Financial Accounting Principles Report - Analysis and Review

VerifiedAdded on 2021/02/19

|22

|2706

|367

Report

AI Summary

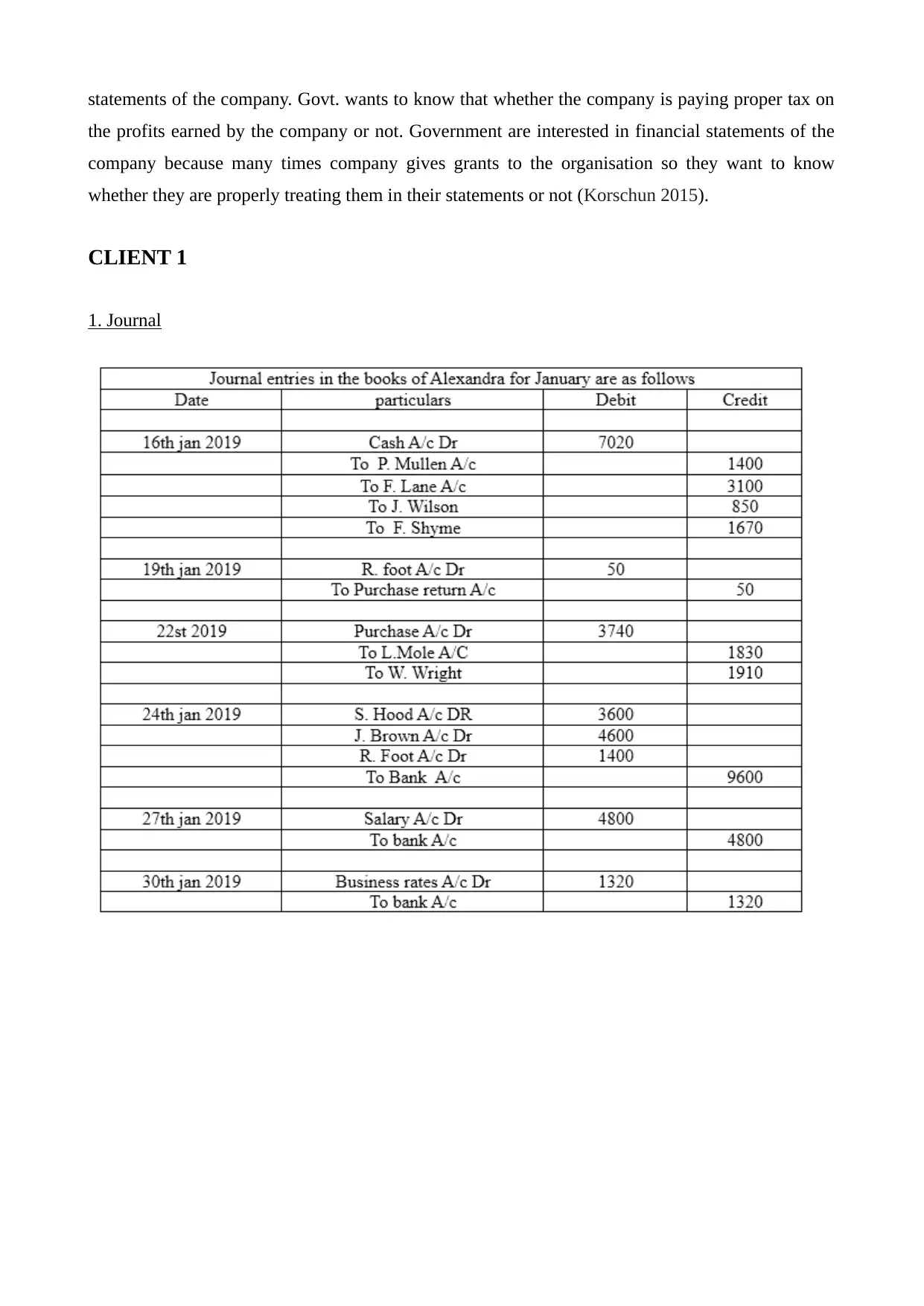

