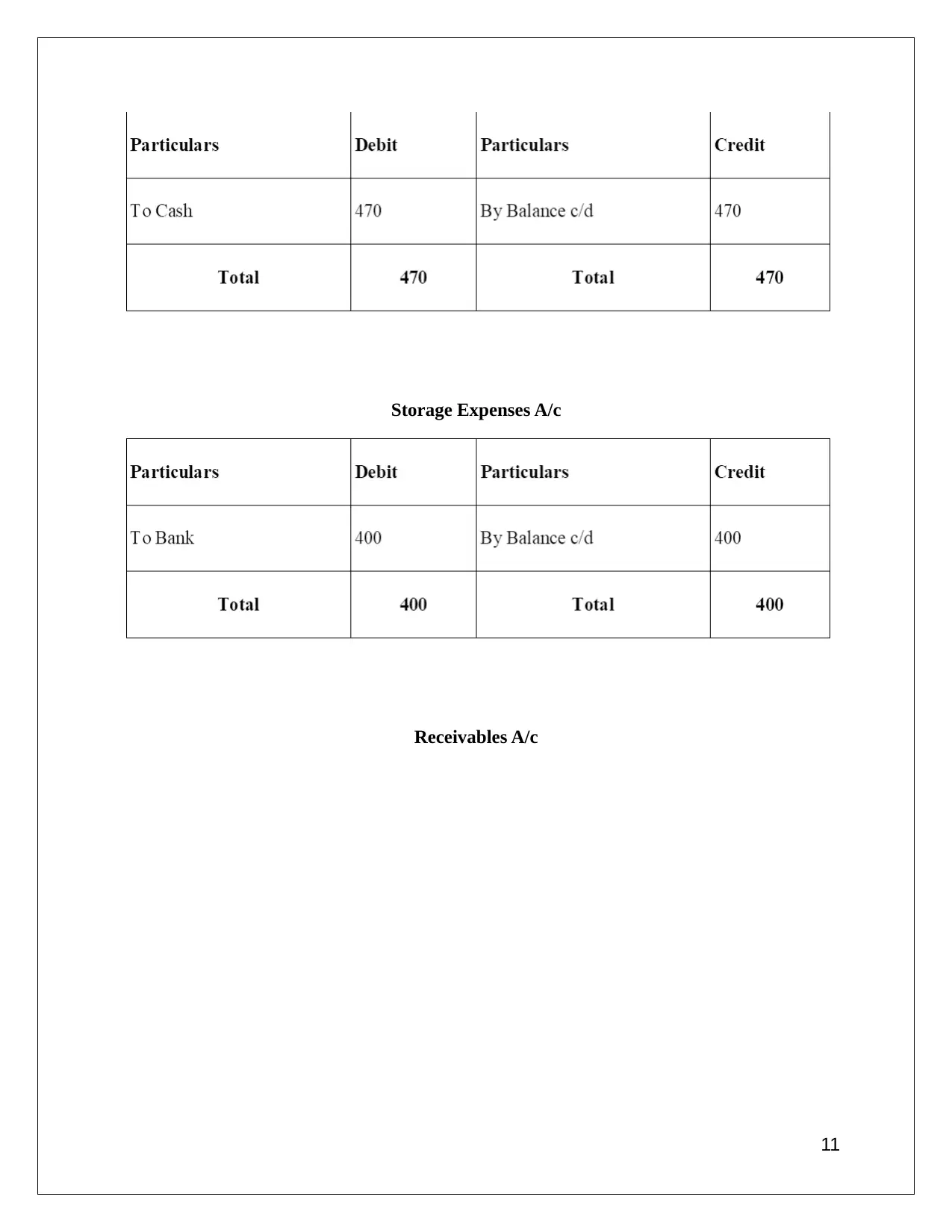

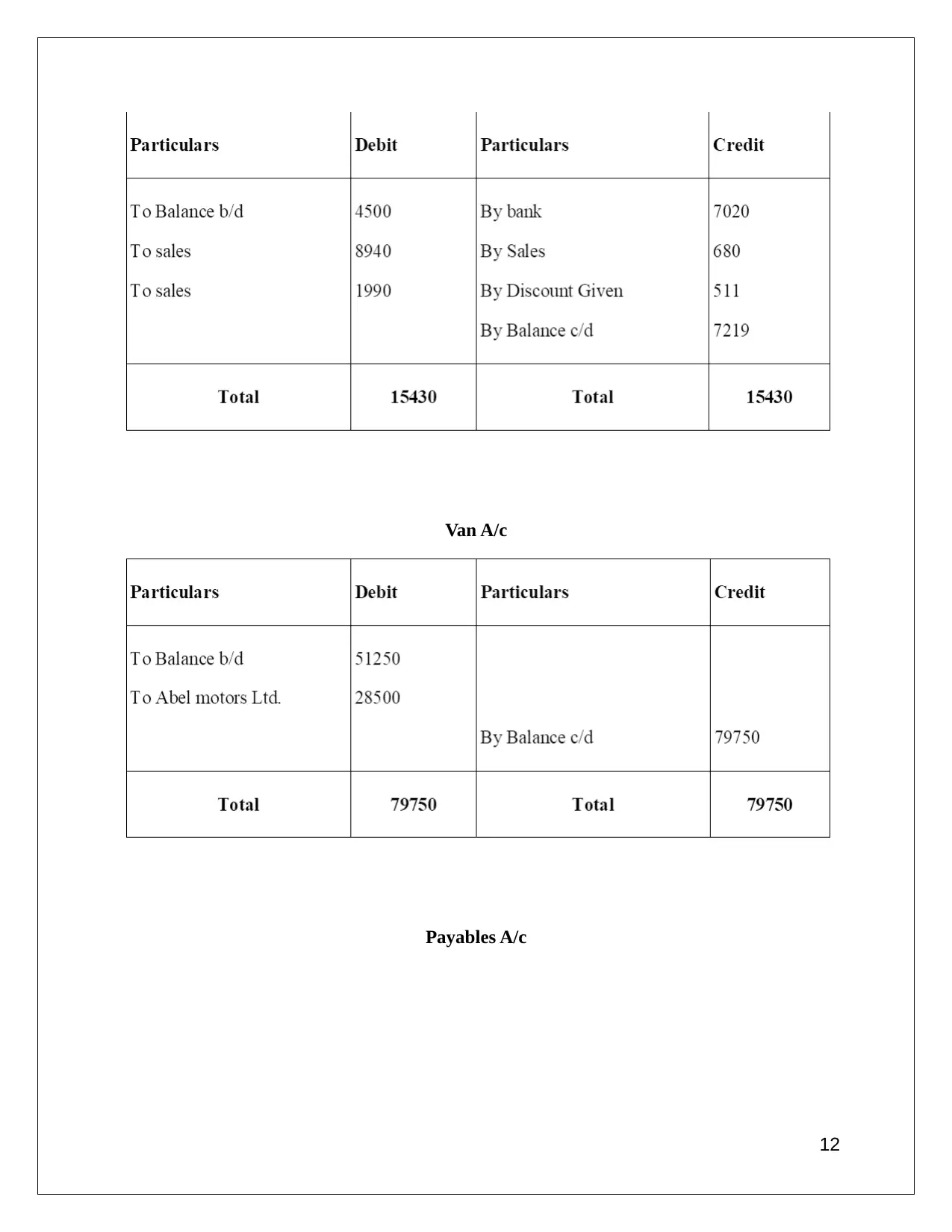

This report provides a detailed analysis of financial accounting principles, including definitions, regulations, and accounting rules such as the double-entry system and various accounting principles and conventions like consistency, materiality, and disclosure. It features a portfolio of six clients, showcasing practical applications of these principles through journal entries, ledger accounts, profit and loss statements, and balance sheets. The report also covers specific accounting concepts like prudence, consistency, and depreciation methods, along with bank reconciliation statements, control accounts, and the use of suspense accounts for managing temporary or doubtful transactions. This comprehensive overview aims to provide a clear understanding of financial accounting practices and their real-world implementation.

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.