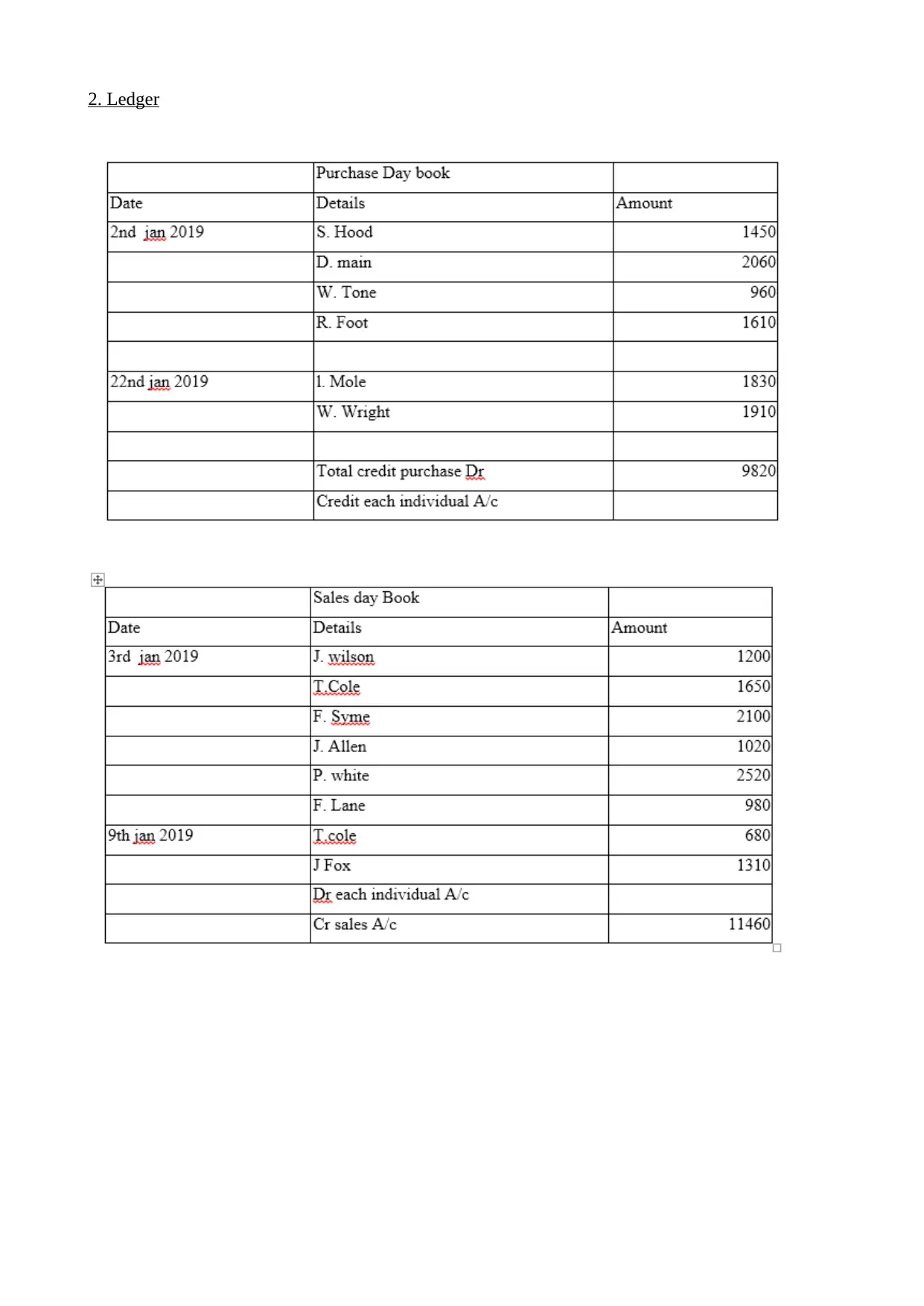

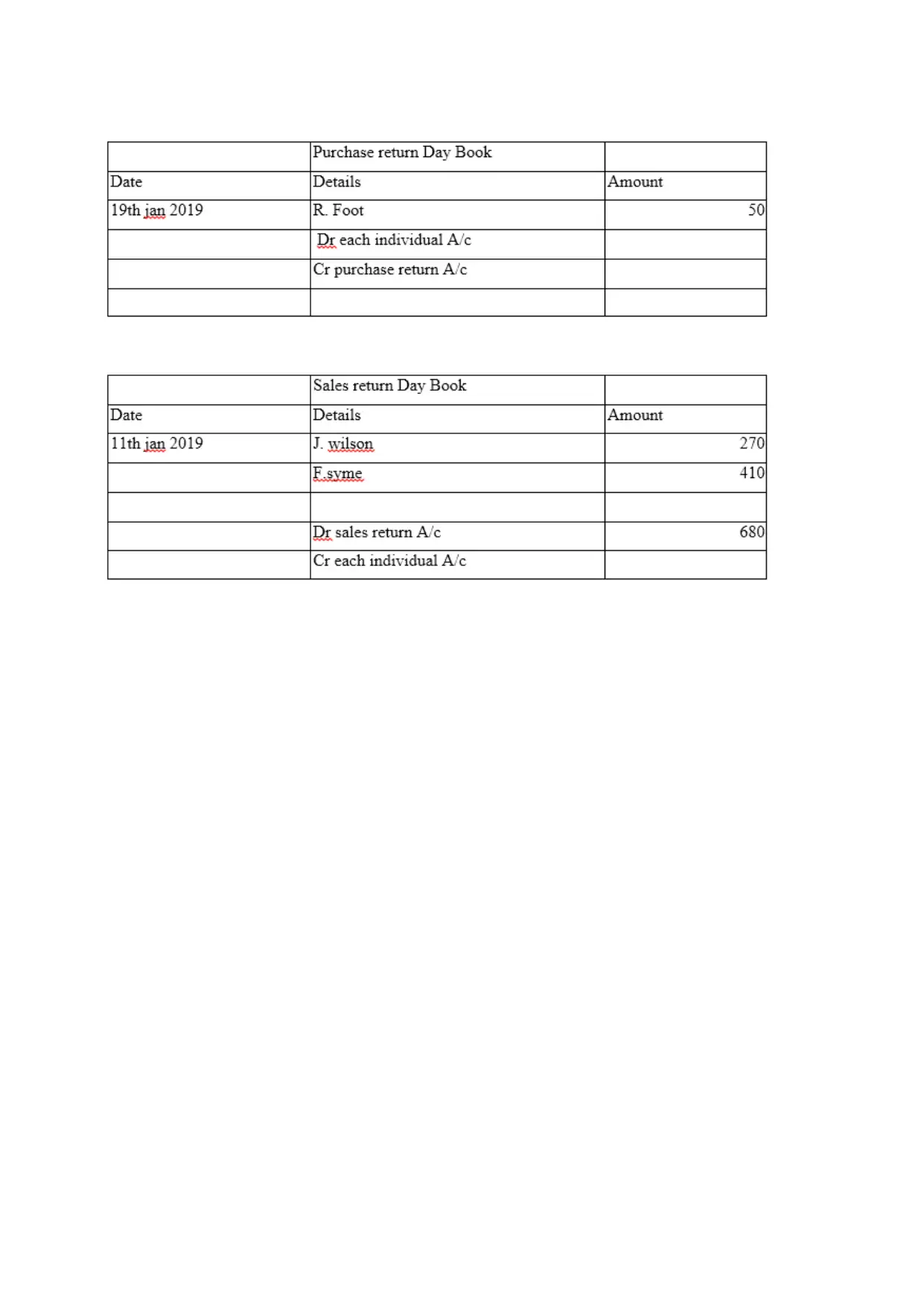

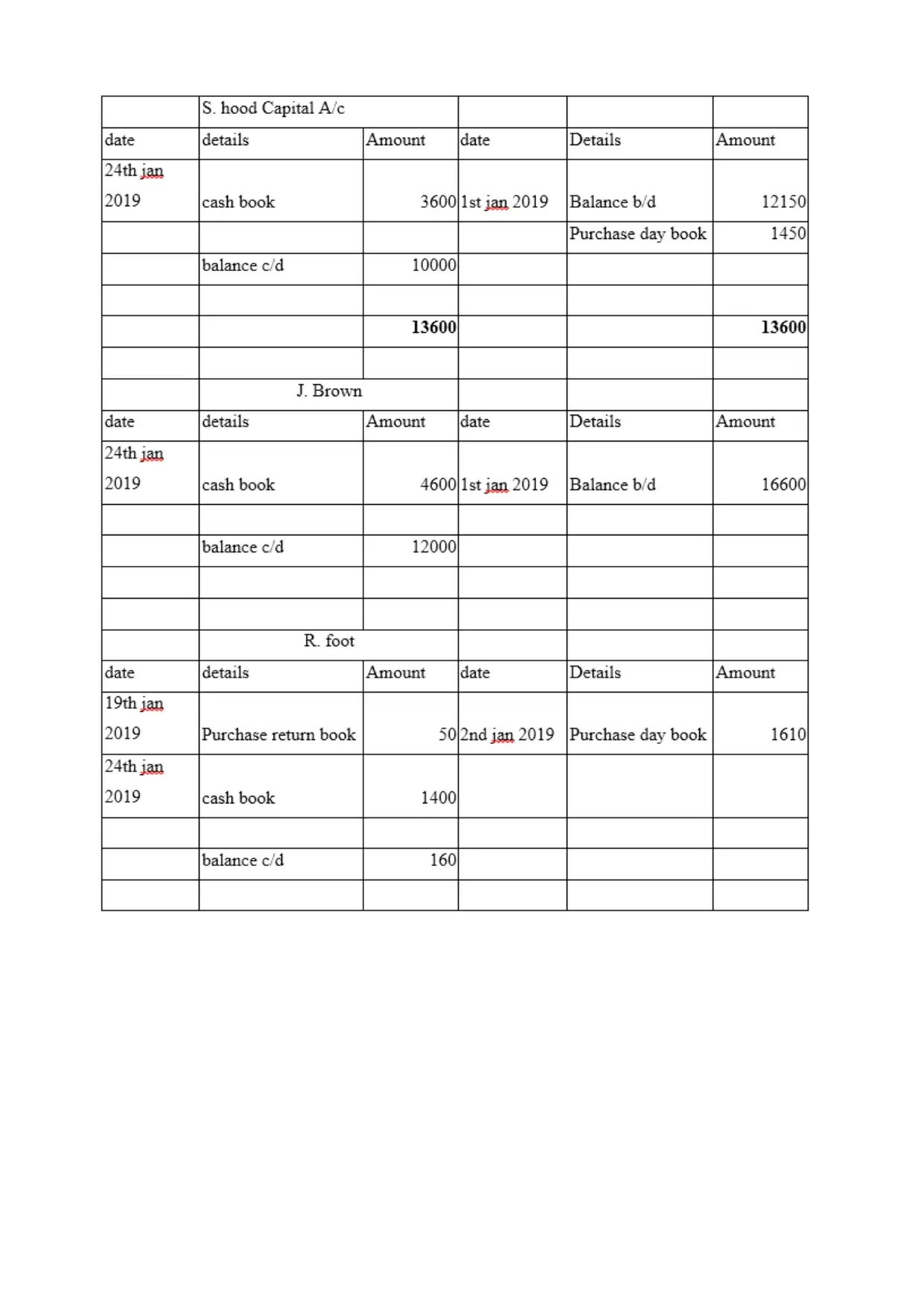

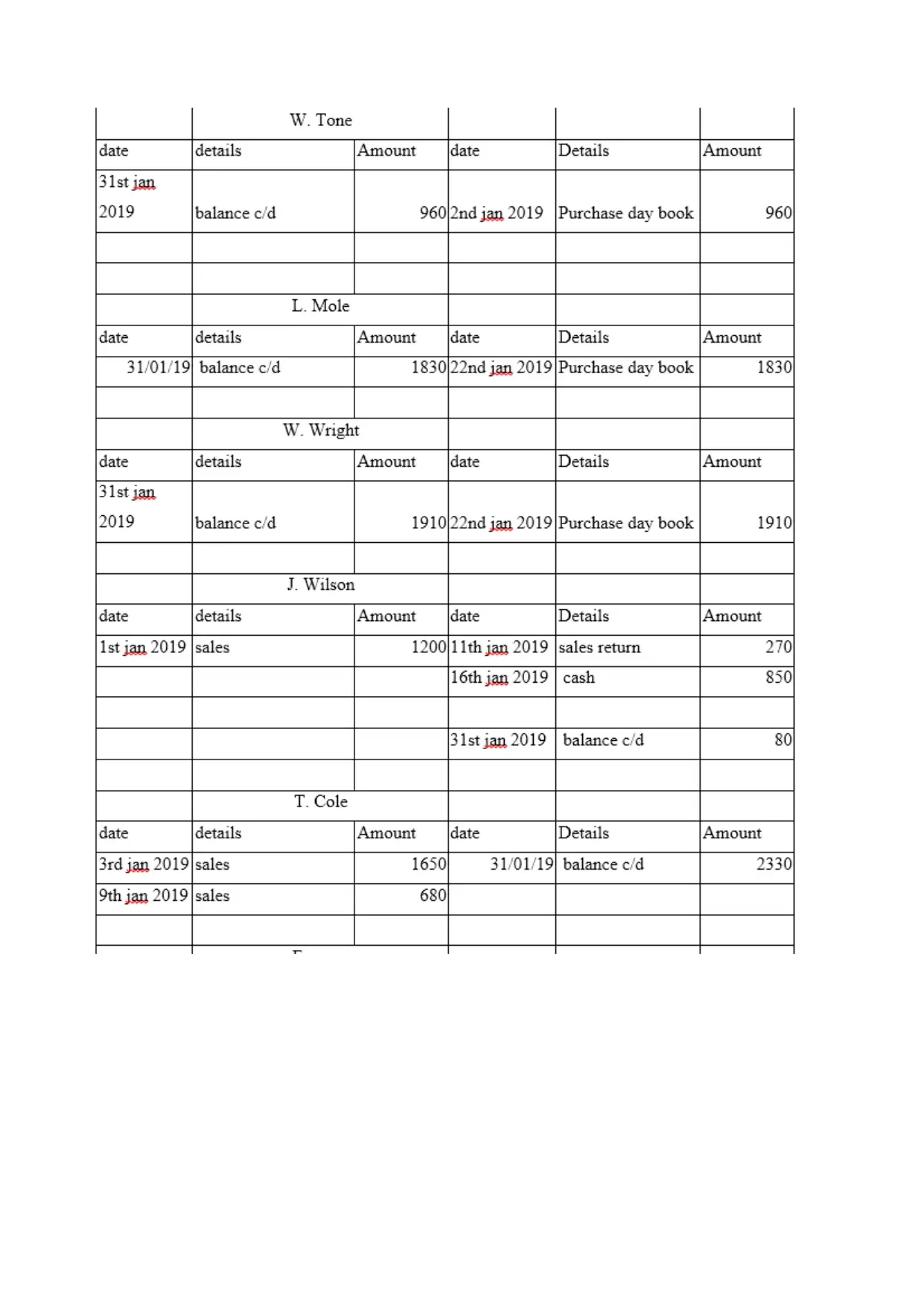

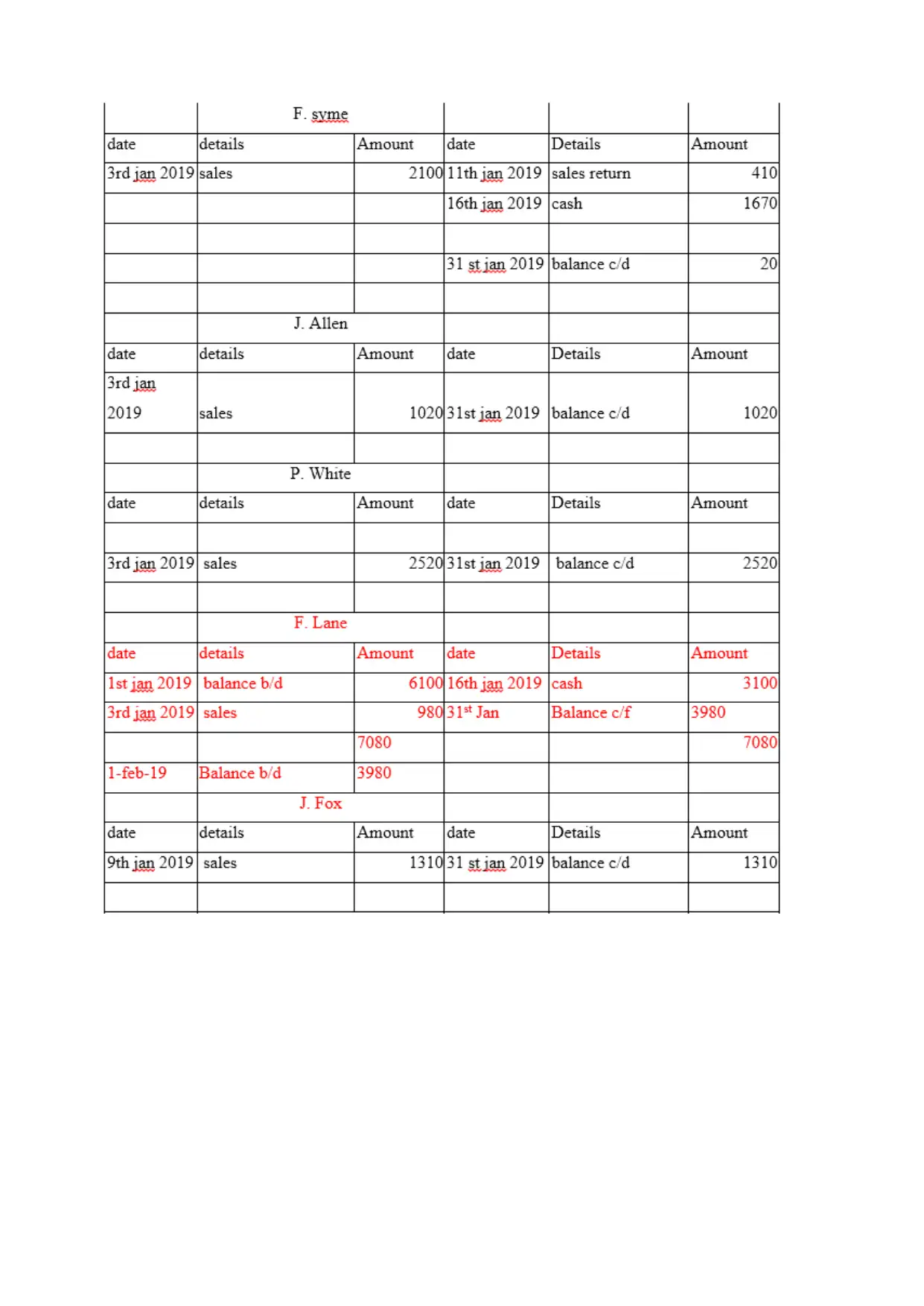

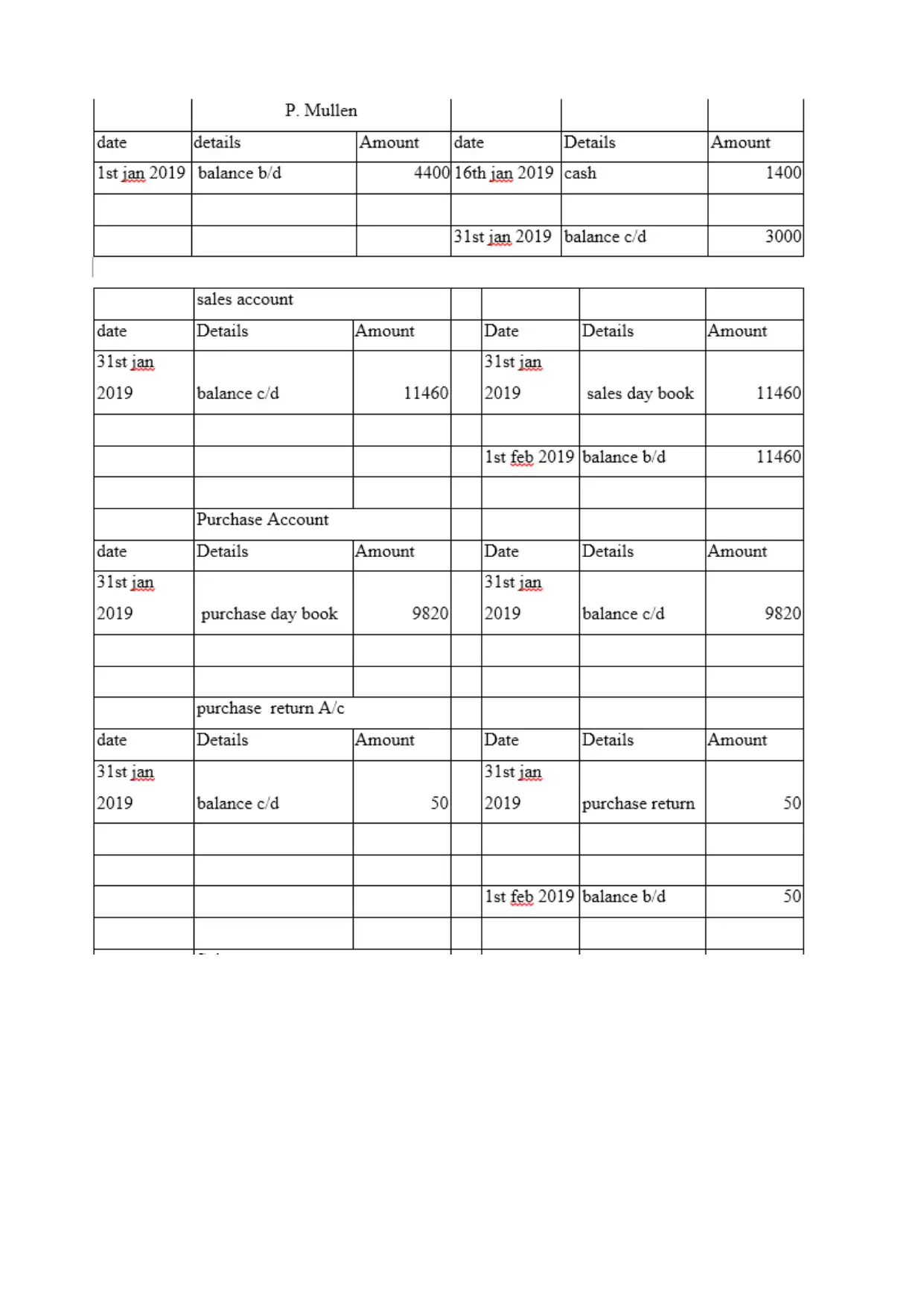

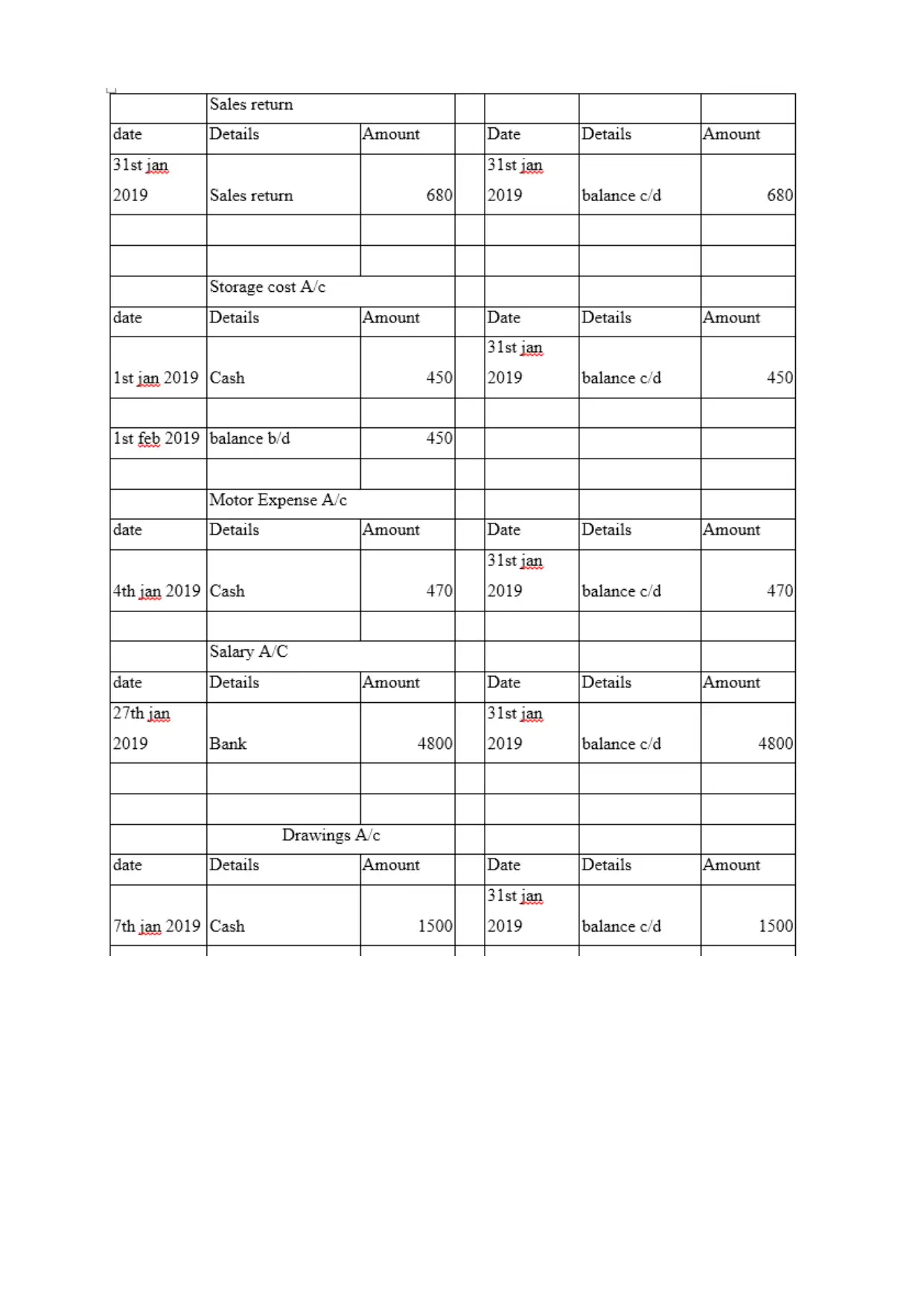

This report delves into the core principles of financial accounting, encompassing the processes, concepts, and theories essential for preparing accurate financial statements. It begins by defining the meaning and purpose of financial statements, emphasizing their crucial role in providing a clear picture of a business's financial health. The report then explores the significance of various stakeholders, both internal (owners, management) and external (creditors, customers, shareholders, government authorities), and their respective interests in financial information. It further examines key accounting concepts such as depreciation methods (straight-line and written-down value), the purpose of bank reconciliation statements, and the importance of control and suspense accounts. The report provides insights through different client examples, illustrating practical applications of these principles and their impact on business operations and decision-making.

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.